The Langevin equation for systems with a preferred spatial direction

Abstract

In this paper, we generalize the theory of Brownian motion and the Onsager-Machlup theory of fluctuations for spatially symmetric systems to equilibrium and nonequilibrium steady-state systems with a preferred spatial direction, due to an external force. To do this, we extend the Langevin equation to include a bias, which is introduced by the external force and alters the Gaussian structure of the system’s fluctuations. By solving this extended equation, we demonstrate that the statistical properties of the fluctuations in these systems can be predicted from physical observables, such as the temperature and the hydrodynamic gradients.

I Introduction

The dynamical theory of fluctuations in physical systems began to assume its modern form with the seminal papers of Onsager and Machlup Onsager and Machlup (1953); Machlup and Onsager (1953). They proposed to describe the time evolution of the thermodynamic fluctuating quantities, as well as of the hydrodynamic and electrodynamic variables, by a stochastic Langevin equation (Coffey and Kalmykov, 2012, Chapters 1-2). Originally Onsager and Machlup considered fluctuations only in equilibrium systems. Generalizations of the Langevin equation for fluctuations to nonequilibrium steady states followed, e.g. Refs. Kanazawa et al. (2015a, b); Morgado and Queirós (2016), as discussed later in this paper.

The formalism of the Langevin equation was first developed in the theory of Brownian motion (Coffey and Kalmykov, 2012, Chapters 1-2). Later Onsager and Machlup proposed Onsager and Machlup (1953); Machlup and Onsager (1953) that the fluctuations of the thermodynamic quantities can be described by the same stochastic equation, as used for the velocity fluctuations of a Brownian particle in an equilibrium system. That is, the time evolution of a fluctuating quantity obeys the following Langevin dynamics 111 The differential equation (1) is of the first order with respect to time. A second order version of the Langevin equation was considered in LABEL:MO1953 for systems, in which the fluctuations of the currents should be taken into account. This modifies merely the deterministic character of the resulting dynamics, while the steady-state probability of the fluctuations, studied in this paper, remain unchanged, cf (Chandrasekhar, 1943, Section II.3). :

| (1) |

Here and are positive constants, whose values and physical interpretation depends on the system under consideration, while is the time and is a white noise, defined as a differential of a Wiener process (Coffey and Kalmykov, 2012, Chapter 1):

| (2) |

The first term on the right hand side of Eq. (1) is a damping force with a friction constant , which ensures that the fluctuations of the quantity decay to a macroscopically observable average value . The second term, , represents physically a microscopic noise of constant intensity . It has a Gaussian nature, since in Eq. (2) is by definition a normally distributed random variable of zero mean and variance .

By solving Eq. (1), Onsager and Machlup predicted a Gaussian structure of the fluctuations in equilibrium systems. However, they explicitly omitted in their treatment Onsager and Machlup (1953) rotating systems and systems subject to an external field, because these do not possess the property of microscopic reversibility.

In this paper, we will treat the dynamical theory of fluctuations for a class of systems subject to an external field. This includes not only equilibrium systems in an external potential, such as a gravitational potential, but in addition systems maintained in a nonequilibrium steady state by an external thermodynamic, hydrodynamic or electrodynamic gradient.

Indeed, recent studies confirm a non-Gaussian structure of fluctuations in this class of systems Kanazawa et al. (2015a); Gustavsson et al. (2006); Utsumi and Saito (2009); Belousov et al. (2016). In particular, Refs. Gustavsson et al. (2006); Utsumi and Saito (2009); Belousov et al. (2016) report that the probability distribution of their fluctuations becomes asymmetric and, thus, acquires a skewness 222 Skewness is related to the third moment of a probability distribution, so that symmetric distributions, like the Gaussian, have zero skewness. .

