Stochastic Proximal Gradient Algorithms

for Penalized Mixed Models

Abstract

Motivated by penalized likelihood maximization in complex models, we study optimization problems where neither the function to optimize nor its gradient have an explicit expression, but its gradient can be approximated by a Monte Carlo technique. We propose a new algorithm based on a stochastic approximation of the Proximal-Gradient (PG) algorithm. This new algorithm, named Stochastic Approximation PG (SAPG) is the combination of a stochastic gradient descent step which - roughly speaking - computes a smoothed approximation of the gradient along the iterations, and a proximal step. The choice of the step size and of the Monte Carlo batch size for the stochastic gradient descent step in SAPG are discussed. Our convergence results cover the cases of biased and unbiased Monte Carlo approximations. While the convergence analysis of some classical Monte Carlo approximation of the gradient is already addressed in the literature (see Atchadé et al., 2017), the convergence analysis of SAPG is new. Practical implementation is discussed and guidelines to tune the algorithm are given. The two algorithms are compared on a linear mixed effect model as a toy example. A more challenging application is proposed on non-linear mixed effect models in high dimension with a pharmacokinetic data set including genomic covariates. To our best knowledge, our work provides the first convergence result of a numerical method designed to solve penalized Maximum Likelihood in a non-linear mixed effect model.

Keywords: Proximal-Gradient algorithm; Stochastic Gradient; Stochastic EM algorithm; Stochastic Approximation; Non-linear mixed effect models.

1 Introduction

Many problems in computational statistics reduce to the maximization of a criterion

| (1) |

and the functions satisfy

H 1.

the function is convex, not identically , and lower semi-continuous.

H 2.

the function is continuously differentiable on and its gradient is of the form

| (2) |

denotes the gradient operator and is a probability distribution on a measurable subset of . The measurable functions and are known but the expectation of the function with respect to may be intractable. Furthermore, there exists a finite non-negative constant such that for all ,

| (3) |

is the Euclidean norm.

Examples of functions satisfying Eq. (2) are given below. We are interested in numerical methods for solving Eq. (1), robust to the case when neither nor its gradient have an explicit expression.

Such an optimization problem occurs for example when computing a penalized maximum likelihood estimator in some parametric model indexed by : denotes the log-likelihood of the observations (the dependence upon is omitted) and is the penalty term.

The optimization problem Eq. (1) covers the computation of the maximum when the parameter is restricted to a closed convex subset of ; in that case, is the characteristic function of i.e. for any and otherwise. It also covers the case when is the ridge, the lasso or the elastic net penalty; and more generally, the case when is the sum of lower semi-continuous non-negative convex functions.

A first example of such a function is given by the log-likelihood in a latent variable model with complete likelihood from the -parameter exponential family (see e.g. Bickel and Doksum (2015) and Bartholomew et al. (2011) and the references therein). In that case, is of the form

| (4) |

where denotes the scalar of two vectors , , and are measurable functions, and is a -finite positive measure on . The quantity is known as the complete log-likelihood, and is the latent data vector. Under regularity conditions, we have

| (5) |

where denotes the transpose of the jacobian matrix of the function at .

A second example is given by the log-likelihood of independent observations from a log-linear model for Markov random fields. In this model, is given by

| (6) |

The function is known as the partition function. Under regularity conditions, we have

| (7) |

In these two examples, the integrals in Eqs. (4) to (7) are intractable except for toy examples: neither the function nor its gradient are available. Nevertheless, all the integrals in Eqs. (4)-(7) can be approximated by a Monte Carlo sum (see e.g. Robert and Casella, 2004). In the first example, this Monte Carlo approximation consists in imputing the missing variables ; it is known that such an imputation is far more efficient when the Monte Carlo samples are drawn under , i.e. the a posteriori distribution of the missing variables given the observations (see Eq. (5)) than when they are drawn under the a priori distribution. This remark is the essence of the Expectation Maximization (EM) algorithm (introduced in Dempster et al., 1977), a popular iterative procedure for maximizing the log-likelihood in latent variable models.

In this paper, we are interested in first order optimization methods to solve Eq. (1), that is methods based on the gradient. In Section 2.1, we describe two stochastic first-order descent methods, which are stochastic perturbations of the Proximal-Gradient (PG) algorithm (introduced in Combettes and Pesquet (2011); see also Beck and Teboulle (2009); Parikh and Boyd (2013) for literature reviews on Proximal-Gradient algorithms). The two algorithms are the Monte Carlo Proximal-Gradient algorithm (MCPG) and the Stochastic Approximation Proximal-Gradient algorithm (SAPG), which differ in the approximation of the gradient and more precisely, of the intractable integral (see Eq. (2)). In MCPG, at each iteration of the algorithm, this expectation evaluated at the current point is approximated by a Monte Carlo sum computed from samples approximating . In SAPG, the approximation is computed as a Monte Carlo sum based on all the points drawn during all the previous iterations of the algorithm .

When is the log-likelihood of a latent variable model, we prove in Section 2.2 that our algorithms are Generalized EM algorithms (see e.g. McLachlan and Krishnan, 2008; Ng et al., 2012) combined with a stochastic E-step: in MCPG and SAPG, the stochastic E-step mimics respectively the E-step of the Monte Carlo EM (Wei and Tanner, 1990; Levine and Fan, 2004) and the E-step of the Stochastic Approximation EM (see e.g. Delyon et al., 1999).

Section 3 is devoted to the convergence analysis of MCPG and SAPG. These algorithms can be seen as perturbed Proximal-Gradient algorithms when the perturbation comes from replacing the exact quantity by a Monte Carlo approximation at each iteration of the algorithm. Our convergence analysis covers the case when the points are sampled from a Markov chain Monte Carlo sampler (MCMC) with target distribution - and therefore, it also covers the case of i.i.d. draws. This implies that the estimator of may be biased. There exist many contributions in the literature on the convergence of perturbed Proximal-Gradient algorithms when is concave, but except in the works by Atchadé et al. (2017) and Combettes and Pesquet (2015), most of them assume that the error is unbiased and gets small when (see e.g. Rosasco et al., 2014; Combettes and Pesquet, 2016; Rosasco et al., 2016; Lin et al., 2015). In this paper, we provide sufficient conditions for the almost-sure convergence of MCPG and SAPG under the assumption that is concave and with no assumptions on the bias of . The convergence analysis of MCPG is a special case of (Atchadé et al., 2017, Section 4); to our best knowledge, the convergence of SAPG is a new result.

Practical implementation is discussed in Section 4. Some guidelines are given in Section 4.2 to choose the sequences involved in the stochastic approximation procedures. Then, MCPG and SAPG are compared through a toy example in Section 4.3. A more challenging application to penalized inference in a mixed effect model is detailed in Section 5. Mixed models are applied to analyze repeated data in a population of subjects. The independent vectors of observations of the subjects are modeled by

| (8) |

with individual latent variable independent of the measurement error vector and the regression function that depends on the vector of observation times . Mixed models thus enter the class of models given by Eq. (4) with latent variables . When a covariate model is introduced, the number of covariates can be large, but with only a few of them being influential. This is a sparse estimation problem and the selection problem can be treated through the optimization of a penalized version of the log-likelihood Eq. (4). In non-linear mixed models, the optimization problem is not explicit and stochastic penalized versions of EM (Bertrand and Balding, 2013; Ollier et al., 2016; Chen et al., 2017) have been proposed. To our best knowledge, stochastic Proximal-Gradient algorithms have not been proposed for mixed models.

