The De-Biased Whittle Likelihood

Abstract

The Whittle likelihood is a widely used and computationally efficient pseudo-likelihood. However, it is known to produce biased parameter estimates for large classes of models. We propose a method for de-biasing Whittle estimates for second-order stationary stochastic processes. The de-biased Whittle likelihood can be computed in the same operations as the standard approach. We demonstrate the superior performance of the method in simulation studies and in application to a large-scale oceanographic dataset, where in both cases the de-biased approach reduces bias by up to two orders of magnitude, achieving estimates that are close to exact maximum likelihood, at a fraction of the computational cost. We prove that the method yields estimates that are consistent at an optimal convergence rate of , under weaker assumptions than standard theory, where we do not require that the power spectral density is continuous in frequency. We describe how the method can be easily combined with standard methods of bias reduction, such as tapering and differencing, to further reduce bias in parameter estimates.

Keywords: Parameter estimation; Pseudo-likelihood; Periodogram; Aliasing; Blurring; Tapering; Differencing.

††1 Data Science Institute / Department of Mathematics and Statistics, Lancaster University, UK (email: a.sykuslki@lancaster.ac.uk)

††2 Department of Statistical Science, University College London, UK

††3 NorthWest Research Associates, Redmond WA, USA

1 Introduction

This paper introduces an improved computationally-efficient method of estimating time series model parameters of second-order stationary processes. The standard approach is to maximize the exact time-domain likelihood, which in general has computational efficiency of order for regularly-spaced observations (where is the length of the observed time series) and produces estimates that are asymptotically efficient, converging at a rate of . A second approach is the method of moments, which in general has a computational efficiency of smaller order but with poorer statistical performance (Brockwell & Davis, 1991, p.253), exhibiting both bias and often a higher variance. A third approach of approximating the exact likelihood, often referred to as quasi-, pseudo-, or composite-likelihoods, is receiving much recent attention across statistics, see e.g. Fan et al. (2014) and Guinness & Fuentes (2017). In time series analysis, such likelihood approximations offer the possibility of considerable improvements in computational performance (usually scaling as order ), with only small changes in statistical behaviour, see e.g. Dutta & Mondal (2015) and Anitescu et al. (2016). Here we introduce a pseudo-likelihood that is based on the Whittle likelihood (Whittle, 1953) which we will show offers dramatic decreases in bias and mean-squared error in applications, yet with no significant increase in computational cost, and no loss in consistency or rate of convergence. We will refer to our pseudo-likelihood as the de-biased Whittle likelihood.

The Whittle likelihood of Whittle (1953) is a frequency-domain approximation to the exact likelihood. This method is considered a standard method in parametric spectral analysis on account of its order computational efficiency (Choudhuri et al., 2004; Fuentes, 2007; Matsuda & Yajima, 2009; Krafty & Collinge, 2013; Jesus & Chandler, 2017). However, it has been observed that the Whittle likelihood, despite its desirable asymptotic properties, may exhibit poor properties when applied to real-world, finite-length time series, particularly in terms of estimation bias (Dahlhaus, 1988; Velasco & Robinson, 2000; Contreras-Cristan et al., 2006). Bias is caused by spectral blurring, sometimes referred to as spectral leakage (Percival & Walden, 1993). Furthermore, when the time series model is specified in continuous time, but observed discretely, then there is the added problem of aliasing, which if unaccounted for will further increase bias in Whittle estimates. The challenge is to account for such sampling effects and de-bias Whittle estimates, while retaining the computational efficiency of the method. We here define such a procedure, which can be combined with tapering and appropriate differencing, as recommended by Dahlhaus (1988) and Velasco & Robinson (2000). This creates an automated procedure that incorporates all modifications simultaneously, without any hand-tuning or reliance on process-specific analytic derivations such as in Taniguchi (1983).

We compare pseudo-likelihood approaches with simulated and real-world time series observations. In our example from oceanography, the de-biased Whittle likelihood results in parameter estimates that are significantly closer to maximum likelihood than standard Whittle estimates, while reducing the computational runtime of maximum likelihood by over a factor of 100, thus demonstrating the practical utility of our method. Additionally, the theoretical properties of our new estimator are studied under relatively weak assumptions, in contrast to Taniguchi (1983), Dahlhaus (1988), and Velasco & Robinson (2000). Taniguchi studies autoregressive processes that depend on a scalar unknown parameter. Dahlhaus studies processes whose spectral densities are the product of a known function with peaks that increase with sample size, and a latent spectral density that is twice continuously differentiable in frequency. Velasco and Robinson study processes that exhibit power-law behaviour at low frequencies and require continuous differentiability of the spectrum (at all frequencies except zero). Our assumptions on the spectral density of the time series will be milder. In particular, we will not require that the spectral density is continuous in frequency. Despite this, we are still able to prove consistency of de-biased Whittle estimates, together with a convergence rate matching the optimal .

2 Definitions and Notation

We shall assume that the stochastic process of interest is modelled in continuous time, however, the de-biased Whittle likelihood can be readily applied to discrete-time models, as we shall discuss later. We define as the infinite sequence obtained from sampling a zero-mean continuous-time real-valued process , where is a length- vector that specifies the process. That is, we let , where is a positive or negative integer, , and is the sampling interval. If the process is second-order stationary, we define the autocovariance sequence by for , where is the expectation operator. The power spectral density of forms a Fourier pair with the autocovariance sequence, and is almost everywhere given by

| (1) |

As is a discrete sequence, its Fourier representation is only defined up to the Nyquist frequency . Thus there may be departures between and the continuous-time process spectral density, denoted as , which for almost all is given by

| (2) |

Here (for ) is the continuous-time process autocovariance, which is related to via , when is an integer. It follows that

| (3) |

Thus contributions to outside of the range of frequencies are said to be folded or wrapped into . We have defined both and , as both quantities are important in separating aliasing from other artefacts in spectral estimation.

In addition to these theoretical quantities, we will also require certain quantities that are computed directly from a single length- sample . A widely used, but statistically inconsistent, estimate of is the periodogram, denoted , which is the squared absolute value of the Discrete Fourier Transform (DFT) defined as

| (4) |

Note that and are taken to be properties of the observed realisation and are not regarded as functions of .

