Stepwise Choice of Covariates in High Dimensional Regression

Laurie Davies

Faculty of Mathematics

University of Duisburg-Essen, 45117 Essen, Federal Republic of

Germany

e-mail:laurie.davies@uni-due.de

Abstract

Given data and covariates one problem in linear regression is to decide which if any of the covariates to include. There are many articles on this problem but all are based on a stochastic model for the data. This paper gives what seems to be a new approach which does not require any form of model. It is conceptually and algorithmically simple. Instead of testing whether a regression parameter is zero it asks to what extent the corresponding covariate is better than Gaussian noise as measured by the probability of a greater reduction in the sum of squared residuals. An exact expression for this probability is available and consistency results can be proved under appropriate assumptions. The idea can be extended to non-linear and robust regression.

Subject classification: 62J05

Key words: stepwise regression; high dimensions.

1 Introduction

Most if not all approaches for choosing covariates in high dimensional linear regression are based on the model

| (1) |

where just of the are non-zero or large, the remainder being zero or small. The following approach differs in that it is not based on the model (1) or indeed any model. Whether a covariate is included or not depends only on the degree to which it is better than standard Gaussian white noise.

More precisely, suppose that at one stage of the stepwise procedure a subset of the covariates of size has been included in the regression. Denote the indices of this subset by and the mean sum of squared residuals by . Now include the covariate with and denote the mean sum of squared residuals based on by . Including the best of the covariates not in leads to a minimum mean sum of squared residuals

The covariates not in are now replaced in their entirety by standard Gaussian white noise. Including the random covariate corresponding to leads to a random mean sum of squared residuals and including the best of the random covariates to a minimum mean sum of squared residuals

The probability that the random covariates are better than the actual ones given is

It can be shown that

| (2) |

where denotes a beta random variable with parameters and . This was a personal communication from Lutz Dümbgen, his proof is given in the appendix. It replaces the approximation based on the chi-squared distribution which was used in earlier versions of this paper. Thus

so that finally

| (3) |

where denotes the distribution function of This is the -value for the inclusion of the next covariate. It is worth noting that (3) takes into account the number of covariates already active whose influence is small and the total number of covariates not yet included whose influence is large for large .

If covariates have been included with -values then the probability that each and every one of them is better than Gaussian noise is

| (4) |

This is because at each stage independent Gaussian covariates are used.

One proposal is simply to calculate the -values (3) until the first one that exceeds a given , say , and then include all previous covariates. This leads to the stopping rule

| (5) |

where is the quantile function of the beta distribution with parameters and . The asymptotic version for large and is

A proof is given in the appendix.

The calculation of the -values (3) does not require the choice of a regularization parameter. There is no need for cross-validation or indeed any form of simulation. Furthermore, as the procedure is not based on the linear model (1) it does not require an estimate for the error variance . The method is invariant with respect to affine changes of units and to permutations of the covariates. There are no problems of multiple testing as this is covered by (4). The method can be extended to robust regression, to non-linear approximations of the form if has a Taylor expansion and to the Kullback-Leibler discrepancy where this is appropriate. In these extensions there is no exact form for the -values corresponding to (3) but there exist simple approximations based on the chi-squared distribution.

This paper is based on [Davies, 2016b, Davies, 2016c]. The paper [Davies, 2016b] goes beyond the choice of covariates and considers non-significance regions in place of confidence regions for the values of the parameter . This will not be considered here.

Stepwise regression is treated in Section 2; linear least squares regression in Section 2.1, -regression in Section 2.2 and non-linear approximation in Section 2.3. A consistency result for least squares linear regression is proved in Section 3.1 and the false discovery rate is considered in Section 3.2. Results of simulations following [van de Geer et al., 2014] and [Jia and Rohe, 2015] are given in Section 4.1 and results for in Section 4.2. The proofs of (2) and (1) are given in an appendix.

2 Stepwise regression

2.1 Least squares regression

As an example we take the leukemia data ([Golub et al., 1999]

http://www-genome.wi.mit.edu/cancer/

which was analysed in [Dettling and Bühlmann, 2003]. The number of patients is with covariates. The dependent variable takes on only the values 0 and 1 depending on whether the patient suffers from acute lymphoblastic leukemia or acute myeloid leukemia. The first five genes in order of inclusion with their associated -values as defined by (3) are as follows:

| (7) |

|

According to this relevant genes are 1182, 1219 and 2888. Given these three genes the remaining 3568 are individually no better than random noise with respect to the two forms of leukemia. In particular gene 1946 is no better than random Gaussian noise.

A linear regression based on the genes 1182, 1219, 2888 and 1946 results in the -values 0.0000, 9.84e-8, 5.74e-7 and 8.20e-5 respectively. The difference between the -value 8.20e-5 and the -value 0.0254 for gene 1946 is that the latter takes into account that the gene 1946 is the best of 3568 genes and the former does not.

The time required was 0.1 seconds using a Fortran 77 programme linked to R. The source code for beta distribution function was a double precision version of that given in [Press et al., 2003].