2 Stochastic Proximal-Gradient based algorithms

In this section, we describe first-order based algorithms for solving Eq. (1) under the assumptions H1 and H2, when the expectation in Eq. (2) is intractable.

2.1 The MCPG and SAPG algorithms

Both MCPG and SAPG are iterative algorithms, each update relies on the combination of a gradient step and a proximal operator. The proximal map (Moreau (1962), see also Bauschke and Combettes (2011); Parikh and Boyd (2013)) associated to a convex function is defined for any and by

| (9) |

Note that under H1, for any and , there exists an unique point minimizing the RHS of Eq. (9). This proximal operator may have an explicit expression. When is the characteristic function

for some closed convex set , then is the projection of on . This projection is explicit for example when is an hyper-rectangle. Another example of explicit proximal operator is the case associated to the so-called elastic net penalty i.e. with , and , then for any component ,

The Proximal-Gradient algorithm for solving the optimization problem Eq. (1) produces a sequence as follows: given a -valued sequence ,

| (10) |

This update scheme can be explained as follows: by H2, we have for any ,

This minorizing function is equal to at the point ; the maximization (w.r.t. ) of the RHS yields given by Eq. (10). The Proximal-Gradient algorithm is therefore a Minorize - Majorization (MM) algorithm and the ascent property holds: for all . Sufficient conditions for the convergence of the Proximal-Gradient algorithm Eq. (10) can be derived from the results by Combettes and Wajs (2005); Parikh and Boyd (2013) or from convergence analysis of MM algorithms (see e.g. Zangwill, 1969; Meyer, 1976).

In the case can not be computed, we describe two strategies for a Monte Carlo approximation. At iteration , given the current value of the parameter , points from the path of a Markov chain with target distribution are sampled. A first strategy consists in replacing by a Monte Carlo mean:

| (11) |

A second strategy, inspired by stochastic approximation methods (see e.g. Benveniste et al., 1990; Kushner and Yin, 2003) consists in replacing by a stochastic approximation

| (12) |

where is a deterministic -valued sequence. These two strategies yield respectively the Monte Carlo Proximal-Gradient (MCPG) algorithm (see Algorithm 1) and the Stochastic Approximation Proximal- Gradient (SAPG) algorithm (see Algorithm 2).

In Section 3, we prove the convergence of MCPG to the maximum points of when is concave, for different choices of the sequences including decreasing or constant step sizes and respectively, constant or increasing batch size . We also establish the convergence of SAPG to the maximum points (in the concave case); only the case of a constant batch size and a decreasing step size is studied, since this framework corresponds to the Stochastic Approximation one from which the update rule Eq. (12) is inherited (see details in Delyon et al., 1999). From a numerical point of view, the choice of the sequences , and is discussed in Section 4: guidelines are given in Section 4.2 and the behavior of the algorithm is illustrated through a toy example in Section 4.3.

2.2 Case of latent variable models from the exponential family

In this section, we consider the case when is given by Eq. (4). A classical approach to solve penalized maximum likelihood problems in latent variables models with complete likelihood from the exponential family is the Expectation-Maximization (EM) algorithm or a generalization called the Generalized EM (GEM) algorithm (Dempster et al., 1977; McLachlan and Krishnan, 2008; Ng et al., 2012). Our goal here, is to show that MCPG and SAPG are stochastic perturbations of a GEM algorithm.

The EM algorithm is an iterative algorithm: at each iteration, given the current parameter , the quantity , defined as the conditional expectation of the complete log-likelihood under the a posteriori distribution for the current fit of the parameters, is computed:

| (13) |

The EM sequence for the maximization of the penalized log-likelihood is given by (see McLachlan and Krishnan, 2008, Section 1.6.1.)

| (14) |

When is intractable, it was proposed to replace in this EM-penalized algorithm by an approximation - see Algorithm 3. When (see Eq. (11)), this yields the so-called Monte Carlo-EM penalized algorithm (MCEM-pen), trivially adapted from MCEM proposed by Wei and Tanner (1990); Levine and Fan (2004). Another popular strategy is to replace by (see Eq. (12)) yielding to the so-called Stochastic Approximation-EM penalized algorithm (SAEM-pen) - (see Delyon et al. (1999) for the unpenalized version).

When the maximization of Eq. (13) is not explicit, the update of the parameter is modified as follows, yielding the Generalized EM-penalized algorithm (GEM-pen):

| (15) |

This update rule still produces a sequence satisfying the ascent property which is the key property for the convergence of EM (see e.g. Wu, 1983). Here again, the approximations defined in Eq. (11) and Eq. (12) can be plugged in the GEM-pen update Eq. (15) when is not explicit.

We show in the following proposition that the sequence produced by the Proximal-Gradient algorithm Eq. (10) is a GEM-pen sequence since it satisfies the inequality Eq. (15). As a consequence, MCPG and SAPG are stochastic GEM-pen algorithms.

Proposition 1.

Let satisfying H1 and be of the form Eq. (4) with continuously differentiable functions , and . Set . Define by where is given by Eq. (5). Assume that there exists a constant such that for any , and any ,

| (16) |

Let be a (deterministic) positive sequence such that for all .

Then the Proximal-Gradient algorithm Eq. (10) is a GEM-pen algorithm for the maximization of .

3 Convergence of MCPG and SAPG

The convergence of MCPG and SAPG is established by applying recent results from Atchadé et al. (2017) on the convergence of perturbed Proximal-Gradient algorithms. (Atchadé et al., 2017, Theorem 2) applied to the case is of the form , where is an intractable expectation and are explicit, yields

Theorem 2.

We check the conditions of Theorem 2 in the case is resp. given by Eq. (11) for the proof of MCPG and by Eq. (12) for the proof of SAPG. Our convergence analysis is restricted to the case is concave; to our best knowledge, the convergence of the perturbed Proximal-Gradient algorithms when is not concave is an open question.

The novelty in this section is Proposition 5 and Theorem 6 which provide resp. a control of the -norm of the error and the convergence of SAPG. These results rely on a rewriting of taking into account that is a weighted sum of the function evaluated at all the samples drawn from the initialization of the algorithm. This approximation differs from a more classical Monte Carlo approximation (see Theorems 3 and 4 for the convergence of MCPG, which are special cases of the results in Atchadé et al. (2017)).

We allow the simulation step of MCPG and SAPG to rely on a Markov chain Monte Carlo sampling: at iteration , the conditional distribution of given the past is where is a Markov transition kernel having as its unique invariant distribution. The control of the quantities requires some ergodic properties on the kernels along the path produced by the algorithm. These properties have to be uniform in , a property often called the “containment condition” (see e.g. the literature on the convergence of adaptive MCMC samplers, for example Andrieu and Moulines (2006); Roberts and Rosenthal (2007); Fort et al. (2011b)). There are therefore three main strategies to prove the containment condition. In the first strategy, is assumed to be bounded, and a uniform ergodic assumption on the kernels is assumed. In the second one, there is no boundedness assumption on but the property has to be established prior the proof of convergence; a kind of local boundedness condition on the sequence is then applied - see e.g. Andrieu and Moulines (2006); Fort et al. (2011b). The last strategy consists in showing that for some deterministic sequence vanishing to zero when at a rate compatible with the decaying ergodicity rate - see e.g. Saksman and Vihola (2010). The last two strategies are really technical and require from the reader a strong background on controlled Markov chain theory; for pedagogical purposes, we therefore decided to state our results in the first context: we will assume that is bounded.