3 Maximum Likelihood and the Whittle Likelihood

Consider the discrete sample , which is organized as a length column vector. Under the assumption that is drawn from , the expected autocovariance matrix is , where the superscript “” denotes the transpose, and the components of are given by . Exact maximum likelihood inference can be performed for Gaussian data by evaluating the log-likelihood (Brockwell & Davis, 1991, p.254) given by

| (5) |

where the superscript “” denotes the matrix inverse, and is the determinant of . We have removed additive and multiplicative constants not affected by in (5). The optimal choice of for our chosen model to characterize the sampled time series is then found by maximizing the likelihood function in (5) leading to

where defines the parameter space of . Because the time-domain maximum likelihood is known to have optimal properties, any other estimator will be compared with the properties of this quantity.

A standard technique for avoiding expensive matrix inversions is to approximate (5) in the frequency domain, following the seminal work of Whittle (1953). This approach approximates using a Fourier representation, and utilizes the special properties of Toeplitz matrices. Given the observed sampled time series , the Whittle likelihood, denoted is

| (6) |

where is the set of discrete Fourier frequencies given by

| (7) |

The subscript “” in is used to denote “Whittle.” We have presented the Whittle likelihood in a discretized form here, as its usual integral representation must be approximated for finite-length time series. In general, if the summation in (6) is performed over subsets of then the resulting procedure is semi-parametric.

The Whittle likelihood approximates the time-domain likelihood when all Fourier frequencies are used in (7), i.e. , and this statement can be made precise (Dzhaparidze & Yaglom, 1983). Its computational efficiency is a significantly faster , versus for maximum likelihood, as the periodogram can be computed using the Fast Fourier Transform, thus explaining its popularity in practice.

4 Modified pseudo-likelihoods

The standard version of the Whittle likelihood (6) is calculated using the periodogram, . This spectral estimate, however, is known to be a biased measure of the continuous-time process’s spectral density for finite samples, due to blurring and aliasing effects (Percival & Walden, 1993), as discussed in the introduction. Aliasing results from the discrete sampling of the continuous-time process to generate an infinite sequence, whereas blurring is associated with the truncation of this infinite sequence over a finite-time interval. The desirable properties of the Whittle likelihood rely on the asymptotic behaviour of the periodogram for large sample sizes. The bias of the periodogram for finite samples however, will translate into biased parameter estimates from the Whittle likelihood, as has been widely reported (see e.g. Dahlhaus (1988)).

In this section we propose a modified version of the Whittle likelihood in Section 4.1 which de-biases Whittle estimates. Furthermore, tapering and differencing are two well-established methods for improving Whittle estimates (Dahlhaus, 1988; Velasco & Robinson, 2000). In Sections 4.2 and 4.3 we respectively outline how the de-biased Whittle likelihood can be easily combined with either of these procedures.

4.1 The de-biased Whittle likelihood

We introduce the following pseudo-likelihood function given by

| (8) | |||||

| (9) |

where the subscript “” stands for “de-biased.” Here in (6) has been replaced by , which is the expected periodogram, and may be shown to be given by the convolution of the true modelled spectrum with the Fejér kernel , such that (Bloomfield, 1976). We call (8) the de-biased Whittle likelihood, where the set is defined as in (7).

Replacing the true spectrum with the expected periodogram in (8) is a straightforward concept, however, our key innovation lies in formulating its efficient computation without losing efficiency. If we directly use (9), then this convolution would usually need to be approximated numerically, and could be computationally expensive. Instead we utilize the convolution theorem to express the frequency-domain convolution as a time-domain multiplication (Percival & Walden, 1993, p.198), such that

| (10) |

where denotes the real part. Therefore can be exactly computed at each Fourier frequency directly from , for , by using a Fast Fourier Transform in operations. Care must be taken to subtract the variance term, , to avoid double counting contributions from . Both aliasing and blurring effects are automatically accounted for in (10) in one operation; aliasing is accounted for by sampling the theoretical autocovariance function at discrete times, while the effect of blurring is accounted for by the truncation of the sequence to finite length, and the inclusion of the triangle function in the expression.

The de-biased Whittle likelihood can also be used for discrete-time process models, as (10) can be computed from the theoretical autocovariance sequence of the discrete process in exactly the same way. Furthermore, the summation in (8) can be performed over a reduced range of frequencies to perform semi-parametric inference. If the analytic form of is unknown or expensive to evaluate, then it can be approximated from the spectral density using Fast Fourier Transforms, thus maintaining computational efficiency.

As an aside, we point out that computing the standard Whittle likelihood of (6) with the aliased spectrum defined in (1), without accounting for spectral blurring, would in general be more complicated than using the expected periodogram . This is because the aliased spectrum seldom has an analytic form for continuous processes, and must be instead approximated by either explicitly wrapping in contributions from from frequencies higher than the Nyquist as in (3), or via an approximation to the Fourier transform in (1). This is in contrast to the de-biased Whittle likelihood, where the effects of aliasing and blurring have been computed exactly in one single operation using (10). Thus addressing aliasing and blurring together using the de-biased Whittle likelihood is simpler and computationally faster to implement than accounting for aliasing alone.

4.2 The de-biased tapered Whittle likelihood

To ameliorate spectral blurring of the periodogram, a standard approach is to pre-multiply the data sequence with a weighting function known as a data taper (Thomson, 1982). The taper is chosen to have spectral properties such that broadband blurring will be minimized, and the variance of the spectral estimate at each frequency is reduced, although the trade-off is that tapering increases narrowband blurring as the correlation between neighbouring frequencies increases.

The tapered Whittle likelihood (Dahlhaus, 1988) corresponds to replacing the direct spectral estimator formed from in (4) with one using the taper

| (11) |

where is real-valued. Setting for recovers the periodogram estimate of (6). To estimate parameters we then maximize

| (12) |

where the subscript “” denotes that a taper has been used. Velasco & Robinson (2000) demonstrated that for certain discrete processes it is beneficial to use this estimator, rather than the standard Whittle likelihood, for parameter estimation, particularly when the spectrum exhibits a high dynamic range. Nevertheless, tapering in itself will not remove all broadband blurring effects in the likelihood, because we are still comparing the tapered spectral estimate against the theoretical spectrum, and not against the expected tapered spectrum. Furthermore, there remain the issues of narrowband blurring, as well as aliasing effects with continuous sampled processes.