Interest in the above data centred on classifying patients based on their gene expression data. The -values suggest that for this it is only necessary to base the classification on the genes 1182, 1219 and 2888. A simple linear regression based on genes 1182,1219 and 2888 results in one misclassification.

If the fourth covariate 1946 is also included when classifying the patients there are no misclassifications. However if all the covariates except 1182, 1219 and 2888 are replaced by Gaussian white noise then in about 7% of the cases including the fourth covariate results in no misclassifications. Including the fourth and fifth covariates results in no misclassifications in about 60% of the cases. This is in spite of the fact that additional covariates are no more than Gaussian noise.

The above does not imply that 1182, 1219 and 2888 are the only relevant genes. To see this remove these genes and repeat the analysis. This leads to

| (8) |

|

The genes 1652, 979, 657 and 2260 can now be removed and the process continued. If this is done it results in 281 genes which are possibly relevant.

2.2 -regression

The method can be applied to regression but with the disadvantage that there does not exist a simple expression corresponding to (3). If there is a particular interest in regression simulations will be required. If however regression is only used as a protection against outlying -values this can be provided by -regression for which an approximate version of (3) involving the chi-squared distribution is available.

Let by a symmetric, positive and twice differentiable convex function with . The default function will be the Huber’s -function with a tuning constant ([Huber and Ronchetti, 2009], page 69) defined by

| (9) |

The default value of will be .

For a given subset of size the sum of squared residuals is replaced by

| (10) |

which can be calculated using the algorithm described in 7.8.2 of [Huber and Ronchetti, 2009]. The minimizing will de denoted by . A proposal for the choice of is given below.

For some put

| (11) |

and

| (12) |

Replace all the covariates not in by standard Gaussian white noise, include the th random covariate denoted by and put

| (13) |

A Taylor expansion gives

| (14) | |||||

with . This leads to the asymptotic -value

| (15) |

corresponding to the exact -value (3) for linear regression. Here

It remains to specify the choice of scale . The initial value of is the median absolute deviation of multiplied by the Fisher consistency factor 1.4826. If the have a large atom more care is needed. Let be the size of the largest atom. Instead of the median of the absolute deviations from the median we now take the quantile (see Chapter 4 of [Davies, 2014]). Let denote the scale at some point of the procedure with covariates already included. After the next covariate has been included the new scale is taken to be

| (16) |

where the are the residuals based on the covariates and is the Fisher consistency factor given by

where is (see [Huber and Ronchetti, 2009]). Other choices are also possible.

2.3 Non-linear approximation

The dependent variable is now approximated by for some smooth function . Consider a subset , write

| (17) |

and denote the minimizing by . Now include one additional covariate with to give , denote the mean sum of squared residuals by and the minimum over all possible choice of by . As before all covariates not in are replaced by standard Gaussian white noise. Include the th random covariate denoted by , put

and denote the minimum over all possible choice of by .

Arguing as in the last section for robust regression results in

| (18) |

where

| (19) |

The asymptotic -value corresponding to the asymptotic -value (15) for -regression is

| (20) |

If is the logistic function

| (21) | |||||

where

The opportunity is now taken to correct an error in [Davies, 2014]. The term

occurs repeatedly in Chapter 11.6.1.2 and should be replaced by

agreeing with (21).

Robust non-linear regression can be treated in the same manner but the expressions become unwieldy.

2.4 Kullback-Leibler and logistic regression

In some data sets, for example the leukemia data of Section 2.1, the dependent variable takes on only the values zero and one. For such data least squares combined with the logistic model can cause problems: it can happen that for some the estimated probability is although . An example is provided by the colon cancer data ([Alon et al., 1999], http://microarray.princeton. edu/oncology/.). The sample size is and there are 2000 covariates. The logistic model based on least squares with a cut-off -value of 0.01 results in two covariates. If these two covariates are used to classify the cancer there are three errors. In two cases the probability based on the logistic model is one whereas the dependent variable has the value zero. In the third case the values are zero and one respectively.

The problem can be avoided by using the Kullback-Leibler discrepancy

| (22) |

where

The arguments of the previous two sections lead to the asymptotic -values

| (23) |

where is the minimum Kullback-Leibler discrepancy based on a subset and the minimum value through the inclusion of one additional covariate. The are the values of giving the minimum .

Repeating the least squares analysis for the colon data but now using the Kullback-Leibler divergence results in the single gene number 377. The number of misclassifications based on this gene is nine. The second gene 356 has a -value of 0.053. If this is included the number of misclassifications is reduced to two but the status of this second gene is not clear.

3 Consistency and false discovery rate

3.1 Consistency:

To prove a consistency result a model with error term is necessary. It is defined as follows. There are covariates and the response is given by the first

| (24) |

where the are i.i.d. Gaussian random variables with zero mean and variance . Given a sample of size both and will be allowed to depend on . Without loss of generality the covariates will be standardized to have norm , that is .