By allowing MCMC approximations, we propose a theory which covers the case of a biased approximation, called below the biased case: conditionally to the past

| (17) |

the expectation of is not : . As soon as the samplers are ergodic enough (for example, under H4a) and H4b)), the bias vanishes when the number of Monte Carlo points tends to infinity. Therefore, the proof for the biased case when the sequence is constant is the most technical situation since the bias does not decay. It relies on a specific decomposition of the error into a martingale increment with bounded -moments, and a remainder term which vanishes when even when the batch size is constant. Such a behavior of the remainder term is a consequence of regularity properties on the functions , , (see H3c)), on the proximity operator (see H3d)) and on the kernels (see H4c)).

Our theory also covers the unbiased case i.e. when

We therefore establish the convergence of MCPG and SAPG by strengthening the conditions H1 and H2 with

H 3.

-

a)

is concave and the set is a non-empty subset of .

-

b)

is bounded.

-

c)

There exists a constant such that for any ,

where for a matrix , denotes the operator norm associated with the Euclidean vector norm.

-

d)

.

Note that the assumptions H3b)-H3c) imply Eq. (3) and . When is a compact convex set, then H3d) holds for the elastic net penalty, the Lasso or the fused Lasso penalty. (Atchadé et al., 2017, Proposition 11) gives general conditions for H3d) to hold.

Before stating the ergodicity conditions on the kernels , let us recall some basic properties on Markov kernels. A Markov kernel on the measurable set is an application on , taking values in such that for any , is a probability measure on ; and for any , is measurable. Furthermore, if is a Markov kernel, denotes the -th iterate of defined by induction as

Finally, the kernel acts on the probability measures: for any probability measure on , is a probability measure defined by

and acts on the positive measurable functions: for a measurable function , is a measurable function defined by

We refer the reader to Meyn and Tweedie (2009) for the definitions and basic properties on Markov chains. Given a measurable function , define the -norm of a signed measure on and the -norm of a function :

these norms generalize resp. the supremum norm of a function and the total variation norm of a measure.

Our results are derived under the following conditions on the kernels:

H 4.

-

a)

There exist , and a measurable function such that

-

b)

There exist constants and such that for any and ,

-

c)

There exists a constant such that for any ,

Sufficient conditions for the uniform-in- ergodic behavior H4b) are given e.g. in (Fort et al., 2011a, Lemma 2.3.): this lemma shows how to deduce such a control from a minorization condition and a drift inequality on the Markov kernels. Examples of MCMC kernels satisfying these assumptions can be found in (Andrieu and Moulines, 2006, Proposition 12) and (Saksman and Vihola, 2010, Proposition 15) for the adaptive Hastings-Metropolis algorithm, in (Fort et al., 2011a, Proposition 3.1.) for an interactive tempering sampler, in (Schreck et al., 2013, Proposition 3.2.) for the equi-energy sampler, and in (Fort et al., 2015, Proposition 3.1.) for a Wang-Landau type sampler.

Theorem 3 establishes the convergence of MCPG when the number of points in the Monte Carlo sum is constant over iterations and the step size sequence vanishes at a convenient rate. It is proved in (Atchadé et al., 2017, Theorem 4).

Theorem 3.

Assume H1, H2, H3a-c) and H4a-b). Let be the sequence given by Algorithm 1 with a -valued sequence such that and , and with a constant sequence .

Then, with probability one, there exists such that .

Theorem 4 establishes the convergence of MCPG when the number of points in the Monte Carlo sum is increasing; it allows a constant stepsize sequence . It is proved in (Atchadé et al., 2017, Theorem 6).

Theorem 4.

Assume H1, H2, H3a-c) and H4a-b). Let be the sequence given by Algorithm 1 with a -valued sequence and an integer valued sequence such that and .

In the biased case, assume also .

Then, with probability one, there exists such that .

MCPG and SAPG differ in their approximation of at each iteration. We provide below a control of this error for a constant or a polynomially increasing batch size , and polynomially decreasing stepsize sequences and .

The proof is given in Appendix C. This proposition shows that when applying MCPG with a constant batch size , the error does not vanish; this is not the case for SAPG, since even when , the error vanishes as soon as . Since the case "constant batch size" is the usual choice of the practitioners in order to reduce the computational cost of the algorithm, this proposition supports the use of SAPG instead of MCPG.

We finally study the convergence of SAPG without assuming that the batch size sequence is constant, which implies the following assumption on the sequences .

H 5.

The step size sequences , and the batch size sequence satisfy

-

a)

, , , , ,

where .

-

b)

Furthermore,

Let us comment this assumption in the case the batch size sequence is constant. This situation corresponds to the "stochastic approximation regime" where the number of draws at each iteration is (or say, for any ), and it also corresponds to what is usually done by practitioners in order to reduce the computational cost. When for any , then for any . This implies that the condition H5 is satisfied with polynomially decreasing sequences with (and for any ).

When for , then (see Lemma 9). Hence, using Lemma 9, H5a) and H5b) are satisfied with where , and for any .

We can not have since it implies for any .

Theorem 6.

Then with probability one, there exists such that .

Proof.

The proof is in Section D. ∎

4 Numerical illustration in the convex case

In this section, we illustrate the behavior of the algorithms MCPG and SAPG on a toy example. We first introduce the example and then give some guidelines for a specific choice of the sequences , . Finally, the algorithms are compared more systematically on repeated simulations.

4.1 A toy example

The example is a mixed model, where the regression function is linear in the latent variable . More precisely, we observe data from subjects, each individual data being a vector of size : . For the subject , , is the -th measurement at time , . It is assumed that are independent and for all ,

| (18) |

that is, a linear regression model with individual random intercept and slope, the -valued vector being denoted by . The latent variable is . Furthermore,

| (19) |

here, is an unknown parameter and the design matrix is known

| (20) |

The optimization problem of the form Eq. (1) that we consider is the log-likelihood penalized by a lasso penalty: the objective is the selection of the influential covariates

on the two components of . We thus penalize all the elements except and which correspond to the two intercepts; hence, we set

The above model is a latent variable model with complete log-likelihood equal to - up to an additive constant

It is of the form by setting (with denoting the transpose of a matrix)

The a posteriori distribution is a Gaussian distribution on , equal to the product of Gaussian distributions on :

| (21) |

Hence, is explicit and given by

| (22) |

with

| (23) |

Finally, note that in this example, the function is explicit and given by (up to an additive constant)

Thus is a concave function. Furthermore, in this toy example, is linear so that the Lipschitz constant is explicit and equal to

| (24) |

where for a matrix A, denotes the spectral norm. Finally, we assumed that

to fulfill the theoretical boundedness assumption. The MCMC algorithm includes a projection step on if necessary. But in practice, it never happens.

