11email: bryan.liu (at) asos.com 22institutetext: Department of Computing, Imperial College London, London, UK

Generalising Random Forest Parameter Optimisation to Include Stability and Cost

Abstract

Random forests are among the most popular classification and regression methods used in industrial applications. To be effective, the parameters of random forests must be carefully tuned. This is usually done by choosing values that minimize the prediction error on a held out dataset. We argue that error reduction is only one of several metrics that must be considered when optimizing random forest parameters for commercial applications. We propose a novel metric that captures the stability of random forest predictions, which we argue is key for scenarios that require successive predictions. We motivate the need for multi-criteria optimization by showing that in practical applications, simply choosing the parameters that lead to the lowest error can introduce unnecessary costs and produce predictions that are not stable across independent runs. To optimize this multi-criteria trade-off, we present a new framework that efficiently finds a principled balance between these three considerations using Bayesian optimisation. The pitfalls of optimising forest parameters purely for error reduction are demonstrated using two publicly available real world datasets. We show that our framework leads to parameter settings that are markedly different from the values discovered by error reduction metrics alone.

Keywords:

Bayesian optimisation; parameter tuning; random forest; machine learning application; model stability1 Introduction

Random forests are ensembles of decision trees that can be used to solve classification and regression problems. They are very popular for practical applications because they can be trained in parallel, easily consume heterogeneous data types and achieve state of the art predictive performance for many tasks [6, 14, 15].

Forests have a large number of parameters (see [4]) and to be effective their values must be carefully selected [8]. This is normally done by running an optimisation procedure that selects parameters that minimize a measure of prediction error. A large number of error metrics are used depending on the problem specifics. These include prediction accuracy and area under the receiver operating characteristic curve (AUC) for classification, and mean absolute error (MAE) and root mean squared error (RMSE) for regression problems. Parameters of random forests (and other machine learning methods) are optimized exclusively to minimize error metrics. We make the case to consider monetary cost in practical scenarios and introduce a novel metric which measures the stability of the model.

Unlike many other machine learning methods (SVMs, linear regression, decision trees), predictions made by random forests are not deterministic. While a deterministic training method has no variability when trained on the same training set, it exhibits randomness from sampling the training set. We call the variability in predictions due solely to the training procedure (including training data sampling) the endogenous variability. It has been known for many years that instability plays an important role in evaluating the performance of machine learning models. The notion of instability for bagging models (like random forests) was originally developed by Breiman [2, 1], and extended explicitly by Elisseeff et. al. [5] to randomised learning algorithms, albeit focusing on generalisation/leave-one-out error (as is common in computational learning theory) rather than the instability of the predictions themselves.

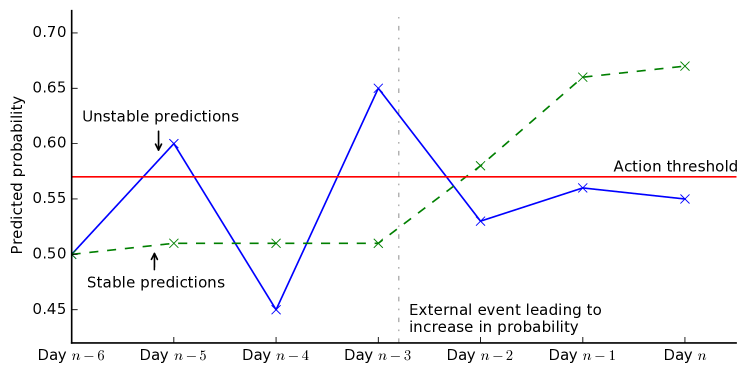

It is often the case that changes in successive prediction values are more important than the absolute values. Examples include predicting disease risk [9] and changes in customer lifetime value [3]. In these cases we wish to measure a change in the external environment. We call the variability in predictions due solely to changes in the external environment exogenous variability. Figure 1 illustrates prediction changes with and without endogenous changes on top of exogenous change. Ideally we would like to measure only exogenous change, which is challenging if the endogenous effects are on a similar or larger scale.