A useful feature of our de-biasing procedure is that it can be naturally combined with tapering. To do this we define the likelihood given by

| (13) | |||||

with as defined in (11) such that . We call the de-biased tapered Whittle likelihood and the expected tapered spectrum which can be computed exactly and efficiently using a similar calculation to (10) to find such that

Accounting for the particular taper used in accomplishes de-biasing of the tapered Whittle likelihood, just as using the expected periodogram does for the standard Whittle likelihood. The time-domain kernel can be pre-computed using FFTs or using a known analytical form. Then during optimization, an FFT of this fixed kernel multiplied by the autocovariance sequence is taken at each iteration. Thus the de-biased tapered Whittle likelihood is also an pseudo-likelihood estimator.

Both the de-biased tapered and de-biased periodogram likelihoods have their merits, but the trade-offs are different with nonparametric spectral density estimation than they are with parametric model estimation. Specifically, although tapering decreases the variance of nonparametric estimates at each frequency, it conversely may increase the variance of estimated parameters. This is because the taper is reducing degrees of freedom in the data, which increases correlations between local frequencies. On the other hand, the periodogram creates broadband correlations between frequencies, especially for processes with a high dynamic range, which also contributes to variance in parameter estimates. We explore these trade-offs in greater detail in Section 5.

4.3 The de-biased Whittle likelihood with differenced data

Another method of reducing the effects of blurring on Whittle estimates is to fit parameters to the differenced process. This was illustrated in Velasco & Robinson (2000), where the Whittle likelihood was found to perform poorly with fractionally integrated processes that exhibited higher degrees of smoothness, but improved when working with the differenced process as this reduced the dynamic range of the spectrum and hence decreased broadband blurring.

Whittle likelihood using the differenced process proceeds as follows. Define for the continuous-time differenced process, and for the sampled process. The spectral density of , denoted , can be found from via the relationship

Then the Whittle likelihood for differenced processes is performed by maximizing

| (14) |

where is the periodogram of the sample . The set of Fourier frequencies are now , where one degree of freedom has been lost by differencing, and a second has been lost as the zero frequency should be excluded because the spectral density is now equal to zero here. The de-biased Whittle likelihood is also straightforward to compute from over the same set of Fourier frequencies

| (15) | ||||

where and is the autocovariance of where

from direct calculation. This likelihood remains an operation to evaluate, as computing all required from is , and the rest of the calculation is as in (10). Differencing and tapering can be easily combined in , with both the standard and de-biased Whittle likelihoods. Furthermore, differencing can be applied multiple times if required.

To see how differencing can reduce the variance of the estimators, we investigate the variance of the score of the de-biased Whittle likelihood, which (as derived in equation (33) of the Appendix material) can be bounded for each scalar by

| (16) |

where is the upper bound on the partial derivative of the expected periodogram with respect to , and and are upper and lower bounds on the spectral density respectively (assumed finite and non-zero). The significance of (16) is that the bound on the variance of the score is controlled by the dynamic range of the spectrum, as a high dynamic range will lead to large values of . This suggests that one should difference a process with steep spectral slopes, as this will typically reduce the dynamic range of the spectrum thus reducing , in turn decreasing the bound on the variance. Differencing multiple times however may eventually send to zero, such that at some point the ratio will increase, in turn increasing the bound on the variance.

5 Monte-Carlo Simulations

All simulation results in Sections 5 and 6 can be exactly reproduced in MATLAB, and all data can be downloaded, using the software available at www.ucl.ac.uk/statistics/research/spg/software. As part of the software we provide a simple package for estimating the parameters of any time series observation modelled as a second-order stationary stochastic process specified by its autocovariance.

5.1 Comparing the standard and de-biased Whittle likelihood

In this section we investigate the performance of the standard and de-biased Whittle likelihoods in a Monte Carlo study using observations from a Matérn process (Matérn, 1960), as motivated by the simulation studies of Anitescu et al. (2012) who study the same process. The Matérn process is a three-parameter continuous Gaussian process defined by its continuous-time unaliased spectrum

| (17) |

The parameter sets the magnitude of the variability, is the damping timescale, and controls the rate of spectral decay, or equivalently the smoothness or differentiability of the process. For large the power spectrum exhibits a high dynamic range, and the periodogram will be a poor estimator of the spectral density due to blurring. Conversely, for small there will be departures between the periodogram and the continuous-time spectral density because of aliasing. We will therefore investigate the performance of estimators over a range of values.

In Fig. 1 we display the bias and standard deviation of the different Whittle estimators for the three parameters where varies from in intervals of . We fix and , but estimate all three parameters assuming they are unknown. For each value of , we simulate 10,000 time series each of length , and use these replicated series to calculate biases and standard deviations for each estimator. We implement several different Whittle estimators: standard Whittle likelihood (6), tapered Whittle likelihood (12), and differenced Whittle likelihood (14). In addition, for each of these we implement the de-biased version (equations (8), (13), and (15), respectively). The choice of data taper is the Discrete Prolate Spheroidal Sequence (DPSS) taper (Slepian & Pollak, 1961), with bandwidth parameter equal to 4, where performance was found to be broadly similar across different choices of bandwidth (not shown). We also performed fits using combined differenced and tapered versions of both the standard and de-biased Whittle likelihoods, as discussed in Section 4.3, and found that results were virtually identical to tapering without differencing (also not shown). The optimization is performed in MATLAB using fminsearch, and uses identical settings for all likelihoods. Initialized guesses for the slope and amplitude are found using a least squares fit in the range , and the initial guess for the damping parameter is set at a mid-range value of 100 times the Rayleigh frequency (i.e. .)

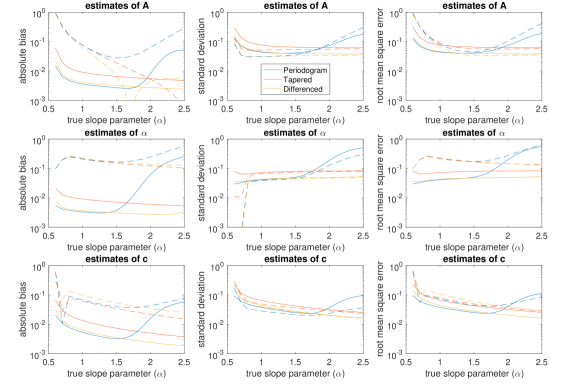

The first column in Fig. 1 displays the absolute bias of each estimator for the three Matérn parameters. The absolute biases are displayed on a log10 scale, and in many instances we can see bias reductions of over a factor of 10 in each of the parameters, representing over a 90% bias reduction. The “U” shape over the range of values, with the standard Whittle likelihood using the periodogram, corresponds to aliasing effects for small and blurring effects for large . Differencing and tapering ameliorate the blurring effects for high , but not the aliasing effects for low . De-biased methods, particularly when combined with differencing, remove bias most consistently across the full range of values.

