Stoch. Control and Differ. Games with Path-Depend. of ControlsY. F. Saporito

Stochastic Control and Differential Games with Path-Dependent Influence of Controls on Dynamics and Running Cost

Abstract

In this paper we consider the functional Itô calculus framework to find a path-dependent version of the Hamilton-Jacobi-Bellman equation for stochastic control problems that feature dynamics and running cost that depend on the path of the control. We also prove a Dynamic Programming Principle for such problems. We apply our results to path-dependence of the delay type. We further study Stochastic Differential Games in this context.

keywords:

Functional Itô Calculus, Path-dependence, Stochastic Control, Stochastic Games, Delay.49L99, 91A15, 60H30

1 Introduction

Stochastic control problems and differential games appear naturally in various areas of applications. Portfolio allocation, investment-consumption utility maximization, hedging in incomplete markets and real options are some important examples in Finance and Economics. See, for instance, Pham (2009) and Carmona (2016). The standard case deals with a controlled diffusion

and a cost functional

where is a admissible control and and are suitable functions. The quantity of interest here is the value function:

where is the set of admissible controls.

Two very important results on Stochastic Control are the Dynamic Programming Principle (DPP) and the Verification Theorem for the related Hamilton-Jacobi-Bellman (HJB) equation. The main contribution of our paper is to extend the DPP and the HJB to stochastic control problems that feature dynamics and running cost that depend on the path of the control . The main example to have in mind is the following delayed-control diffusion

| (1) |

for a non-random, fixed . In this case, we say the control problem exhibits path-dependence in the control. This is not to be confused with the Closed-Loop Perfect State (CLPS) controls, which means that the control is progressively-measurable with respect to the filtration generated by the process .

Stochastic control has been already extended to consider path-dependence of dynamics and running cost with respect to the state variable , see, for example, Fournié (2010), Xu (2013) and Ji et al. (2015). We say the control problem in this case exihbits path-depndence in the state variable. Functional Itô calculus was also applied to the stochastic control problem of portfolio optimization with bounded memory in Pang and Hussain (2015). Furthermore, the theory was applied to zero-sum stochastic differential games in Pham and Zhang (2014). However, these references do not deal with path-dependent influence of the control, only path-dependence in the state of the system. This generalization is fundamentally different from the one pursued in our paper, which will become clear in the sections to follow, see Remark 2.8.

General path-dependent effect of the control in the dynamics and the running cost are still incipient in theory and applications of stochastic control and differential games. This is very likely related to the lack of theoretical tools to deal with such objects in an appropriate way. We hope this work will provide a useful framework.

For example, in Gozzi and Marinelli (2006) and Gozzi and Masiero (2017a, b), the authors considered a class of problems that exhibit a particular type of path-dependence in the control, namely delayed controls. The method implemented there is a classical infinite-dimensional analysis and they derived an infinite-dimensional HJB equation. However, their method is strongly related to the delay-type of path-dependence. Additionally, we forward the reader to the following articles Huang et al. (2012); Chen and Wu (2011); Alekal et al. (1971). These results were recently applied to stochastic games in Carmona et al. (2016).

Our approach uses the functional Itô calculus framework, introduced by Bruno Dupire in the seminal paper Dupire (2009), which allows us to consider more general path-dependent structures. Although our method could be also seen as an infinite-dimensional analysis, it is rather different than the one applied in Gozzi and Marinelli (2006) and Gozzi and Masiero (2017a, b). Our method delivers an HJB equation that can be applied to virtually any path-dependent structure in the control and it could be formulated in the deterministic case as well. Our assumptions are mainly related to the well-posedness of the optimal control problem (smoothness, measurability and integrability). Additionally, our method could be applied to delay of the type of Equation (1) with no additional difficulty, which is not the case of the method derived in the aforesaid references. See Section 2.2.1 for more details.

The structure of the paper is as follows. We finish this introduction with the main definitions and results of functional Itô calculus. In Section 2.1, we introduce the problem we are considering and derive the main results of our work: the DPP in Theorem 2.2 and the Verification Theorem for the path-dependent HJB equation in Theorem 2.5. An example is analyzed in Section 2.2.1. Additionally, in Section 2.3, we briefly study stochastic differential games with path-dependence effects of the control in the dynamics and running cost.

1.1 A Crash Course in Functional Itô Calculus

The important notions of the functional Itô calculus framework will be introduced in this section. For more details and results, we forward the reader to Dupire (2009); Cont and Fournié (2010).

We start by fixing a time horizon . Denote the space of càdlàg paths in taking values in and define and . Elements of are two paths taking values in and , respectively, with the same time interval as domain. When it is not necessary to distinguish the dimensions of these spaces, we will use the notation .