The above mentioned theoretical and experimental studies indicate that the probability distribution of fluctuations is biased in the presence of a preferred spatial direction, which is induced by an externally applied force. In contrast to such systems, the original Langevin equation Eq. (1) has a peculiar symmetry, since it has no preferred spatial direction. For, it assigns equal probabilities to both positive and negative fluctuations of , i.e. neither positive, nor negative fluctuations are favored. However, this symmetry is broken, when an external field introduces a special direction and, as conjectured in Utsumi and Saito (2009); Belousov et al. (2016), alters the microscopic noise in this class of systems. A consequence of this is a non-Gaussian structure of their fluctuations.

This symmetry argument can be introduced formally using the principle of dissymmetry due to Curie Shubnikov (1988); Curie, P. (1894). In the treatment of Onsager and Machlup Onsager and Machlup (1953) it was implicit, that the systems they considered belong to Curie’s limiting point group of the highest symmetry Shubnikov (1988). A skewness of the fluctuations was observed in the systems, which lack some symmetry operations with respect to this point group. In all these cases the bias of the fluctuations is evidently due to a reduction of symmetry or, as introduced by Curie, due to a dissymmetry 333 “C’est la dissymétrie qui crée le phénomène” (It is the dissymetry, which creates the phenomenon) Curie, P. (1894). with respect to the systems regarded by Onsager and Machlup. In this paper, we will develop a Langevin equation for the class of physical systems with a polar direction Shubnikov (1988), which is due to the external force.

We emphasize the role of the spatial asymmetry, in contrast to the temporal asymmetry of microscopically irreversible systems, which are dealt with by the Microscopic Fluctuation Theory 444 To reverse the evolution of such systems, the sign of the external force should be changed together with that of the velocities and of the time Bertini et al. (2015). Bertini et al. (2015). It was long thought, that macroscopic irreversibility would be an immanent property of all systems in an external potential. However, it was shown, that the presence of a magnetic field does not change the time-reversal symmetry of an equilibrium system Bonella et al. (2014), while altering the probability structure of its fluctuations Utsumi and Saito (2009), as discussed earlier. In Sec. VI, we will remark, though, that a magnetic field may not belong to the class of systems, which are liable to the theoretical arguments of this paper.

Recently it was shown in LABEL:KSSH2015I, that the original Langevin equation can be extended by adding a third stochastic term, which acts as an external force and causes, together with the white noise, a non-Gaussian behavior of the fluctuations in a nonequilibrium system. To make further progress, the authors of Refs. Kanazawa et al. (2015b); Morgado and Queirós (2016) assumed, that this term is a Poisson process, and added it to Eq. (1), which then reads

| (3) |

Here is the Poisson process, also referred to as a shot noise (Stratonovich, 1967, Chapter 6), which has a constant rate parameter and, in general, a variable intensity parameter Morgado and Queirós (2016).

The Poisson process assigns a non-zero probability only to non-negative numbers, so that the role it plays in Eq. (3) is two-fold. First, it acts as an external force and, second, it introduces a bias, which makes Eq. (3) consistent with the symmetry of the class of systems considered here. Also, the microscopic noise is not represented solely by the white noise, but has an additional contribution due to the stochastic nature of the third term, .

Apparently the shot noise in Eq. (3) was motivated by its applications in the theory of electric conductance Kanazawa et al. (2015b); Blanter and Büttiker (2000). The Poisson process is discrete and makes Eq. (3) singular, cf. Morgado and Queirós (2016). Although in the theory of electric conductance this singularity is explained by the discrete nature of the electric charge Blanter and Büttiker (2000), it is a rather curious aspect of Eq. (3) for a Langevin dynamics in the context of classical statistical mechanics.