Besides stability and error our framework also accounts for the cost of running the model. The emergence of computing as a service (Amazon elastic cloud, MS Azure etc.) makes the cost of running machine learning algorithms transparent and, for a given set of resources, proportional to runtime.

It is not possible to find parameter configurations that simultaneously optimise cost, stability and error. For example, increasing the number of trees in a random forest will improve the stability of predictions, reduce the error, but increase the cost (due to longer runtimes). We propose a principled approach to this problem using a multi-criteria objective function.

We use Bayesian optimisation to search the parameter space of the multi-criteria objective function. Bayesian optimisation was originally developed by Kushner [10] and improved by Mockus [12]. It is a non-linear optimisation framework that has recently become popular in machine learning as it can find optimal parameter settings faster than competing methods such as random / grid search or gradient descent [13]. The key idea is to perform a search over possible parameters that balances exploration (trying new regions of parameter space we know little about) with exploitation (choosing parts of the parameter space that are likely to lead to good objectives). This is achieved by placing a prior distribution on the mapping from parameters to the loss. An acquisition function then queries successive parameter settings by balancing high variance regions of the prior (good for exploration) with low mean regions (good for exploitation). The optimal parameter setting is then obtained as the setting with the lowest posterior mean after a predefined number of query iterations.

We demonstrate the success of our approach on two large, public commercial datasets. Our work makes the following contributions:

-

1.

A novel metric for the stability of the predictions of a model over different runs and its relationship with the variance and covariance of the predictions.

-

2.

A framework to optimise model hyperparameters and training parameters against the joint effect of prediction error, prediction stability and training cost, utilising constrained optimisation and Bayesian optimisation.

-

3.

A case study on the effects of changing hyperparameters of a random forest and training parameters on the model error, prediction stability and training cost, as applied on two publicly available datasets.

The rest of the paper is organized as follows: in section 2 we propose a novel metric to assess the stability of random forest predictions, in section 3 we propose a random forest parameter tuning framework using a set of metrics, in section 4 we discuss the effects of the hyper-parameters on the metrics and illustrate the usefulness of the proposed optimization framework to explore the trade-offs in the parameter space in section 5.

2 Prediction Stability

Here we formalise the notion of random forest stability in terms of repeated model runs using the same parameter settings and dataset (ie. all variability is endogenous). The expected squared difference between the predictions over two runs is given by

| (1) |

where is the probability from the run that the data point is of the positive class in binary classification problems (note this can be extended to multiclass classification and regression problems). We average over runs to give the Mean Squared Prediction Delta (MSPD):

| (2) | ||||

| (3) |

where is the expectation over all validation data, is a mapping from a sample to a label on a given run, is the variance of the predictions of a single data point over model runs, and is the covariance of predictions of a single data point over two model runs.111A full derivation is available at our GitHub repository https://github.com/liuchbryan/generalised_forest_tuning.

The covariance, the variance and hence the model instability are closely related to the forest parameter settings, which we discuss in section 4. It is convenient to measure stability on the same scale as the forest predictions and so in the experiments we report the .

3 Parameter Optimisation Framework

In industrial applications, where ultimately machine learning is a tool for profit maximisation, optimising parameter settings based solely on error metrics is inadequate. Here we develop a generalised loss function that incorporates our stability metric in addition to prediction error and running costs. We use this loss with Bayesian optimisation to select parameter values.

3.1 Metrics

Before composing the loss function we define the three components:

Stability

We incorporate stability (defined in section 2) in to the optimization framework with the use of the RMSPD.

Error reduction

Many different error metrics are used with random forests. These include F1-score, accuracy, precision, recall and Area Under the receiver operating characteristics Curve (AUC) and all such metrics fit within our framework. In the remainder of the paper we use the AUC because for binary classification, most other metrics require the specification of a threshold probability. As random forests are not inherently calibrated, a threshold of 0.5 may not be appropriate and so using AUC simplifies the exposition [3].

