Asymptotically Minimax Prediction

in Infinite Sequence Models

Abstract

We study asymptotically minimax predictive distributions in infinite sequence models. First, we discuss the connection between prediction in an infinite sequence model and prediction in a function model. Second, we construct an asymptotically minimax predictive distribution for the setting in which the parameter space is a known ellipsoid. We show that the Bayesian predictive distribution based on the Gaussian prior distribution is asymptotically minimax in the ellipsoid. Third, we construct an asymptotically minimax predictive distribution for any Sobolev ellipsoid. We show that the Bayesian predictive distribution based on the product of Stein’s priors is asymptotically minimax for any Sobolev ellipsoid. Finally, we present an efficient sampling method from the proposed Bayesian predictive distribution.

keywords:

[class=MSC]keywords:

and

1 Introduction

We consider prediction in an infinite sequence model. The current observation is a random sequence given by

| (1) |

where is an unknown sequence in and is a random sequence distributed according to on . Here is a product -field of the Borel -field on the Euclidean space . Based on the current observation , we estimate the distribution of a future observation given by

| (2) |

where is distributed according to . We denote the true distribution of with by and the true distribution of with by . For simplicity, we assume that and are independent.

Prediction in an infinite sequence model is shown to be equivalent to the following prediction in a function model. Consider that we observe a random function given by

| (3) |

where is the -space on with the Lebesgue measure, is an unknown absolutely continuous function of which the derivative is in , is a known constant, and follows the standard Wiener measure on . Based on the current observation , we estimate the distribution of a random function given by

| (4) |

where is a known constant, and follows the standard Wiener measure on . The details are provided in Section 2. Xu and Liang [19] established the connection between prediction of a function on equispaced grids and prediction in a high-dimensional sequence model, using the asymptotics in which the dimension of the parameter grows to infinity according to the growth of the grid size. Our study is motivated by Xu and Liang [19] and is its generalization to the settings in which the parameter is infinite-dimensional.

Using the above equivalence, we discuss the performance of a predictive distribution of based on in an infinite sequence model. Let be the whole set of probability measures on and let be the decision space . We use the Kullback–Leibler loss as a loss function: for all and all , if is absolutely continuous with respect to , then

and otherwise . The risk of a predictive distribution in the case that the true distributions of and are and , respectively, is denoted by

We construct an asymptotically minimax predictive distribution that satisfies

where with a known non-zero and non-decreasing divergent sequence and with a known constant . Note that for any , the minimax risk is bounded above by . Further, note that using the above equivalence between the infinite sequence model and the function model, the parameter restriction in the infinite sequence model that corresponds to the restriction that the corresponding parameter in the function model is smooth; represents the volume of the parameter space, and the growth rate of represents the smoothness of the functions.

The constructed predictive distribution is the Bayesian predictive distribution based on the Gaussian distribution. For a prior distribution of , the Bayesian predictive distribution based on is obtained by averaging with respect to the posterior distribution based on . Our construction is a generalization of the result in Xu and Liang [19] to infinite-dimensional settings. The details are provided in Section 3.

Further, we discuss adaptivity to the sequence and . In applications, since we do not know the true values of and , it is desirable to construct a predictive distribution without using and that is asymptotically minimax in any ellipsoid in the class. Such a predictive distribution is called an asymptotically minimax adaptive predictive distribution in the class. In the present paper, we focus on an asymptotically minimax adaptive predictive distribution in the simplified Sobolev class , where .

Our construction of the asymptotically minimax adaptive predictive distribution is based on Stein’s prior and the division of the parameter into blocks. The proof of the adaptivity relies on a new oracle inequality related to the Bayesian predictive distribution based on Stein’s prior; see Subsection 4.2. Stein’s prior on is an improper prior whose density is . It is known that the Bayesian predictive distribution based on that prior has a smaller Kullback–Leibler risk than that based on the uniform prior in the finite dimensional Gaussian settings; see Komaki [9] and George, Liang and Xu [8]. The division of the parameter into blocks is widely used for the construction of the asymptotically minimax adaptive estimator; see Efromovich and Pinsker [7], Cai, Low and Zhao [4], and Cavalier and Tsybakov [5]. The details are provided in Section 4.

2 Equivalence between predictions in infinite sequence models and predictions in function models

In this section, we provide an equivalence between prediction in a function model and prediction in an infinite sequence model. The proof consists of the two steps. First, we provide a connection between predictions in a function model and predictions in the submodel of an infinite sequence model. Second, we extend predictions in the submodel to predictions in the infinite sequence model.

