two-sample testing in non-sparse

high-dimensional linear models

Abstract

In analyzing high-dimensional models, sparsity of the model parameter is a common but often undesirable assumption. Though different methods have been proposed for hypothesis testing under sparsity, no systematic theory exists for inference methods that are robust to failure of the sparsity assumption. In this paper, we study the following two-sample testing problem: given two samples generated by two high-dimensional linear models, we aim to test whether the regression coefficients of the two linear models are identical. We propose a framework named TIERS (short for TestIng Equality of Regression Slopes), which solves the two-sample testing problem without making any assumptions on the sparsity of the regression parameters. TIERS builds a new model by convolving the two samples in such a way that the original hypothesis translates into a new moment condition. A self-normalization construction is then developed to form a moment test. We provide rigorous theory for the developed framework. Under very weak conditions of the feature covariance, we show that the accuracy of the proposed test in controlling Type I errors is robust both to the lack of sparsity in the features and to the heavy tails in the error distribution, even when the sample size is much smaller than the feature dimension. Moreover, we discuss minimax optimality and efficiency properties of the proposed test. Simulation analysis demonstrates excellent finite-sample performance of our test. In deriving the test, we also develop tools that are of independent interest. The test is built upon a novel estimator, called Auto-aDaptive Dantzig Selector (ADDS), which not only automatically chooses an appropriate scale (variance) of the error term but also incorporates prior information. To effectively approximate the critical value of the test statistic, we develop a novel high-dimensional plug-in approach that complements the recent advances in Gaussian approximation theory.

, and

1 Introduction

High-dimensional data are increasingly encountered in many applications of statistics and most prominently in biological and financial research. A common feature of the statistical models used to study high-dimensional data is that while the dimension of the model parameter is high, the sample size is relatively small. This is the so-called High-Dimensional Low-Sample Setting (HDLSS) where as . For such models, a common underlying theoretical assumption is that the effective dimensionality of the data is small, i.e., the number of non-zero components of the model parameter, denoted by , is either fixed or grows slowly as with . Hypothesis testing in such HDLSS settings has recently gained a great deal of attention (see Dezeure et al. (2015) for a review). The problem is fundamentally difficult to solve due to the bias propagation induced by the regularized estimators (Zhang and Zhang (2014)), all of which are specifically designed to resolve the curse-of-dimensionality, , phenomenon. Bias propagation is apparent across models and across regularizations (Zhang and Huang (2008); Fan and Lv (2011)).

However, since consistent estimation without sparsity (i.e., ) has not been successfully resolved, hypothesis testing in such models has not been addressed until now. Yet, many scientific areas do not support the sparsity assumption and thus require development of new inferential methods that are robust to non-sparsity. A natural question is whether or not we can design effective method for hypothesis testing that allows for such non-sparse high-dimensional models. We answer this question in the context of two-sample simultaneous tests of equality of parameters of the regression models. Below we present a couple of examples that highlight the importance and applications of the problem we consider.

(a) (Dense Differential Regressions) In many situations, two natural subgroups in the data occur; for example, suppose that treatments and are given to and patients, respectively, and that the -th subject who receives treatment () has response to treatment at the level , where the expected value of is for and . Specifically, we intend to test the null hypotheses that

The effects of the treatment are typically collected in the vectors . Such effects are rarely sparse as therapies for highly diverse illnesses largely benefit from complicated treatments, for example, radio-chemotherapy (Allan et al. (2001)). In this case, treatment affects a large number of levels of the molecular composition of the cell and many malfunctions have been shown to relate to cancer-like behavior. Hence, in such setting, it is pertinent to consider vector that measures the treatment on the genetic cell or molecular level, leading to a high-dimensional feature vector with that is in principle not sparse.

(b) (Dense Differential Networks) Hypotheses concerning differences in molecular influences or biological network structure using high-throughput data have become prevalent in modern FMRI studies. Namely, one is interested in discovering “brain connectivity networks” and comparing two of such networks between subgroups of population. Here, one is interested in discovering the difference between two populations modeled by Gaussian graphical models. Significance testing for network differences is a challenging statistical problem, involving high-dimensional estimation and comparison of non-nested hypotheses. In particular, one can consider -dimensional Gaussian random vectors and . The conditional independence graphs are characterized by the non-zero entries of the precision matrices and (Meinshausen and Bühlmann (2006)). Given an -sample of and an -sample of with , the objective is to test

without assuming any sparse structure on the precision matrices.

1.1 This paper

In this paper we consider the following two-sample, linear regression models

| (1.1) |

and

| (1.2) |

with the unknown parameters of interest, and . For simplicity of presentation, we consider Gaussian random design, i.e. -dimensional design vectors and follow normal distribution and with unknown covariance matrices and . Moreover, the noise components are mean zero, independent from the design and have a distribution with unknown standard deviations and . In this formal setting, our objective is to test whether model (1.1) is the same as the model (1.2), i.e., to develop a test for the hypothesis of our interest

| (1.3) |

with and . We will work with two independent samples and of size but similar constructions can be exploited for the two samples of unequal sizes.

Here, we propose a hypothesis test for (1.3) that provides a valid error control without making any assumptions about the sparsity of the two model parameters. Although testing in high-dimensions has gained a lot of attention recently, the procedure proposed is, to the best of our knowledge, the first to possess all of the following properties.

-

(a)

The proposed test, named TestIng Equality of Regression Slopes (TIERS from here on), is valid regardless of the assumption of sparsity of the model parameters and . Type I error converges to the nominal level even if and .

-

(b)

TIERS remains valid under any distribution of the model errors even in the high-dimensional case. In particular, TIERS is robust to heavy-tailed distribution in the errors and , such as the Cauchy distribution.

-

(c)

Under weak regularity conditions, TIERS is nearly efficient compared to an oracle testing procedure and enjoys minimax optimality. Whenever, , TIERS achieves the aforementioned efficiency and optimality properties regardless of the sparsity in and .

The approach also extends naturally to groups of regressions and can provide Type I and Type II errors using only convex optimization or linear programming. Additionally, the test can be generalized to the case where one considers nested models. Likewise, tests of the null hypothesis : can be performed.

1.2 Previous work

Hypothesis testing in high-dimensional regression is extremely challenging. Most estimators cannot guard against inclusion of noise variables unless restrictive and unverifiable assumptions (for example, irrepresentable condition (Zhao and Yu (2006)) or minimum signal strength (Fan and Peng (2004)) are made. Early work on p-values includes methods based on multiplicity correction that are conservative in their Type I error control (Meinshausen, Meier and Bühlmann (2009); Bühlmann (2013)), bootstrap methods that control false discovery rate (Meinshausen, Meier and Bühlmann (2009); Mandozzi and Bühlmann (2016)) and inference methods guaranteeing asymptotically exact tests under the irrepresentable condition (Fan and Li (2001)). More recently, there have been series of important studies that design asymptotically valid tests while relaxing the irrepresentable condition. Pioneering work of Zhang and Zhang (2014) develops de-biasing technique and shows that low-dimensional projections are an efficient way of constructing confidence intervals. In a major generalization, Van de Geer et al. (2014) consider a range of models which includes the linear models and the generalized linear models and obtain valid inference methods when . The literature has also seen work similar in spirit for Gaussian graphical models (Ren et al. (2015)). Javanmard and Montanari (2015) compute optimal sample size and minimax optimality of a modified de-biasing method of Javanmard and Montanari (2014), which allows for non-sparse precision matrix in the design. Zhang and Cheng (2016) and Dezeure, Bühlmann and Zhang (2016) evaluate approximating the overall level of significance for simultaneous testing of model parameters. They demonstrate that the multiplier bootstrap of Chernozhukov, Chetverikov and Kato (2013) can accurately approximate the overall level of significance whenever the true model is sparse enough.

However, the above mentioned work requires model sparsity i.e. as and is hence too restrictive to be used in many scientific data applications (social or biological networks for example). Moreover, despite the above progress in one-sample testing, two-sample hypothesis testing has not been addressed much in the existing literature. In the context of high-dimensional two-sample comparison of means, Bai and Saranadasa (1996); Chen and Qin (2010); Lopes, Jacob and Wainwright (2011); Cai, Liu and Xia (2014) have introduced global tests to compare the means of two high-dimensional Gaussian vectors with unknown variance with and without direct sparsity in the model. Recently Cai, Liu and Xia (2013) and Li and Chen (2012) develop two-sample tests for covariance matrices of two high-dimensional vectors specifically extending the Hotelling’s statistics to high-dimensional setting, while Zhu et al. (2016) develop new spectral test that allows for block sparsity patterns. Charbonnier, Verzelen and Villers (2015) address the more general heterogeneity test but heavily relies on the direct sparsity in the model parameters. The latest effort in this direction is the work of Städler and Mukherjee (2016) where the authors extend screen-and-clean procedure of Wasserman and Roeder (2009) to the two-sample setting. The authors provide asymptotic Type I error guarantees that are only valid under sparse models. Notice that the last two methods are based on model selection and hence do not apply to dense models because, if , perfect model selection simply means including all the features (-dimensional with ).