Cost reduction

It is increasingly common for machine learning models to be run on the cloud with computing resources paid for by the hour (e.g. Amazon Web Services). Due to the exponential growth in data availability, the cost to run a model can be comparable with the financial benefit it produces. We use the training time (in seconds) as a proxy of the training cost.

3.2 Loss-function

We choose a loss function that is linear in cost, stability and AUC that allows the relative importance of these three considerations to be balanced:

| (4) |

where is the number of trees in the trained random forest, is the maximum depth of the trees, and is the proportion of data points used in training; are weight parameters. We restrict our analysis to three parameters of the random forest, but it can be easily extended to include additional parameters (e.g. number of features bootstrapped in each tree).

The weight parameters and are specified according to business/research needs. We recognise the diverse needs across different organisations and thus refrain from specifying what constitutes a “good” weight parameter set. Nonetheless, a way to obtain the weight parameters is to quantify the gain in AUC, the loss in RMSPD, and the time saved all in monetary units. For example, if calculations reveal 1% gain in AUC equates to £50 potential business profit, 1% loss in RMSPD equates to £10 reduction in lost business revenue, and a second of computation costs £0.01, then and can be set as 5,000, 1,000 and 0.01 respectively.

3.3 Bayesian Optimisation

The loss function is minimized using Bayesian optimisation. The use of Bayesian optimisation is motivated by the expensive, black-box nature of the objective function: each evaluation involves training multiple random forests, a complex process with internal workings that are usually masked from users. This rules out gradient ascent methods due to unavailability of derivatives. Exhaustive search strategies, such as grid search or random search, have prohibitive runtimes due to the large random forest parameter space.

4 Parameter Sensitivity

Here we describe three important random forest parameters and evaluate the sensitivity of our loss function to them.

4.1 Sampling training data

Sampling of training data – drawing a random sample from the pool of available training data for model training – is commonly employed to keep the training cost low. A reduction in the size of training data leads to shorter training times and thus reduces costs. However, reducing the amount of training data reduces the generalisability of the model as the estimator sees less training examples, leading to a reduction in AUC. Decreasing the training sample size also decreases the stability of the prediction. This can be understood by considering the form of the stability measure of , the RMSPD (equation 2). The second term in this equation is the expected covariance of the predictions over multiple training runs. Increasing the size of the random sample drawn as training data increases the probability that the same input datum will be selected for multiple training runs and thus the covariance of the predictions increases. An increase in covariance leads to a reduction in the RMSPD (see equation 3).

4.2 Number of trees in a random forest

Increasing the number of trees in a random forest will decrease the RMSPD (and hence improve stability) due to the Central Limit Theorem (CLT). Consider a tree in a random forest with training data bootstrapped. Its prediction can be seen as a random sample from a distribution with finite mean and variance .222This could be any distribution as long as its first two moments are finite, which is usually the case in practice as predictions are normally bounded. By averaging the trees’ predictions, the random forest is computing the sample mean of the distribution. By the CLT, the sample mean will converge to a Gaussian distribution with variance , where is the number of trees in the random forest.

To link the variance to the MSPD, recall from equation 2 that MSPD captures the interaction between the variance of the model and covariance of predictions between different runs:

The covariance is bounded below by the negative square root of the variance of its two elements, which is in turn bounded below by the negative square root of the larger variance squared:

| (5) |

Given and have the same variance as (being the models with the same training proportion across different runs), the inequality 5 can be simplified as:

| (6) |

MSPD is then bounded above by a multiple of the expected variance of :

| (7) |

which decreases as increases, leading to a lower RMSPD estimate.

While increasing the number of trees in a random forest reduces error and improves stability in predictions, it increases the training time and hence monetary cost. In general, the runtime complexity for training a random forest grows linearly with the number of trees in the forest.