A data set is simulated using this model with , ,

and ,

. The design components

(see Eq. (20)) are drawn from

a centered Gaussian distribution with covariance matrix

defined by

(). To sample the observations, we use a parameter

vector defined as follows:

; the other components are set

to zero, except components randomly selected ( among the

components and among the components

) and chosen uniformly in -

see the last row on Figure 7.

4.2 Guidelines for the implementation

In this section, we give some guidelines on the choice of the sequences and . We illustrate the results on single runs of each algorithm. We use the same random draws for all the algorithms to avoid potential differences due to the randomness of the simulations. Similar results have been observed when simulations are replicated. We refer to Section 4.3 for replicated simulations.

Classical sequences and are of the form:

| (25) |

| (26) |

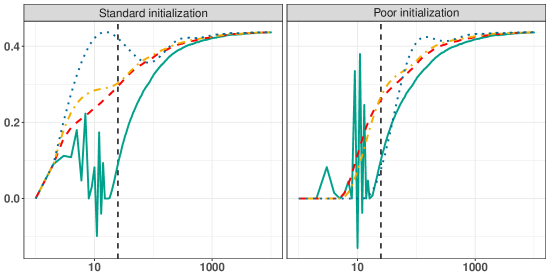

Impact of and on the transient phase: the theoretical study on the asymptotic behavior of SAPG and MCPG is derived under the assumption that : when , this property holds for any large enough. In this section, we illustrate the role of for small values of that is, in the transient phase of the algorithm. In Figure 1, we display the behavior of MCPG and SAPG for two different values of the initial point : on the left, it corresponds to a standard initialization () while on the right, it corresponds to a poor initialization - which mimics what may happen in practice for challenging numerical applications.

On both plots, we indicate by a vertical line the smallest such that - remember that in this example, is explicit (see Eq. (24)). The plots show the estimation of component #245, as a function of the number of iterations . In all cases, , , , and for SAPG, . The dotted blue curve displays a run of SAPG when ; the dashed-dotted yellow curve displays a run of SAPG when ; the dashed red curve displays a run of SAPG when ; the green solid curve displays a run of MCPG when .

The stability of MCPG during the transient phase depends crucially on the first values of the sequence . Then when is large enough so that (after the vertical line), MCPG is more stable and gets smoother. For SAPG, a small value of implies an important impact of the initial point . When this initial point is poorly chosen, a small value of delays the convergence of SAPG. A value of around is a good compromise.

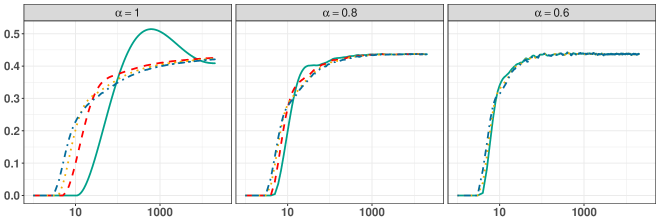

Role of and : Figure 2 displays the behavior of SAPG for different values of and with , and . The plots show that the larger the parameter is, the longer the transient phase is. We then recommend to set close to . The parameter seems to have an impact only when is close to . Therefore, we recommend to set constant during the transient phase () and then to decrease it rapidly in the convergence phase.

Random stepsize sequence : The convergence of the SAPG algorithm can suffer from the scale difference of the parameters, when run with the same stepsize sequence applied to each component of .

Ideally each component of should have a specific value adapted to its scale. But it can be time-consuming to find, by hand-tuning, a sequence that ensures a fast and stable convergence of the algorithm. As an alternative, we suggest to use a matrix-valued random sequence and replace the update rule of SAPG by

We propose to define the matrix as a diagonal matrix with entries depending on , where is an approximation of the hessian of the likelihood (we give an example of such an approximation in Section 5). Through numerical experiments, we observed that asymptotically, converges. Hence, to ensure a stepsize sequence decaying like asymptotically, we propose the following definition of the random sequence:

| (27) |

4.3 Long-time behavior of the algorithm

In this section, we illustrate numerically the theoretical results on the long term convergence of the algorithms MCPG, SAPG and SAEM-pen (i.e. Algorithm 3 applied with ) and EM-pen on the toy model. In this example, the exact algorithm EM-pen (see Eq. (14)) applies: the quantity is an explicit expectation under a Gaussian distribution . Therefore, we use this example (i) to illustrate the convergence of the three stochastic methods to the same limit point as EM-pen, (ii) to compare the two approximations and of in a GEM-pen approach, and (iii) to study the effect of relaxing the M-step by comparing the GEM-pen and EM-pen approaches namely SAPG and SAEM-pen.

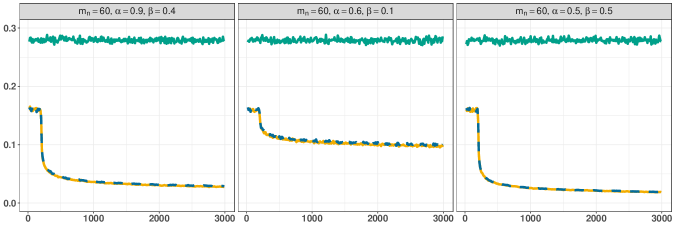

The sequences and are defined as follows: , and ; three different pairs are considered: , , and . The algorithms are implemented with a fixed batch size . independent runs of each algorithm are performed. For the penalty term, we set . In MCPG, SAPG and SAEM-pen, the simulation step at iteration relies on exact sampling from - see Eq. (21); therefore, in this toy example, the Monte Carlo approximation of is unbiased.

On Figure 3, for the three algorithms MCPG, SAPG and SAEM-pen, the evolution of an approximation of with iterations is plotted, where, for a random variable , . This -norm is approximated by a Monte Carlo sum computed from independent realizations of ; here, is explicit (see Eq. (22)). SAEM-pen and SAPG behave similarly; the -norm converges to , and the convergence is slower when - this plot illustrates the result stated in Proposition 5, Section 3. This convergence does not hold for MCPG because the size of the Monte Carlo approximation is kept fixed.

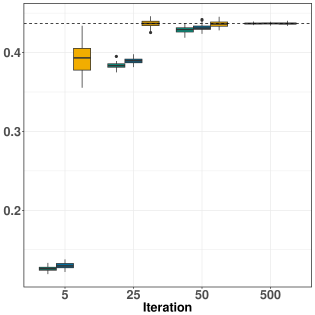

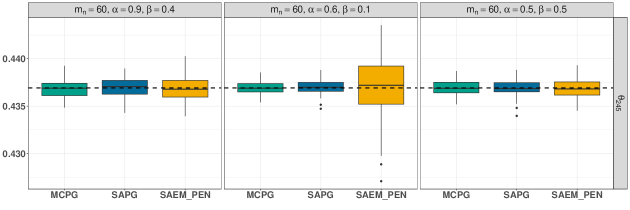

We compared the limiting vectors obtained by each algorithm, over the independent runs. They are all equal, and the limiting vector is also the limiting value of the EM-pen algorithm. In order to discuss the rate of convergence, we show the behavior of the algorithms when estimating the component of the regression coefficients; this component was chosen among the non-null component of . Figure 4 shows the boxplot of estimations of the component of the vector , when , for the algorithms MCPG, SAPG and SAEM-pen with . Here, SAPG and MCPG behave similarly, with a smaller variability among the runs than SAEM-pen. SAEM-pen converges faster than SAPG and MCPG which was expected since they correspond respectively to stochastic perturbations of EM-pen and GEM-pen algorithms. Figure 5 shows the boxplot of estimations by MCPG, SAPG and SAEM-pen of the component after iterations with different values for the parameters and . We observe that the three algorithms give similar final estimates for the three conditions on parameters and . This is due to the fact that with , the algorithms have already attained the convergence phase when . This allows the algorithms to quickly converge toward the limit points when .