The detailed description of prediction in a function model is as follows. Let , where denotes the derivative of . Let be the inner product of . Let be the whole set of probability distributions on , where is the Borel -field of . denotes the Kullback–Leibler loss of in the setting that the true parameter function is .

Let be the covariance operator of : for any , . By Mercer’s theorem, there exists a non-negative monotone decreasing sequence and an orthonormal basis in such that

Explicitly, is and is for .

The detailed description of prediction in the sub-model of an infinite sequence model is as follows. Let be . Note that is a measurable set with respect to , because is the pointwise -limit of and we use Theorem 4.2.2. in Dudley [6]. Let be the whole set of probability distributions on , where is the relative -field of .

The following theorem states that the Kullback–Leibler loss in the function model is equivalent to that in the submodel of the infinite sequence model.

Theorem 2.1.

For every and every , there exist and such that

Conversely, for every and every , there exist and such that

Proof.

We construct pairs of a measurable one-to-one map and a measurable one-to-one map .

Let be defined by

is well-defined as a map from to because for and in such that , we have , and because for , we have .

We show that is one-to-one, onto, and measurable. is one-to-one because if , then we have for all . is onto because if , satisfies that . is measurable because is continuous with respect to the norm of and , and because is equal to the Borel -field with respect to . is continuous, because we have

Further, the restriction of to is a one-to-one and onto map from to .

Let be defined by . is the inverse of . Thus, is one-to-one, onto, and measurable.

Since the Kullback–Leibler divergence is unchanged under a measurable one-to-one mapping, the proof is completed. ∎

Remark 2.2.

The following theorem justifies focusing on prediction in instead of prediction in .

Theorem 2.3.

For every and , there exists such that

In particular, for any subset of ,

where .

Proof.

Note that by the Karhunen–Loève theorem. For such that , and then for any , . For such that ,

where is the restriction of to . ∎

3 Asymptotically minimax predictive distribution

In this section, we construct an asymptotically minimax predictive distribution for the setting in which the parameter space is an ellipsoid with a known sequence and with a known constant . Further, we provide the asymptotically minimax predictive distributions in two well-known ellipsoids; a Sobolev and an exponential ellipsoids.

3.1 Principal theorem of Section 3

We construct an asymptotically minimax predictive distribution in Theorem 3.1.

We introduce notations used in the principal theorem. For an infinite sequence , let be with variance . Then, the posterior distribution based on is

| (5) |

The Bayesian predictive distribution based on is

| (6) |

For the derivations of (5) and (6), see Theorem 3.2 in Zhao [21]. Let and be defined by

| (7) |

respectively. Let be the infinite sequence of which the -th coordinate for is defined by

| (8) |

where , and is determined by

Let be the number defined by

| (9) |

The following is the principal theorem of this section.

Theorem 3.1.

Let be . Assume that . If as and , then

Further, the Bayesian predictive distribution based on is asymptotically minimax:

as .

The proof is provided in the next subsection.

3.2 Proof of the principal theorem of Section 3

The proof of Theorem 3.1 requires five lemmas. Because the parameter is infinite-dimensional, we need Lemmas 3.2 and 3.5 in addition to Theorem 4.2 in Xu and Liang [19].

The first lemma provides the explicit form of the Kullback–Leibler risk of the Bayesian predictive distribution . The proof is provided in Appendix A.

Lemma 3.2.

If and , then and are mutually absolutely continuous given -a.s. and the Kullback–Leibler risk of the Bayesian predictive distribution is given by

| (10) |

The second lemma provides the Bayesian predictive distribution that is minimax among the sub class of . The proof is provided in Appendix A.

Lemma 3.3.

Assume that . Then, for any and any , is finite and is uniquely determined. Further,

The third lemma provides the upper bound of the minimax risk.

Lemma 3.4.

Assume that . Then, for any and any ,

Proof.

Since the class is included in , the result follows from Lemma 3.3. ∎

We introduce the notations for providing the lower bound of the minimax risk. These notations are also used in Lemma 4.2. Fix an arbitrary positive integer . Let be . Let be . Let and be and , respectively. Let be the -dimensional parameter space defined by

Let be the -dimensional Kullback–Leibler risk

of predictive distribution on . Let be the minimax risk

where is with the whole set of probability distributions on .

The fourth lemma shows that the minimax risk in the infinite sequence model is bounded below by the minimax risk in the finite dimensional sequence model. The proof is provided in Appendix A.

Lemma 3.5.

Let be any positive integer. Then, for any and any ,

The fifth lemma provides the asymptotic minimax risk in a high-dimensional sequence model. It is due to Xu and Liang [19].

Lemma 3.6 (Theorem 4.2 in Xu and Liang [19]).