In this paper we propose to replace the shot noise in the Ansatz of Refs. Kanazawa et al. (2015b); Morgado and Queirós (2016) by a different non-Gaussian stochastic term, so that the extended Langevin equation for the fluctuations in systems with a preferred spatial direction would read:

| (4) |

Here is a positive or negative constant, while is a time differential of a Gamma process with a time scale parameter 555 The Gamma process is characterized by statistically independent increments, each having a Gamma probability distribution (Frenk and Nicolai, 2007; Dufresne et al., 1991; Steutel and Van Harn, 2003, Chapter I). , cf. (Frenk and Nicolai, 2007; Dufresne et al., 1991; Steutel and Van Harn, 2003, Chapter I). We will call an exponential noise for a reason, clarified in Sec. IV.

The first improvement achieved by Eq. (4), with respect to Eq. (3), is its statistical foundation, which is comparable to that of the original Langevin equation. For, unlike the shot noise assumed in Eq. (3), both the white noise and the exponential noise in Eq. (4) can be deduced from simplified models of the physical systems studied in this paper. In fact, Chandrasekhar (Chandrasekhar, 1943, Chapter I) considered a discrete physical model of microscopic noise and obtained the Wiener process as a continuous limit of a simple symmetric random walk. We adapt the same approach here, by modeling the effect of an external force with an asymmetric random walk, which in a similar continuous limit leads to the concept of exponential noise. To complete the analogy with Chandrasekhar’s method, we will verify in Sec. IV that, like the Wiener process, the Gamma process also arises in a more elaborate model of a random flight.

The second advantage of Eq. (4) is that, since the exponential noise is not singular, in contrast to the shot noise, it fits more naturally into a stochastic differential equation. While the Poisson process is discrete, it has a highly non-trivial continuous counterpart Ilienko (2013), which is, nonetheless, not considered by the proponents of Eq. (3). As mentioned earlier, the discrete nature of the third term in Eq. (3) introduces a singularity. In contrast to this, the Gamma process, like the Wiener process, is non-singular and assumes a simple mathematical expression in both continuous and discrete stochastic dynamics. Therefore the theory and the treatment of the Langevin equation Eq. (4) is in principle simpler than that of Eq. (3).

In Sec. V we will show that the statistical properties of the fluctuating quantity , which evolves according to the extended Langevin equation (4), can be computed in terms of the same physical parameters, which characterize the macroscopic state of the systems, studied in this paper. In particular, we will confirm the non-Gaussian structure of the fluctuations by calculating their skewness. Moreover, the sign of the skewness will depend on the external force in a manner, which was already observed by an earlier experiment Belousov et al. (2016).

Finally, we note that, while the behavior exhibited by Eq. (3) is qualitatively very similar to that of Eq. (4), they differ in principle. Equation (3) may be applicable to some systems, which are listed in LABEL:MorgadoQ2016 and which need a noise term of a discrete nature, e.g. systems of a small size. Nonetheless, in this paper we argue that Eq. (4) will find a broader range of applications for a variety of physical systems considered by classical statistical mechanics.

II A simplified physical example

To provide a physical insight into the dynamics, described by a Langevin equation of the form Eq. (3) or Eq. (4), we consider in this section a macroscopic system as an idealization of the systems studied by classical statistical mechanics, which are of interest in this paper. This will allow us to develop a decomposition of the random noise into two parts: a symmetric and asymmetric random processes, respectively. The latter will also incorporate the action of an external field. As discussed afterwards, such a decomposition is not obvious at the level of classical statistical mechanics, but it is much clearer in the example considered below or some biological systems.

First, consider a man in a boat on a lake. When the man just sits in the boat, the motion of the boat can be described by the Langevin equation (1), where the damping force would be due to the friction of the boat in the water and the white noise would be caused by spontaneous fluctuations due to the waves on the water surface and the wind blows. The stochastic term is motivated by the symmetry of this physical system, which a priori does not favor any direction of motion, so that the excitations pushing the boat forward or backward are equally probable. As a result, the boat’s velocity is distributed symmetrically around zero.

