\pkgRgbp: An \proglangR Package for Gaussian, Poisson,

and Binomial Random Effects Models

with Frequency Coverage Evaluations

Hyungsuk Tak, Joseph Kelly, Carl Morris \Plaintitle\pkgRgbp: An R Package for Gaussian, Poisson, and Binomial Random Effects Modeling and Frequency Method Checking on Overdispersed Data \Shorttitle\pkgRgbp: Random Effects Models, with Frequency Coverage Evaluations \Abstract

\pkgRgbp is an \proglangR package that provides estimates and verifiable confidence intervals for random effects in two-level conjugate hierarchical models for overdispersed Gaussian, Poisson, and Binomial data. \pkgRgbp models aggregate data from independent groups summarized by observed sufficient statistics for each random effect, such as sample means, possibly with covariates. \pkgRgbp uses approximate Bayesian machinery with unique improper priors for the hyper-parameters, which leads to good repeated sampling coverage properties for random effects. A special feature of \pkgRgbp is an option that generates synthetic data sets to check whether the interval estimates for random effects actually meet the nominal confidence levels. Additionally, \pkgRgbp provides inference statistics for the hyper-parameters, e.g., regression coefficients.

\Keywordsoverdispersion, hierarchical model, adjustment for density maximization, frequency method checking, \proglangR

\Plainkeywordsmultilevel model, conjugate hierarchical generalized linear models, frequency method checking, coverage probability, shrinkage, R

\Address

Hyungsuk Tak

Department of Statistics

Harvard University

1 Oxford Street, Cambridge, MA

E-mail:

Joseph Kelly

Google, Inc.

76 Ninth Avenue, New York, NY

E-mail:

Carl Morris

Department of Statistics

Harvard University

1 Oxford Street, Cambridge, MA

E-mail:

1 Introduction

Gaussian, Poisson, or Binomial data from several independent groups sometimes have more variation than the assumed Gaussian, Poisson, or Binomial distributions of the first-level observed data. To account for this extra variability, called overdispersion, a two-level conjugate hierarchical model regards first-level mean parameters as random effects that come from a population-level conjugate prior distribution. The main goal of our two-level conjugate modeling is to estimate these random effects for a comparison between groups. For example, this model can be used to estimate unknown true batting averages (random effects) of baseball players for a comparison among players based on their numbers of hits and at-bats possibly with their covariate information.

With an assumption of homogeneity within each group, the observed data are group-level aggregate data from independent groups, composed of sufficient statistics for their random effects (without the population-level data). Specifically, the data for the Gaussian model consist of each group’s sample mean and its standard error, those for the Poisson model use each group’s outcome count and an exposure measure, and those for the Binomial model use the number of each group’s successful outcomes together with the total number of trials. For example, the observed data for the Binomial model can be the number of hits out of at-bats for each of baseball players, a sufficient statistic for the unknown true batting average of each player. The data analyzed by \pkgRgbp may incorporate each group’s covariate information, e.g., each player’s position.

These types of data are common in various fields for estimating random effects. For example, biologists may be interested in unknown true tumor incidence rates in analyzing litter data composed of each litter’s number of tumor-bearing animals out of total number of animals at risk (tamura1987stabilized). The unknown true mortality rates on myocardial infarction can be estimated based on the death rate data collected from several independent clinical studies via a meta analysis (gelman2014bayesian). County-level or state-level summary data in small area estimation problems (ghosh1994small; rao2003small) can be used to estimate population parameters, such as unknown unemployment rates.

For such data, assuming homogeneity within each group, \pkgRgbp’s two-level model may be viewed as a conjugate hierarchical generalized linear model (HGLM, lee1996hierarchical) where each random effect comes from a conjugate prior distribution. However, the HGLM focuses on estimating regression coefficients to explore associations between covariates and observed data. While \pkgRgbp does that too, its emphasis concerns making valid point and interval estimates for the random effects for a comparison among groups.

A defining feature of \pkgRgbp is to evaluate the repeated sampling coverage properties of the interval estimates for random effects (morris1997; daniels1999prior; tang2002fitting; tang2011; morris2012). This procedure distinguishes \pkgRgbp from other \proglangR packages for similar hierarchical models, such as \pkghglm (ronnegaard2011hglm) for fitting conjugate hierarchical generalized models, because most software produces only estimation results without providing a quick way to evaluate their estimation procedures. The evaluation procedure which we call frequency method checking uses a parametric bootstrapping method that generates synthetic data sets given the fitted values of the estimated hyper-parameters. The frequency method checking estimates the coverage rates of interval estimates based on the simulated data sets and checks whether the estimated coverage rates achieve (or exceed) the nominal confidence level.

Rgbp combines Bayesian modeling tools with our improper hyper-prior distributions on the second-level parameters. These hyper-prior distributions are known to produce good repeated sampling coverage rates for the Bayesian interval estimates for the random effects in two-level Gaussian models (tang2011; morris2012; kelly2014advances). We extend these hyper-prior distributions for \pkgRgbp’s Poisson and Binomial hierarchical models.

For fitting the hierarchical model, \pkgRgbp uses adjustment for density maximization (ADM, carl1988; morris1997; tang2011). ADM approximates a posterior density or a likelihood function by fitting a selected (one dimensional) Pearson family, based on the first two derivatives of the given density function. For example, when the Normal distribution is the chosen Pearson family, ADM reduces to a Delta method via maximum likelihood estimation. Besides ADM, \pkgRgbp provides an option for the Binomial hierarchical model to draw independent posterior samples of random effects and hyper-parameters via an acceptance-rejection method (robert2013monte).

The rest of this paper is organized as follows. We specify the Bayesian hierarchical models and discuss their posterior propriety in Section 2. In Section 3, we explain the inferential models used to estimate the model parameters. We describe the estimation procedures including ADM and the acceptance-rejection method in Section 4 and 5, respectively. We introduce frequency method checking techniques in Section 6. We explain the basic usages of \pkgRgbp’s main functions with three examples in Section 7, and specify the functions further with various options in Section LABEL:sec5.