Based on these lemmas, we present the proof of Theorem 3.1.

3.3 Examples of asymptotically minimax predictive distributions

In this subsection, we provide the asymptotically minimax Kullback–Leibler risks and the asymptotically minimax predictive distributions in the case that is a Sobolev ellipsoid and in the case that it is an exponential ellipsoid.

3.3.1 The Sobolev ellipsoid

The simplified Sobolev ellipsoid is with and . We set for . This setting is a slight generalization of Section 5 of Xu and Liang [19], in which the asymptotic minimax Kullback–Leibler risk with is obtained.

We expand and . From the definition of , we have . Thus, we have

where we use the convergence of the Riemann sum with the function . Then,

| (11) |

and

Thus, we obtain the asymptotically minimax risk

| (12) |

where

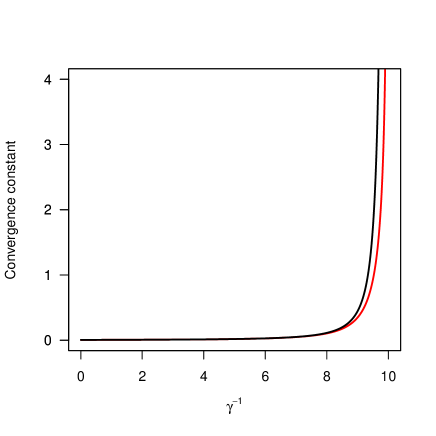

We compare the Kullback–Leibler risk of the asymptotically minimax predictive distribution with the Kullback–Leibler risk of the plug-in predictive distribution that is asymptotically minimax among all plug-in predictive distributions. The latter is obtained using Pinsker’s asymptotically minimax theorem for estimation (see Pinsker [14]). We call the former and the latter risks the predictive and the estimative asymptotically minimax risks, respectively. The orders of and in the predictive asymptotic minimax risk are both the -th power. These orders are the same as in the estimative asymptotically minimax risk. However, the convergence constant and the convergence constant in the estimative asymptotically minimax risk are different. Note that the convergence constant in the estimative asymptotically minimax risk is the Pinsker constant multiplied by . Figure 1 shows that the convergence constant becomes smaller than the convergence constant in the estimative asymptotically minimax risk as increases. Xu and Liang [19] also pointed out this phenomenon when .

3.3.2 The exponential ellipsoid

The exponential ellipsoid is , with and . We set for .

We expand and . From the definition of , we have . Thus,

where is a bounded term with respect to . Then,

and

Thus, we obtain the asymptotically minimax risk

| (13) |

We compare the predictive asymptotically minimax risk with the estimative asymptotically minimax risk in the exponential ellipsoid. From (13),

From Pinsker’s asymptotically minimax theorem,

Thus, for any ,

In an exponential ellipsoid, the order of in the predictive asymptotically minimax risk is the same as that in the estimative asymptotically minimax risk. The convergence constant in the predictive asymptotically minimax risk is strictly smaller than that in the estimative asymptotically minimax risk.

Remark 3.7.

There are differences between the asymptotically minimax risks in the Sobolev and the exponential ellipsoids. The constant has the same order in the asymptotically minimax risk as that of when the parameter space is the Sobolev ellipsoid. In contrast, the constant disappears in the asymptotically minimax risk when the parameter space is the exponential ellipsoid.

4 Asymptotically minimax adaptive predictive distribution

In this section, we show that the blockwise Stein predictive distribution is asymptotically minimax adaptive on the family of Sobolev ellipsoids. Recall that the Sobolev ellipsoid is with and .

4.1 Principal theorem of Section 4

For the principal theorem, we introduce a blockwise Stein predictive distribution and a weakly geometric blocks system.

A blockwise Stein predictive distribution for a set of blocks is constructed as follows. Let be any positive integer. We divide into blocks: . We denote the number of elements in each block by . Corresponding to the division into the blocks , we divide into , , and . In the same manner, we divide into ,, and . Let be the blockwise Stein prior with the set of blocks defined by

where is the square norm. We define the blockwise Stein predictive distribution with the set of blocks as

| (14) |

where is the posterior density of . In regard to estimation, Brown and Zhao [3] discussed the behavior of the Bayes estimator based on the blockwise Stein prior.

The weakly geometric blocks (WGB) system is introduced as follows. The WGB system with cardinalities is the division of , where . It is defined by

| (15) |

where and . The WGB system has been used for the construction of an asymptotically minimax adaptive estimator; see Cavalier and Tsybakov [5] and Tsybakov [16].

The following is the principal theorem. Let be . Let be the WGB system defined by (15) with cardinalities . Let be the blockwise Stein predictive distribution with the WGB system defined by (14).