1.3 Challenges of two-sample testing in non-sparse models

The central problem of two-sample testing with is in finding an adequate measure of comparison of the estimators between the two samples. In light of the great success in designing tests for one sample, it becomes natural to expect that the developed methods trivially apply to the two sample case. However, the situation is far from trivial when the sparsity assumption fails. Below we illustrate this problem via a specific example of dense and high-dimensional linear model.

In particular, we show that a naive extension of the powerful de-biasing procedure to the two-sample problem, fails whenever the model is dense enough. To that end, we consider a simple Gaussian design with and assume that the errors are independent with the standard Gaussian distribution, . The true parameters have non-zero elements (dense) and take the following form

| (1.4) |

where denotes a -dimensional vector of ones and is a constant.

For simplicity, we consider the “oracle” de-biasing (de-sparsifying) estimator, which is the estimator defined in Equation (5) of Van de Geer et al. (2014) except that the node-wise Lasso estimators for the precision matrices ( and ) are replaced by their true values, . We compute this “oracle” de-biasing estimators for both samples

for , where the initial estimator is the scaled Lasso estimator (Sun and Zhang (2012)) defined as

| (1.5) |

Here, is set to be , where is a constant. As discussed after Theorem 2.2 of Van de Geer et al. (2014), de-biasing principles suggest a “naive” generalization of the one-sample T-test with a test statistic of the form

A test of nominal size , would reject whenever for the critical value defined as , where and is the inverse with respect to the first argument of with

and a -dimensional Gaussian vector with mean and covariance .

Lemma 1.

Let the null hypothesis (1.3) hold. Consider de-biased estimators , with . Then, in the above setting, as

where .

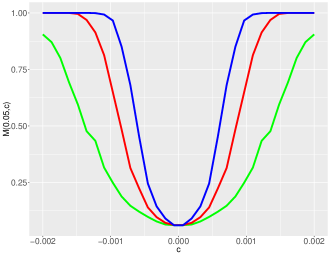

Lemma 1 establishes that under , the “naive” test has power approaching . Notice that for the naive test to be valid, we need for all . In Figure 1.1, we plot the function for several combinations of . As we can see, can be substantially larger than 0.05 and even reach one for . In other words, the probability of rejecting a true hypothesis can approach one when the model is not sparse. Hence, naively applying existing methods does not solve the two-sample testing problem in dense high-dimensional models.

1.4 Notations and Organization of the paper

Throughout this paper, ⊤ denotes the matrix transpose and denotes the identity matrix. The (multivariate) Gaussian distribution with mean (vector) and variance (matrix) is denoted by . The cumulative distribution of the standard normal distribution is denoted by . For a vector , we define its -norm as follows: for ), and , where denotes the indicator function. For matrix , its entry is denoted by , its -th row by and its -th column by . We define , where the maximum is taken over all indices. We use and to denote the maximal and minimal singular values, respectively. For two sequences , we use to denote that there exist positive constants such that , and . For two real numbers and , let and denote and , respectively. We use “s.t.” as the abbreviation for “subject to”. For two random quantities and (scalars, vectors and matrices), denotes the independence of and .

The rest of the paper is structured as follows. We develop the new methodology and the testing procedure in Section 2, where a novel ADDS estimator is also introduced. In Section 3, we develop a general theory of approximating the distribution of a large of class of test statistics with functions of Gaussian distributions. In Section 4, we derive theoretical properties of our test, such as size and power guarantees and efficiencies, and extend the results to non-Gaussian designs. In Section 5, Monte Carlo simulations are employed to assess the finite-sample performance of the proposed test. The proofs for all of the theoretical results are contained in the appendix.

2 Methodology

In this section we propose a new two-step methodology for testing in non-sparse and high-dimensional two-sample models. In the first step, we match the variables from the two samples to obtain a convolved sample, which satisfies a new model, referred to as the convolution regression model. This novel construction allows us to reformulate the hypothesis of interest (1.3) into testable moment conditions on the convolved sample. In the second step, we construct a suitable moment test by utilizing plug-in principles and self-normalization. Therefore, convolving the two-samples allows us to work directly with a specific moment constraint. This substantially simplifies the problem and facilitates the theoretical analysis in non-sparse high-dimensional models. In contrast, the traditional Wald or Score methods for testing are no longer suitable in the current context.

2.1 Constructing testable moment conditions via convolution

This section introduces the idea of constructing a convolution regression equation, which naturally generates moment conditions that are equivalent to the original null hypothesis (1.3). Throughout this section, our interest is on analyzing Gaussian designs, which are common in applications. Extensions to non-Gaussian designs are presented in Section 4.

We propose to reformulate the models (1.1) and (1.2) into a new model, in which appears as a regression coefficient, and then use it to derive a moment condition corresponding to the testing problem . Instead of naively concatenating two samples, we consider convolving the variables from the two respective samples as follows. Define the convolved response and error and and the new design matrices and as well as . With this notation at hand, (1.1) and (1.2) imply the following convolved regression model:

| (2.1) |

with unknown parameters

In the above convolved model, parameter is of main interest as the null hypothesis in (1.3) is equivalent to

Due to the high-dimensionality and potential lack of sparsity in and , we cannot simply estimate and and test . In order to construct a number of testable moment restrictions, we use the conditioning information between and . Namely, we introduce the following parameter

describing correlation between the column and the design matrix . In the case of Gaussian designs parameter also encodes their dependence structure. If we know then we can decouple the parameter of interest from the nuisance parameter in (2.1). In order to see that, observe that

| (2.2) |

defined for satisfies that , where . Additionally for Gaussian design we have . However, observe that can be highly dependent.

The following lemma characterizes the unknown parameter and the covariance structure of the vector of (2.2), i.e., . The proof is merely straight-forward computation and is thus omitted.

Now we illustrate how vector can be utilized to decouple from . First, observe that

where equalities hold by (2.1) and (2.2), respectively. Second, we observe that by Lemma 2, the matrix is nonsingular as long as and are nonsingular. Since , it follows that the original hypothesis holds if and only if . Therefore, the two problems are equivalent and we can proceed to test the following moment condition

| (2.3) |

We will show that this restriction allows for the construction of a highly successful test while allowing to be fully dense vector with .

2.2 Testing the moment condition (2.3)

Now we discuss the effective construction of the test. The moment condition (2.3) involves the unknown quantities and , which we replace with estimated counterparts. However, observe that the convolved model does not have the same distributional or sparsity properties as the original linear models. We do not assume consistent estimation for and the validity of our test is built upon consistent estimation of only. We start by introducing some notations.

Given the two samples and , we define a new response vector , and use a matrix , and . Furthermore, we define two new design matrices, and . We denote by the -th row of . Finally, the -th column of , and will be denoted by , and , respectively.

2.2.1 Auto-aDaptive Dantzig Selector (ADDS)

We propose a novel estimator for , which can be used to construct the test statistic. Let

| (2.4) |

where is a tuning parameter that does not depend on . Moreover, let

| (2.5) |

Our estimator for , referred to as the Auto-aDaptive Dantzig Selector (ADDS), is defined as

| (2.6) |

An advantage of the proposed estimator is that it simultaneously estimates and and is thus “scale-free”. The intuition behind the proposed ADDS is that estimation of the signal and estimation of its variance are closely related and can benefit from each other: a more accurate estimation of the variance can lead to a better signal estimation and a more accurate signal estimation can help estimate the variance better. Notice that the solution is well defined if ; when , exists and satisfies the constraint in the optimization problem (2.5). Moreover, the solution path can be computed very efficiently using algorithms such as DASSO (James, Radchenko and Lv (2009)) and the parametric simplex method (Pang, Liu and Vanderbei (2014); Vanderbei (2014)). Once the solution path is obtained, computing is only a one-dimensional optimization problem and thus can be solved efficiently.

The estimator for also takes the form of ADDS estimator and is defined as follows. For every , is defined by

| (2.7) |

and

| (2.8) |

where is a tuning parameter.

Then, the ADDS estimator of is defined as

| (2.9) |

Observe that ADDS estimator allows for adaptive and more accurate tuning of the heteroscedastic components . Another advantage of ADDS is that the structure of the ADDS allow us to derive certain properties of our test without any restrictions on the distribution of the vector . We relegate further discussions of ADDS for the Section 4.1.

2.2.2 A new test statistics

In this section we propose a new test statistics and a new simulation method to obtain its critical value.

We develop a test statistic for testing (1.3) as a scale-adjusted estimator of the moment condition (2.3) that requires estimates of and . For and defined in (2.9) and (2.6), we define our test statistic

| (2.10) |

with defined as

The value of tends to be moderate when is true, and large when is false. Therefore, our test is to reject in favor of if is “too large.” Observe that the distribution of the test statistic is difficult to obtain due to the complicated dependencies between different entries of . However, we propose a new plug-in Gaussian approximation method that automatically takes into account such inter-dependence and the high-dimensionality. The critical value is defined as the pre-specified quantile of the norm of a zero-mean Gaussian vector with known covariance matrix and is thus easy to compute by simulation.

Under , the behavior of the test statistic can be analyzed through the following decomposition

where ,

and with

As we will show in the proof,

and the behavior of is driven by .