A given subset of will be denoted by . For the subset will be denoted by , the complements of and with respect to by and respectively. The projection onto the linear space spanned by the will be denoted by with the corresponding notation for , and . Finally put

with the corresponding definitions of , and

Let and be the sum of squared residuals after regressing on the covariates for in and respectively. From and the Gaussian assumption on the errors (which can be relaxed) it follows that the asymptotic values of and are given by

| (25) | |||||

| (26) |

respectively. Given the covariates are specified sequentially up to but excluding the first covariate whose -values exceeds for some sequence tending to zero but such that

| (27) |

Theorem 3.1.

Suppose that there exists a and a such that for all

sufficiently large the following holds:

(i) for each proper subset of

there exists a such that

| (28) |

(ii) for all subsets of and for all

| (29) |

Then the procedure described above is consistent.

Proof.

For large

It follows from (5), (1), the choice of the and (i) of the theorem that if covariates with have been included then either all covariates have been included or there exists at least one covariate which is a candidate for inclusion. From (5), (1), the choice of and (ii) it follows that there is no covariate with which is a candidate for inclusion. The procedure therefore continues until all covariates are included and then terminates. ∎

It is perhaps worth emphasizing that the theorem does not require that the covariates be uncorrelated. To take a concrete example put so that

where and the correlation between and is . Suppose that so that is the first candidate for inclusion. Then for large will be included if

for some .

If however the covariates are orthogonal then (28) simplifies and becomes

| (30) |

Theorem 1 of [Lockhart et al., 2014] gives a consistency result for orthogonal covariates with norm one, namely (in the present notation)

| (31) |

If more care is taken (30) can be expressed in the same manner with . At first glance (30) differs from (31) by the inclusion of . However lasso requires a value for which causes problems , particularly if (see [Lockhart et al., 2014]). The term is nothing more than the approximation for and can therefore be interpreted, if one wishes, as an estimate for based on the sum of squared errors of the covariates which are active at this stage.

3.2 False discovery rate

In this section we suppose that the data are generated as under (1) with given and the errors are Gaussian white noise. We suppose further that there are additional covariates which are Gaussian white noise independent of the and the . A false discovery is the inclusion of a variable in the final active set. We denote the number of false discoveries by . The following theorem holds.

Theorem 3.2.

Let be the event that none of the covariates are included and the event they are all and moreover the first to be included. Then

Proof.

Consider and suppose that of the random covariates are active and consider the probability that these are indexed by in the order of inclusion. At each stage the residuals are independent of the covariates not yet included due to the independence of the random covariates and the errors . The probability that is included is the probability that the threshold is not exceeded which is approximately (see the Appendix). Thus the probability that the included covariates are indexed by is approximately . There are choices for the covariates and hence

Summing over gives

The same argument works for . ∎ ∎

Sufficient conditions for the to be large can be given. For example for suppose the fixed covariates satisfy

for some . Then the proof of (1) given in the appendix shows that the probability that (3.2) holds for one the random covariates is asymptotically . From this it follows for large .

Simulations suggest that the result holds under more general conditions. As an example we use a a simulation scheme considered in [Candes et al., 2017]. The covariates are Gaussian but given by an AR(1) process with coefficient 0.5. The dependent variable is given by the logit model

It is clear that the conditions imposed above do not hold. The covariates are not independent and rather than approximately 1. We consider four different sample sizes , and the two cases with the values of and reversed. The results for least squares using the logit model are given in Table 1 for . The first line for the sample sizes gives the average number of false discoveries, the second line gives the average number of correct discoveries. The results are based on 1000 simulations. It is seen that the average number of false discoveries is indeed well described by . The results for least squares based and the logit model combined with Kullback-Leibler are essentially the same.

| 500 | 200 | 0.012 | 0.051 | 0.103 |

|---|---|---|---|---|

| 0.594 | 1.063 | 1.343 | ||

| 5000 | 2000 | 0.010 | 0.059 | 0.106 |

| 6.420 | 7.015 | 7.196 | ||

| 200 | 500 | 0.010 | 0.043 | 0.102 |

| 0.029 | 0.130 | 0.179 | ||

| 2000 | 5000 | 0.006 | 0.058 | 0.112 |

| 2.92 | 3.477 | 3.701 |

4 Simulations and real data

4.1 The ProGau, ProPre1 and ProPre2 procedures

The procedure described in this paper with will be denoted by ProGau. Two modifications, ProPre1 and ProPre2, are also considered both of which are intended to ameliorate the effects of high correlation between the covariates. They are based on [Jia and Rohe, 2015] and are as follows. Let

be the singular value decomposition of the covariates . Put

where is the diagonal matrix consisting of the reciprocals of the non-zero values of . Then is replaced by and by . The ProPre1 procedure is to apply the ProGau procedure to .

The third procedure to be denoted by ProPre2 is to first precondition the data as above but then to set in (5). This gives a list of candidate covariates. A simple linear regression is now performed using these covariates. Covariates with a large -value in the linear regression are excluded and the remaining covariates accepted. A large -value is defined as follows: given as in ProGau and ProPre1 the cut-off -value in the linear regression to be as in (5). As is small and large with respect to this corresponds approximately to a -values of . This is somewhat ad hoc it specifies a well defined procedure which can be compared with other procedures.