Theorem 4.1.

If for some , then for any and for any ,

4.2 Oracle inequality of the Bayesian predictive distribution based on Stein’s prior

Before considering the proof of Theorem 4.1, we show an oracle inequality related to Stein’s prior for that is useful outside of the proof of Theorem 4.1. Recall that the -dimensional Kullback–Leibler risk of the predictive distribution on is defined by

where and are and , respectively. For a positive integer , let be the Bayesian predictive distribution on based on the -dimensional Stein’s prior .

Lemma 4.2.

Let be any positive integer such that . For any ,

| (16) |

Remark 4.3.

We call inequality (16) an oracle inequality of Stein’s prior for the following reason. By the same calculation in (21) in the proof of Lemma 3.3, the second term on the right hand side of inequality (16) is the oracle Kullback–Leibler risk, that is, the minimum of the Kullback–Leibler risk in the case that the action space is

and in the case that we are permitted to use the value of the true parameter . Therefore, Lemma 4.2 tells us that the Kullback–Leibler risk of the -dimensional Bayesian predictive distribution based on Stein’s prior is bounded above by a constant independent of plus the oracle Kullback–Leibler risk.

Proof of Lemma 4.2.

First,

where is the Bayesian predictive distribution based on the uniform prior , and and are the Bayes estimators based on the uniform prior and based on Stein’s prior , respectively. Here is the expectation of with respect to the -dimensional Gaussian distribution with mean and covariance matrix . For the proof of the identity, see Brown, George and Xu [2].

Second,

where is the James–Stein estimator. For the first inequality, see Kubokawa [10]. For the second inequality, see e.g. Theorem 7.42 in Wasserman [17]. Thus, we have

Since

it follows that

Here, we use

∎

Remark 4.4.

As a corollary of Lemma 4.2, we show that the Bayesian predictive distribution based on Stein’s prior is asymptotically minimax adaptive in the family of -balls . The -ball is . Note that another type of an asymptotically minimax adaptive predictive distribution in the family of -balls has been investigated by Xu and Zhou [20].

Lemma 4.5.

Let be . If for some , then for any , the blockwise Stein predictive distribution with the single block on satisfies

4.3 Proof of the principal theorem of Section 4

In this subsection, we provide the proof of Theorem 4.1. The proof consists of the following two steps. First, in Lemma 4.7, we examine the properties of the blockwise Stein predictive distribution with a set of blocks. The proof of Lemma 4.7 requires Lemma 4.6. Second, we show that the blockwise Stein predictive distribution with the weakly geometric blocks system is asymptotically minimax adaptive on the family of Sobolev ellipsoids, using Lemma 4.7 and the property of the WGB system (Lemma 4.8).

For the proof, we introduce two subspaces of the decision space. For a given set of blocks , let be

where and let be

where .

Although the decision space is included in the decision space , the following lemma states that if the growth rate of the numbers in each block in is controlled, then the infimum of the Kullback–Leibler risk among is bounded by a constant plus a constant multiple of the infimum of the Kullback–Leibler risk among . The proof is provided in Appendix B.

Lemma 4.6.

Let be any positive integer. Let be a set of blocks whose cardinalities satisfy

for some . Then, for any ,

The following lemma states the relationship between the Kullback–Leibler risk of the blockwise Stein predictive distribution and that of the predictive distribution in . The proof is provided in Appendix B.

Lemma 4.7.

Let be any positive integer. Let be a set of blocks whose cardinalities satisfy

for some . Let be the blockwise Stein predictive distribution with the set of blocks defined by (14). Then, for any ,

| (17) |

The following lemma states that the WBG system satisfies the assumption in Lemmas 4.6 and 4.7. The proof is due to Tsybakov [16].

Lemma 4.8 (e.g., Lemma 3.12 in Tsybakov [16]).

Let be . Let be the WGB system defined by (15) with cardinalities . Then, there exist and such that

and

Based on these lemmas, we provide the proof of Theorem 4.1.

Proof of Theorem 4.1.

First, since the WGB system satisfies the assumption in Lemma 4.7, it follows from Lemma 4.7 that for ,

Second, we show that the asymptotically minimax predictive distribution in Theorem 3.1 is also characterized as follows: for a sufficiently small ,

It suffices to show that the Bayesian predictive distribution is included in for a sufficiently small . This is proved as follows. Recall that defined by (9) is the maximal index of which defined by (8) is non-zero. From the expansion of given in (11), for a sufficiently small , for with some constant , vanishes. Since for , the Bayesian predictive distribution is included in for a sufficiently small .