Moreover, when considering examples with delay, one could consider , where is the largest possible value for the delay. In the examples studied here, we will assume that any path at negative time is zero. This does not increase the difficulty in our calculations and could be easily relaxed.

Capital letters will denote elements of (i.e. paths) and lower-case letters will denote spot value of paths. In symbols, means and , for .

A functional is any function . For such objects, we define, when the limits exist, the time and space functional derivatives, respectively, as

| (2) | ||||

| (3) |

where

see Figures 2 and 2. In the case when the path lies in a multidimensional space, the path deformations above are understood as follows: the flat extension is applied to all dimension jointly and equally and the bump is applied to each dimension individually.

We consider here continuity of functionals as the usual continuity in metric spaces with respect to the metric:

where, without loss of generality, we are assuming , and

The norm is the usual Euclidean norm in the appropriate Euclidian space, depending on the dimension of the path being considered. This continuity notion could be relaxed, see, for instance, Oberhauser (2016).

Moreover, we say a functional is boundedness-preserving if, for every compact set , there exists a constant such that , for every path satisfying .

A functional is said to belong to if it is -continuous, boundedness-preserving and it has -continuous, boundedness-preserving derivatives , and . Here, clearly, .

The Itô formula can be generalized to this framework. The proof can be found in Dupire (2009). We start by fixing a probability space .

Theorem 1.1 (Functional Itô Formula; Dupire (2009)).

Let be a continuous semimartingale and . Then, for any ,

2 Main results

2.1 Stochastic Control with Path-Dependent Controls

We suggest the reader to always keep in mind this example:

Consider a -dimensional Brownian motion on and a filtration in this space, satisfying the usual conditions, to which the Brownian motion is adapted. One could assume that is the augmented natural filtration of . The set of admissible controls , or just , is the space of -progressively measurable, càdlàg processes in taking value in some subset . Additional restrictions on will be assumed.

We will consider the following path-dependent controlled diffusion dynamics for :

| (7) |

where , i.e. the path of the control up to time , and , with denoting the space of matrices. Notice that we are allowing for path-dependence of and on the state system, , and on the control, .

To guarantee existence and uniqueness of strong solutions, we assume there exists a constant such that

for all , . These assumptions could be weaken, but it is outside the scope of this work.

Moreover, we consider the following class of cost functionals :

| (8) |

where and satisfy certain measurability and integrability conditions. Notice that . We additionally assume that the admissible controls in satisfy straightforward integrability conditions depending on the functionals , and so that Equations (7) and (8) are well-defined.

We will use the following notation:

| (12) |

The path is equal up to time (excluding it) and then follows the control . Notice that, for any and , the control is admissible.

We then define the value functional :

Remark 2.1 (Càdlàg Controls).

The framework we are considering requires the additional assumption that the control is càdlàg, as it was stated above in the definition of . This is inherent of the functional Itô calculus theory and it allows us to use this technique to analyze these complex stochastic control problems we are considering here. From an application point-of-view, this restriction is not very strong as one would usually restrict even further the space of admissible controls. Although outside the scope of this paper, one could analyze whether the value function considered here is the same as the one for the more general class of progressively-measurable controls.

We now state and prove the Dynamic Programming Principle for the control problem being considering.

Theorem 2.2 (Dynamic Programming Principle (DPP)).

For any ,

Proof 2.3.

The proof follows the same steps as in the path-independent case, since all the coefficients are still adapted. We follow the structure of the proof in Pham (2009).

Firstly, notice that, for any and , we have the following equivalence of paths

Then,

and conditioning on the path , we find

| (13) |

From this and choosing the control to be , it is clear that

Taking the infimum with respect to , we find

To prove the opposite inequality, fix and . Then, for any , there exists such that

It can be shown by the Measurable Selection Theorem (see, for example, Soner and Touzi (2002)) that belongs to (i.e. it is progressively measurable). Since , by Equation (13), and , we find

which implies, by the fact and are arbitrary, that

from where the final result follows.

2.2 The Path-Dependent Hamilton-Jacobi-Bellman Equation

In this section we will state the HJB equation related to our control problem and also prove a verification theorem for such equation. In the framework of the functional Itô calculus, this type of equation is called path-dependent Partial Differential Equation, PPDE. See for example, Ekren et al. (2016a, b, 2014).

We start by defining the Hamiltonian :

and the modified Hamiltonian :

| (14) |

The symbol denotes the space of functionals and is the space of symmetric matrices. Notice that is changing the last value of the control to .