At first sight it may appear that the use of -values deriving from a linear regression implies the acceptance of the linear model (1). This is not so. In [Davies, 2016b] non-significance regions are defined based on random perturbations of the covariates. The resulting regions are asymptotically the same as the confidence regions derived from the linear model (1) but do not suppose it.

4.2 Simulations

Linear regression

The first set of simulations we report are the equi-correlation simulations described in Section 4.1 of [van de Geer et al., 2014]. The sample size is and the number of covariates is . The covariates are generated as Gaussian random variables with covariance matrix where and . Four different scenarios are considered. The number of non-zero coefficients in the data generate according to the linear model is either or and they are all either i.i.d. or i.i.d. . The error term in the model is i.i.d .

Although [van de Geer et al., 2014] is concerned primarily with confidence interval Tables 5-8 give the results of simulations for testing all the hypotheses . This is equivalent to choosing those covariates for which is rejected. The measures of performance are the power and the family-wise error rate FWER. The power is the proportion of correctly identified active covariates. The FWER is the proportion of times the estimated set of active covariates contains a covariate which is not active. In Tables 6 and 8 of [van de Geer et al., 2014] the active covariates are chosen at random. As ProGau, ProPre1 and ProPre2 are equivariant with respect to permutations of the covariates the active covariates are either or as in Tables 5 and 7 of [van de Geer et al., 2014].

The results given in Table 2. The results for Lasso-Pro are taken from [van de Geer et al., 2014]. As is seen from Table 2 the best overall procedure is ProPre2. In the case and coefficients it is slightly worse that Lasso-Proc but the difference could well be explicable by simulation variation. For ProGau, ProPre1 and ProPre2 500 simulations were performed.

| Lasso-Pro | 0.56 | 0.10 | 0.79 | 0.11 | 0.70 | 1.00 | 0.92 | 1.00 |

|---|---|---|---|---|---|---|---|---|

| ProGau | 0.60 | 0.19 | 0.79 | 0.07 | 0.25 | 0.97 | 0.46 | 0.96 |

| ProPre1 | 0.41 | 0.01 | 0.71 | 0.01 | 0.09 | 0.01 | 0.29 | 0.00 |

| ProPre2 | 0.55 | 0.12 | 0.79 | 0.07 | 0.44 | 0.26 | 0.73 | 0.09 |

Tables 1-4 of [van de Geer et al., 2014] give the results of some simulations on the covering frequencies and the lengths of confidence intervals. Again we shall restrict the comparisons to the four cases detailed above. The average cover for the active set is defined by

and the average length by

with analogous definitions for the complement . The are the confidence intervals for the coefficients used to generate the data.

The -confidence intervals for the covariates for the procedures ProGau, ProPre1 and ProPre2 are calculated as follows. Let denote the estimated active set. For the covariates in the confidence intervals are those calculated from a simple linear regression. For a covariate in the confidence interval is calculates by appending this covariate to the set , performing a linear regression and using confidence interval from this regression. It is pointed out again that these confidence intervals are not dependent on the linear model (1).

The results are given in Table 3 with the Lasso-Pro results taken from [van de Geer et al., 2014]. For and the standard deviations of the estimates of the are approximately 0.186 and 0.216 respectively. Thus for a coverage probability of the optimal lengths of the confidence intervals are approximately and respectively. For the Lasso-Pro procedure with the stated coverage probabilities the lengths of the confidence intervals for with are 78% for and 74% for . For and the corresponding percentages are 10% for and 5% for . For with the percentages are 73% for and 85% for . For the intervals are approximately 25% shorter than the optimal intervals. The explanation would seem to be the following (personal communication from Peter Bühlmann). The theorems of [van de Geer et al., 2014] require to guarantee an asymptotically valid uniform approximation and prevent super efficiency. On plugging in and gives so that is, so to speak, not in the range of applicability of the theorems. The lengths for with are only slightly longer than the optimal intervals so even here there may be a super efficiency effect.

We note that in this simulation ProPre1 is dominated by ProGau.

| Lasso-Pro | 0.89 | 0.82 | 0.87 | 0.82 | 0.56 | 0.56 | 0.53 | 0.55 | |

|---|---|---|---|---|---|---|---|---|---|

| 0.95 | 0.80 | 0.96 | 0.80 | 0.93 | 0.57 | 0.93 | 0.56 | ||

| ProGau | 0.84 | 0.70 | 0.89 | 0.73 | 0.81 | 1.42 | 0.84 | 1.81 | |

| 0.91 | 0.76 | 0.93 | 0.78 | 0.78 | 1.43 | 0.84 | 1.82 | ||

| ProPre1 | 0.52 | 0.55 | 0.79 | 0.72 | 0.03 | 1.65 | 0.24 | 2.86 | |

| 0.48 | 0.63 | 0.80 | 0.79 | 0.02 | 1.71 | 0.23 | 2.96 | ||

| ProPre2 | 0.76 | 0.68 | 0.87 | 0.73 | 0.62 | 1.24 | 0.85 | 1.08 | |

| 0.77 | 0.75 | 0.89 | 0.78 | 0.60 | 1.26 | 0.87 | 1.09 | ||

Simulation experiments are reported in [Jia and Rohe, 2015]. The ones to be given here correspond to those of Figure 4 of [Jia and Rohe, 2015]. The sample size is with and 30000. The covariates have covariance matrix with and with and . The number of active covariates is with coefficients . The noise is i.i.d. . The results are given in Table 4.