Combining the first argument with the second argument yields

This completes the proof. ∎

5 Numerical experiments

In Subsection 5.1, we provide an exact sampling method for the blockwise Stein predictive distribution. In Subsection 5.2, we provide two numerical experiments concerning the performance of that predictive distribution.

5.1 Exact sampling from the blockwise Stein predictive distribution

We provide an exact sampling method from the posterior distribution based on Stein prior on . Owing to the block structure, it suffices to provide an exact sampling method from the posterior distribution based on Stein’s prior.

We use the following mixture representation of Stein’s prior:

where is a constant depending only on . Thus, as for the posterior distribution of , we have

where

and

Here is the probability density function of the normal distribution. Under the transformation , the distribution of is a truncated Gamma distribution:

Therefore, we obtain an exact sampling from the posterior distribution based on Stein’s prior by sampling the normal distribution and the truncated Gamma distribution. For the sampling from the truncated Gamma distribution, we use the acceptance-rejection algorithm for truncated Gamma distributions based on the mixture of beta distributions; see Philippe [13].

5.2 Comparison with a fixed variance

Though we proved the asymptotic optimality of the blockwise Stein predictive distribution with the WGB system, it does not follow that the blockwise Stein predictive distribution behaves well with a fixed variance .

In this subsection, we examine the behavior with a fixed of the blockwise Stein predictive distribution with the WGB system compared to the plugin predictive distribution with the Bayes estimator based on the blockwise Stein prior and the asymptotically minimax predictive distribution in the Sobolev ellipsoid given in Theorem 3.1. In this subsection, we call the asymptotically minimax predictive distribution in the Sobolev ellipsoid given in Theorem 3.1 the Pinsker-type predictive distribution with and .

For the comparison, we consider the 6 predictive settings with :

-

•

In the first setting, for and ;

-

•

In the second setting, for and ;

-

•

In the third setting, for and ;

-

•

In the fourth setting, for and ;

-

•

In the fifth setting, for and ;

-

•

In the sixth setting, for and .

Let .

In each setting, we obtain samples of distributed according to the blockwise Stein predictive distribution with the WGB system up to the -th order using the sampling method described in Subsection 5.1, and we construct the coordinate-wise -predictive interval of using samples. In each setting, we use the Pinsker-type predictive distribution with and such that : we use and in the firth, second, and third settings. We use and in the fourth, fifth, and sixth settings.

In each setting, we obtain 5000 samples from the true distribution of and calculate the means of the coordinate-wise mean squared errors normalized by , and then calculate the means and the standard deviations of the counts of the samples included in the predictive intervals.

| Setting number | Bayes with WGBStein | Plugin with WGBStein | Pinsker |

|---|---|---|---|

| First | 1.11 | 1.11 | |

| Second | 1.89 | 1.89 | |

| Third | 8.54 | 8.52 | |

| Fourth | 1.08 | 1.08 | |

| Fifth | 1.89 | 1.89 | |

| Sixth | 21.3 | 21.3 |

| Setting number | Bayes with WGBStein | Plugin with WGBStein | Pinsker |

|---|---|---|---|

| First | 82.4 (4.53) | 78.6 (5.28) | (4.03) |

| Second | 91.1 (8.08) | 71.4 (14.9) | (4.56) |

| Third | 98.9 (5.72) | 45.8 (29.8) | (5.06) |

| Fourth | 82.3 (3.04) | 78.4 (6.11) | (3.44) |

| Fifth | 91.6 (7.66) | 71.0 (14.6) | (8.21) |

| Sixth | 97.1 (13.9) | 52.9 (26.9) | (11.3) |

Tables 1 and 2 show that the Pinsker-type predictive distribution (abbreviated by Pinsker) has the smallest mean squared error and has the sharpest predictive interval. It is because the Pinsker-type predictive distribution uses and . The blockwise Stein predictive distribution (abbreviated by Bayes with WGBStein) and the plugin predictive distribution with the Bayes estimator based on the blockwise Stein prior (abbreviated by Plugin with WGBStein) have nearly the same performance in the mean squared error. The blockwise Stein predictive distribution has a wider predictive interval than the plugin predictive distribution. Its predictive interval has a smaller variance than that of the plugin predictive distribution in all settings. In the next paragraph, we consider the reason for this phenomenon by using the transformation of the infinite sequence model to the function model discussed in Section 2.