The second column displays the standard deviations of the estimates. These are broadly comparable between the methods, although methods that use the periodogram suffer from reduced performance for high due to broadband spectral blurring. The dip when estimating for low values with standard methods is due to boundary effects in the optimization. Here the estimate of cannot go below 0.5, and due to severe aliasing, the optimization typically converges to this lower bound when the true is less than 0.7, such that the estimate is badly biased, but not variable. As we have used 10,000 replicates, the standard error of the reported biases can be observed by eye, by dividing the corresponding standard deviations by , meaning that the observed bias reductions using our approach appear highly significant.

The final column displays the root-mean-square-error (RMSE), thus combining information from the first two columns. With standard methods, the observed biases are in general larger than the standard deviations, so the shapes of the RMSE curves generally follow those of the biases. The de-biased methods are significantly less biased such that standard deviation is now the main contribution to RMSE. Overall, because bias tends to dominate variance with the standard Whittle estimates, the de-biased methods improve upon the standard methods with only a few exceptions, and can reduce error by an order of magnitude.

| Inference Method | Eqn | Bias | SD | RMSE | |||

|---|---|---|---|---|---|---|---|

| Standard Whittle (periodogram) | (6) | 23. | 69% | 10. | 34% | 26. | 66% |

| De-Biased Whittle (periodogram) | (8) | 3. | 96% | 12. | 97% | 13. | 75% |

| Standard Whittle (tapered) | (12) | 18. | 11% | 12. | 23% | 23. | 12% |

| De-Biased Whittle (tapered) | (13) | 2. | 60% | 14. | 15% | 14. | 41% |

| Standard Whittle (differenced) | (14) | 18. | 99% | 9. | 33% | 22. | 09% |

| De-Biased Whittle (differenced) | (15) | 1. | 19% | 8. | 90% | 8. | 99% |

Finally, in Table 1 we aggregate all information in Fig. 1 to provide the average percentage bias (relative to the true parameter values), standard deviation, and RMSE for each likelihood estimator and each parameter combination. Of all the estimators, the de-biased Whittle likelihood using the differenced process performs best. Overall, of the three modifications to the standard Whittle likelihood—de-biasing, tapering and differencing—the de-biasing method proposed here is the single procedure that yields the greatest overall improvement in parameter estimation.

5.2 Comparison with time-domain estimators

Time-domain pseudo-likelihood procedures have been proposed in Anitescu et al. (2012) (see also Dutta & Mondal (2015) and Anitescu et al. (2016)) who use Hutchinson trace estimators and circulant embedding techniques, removing the need to calculate a matrix inverse or determinant. We contrast the approach proposed here with that of Anitescu et al. (2012) using the MATLAB package “ScalaGauss” supplied by those authors at http://press3.mcs.anl.gov/scala-gauss/software/. We use the same parameters of their example code for a Matérn process, which estimates the damping parameter, and assumes the slope parameter is known, and the amplitude parameter is known up to a proportion of the damping parameter. The parameters used, when transformed into the form of (17), are and . As the slope parameter is high, we fit the de-biased Whittle to the differenced process. We perform 10,000 repeats and report the results in Table 2. We include results for maximum likelihood, standard Whittle likelihood, and standard and de-biased tapered likelihoods.

Standard Whittle likelihood performs extremely poorly due to the blurring effects of using the periodogram. The de-biased Whittle likelihood and the method of Anitescu et al. (2012) return estimation errors that are very close to maximum likelihood. The method of Anitescu et al. (2012) however, requires an order of magnitude more processing time than the de-biased and standard Whittle likelihood. This is because the method involves many more steps in the procedure, such as generating random numbers to form the Hutchinson trace estimators. To speed up the Anitescu et al. (2012) method, we have included results with a modified version which uses only one Hutchinson trace estimator (as opposed to the 50 used in the example code). The method still remains slower than the de-biased Whittle likelihood, and now yields slightly worse estimation accuracy. The de-biased method appears to be the best method at combining the fit quality of time-domain maximum likelihood, with the speed of the standard Whittle method.

| Inference Method | Eqn | Bias | SD | RMSE | CPU (sec.) | |||

|---|---|---|---|---|---|---|---|---|

| Maximum likelihood | (5) | 0. | 029% | 2. | 204% | 2. | 204% | 4.257 |

| Standard Whittle (periodogram) | (6) | 107. | 735% | 101. | 357% | 147. | 916% | 0.139 |

| De-Biased Whittle (differenced) | (15) | 0. | 030% | 2. | 212% | 2. | 212% | 0.157 |

| Standard Whittle (tapered) | (12) | 25. | 550% | 20. | 459% | 32. | 731% | 0.168 |

| De-Biased Whittle (tapered) | (13) | 0. | 023% | 2. | 558% | 2. | 558% | 0.198 |

| Anitescu et al. (normal version) | 0. | 029% | 2. | 205% | 2. | 205% | 1.998 | |

| Anitescu et al. (faster version) | 0. | 035% | 2. | 223% | 2. | 223% | 0.438 | |

6 Application to Large-Scale Oceanographic Data

In this section we examine the performance of our method when applied to a real-world large-scale dataset, by analysing data obtained from the Global Drifter Program, which maintains a publicly-downloadable database of position measurements obtained from freely-drifting satellite-tracked instruments known as drifters (http://www.aoml.noaa.gov/phod/dac/index.php). In total over 23,000 drifters have been deployed, with interpolated six-hourly data available since 1979 and one-hourly data since 2005 (see Elipot et al. (2016)), with over 100 million data points available in total. The collection of such data is pivotal to the understanding of ocean circulation and its impact on the global climate system (see Griffa et al. (2007)); it is therefore essential to have computationally efficient methods for their analysis.

In Fig. 2, we display 50-day position trajectories and corresponding velocity time series for three drifters from the one-hourly data set, each from a different major ocean. These trajectories can be considered as complex-valued time series, with the real part corresponding to the east/west velocity component and the imaginary part corresponding to the north/south velocity component. We then plot the periodogram of the complex-valued series, which has different power at positive and negative frequencies, distinguishing directions of rotation on the complex plane (Schreier & Scharf, 2010). The de-biased Whittle likelihood for complex-valued proper processes is exactly the same as (8)–(10) (see also Sykulski et al. (2016)), where the autocovariance sequence of a complex-valued process is . For proper processes the complementary covariance is at all lags (Schreier & Scharf, 2010), and can thus be ignored in the likelihood, as captures all second-order structure in the zero-mean process.