It is seen that ProPre2 gives the best results for and 30000 but fails in terms of false negatives for . More generally ProPre2 fails for in the range 230-280. This seems to correspond to the peaks in the black ‘puffer’ lines of Figure 4 of [Jia and Rohe, 2015]. An explanation of this phenomenon is given in [Jia and Rohe, 2015]. For in the range 280-30000 ProPre2 outperforms ProGau and ProPre2 and also all the methods in Figure 4 of [Jia and Rohe, 2015], particularly with respect to the number of false positives.

| 250 | 5000 | 10000 | 15000 | 30000 | ||||||

| ProGau | 0.00 | 1.55 | 9.12 | 7.87 | 15.1 | 9.32 | 17.3 | 10.0 | 18.1 | 9.91 |

| ProPre1 | 20.0 | 0.00 | 15.7 | 0.01 | 17.7 | 0.00 | 17.2 | 0.00 | 18.6 | 0.01 |

| ProPre2 | 19.3 | 0.44 | 0.00 | 0.02 | 0.00 | 0.07 | 0.47 | 0.16 | 0.85 | 1.08 |

| 250 | 5000 | 10000 | 15000 | 30000 | ||||||

| ProGau | 0.00 | 0.18 | 3.38 | 2.96 | 8.04 | 4.11 | 11.7 | 5.00 | 16.1 | 5.94 |

| ProPre1 | 14.3 | 0.40 | 13.48 | 0.00 | 15.8 | 0.00 | 17.4 | 0.00 | 18.2 | 0.01 |

| ProPre2 | 17.0 | 0.00 | 0.00 | 0.02 | 0.00 | 0.04 | 0.11 | 0.06 | 0.81 | 0.09 |

Logistic regression

Logistic regression was also considered in

[van de Geer et al., 2014]. Table 5 gives the results of some

simulations as described in [van de Geer et al., 2014]: it includes Table 9

of [van de Geer et al., 2014]. The sample size is and the number of

covariates is . The covariates are

generated as Gaussian random variables with mean zero and covariance

matrix with for and

. The parameter is given by

with and . The dependent variables are generated as a independent

binomial random variables with (see

[van de Geer et al., 2014]). The KL-procedure of the table is as described

in Section 2.4 . The cut-off -value is so that all covariates

are included up to but excluding the first with a -value exceeding 0.01.

| Logistic regression | ||||

|---|---|---|---|---|

| Toeplitz | ||||

| measure | method | |||

| Power | Lasso-ProG | 0.06 | 0.27 | 0.50 |

| MS-Split | 0.07 | 0.37 | 0.08 | |

| KL-procedure | 0.26 | 0.32 | 0.37 | |

| FWER | Lasso-ProG | 0.03 | 0.08 | 0.23 |

| MS-Split | 0.01 | 0.00 | 0.00 | |

| KL-procedure | 0.03 | 0.02 | 0.01 | |

4.3 Real data

The real data includes three of the data sets used in

[Dettling and Bühlmann, 2003], namely Leukemia ([Golub et al., 1999],

http://www-genome.wi.mit.edu/cancer/.), Colon ([Alon et al., 1999],

http://microarray.princeton. edu/oncology/.) and

Lymphoma ([Alizadeh et al., 2000], http://llmpp.nih.gov/

lymphoma/data/figure1). A fourth data set SRBCT is included. All data

sets were downloaded from

http://stat.ethz.ch/~dettling/bagboost.html

A fifth data set, prostate cancer prostate.rda was downloaded

from the lasso2 package available from the CRAN R package

repository.

The dependent variable is integer valued in all

cases, each integer denoting a particular form, or absence, of

cancer.

Least squares

The data set Leukemia was analysed in Section 2.1 using

ProGau with the -values of the first five genes given

(7). Classification of the form of cancer

based on these three genes results in one misclassification.

If this is repeated using ProPre1 the result

is

| (32) |

|

Classifying the cancer using gene 979 only results in 15 misclassifications. The procedure ProPre2 also results in the single gene 979 and 15 misclassifications. The results for the remaining real data sets given above are equally poor so the procedures ProPre1 and ProPre2 will not be considered any further.

Table 6 gives the results for ProGau for all five data sets. The second row gives the sample size, the number of covariates followed by the number of different cancers. The rows 4-8 give the covariates in order and their -values. These are included in order up to but excluding the first covariate with a -value exceeding 0.01. The row 9 gives the number of misclassifications based on the included covariates. Row 10 gives the number of possibly relevant covariates calculates as described in Section 2.1.

In previous versions of this paper the number of misclassifications based on ProGau as described above was compared with the results given in Table 1 of [Dettling and Bühlmann, 2003]. The comparison is illegitimate. The results in [Dettling and Bühlmann, 2003] are calculated by cross validation: each observation is in turn classified using the remaining observations and Table 1 of [Dettling and Bühlmann, 2003] reports the number of misclassification using different procedures. Line 11 gives the results for the following procedure based on ProGau.