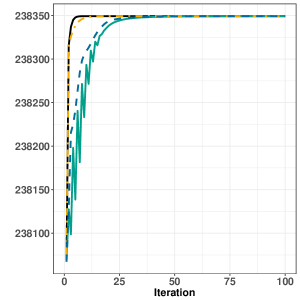

Figure 6 shows the convergence of a Monte Carlo approximation of based on independent estimations obtained by three different algorithms: EM-pen, MCPG, SAPG and SAEM-pen run with and . Here again, all the algorithms converge to the same value and EM-pen and SAEM-pen converge faster than MCPG and SAPG. We observe that the path of SAPG is far more smooth than the path of MCPG.

Finally, Figure 7 shows the support of the vector (where the component and are removed) estimated by MCPG, SAPG, SAEM-pen and EM-pen (the estimated support is the same for the four algorithms). The frequency, among independent runs, for each component to be in the support of the limit value , is displayed. Algorithms are implemented with and . For all algorithms, we observe that most of the non-null components of are non-null components of . Note also that the stochastic algorithms MCPG, SAPG and SAEM-pen converge to the same vector as EM-pen.

5 Inference in non-linear mixed models for pharmacokinetic data

In this section, SAPG is applied to solve a more challenging problem. The objective is to illustrate the algorithm in cases that are not covered by the theory. The application is in pharmacokinetic analysis, with non-linear mixed effect models (NLMEM); in this application, the penalized maximum-likelihood inference is usually solved by the SAEM-pen algorithm, possibly combined with an approximation of the M-step when it is non explicit. This section also provides a numerical comparison of SAPG and SAEM-pen. Both algorithms have a simulation step; in this more challenging application, it will rely on a Markov chain Monte Carlo (MCMC) sampler - see Section 5.1. Therefore, for both algorithms, is approximated by a biased Monte Carlo sum.

We start with a presentation of the statistical analysis and its translation into an optimization problem; we then propose a modification of the SAPG by allowing a random choice of the stepsize sequence , to improve the numerical properties of the algorithm. We conclude the section by a comparison of the methods on a pharmacokinetic real data set.

5.1 The non-linear mixed effect model

Pharmacokinetic data are observed along time for patients. Let be the vector of the drug concentrations observed at time () for the -th patient (). The kinetic of the drug concentration is described by a non-linear pharmacokinetic regression model , which is a function of time and unobserved pharmacokinetic parameters . These parameters are typically the rates of absorption or elimination of the drug by the body. An example is detailed below. The variability among patients is modeled by the randomness of the hidden variables . These pharmacokinetic parameters may be influenced by covariates, such as age, gender but also genomic variables. Among these high dimension factors, only few of them are correlated to . Their selection can thus be performed by optimizing the likelihood with a sparsity inducing penalty, an optimization problem that enters problem Eq. (1). However, the likelihood is generally not concave, that is, through this example, we explore beyond the framework in which we are able to prove the convergence of MCPG and SAPG (see Section 3).

Let us now detail the model and the optimization problem. The mixed model is defined as

| (28) |

where the measurement errors are centered, independent and identically normally distributed with variance . Individual parameters for the -th subject is a -dimensional random vector, independent of . In a high dimension context, the ’s depend on covariates (typically genomics variables) gathered in a matrix design . The distribution of is usually assumed to be normal with independent components

| (29) |

where is the mean parameter vector and is the covariance matrix of the random parameters , assumed to be diagonal. The unknown parameters are .

A typical function is the two-compartmental pharmacokinetic model with first order absorption, describing the distribution of a drug administered orally. The drug is absorbed from the gut and reaches the blood circulation where it can spread in peripheral tissues. This model corresponds to with defined as

| (30) | |||||

with , , and where , , are the amount of drug in the depot, central and peripheral compartments, respectively; , are the volume of the central compartment and the peripheral compartment, respectively; and are the inter compartment and global elimination clearances, respectively. To assure positiveness of the parameters, the hidden vector is

It is easy to show that the model described by Eqs. (28)-(29) belongs to the curved exponential family (see Eq. (4)) with minimal sufficient statistics:

and , . The function is given by .

The selection of genomic variables that influence all coordinates of could be obtained by optimizing the log-likelihood penalized by the function , the norm of with a regularization parameter.

However, this estimator is not invariant under a scaling transformation (ie ) (see e.g. (Lehmann and Casella, 2006)). In our high dimension experiments, the scale of the hidden variables has a non negligible influence on the selection of the support. To be more precise, let us denote, for ,

the coordinates corresponding to the -th pharmacokinetic parameter of function . When the variance of the random parameters is low, the algorithms tend to select too many covariates. This phenomenon is strengthened with a small number of subjects as random effect variances are more difficult to estimate. A solution is to consider the following penalty

that makes the estimator invariant under scaling transformation. It was initially proposed by Städler et al. (2010) to estimate the regression coefficients and the residual error’s variance in a mixture of penalized regression models. However, the resulting optimization problem is difficult to solve directly because the variance of the random effect appears in the penalty term. Therefore, we propose a new parameterization

and . Then, the optimization problem is the following:

| (31) |

This problem can be solved using MCPG, SAPG or SAEM-pen algorithms. Indeed, the complete log-likelihood is now - up to an additive constant -

It is again a complete likelihood from the exponential family, with the statistic unchanged and the functions and given by - up to an additive constant -

With these definitions of and , the M-step of SAEM-pen amounts to compute the optimum of a convex function, which is solved numerically by a call to a cyclical coordinate descent implemented in the R package glmnet (Friedman et al., 2010).

MCMC sampler.

In the context of non-linear mixed models, simulation from can not be performed directly like in the toy example. We then use a MCMC sampler based on a Metropolis Hastings algorithm to perform the simulation step. Two proposal kernels are successively used during the iterations of the Metropolis Hastings algorithm. The first kernel corresponds to the prior distribution of that is the Gaussian distribution . The second kernel corresponds to a succession of uni-dimensional random walk in order to update successively each component of . The variance of each random walk is automatically tuned to reach a target acceptance ratio following the principle of an adaptive MCMC algorithm (Andrieu and Thoms, 2008).

Adaptive random stepsize sequences.

In the context of NLMEM, numerical experiments reveal that choosing a deterministic sequence that achieve a fast convergence of SAPG algorithm could be difficult. Indeed, parameters to estimate are of different scales. For example, random effect and residual variances are constrained to be positive. Some of them are close to zero, some are not. As explained in Section 4.2, an alternative is to implement a matrix-valued random sequence . The gradient and the hessian of the likelihood can be approximated by stochastic approximation using the Louis principle (see McLachlan and Krishnan, 2008, Chapter 4). Let us denote the stochastic approximation of the hessian obtained at iteration as explained by Samson et al. (2007). Note that no supplementary random samples are required to obtain this approximation. Along the iterations, each diagonal entry of the matrix converges: this limiting value can be seen as a simple way to automatically tune a good , that is parameter specific. The entries are then defined by Eq. (27).