We model the velocity time series as a complex-valued Matérn process, with power spectral density given in (17), as motivated by Sykulski et al. (2016) and Lilly et al. (2017). To account for a type of circular oscillations in each time series known as inertial oscillations, which create an off-zero spike on one side of the spectrum, we fit the Matérn process semi-parametrically to the opposite “non-inertial” side of the spectrum (as displayed by the red-solid line in the figure). We overlay the fit of the de-biased Whittle likelihood to the periodograms in Fig. 2. For a full parametric model of surface velocity time series, see Sykulski et al. (2016). We have selected drifters without noticeable tidal effects; for de-tiding procedures see Pawlowicz et al. (2002).

| Drifter | Inference | Damping | Slope | Diffusivity | CPU (s) | |||

|---|---|---|---|---|---|---|---|---|

| location | method | (days) | (m2/s) | |||||

| Maximum likelihood | 10. | 65 | 1.460 | 0. | 49 | 20. | 89 | |

| Atlantic | De-biased Whittle | 9. | 84 | 1.462 | 0. | 44 | 0. | 06 |

| Standard Whittle | 30. | 19 | 1.097 | 0. | 65 | 0. | 02 | |

| Maximum likelihood | 10. | 63 | 1.829 | 5. | 09 | 31. | 65 | |

| Pacific | De-biased Whittle | 11. | 82 | 1.886 | 6. | 00 | 0. | 09 |

| Standard Whittle | 19. | 59 | 1.566 | 7. | 18 | 0. | 02 | |

| Maximum likelihood | 21. | 76 | 1.825 | 30. | 47 | 30. | 37 | |

| Indian | De-biased Whittle | 19. | 91 | 1.802 | 22. | 71 | 0. | 11 |

| Standard Whittle | 39. | 99 | 1.545 | 31. | 19 | 0. | 01 | |

We estimate the Matérn parameters for each time series using the de-biased and regular Whittle likelihood, as well as exact maximum likelihood. The latter of these methods can be performed over only positive or negative frequencies by first decomposing the time series into analytic and anti-analytic components using the discrete Hilbert transform, see Marple (1999), and then fitting the corresponding signal to an adjusted Matérn autocovariance that accounts for the effects of the Hilbert transform. The details for this procedure are provided in the online code.

The parameter estimates from the three likelihoods are displayed in Table 3, along with the corresponding CPU times. We reparametrize the Matérn to output three important oceanographic quantities: the damping timescale, the decay rate of the spectral slope, and the diffusivity (which is the rate of particle dispersion) given by (Lilly et al., 2017, eq.(43)). From Table 3 it can be seen that the de-biased Whittle and maximum likelihoods yield similar values for the slope and damping timescale, however, regular Whittle likelihood yields parameters that differ by around 15% for the slope, and over 100% for the damping timescale. These are consistent with the significant biases reported in our simulation studies in Section 5. The diffusivity estimates vary across all estimation procedures, and this variability is likely due to the fact that diffusivity is a measure of the spectrum at frequency zero, hence estimation is performed over relatively few frequencies. The time-domain maximum likelihood is over two orders of magnitude slower to execute than the de-biased Whittle likelihood. When this difference is scaled up to fitting all time series in the Global Drifter Program database, then time-domain maximum likelihood becomes impractical for such large datasets (taking years rather than days on the machine used in this example). The de-biased Whittle likelihood, on the other hand, retains the speed of Whittle likelihood, whilst returning estimates that are close to maximum likelihood. This section therefore serves as a proof of concept of how the de-biased Whittle likelihood is a useful tool for efficiently estimating parameters from large datasets.

7 Properties of the De-Biased Whittle Likelihood

In this section, we establish consistency and optimal convergence rates for de-biased Whittle estimates with Gaussian processes. We will assume that the process is Gaussian in our proofs, however, formally we only require that the Fourier transform of the process is Gaussian. This is in general a weaker requirement. Processes that are non-Gaussian in the time domain may in fact have Fourier transforms with approximately Gaussian distributions for sufficiently large sample size. This is a consequence of a central limit theorem (Brillinger, 2001, p.94), which also provides formal conditions when the Gaussian assumption is asymptotically valid. Serroukh & Walden (2000) provide practical examples which satisfy such conditions.

To show that de-biased Whittle estimates converge at on optimal rate, the main challenge is that although our pseudo-likelihood accounts for the bias of the periodogram, there is still present the broadband correlation between different frequencies caused by the leakage associated with the Fejér kernel. This is what prevents the de-biased Whittle likelihood from being exactly equal to the time-domain maximum likelihood for Gaussian data. To establish optimal convergence rates, we bound the asymptotic behaviour of this correlation. The statement is provided in Theorem 1, with the proof provided in the Appendix. The proof is composed of several lemmas which, for example, place useful bounds on the expected periodogram, the variance of linear combinations of the periodogram at different frequencies, and also the first and second derivatives of the de-biased Whittle likelihood. Together these establish that the de-biased Whittle likelihood is a consistent estimator with estimates that converge in probability at an optimal rate of , under relatively weak assumptions.

Theorem 1.

Assume that is an infinite sequence obtained from sampling a zero-mean continuous-time real-valued process , which satisfies the following assumptions:

-

1.

The parameter set is compact with a non-null interior, and the true length- parameter vector lies in the interior of .

-

2.

Assume that for all and , the spectral density of the sequence is bounded below by , and bounded above by .

-

3.

If , then there is a space of non-zero measure such that for all in this space .

-

4.

Assume that is continuous in and Riemann integrable in .

-

5.

Assume that the expected periodogram , as defined in (9), has two continuous derivatives in which are bounded above in magnitude uniformly for all , where the first derivative in also has frequencies in that are non-zero.

Then the estimator

for a sample , where is the de-biased Whittle likelihood of (8), satisfies

Standard theory shows that standard Whittle estimates are consistent with optimal convergence rates for Gaussian processes if the spectrum (and its first and second partial derivatives in ) are continuous in and bounded from above and below (see Dzhaparidze & Yaglom (1983)), as well as being twice continuously differentiable in . In contrast, we have not required that the spectrum nor its derivatives are continuous in ; such that Theorem 1 will hold for discontinuous spectra, as long as the other assumptions are satisfied such as Riemann integrability. As detailed in the Appendix, this is possible because the expectation of the score is now zero after de-biasing (equation (32) in the Appendix material, which would not be the case for the standard Whittle likelihood), such that we only need to consider the variance of the score and Hessian. To control these variances we make repeated use of a bound on the variance of linear combinations of the periodogram (Lemma 8)—a result previously established in (Giraitis & Koul, 2013, Theorem 3.1) under a different set of assumptions.