Our approximation procedure is rooted in the implicit independence in the linear approximation term , where is the -th entry of and is the -th row of . Suppose that (1.3) holds. Notice that is independent of by construction and that we purposely constructed ADDS estimator as a function of only. Therefore, is independent of . Because of this independence,

| (2.11) |

where

Observe that covariance matrix is an unknown nuisance parameter in approximating the distribution of with . Per Lemma 2, is a positive-definite matrix of growing dimensions. We propose to construct , an estimator for , and then use a plug-in approach for the critical value by simulating the distribution of . We consider a natural estimator

| (2.12) |

where is the -th row of . In Section 3, we develop a general approximation theory that does not depend on the specific form of , as long as it is a sufficiently good estimator of . For the ease of presentation, we introduce the function with . Notice that for a given matrix , can be easily computed via simulation. We summarize our method in Algorithm 1.

Remark 1.

Notice that we assume the Gaussianity of and thus the distribution of is exactly Gaussian. The above setup is more general in that it also applies when the Gaussianity of fails. See Section 4.6 for details.

The methodology for our approximation when the null hypothesis prevails closely parallels that for construction of critical values in classical statistics, in which the limiting distribution of the test statistics can be derived but contains unknown nuisance parameters. In low-dimensional problems it is common to resort to a plug-in principle where the nuisance parameter is replaced by its consistent estimate. In this paper, we deal with high-dimensional problems for which the extreme dimensionality renders the classical central limit theorems non applicable and poses challenges in deriving accurate approximations of the distributions of test statistics. With recent advances in high-dimensional central limit theorem (see Chernozhukov, Chetverikov and Kato (2013) for example), we are able to generalize the classical plug-in method to the high-dimensional settings.

3 A high-dimensional plug-in principle

Many test statistics related to ratios, correlation and regression coefficients in statistics may be expressed as a nonlinear function of the vector of population quantities. Additionally, in high-dimensional setting test statistics often take the form of the maximum of a large number of random quantities , with . Individual ’s can be studentized t-statistics, such as in Dezeure, Bühlmann and Zhang (2016), or simply the difference between a parameter and its estimator, such as in Zhang and Cheng (2016). Studying asymptotic distribution of such non-linear quantities is extremely difficult. However, linearization may prove to be a useful technique. Linearization decomposes a test statistic of interest into a linear term and an approximation error:

In display above we consider with and .

In this section, we propose a general method of computing the critical value of the test statistic . This method is simple to implement and applies to a wide range of problems for which the above decomposition holds. The method is based on Gaussian approximations, as they enable easy approximations by simulation. Apart from high-dimensionality, the challenge is the presence of the approximation error and the fact that the linear terms are often not observed, i.e. depend on unknown parameters.

To present the main result, we define the covariance matrix , where is a -algebra such that , conditional on , is independent (or weakly dependent, e.g., strong mixing) across . Moreover, we make assumptions on the structure of matrix and linearization terms.

Assumption 1.

Suppose that

(i) there exist constants such that

(ii) ;

(iii) and there exists a matrix such that .

Assumption 1(ii) states a Gaussian approximation for the partial sum . Sufficient conditions for this assumption are provided by Chernozhukov, Chetverikov and Kato (2013, 2014); see Proposition 1 in the appendix. Assumption 1(iii) is very mild and only assumes entry-wise consistency of the matrix estimator. For example, if is sub-Gaussian (Vershynin (2010)) and is observed, Bernstein’s inequality and the union bound imply that the sample covariance matrix satisfies this assumption if .

Theorem 3.

Suppose that Assumption 1 holds. Then, as

Theorem 3 states that, under the regularity conditions stated in Assumption 1, the distribution of the test statistic can be approximated by , which can be easily simulated. Notice that the multiplier bootstrap method by Chernozhukov, Chetverikov and Kato (2013, 2014), which requires explicit observations of , does not apply in our context.

4 Theoretical results

In this section we present theoretical guarantees and optimality of the test proposed in Section 2. We also consider extensions to non-Gaussian designs and present theoretical results in this setting as well. We start by deriving the theoretical properties of ADDS.

4.1 ADDS properties

Auto-aDaptive Dantzig Selector introduced in Section 2.2.1 is broadly applicable to a class of linear models where an estimator of the high-dimensional parameter is needed together with its scale. In this section we provide more details of the proposed estimator and its properties in a setup where apart from a sparsity constraint we allow for a general class of constraints as well. Our result is comparable to the Dantzig selector; see Candes and Tao (2007) and Bickel, Ritov and Tsybakov (2009).

With a slight abuse in notation, we consider a model

where is a response vector, is a design matrix, is an error of the model and is the unknown parameter of interest. Let be a mapping such that (1) for any and (2) for . We shall provide more discussion on the set later. Then a generalized ADDS is defined as

| (4.1) |

where is a tuning parameter that does not depend on the magnitude of . Then we compute

| (4.2) |

Now the ADDS estimator for is defined as

| (4.3) |

In the proposed method, the estimation starts with the framework of Dantzig selector where the tuning parameter is split into two components: a variance-tuning component and variance-free component . Variance is therefore treated as another tuning parameter and the standardized “regularization” tuning parameter is fixed at an optimal theoretical value proportional to . In practice, we can obtain by simulating , where . In the first step (4.1), we compute the solution path, which maps the variance tuning parameter to its estimate . Then in the second step (4.2), we compute an “optimal” choice for the variance tuning parameter . The ADDS is then defined as the point on the solution path corresponding to this optimal choice .

The set is introduced for a general setup, where additional constraints other than the usual Dantzig restrictions are imposed. These additional constraints are represented by the set . This set could incorporate prior knowledge of the parameter of interest, e.g., a bound for the signal-to-noise ratio represented by with some pre-specified . In case of non-Gaussian designs (see Algorithm 2), an additional constraint is placed to ensure the high-dimensional central limit theorem. Other strategies in literature, such as the square-root Lasso by Belloni, Chernozhukov and Wang (2011), the scaled Lasso by Sun and Zhang (2012) and self-tuned Dantzig selector by Gautier and Tsybakov (2013), do not have this flexibility.

Assumption 2.

There exist constants such that (i) , (ii) , (iii) , (iv) and the matrix is such that the Restricted Eigenvalue condition holds, i.e., (v)

| (4.4) |

In the usual linear regression setup, one can typically show that Assumption 2 holds with high probability. This is in line with the usual argument in high-dimensional statistics, where the conclusion often states the properties of an estimator on an event that occurs with probability close to one. Now we present the behavior of ADDS under Assumption 2.

Theorem 4.

Notice that might not always be equal to the standard deviation . In fact, is only a rough proxy of since any number in can serve as . This flexibility is especially useful for misspecified models, where is correlated with the design and is a quantity that depends on this correlation. Since defined in (2.6) does not contain , the alternative hypothesis corresponds to a misspecified regression and we shall derive the power properties by exploiting the aforementioned flexibility in the interpretation of . Due to this flexibility, it is not reasonable to expect consistent estimator for , but Theorem 4 implies that ADDS estimator can generate an estimator that automatically approaches . Under Assumption 2,

In other words, whenever , we obtain that is a consistent estimator for .

4.2 Size properties

We now turn to the properties of the introduced TIERS test while imposing extremely weak conditions when both and tend to .

Assumption 3.

Conditions (i)-(iii) of Assumption 3 are very mild. Gaussian designs are considered for the simplicity of the proofs. We study general sub-Gaussian designs in Section 4.6. Moreover, well-behaved designs with bounded eigenvalues of the covariance matrix is a common condition imposed in the literature. Finally, condition (iii) imposes column-wise sparsity of the matrix . When for , Lemma 2 implies that , regardless of the sparsity of and , hence satisfying the imposed sparsity assumption. Observe that in contrast to the existing literature we do not assume sparsity of and (or their inverses), by Lemma 2 we only require certain products to be approximately sparse, a condition that is weaker and more flexible; see Cai and Liu (2011). Our first result is on the Type I error of the introduced TIERS test.

There are two unique features of this result. Firstly, we do not assume any sparsity condition on and . This is remarkable in high dimensions with . Secondly, the result of Theorem 5 holds without imposing any restriction on the distribution of the errors and in the models (1.1) and (1.2), respectively. This surprising property is achieved by the special design of the “partial self-normalization” of the test statistic and scale-free estimation of the introduced ADDS estimator. Notice that (2.11) holds does not require any assumption on the distribution of the error terms, such as the existence of probability densities. In light of this, we show that regardless of the sparsity of and/or the distribution of , the term “partially self-normalized” by is free of scales of the error terms and has a normal distribution under (1.3). Moreover, as pointed out by de la Pena, Klass and Leung Lai (2004), self-normalization often eliminates or weakens moment assumptions.

4.3 Power properties

Due to the convolved regression model (2.1), we can assess the power properties of the TIER test by considering the following alternative hypothesis

| (4.10) |

It is clear that the difficulty of differentiating from depends on the magnitude of . We shall establish the rate for magnitude of such that our test has power approaching one; see Theorem 6. Later, we shall also show that this rate is optimal; see Theorems 7 and 8.