2 Conjugate hierarchical modeling structure

Rgbp allows users to choose one of three hierarchical models according to the type of data, namely Normal-Normal, Poisson-Gamma, and Binomial-Beta models. Although there are more hierarchical models, we choose the three models because these are based on the most common types of data we may encounter in practice. Also, their conjugacy leads to linear posterior means simplifying computations.

Our parametrization of the three hierarchical models leads to an intuitive shrinkage interpretation in inference because the shrinkage factors under our parametrization are determined by the relative amount of information in the prior compared to the data (morris1983natural).

2.1 Normal-Normal model for Gaussian data

The following Normal-Normal hierarchical model (hereafter the Gaussian model) assumed by \pkgRgbp is useful when the group-level aggregate data from independent groups are continuous (or approximately continuous) variables with known standard errors. The subscript j below indicates the jth group among k groups in the dataset. For ,

| (1) | ||||

| (2) |

where is an observed unbiased estimate, e.g., sample mean, for random effect , is a completely known standard error of , is an expected random effect defined as , and is the number of unknown regression coefficients. It is assumed that the second-level variance is unknown and that the vector of regression coefficients is also unknown unless otherwise specified. If no covariates are available, but with an unknown intercept term, then () and thus for all , resulting in an exchangeable conjugate prior distribution for the random effects. Based on these conjugate prior distributions for random effects, it is easy to derive the conditional posterior distribution of each random effect. For ,

| (3) |

where is a shrinkage factor of group and . The conditional posterior mean , denoted by , is a convex combination of the observed sample mean and the expected random effect weighted by the shrinkage factor . If the variance of the conjugate prior distribution, , is smaller than the variance of the observed distribution, , then we expect the posterior mean to borrow more information from the second-level conjugate prior distribution.

2.2 Poisson-Gamma model for Poisson data

Rgbp can estimate a conjugate Poisson-Gamma hierarchical model (hereafter the Poisson model) when the group-level aggregate data from independent groups consist of non-negative count data without upper limit. However, its usage is limited to the case where the expected random effect, , is known (or equivalently all the regression coefficients are known ()); we may be able to obtain this information from the past studies or from experts. For ,

| (4) | ||||

| (5) |

where is the number of events happening, is the exposure of group , which is not necessarily an integer, is the known expected random effect (), and is the unknown second-level variance component. The mean and variance of this conjugate Gamma prior distribution are and , respectively111The density function of this Gamma prior distribution in (5) is . albert1988computational interprets as the amount of prior information as represents the amount of observed information because the uncertainty of the conjugate prior distribution increases as decreases and vice versa. The conditional posterior distribution of the random effect for this Poisson model is

| (6) |

where . The mean and variance of the conditional posterior distribution are

| (7) |

where is the shrinkage factor of group , the relative amount of information in the prior compared to the data. The conditional posterior mean is a convex combination of and weighted by . If the conjugate prior distribution contains more information than the observed data have, i.e., ensemble sample size exceeds individual sample size , then the posterior mean shrinks towards the prior mean by more than 50%.

The conditional posterior variance in (7) is linear in the conditional posterior mean, whereas a slightly different parameterization for a Poisson-Gamma model has been used elsewhere (morris1997) that makes the variances quadratic functions of means.

2.3 Binomial-Beta model for Binomial data

Rgbp can fit a conjugate Binomial-Beta hierarchical model (hereafter the Binomial model) when the group-level aggregate data from independent groups are composed of each group’s number of successes out of total number of trials. The expected random effect in the Binomial model is either known () or unknown (). For ,

| (8) | ||||

| (9) |

where is the number of successes out of trials, is the expected random effect of group defined as . The vector of the logistic regression coefficients and the second-level variance component are unknown. The mean and variance of the conjugate Beta prior distribution for group are and , respectively. The resultant conditional posterior distribution of random effect is

| (10) |

where is the observed proportion of group . The mean and variance of the conditional posterior distribution are

| (11) |

The conditional posterior mean is a convex combination of and weighted by like the Poisson model. If the conjugate prior distribution contains more information than the observed distribution does (), then the resulting conditional posterior mean borrows more information from the conjugate Beta prior distribution.

2.4 Hyper-prior distribution

Hyper-prior distributions are the distributions assigned to the second-level parameters called hyper-parameters. Our choices for the hyper-prior distributions are

| (12) |

The improper flat hyper-prior distribution on is a common non-informative choice. In the Gaussian case, the flat hyper-prior distribution on the second-level variance is known to produce good repeated sampling coverage properties of the Bayesian interval estimates for the random effects (tang2011; morris2012; kelly2014advances). The resulting full posterior distribution of the random effects and hyper-parameters is proper if (tang2011; kelly2014advances).

In the other two cases, Poisson and Binomial, the flat prior distribution on induces the same improper prior distribution on shrinkages () as does with the Uniform() for the Gaussian case. The Poisson model with this hyper-prior distribution on , i.e., , provides posterior propriety if there are at least two groups whose observed values are non-zero and the expected random effects, , are known (); see Appendix LABEL:propriety_poisson for its proof. If is unknown, \pkgRgbp cannot yet give reliable results because we have not verified posterior propriety. If the Poisson is being used as an approximation to the Binomial and the exposures are known integer values, then we recommend using the Binomial model with the same hyper-prior distributions.

As for posterior propriety of the Binomial model, let us define an interior group as the group whose number of successes are neither 0 nor , and as the number of interior groups among groups. The full posterior distribution of random effects and hyper-parameters is proper if and only if there are at least two interior groups in the data and the covariate matrix of the interior groups is of full rank () (tak2016propriety).