It can be easily shown that the assumptions in Theorem 1 are weaker than standard Whittle assumptions, despite requiring statements on the behaviour of the expected periodogram in Assumption 5. This is because if the spectral density (and its first and second partial derivatives in ) are continuous in both and , then it can be shown by applying the Leibniz’ integration rule to the first and second derivatives of (9) in , that twice continuously differentiable in implies that is twice continuously differentiable in . To show this we make use of (Stein & Shakarchi, 2003, Prop 3.1) which states that the convolution of two integrable and periodic functions is itself continuous. This result can also be used to show that is always continuous in , even if is not, as from (9) we see that is the convolution of and the Fejér kernel—two functions which are integrable and -periodic in . Therefore, not only does remove bias from blurring and aliasing, and is computationally efficient to compute, but it also has desirable theoretical properties leading to consistency and optimal convergence rates of de-biased Whittle estimates under weaker assumptions.

Appendix

In the Appendix we prove that de-biased Whittle estimates converge at an optimal rate (Theorem 1). To prove Theorem 1 we will first show that the debiased Whittle estimator is consistent (Proposition 1) in a series of steps using eight Lemmas. Consistency will be established by showing that properties of the debiased Whittle estimator converge to that of the standard Whittle estimator. Then having established consistency, we establish the convergence rates via Lemma 9, where the differences between the debiased and standard Whittle estimators will become especially clear. This allows us to establish optimal convergence rates under weaker assumptions in Theorem 1, where we shall not require that the spectral density is continuous in frequency.

Without loss of generality, we shall assume that the sampling interval is set to in this section. We need to make the following assumptions on the stochastic process to achieve consistency and optimal convergence rates:

-

1.

The parameter set is compact with a non-null interior, and the true length- parameter vector lies in the interior of .

-

2.

Assume that for all and , the spectral density of the sequence is bounded below by , and bounded above by .

-

3.

If , then there is a space of non-zero measure such that for all in this space .

-

4.

Assume that is continuous in and Riemann integrable in .

-

5.

Assume that the expected periodogram , as defined in (9), has two continuous derivatives in which are bounded above in magnitude uniformly for all , where the first derivative in also has frequencies in that are non-zero.

We start with the following lemma which bounds the behaviour of the expected periodogram.

Lemma 1.

For all and , the expected periodogram is bounded below (by a positive real number), and above, independently of and .

Proof.

We start by noting that

as given in (9) when . From Assumption 2 we have that and also that . It therefore follows that

such that the expected periodogram is upper bounded by . We also have that

such that the expected periodogram is lower bounded by . ∎

Following the work of Taniguchi (1979) and Guillaumin et al. (2017), we now introduce the following quantity

| (18) |

for all and . We also define

| (19) |

The minimum of for fixed is well defined since the set is compact, and the function is continuous in (from Assumptions 1 and 5). However in cases where the minimum is not unique but exists at multiple parameter values, will denote any of these values, chosen arbitrarily. We proceed with seven further lemmas that are required in proving Proposition 1 which establishes consistency, starting with Lemma 2 which we repeatedly use in the lemmas that follow.

Lemma 2.

The function , defined on the set of positive real numbers, admits a global unique minimum for where it takes the value 1.

Proof.

This can be easily shown by taking the derivative of . ∎

Proof.

We have that for all

where from Lemma 2 we have an equality if and only if for all , which is clearly satisfied for . ∎

This shows that for all , the function reaches a global minimum at the true parameter vector , although we have not proven any uniqueness properties at this stage. Now because is changing with , we require the following five lemmas.

Lemma 4.

Define such that is continuous at . For all , there exists and an integer such that for all , if is such that

Proof.

By Assumption 4, is Riemann integrable in , and therefore is continuous almost everywhere. It follows that there then exists an such that is continuous at . Now let . By continuity of at , there exists such that for all such that . According to (Brockwell & Davis, 1991, p.71) there exists an integer such that, for all

We then have for such that

Observing that for (in the first integral of the above equation) and given our choice of , we have by the triangle inequality , such that and thus we obtain

This concludes the proof. ∎

Lemma 5.

Recalling the definition of in (18), we have that

| (20) |

Proof.

We have

Define

where , i.e. corresponds to the closest smaller Fourier frequency to . Then,

We shall now use the bounded convergence theorem, for which we need to show that converges almost everywhere. We recall is continuous almost everywhere. Now take such that is continuous at . Let . Using Lemma 4, there exists and an integer such that, for all satisfying , and for all , .

Additionally, converges to when goes to infinity, such that there exists an integer such that for . Therefore, eventually in , we have . Thus, converges to . As we have shown this for almost every , we have proved the point-wise convergence of to almost everywhere with respect to on . The same reasoning shows the point-wise convergence of to and that of to almost everywhere with respect to on , as and are bounded below. As the finite intersection of Lebesgue sets each having measure is a Lebesgue set with measure , converges point-wise almost everywhere to the integrand of the right-hand-side of (20). Moreover, is clearly upper bounded in absolute value by an integrable function according to Lemma 1, such that we can apply the dominated convergence theorem and conclude that the sum on the left-hand-side of (20) converges to the integral on the right-hand-side of (20) as goes to infinity. ∎

Lemma 6.

If and if is a sequence of parameter vectors converging to , then it follows that

Proof.

By the triangle inequality and having proved Lemma 5 we only need to prove that

converges to zero. This quantity can be written as

which converges to zero because of the upper bound on the absolute derivative of and lower bound for . ∎

Lemma 7.

If is a sequence of parameter vectors such that converges to zero when goes to infinity, then converges to .

Proof.

Let be a sequence of parameter vectors such that

| (21) |

We assume, with the intent to reach a contradiction, that the sequence does not converge to . By compactness of , there exists an increasing function from the set of positive integers to the set of positive integers, denoted , and distinct from , such that the sequence converges to as goes to infinity.

We now show that the functions and , defined on , are asymptotically equivalent. For this, we first need the following lemma where we bound the asymptotic variance of linear combinations of the periodogram, a result previously established in (Giraitis & Koul, 2013, Theorem 3.1) and Guillaumin et al. (2017) under different sets of assumptions.