The notation and mean

where and .

As we will conclude, the HJB equation in this case is given by the following PPDE:

| (18) |

for any .

Here, the time derivative is with respect to both variable and :

and the space derivative is with respect to :

In a less compact notation, we could write the path-dependent HJB equation (18) as

Remark 2.4.

This remark will be the cornerstone of the proof of the Verification Theorem presented below. Notice that , by the definition of the operator given in (12). Denoting the functional derivatives with respect to the control by , we conclude , and . Hence, the dynamics of the control will not impact the computations in the proof of the following theorem. This is similar to what Cont and Fournié (2010) assumed in order to consider functionals depending on the quadratic variation. These authors called such property predictability.

Moreover, if a smooth functional is predictable in a variable, then any space functional derivative will be predictable in that variable. However, the time functional derivative might not be predictable, in general. For example, the running integral functional is predictable, but is not.

Theorem 2.5 (Verification Theorem).

Suppose solves the HJB equation (18). Under mild integrability conditions,

for any . Moreover, if there exists such that, for any ,

| (19) | ||||

then . All the functional derivatives in (19) are computed at .

Proof 2.6.

Let us apply the Functional Itô Formula, Theorem 1.1, to , for fixed . Notice that the path is frozen and that we are considering the control , which means we follow the path as the control up to time (excluding it) and then from to . Moreover, since the functional derivatives of with respect to the control are zero, it is not required to consider the dynamics of the control , see Remark 2.4. Furthermore, the time derivative is with respect to both variables. In the computation that follows we suppress the superscript of for a cleaner exposition:

Under integrability conditions and applying localization techniques, we might assume, without loss of generality, that the Itô integral above is a martingale. Therefore, taking expectation on both sides, we conclude:

Remark 2.7.

We will see an interesting application of the Verification Theorem above in Section 2.2.1, where we study the case of control with delay.

Remark 2.8.

We would like to stress the difference between the case where the stochastic control problem exhibits a path-dependent effect of control and state variables, which we are dealing with in this paper, and the case where there is only path-dependent effect of state variables. In this case, it is not necessary to consider as variable of the path of the control, . It is enough to define

where is the space of admissible controls on . The HJB equation in this becomes

See, for example, Fournié (2010), Xu (2013) or Ji et al. (2015).

Remark 2.9.

It is obvious that if the dynamics of and the functionals and are path-independent in the state variable and control, we find the classical HJB equation. Moreover, if the path-dependence is only in the control, meaning that, for ,

the path-dependent HJB Equation (18) becomes

| (23) |

where is the usual derivative with respect to the state variable and

It is worth noticing that is still a functional derivative. More precisely,

2.2.1 Delayed Control

We will exemplify the results derived in the section above, mainly the path-dependent HJB equation, by considering the delay type of path-dependence in the control as in Gozzi and Marinelli (2006), see also Gozzi and Masiero (2017a, b); Huang et al. (2012); Chen and Wu (2011); Alekal et al. (1971). Namely, we will assume that the drift and the volatility are given by

where or, the more complicated case, dealt in Gozzi and Masiero (2017a, b), where is a measure. A very important example being the Dirac mass at , denoted by . In the measure case, we assume, without loss of generality, there is no Dirac mass at 0. As we will see below, differently than the aforesaid references, the framework proposed here can deal with both these situations without additional difficulty.

The Hamiltonian becomes

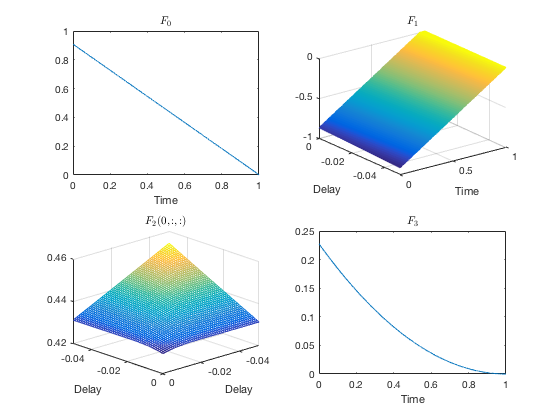

In order to get a complete characterization of the value functional (up to computing the solution of a system of PDEs), we consider the following linear-quadratic example:

Hence

Remark 2.10.

Notice that even though is not a smooth functional (since the delayed functional is not time functional differentiable), one would expect (as it is the case) that the value function is indeed smooth in the functional sense. The idea behind this fact is that the spot delayed dependence of generates a continuum delayed dependence on the value function, see Equation (24) below.