Assumption 4.

Let Assumption 3 hold. In addition, suppose (1) that and (2) that there exist constant such that and .

Assumption 4 is reasonably weak. It is not surprising that certain sparse structure is needed to guarantee asymptotic power of high-dimensional tests. However, we still allow for lack of sparsity structure in the model parameters and . In particular, we only require sparsity of and that the product is small. For example, if for some dense and , then and , satisfying Assumption 4. Moreover, for sparse vectors and the rate condition matches those of one-sample testing; see Van de Geer et al. (2014) and Cai and Guo (2015).

Theorem 6.

For power comparison, we consider two benchmarks in the next two sections: the most powerful test, which is infeasible, and the minimax optimality. We show that, in terms of rate for the magnitude of deviations from the null hypothesis, our test differs from the most powerful test by only a logarithm factor and achieves the minimax optimality whenever the model possesses certain sparsity properties. In this sense, our test is efficient in sparse settings and is robust to the lack of sparsity and heavy tails.

4.4 Efficiency

In the rest of the section, we assume that the data is jointly Gaussian and derive the optimal power of the likelihood-ratio test of one distribution against another. As such a test is the most powerful test for distinguishing two given distributions (Lehmann and Romano (2006)), we named it the oracle test. We proceed to show that the power of our test differs from that of the oracle test by a logarithmic factor.

Let the distribution of the data be indexed by . The probability, expectation and variance under are denoted by , and , respectively. Consider the problem of testing

versus

Theorem 7.

Let the data be jointly Gaussian. Consider the likelihood ratio test of nominal size for the above problem. Then, as , the power of the likelihood ratio test is

with

Due to the optimality of the likelihood ratio test, Theorem 7 says that there does not exist any test that has power approaching one against the alternatives where , even if , , , and are known. In the extreme sparse setting with and , Theorem 7 in turn implies that one should not expect perfect power against . On the other hand, Theorem 6 says that our test has asymptotically perfect power against when , and is sparse. In this sense, our test is nearly optimal – in terms of the magnitude of deviations from the null hypothesis, our test differs from the most powerful test up to a mere logarithm factor.

4.5 Minimax Optimality

Notice that the critical value of the above likelihood ratio test depends on in the alternative hypothesis. In practice, the value of is often unknown; in fact, the values of , , , and are usually unknown as well. We thus compare our test with a benchmark test that has guaranteed power against a class of alternative hypotheses (in terms of ).

We define

where are constants. For , we also define

We consider the problem of testing

Theorem 8.

Let . Suppose that the data is jointly Gaussian, and . Then for any test satisfying , we have

Theorem 8 says that there does not exist any test that has power against all the alternatives in for some fixed . This means that power can only be guaranteed uniformly against alternatives with deviations of magnitude of at least in terms of . Comparing with the the power that TIER test achieves in Theorem 6, the test TIER is rate-optimal when Assumption 4 holds.

4.6 Considerations for Non-Gaussian Designs

Here, we highlight the extension of the proposed methodology for non-Gaussian designs. For non-Gaussian designs, in order to better control the estimation error, we propose to augment the ADDS estimator for with an additional constraint on the size of the residuals. Namely, we define

| (4.11) |

For some tuning parameter and . Then, we compute

| (4.12) |

Now our estimator for , is defined as

| (4.13) |

4.6.1 Type I error control

Next, we present size properties for the developed test TIERS+ summarized in Algorithm 2. Such a result requires certain high-level conditions on the errors and the design, which we present below.

Assumption 5.

Here, the design matrices are allowed to be sub-Gaussian and the errors of the original models (1.1) and (1.2) are still unrestricted. The following Theorem 9 shows that TIERS+ test has asymptotically Type I-error equal to the nominal level .

Similar to Theorem 5, Theorem 9 is not based on the assumption of sparsity and does not need any assumption on the distribution of the error terms and . Theorem 9 establishes though somewhat stronger conditions on the growth of the dimension . Now, can grow with as , rather than . This can be considered as a price to pay for allowing for such weak distributional assumptions on both the errors and the designs of the models.

4.6.2 Type II error control

Now we turn to power considerations and establish asymptotically that TIERS+ is powerful as long as certain assumptions on the model structure are imposed.

Assumption 6.

Assumption 6 only imposes bounded ninth moment of the error distribution in addition to the size requirements of the model parameter (a condition needed for Gaussian designs as well – see Assumption 4).

The next result establishes asymptotic power of the TIERS+ test for a class of alternatives defined in (4.10) where .

Theorem 10.

Per Theorem 10 we conclude that TIERS+ preserves power properties similar to TIERS. In particular, whenever the model is sparse, the test achieves optimal power and does not lose efficiency compared to tests designed only for sparse models.

5 Numerical Examples

In this section we present finite-sample evidence of the accuracy of the proposed method. We consider two broad groups of examples: differential regressions and differential networks.

5.1 Differential Regressions

In all the setups, we consider and . We consider the Toeplitz design and with and . We consider two specifications for the model parameters:

-

(1)

In the sparse regime, and , i.e., ;

-

(2)

In the dense regime, with entries of being drawn from the uniform distribution on and .

The null hypothesis (1.3) corresponds to and alternative hypotheses correspond to . We also consider two specifications for the error distributions

-

(a)

In the light-tail case, and are drawn from the standard normal distribution,

-

(b)

In the heavy-tail case, and are drawn from the standard Cauchy distribution.

These different specifications will be denoted as follows: SL (for sparse and light-tail), SH (for sparse and heavy-tail), DL (for dense and light-tail) and DH (for dense and heavy-tail).

| SL | SH | DL | DH | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| -TIERS | -TIERS | -TIERS | -TIERS | ||||||||

| 0.00 | 4% | 0 | 2% | 0 | 3% | 0 | 2% | ||||

| 0.32 | 14% | 4 | 16% | 0.48 | 6% | 4 | 10% | ||||

| 0.44 | 42% | 8 | 42% | 2.16 | 44% | 8 | 40% | ||||

| 0.48 | 52% | 12 | 57% | 2.40 | 56% | 12 | 56% | ||||

| 0.52 | 67% | 16 | 67% | 2.64 | 68% | 16 | 68% | ||||

| 0.60 | 78% | 20 | 74% | 2.88 | 78% | 20 | 74% | ||||

| 0.64 | 88% | 24 | 83% | 3.12 | 85% | 24 | 82% | ||||

| 0.68 | 92% | 44 | 90% | 3.36 | 90% | 44 | 90% | ||||

| 0.72 | 96% | 68 | 93% | 3.60 | 92% | 64 | 92% | ||||

| 0.76 | 97% | 124 | 86% | 3.84 | 95% | 124 | 96% | ||||

| 0.88 | 99% | 168 | 97% | 4.08 | 98% | 168 | 97% | ||||

| 0.92 | 100% | 268 | 100% | 4.56 | 100% | 264 | 99% | ||||

| SL | SH | DL | DH | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| -TIERS | -TIERS | -TIERS | -TIERS | ||||||||

| 0.00 | 6 % | 0 | 2 % | 0 | 2 % | 0 | 6 % | ||||

| 0.44 | 7 % | 8 | 10 % | 2.16 | 9 % | 8 | 9 % | ||||

| 0.48 | 8 % | 12 | 23 % | 2.40 | 12 % | 12 | 28 % | ||||

| 0.96 | 51 % | 28 | 56 % | 3.60 | 50 % | 28 | 55 % | ||||

| 1.04 | 65 % | 48 | 69 % | 4.08 | 69 % | 44 | 67 % | ||||

| 1.16 | 78 % | 56 | 77 % | 4.32 | 79 % | 56 | 78 % | ||||

| 1.20 | 85 % | 64 | 82 % | 4.56 | 82 % | 64 | 82 % | ||||

| 1.24 | 93 % | 108 | 90 % | 5.04 | 92 % | 92 | 90 % | ||||

| 1.28 | 95 % | 140 | 93 % | 5.38 | 93 % | 136 | 92 % | ||||

| 1.32 | 96 % | 200 | 94 % | 5.76 | 96 % | 200 | 95 % | ||||

| 1.60 | 99 % | 284 | 97 % | 6.00 | 97 % | 284 | 97 % | ||||

| 1.64 | 100 % | 320 | 100 % | 6.24 | 100 % | 330 | 100 % | ||||

The summary of the results is presented in Tables 1 - 3 where the rejection probabilities are computed based on repetitions. The tuning parameter is chosen as adaptively as

We vary deviations from the null to highlight power properties as well as the Type I errors. From the tables we observe that the TIERS performs exceptionally well in both Gaussian and heavy-tailed setting for the error terms. The rejection probabilities under the null hypothesis () are close to the nominal size 5% in all the settings, as expected from our theory.