Lemma 8.

Assume that is an infinite sequence obtained from sampling a zero-mean continuous-time real-valued process with a spectral density that is bounded above by the finite value . Additionally, assume that the deterministic function has a magnitude that is bounded above by for all . Then linear combinations of values of the periodogram, , at different frequencies, have a variance that is upper bounded by

Proof.

By definition, for

Then, using the fact that the Fourier transform of a Gaussian process is also Gaussian, we may use Isserlis’ theorem (Isserlis, 1918) and so obtain that

where is the Discrete Fourier Transform. Thus it follows that

| (22) |

Recalling that , and after defining the vector for , such that , then we can represent the covariance of the Fourier transform as given by

| (23) |

Substituting (23) into (22), it follows that

| (24) |

and so (24) is a positive quadratic form. We note that . Therefore these relationships, given (22), imply that

| (25) |

It can then easily be verified that

where is the identity matrix and is given in (7). This follows as any off-diagonal term for . Therefore (25) simplifies to

| (26) |

The matrix is Hermitian, so it can be written where is unitary and is the diagonal matrix consisting of the set of eigenvalues , such that

| (27) |

where denotes the maximal eigenvalue of , and the last equality uses that . It is well known that for a Toeplitz covariance matrix with eigenvalues and associated with the spectral density , then , see for example (Lee & Messerschmitt, 1988, p. 384). Therefore, by combining (26) and (27) it follows that

as , thus yielding the desired result. ∎

Remembering that , we thus have

We are now able to state a consistency theorem for our estimator .

Proposition 1.

Assume that is an infinite sequence obtained from sampling a zero-mean continuous-time real-valued process which satisfies Assumptions (1–5). Then the estimator

for a sample , where is the de-biased Whittle likelihood of (8), satisfies

Proof.

Denote and defined for any . We have

We have shown in Lemma 1 that is bounded below in both variables and by a positive real number, independently of . Therefore, making use of Lemmas 1 and 8 we have

| (28) |

where indicates that the convergence is in probability, as the difference is of stochastic order . In particular (28) implies that

i.e.

| (29) |

Relation (28) also implies that

| (30) |

such that using the triangle inequality, (29) and (30), we get

We then obtain the stated proposition making use of Lemmas 3 and 7. ∎

Before proceeding to prove optimal convergence rates of de-biased Whittle estimates (Theorem 1), we require one further lemma.

Lemma 9.

Assume that is an infinite sequence obtained from sampling a zero-mean continuous-time real-valued process which satisfies Assumptions (1–5). Then the pseudo-likelihood , defined in (8), has first and second derivatives in each component of , denoted , for , that satisfy

and

respectively, where

Proof.

We start by evaluating the score directly from (8)

| (31) |

If we take the expectation of (31) then, recalling that ,

| (32) |

Note that for finite sample sizes in general , so the expectation of the score would not exactly be zero for the standard Whittle likelihood.

Furthermore, using Lemma 8 with , the variance of the score takes the form of

| (33) |

where and from Lemma 1. We can therefore conclude using Chebyshev’s inequality (Papoulis, 1991, pp.113–114) that we can fix such that

where denotes the probability of the argument. We may therefore deduce that

Next we examine the Hessian. Again from (8) we have

thus as it follows that

| (34) |

As is bounded above and below (from Lemma 1), and is bounded above and also bounded below at frequencies (using Assumption 2) we have

| (35) |

Furthermore, we have that,

We define

In this instance we can bound the variance, using Lemma 8, by

| (36) |

We can therefore conclude from (34)–(36), and using Chebyshev’s inequality, that

This yields the second result. ∎

Lemma 9 shows the order of the first and second derivative of . Mutatis mutandis we can show the corresponding results hold for and , the Hessian matrix. We have now proved the ancillary results required to prove Theorem 1.

Proof.

We let the -vector lie in a ball centred at the -vector with radius (this is a shrinking radius as Proposition 1 has shown consistency). We additionally define the Hessian matrix , having entries given by

Then as Proposition 1 has shown we can write for some , applying the Taylor expansion of (Brockwell & Davis, 1991, p.201),

| (37) |

We shall now understand the terms of this expression better. We note directly that

| (38) |

We see from this expression, coupled with Lemma 8 and Chebyshev’s inequality, that

such that the limiting behaviour of the second partial derivatives need not be determined, as they are by assumption finite (Assumption 5). Then if we define

and by taking expectations of (38) we see that

as we have already noted that both and are bounded and Riemann integrable as per Lemma 9. Furthermore,

as is bounded above and below independently of , and is bounded above, and bounded below for frequencies (from Assumption 5).

We also note that the elements of the matrix take the form of linear combinations of and so the element-wise extension of Lemma 8 applies. This means

| (39) |

From Proposition 1 we then observe that

By applying the Taylor expansion of (Brockwell & Davis, 1991, p.201), we observe that

where neither of the terms depend on or because of the upper bound on the magnitude of the first and second derivatives of with respect to in Assumption 5. Therefore, and because is bounded below from Assumption 2,

since converges to . Writing the Hessian at as

where

is bounded according to our set of assumptions, we then observe using the triangle inequality that

The first sum converges to zero in probability given the bound of the derivative of with respect to from Assumption 5, and the second sum converges to zero according to Lemma 8. It follows that

| (40) |

References

- Anitescu et al. (2016) Anitescu, M., Chen, J. & Stein, M. L. (2016). An inversion-free estimating equations approach for Gaussian process models. J. Comput. Graph. Stat. 26, 98–107.

- Anitescu et al. (2012) Anitescu, M., Chen, J. & Wang, L. (2012). A matrix-free approach for solving the parametric Gaussian process maximum likelihood problem. SIAM J. Sci. Comput. 34, A240–A262.

- Bloomfield (1976) Bloomfield, P. (1976). Fourier analysis of time series: an introduction. John Wiley.

- Brillinger (2001) Brillinger, D. R. (2001). Time series: data analysis and theory. SIAM.

- Brockwell & Davis (1991) Brockwell, P. J. & Davis, R. A. (1991). Time series: theory and methods. Springer.

- Choudhuri et al. (2004) Choudhuri, N., Ghosal, S. & Roy, A. (2004). Contiguity of the Whittle measure for a Gaussian time series. Biometrika 91, 211–218.