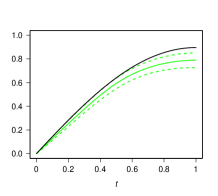

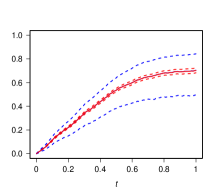

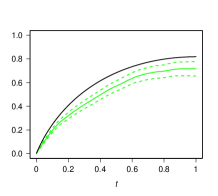

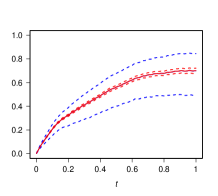

Using the function representation of the infinite sequence model discussed in Section 2, we examine the behavior of the predictive distributions in the second and fifth settings. Figure 2 shows the mean path and the predictive intervals of predictive distributions at and the values of the true function at . Figure 2 (a), Figure 2 (b), Figure 2 (c), and Figure 2 (d) represent the Pinsker-type predictive distribution and the true function in the second setting, the blockwise Stein predictive distribution and the plugin predictive distribution in the second setting, the Pinsker-type predictive distribution and the true function in the fourth setting, and the blockwise Stein predictive distribution and the plugin predictive distribution in the fourth setting, respectively. The solid line represents the true function and the mean paths. The dashed line represents the pointwise predictive intervals. The black, green, blue, and red lines correspond to the true function, the Pinsker-type predictive distribution, the blockwise Stein predictive distribution, and the plugin predictive distribution, respectively.

The mean paths of the blockwise Stein predictive distribution and the plugin predictive distributions are more distant from the true function than that of the Pinsker-type predictive distribution, corresponding to the results in Table 1. The predictive intervals of the blockwise Stein predictive distribution are wider than these of the other predictive distributions, corresponding to the results in Table 2. Though the blockwise Stein predictive distribution has a mean path that is more distant from the true function than the Pinsker-type predictive distribution, it has a wider predictive interval and captures future observations. In contrast, although the plugin predictive distribution has nearly the same mean path as the blockwise Stein predictive distribution does, it has a narrow predictive interval and does not capture future observations.

6 Discussions and Conclusions

In the paper, we have considered asymptotically minimax Bayesian predictive distributions in an infinite sequence model. First, we have provided the connection between prediction in a function model and prediction in an infinite sequence model. Second, we have constructed an asymptotically minimax Bayesian predictive distribution for the setting in which the parameter space is a known ellipsoid. Third, using the product of Stein’s priors based on the division of the parameter into blocks, we have constructed an asymptotically minimax adaptive Bayesian predictive distribution in the family of Sobolev ellipsoids.

We established the fundamental results of prediction in the infinite-dimensional model using the asymptotics as . The approach was motivated by Xu and Liang [19]. Since it is not always appropriate to use asymptotics in applications, the next step is to provide the result for a fixed .

We discussed the asymptotic minimaxity and the adaptivity for the ellipsoidal parameter space. There are many other types of parameter space in high-dimensional and nonparametric models; for example, Mukherjee and Johnstone [12] discussed the asymptotically minimax prediction in high-dimensional Gaussian sequence model under sparsity. For future work, we should focus on the asymptotically minimax adaptive predictive distributions in other parameter spaces.

7 Acknowledgements

The authors thank the Editor, an associate editor, reviewers for their careful reading and constructive suggestions on the manuscript. This work is supported by JSPS KAKENHI Grand number 26280005.

Appendix A Proofs of Lemmas in Section 2

Proof of Lemma 3.2.

The proof is similar to that of Lemmas 5.1 and 6.1 in Belitser and Ghosal [1]. We denote the expectation of and with respect to and by .

First, we show that and are mutually absolutely continuous given -a.s. if and . From Kakutani’s theorem (pp. 150–151 in Williams [18]), and are mutually absolutely continuous given -a.s. if and only if

| (18) |

Since the right hand side of (18) is the limit of the product of

| (19) |

and

| (20) |

as , it suffices to show that both (19) and (20) converge to non-zero constants. Quantity (19) converges to a non-zero constant because the product with converges to a non-zero constant provided that converges, and because

Quantity (20) converges to a non-zero constant because

Thus, and are mutually absolutely continuous given -a.s..

Second, we show that is given by (10). Let be the finite dimensional projection . Let and be the induced probability measures of and by the finite-dimensional projection , respectively. From Kakutani’s theorem, we have

Then, it suffices to show that the almost sure convergence in the right hand side is also the convergence in the expectation. Here,

where is

Here is a zero-mean martingale such that ; From the martingale convergence theorem (p. 111 in Williams [18]), converges to , -a.s. and . Since , equality (10) follows. ∎

Proof of Lemma 3.3.

First, the finiteness of is derived from the assumption for . is uniquely determined because is continuous and strictly decreasing with respect to . Note that is also a function with respect to .