In the case of light-tailed models (SL and DL) TIERS achieves perfect power relatively quickly independent of the sparsity of the underlying model. The dense case required larger deviations from the null to reach power of one. In the case of heavy-tailed models, TIERS shows excellent performance irrespective of the sparsity of the model. In comparison with the models with light-tailed errors, the models with the heavier tails need larger deviations from the null in order to reach the same power. This is expected as the simulated Cauchy errors had an average variance of about over independent repetitions. Remarkably, dense models with heavy tailed errors performed extremely close to those of sparse models with heavy tailed errors, indicating that the heavy tails are the main driver of the power loss.

| SL | SH | DL | DH | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| -TIERS | -TIERS | -TIERS | -TIERS | ||||||||

| 0.00 | 2 % | 0 | 5 % | 0 | 4 % | 0 | 7 % | ||||

| 0.28 | 12 % | 4 | 10 % | 0.48 | 6 % | 4 | 12 % | ||||

| 0.44 | 23 % | 8 | 26 % | 2.16 | 32 % | 8 | 26 % | ||||

| 0.48 | 27 % | 12 | 48 % | 2.40 | 46 % | 12 | 47 % | ||||

| 0.52 | 36 % | 16 | 56 % | 2.64 | 56 % | 16 | 56 % | ||||

| 0.64 | 64 % | 20 | 62 % | 2.88 | 66 % | 20 | 61 % | ||||

| 0.72 | 75 % | 32 | 74 % | 3.12 | 77 % | 32 | 74 % | ||||

| 0.80 | 85 % | 72 | 86 % | 3.36 | 85 % | 72 | 86 % | ||||

| 0.84 | 91 % | 124 | 92 % | 3.60 | 91 % | 124 | 92 % | ||||

| 0.92 | 97 % | 160 | 95 % | 3.84 | 95 % | 180 | 9 % | ||||

| 1.04 | 99 % | 244 | 97 % | 4.32 | 97 % | 244 | 97 % | ||||

| 1.20 | 100 % | 288 | 100 % | 4.80 | 100 % | 288 | 99 % | ||||

5.2 Differential Networks

We consider two independent Gaussian graphical models, where and . The goal is to conduct inference on the first row of the precision matrices by testing

We consider the follow specification

Notice that we can write the model in the regression form: and , where and are the error terms. Therefore, it is equivalent to testing

We set and

As in the linear case, represents the deviations from the null hypothesis and corresponds to the null hypothesis. We consider two cases for :

-

1.

In the sparse case, .

-

2.

In the dense case, with entries of being drawn from the uniform distribution on .

We consider two regimes for : sparse regime and dense regime.

-

(a)

For the sparse regime, we follow Ren et al. (2015) by setting , where is block diagonal with , and on the diagonal. Here, , and . For , we set , and , where , and .

-

(b)

For the dense regime, we set .

It is worth pointing out that no existing method applies to the setting of , i.e. the setting of large-scale and dense graphical models. The results are summarized in Table 4, where four cases are considered: S+S (for sparse and sparse ), D+S (for dense and sparse ), S+D (for sparse and dense ) and D+D (for dense and dense ).

In both sparse and dense settings, TIER performs well in terms of (1) controlling the size for and (2) exhibiting power against alternatives . As should be expected, TIER has better power in sparse specifications than in dense specifications, although the power eventually reaches on in all the settings.

| S+S | D+S | S+D | D+D | ||

|---|---|---|---|---|---|

| 0.00 | 5% | 3% | 0.00 | 5% | 7% |

| 0.48 | 14% | 11% | 1.68 | 15% | 5% |

| 0.52 | 21% | 13% | 1.82 | 30% | 6% |

| 0.60 | 35% | 25% | 1.96 | 41% | 8% |

| 0.72 | 59% | 51% | 2.10 | 53% | 8% |

| 0.84 | 76% | 71% | 2.38 | 69% | 15% |

| 0.88 | 81% | 77% | 2.66 | 78% | 25% |

| 0.92 | 84% | 82% | 3.78 | 89% | 69% |

| 0.96 | 88% | 88% | 3.92 | 90% | 69% |

| 1.08 | 94% | 97% | 5.00 | 96% | 92% |

| 1.44 | 99% | 99% | 7.00 | 98% | 95% |

| 1.60 | 100% | 100% | 8.00 | 100% | 100% |

Conclusions and discussions

We have presented a framework for performing inference on the equivalence of the coefficients vectors between two linear regression models. We show that the rejection probability of the proposed tests under the null hypothesis converges to the nominal size under extremely weak conditions: (1) no assumption on the structure or sparsity of the coefficient vector and (2) no assumption on the error distribution. If the features in the two samples have the same variance matrix, then our result does not require any assumption on the feature covariance either. To the best of our knowledge, this is the first result for two-sample testing in the high-dimensional setting that is robust to the failure of the model sparsity and thus is truly novel. Moreover, we establish both efficiency and optimality of our procedure. Applying this framework to performing inference on differential regressions and differential networks, we obtain new procedures of constructing accurate inferences in situations not previously addressed in the literature.

Our work also opens doors to new research areas in statistics. In terms of methodology, our work exploits the implication of the null hypothesis and can be extended to other inference problems. For example, it is practically important to extend our method to the high-dimensional ANCOVA problems, where the hypothesis of interest involves equivalence of parameters in multiple samples. Another extension is the inference of partial equivalence. Consider the problem of two or more samples generated by linear models, where the goal is to test the hypothesis that certain components in the model parameter are identical in the two samples. One important application is specification tests in large-scale models. Suppose that the data is collected from many different sources and contain several subgroups of observations. A common approach of extracting information from these datasets is to assume that all the subgroups are generated from linear models but these different subgroups share the same values in certain entries of the model parameters. Numerous methods have been developed in order to estimate the common components. However, as far as we know, no work exists that can be used to verify whether it is reasonable to assume common components. Our work can be further extended to provide simple tests for the specification of the common parameter values.

Appendix A Sufficient condition of Gaussian approximation in high dimensions

For the reader’s convenience, we state the following result that applies to the conditional probability measure . This result can be used to verify assumption (ii) of Theorem 3.

Proposition 1 (Proposition 2.1 of Chernozhukov, Chetverikov and Kato (2014)).

Let be a sequence of random vectors in such that, conditional on some -algebra , is independent across and has zero mean. Let . Suppose that

-

(i)

there exists a constant such that .

-

(ii)

there exists a sequence of -measurable random variables such that , and .

-

(iii)

either (1) or

(2) for some and .

Then, when and , we have

Appendix B Proof of Lemma 1

Proof of Lemma 1.

Let and

and define the event ,

where

for . We proceed in two steps: (1) show the result assuming and (2) show .

Step 1: show the result assuming .

Let and

For , on the event , the trivial estimator satisfies the KKT optimality conditions of the scaled Lasso optimization (1.5):

where denotes the -th entry of , denotes the -th column of and is the sign function defined by for and . Therefore, on the event , a trivial solution of all zeros is a scaled Lasso solution, i.e. . Since (by (1.3)), we have that, on the event ,

Since , we have

| (B.1) |

Notice that, conditional on , is Gaussian with mean and variance .

Therefore,

is the conditional distribution function of

.

Thus, the desired result follows by (B.1).

Step 2: show .

We show . Recall that . Let . For simplicity, we drop the subscript and write , and , instead of , and . Moreover, for , we define as the -th column of and

Notice that and for any . Let be a constant satisfying ; this is possible since is a constant.

Observe that

with . Since is the average of independent random variables, the classical central limit theorem implies that

This means that

Since is also the average of independent random variables, which are sub-exponential, the Bernstein’s inequality and the union bound imply that, there exists a constant such that

Hence, with

| (B.2) |

Conditional on , is Gaussian with mean zero and variance , where . Recall the elementary inequality that for and , . It follows that

B.1 Proof of Theorem 3

Proof of Theorem 3.

For notational convenience, we denote by by . Let . We proceed in two steps, where we show that (1) can be approximated by and (2) can be approximated by . Since , we have that

| (B.6) |

Step 1: show that can be approximated by .

Fix an arbitrary and define . Let , and . By assumption, . Let . Notice that

| (B.7) | |||||

where holds by the definition of . Therefore,

| (B.8) | |||

where follows by Lemma 17 and the definition of , follows by (B.7) and follows by Lemma 18. It follows that, ,

where holds by and : since and is bounded (hence uniformly integrable), Theorem 5.4 on page 220 of Gut (2012) implies . Since is arbitrary, we have

By the Markov’s inequality,

| (B.9) |

Step 2: show that can be approximated by .

Let , where is the -algebra generated by and . Let and . Hence, we have that

| (B.10) |

B.2 Proof of Theorem 4

Proof of Theorem 4.

The arguments are similar to the proof of Theorem 7.2 of Bickel, Ritov and Tsybakov (2009). Let , and . Here, for any vector , we define . The proof proceeds in two steps. In the first step, we show that ; in the second step, we show the desired results.