5.2 Simulated data set.

The convergence of the corresponding algorithms is illustrated on simulated data. Data are generated with the model defined by Eq. (5.1) and , , . The design matrix is defined by Eq. (20), with components drawn from with (). Parameter values are

the other components are set to zero, except and that are set to . The matrix is diagonal with diagonal elements equal to .

The penalty function is set to

| (32) |

only the parameters corresponding to a covariate effect being penalized. The optimization problem Eq. (1) with regularization parameter is solved on this dataset with SAEM-pen and SAPG; we run SAPG with the random sequence as described above (see (27)) with . For both algorithms, the stochastic approximation step size was set to:

| (33) |

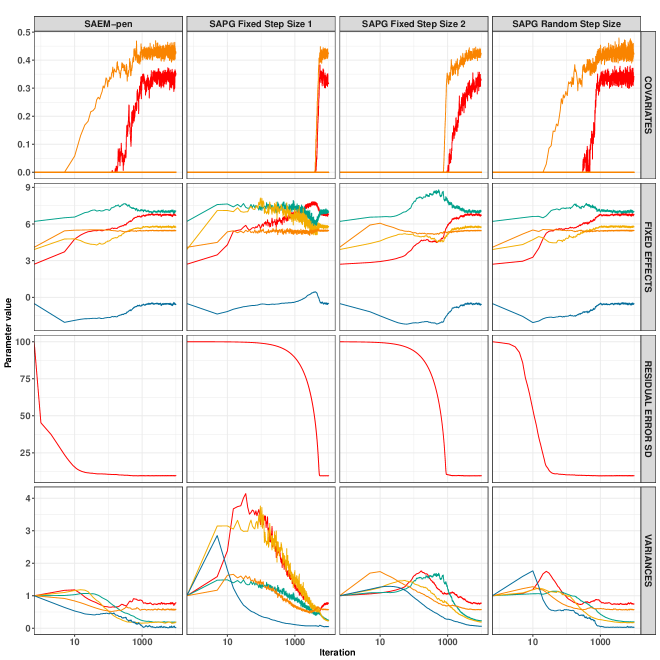

We set and . Figure 8 shows the convergence of SAEM-pen and three parameterizations of SAPG: i) a version with for all the components of , ii) a version with for , for and for , and iii) a version with adaptive random step sizes. For the four algorithms, all the parameters corresponding to a covariate effect are estimated to zero except the two components and . The version of SAPG with a same for all the component is the one that converge the most slowly. When the is tuned differently according the type of parameters, the convergence of SAPG is accelerated. Algorithms SAEM-pen and SAPG with adaptive random step sizes have a similar fast convergence profile.

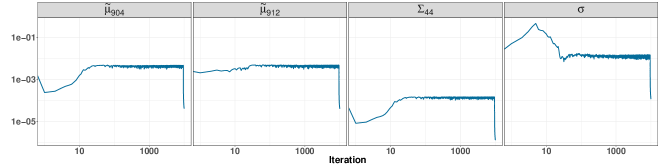

Figure 9 presents the evolution of four entries of the matrix along the iterations of SAPG, corresponding to the components , , and . We can notice that they are not on the same scale. They vary during the first iterations and converge to limiting values before iteration . Then the step sizes decrease to 0, following the definition given in Eq. (27).

5.3 Application to real data

Algorithms SAEM-pen and SAPG with matrix-valued random sequence are applied to real data of the pharmacokinetic of dabigatran () from two cross over clinical trials (Delavenne et al., 2013; Ollier et al., 2015). These trials studied the drug-drug interaction between and different Pgp-inhibitors. From these trials, the pharmacokinetics of are extracted from subjects with no concomitant treatment with Pgp-inhibitors. The concentration of dabigatran is measured at sampling times for each patient. Each subject is genotyped using the DMET microarray from Affymetrix. Single nucleotide polymorphisms (SNP) showing no variability between subjects are removed and SNP are included in the analysis.

Function of the non-linear mixed model is defined as the two compartment pharmacokinetic model with first order absorption previously described (see Eq. (5.1)) (Delavenne et al., 2013). The penalty function is defined by Eq. (32).

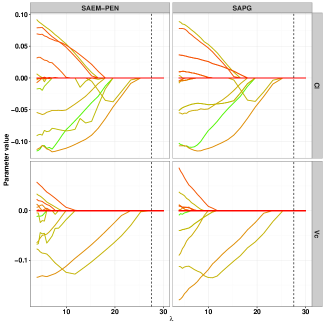

Because of the limited number of subjects, the influence of genetic covariates is only studied on and parameters, that characterize the elimination process and are the most likely to be influenced by the genetic. Finally, random effect variances of and are set to in accordance with previously published population pharmacokinetic of dabigatran (Delavenne et al., 2013). The other variance parameters are estimated. The penalized likelihood problem (Eq. 31) is solved on the data with the SAEM-pen and SAPG algorithms, for different values of parameter . SAPG algorithm is run using the random sequence given in Eq. (27). The best regularization parameter is chosen with a data-driven approach based on the EBIC criteria (Chen and Chen, 2008).

Figure 10 shows the results. The regularization paths of and parameters using both algorithms correspond to the evolution of covariate coefficient estimates as a function of the value of . They are reconstructed with low noise for both algorithms, are very similar for high values of but less for lower values of .

Finally, the selected model has all covariates parameters set to zero. This means that none of the genetic covariates influence the distribution of the individual parameters. This result is not surprising given the low number of subjects and the fact that a large part of the inter individual variability is due to the dissolution process of the drug (Ollier et al., 2015) and is therefore not influenced by genetic covariates. This lack of relationship between dabigtran’s pharmacokinetic parameters and genetic covariates has already been highlighted in an other study (Gouin-Thibault et al., 2017).

6 Conclusion

In this work, we propose a new Stochastic Proximal-Gradient algorithm to solve penalized maximum likelihood problems when the likelihood is intractable: the the gradient is approximated through a stochastic approximation scheme. We provide a theoretical convergence analysis of this new algorithm and illustrate these results numerically on a simulated toy example in the case of a concave likelihood function. The robustness to the non concave case is explored through a more challenging application to population pharmacokinetic analysis relying on penalized inference in non-linear mixed effects models.

Appendix

Appendix A Proof of Proposition 1

Lemma 7.

Under the assumptions of Proposition 1, for any , and any ,

| (34) |

Proof.

Fix and . The derivative of the function is and this gradient is -lipschitz. From a Taylor expansion to order at and since the gradient is Lipschitz, we have

We then choose , use and conclude by the equality . ∎

Proof of Proposition 1

Appendix B Technical lemmas

Define

Lemma 8.

For any , .

Proof.

For any , we have from which the result follows. ∎

Lemma 9.

Let and . Set for any . Then for any large enough,

Furthermore, .

The proof of Lemma 9 relies on standard Taylor’s expansions with explicit formulas for the remainder. The proof is omitted.

Lemma 10.

Let and . For any , when ,

Proof.