The th observation is eliminated leaving observations. Each of these is eliminated in turn and the ProGau procedure applied to the remaining observations. This gives sets of active covariates. The ten most frequent covariates are then used to classify the th observation. This is done for . The sample is augmented by all misclassified observations and the procedure applied to the new sample. This is a form of boosting. This is done 60 times or until all observations are correctly classified which ever happens first. The numbers in row 11 give the number of misclassifications followed by the number of additional observations.

| Linear regression: least squares | |||||||||

| Leukemia | Colon | Lymphoma | SRBCT | Prostate | |||||

| 72, 3571, 2 | 62, 2000, 2 | 62, 4026, 3 | 63, 2308, 4 | 102, 6033, 2 | |||||

| cov. | -val. | cov. | -val. | cov. | -val. | cov. | -val. | cov. | -val. |

| 1182 | 0.0000 | 493 | 7.40e-8 | 2805 | 0.0000 | 1389 | 2.32e-9 | 2619 | 0.0000 |

| 1219 | 8.57e-4 | 175 | 4.31e-1 | 3727 | 8.50e-9 | 1932 | 2.02e-7 | 203 | 5.75e-1 |

| 2888 | 3.58e-3 | 1909 | 5.16e-1 | 632 | 1.17e-4 | 1884 | 9.76e-5 | 1735 | 4.96e-1 |

| 1946 | 2.54e-1 | 582 | 3.33e-1 | 714 | 2.30e-2 | 1020 | 1.70e-1 | 5016 | 9.81e-1 |

| 2102 | 1.48e-1 | 1772 | 9.995e-1 | 2036 | 2.94e-1 | 246 | 6.75e-2 | 2940 | 9.52e-1 |

| 1 | 9 | 1 | 13 | 8 | |||||

| 281 | 45 | 1289 | 115 | 185 | |||||

| 0, 10 | 0, 59 | 0, 7 | 0, 75 | 1,42 | |||||

Robust regression

Table 7 corresponds to

Table 6. In all cases the first gene is the

same. For the lymphoma and SRBCT data sets the first five genes are

the same and in the same order. Nevertheless there are differences

which may be of importance.

One simple but, because of the nature of dependent variable, somewhat artificial example which demonstrates this it to change the first value for the colon data from 0 to -10. The first gene using least squares is now 1826 with a -value of 0.352. This results not surprisingly in 23 misclassifications of the remaining 61 tissues. For the robust regression the first gene is again 493 with a -value of 1.40e-5 which results in nine misclassifications as before.

In the real data examples considered here the dependent variable denotes a form of cancer and is therefore unlikely to contain outliers. Nevertheless the stepwise regression procedure can reveal outliers or exotic observations. Given residuals a measure for the outlyingness of is where . Hampel’s 5.2 rule ([Hampel, 1985]) is to identify all observations whose outlyingness value exceeds 5.2 as outliers. For the leukemia data based on the first three covariates and using least squares the observations numbered 21, 32 and 35 were identified as outliers with outlyingness values 5.53, 9.78 and 5.96 respectively. The robust regression for the same data resulted in four outliers, 32, 33, 35 and 38 with values 18.0, 6.46, 18.42 and 7.50 respectively. The observations 32 and 35 are also identified by least squares but the outlyingness values for the robust regression are much larger .

| Robust linear regression | |||||||||

| Leukemia | Colon | Lymphoma | SRBCT | Prostate | |||||

| 72, 3571 | 62, 2000 | 62, 4026 | 63, 2308 | 102, 6033 | |||||

| cov. | -val. | cov. | -val. | cov. | -val. | cov. | -val. | cov. | -val. |

| 1182 | 1.11e-9 | 493 | 2.76e-5 | 2805 | 1.11e-10 | 1389 | 1.65e-5 | 2619 | 1.34e-12 |

| 2888 | 7.41e-5 | 449 | 5.04e-1 | 3727 | 8.82e-6 | 1932 | 4.65e-6 | 1839 | 1.47e-1 |

| 1758 | 2.35e-5 | 1935 | 1.26e-1 | 632 | 1.39e-3 | 1884 | 7.15e-4 | 2260 | 7.70e-3 |

| 3539 | 4.89e-2 | 175 | 8.95e-1 | 714 | 4.04e-2 | 1020 | 9,85e-2 | 1903 | 8.23e-1 |

| 3313 | 2.86e-2 | 792 | 1.86e-1 | 2036 | 3.71e-1 | 246 | 3.99e-2 | 5903 | 7.65e-1 |

| 1, 1.39% (2) | 9, 14.52% (2) | 1, 1.61% (3) | 13, 20.63% (4) | 8, 7.77% (2) | |||||

| Logistic regression: Kullback-Leibler | |||||

| Leukemia | Colon | Prostate | |||

| 72, 3571 | 62, 2000 | 102, 6033 | |||

| cov. | -val. | cov. | -val. | cov. | -val. |

| 956 | 0.0000 | 377 | 2.12e-7 | 2619 | 0.0000 |

| 1356 | 8.14e-2 | 356 | 5.35e-2 | 4180 | 6.69e-1 |

| 264 | 1.00e-0 | 695 | 1.0000 | 1949 | 9.88e-1 |

| 6, 8.33% | 10, 16.13% | 9, 8.82% | |||

Logistic regression

For the leukemia, colon and prostate data the dependent variate

takes on only the values zero and one. These data

sets can therefore can be analysed using logistic regression and the

Kullback-Leibler discrepancy (see Section 2.4).