Step 1: show

Since and , we have and thus . It follows, by the triangular inequality, that

| (B.12) | ||||

| (B.13) |

Since and , the triangular inequality implies that . Then

where follows by (B.13) and follows by Holder’s inequality. By (4.4) and (B.13), . Therefore, the above display implies that

| (B.14) |

and

| (B.15) |

Step 2: show the desired results

Recall and define . By (B.16), we have and thus (by the property of for ), implying that . By construction, the mapping is non-increasing. It follows that . Recall from Step 1, we have that . Therefore,

which means that and thus . It follows, by the triangular inequality, that

| (B.17) |

Since and , we have that

| (B.18) |

Hence,

| (B.19) |

where follows by Holder’s inequality, follows by (B.17) and (B.18) and follows by Holder’s inequality. By (4.4) and (B.17), we have . This and (B.19) imply that

| (B.20) |

and thus

| (B.21) |

Since , it follows that

| (B.23) |

By the definition of (4.2), . We have proved claim (4.5). We prove claim (4.6) by combining (B.21) and (B.23). We obtain claim (4.7) by noticing that

where follows by (B.17), follows by Holder’s inequality, follows by (B.20) and follows by (B.23).

B.3 Proof of Theorem 5

We introduce some notations that will be used in the rest of the paper. Let with . Let .

Proof of Lemma 11.

Define the event with

Since and entries of have bounded sub-exponential norms (due to the sub-Gaussian property of and ), it follows, by Bernstein’s inequality and the union bound, that . Moreover, by Theorem 6 in Rudelson and Zhou (2013), the restricted eigenvalue condition in (4.4) (with ) holds for some constant with probability approaching one. It follows, by Theorem 4, that

and

This proves part (1). Observe that

where and follow by (2.4) and (2.5), respectively. Part (2) follows by Holder’s inequality:

The proof is complete.∎

Proof of Lemma 12.

Notice that

| (B.24) | |||||

We bound both terms separately. Since entries in are Gaussian with bounded variance, the entries in have sub-exponential norms bounded above by some constant . It follows, by Proposition 5.16 of Vershynin (2010), that ,

where is a universal constant. Therefore, by taking , we have

| (B.25) |

Proof of Theorem 5.

Consider the test statistic (2.10). Assume that (1.3) is true. We observe the following decomposition:

| (B.27) |

where

We invoke Theorem 3 to obtain the desired result.

Let denote the -algebra generated by and . Notice that under ,

due to (2.1). Since is a function of (and thus a function of and ), is a function of and . Notice that is independent of . It follows, by the Gaussianity of and , that

where . In other words,

Therefore, we have verified all the assumptions of Theorem 3, which then implies the desired result. ∎

B.4 Proof of Theorem 6

Lemma 13.

Proof of Lemma 13.

Notice that the entries of are i.i.d random variables that are independent of . We apply Lemma 19 with , and for . It follows that

Notice that is the average of independent random variables. By the law of large numbers, . Therefore,

with probability approaching one. The proof is complete. ∎

Proof of Theorem 6.

By (2.1) and (2.2), we have that . We apply Theorem 4 with and . Notice that, by Theorem 6 in Rudelson and Zhou (2013), the restricted eigenvalue condition in (4.4) holds for some constant with probability approaching one. Also notice that

Thus, by Theorem 4 and Lemma 13, together with , it follows that, with probability approaching one,

| (B.28) |

where . Let satisfy that , where is the th column of .

Step 1: derive the behavior of the test statistic.

By the triangular inequality, we have

| (B.29) | ||||

Notice that

| (B.30) |

where follows by Holder’s inequality, follows by (due to Lemma 11) and (B.28)(3) and holds by .

Since has bounded sub-Gaussian norms, the law of large numbers implies that and hence

for any constant . By the sub-Gaussian property of , we apply Lemma 19 (with and for ). It follows that

By Holder’s inequality and (B.28)(2), it follows that

| (B.31) |

where holds by .

Notice that is bounded by a constant , where is the constant in Assumption 4. The Lyapunov’s central limit theorem implies that

Hence,

| (B.32) |

where holds by (B.28)(1).

Due to the (sub)-Gaussian property of and the definition of , is bounded above by a constant. Again, the Lyapunov’s central limit theorem implies that

Hence, it follows, by (B.28)(1), that

| (B.33) |

Therefore, for any ,

where holds by (B.29) and the sub-additivity of probability measures, holds by (B.30), (B.31) and (B.32), holds by (B.33) and holds by (B.28)(1). Recall that

Therefore, there exist constants such that

Hence, the above display implies that for any ,

| (B.34) |

Step 2: derive the behavior of the critical value.

Recall the elementary inequality that for , for all . By the union bound, we have that

where . It follows that, ,

Let be a constant such that . By Lemma 12, . Hence,

| (B.35) |

Let . Notice that for large ,

Then the desired result holds with and . The proof is complete. ∎

B.5 Proof of Theorems 7 and 8

Proof of Theorem 7.

Let

and

Let with and . The proof proceeds in two steps. First, we characterize the test statistic and the critical value; second, we derive the behavior of the test statistic under .

Step 1: characterize the test statistic and the critical value.

Notice that the log likelihood under is

where

The log likelihood under is

where

Notice that and thus the likelihood ratio test can be written with the test statistic being

| (B.36) |

where

Let be the critical value for a test of nominal size , i.e., .

Notice that, under ,

By the Gaussian assumption, we have

By the Lyapunov’s central limit theorem applied to , we have that

| (B.37) |

By (B.36), we have

where follows by (B.37) and Polya’s theorem (Theorem 9.1.4 of Athreya and Lahiri (2006)). Therefore,

| (B.38) |

Step 2: behavior of the test statistic under .

Notice that, under ,

Similarly as before, we have that

Proof of Theorem 8.

Let be a test such that . Define

with , and . For , let

where is the th column of , and . Define

Lemma 2 implies that . Then and with . Notice that

| (B.39) | ||||

where holds by , holds by , holds by and follows by Lyapunov’s inequality.

By Step 1 of the proof of Theorem 7, we have that

| (B.40) |

By the moment generating function (MGF) of Gaussian distributions, and thus

| (B.41) |

Similarly, we also have . Since

it follows, by and the MGF of chi-squared distributions, that

| (B.42) |

Next, observe

| (B.43) |

where follows by the Gaussian MGF and the fact that

is Gaussian with mean and variance

Notice that, for , and are independent Gaussian random variables since is diagonal. Hence, for ,

| (B.45) |

where follows by Gaussian MGF and the definition of s and follows by

chi-squared MGF and the definition of s. We combine (B.43) and (B.45), obtaining

| (B.46) |

Since , we have that . Therefore,

Recall the fact that if , then . Since , we have

Thus, (B.46) and the above two displays imply that

By (B.41), we have that . By (B.39) and (B.40), it follows that

The proof is complete. ∎

B.6 Proof of Theorems 9 and 10

Lemma 14.

Let be a random variable. Suppose that there exists a constant such that . Then , where .

Proof of Lemma 14.

Let . Since , we have the decomposition

Define the sequence of constants

By Fubini’s theorem,

| (B.47) |

where follows by and follows by the elementary inequality that

for . Notice that, for ,

where holds by and holds by the definition of in the statement of the lemma. The above display implies that, ,

It follows, by (B.47), that

It can be shown that . Thus, . ∎

Proof of Lemma 15.

Part (1) follows the same argument as the proof of part(1) in Lemma 11 since changing the distribution of and from Gaussian to sub-Gaussian does not affect the arguments.

Proof of Theorem 9.

The argument is similar to the proof of Theorem 5, except that we need to invoke a high-dimensional central limit theorem under non-Gaussian designs. We proceed in two steps. First, we show the desired result assuming a “central limit theorem” (stated below in (B.52)) and then we show the “central limit theorem”.

Step 1: show the desired result assuming a “central limit theorem”

Consider the test statistic (4.14). Assume that (1.3) is true. Then

| (B.48) | ||||

| (B.49) |

where

and with . Let be the -algebra generated by and .

Since and are computed using only and , which, under (1.3), are independent of , it follows that

By , we have . By Assumption 5 and Lemma 2, there exist constant constants such that

| (B.50) |

We prove the result assuming the following claim, which is proved afterwards:

| (B.52) |

We apply Theorem 3 to the decomposition (B.49). From (B.51), (B.50) and (B.52), all the assumptions of Theorem 3 are satisfied. Therefore, the desired result follows by Theorem 3.

Step 2: show the “central limit theorem”

It remains to prove the claim in (B.52). To this end, we invoke Proposition 1. Hence, we only need to verify the following conditions.

-

(a)

There exists a constant such that .

-

(b)

There exists a sequence of -measurable random variables such that , and .

-

(c)

.

Notice that Condition (a) follows by (B.50) and . To show the other two conditions, notice that, by the constraints (4.11) and (4.12), and . Therefore,

| (B.53) |

Since has a bounded sub-Gaussian norm, there exists a constant such that and , and . By the sub-Gaussian property and Lemma 14, there exists a constant such that . We define

| (B.54) |

By (B.53), we have that

Lemma 16.

Proof of Lemma 16.

Let . Then . By the law of large numbers, . Hence,

Since and entries of have sub-Gaussian norms bounded above by some constant , we can apply Lemma 19 (with and for ). It follows that

where is a constant depending only on . To see , first notice that, by Minkowski’s inequality and the bounded ninth moment of , there exists a constant such that

Therefore, there exists a constant such that

| (B.55) |

where follows by Markov’s inequality and holds by the definition of and the fact that eigenvalues of is bounded away from zero (due to Lemma 2). Hence,

where holds by (B.55) and holds by for (here ). The proof is complete. ∎

B.7 Technical tools

Lemma 17.