3 The inferential model

The likelihood function of hyper-parameters, and , for the Gaussian model is derived from the independent Normal distributions of the observed data with random effects integrated out.

| (13) |

The joint posterior density function of hyper-parameters for the Gaussian model is proportional to their likelihood function in (13) because we use flat improper hyper-prior density functions for and :

| (14) |

The likelihood function of for the Poisson model comes from the independent Negative-Binomial distributions of the observed data with the random effects integrated out.

| (15) |

where is a gamma function defined as for a positive constant . The posterior density function of for the Poisson model is the likelihood function in (15) times the hyper-prior density function of , i.e., :

| (16) |

The likelihood function of hyper-parameters and for the Binomial model is derived from the independent Beta-Binomial distributions of the observed data with random effects integrated out (skellam1948).

| (17) |

where the notation indicates a beta function for positive constants and . The joint posterior density function of hyper-parameters for the Binomial model is proportional to their likelihood function in (17) multiplied by the hyper-prior density functions of and based on distributions in (12):

| (18) |

Our goal is to obtain the point and interval estimates of the random effects from their joint unconditional posterior density which, for the Gaussian model, can be expressed as

| (19) |

where and the distributions in the integrand are given in (3) and (14). For the Poisson model, the joint unconditional posterior density for the random effects is

| (20) |

where and the distributions in the integrand are given in (6) and (16). For the Binomial model, the joint unconditional posterior density for the random effects is

| (21) |

where and the distributions in the integrand are given in (10) and (18).

4 Estimation via the adjustment for density maximization

We illustrate our estimation procedure which utilizes adjustment for density maximization (ADM, carl1988; morris1997; tang2011). ADM is a method to approximate a distribution by a member of Pearson family of distributions and obtain moment estimates via maximization. The ADM procedure for the Gaussian model adopted in \pkgRgbp is well documented in kelly2014advances and thus we describe the ADM procedure using the Poisson and Binomial model in this section.

4.1 Estimation for shrinkage factors and expected random effects

Our goal here is to estimate the unconditional posterior moments of the shrinkage factors and the expected random effects because they are used to estimate the unconditional posterior moments of the random effects.

4.1.1 Unconditional posterior moments of shrinkage factors

It is noted that the shrinkage factors are a function of , i.e., (or a function of for the Gaussian model). A common method of estimation of is to approximate the likelihood of with two derivatives and use a Delta method for an asymptotic Normal distribution of . This Normal approximation, however, is defined on whereas lies on the unit interval between 0 and 1, and hence in small sample sizes the Delta method can result in point estimates lying on the boundary of the parameter space, from which the restricted MLE procedure sometimes suffers (tang2011).

To continue with a maximization-based estimation procedure but to steer clear of aforementioned boundary issues we make use of ADM. The ADM approximates the distribution of the function of the parameter of interest by one of the Pearson family distributions using the first two derivatives as the Delta method does; the Delta method is a special case of the ADM based on the Normal distribution.

The ADM procedure specified in tang2011 assumes that the unconditional posterior distribution of a shrinkage factor follows a Beta distribution; for ,

| (22) |

The mean of Beta distribution is not the same as its mode . The ADM works on an adjusted posterior distribution so that the mode of is the same as the mean of the original Beta distribution. The assumed posterior mean and variance of the th shrinkage factor are

| (23) | ||||

| (24) |

The ADM estimates these mean and variance using the marginal posterior distribution of , . The marginal likelihood, , for the Binomial model is obtained via the Laplace approximation with a Lebesque measure on and that for the Poisson model is specified in (15).

Considering that (23) involves maximization and (24) involves calculating the second derivative of , we work on a logarithmic scale of , i.e., (or for the Gaussian model). This is because the distribution of is more symmetric than that of and is defined on a real line without any boundary issues. Because is proportional to the marginal posterior density as shown in tang2011, the posterior mean in (23) is estimated by

| (25) |

where is the mode of , i.e., .

To estimate the variance in (24), tang2011 introduced the invariant information defined as

This invariant information is the negative second-derivative of evaluated at the mode . Using the invariant information, we estimate the unconditional posterior variance of shrinkage factor in (24) by

| (27) |

We obtain the estimates of and , the two parameters of the Beta distribution in (22), by matching them to the estimated unconditional posterior mean and variance of specified in (25) and (27) as follows.

| (28) |

The moments of the Beta distribution are well defined as a function of and , i.e., for . Their estimates are

| (29) |

The ADM approximation to the shrinkage factors via Beta distributions is empirically proven to be more accurate than a Laplace approximation (carl1988; morris1997; tang2011; morris2012).

4.1.2 Unconditional posterior moments of expected random effects

We estimate the unconditional posterior moments of expected random effects using their relationship to the conditional posterior moments. For a non-negative constant , the unconditional posterior moments are

| (30) |

We approximate the unconditional posterior moments on the left hand side by the conditional posterior moments with inserted (kass1989approximate), i.e., by .

However, calculating conditional posterior moments of each expected random effect involves an intractable integration. For example, the first conditional posterior moment of is

| (31) |

Thus, we use another ADM, assuming the conditional posterior distribution of each expected random effect is a Beta distribution as follows.

| (32) |

where is a random variable following a Gamma distribution and independently has a Gamma( distribution. The representation in (32) is equivalent to , a ratio of two independent Gamma random variables. Its mean and variance are

| (33) | ||||

| (34) |

To estimate and , we assume that the conditional posterior distribution of given and follows a Normal distribution with mean and variance-covariance matrix , where is the mode of and is an inverse of the negative Hessian matrix at the mode. Thus, the posterior distribution of is also Normal with mean and variance .

Using the property of the log-Normal distribution for , we estimate the posterior mean and variance in (33) and (34) as

| (35) | ||||

| (36) |

We estimate the values of and by matching them to the estimated unconditional posterior mean and variance of in (35) and (36), that is,

| (37) |

Finally, we estimate the unconditional posterior moments of the expected random effects by

| (38) |

The ADM approximation to a log-Normal density via a F-distribution (represented by a ratio of two independent Gamma random variables) is known to be more accurate than the Laplace approximation (carl1988).