Table 8 gives the results corresponding to

those of Table 6.

The second covariates for the leukemia and colon data exceed the

cut-off -value of 0.05 but could nevertheless be relevant. If they

are included the number of misclassifications are zero and four

respectively.

The birthday data

The data consist of the number of births on every day from 1st January

1969 to the 31st December 1988. The sample size is . The data

are available as ‘Birthdays’ from the R-package ‘mosaicData’. They

have been analysed in [Gelman et al., 2013].

In a first step a trend was calculated using a polynomial of order 7 by means of a robust regression using Huber’s -function with tuning constant (page 174 of [Huber and Ronchetti, 2009]).

The trend was subtracted and the residuals were analysed by means of a robust stepwise regression again using Huber’s -function with tuning constant . The covariates were the trigonometric functions

but with the difference that the and were treated in pairs

and . The cut-off -value was . This resulted

in 54 pairs being included in the regression. The first five periods

in order of importance were 7 days, 3.5 days, one year, six months and

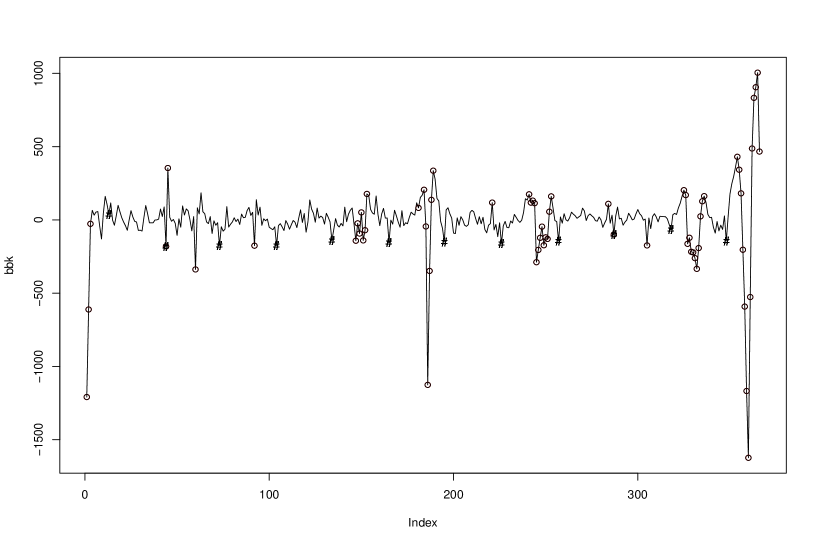

2.33 days ( of a week). Figure 1 shows the

average size of the residual for each day of the year. The marked days

are 1st-3rd January, 14th February, 29th February, 1st April, Memorial

Day, Independence Day, 8th August (no explanation), Labor Day,

Veterans Day, Thanksgiving, Halloween, Christmas, and the 13th of each month.

Graphs

Given variables a graphical representation of their

mutual dependencies can be constructed. The nodes of the graph

represent the variables and the edges indicate the existence of

dependencies between the joined nodes. A graph can be construct by

performing a stepwise regression of each variable on the others and

then joining that variable with those variables in the active subset

for that variable. In all there are regressions and to take

this into account the cut-off -value is replaced by

. For the colon data with this results in a

graph with 1851 edges and a computing time of 45 seconds. For the

prostate data the graph has 7178 edges and the computing time was 15.5

minutes

.

In [Meinshausen and Bühlmann, 2006] the authors give a lasso based method for choosing a graph. A major problem with lasso is the choice of the regularizing parameter . In the case of graphs however the authors show that there is a criterion which allows a specification of : if is given as in (9) on page 1446 of their paper then is an upper bound for the probability of falsely joining two distinct connected components of the graph.

As an example they simulated a Gaussian sample with and based on a random graph with 1747 edges. Unfortunately there is an error in the description of the construction of the graph. The stated probability (bottom line of page 1447) of joining two given nodes is not consistent with the graph in Figure 1 of the paper (confirmed in a personal communication by Nicolai Meinshausen). In the reconstruction of the graph 1109 of the 1747 edges were correctly identified and there were two false positives. An attempt was made to construct a graph similar to that of [Meinshausen and Bühlmann, 2006]. The resulting graph had 1829 edges. In 10 simulations the average number of correctly identified edges was 1697 and on average there were 0.8 false positives. These results are better than those based on the lasso. This is one more indication that the stepwise procedure of [Davies, 2016a] is not only much simpler than lasso it also gives better results.