We have

Let such that for any , . For any constant , there exist constants (whose value can change upon each appearance) such that

This concludes the proof. ∎

Lemma 11.

Let be a sequence of matrices and be a sequence of vectors. Let be given by Eq. (12). For any

Proof.

By definition of , it holds where

By iterating, we have

from which the lemma follows. ∎

Proof.

By H4a), there exists a constant such that for any and , . In addition, by the drift assumption on the kernels , we have

Similarly, by using , we have

A trivial induction shows that

from which the first two results follow. For the third one: by Lemma 11 applied with (the identity matrix) and , we have for any ,

By the Minkowsky inequality and the inequality , we have

By definition, and by Lemma 8,

Hence, . ∎

Define the Proximal-Gradient operator

Lemma 13.

Proof.

The proof of (i) is on the same lines as the proof of (Atchadé et al., 2017, Lemma 15), and is omitted. For (ii), we write by using H3b) and H3c),

We then conclude by (i). The LHS in (iii) is upper bounded by

Under H3, there exists a constant such that for all and (see (Atchadé et al., 2017, Proposition 12))

We then conclude by (i). ∎

Lemma 14.

Assume H4. For any , there exists a function such that and . In addition, there exists a constant such that for any ,

Proof.

Set . Observe that, when exists, this function satisfies . Note that under H4a)-H4b), there exist and such that for any ,

the RHS is finite, thus showing that exists. This inequality also proves that . The Lipschitz property is established in (Fort et al., 2011a, Lemma 4.2.) and its proof uses H4c). ∎

Appendix C Proof of Proposition 5

Throughout this section, set . By Lemma 11, with

Since , then

By H3c), Lemma 12 and Lemma 13, there exists a constant such that . By Lemma 10, this yields . For the last term, we use a martingale decomposition.

By Lemma 14, there exists a function such that

and . Hence, we write

with

we used that . Upon noting that is a martingale-increment, and

is a martingale-increment, we have by two successive applications of (Hall and Heyde, 1980, Theorem 2.10):

By Lemma 10, this term is . For the second term, we write

By Lemma 12 and Lemma 14, the RHS is so that this second term is . Finally, for the third term, by using Lemma 12, Lemma 13 and Lemma 14, we write

Again by Lemma 10, this last term is . Therefore, .

Appendix D Proof of Theorem 6

Throughout the proof, we will write instead of .

Proof of Theorem 6

We prove the almost-sure convergence of the three random sums given in Theorem 2. The third one is finite almost-surely since its expectation is finite (see Proposition 15). The first two ones are of the form where is respectively

Note that (the filtration is defined by Eq. (17)). By Lemma 13 and H3b-c), for both cases, there exists a constant such that almost-surely, for any ,

We then conclude by Proposition 16.

Proof.

Proposition 16.

By Lemma 11 applied with , we decompose this sum into four terms:

We have by using Eq. (35),

By H5a), so the RHS is finite thus implying that is finite almost-surely.

Using Eq.(36), there exists a constant such that

By H3b)-H3c), H5a) and Lemma 12, the RHS is finite thus implying that is finite almost-surely.

Similarly, there exists a constant such that

By H3c), the RHS is bounded (up to a multiplicative constant) by ; and by H5a) and Lemmas 12 and 13, this sum is finite. Hence is finite almost-surely.

We give the proof of the convergence of the last term in the biased case: . The proof in the unbiased case corresponds to the following lines with and . Set . By Lemma 14, there exists such that

and . Hence, we have

where

Upon noting that , the almost-sure convergence of the series is proved by checking criteria for the almost-sure convergence of a martingale. By (35), there exists a constant such that

By H5a), Lemma 12 and (Hall and Heyde, 1980, Theorem 2.10), the RHS is finite. (Hall and Heyde, 1980, Theorem 2.17) implies that is finite almost-surely. For the second term, we write

so that, by Lemmas 12 and 14, this series is finite almost-surely if . From Eq. (35) and Eq. (36), there exists a constant such that

References

- Andrieu and Moulines [2006] C. Andrieu and E. Moulines. On the ergodicity properties of some adaptive MCMC algorithms. Annals of Applied Probability, 16(3):1462–1505, 2006.

- Andrieu and Thoms [2008] C. Andrieu and J. Thoms. A tutorial on adaptive MCMC. Statistics and Computing, 18(4):343–373, 2008.

- Atchadé et al. [2017] Y. Atchadé, G. Fort, and E. Moulines. On perturbed proximal gradient algorithms. Journal of Machine Learning Research, 18(10):1–33, 2017.

- Bartholomew et al. [2011] D. Bartholomew, M. Knott, and I. Moustaki. Latent variable models and factor analysis. Wiley Series in Probability and Statistics. John Wiley & Sons, Ltd., Chichester, third edition, 2011.

- Bauschke and Combettes [2011] H.H. Bauschke and P.L. Combettes. Convex analysis and monotone operator theory in Hilbert spaces. CMS Books in Mathematics/Ouvrages de Mathématiques de la SMC. Springer, New York, 2011.

- Beck and Teboulle [2009] Amir Beck and Marc Teboulle. A fast iterative shrinkage-thresholding algorithm for linear inverse problems. SIAM Journal on Imaging Sciences, 2(1):183–202, 2009.

- Benveniste et al. [1990] A. Benveniste, M. Métivier, and P. Priouret. Adaptive algorithms and stochastic approximations, volume 22 of Applications of Mathematics. Springer-Verlag, Berlin, 1990.

- Bertrand and Balding [2013] J. Bertrand and D.J. Balding. Multiple single nucleotide polymorphism analysis using penalized regression in nonlinear mixed-effect pharmacokinetic models. Pharmacogenetics and Genomics, 23(3):167–174, 2013.

- Bickel and Doksum [2015] P. J. Bickel and K. A. Doksum. Mathematical statistics—basic ideas and selected topics. Vol. 1. Texts in Statistical Science Series. CRC Press, Boca Raton, FL, second edition, 2015.

- Chen et al. [2017] H. Chen, D. Zeng, and Y. Wang. Penalized nonlinear mixed effects model to identify biomarkers that predict disease progression. Biometrics, 2017.

- Chen and Chen [2008] J. Chen and Z. Chen. Extended Bayesian information criteria for model selection with large model spaces. Biometrika, 95(3):759–771, 2008.

- Combettes and Pesquet [2015] Patrick L Combettes and Jean-Christophe Pesquet. Stochastic quasi-fejér block-coordinate fixed point iterations with random sweeping. SIAM Journal on Optimization, 25(2):1221–1248, 2015.

- Combettes and Wajs [2005] Patrick L Combettes and Valérie R Wajs. Signal recovery by proximal forward-backward splitting. Multiscale Modeling & Simulation, 4(4):1168–1200, 2005.

- Combettes and Pesquet [2011] P.L. Combettes and J.C. Pesquet. Proximal splitting methods in signal processing. In Fixed-point algorithms for inverse problems in science and engineering, volume 49 of Springer Optim. Appl., pages 185–212. Springer, New York, 2011.

- Combettes and Pesquet [2016] P.L. Combettes and J.C. Pesquet. Stochastic Approximations and Perturbations in Forward-Backward Splitting for Monotone Operators. Online Journal Pure and Applied Functional Analysis, 1(1):1–37, 2016.