For the Gaussian model (tang2011), the conditional posterior distribution of given and is Normal whose mean and variance-covariance matrix are

| (39) |

respectively, where is a covariate matrix and is a diagonal matrix with the -th diagonal element equal to . Because given and is also Normally distributed, we easily obtain the conditional posterior moments of given and use them to estimate unconditional posterior moments of .

4.2 Estimation for random effects

We illustrate how we obtain approximate unconditional posterior distributions of random effects using the estimated unconditional posterior moments of shrinkage factors and those of expected random effects. It is intractable to derive analytically the unconditional posterior distribution of each random effect for the three models. Thus, we approximate the distributions by matching the estimated posterior moments with a skewed-Normal distribution (azzalini1985class) for the Gaussian model, a Gamma distribution for the Poisson model, and a Beta distribution for the Binomial model; for ,

| (40) | ||||

| (41) | ||||

| (42) |

where of the skewed-Normal distribution are location, scale, and skewness parameters, respectively.

morris2012 first noted that the unconditional posterior distribution of the random effect in a two-level conjugate Gaussian model might be skewed. kelly2014advances shows that the skewed-Normal approximation to the unconditional posterior distribution of the random effect is better than a Normal approximation () in terms of the repeated sampling coverage properties of random effects. kelly2014advances estimates the first three moments of the random effects by noting that is Normally distributed given and , and thus estimates the moments by using the ADM approximation of the shrinkage factors, , and the law of third cumulants (brill). The three estimated moments are then matched to the first three moments of the skewed-Normal distribution, i.e., , , and Skewness (azzalini1985class). The full derivation can be found in kelly2014advances.

The unconditional posterior mean and variance of random effect in the Poisson model are

| (43) | ||||

| (44) | ||||

| (45) | ||||

| (46) |

To estimate these, we insert the estimated unconditional posterior moments of shrinkage factors in (29) into both (43) and (46). Let and denote the estimated unconditional posterior mean and variance, respectively. The estimates of the two parameters and in (41) are

| (47) |

To estimate the unconditional posterior moments of random effects in the Binomial model, we assume that hyper-parameters and are independent a posteriori. With this assumption, the unconditional posterior mean and variance of random effect are

| (48) | ||||

| (49) | ||||

| (50) | ||||

| (51) | ||||

| (52) |

where the approximation in (51) is a first-order Taylor approximation. By inserting the estimated unconditional posterior moments of shrinkage factors in (29) and those of expected random effect in (38) into both (48) and (52), we obtain the estimates of the unconditional posterior mean and variance of each random effect, denoted by and , respectively. We thus obtain the estimates of two parameters and in (42) as follows.

| (53) |

Finally, the assumed unconditional posterior distribution of random effect for the Gaussian model is

| (54) |

that for the Poisson model is

| (55) |

and that for the Binomial model is

| (56) |

Our point and interval estimates of each random effect are the mean and (2.5%, 97.5%) quantiles (if we assign 95% confidence level) of the assumed unconditional posterior distribution in (54), (55), or (56).

For the Binomial model, \pkgRgbp provides a fully Bayesian approach for drawing posterior samples of random effects and hyper-parameters, which we illustrate in the next section.

5 The acceptance-rejection method for the Binomial model

In this section, we illustrate an option of \pkgRgbp that provides a way to draw posterior samples of random effects and hyper-parameters via the acceptance-rejection (A-R) method (robert2013monte) for the Binomial model. Unlike the approximate Bayesian machinery specified in the previous section, this method does not assume that hyper-parameters are independent a posteriori. The joint posterior density function of and based on their joint hyper-prior density function in (12) is

| (57) |

The A-R method is useful when it is difficult to sample a parameter of interest directly from its target probability density , which is known up to a normalizing constant, but an easy-to-sample envelope function is available. The A-R method samples from the envelope and accepts it with a probability , where is a constant making for all . The distribution of the accepted exactly follows . The A-R method is stable as long as the tails of the envelope function are thicker than those of the target density function.

The goal of the A-R method for the Binomial model is to draw posterior samples of hyper-parameters from (57), using an easy-to-sample envelope function that has thicker tails than the target density function.

We factor the envelope function into two parts, to model the tails of each function separately. We consider the tail behavior of the conditional posterior density function to establish ; behaves as when goes to and as when goes to . It indicates that is skewed to the left because the right tail touches the -axis faster than the left tail does as long as . A skewed -distribution is a good candidate for because it behaves as a power law on both tails, leading to thicker tails than those of .

It is too complicated to figure out the tail behaviors of . However, because in the Gaussian model (as an approximation) has a multivariate Gaussian density function (tang2011; kelly2014advances), we consider a multivariate -distribution with four degrees of freedom as a good candidate for .

Specifically, we assume

| (58) | |||||

| (59) |

where Skewed- represents a density function of a skewed -distribution of with location , scale , degree of freedom , and skewness for any positive constants and (jones2003skew). jones2003skew derive the mode of as

| (60) |

and provide a representation to generate random variables that follows Skewed-;

| (61) |

They also show that the tails of the skewed- density function follow a power law with on the left and on the right when .

The notation in (59) indicates a density function of a multivariate -distribution of with four degrees of freedom, a location vector , and a scale matrix that leads to the variance-covariance matrix .

Rgbp determines the parameters of and , i.e., , , , , , and , to make the product of and similar to the target joint posterior density . First, \pkgRgbp obtains the mode of , , and the inverse of the negative Hessian matrix at the mode. We define to indicate the (1, 1) element of the negative Hessian matrix and to represent the negative Hessian matrix without the first row and the first column.

For , \pkgRgbp sets () to if is less than 10 (or to otherwise) for a left-skewness and these small values of and lead to thick tails. \pkgRgbp matches the mode of specified in (60) to by setting the location parameter to . \pkgRgbp sets the scale parameter to , where is a tuning parameter; when the A-R method produces extreme weights defined in (62) below, we need enlarge the value of .