- Contreras-Cristan et al. (2006) Contreras-Cristan, A., Gutiérrez-Peña, E. & Walker, S. G. (2006). A note on Whittle’s likelihood. Commun. Stat.-Simul. C. 35, 857–875.

- Dahlhaus (1988) Dahlhaus, R. (1988). Small sample effects in time series analysis: A new asymptotic theory and a new estimate. Ann. Stat. 16, 808–841.

- Dutta & Mondal (2015) Dutta, S. & Mondal, D. (2015). An h-likelihood method for spatial mixed linear models based on intrinsic auto-regressions. J. R. Statist. Soc. B 77, 699–726.

- Dzhaparidze & Yaglom (1983) Dzhaparidze, K. O. & Yaglom, A. M. (1983). Spectrum parameter estimation in time series analysis. In Developments in Statistics, P. R. Krishnaiah, ed. Academic Press, Inc., pp. 1–96.

- Elipot et al. (2016) Elipot, S., Lumpkin, R., Perez, R. C., Lilly, J. M., Early, J. J. & Sykulski, A. M. (2016). A global surface drifter data set at hourly resolution. J. Geophys. Res. Oceans 121, 2937–2966.

- Fan et al. (2014) Fan, J., Qi, L. & Xiu, D. (2014). Quasi-maximum likelihood estimation of GARCH models with heavy-tailed likelihoods. J. Bus. Econ. Stat. 32, 178–191.

- Fuentes (2007) Fuentes, M. (2007). Approximate likelihood for large irregularly spaced spatial data. J. Am. Stat. Soc. 102, 321–331.

- Giraitis & Koul (2013) Giraitis, L. & Koul, H. L. (2013). On asymptotic distributions of weighted sums of periodograms. Bernoulli 19, 2389–2413.

- Griffa et al. (2007) Griffa, A., Kirwan, A. D., Mariano, A. J., Özgökmen, T. & Rossby, T. (2007). Lagrangian analysis and prediction of coastal and ocean dynamics. Cambridge University Press.

- Guillaumin et al. (2017) Guillaumin, A. P., Sykulski, A. M., Olhede, S. C., Early, J. J. & Lilly, J. M. (2017). Analysis of non-stationary modulated time series with applications to oceanographic surface flow measurements. Journal of Time Series Analysis 38, 668–710.

- Guinness & Fuentes (2017) Guinness, J. & Fuentes, M. (2017). Circulant embedding of approximate covariances for inference from Gaussian data on large lattices. J. Comput. Graph. Stat. 26, 88–97.

- Isserlis (1918) Isserlis, L. (1918). On a formula for the product-moment coefficient of any order of a normal frequency distribution in any number of variables. Biometrika 12, 134–139.

- Jesus & Chandler (2017) Jesus, J. & Chandler, R. E. (2017). Inference with the Whittle likelihood: A tractable approach using estimating functions. J. Time Ser. Anal. 38, 204–224.

- Krafty & Collinge (2013) Krafty, R. T. & Collinge, W. O. (2013). Penalized multivariate Whittle likelihood for power spectrum estimation. Biometrika 100, 447–458.

- Lee & Messerschmitt (1988) Lee, E. A. & Messerschmitt, D. G. (1988). Digital communication. Kluwer Academic Publishers, Boston.

- Lilly et al. (2017) Lilly, J. M., Sykulski, A. M., Early, J. J. & Olhede, S. C. (2017). Fractional Brownian motion, the Matérn process, and stochastic modeling of turbulent dispersion. Nonlinear Proc. Geoph. 24, 481– 514.

- Marple (1999) Marple, S. L. (1999). Computing the discrete-time “analytic” signal via FFT. IEEE T. Signal Proces. 47, 2600–2603.

- Matérn (1960) Matérn, B. (1960). Spatial Variation: Stochastic Models and Their Application to Some Problems in Forest Surveys and Other Sampling Investigations. Statens Skogsforskningsinstitut.

- Matsuda & Yajima (2009) Matsuda, Y. & Yajima, Y. (2009). Fourier analysis of irregularly spaced data on . J. R. Statist. Soc. B 71, 191–217.

- Papoulis (1991) Papoulis, A. (1991). Probability, random variables, and stochastic processes. McGraw-Hill, Inc.

- Pawlowicz et al. (2002) Pawlowicz, R., Beardsley, B. & Lentz, S. (2002). Classical tidal harmonic analysis including error estimates in MATLAB using T_TIDE. Computers & Geosciences 28, 929–937.

- Percival & Walden (1993) Percival, D. B. & Walden, A. T. (1993). Spectral Analysis for Physical Applications: Multitaper and conventional univariate techniques. Cambridge University Press.

- Schreier & Scharf (2010) Schreier, P. J. & Scharf, L. L. (2010). Statistical signal processing of complex-valued data: the theory of improper and noncircular signals. Cambridge University Press.

- Serroukh & Walden (2000) Serroukh, A. & Walden, A. T. (2000). Wavelet scale analysis of bivariate time series ii: statistical properties for linear processes. J. Nonparametr. Stat. 13, 37–56.

- Slepian & Pollak (1961) Slepian, D. & Pollak, H. O. (1961). Prolate spheroidal wave functions, Fourier analysis and uncertainty–I. Bell Syst. Tech. J. 40, 43–63.

- Stein & Shakarchi (2003) Stein, E. M. & Shakarchi, R. (2003). Fourier analysis: an introduction. Princeton University Press.

- Sykulski et al. (2016) Sykulski, A. M., Olhede, S. C., Lilly, J. M. & Danioux, E. (2016). Lagrangian time series models for ocean surface drifter trajectories. J. R. Statist. Soc. C 65, 29–50.

- Taniguchi (1979) Taniguchi, M. (1979). On estimation of parameters of gaussian stationary processes. J. Appl. Probab. 16, 575–591.

- Taniguchi (1983) Taniguchi, M. (1983). On the second order asymptotic efficiency of estimators of Gaussian ARMA processes. Ann. Stat. 11, 157–169.

- Thomson (1982) Thomson, D. J. (1982). Spectrum estimation and harmonic analysis. Proc. IEEE 70, 1055–1096.

- Velasco & Robinson (2000) Velasco, C. & Robinson, P. M. (2000). Whittle pseudo-maximum likelihood estimation for nonstationary time series. J. Am. Stat. Soc. 95, 1229–1243.

- Whittle (1953) Whittle, P. (1953). Estimation and information in stationary time series. Ark. Mat. 2, 423–434.