4.3 Maximum depth of a tree

The maximum tree depth controls the complexity of each decision tree and the computational cost (running time) increases exponentially with tree depth. The optimal depth for error reduction depends on the other forest paramaters and the data. Too much depth causes overfitting. Additionally, as the depth increases the prediction stability will decrease as each model tends towards memorizing the training data. The highest stability will be attained using shallow trees, however if the forest is too shallow the model will underfit resulting in low AUC.

5 Experiments

We evaluate our methodology by performing experiments on two public datasets: (1) the Orange small dataset from the 2009 KDD Cup and (2) the Criteo display advertising challenge Kaggle competition from 2014. Both datasets have a mixture of numerical and categorical features and binary target labels (Orange: 190 numerical, 40 categorical, Criteo: 12 numerical, 25 categorical).

We report the results of two sets of experiments: (1) Evaluating the effect of changing random forest parameters on the stability and loss functions (2) Bayesian optimisation with different weight parameters.

We train random forests to predict the upselling label for the Orange dataset and the click-through rate for the Criteo dataset. Basic pre-processing steps were performed on both datasets to standardise the numerical data and transform categoricals into binary indicator variables. We split the datasets into two halves: the first as training data (which may be further sampled at each training run), and the later as validation data. All data and code required to replicate our experiments is available from our GitHub repository.333https://github.com/liuchbryan/generalised_forest_tuning

5.1 Parameter Sensitivity

In the first set of experiments we evaluate the effect of varying random forest parameters on the components of our loss function.

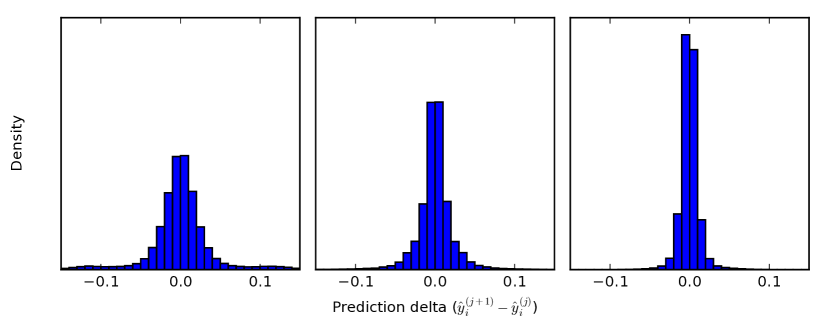

Figure 2 visualises the change in the RMSPD with relation to the number of trees in the random forest. The plots show distributions of prediction deltas for the Orange dataset. Increasing the number of trees (going from the left to the right plot) leads to a more concentrated prediction delta distribution, a quality also reflected by a reduction in the RMSPD.

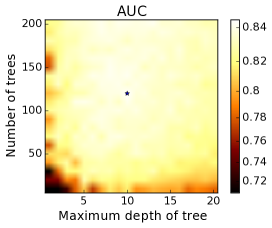

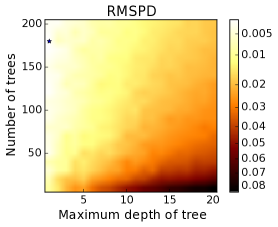

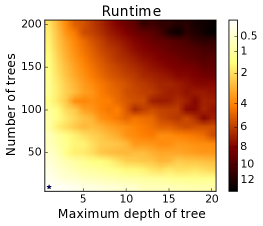

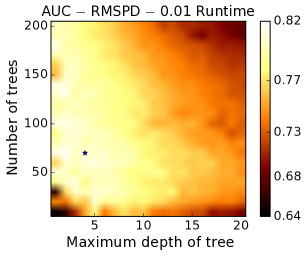

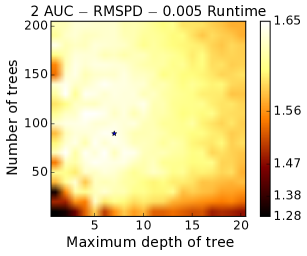

Figure 3 shows the AUC, runtime, RMSPD and loss functions averaged over multiple runs of the forest for different settings of number of trees and maximum tree depth. It shows that the AUC plateaus for a wide range of combinations of number of trees and maximum depth. The RMSPD is optimal for large numbers of shallow trees while runtime is optimised by few shallow trees. When we form a linear combination of the three metrics, the optimal solutions are markedly different from those discovered by optimising any single metric in isolation. We show this for and .