For , \pkgRgbp sets the location vector to the mode and the scale matrix to so that the variance-covariance matrix becomes .

For implementation of the acceptance-rejection method, \pkgRgbp draws four times more trial samples than the desired number of samples, denoted by , independently from and . \pkgRgbp calculates weights, each of which is defined as

| (62) |

Rgbp accepts each pair of with a probability where is set to the maximum of all the weights. When \pkgRgbp accepts more than pairs, it discards the redundant. If \pkgRgbp accepts less than pairs, then it additionally draws (six times the shortage) pairs and calculates a new maximum from all the previous and new weights; \pkgRgbp accepts or rejects the entire pairs again with new probabilities , .

6 Frequency method checking

The question as to whether the interval estimates of random effects for given confidence level obtained by a specific model achieve the nominal coverage rate for any true parameter values is one of the key model evaluation criteria. Unlike standard model checking methods that test whether a two-level model is appropriate for data (dean1992testing; modelchecking1996), frequency method checking is a procedure to evaluate the coverage properties of the model. Conditioning that the two-level model is appropriate, the frequency method checking generates pseudo-data sets given specific values of hyper-parameters and estimates unknown coverage probabilities based on these mock data sets (a parametric bootstrapping). We describe the frequency method checking based on the Gaussian model because the idea can be easily applied to the other two models.

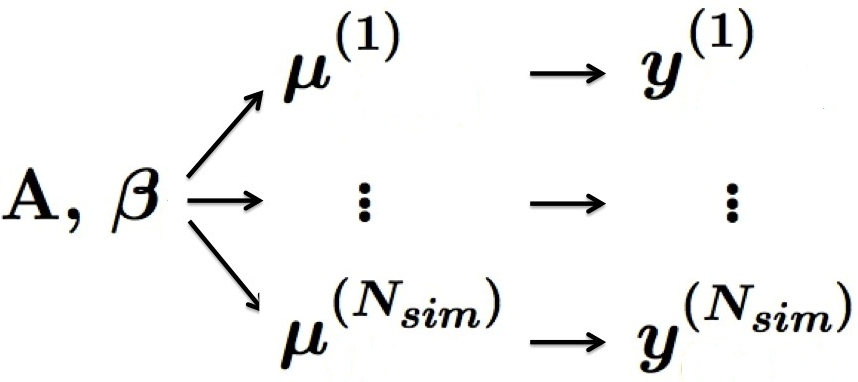

6.1 Pseudo-data generation

Figure 1 displays the process of generating pseudo-data sets. It is noted that the conjugate prior distribution of each random effect in (2) is completely determined by two hyper-parameters, and . Fixing these hyper-parameters at specific values, we generate sets of random effects from the conjugate prior distribution, i.e., {, where the superscript indicates the -th simulation. Next, using the distribution of observed data in (1), we generate sets of observed data sets given each .

6.2 Coverage probability estimation

After fitting the Gaussian model for each simulated data set, we obtain interval estimates of the random effects . Let represent the lower and upper bounds of the interval estimate of random effect based on the -th simulation given a specific confidence level. We define the coverage indicator of random effect on the -th mock data set as

| (63) |

This shrinkage indicator is equal to the value one if the random effect in simulation is between its interval estimates and zero otherwise.

6.2.1 Simple unbiased coverage estimator.

When the confidence level is 95%, the proportion of 95% interval estimates that contain random effect is an intuitive choice for the coverage rate estimator for random effect . This estimator implicitly assumes that there exist unknown coverage probabilities of random effects, denoted by for , depending on the values of the hyper-parameters that generate random effects and mock data sets. The coverage indicators for random effect in (63) is assumed to follow an independent and identically distributed Bernoulli distribution given the unknown coverage rate . The sample mean of these coverage indicators is a simple unbiased coverage estimator for ; for ,

| (64) |

The unbiased variance estimator of is, for ,

| (65) |

6.2.2 Rao-Blackwellized unbiased coverage estimator.

Frequency method checking is computationally expensive in nature because it fits a model on every mock data set. The situation deteriorates if the number of simulations or the size of data is large, or the estimation method is computationally demanding. morris1997 and tang2002fitting use a Rao-Blackwellized (RB) unbiased coverage estimator for the unknown coverage rate of each random effect, which is more efficient than the simple unbiased coverage estimator. For ,

| (66) |

where the sample mean of the interior conditional expectations in (66) is the RB unbiased coverage estimator. Specifically,

| (67) | ||||

| (68) |

We can easily compute the conditional posterior probabilities in (68) using the cumulative density function of the Gaussian conditional posterior distribution of each random effect in (3). The variance of does not exceed the variance of a simple unbiased coverage estimator, (radhakrishna1945information; blackwell1947conditional).

If one dataset is simulated for each set of random effects , the variance estimator below is an unbiased estimator of . For

| (69) |

6.2.3 Overall unbiased coverage estimator

To summarize the frequency method checking, we report the overall unbiased coverage estimate and its variance estimate,

| (70) |

7 Examples

In this section, we demonstrate how \pkgRgbp can be used to analyze three realistic data sets: Medical profiling of 31 hospitals with Poisson distributed fatality counts; educational assessment of eight schools with Normally distributed data; and evaluation of 18 baseball hitters with Binomial success rates and one covariate. For each example, we construct 95% confidence intervals. Additional usages and options of the functions in \pkgRgbp can be found in Section LABEL:sec5.

7.1 Poisson data with 31 hospitals: Known expected random effect

We analyze a data set of 31 hospitals in New York State consisting of the outcomes of the coronary artery bypass graft (CABG) surgery (morris2012). The data set contains the number of deaths, , for a specified period after CABG surgeries out of the total number of patients, , receiving CABG surgeries in each hospital. A goal would be to obtain the point and interval estimates for the unknown true fatality rates (random effects) of 31 hospitals to evaluate each hospital’s reliability on the CABG surgery (morris1995 use a similar Poisson model to handle these hospital profile data). We interpret the caseloads, , as exposures and assume that the state-level fatality rate per exposure of this surgery is known, ().