Now imagine, that the man begins to paddle, so that the boat is propelled forward, by impulses, which are imparted by the oar at a certain rate. This rate will depend on the rowing rhythm, which is, in general, irregular. For instance, the man sometimes may row slower and other times faster. This irregularity of the rowing rhythm can be accounted for statistically, if we regard the total force imparted by the rower to the boat as a random variable, which has some definite average value over a sufficiently long time interval and assumes only non-negative values. This random variable, when added to the original Langevin equation Eq. (1) as a third term, yields a stochastic dynamics of the form Eq. (3) or Eq. (4).

This new stochastic term, which represents an external force acting on the boat, has one important attribute, which distinguishes it from the white noise term discussed earlier. Namely, the external force assumes only non-negative values, since the rower propels the boat always forward. Clearly, the average velocity of the boat will then be positive. However, due to the external force, the fluctuations of the velocity are amplified in the forward direction and suppressed in the backward direction. This introduces a bias for the forward fluctuations of the boat’s velocity and, thus, reduces the symmetry of the system.

Here it is relevant to remark, that if the third term in Eq. (3) or in Eq. (4) were either a constant or another Wiener process, the resulting fluctuations would have a Gaussian structure. In fact, a certain change of variables would then transform these equations into the form of Eq. (1). Therefore, both the stochastic nature and the absence of negative values of the external force turn out to be crucial to reproduce the non-Gaussian nature of the fluctuations in the class of systems considered in this paper.

Generalizing the above argument, we will assume that in all physical systems of interest for this paper, the random noise can be represented as a linear superposition of a symmetric term, being the white noise, and some asymmetric term, which corresponds to the external force. The latter is asymmetric, because it never takes on negative values. Both models discussed in the Introduction, Eq. (3) and Eq. (4), are constructed in this way.

The described decomposition of the random noise will be assumed, inspite of the fact, that in a real thermodynamic, hydrodynamic or electrodynamic system the microscopic noise and the external force can not be easily separated. For example, a Brownian particle, which collides with the molecules of a fluid subject to a density gradient, will drift, on average, in a certain direction. Then, since both the microscopic noise and the external force acting on the Brownian particle are both caused by the collisions with the fluid molecules, it is not obvious that each of the two can be represented in the Langevin equation by a distinct separate term of stochastic nature.

Nonetheless, some biological systems Codling et al. (2008), which are traditionally modeled by stochastic dynamics, bear some similarity to the rower example. For instance, a bacterium, swimming in a liquid by moving its flagellum, is an obvious parallel with the man paddling a boat.

III White noise

This section reviews a simple 1-Dimensional (1D) random walk, as it was used by Chandrasekhar (Chandrasekhar, 1943, Chapter I) to motivate the white noise term for the Langevin dynamics described by Eqs. (1), (3) and (4). In a slightly modified form, the same approach will be adopted in the next section to deduce the form of the third term in Eq. (4).

Consider a particle, which suffers displacements along a line in the form of discrete steps of equal length. The particle moves one step forward with probability , while the probability of a backward step is . Equal probabilities of backward and forward displacements do not favor any direction of the motion. This is consistent with the symmetry of the system, described in Sec. II, where a man sits in a boat without doing anything.

The problem is to find the probability , that the particle has moved to a point after a series of steps, . Without loss of generality, we assume that the initial position of the particle is at zero , so that the total displacement equals the final position of the particle. The exact solution is given by the binomial distribution (Chandrasekhar, 1943, Chapter I):

| (5) |

As can be shown (Chandrasekhar, 1943, Chapter I), the binomial distribution Eq. (5) with approaches asymptotically a Gaussian 666 The Gaussian approximation is accurate only around the mean value of , cf. Keller (2004). Nonetheless, the original theory of Langevin equation is not concerned with corrections for the large deviations from the mean, which have vanishingly small probabilities. :

| (6) |

To obtain the continuous limit of Eq. (6), one introduces a density of sites accessible to the particle per unit length and the rate of displacements suffered per unit time , where and are now, respectively, the continuous increments of coordinate and time. Then, using Eq. (6) for and fixed in the limit and , one finds from Eq. (6) the probability density of particle’s displacement within a time interval (Chandrasekhar, 1943, Chapter I):

| (7) |

where .