Second, we show that

Since the function

has a minimum at , for ,

| (21) |

Since the minimax risk is greater than the maximin risk,

| (22) | |||||

Finally, we show that

Substituting into (10) for any yields

with equality if . Thus,

Since

it follows that

∎

Proof of Lemma 3.5.

First, note that the following equivalence holds:

for -almost all . This is because two Gaussian measures and are mutually absolutely continuous if and only if .

Second, from the above equivalence, we have the following lower bound of the minimax risk: for any ,

where we denote with for by .

Third, we further bound the previous lower bound. Hereafter, we fix . To do this, we consider the decomposition of the density with respect to as follows. Let be the projection . The projection induces a marginal probability measure on and a conditional probability measure on such that for any measurable set ,

In accordance with the decomposition of into two probability measures and , we decompose the density with respect to as

for almost all . See p.119 in Pollard [15] for the decomposition. From the decomposition of the density and from Jensen’s inequality, for and for such that , we have

We denote the probability measure obtained by taking the conditional expectation of conditioned by under by , because it does not depend on given . By the definition of ,

By Jensen’s inequality and by the above equality,

Thus,

where is the expectation of and with respect to and . Hence,

∎

Appendix B Proofs of Lemmas in Section 4

Proof of Lemma 4.7.

From Lemma 3.2, the Kullback–Leibler risk of is given by

where for , is the Bayesian predictive distribution on based on Stein’s prior . For the block with , inequality (16) holds. For the block with , the inequality

holds because the left hand side in the above inequality is monotone increasing with respect to . Thus,

Proof of Lemma 4.6.

It suffices to show that for any , there exists such that

| (24) |

where and are Bayesian predictive distributions on based on and , respectively.

For any , we define as

| (29) |

For and for , let be because does not change in the same block . Then,

| (30) |

From the inequality that for , the second term in (30) is bounded above as follows:

Thus,

| (31) |

For the first term on the right hand side of (31), from the definition of ,

| (32) |

Note that the function defined by

is monotone increasing with respect to and then because

Since for ,

Thus, the first term in (32) is bounded as follows:

| (33) |

From the assumption on the cardinalities of the blocks and from the inequality that for ,

| (34) |

References

- Belitser and Ghosal [2003] {barticle}[author] \bauthor\bsnmBelitser, \bfnmE.\binitsE. and \bauthor\bsnmGhosal, \bfnmS.\binitsS. (\byear2003). \btitleAdaptive Bayesian inference of the mean of an inifinite-dimensional normal distribution. \bjournalAnn. Statist. \bvolume31 \bpages pp. 536–559. \endbibitem

- Brown, George and Xu [2008] {barticle}[author] \bauthor\bsnmBrown, \bfnmL.\binitsL., \bauthor\bsnmGeorge, \bfnmE.\binitsE. and \bauthor\bsnmXu, \bfnmX.\binitsX. (\byear2008). \btitleAdmissible predictive density estimation. \bjournalAnn. Statist. \bvolume36 \bpagespp. 1156–1170. \endbibitem

- Brown and Zhao [2009] {barticle}[author] \bauthor\bsnmBrown, \bfnmL.\binitsL. and \bauthor\bsnmZhao, \bfnmL.\binitsL. (\byear2009). \btitleEstimators for Gaussian modles having a block-wise structure. \bjournalStatist. Sinica \bvolume19 \bpagespp. 885–903. \endbibitem

- Cai, Low and Zhao [2000] {btechreport}[author] \bauthor\bsnmCai, \bfnmT.\binitsT., \bauthor\bsnmLow, \bfnmM.\binitsM. and \bauthor\bsnmZhao, \bfnmL.\binitsL. (\byear2000). \btitleSharp adaptive estimation by a blockwise method \btypeTechnical Report, \bpublisherWarton School, University of Pennsylvania, Philadelphia. \endbibitem

- Cavalier and Tsybakov [2001] {barticle}[author] \bauthor\bsnmCavalier, \bfnmL.\binitsL. and \bauthor\bsnmTsybakov, \bfnmA.\binitsA. (\byear2001). \btitlePenalized blockwise Stein’s method, monotone oracles and sharp adaptive estimation. \bjournalMath. Methods of Statist. \bvolume10 \bpagespp. 247–282. \endbibitem

- Dudley [2002] {bbook}[author] \bauthor\bsnmDudley, \bfnmR.\binitsR. (\byear2002). \btitleReal analysis and Probability, \bedition2nd ed. \bpublisherCambridge University Press. \endbibitem