The following code can be used to load these data into \proglangR. {CodeChunk} {CodeInput} R> library("Rgbp") R> data("hospital") R> y <- hospitaln

The function \codegbp can then be used to fit a Poisson-Gamma to the fatality rates in New York States with the expected random effect, , equal to 0.03.

R> p.output <- gbp(y, n, mean.PriorDist = 0.03, model = "poisson") R> p.output {CodeOutput} Summary for each unit (sorted by n):

obs.mean n prior.mean shrinkage low.intv post.mean upp.intv post.sd 1 0.0448 67 0.03 0.911 0.0199 0.0313 0.0454 0.00653 2 0.0294 68 0.03 0.910 0.0189 0.0299 0.0435 0.00631 3 0.0238 210 0.03 0.765 0.0185 0.0285 0.0407 0.00566 4 0.0430 256 0.03 0.728 0.0225 0.0335 0.0467 0.00619 5 0.0335 269 0.03 0.718 0.0208 0.0310 0.0432 0.00573 6 0.0438 274 0.03 0.714 0.0229 0.0339 0.0472 0.00621 7 0.0432 278 0.03 0.711 0.0228 0.0338 0.0469 0.00617 8 0.0136 295 0.03 0.699 0.0157 0.0250 0.0366 0.00534 9 0.0288 347 0.03 0.663 0.0200 0.0296 0.0410 0.00536 10 0.0372 349 0.03 0.662 0.0222 0.0325 0.0446 0.00571 11 0.0391 358 0.03 0.656 0.0228 0.0331 0.0454 0.00579 12 0.0177 396 0.03 0.633 0.0165 0.0255 0.0363 0.00506 13 0.0278 431 0.03 0.613 0.0200 0.0292 0.0400 0.00511 14 0.0249 441 0.03 0.608 0.0191 0.0280 0.0387 0.00502 15 0.0273 477 0.03 0.589 0.0199 0.0289 0.0394 0.00499 16 0.0455 484 0.03 0.585 0.0256 0.0364 0.0491 0.00601 17 0.0304 494 0.03 0.580 0.0211 0.0302 0.0409 0.00506 18 0.0220 501 0.03 0.577 0.0180 0.0266 0.0369 0.00483 19 0.0277 505 0.03 0.575 0.0202 0.0290 0.0395 0.00494 20 0.0204 540 0.03 0.559 0.0173 0.0258 0.0358 0.00474 21 0.0284 563 0.03 0.548 0.0206 0.0293 0.0395 0.00485 22 0.0236 593 0.03 0.535 0.0187 0.0270 0.0369 0.00466 23 0.0150 602 0.03 0.532 0.0147 0.0230 0.0329 0.00466 24 0.0238 629 0.03 0.521 0.0188 0.0271 0.0368 0.00460 25 0.0204 636 0.03 0.518 0.0173 0.0254 0.0351 0.00455 26 0.0480 729 0.03 0.484 0.0286 0.0393 0.0516 0.00587 27 0.0306 849 0.03 0.446 0.0223 0.0303 0.0397 0.00445 28 0.0274 914 0.03 0.428 0.0208 0.0285 0.0374 0.00423 29 0.0213 940 0.03 0.421 0.0176 0.0249 0.0335 0.00407 30 0.0293 1193 0.03 0.364 0.0223 0.0296 0.0379 0.00397 31 0.0201 1340 0.03 0.338 0.0170 0.0235 0.0310 0.00360 Mean 517 0.03 0.600 0.0201 0.0293 0.0403 0.00517

The output contains information about (from the left) the observed fatality rates , caseloads , known expected random effect , shrinkage estimates , lower bounds (2.5%) of posterior interval estimates , posterior means , upper bounds (97.5%) of posterior interval estimates , and posterior standard deviations for random effects based on the assumed unconditional Gamma posterior distributions in (55).

A function \codesummary shows selective information about hospitals with minimum, median, and maximum exposures and the estimation result of the hyper-parameter . {CodeChunk} {CodeInput} R> summary(p.output) {CodeOutput} Main summary:

obs.mean n prior.mean shrinkage low.intv post.mean Unit with min(n) 0.0448 67 0.03 0.911 0.0199 0.0313 Unit with median(n) 0.0455 484 0.03 0.585 0.0256 0.0364 Unit with max(n) 0.0201 1340 0.03 0.338 0.0170 0.0235 Overall Mean 517 0.03 0.600 0.0201 0.0293

upp.intv post.sd 0.0454 0.00653 0.0491 0.00601 0.0310 0.00360 0.0403 0.00517

Second-level Variance Component Estimation Summary: alpha=log(A) for Gaussian or alpha=log(1/r) for Binomial and Poisson data:

post.mode.alpha post.sd.alpha post.mode.r -6.53 0.576 684 The output of \codesummary shows that , which is an indicator of how valuable and informative the second-level hierarchy is. It means that the 25 hospitals with caseload less than 684 patients shrink their sample means towards the prior mean (0.03) more than 50%. For example, the shrinkage estimate of the first hospital () was calculated by 684 / (684 + 67), where 67 is its caseload (). As for this hospital, using more information from the conjugate prior distribution is an appropriate choice because the amount of observed information (67) is much less than the amount of state-level information (684).

To obtain a graphical summary, we use the function \codeplot.