We consider the following ansatz for the value functional, as it was examined, for instance, in Huang et al. (2012):

| (24) | ||||

where we assume that is symmetric in the last two variables as it is usually done in these problems:

We can compute the derivatives of explicitly and see that . The time functional derivative would be more complicated, but for this ansatz, it may be verified that it is equivalent to taking derivative with respect to :

| (25) | |||

| (26) | |||

| (27) | |||

Combining all derivatives into the modified Hamiltonian (14), we find that the terms that depend on the current control are:

| (28) |

The infimum is then attained at

and the minimum value of the expression (28) is given by . The HJB equation in this example becomes:

| (34) |

Notice that removes the terms that depend on in Equation (27). Additionally, the optimal control is given by

Therefore, we find that, for any and ,

| (38) | ||||

| (45) | ||||

| (53) | ||||

| (57) |

In Figure 3, we show the numerical solution of the PDE system above for the following parameters: , , , , and .

2.3 Stochastic Differential Games

In this section, we will briefly analyze Stochastic Differential Games. Firstly, we present the general theory relating the game value function and a version of the HJB equation when there is path-dependence in the control. Then, we exemplify the theory using the delayed stochastic differential game proposed in Carmona et al. (2016).

Consider agents indexed by . These agents will act on a system whose state is described below:

where , , is a -dimensional standard Brownian motion, with being the -dimensional control chosen by agent taking values in . Moreover,

with . The set of admissible controls of agent is denoted by and . The agent chooses its own control to minimize its own cost functional:

where and are his/hers terminal and running costs. We will define now the concept of equilibrium we will consider. The following notation will be used: for any : and .

Definition 2.11 (Nash Equilibrium).

An admissible strategy is called a Nash equilibrium if, for any and , we have

Moreover, the Nash equilibrium can be further classified as

-

•

Open Loop: ;

-

•

Closed Loop: ,

for some functional . See Carmona (2016).

In what follows, since we will use the HJB approach, we will be seeking a closed-loop Nash equilibrium.

Assuming that the other agents have already optimized their actions, denoted by , the value functional for agent will be then given by

The DPP in this case (see Theorem 2.2) becomes

Furthermore, under the assumptions of Theorem 2.5, we have a verification theorem for the following HJB Equation

where

Notice that changes the control at time to .

2.3.1 Delayed Games

We will now study the model introduced in Carmona et al. (2016), where the authors proposes a stochastic differential game with delay in the control to analyze the systemic risk within a bank system.

Fix , and

where and is the identity matrix in . Let us consider the same ansatz for the value functional as in Carmona et al. (2016),

Assuming that has been chosen, for , by the reasoning outlined in Section 2.2.1, the optimal control for the player is given by

This is the same optimal control found in the aforesaid reference.

Assuming each player is following this strategy and noticing that in the formula for should be replaced by (and not ), we find that the HJB equation turns into

| (63) |

3 Conclusions

In this paper, we have studied stochastic control and differential games when there exists path-dependence effect of the control of the agent in the dynamics of the state and in the running cost. We have analyzed the important example of delayed dependence. The framework used was the functional Itô calculus, which has been proven to be an excellent tool to deal with complicated path-dependence structures, see Jazaerli and Saporito (2017). Although we have focused on delayed dependence, because of practical importance, there are no major impediments to examine more interesting structures. We hope this work will allow the consideration of different path-dependent structures in other applications.

Compared to the theory of Gozzi and Marinelli (2006) and Gozzi and Masiero (2017a, b), that deals with the delayed case, the method proposed here allows in principle very general path-dependence in the controls. Moreover, it could be directly applied to (Dirac) measures, as it was done in Section 2.2.1.

Future research will be conducted to analyze viscosity solutions (existence and uniqueness) of the path-dependent HJB derived here. Viscosity solution of similar PPDEs have been extensively studied in recent years, see for example Ekren et al. (2014, 2016a, 2016b). Moreover, it would be interesting to apply the theory developed here to Stackelberg games, see for instance Bensoussan et al. (2015).

Acknowledgements

I would like to thank J.P. Fouque for bringing such a interesting problem to my attention and for all the insightful conversations. I also thank J. Zhang and M. Mousavi for the innumerous helpful discussions and comments.

References

- Alekal et al. [1971] Y. Alekal, P. Brunovsky, D. Chyung, and E. Lee. The Quadratic Problem for Systems with Time Delays. IEEE Trans. Autom. Control, 16(6):673–687, 1971.

- Bensoussan et al. [2015] A. Bensoussan, M. H. M. Chau, and S. C. P. Yam. Mean Field Stackelberg Games: Aggregation of Delayed Instructions. SIAM J. Control Optim., 53(4):2237–2266, 2015.