The coordinate is thus a Gaussian random variable. Therefore the continuous limit, used to obtain Eq. (7), can be interpreted in terms of the Wiener process, cf. (Chandrasekhar, 1943, Chapter II Lemma I), which allows us then to pose that:

| (8) |

Instead of random displacements in the coordinate space, one can consider “displacements” in a velocity space, as in the problem of Brownian motion. This way one obtains the white noise in the Langevin equation Eq. (1).

The equal length of each step in this simple random walk problem turns out to be insignificant, as shown in Ref. (Chandrasekhar, 1943, Chapter I). In particular, random flight models, where the size of each step is sampled from a variety of probability distributions, lead again to a Gaussian distribution of the particle’s total displacement. The key aspect, therefore, is that the considered dynamics favors no particular direction of motion, since it assigns equal probabilities to the forward and backward displacements at each step.

IV Exponential noise

To motivate the third term of the Langevin dynamics Eq. (4), we need to exclude negative values of the external force it represents, as was suggested in Sec. II. This constraint can be implemented in the model of a simple random walk, reviewed in the preceding section, by a minor modification. Namely, the particle now will make only forward steps with the same probability or it will remain at rest with the probability . Then the particle’s position can take on values in the integer range .

As in Sec. III, the problem is again to find the probability that the particle moved from its initial position at zero to the position after steps. The exact solution is again a binomial distribution, which can be obtained by the same argument as Eq. (5) (Chandrasekhar, 1943, Chapter I):

| (9) |

As was done in Sec. III, the binomial probability mass 777 The probability mass function is the discrete analogue of the probability density function for continuous random variables. function Eq. (9) can be approximated by a Gaussian, which has a support . However, we emphasized earlier, that the zero probability of all negative values has a physical significance, because it acts as an external force always acting in the forward direction. For that reason we have to abandon the Gaussian approximation, which holds only for small deviations from the mean, cf. Keller (2004).

Instead of the Gaussian approximation, it would be tempting to resort to the Poisson distribution, which is traditionally used as a limiting case of the binomial distribution Eq. (9) for (Good, 1986; Durrett, 2010, Section 3.6), when a random variable of interest has its support on the half real line . In fact, this approximation leads to the shot noise term in Eq. (3), proposed by Refs. Kanazawa et al. (2015b); Morgado and Queirós (2016). However, in accordance with the ideas developed in Sec. II, the Poisson model is restricted to weak external forces, because it requires a vanishing probability of forward displacements, so that the particle mostly stays where it is. Fortunately, this rather restrictive assumption is irrelevant for the case of interest here, which actually is much better approximated by a different expression, as follows.

For the special case , which is of interest here, we will demonstrate that the binomial distribution Eq. (9) can be approximated by a Gamma distribution (Krishnamoorthy, 2015, Chapter 15) in the limit :

| (10) |

with an average value , a variance and the parameter , which is the mean rate of forward moves per step.