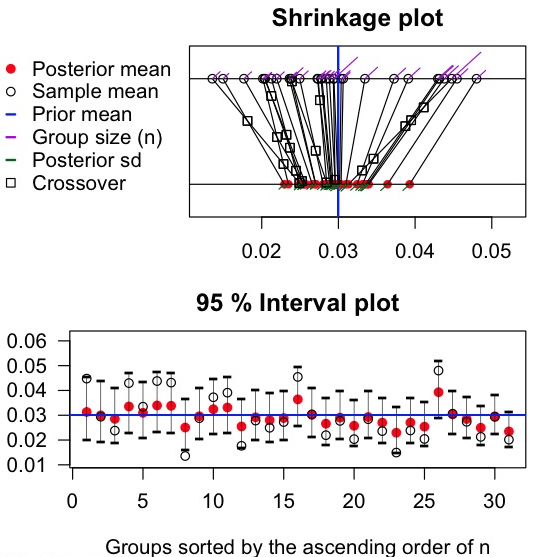

R> plot(p.output)

The shrinkage plot (1975; morris2012) in the first panel of Figure 2 shows the regression towards the mean; the observed fatality rates, denoted by empty dots on the upper horizontal line, are shrinking towards the known expected random effect, denoted by a blue vertical line at 0.03, to the different extents. The red dots on the bottom line denotes the estimated posterior means. Some hospitals’ ranks have changed by shrinking more sharply towards 0.03 than the others. For example, an empty square at the crossing point of the two left-most lines (8th and 23rd hospitals on the list above) indicates that the seemingly safest hospital in terms of the observed mortality rate is probably not the safest in terms of the estimated posterior mean accounting for the different caseloads of these two hospitals.

To be specific, their observed fatality rates (, ) are 0.0136 and 0.0150 and caseloads (, ) are 295 and 602, respectively. Considering solely the observed fatality rates may lead to an unfair comparison because the latter hospital handled twice the caseload. \pkgRgbp accounts for this caseload difference, making the posterior mean for the random effect of the former hospital shrink toward the state-level mean (=0.03) more rapidly than that for the latter hospital.

The point estimates are not enough to evaluate hospital reliability because one hospital may have a lower point estimate but larger uncertainty (variance) than the other. The second plot of Figure 2 displays the 95% interval estimates. Each posterior mean (red dot) is between the sample mean (empty dot) and the known expected random effect (a blue horizontal line).

This 95% interval plot reveals that the 31st hospital has the lowest upper bound even though its point estimate () is slightly larger than that of the 23rd hospital (). The observed mortality rates for these two hospitals () are 0.0150 and 0.0201 and the caseloads () are 602 and 1340 each. The 31st hospital has twice the caseload, which leads to borrowing less information from the New York State-level hierarchy (or shrinking less toward the state-level mean, 0.03) with smaller variance. Based on the point and interval estimates, the 31st hospital seems a better choice than the 23rd hospital. (Note that this conclusion is based on the data, assuming no covariate information about the overall case difficulties in each hospital. A more reliable analysis must take into account all the possible covariate information and instead of our Poisson model, we recommend using our Binomial model to account for covariate information.)

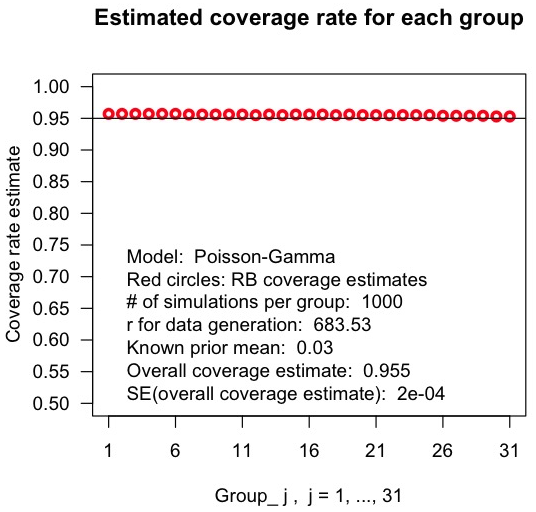

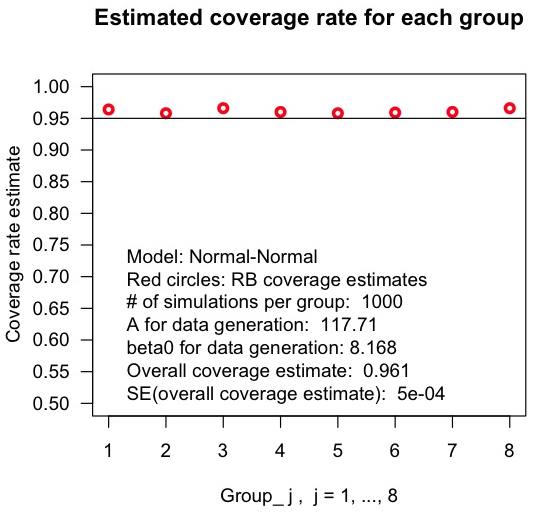

Next, we perform frequency method checking to question how reliable the estimation procedure is, assuming equals its estimated value, . The function \codecoverage generates synthetic data sets starting with the estimated value of as a generative value. For reference, we could designate other generative values of and by adding two arguments, \codeA.or.r and \codemean.PriorDist, into the code below, see Section LABEL:code_model for details.

R> p.coverage <- coverage(p.output, nsim = 1000)

In Figure 3, the black horizontal line at 0.95 represents the nominal confidence level and the red circles indicate RB unbiased coverage estimates, for . The overall unbiased coverage estimate across all the hospitals, in (70), is 0.955. None of RB unbiased coverage estimates for the 31 hospitals are less than 0.95 regardless of their caseloads, which range from 67 for hospital 1 to 1,340 for hospital 31. This result shows that the interval estimates for this particular dataset adequately achieves a 95% confidence level if .

The following code provides 31 RB unbiased coverage estimates and their standard errors (the output is omitted for space reasons). {CodeChunk} {CodeInput} R> p.coveragese.coverageRB

The code below produces 31 simple unbiased coverage estimates and their standard errors. {CodeChunk} {CodeInput} R> p.coveragese.coverageS

It turns out that the variance estimate of the RB unbiased coverage estimate for the first hospital () is about 19 times smaller than that of the simple one (). It means that the RB unbiased coverage estimates based on 1,000 simulations () are as precise as the simple unbiased coverage estimates based on 19,000 simulations in terms of estimating the coverage probability for the first hospital, .