- Carmona [2016] R. Carmona. Lectures on BSDEs, Stochastic Control, and Stochastic Differential Games with Financial Applications. SIAM, 2016.

- Carmona et al. [2016] R. Carmona, J.-P. Fouque, M. Mousavi, and L.-H. Sun. Systemic Risk and Stochastic Games with Delay. To appear in J. Optim. Theory Appl. 2018.

- Chen and Wu [2011] L. Chen and Z. Wu. The Quadratic Problem for Stochastic Linear Control Systems with Delay. In Proceedings of the 30th Chinese Control Conference, pages 1344–1349, July 2011.

- Cont and Fournié [2010] R. Cont and D.-A. Fournié. Change of Variable Formulas for Non-Anticipative Functional on Path Space. J. Funct. Anal., 259(4):1043–1072, 2010.

- Dupire [2009] B. Dupire. Functional Itô Calculus. 2009. Available at SSRN: http://ssrn.com/abstract=1435551.

- Ekren et al. [2014] I. Ekren, C. Keller, N. Touzi, and J. Zhang. On Viscosity Solutions of Path Dependent PDEs. Ann. Probab., 42(1):204–236, 2014.

- Ekren et al. [2016a] I. Ekren, N. Touzi, and J. Zhang. Viscosity Solutions of Fully Nonlinear Parabolic Path Dependent PDEs: Part I. Ann. Probab, 44(2):1212–1253, 2016a.

- Ekren et al. [2016b] I. Ekren, N. Touzi, and J. Zhang. Viscosity Solutions of Fully Nonlinear Parabolic Path Dependent PDEs: Part II. Ann. Probab, 44(4):2507–2553, 2016b.

- Fournié [2010] D.-A. Fournié. Functional Itô Calculus and Applications. PhD thesis, Columbia University, 2010.

- Gozzi and Marinelli [2006] F. Gozzi and C. Marinelli. Stochastic Optimal Control of Delay Equations Arising in Advertising Models. In G. Da Prato and L. Tubaro, editors, Stochastic Partial Differential Equations and Applications - VII, pages 133–148. Chapman & Hall/CRC, 2006.

- Gozzi and Masiero [2017a] F. Gozzi and F. Masiero. Stochastic Optimal Control with Delay in the Control I: Solving the HJB Equation through Partial Smoothing SIAM J. Control Optim., 55(5):2981–3012, 2017.

- Gozzi and Masiero [2017b] F. Gozzi and F. Masiero. Stochastic Optimal Control with Delay in the Control II: Verification Theorem and Optimal Feedbacks. SIAM J. Control Optim., 55(5):3013–3038, 2017.

- Huang et al. [2012] J. Huang, X. Li, and J. Shi. Forward–Backward Linear Quadratic Stochastic Optimal Control Problem with Delay. Sys. Control Lett., 61:623–630, 2012.

- Jazaerli and Saporito [2017] S. Jazaerli and Y. F. Saporito. Functional Itô Calculus, Path-dependence and the Computation of Greeks. Stochastic Process. Appl., 127(12):3997–4028, 2017.

- Ji et al. [2015] S. Ji, L. Wang, and S. Yang. Path-Dependent Hamilton-Jacobi-Bellman Equations Related to Controlled Stochastic Functional Differential Systems. Optim. Control Appl. Meth., 36:109–120, 2015.

- Oberhauser [2016] H. Oberhauser. An extension of the Functional Itô Formula under a Family of Non-dominated Measures. Stoch. Dyn., 16(4), 2016.

- Pang and Hussain [2015] T. Pang and A. Hussain. An Application of Functional Itô’s Formula to Stochastic Portfolio Optimization with Bounded Memory. Proceedings of the Conference on Control and its Applications, 2015.

- Pham [2009] H. Pham. Continuous-time Stochastic Control and Optimization with Financial Applications. Springer, 2009.

- Pham and Zhang [2014] T. Pham and J. Zhang. Two Person Zero-sum Game in Weak Formulation and Path Dependent Bellman-Isaacs Equation. SIAM J. Control Optim., 52(4):2090–2121, 2014.

- Soner and Touzi [2002] H. M. Soner and N. Touzi. Dynamic Programming for Stochastic Target Problems and Geometric Flows. J. Eur. Math. Soc., 4(3):6201–236, 2002.

- Xu [2013] Y. Xu. Probabilistic Solutions for a Class of Path-Dependent Hamilton-Jacobi-Bellman Equations. Stoch. Anal. Appl., 31:440–459, 2013.