Let and be two random vectors. Then ,

Proof of Lemma 17.

By the triangular inequality, we have

and

The above two display imply that

The result follows by noticing that

∎

Lemma 18.

Let be a random vector and a -algebra. If , is Gaussian and almost surely for some constant , then there exists a constant depending only on such that .

Proof of Lemma 18.

By Nazarov’s anti-concentration inequality (Lemma A.1 in Chernozhukov, Chetverikov and Kato (2014)), there exists a constant depending only on such that almost surely,

Since , the desired result follows by

∎

Lemma 19.

Let and be two sequences of random vectors in that are independent across . Suppose that and are also independent and that there exist constants such that , the sub-Gaussian norm of is bounded above by and .

Then, if , then there exists a constant depending only on such that

References

- Allan et al. (2001) {barticle}[author] \bauthor\bsnmAllan, \bfnmJames M.\binitsJ. M., \bauthor\bsnmWild, \bfnmChristopher P.\binitsC. P., \bauthor\bsnmRollinson, \bfnmSara\binitsS., \bauthor\bsnmWillett, \bfnmEleanor V.\binitsE. V., \bauthor\bsnmMoorman, \bfnmAnthony V.\binitsA. V., \bauthor\bsnmDovey, \bfnmGareth J.\binitsG. J., \bauthor\bsnmRoddam, \bfnmPhilippa L.\binitsP. L., \bauthor\bsnmRoman, \bfnmEve\binitsE., \bauthor\bsnmCartwright, \bfnmRaymond A.\binitsR. A. and \bauthor\bsnmMorgan, \bfnmGareth J.\binitsG. J. (\byear2001). \btitlePolymorphism in glutathione S-transferase P1 is associated with susceptibility to chemotherapy-induced leukemia. \bjournalProceedings of the National Academy of Sciences \bvolume98 \bpages11592-11597. \bdoi10.1073/pnas.191211198 \endbibitem

- Athreya and Lahiri (2006) {bbook}[author] \bauthor\bsnmAthreya, \bfnmKrishna B\binitsK. B. and \bauthor\bsnmLahiri, \bfnmSoumendra N\binitsS. N. (\byear2006). \btitleMeasure Theory and Probability Theory. \bpublisherSpringer Science & Business Media. \endbibitem

- Bai and Saranadasa (1996) {barticle}[author] \bauthor\bsnmBai, \bfnmZ. D.\binitsZ. D. and \bauthor\bsnmSaranadasa, \bfnmHewa\binitsH. (\byear1996). \btitleEffect of high dimension: by an example of a two sample problem. \bjournalStatistica Sinica \bvolume6 \bpages311–329. \endbibitem

- Belloni, Chernozhukov and Wang (2011) {barticle}[author] \bauthor\bsnmBelloni, \bfnmAlexandre\binitsA., \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV. and \bauthor\bsnmWang, \bfnmLie\binitsL. (\byear2011). \btitleSquare-root lasso: pivotal recovery of sparse signals via conic programming. \bjournalBiometrika \bvolume98 \bpages791–806. \endbibitem

- Bickel, Ritov and Tsybakov (2009) {barticle}[author] \bauthor\bsnmBickel, \bfnmPeter J\binitsP. J., \bauthor\bsnmRitov, \bfnmYaácov\binitsY. and \bauthor\bsnmTsybakov, \bfnmAlexandre B\binitsA. B. (\byear2009). \btitleSimultaneous analysis of Lasso and Dantzig selector. \bjournalThe Annals of Statistics \bvolume37 \bpages1705–1732. \endbibitem

- Bühlmann (2013) {barticle}[author] \bauthor\bsnmBühlmann, \bfnmP.\binitsP. (\byear2013). \btitleStatistical significance in high-dimensional linear models. \bjournalBernoulli \bvolume19 \bpages1212–1242. \endbibitem

- Cai and Guo (2015) {barticle}[author] \bauthor\bsnmCai, \bfnmT Tony\binitsT. T. and \bauthor\bsnmGuo, \bfnmZijian\binitsZ. (\byear2015). \btitleConfidence intervals for high-dimensional linear regression: Minimax rates and adaptivity. \bjournalarXiv preprint arXiv:1506.05539. \endbibitem

- Cai and Liu (2011) {barticle}[author] \bauthor\bsnmCai, \bfnmTony\binitsT. and \bauthor\bsnmLiu, \bfnmWeidong\binitsW. (\byear2011). \btitleA Direct Estimation Approach to Sparse Linear Discriminant Analysis. \bjournalJournal of the American Statistical Association \bvolume106 \bpages1566–1577. \endbibitem

- Cai, Liu and Xia (2013) {barticle}[author] \bauthor\bsnmCai, \bfnmTony\binitsT., \bauthor\bsnmLiu, \bfnmWeidong\binitsW. and \bauthor\bsnmXia, \bfnmYin\binitsY. (\byear2013). \btitleTwo-Sample Covariance Matrix Testing and Support Recovery in High-Dimensional and Sparse Settings. \bjournalJournal of the American Statistical Association \bvolume108 \bpages265-277. \endbibitem

- Cai, Liu and Xia (2014) {barticle}[author] \bauthor\bsnmCai, \bfnmTony\binitsT., \bauthor\bsnmLiu, \bfnmWeidong\binitsW. and \bauthor\bsnmXia, \bfnmYin\binitsY. (\byear2014). \btitleTwo-sample test of high dimensional means under dependence. \bjournalJournal of the Royal Statistical Society: Series B (Statistical Methodology) \bvolume76 \bpages349–372. \bdoi10.1111/rssb.12034 \endbibitem

- Candes and Tao (2007) {barticle}[author] \bauthor\bsnmCandes, \bfnmEmmanuel\binitsE. and \bauthor\bsnmTao, \bfnmTerence\binitsT. (\byear2007). \btitleThe Dantzig selector: statistical estimation when p is much larger than n. \bjournalThe Annals of Statistics \bvolume35 \bpages2313–2351. \endbibitem

- Charbonnier, Verzelen and Villers (2015) {barticle}[author] \bauthor\bsnmCharbonnier, \bfnmCamille\binitsC., \bauthor\bsnmVerzelen, \bfnmNicolas\binitsN. and \bauthor\bsnmVillers, \bfnmFanny\binitsF. (\byear2015). \btitleA global homogeneity test for high-dimensional linear regression. \bjournalElectronic Journal of Statistics \bvolume9 \bpages318–382. \bdoi10.1214/15-EJS999 \endbibitem

- Chen and Qin (2010) {barticle}[author] \bauthor\bsnmChen, \bfnmSong Xi\binitsS. X. and \bauthor\bsnmQin, \bfnmYing-Li\binitsY.-L. (\byear2010). \btitleA two-sample test for high-dimensional data with applications to gene-set testing. \bjournalThe Annals of Statistics \bvolume38 \bpages808–835. \bdoi10.1214/09-AOS716 \endbibitem

- Chernozhukov, Chetverikov and Kato (2013) {barticle}[author] \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV., \bauthor\bsnmChetverikov, \bfnmDenis\binitsD. and \bauthor\bsnmKato, \bfnmKengo\binitsK. (\byear2013). \btitleGaussian approximations and multiplier bootstrap for maxima of sums of high-dimensional random vectors. \bjournalThe Annals of Statistics \bvolume41 \bpages2786–2819. \endbibitem

- Chernozhukov, Chetverikov and Kato (2014) {barticle}[author] \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV., \bauthor\bsnmChetverikov, \bfnmDenis\binitsD. and \bauthor\bsnmKato, \bfnmKengo\binitsK. (\byear2014). \btitleCentral limit theorems and bootstrap in high dimensions. \bjournalarXiv preprint arXiv:1412.3661. \endbibitem

- de la Pena, Klass and Leung Lai (2004) {barticle}[author] \bauthor\bparticlede la \bsnmPena, \bfnmVictor H.\binitsV. H., \bauthor\bsnmKlass, \bfnmMichael J.\binitsM. J. and \bauthor\bsnmLeung Lai, \bfnmTze\binitsT. (\byear2004). \btitleSelf-normalized processes: exponential inequalities, moment bounds and iterated logarithm laws. \bjournalThe Annals of Probability \bvolume32 \bpages1902–1933. \bdoi10.1214/009117904000000397 \endbibitem

- Dezeure, Bühlmann and Zhang (2016) {barticle}[author] \bauthor\bsnmDezeure, \bfnmRuben\binitsR., \bauthor\bsnmBühlmann, \bfnmPeter\binitsP. and \bauthor\bsnmZhang, \bfnmCun-Hui\binitsC.-H. (\byear2016). \btitleHigh-dimensional simultaneous inference with the bootstrap. \bjournalarXiv preprint arXiv:1606.03940. \endbibitem