5 Acknowledgment

The author thanks Lutz Dümbgen for the exact -value (3) and the proof. He also thanks Peter Bühlmann for help with [van de Geer et al., 2014], Nicolai Meinshausen for help with [Meinshausen and Bühlmann, 2006], Joe Whittaker for the section on graphs, Christian Hennig and Oliver Maclaren for helpful comments on earlier versions.

6 Appendix

Proof of (2).

The result and the following proof are due to Lutz Dümbgen. Given

and linearly independent covariates with consider the best linear

approximation of by the in the

norm:

The residual vector lies in the orthogonal complement of the space spanned by the . The space is of dimension . Let be an additional vector and consider the best linear approximation to based on . This is equivalent to considering the best linear approximation to based on where is the orthogonal projection onto . The sum of squared residuals of this latter

where . If is standard Gaussian white noise then is standard Gaussian white noise in . Let be an orthonormal basis of such that . Then

which has the same distribution as

where the are i.i.d . This proves (2) on noting that the are independent random variables so that

Proof of (1).

Let the required -value for stopping be . Then solving

(3) for small leads to

Now

Thus

which leads to

On putting

it is seen that

References

- [Alizadeh et al., 2000] Alizadeh, A., Eisen, M., Davis, R., Ma, C., Lossos, I., Rosenwald, A., Boldrick, J., Sabet, H., Tran, T., Yu, X., Powell, J., Yang, L., Marti, G., Moore, T., Hudson, J., Lu, L., Lewis, D., Tibshirani, R., Sherlock, G., Chan, W., Greiner, T., Weisenburger, D., Armitage, J., Warnke, R., Levy, R., Wilson, W., Grever, M., Byrd, J., Botstein, D., Brown, P., and Staudt, L. (2000). Distinct types of diffuse large B-cell lymphoma identified by gene expression profiling. Nature, 403:503–511.

- [Alon et al., 1999] Alon, U., Barkai, N., Notterman, D., Gish, K., Ybarra, S., Mack, D., and Levine, A. (1999). Broad patterns of gene expression revealed by clustering analysis of tumor and normal colon tissues probed by oligonucleotide arrays. PNAS, 96(12).

- [Candes et al., 2017] Candes, E., Fan, Y., Janson, L., and Lv, J. (2017). Panning for gold: Model-free knockoffs for high-dimensional controlled variable selection. arXiv:1610.02351v3 [math.ST].

- [Davies, 2014] Davies, L. (2014). Data Analysis and Approximate Models. Monographs on Statistics and Applied Probability 133. CRC Press.

- [Davies, 2016a] Davies, L. (2016a). Stepwise choice of covariates in high dimensional regression. arXiv:1610.05131v2 [math.ST].

- [Davies, 2016b] Davies, P. L. (2016b). Functional choice and non-significance regions in regression. arXiv:1605.01936 [math.ST].

- [Davies, 2016c] Davies, P. L. (2016c). On stepwise regression. arXiv: 1605.04542[math.ST].

- [Dettling and Bühlmann, 2003] Dettling, M. and Bühlmann, P. (2003). Boosting for tumor classification with gene expression data. Bioinformatics, 19(9):1061–1069.

- [Gelman et al., 2013] Gelman, A., Carlin, J., Stern, H., Dunson, D., Vehtari, A., and Rubin, D. (2013). Bayesian Data Analysis. CRC Texts in Statistical Science. CRC Press, third edition.

- [Golub et al., 1999] Golub, T., Slonim, D., P., T., Huard, C., Gaasenbeek, M., Mesirov, J., Coller, H., Loh, M., Downing, J., Caligiuri, M., Bloomfield, C., and Lander, E. (1999). Molecular classification of cancer: class discovery and class prediction by gene expression monitoring. Science, 286(15):531–537.

- [Hampel, 1985] Hampel, F. R. (1985). The breakdown points of the mean combined with some rejection rules. Technometrics, 27:95–107.

- [Huber and Ronchetti, 2009] Huber, P. J. and Ronchetti, E. M. (2009). Robust Statistics. Wiley, New Jersey, second edition.

- [Jia and Rohe, 2015] Jia, J. and Rohe, K. (2015). Preconditioning the lasso for sign consistency. Electron. J. Statist., 9(1):1150–1172.

- [Lockhart et al., 2014] Lockhart, R., Taylor, J., Tibshirani, R. J., and Tibshirani, R. (2014). A significance test for the lasso. Ann. Statist., 42(2):413–468.

- [Meinshausen and Bühlmann, 2006] Meinshausen, N. and Bühlmann, P. (2006). High-dimensional graphs and variable selection with the lasso. Annals of Statistics, 34(3):1436–1462.

- [Press et al., 2003] Press, W. H., Teukolsky, S. A., Vetterling, W. T., and Flannery, B. P. (2003). Numerical Recipes in Fortran 77: The Art of Scientific Computing, volume 1. Cambridge University Press, second edition.

- [van de Geer et al., 2014] van de Geer, S., Bühlmann, P., Ritov, Y., and Dezeure, R. (2014). On asymptotically optimal confidence regions and tests for high-dimensional models. Annals of Statistics, 42(3):1166–1202.