5.2 Bayesian optimization of the trilemma

We also report the results of using the framework to choose the parameters. The aim of these experiments is to show that (1) Bayesian optimisation provides a set of parameters that achieve good AUC, RMSPD and runtime, and (2) by varying the weight parameters in the Bayesian optimisation a user is able to prioritise one or two of the three respective items.

Table 1 summarises the trilemma we are facing – all three parameter tuning strategies improves two of the three practical considerations with the expense of the consideration(s) left.

| Hyperparameter tuning strategy | AUC gain | RMSPD reduction | Cost savings |

|---|---|---|---|

| Increase training proportion | + | + | – |

| Increase number of trees | + | + | – – |

| Reduce maximum depth of trees | – | + | ++ |

The results of our experiments on Bayesian optimisation of the trilemma are shown in tables 2 and 3. The first row in both tables shows the results for a vanilla random forest with no optimisation of the hyper-parameters discussed in the previous section: 10 trees, no limit on the maximum depth of the tree, and using the entire training data set (no sampling). The Bayesian optimisation for each set of weight parameters was run for 20 iterations, with the RMSPD calculated over three training runs in each iteration.

The first observation from both sets of results is that Bayesian optimisation is suitable for providing a user with a framework that can simultaneously improve AUC, RMSPD and runtime as compared to the baseline. Secondly, it is clear that by varying the weight parameters, Bayesian optimisation is also capable of prioritising specifically AUC, RMSPD or runtime. Take for example the third and fourth rows of table 2; setting we see a significant reduction in the RMSPD in comparison to the second row where . Similarly, comparing the fourth row to the second row, increasing from 1 to 5 gives a 1% increase in AUC. In the final row we see that optimising for a short runtime keeps the RMSPD low in comparison to the non-optimal results on the first row and sacrifices the AUC instead.

| AUC | RMSPD | Runtime | ||||||||||||||

| No optimisation: | 0.760 | 0.112 | 1.572 | |||||||||||||

| 1 | 1 | 0.01 | 166 | 6 | 0.100 | 0.829 | 0.011 | 1.142 | ||||||||

| 1 | 5 | 0.01 | 174 | 1 | 0.538 | 0.829 | 0.002 | 1.452 | ||||||||

| 5 | 1 | 0.01 | 144 | 12 | 0.583 | 0.839 | 0.013 | 5.292 | ||||||||

| 1 | 1 | 0.05 | 158 | 4 | 0.100 | 0.8315 | 0.0082 | 1.029 | ||||||||

For the Criteo dataset (table 3) we see on the second and third row that again increasing the parameter leads to a large reduction in the RMSPD. For this dataset the Bayesian optimiser is more reluctant to use a larger number of estimators to increase AUC because the Criteo dataset is significantly larger (around 100 times) than the Orange dataset and so using more trees increases the runtime more severely. To force the optimiser to use more estimators we reduce the priority of the runtime by a factor of ten as can be seen in the final two rows. We see in the final row that doubling the importance of the AUC () leads to a significant increase in AUC () when compared to the non-optimal results.