- Delavenne et al. [2013] X. Delavenne, E. Ollier, T. Basset, L. Bertoletti, S. Accassat, A. Garcin, S. Laporte, P. Zufferey, and P. Mismetti. A semi-mechanistic absorption model to evaluate drug–drug interaction with dabigatran: application with clarithromycin. British Journal of Clinical Pharmacology, 76(1):107–113, 2013.

- Delyon et al. [1999] B. Delyon, M. Lavielle, and E. Moulines. Convergence of a stochastic approximation version of the EM algorithm. Annals of Statistics, 27(1):94–128, 1999.

- Dempster et al. [1977] Arthur P Dempster, Nan M Laird, and Donald B Rubin. Maximum likelihood from incomplete data via the EM algorithm. Journal of the royal statistical society. Series B, pages 1–38, 1977.

- Fort et al. [2011a] G. Fort, E. Moulines, and P. Priouret. Convergence of adaptive and interacting Markov chain Monte Carlo algorithms. Annals of Statistics, 39(6):3262–3289, 2011a.

- Fort et al. [2011b] G. Fort, E. Moulines, and P. Priouret. Convergence of adaptive and interacting Markov chain Monte Carlo algorithms. Annals of Statistics, 39(6), 2011b.

- Fort et al. [2015] Gersende Fort, Benjamin Jourdain, Estelle Kuhn, Tony Lelièvre, and Gabriel Stoltz. Convergence of the wang-landau algorithm. Mathematics of Computation, 84(295):2297–2327, 2015.

- Friedman et al. [2010] J. Friedman, T Hastie, and R. Tibshirani. Regularization paths for generalized linear models via coordinate descent. Journal of Statistical Software, 33(1):1–22, 2010.

- Gouin-Thibault et al. [2017] I Gouin-Thibault, X Delavenne, A Blanchard, V Siguret, JE Salem, C Narjoz, P Gaussem, P Beaune, C Funck-Brentano, M Azizi, et al. Interindividual variability in dabigatran and rivaroxaban exposure: contribution of abcb1 genetic polymorphisms and interaction with clarithromycin. Journal of Thrombosis and Haemostasis, 15(2):273–283, 2017.

- Hall and Heyde [1980] P. Hall and C. C. Heyde. Martingale limit theory and its application. Academic Press, Inc. [Harcourt Brace Jovanovich, Publishers], New York-London, 1980. Probability and Mathematical Statistics.

- Kushner and Yin [2003] H.J. Kushner and G.G. Yin. Stochastic approximation and recursive algorithms and applications, volume 35 of Applications of Mathematics. Springer-Verlag, New York, second edition, 2003.

- Lehmann and Casella [2006] E.L. Lehmann and G. Casella. Theory of point estimation. Springer Science & Business Media, 2006.

- Levine and Fan [2004] R. A. Levine and J. Fan. An automated (Markov chain) Monte Carlo EM algorithm. Journal of Statistical Computation and Simulation, 74(5):349–359, 2004. ISSN 0094-9655.

- Lin et al. [2015] J. Lin, L. Rosasco, S. Villa, and D.X. Zhou. Modified Fejer Sequences and Applications. Technical report, arXiv:1510:04641v1 math.OC, 2015.

- McLachlan and Krishnan [2008] G.J. McLachlan and T. Krishnan. The EM algorithm and extensions. Wiley Series in Probability and Statistics. Wiley-Interscience, Hoboken, NJ, second edition, 2008.

- Meyer [1976] Robert R Meyer. Sufficient conditions for the convergence of monotonic mathematicalprogramming algorithms. Journal of Computer and System Sciences, 12(1):108–121, 1976.

- Meyn and Tweedie [2009] S. Meyn and R. L. Tweedie. Markov chains and stochastic stability. Cambridge University Press, Cambridge, second edition, 2009.

- Moreau [1962] Jean-Jacques Moreau. Fonctions convexes duales et points proximaux dans un espace hilbertien. Comptes Rendus Mathématique de l’Académie des Sciences, 255:2897–2899, 1962.

- Ng et al. [2012] S.K. Ng, T. Krishnan, and G.J. McLachlan. The EM algorithm. In Handbook of computational statistics—concepts and methods. 1, 2, pages 139–172. Springer, Heidelberg, 2012.

- Ollier et al. [2015] E. Ollier, S. Hodin, T. Basset, S. Accassat, L. Bertoletti, P. Mismetti, and X. Delavenne. In vitro and in vivo evaluation of drug–drug interaction between dabigatran and proton pump inhibitors. Fundamental & Clinical Pharmacology, 29(6):604–614, 2015.

- Ollier et al. [2016] E. Ollier, A. Samson, X. Delavenne, and V. Viallon. A saem algorithm for fused lasso penalized nonlinear mixed effect models: Application to group comparison in pharmacokinetics. Computational Statistics & Data Analysis, 95:207–221, 2016.

- Parikh and Boyd [2013] N. Parikh and S. Boyd. Proximal Algorithms. Foundations and Trends in Optimization, 1(3):123–231, 2013.

- Robert and Casella [2004] C. P. Robert and G. Casella. Monte Carlo statistical methods. Springer Texts in Statistics. Springer-Verlag, New York, second edition, 2004.

- Roberts and Rosenthal [2007] G.O. Roberts and J.S. Rosenthal. Coupling and ergodicity of adaptive MCMC. Journal of Applied Probablity, 44:458–475, 2007.

- Rosasco et al. [2014] L. Rosasco, S. Villa, and B.C. Vu. Convergence of a Stochastic Proximal Gradient Algorithm. Technical report, arXiv:1403.5075v3, 2014.

- Rosasco et al. [2016] L. Rosasco, S. Villa, and B.C. Vu. A stochastic inertial forward–backward splitting algorithm for multivariate monotone inclusions. Optimization, 65(6):1293–1314, 2016.

- Saksman and Vihola [2010] E. Saksman and M. Vihola. On the ergodicity of the adaptive Metropolis algorithm on unbounded domains. The Annals of applied probability, 20(6):2178–2203, 2010.

- Samson et al. [2007] A. Samson, M. Lavielle, and F. Mentré. The SAEM algorithm for group comparison tests in longitudinal data analysis based on non-linear mixed-effects model. Statistics in medicine, 26(27):4860–4875, 2007.

- Schreck et al. [2013] A. Schreck, G. Fort, and E. Moulines. Adaptive equi-energy sampler: convergence and illustration. ACM Transactions on Modeling and Computer Simulation, 23(1):Art. 5, 27, 2013.

- Städler et al. [2010] N. Städler, P. Bühlmann, and S. van de Geer. l1-penalization for mixture regression models. TEST, 19(2):209–256, 2010.

- Wei and Tanner [1990] G. Wei and M. Tanner. A Monte-Carlo implementation of the EM algorithm and the poor man’s data augmentation algorithms. Journal of the American statistical Association, 85:699–704, 1990.

- Wu [1983] C.-F.J. Wu. On the convergence properties of the EM algorithm. Annals of Statistics, 11(1):95–103, 1983.

- Zangwill [1969] W.I. Zangwill. Nonlinear programming: a unified approach. Prentice-Hall, Inc., Englewood Cliffs, N.J., 1969. Prentice-Hall International Series in Management.