7.2 Gaussian data with eight schools: Unknown expected random effect and no covariates

The Education Testing Service conducted randomized experiments in eight separate schools (groups) to test whether students (units) SAT scores are affected by coaching. The dataset contains the estimated coaching effects on SAT scores () and standard errors () of the eight schools (1981). These data are contained in the package and can be loaded into \proglangR as follows. {CodeChunk} {CodeInput} R> library("Rgbp") R> data("schools") R> y <- schoolsse

Due to the nature of the test each school’s coaching effect has an approximately Normal sampling distribution with approximately known sampling variances, based on large sample consideration. At the second hierarchy, the mean for each school is assumed to be drawn from a common Normal distribution ().

R> g.output <- gbp(y, se, model = "gaussian") R> g.output {CodeOutput} Summary for each group (sorted by the descending order of se):

obs.mean se prior.mean shrinkage low.intv post.mean upp.intv post.sd 8 12.00 18.0 8.17 0.734 -10.21 9.19 29.9 10.23 3 -3.00 16.0 8.17 0.685 -17.13 4.65 22.5 10.10 1 28.00 15.0 8.17 0.657 -2.32 14.98 38.8 10.56 4 7.00 11.0 8.17 0.507 -8.78 7.59 23.6 8.26 6 1.00 11.0 8.17 0.507 -13.03 4.63 20.1 8.44 2 8.00 10.0 8.17 0.459 -7.25 8.08 23.4 7.81 7 18.00 10.0 8.17 0.459 -1.29 13.48 30.8 8.18 5 -1.00 9.0 8.17 0.408 -13.30 2.74 16.7 7.63 Mean 12.5 8.17 0.552 -9.16 8.17 25.7 8.90 This output from \codegbp summarizes the results. In this Gaussian model the amount of shrinkage for each unit is governed by the shrinkage factor, . As such, schools whose variation within the school () is less than the between-school variation () will shrink greater than . The results provided by \codegpb suggests that there is little evidence that the training provided much added benefit due to the fact that every school’s posterior interval contains zero. In the case where the number of groups is large \pkgRgbp provides a summary feature:

R> summary(g.output) {CodeOutput} Main summary:

obs.mean se prior.mean shrinkage low.intv post.mean Unit with min(se) -1.00 9.0 8.17 0.408 -13.30 2.74 Unit with median(se)1 1.00 11.0 8.17 0.507 -13.03 4.63 Unit with median(se)2 7.00 11.0 8.17 0.507 -8.78 7.59 Unit with max(se) 12.00 18.0 8.17 0.734 -10.21 9.19 Overall Mean 12.5 8.17 0.552 -9.16 8.17

upp.intv post.sd 16.7 7.63 20.1 8.44 23.6 8.26 29.9 10.23 25.7 8.90

Second-level Variance Component Estimation Summary: alpha=log(A) for Gaussian or alpha=log(1/r) for Binomial and Poisson data:

post.mode.alpha post.sd.alpha post.mode.A 4.77 1.14 118

Regression Summary:

estimate se z.val p.val beta1 8.168 5.73 1.425 0.154 The summary provides results regarding the second level hierarchy parameters. It can be seen that the estimate of the expected random effect, (\codebeta1), is not significantly different from zero suggesting that there is no effect of the coaching program on SAT math scores.

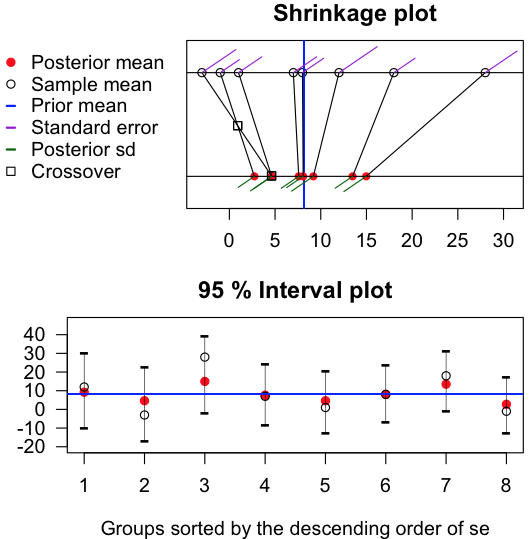

Rgbp also provides functionality to plot the results of the analysis as seen in Figure 4. Plotting the results provides a visual aid to understanding but is only largely beneficial when the number of groups is small.

R> plot(g.output)

The frequency method checking generates new pseudo-data from our assumed model. Unless otherwise specified, the procedure fixes the hyper-parameter values at their estimates ( and in this example) and then simulates random effects for each group . The model is then estimated and this is repeated an (\codensim) number of times to estimate the coverage probabilities of the procedure.

R> g.coverage <- coverage(g.output, nsim = 1000)

As seen in Figure 5 the desired confidence level, denoted by a black horizontal line at 0.95, is achieved for each school in this example. All the coverage estimates depend on the chosen generative values of and , and the assumption that the model is valid.

In addition, RB unbiased coverage estimate and its standard error for each school can be calculated with the command below. {CodeChunk} {CodeInput} R> g.coverage

7.3 Binomial data with 18 baseball players: Unknown expected random effects and one covariate

The data of 18 major league baseball players contain the batting averages through their first 45 official at-bats of the 1970 season (1975). A binary covariate is created that is equal to the value one if a player is an outfielder and zero otherwise. The data can be loaded into \proglangR with the following code. {CodeChunk} {CodeInput} R> library("Rgbp") R> data("baseball") R> y <- baseballAt.Bats R> x <- ifelse(basebally_j∣p_j∼Binomial(45, p_j)j=1, …, 18p^β_2^β_2exp(0.389)=1.48