- Efromovich and Pinsker [1984] {barticle}[author] \bauthor\bsnmEfromovich, \bfnmS.\binitsS. and \bauthor\bsnmPinsker, \bfnmM.\binitsM. (\byear1984). \btitleLearning algorithm for nonparmetric filtering. \bjournalAutomation and Remote Control \bvolume11 \bpagespp.1434–1440. \endbibitem

- George, Liang and Xu [2006] {barticle}[author] \bauthor\bsnmGeorge, \bfnmE.\binitsE., \bauthor\bsnmLiang, \bfnmF.\binitsF. and \bauthor\bsnmXu, \bfnmX.\binitsX. (\byear2006). \btitleImproved minimax predictive densities under Kullback–Leibler loss. \bjournalAnn. Statist. \bvolume34 \bpagespp. 78–91. \endbibitem

- Komaki [2001] {barticle}[author] \bauthor\bsnmKomaki, \bfnmF.\binitsF. (\byear2001). \btitleA shrinkage predictive distribution for multivariate normal observations. \bjournalBiometrika \bvolume88 \bpagespp. 859–864. \endbibitem

- Kubokawa [1991] {barticle}[author] \bauthor\bsnmKubokawa, \bfnmT.\binitsT. (\byear1991). \btitleAn approach to improving the James–Stein estimator. \bjournalJ. Multi. Anal. \bvolume36 \bpagespp. 121–126. \endbibitem

- Mandelbaum [1984] {barticle}[author] \bauthor\bsnmMandelbaum, \bfnmA.\binitsA. (\byear1984). \btitleAll admissible linear estimators of the mean of a Gaussian distribution of a Hilbert space. \bjournalAnn. Statist. \bvolume12 \bpagespp. 1448–1466. \endbibitem

- Mukherjee and Johnstone [2015] {barticle}[author] \bauthor\bsnmMukherjee, \bfnmG.\binitsG. and \bauthor\bsnmJohnstone, \bfnmI.\binitsI. (\byear2015). \btitleExact minimax estimation of the predictive density in sparse Gaussian models. \bjournalAnn. Statist. \bvolume43 \bpagespp. 937–961. \endbibitem

- Philippe [1997] {barticle}[author] \bauthor\bsnmPhilippe, \bfnmA.\binitsA. (\byear1997). \btitleSimulation of right and left truncated gamma distributions by mixtures. \bjournalStatist. and Comput. \bvolume7 \bpagespp. 173–181. \endbibitem

- Pinsker [1980] {barticle}[author] \bauthor\bsnmPinsker, \bfnmM.\binitsM. (\byear1980). \btitleOptimal filtering of square integrable signals in Gaussian white noise. \bjournalProblems Inform. Transmission \bvolume16 \bpages 120–133. \endbibitem

- Pollard [2002] {bbook}[author] \bauthor\bsnmPollard, \bfnmD.\binitsD. (\byear2002). \btitleA User’s Guide to Measure Theoretic Probability. \bpublisherCambridge University Press. \endbibitem

- Tsybakov [2009] {bbook}[author] \bauthor\bsnmTsybakov, \bfnmA.\binitsA. (\byear2009). \btitleIntroduction to Nonparametric Estimation. \bpublisherSpringer Science+Business Media. \endbibitem

- Wasserman [2007] {bbook}[author] \bauthor\bsnmWasserman, \bfnmL.\binitsL. (\byear2007). \btitleAll of Nonparametric Statistics, \bedition3rd ed. \bpublisherSpringer. \endbibitem

- Williams [1991] {bbook}[author] \bauthor\bsnmWilliams, \bfnmD.\binitsD. (\byear1991). \btitleProbability with Martingale. \bpublisherCambridge University Press. \endbibitem

- Xu and Liang [2010] {barticle}[author] \bauthor\bsnmXu, \bfnmX.\binitsX. and \bauthor\bsnmLiang, \bfnmF.\binitsF. (\byear2010). \btitleAsymptotic minimax risk of predictive density estimation for non-parametric regression. \bjournalBernoulli \bvolume16 \bpages pp. 543–560. \endbibitem

- Xu and Zhou [2011] {barticle}[author] \bauthor\bsnmXu, \bfnmX.\binitsX. and \bauthor\bsnmZhou, \bfnmD.\binitsD. (\byear2011). \btitleEmpirical Bayes predictive densities for high-dimensional normal models. \bjournalJ. Multi. Anal. \bvolume102 \bpagespp. 1417–1428. \endbibitem

- Zhao [2000] {barticle}[author] \bauthor\bsnmZhao, \bfnmL.\binitsL. (\byear2000). \btitleBayesian aspects of some nonparametric problems. \bjournalAnn. Statist. \bvolume28 \bpages pp. 532–552. \endbibitem