| AUC | RMSPD | Runtime | ||||||||||||||

| No optimisation: | 0.685 | 0.1814 | 56.196 | |||||||||||||

| 1 | 1 | 0.01 | 6 | 8 | 0.1 | 0.7076 | 0.04673 | 1.897 | ||||||||

| 1 | 5 | 0.01 | 63 | 3 | 0.1 | 0.6936 | 0.01081 | 4.495 | ||||||||

| 1 | 1 | 0.05 | 5 | 5 | 0.1 | 0.688 | 0.045 | 1.136 | ||||||||

| 2 | 1 | 0.05 | 9 | 9 | 0.1 | 0.7145 | 0.03843 | 2.551 | ||||||||

| 1 | 1 | 0.001 | 120 | 2 | 0.1 | 0.6897 | 0.007481 | 7.153 | ||||||||

| 2 | 1 | 0.001 | 66 | 15 | 0.1 | 0.7300 | 0.02059 | 11.633 | ||||||||

6 Conclusion

We proposed a novel metric to capture the stability of random forest predictions, which is key for applications where random forest models are continuously updated. We show how this metric, calculated on a sample, is related to the variance and covariance of the predictions over different runs. While we focused on random forests in this text, the proposed stability metric is generic and can be applied to other non-deterministic models (e.g. gradient boosted trees, deep neural networks) as well as deterministic training methods when training is done with a subset of the available data.

We also propose a framework for multi-criteria optimisation, using the proposed metric in addition to metrics measuring error and cost. We validate this approach using two public datasets and show how optimising a model solely for error can lead to poorly specified parameters.

References

- [1] Breiman, L.: Bagging Predictors. Machine Learning 24(421), 123–140 (1996)

- [2] Breiman, L.: Heuristics of Instability in Model Selection. The Annals of Statistics 24(6), 2350–2383 (1996)

- [3] Chamberlain, B.P., Cardoso, A., Liu, C.H.B., Pagliari, R., Deisenroth, M.P.: Customer Lifetime Value Prediction Using Embeddings. In: Proceedings of the 23rd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining. (2017)

- [4] Criminisi, A.: Decision Forests: A Unified Framework for Classification, Regression, Density Estimation, Manifold Learning and Semi-Supervised Learning. Foundations and Trends® in Computer Graphics and Vision 7(2-3), 81–227 (2011)

- [5] Elisseeff, A., Evgeniou, T., Pontil, M.: Stability of Randomized Learning Algorithms. Journal of Machine Learning Research 6(1), 55–79 (2005)

- [6] Fernández-Delgado, M., Cernadas, E., Barro, S., Amorim, D., Amorim Fernández-Delgado, D.: Do We Need Hundreds of Classifiers to Solve Real World Classification Problems? Journal of Machine Learning Research 15, 3133–3181 (2014)

- [7] Hoffman, M.W., Shahriari, R.: Modular Mechanisms for Bayesian Optimization. NIPS Workshop on Bayesian Optimization pp. 1–5 (2014)

- [8] Huang, B.F.F., Boutros, P.C.: The Parameter Sensitivity of Random Forests. BMC Bioinformatics 17(1), 331 (2016)

- [9] Khalilia, M., Chakraborty, S., Popescu, M.: Predicting Disease Risks From Highly Imbalanced Data Using Random Forest. BMC Medical Informatics and Decision Making 11(1), 51 (2011)

- [10] Kushner, H.J.: A New Method of Locating the Maximum Point of an Arbitrary Multipeak Curve in the Presence of Noise. Journal of Basic Engineering 86(1), 97 (1964)

- [11] Martinez-Cantin, R.: BayesOpt: A Bayesian Optimization Library for Nonlinear Optimization, Experimental Design and Bandits. Journal of Machine Learning Research 15, 3735–3739 (2014)

- [12] Mockus, J.: On Bayesian Methods for Seeking the Extremum. IFIP Technical Conference on Optimization Techniques pp. 400–404 (1974)

- [13] Snoek, J., Larochelle, H., Adams, R.: Practical Bayesian Optimization of Machine Learning Algorithms. In: Advances in Neural Information Processing Systems. pp. 2951–2959 (2012)

- [14] Tamaddoni, A., Stakhovych, S., Ewing, M.: Comparing Churn Prediction Techniques and Assessing Their Performance: A Contingent Perspective. Journal of Service Research 19(2), 123–141 (2016)

- [15] Vanderveld, A., Pandey, A., Han, A., Parekh, R.: An Engagement-Based Customer Lifetime Value System for E-commerce. In: Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining. pp. 293–302 (2016)