- Dezeure et al. (2015) {barticle}[author] \bauthor\bsnmDezeure, \bfnmRuben\binitsR., \bauthor\bsnmBühlmann, \bfnmPeter\binitsP., \bauthor\bsnmMeier, \bfnmLukas\binitsL. and \bauthor\bsnmMeinshausen, \bfnmNicolai\binitsN. (\byear2015). \btitleHigh-Dimensional Inference: Confidence Intervals, p-Values and R-Software hdi. \bjournalStatistical Science \bvolume30 \bpages533–558. \endbibitem

- Fan and Li (2001) {barticle}[author] \bauthor\bsnmFan, \bfnmJianqing\binitsJ. and \bauthor\bsnmLi, \bfnmRunze\binitsR. (\byear2001). \btitleVariable selection via nonconcave penalized likelihood and its oracle properties. \bjournalJournal of the American statistical Association \bvolume96 \bpages1348–1360. \endbibitem

- Fan and Lv (2011) {barticle}[author] \bauthor\bsnmFan, \bfnmJianqing\binitsJ. and \bauthor\bsnmLv, \bfnmJinchi\binitsJ. (\byear2011). \btitleNonconcave Penalized Likelihood With NP-Dimensionality. \bjournalIEEE Transactions on Information Theory \bvolume57 \bpages5467–5484. \endbibitem

- Fan and Peng (2004) {barticle}[author] \bauthor\bsnmFan, \bfnmJianqing\binitsJ. and \bauthor\bsnmPeng, \bfnmHeng\binitsH. (\byear2004). \btitleNonconcave penalized likelihood with a diverging number of parameters. \bjournalThe Annals of Statistics \bvolume32 \bpages928–961. \bdoi10.1214/009053604000000256 \endbibitem

- Gautier and Tsybakov (2013) {bincollection}[author] \bauthor\bsnmGautier, \bfnmEric\binitsE. and \bauthor\bsnmTsybakov, \bfnmAlexandre B\binitsA. B. (\byear2013). \btitlePivotal estimation in high-dimensional regression via linear programming. In \bbooktitleEmpirical Inference \bpages195–204. \bpublisherSpringer. \endbibitem

- Gut (2012) {bbook}[author] \bauthor\bsnmGut, \bfnmAllan\binitsA. (\byear2012). \btitleProbability: a graduate course \bvolume75. \bpublisherSpringer Science & Business Media. \endbibitem

- James, Radchenko and Lv (2009) {barticle}[author] \bauthor\bsnmJames, \bfnmGareth M\binitsG. M., \bauthor\bsnmRadchenko, \bfnmPeter\binitsP. and \bauthor\bsnmLv, \bfnmJinchi\binitsJ. (\byear2009). \btitleDASSO: connections between the Dantzig selector and lasso. \bjournalJournal of the Royal Statistical Society: Series B (Statistical Methodology) \bvolume71 \bpages127–142. \endbibitem

- Javanmard and Montanari (2014) {barticle}[author] \bauthor\bsnmJavanmard, \bfnmAdel\binitsA. and \bauthor\bsnmMontanari, \bfnmAndrea\binitsA. (\byear2014). \btitleConfidence intervals and hypothesis testing for high-dimensional regression. \bjournalThe Journal of Machine Learning Research \bvolume15 \bpages2869–2909. \endbibitem

- Javanmard and Montanari (2015) {barticle}[author] \bauthor\bsnmJavanmard, \bfnmAdel\binitsA. and \bauthor\bsnmMontanari, \bfnmAndrea\binitsA. (\byear2015). \btitleDe-biasing the Lasso: Optimal Sample Size for Gaussian Designs. \bjournalarXiv preprint arXiv:1508.02757. \endbibitem

- Lehmann and Romano (2006) {bbook}[author] \bauthor\bsnmLehmann, \bfnmErich L\binitsE. L. and \bauthor\bsnmRomano, \bfnmJoseph P\binitsJ. P. (\byear2006). \btitleTesting statistical hypotheses. \bpublisherSpringer Science & Business Media. \endbibitem

- Li and Chen (2012) {barticle}[author] \bauthor\bsnmLi, \bfnmJun\binitsJ. and \bauthor\bsnmChen, \bfnmSong Xi\binitsS. X. (\byear2012). \btitleTwo sample tests for high-dimensional covariance matrices. \bjournalThe Annals of Statistics \bvolume40 \bpages908–940. \bdoi10.1214/12-AOS993 \endbibitem

- Lopes, Jacob and Wainwright (2011) {bincollection}[author] \bauthor\bsnmLopes, \bfnmMiles\binitsM., \bauthor\bsnmJacob, \bfnmLaurent\binitsL. and \bauthor\bsnmWainwright, \bfnmMartin J\binitsM. J. (\byear2011). \btitleA More Powerful Two-Sample Test in High Dimensions using Random Projection. In \bbooktitleAdvances in Neural Information Processing Systems 24 (\beditor\bfnmJ.\binitsJ. \bsnmShawe-Taylor, \beditor\bfnmR. S.\binitsR. S. \bsnmZemel, \beditor\bfnmP. L.\binitsP. L. \bsnmBartlett, \beditor\bfnmF.\binitsF. \bsnmPereira and \beditor\bfnmK. Q.\binitsK. Q. \bsnmWeinberger, eds.) \bpages1206–1214. \bpublisherCurran Associates, Inc. \endbibitem

- Mandozzi and Bühlmann (2016) {barticle}[author] \bauthor\bsnmMandozzi, \bfnmJacopo\binitsJ. and \bauthor\bsnmBühlmann, \bfnmPeter\binitsP. (\byear2016). \btitleHierarchical testing in the high-dimensional setting with correlated variables. \bjournalJournal of the American Statistical Association \bvolume11 \bpages331–343. \endbibitem

- Meinshausen and Bühlmann (2006) {barticle}[author] \bauthor\bsnmMeinshausen, \bfnmNicolai\binitsN. and \bauthor\bsnmBühlmann, \bfnmPeter\binitsP. (\byear2006). \btitleHigh-dimensional graphs and variable selection with the lasso. \bjournalThe Annals of Statistics \bvolume34 \bpages1436–1462. \endbibitem

- Meinshausen, Meier and Bühlmann (2009) {barticle}[author] \bauthor\bsnmMeinshausen, \bfnmNicolai\binitsN., \bauthor\bsnmMeier, \bfnmLukas\binitsL. and \bauthor\bsnmBühlmann, \bfnmPeter\binitsP. (\byear2009). \btitlep-Values for High-Dimensional Regression. \bjournalJournal of the American Statistical Association \bvolume104 \bpages1671–1681. \endbibitem

- Pang, Liu and Vanderbei (2014) {barticle}[author] \bauthor\bsnmPang, \bfnmHaotian\binitsH., \bauthor\bsnmLiu, \bfnmHan\binitsH. and \bauthor\bsnmVanderbei, \bfnmRobert J\binitsR. J. (\byear2014). \btitleThe fastclime package for linear programming and large-scale precision matrix estimation in R. \bjournalJournal of Machine Learning Research \bvolume15 \bpages489–493. \endbibitem

- Ren et al. (2015) {barticle}[author] \bauthor\bsnmRen, \bfnmZhao\binitsZ., \bauthor\bsnmSun, \bfnmTingni\binitsT., \bauthor\bsnmZhang, \bfnmCun-Hui\binitsC.-H. and \bauthor\bsnmZhou, \bfnmHarrison H\binitsH. H. (\byear2015). \btitleAsymptotic normality and optimalities in estimation of large Gaussian graphical models. \bjournalThe Annals of Statistics \bvolume43 \bpages991–1026. \endbibitem

- Rudelson and Zhou (2013) {barticle}[author] \bauthor\bsnmRudelson, \bfnmMark\binitsM. and \bauthor\bsnmZhou, \bfnmShuheng\binitsS. (\byear2013). \btitleReconstruction from anisotropic random measurements. \bjournalInformation Theory, IEEE Transactions on \bvolume59 \bpages3434–3447. \endbibitem

- Städler and Mukherjee (2016) {barticle}[author] \bauthor\bsnmStädler, \bfnmNicolas\binitsN. and \bauthor\bsnmMukherjee, \bfnmSach\binitsS. (\byear2016). \btitleTwo-sample testing in high dimensions. \bjournalJournal of the Royal Statistical Society: Series B (Statistical Methodology). \endbibitem

- Sun and Zhang (2012) {barticle}[author] \bauthor\bsnmSun, \bfnmTingni\binitsT. and \bauthor\bsnmZhang, \bfnmCun-Hui\binitsC.-H. (\byear2012). \btitleScaled sparse linear regression. \bjournalBiometrika \bvolume99 \bpages879–898. \endbibitem

- Van de Geer et al. (2014) {barticle}[author] \bauthor\bparticleVan de \bsnmGeer, \bfnmSara\binitsS., \bauthor\bsnmBühlmann, \bfnmPeter\binitsP., \bauthor\bsnmRitov, \bfnmYaacov\binitsY., \bauthor\bsnmDezeure, \bfnmRuben\binitsR. \betalet al. (\byear2014). \btitleOn asymptotically optimal confidence regions and tests for high-dimensional models. \bjournalThe Annals of Statistics \bvolume42 \bpages1166–1202. \endbibitem