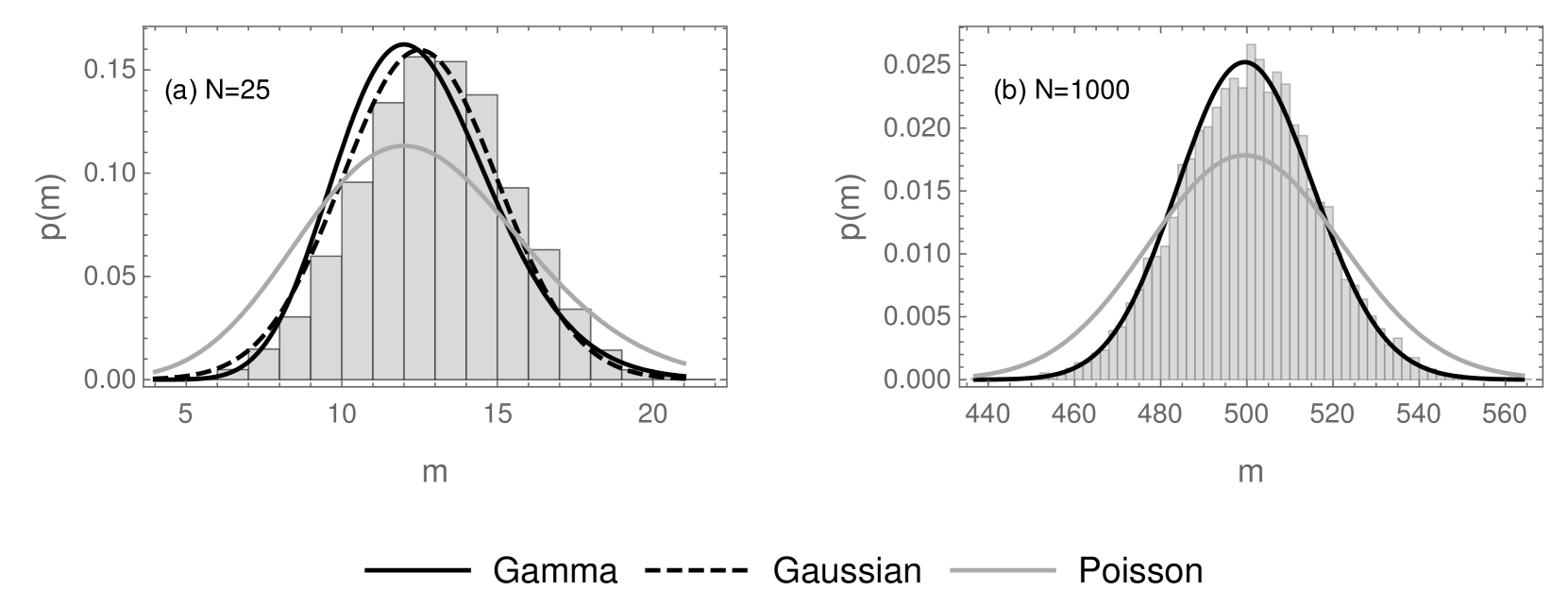

To the best of our knowledge, this work is the first to propose the Gamma approximation of the binomial distribution, which is motivated by the fact that the mean and the variance of in Eq. (9) (Krishnamoorthy, 2015, Chapter 3) coincide with those of (Krishnamoorthy, 2015, Chapter 15). While a formal mathematical argument is given in Appendix A, below we illustrate the efficiency of Eq. (10) by the numerical simulations in Fig. 1. The Gamma approximation becomes indistinguishable from a Gaussian for a sufficiently large , like in Fig. 1(b). An excellent agreement between the histograms and the Gamma probability distribution is evident for increasing in Fig. 1, while the Poisson distribution gives a poor representation of the simulation data, as expected for a non-vanishing probability of the forward step .

To specify the continuous counterparts of the discrete variables and in Eq. (10), we express the average displacement in terms of the displacement rate per unit time and the density of positions per unit length, introduced in Sec. III, so that

| (11) |

where and .

If we fix and for and as in Sec. III, the continuous limit of Eq. (10) then follows from the property of infinite divisibility of the Gamma distribution (Steutel and Van Harn, 2003, Chapter I). This means, in particular, that Eq. (10) can be represented as a sum of independent random variables distributed according to an exponential law of intensity (Krishnamoorthy, 2015, Chapter 15). This property and Eq. (11) both motivate the replacing the sum over in the continuous limit by a time integral of the exponential noise , which is then defined as the differential of the Gamma process , cf. Frenk and Nicolai (2007); Steutel and Van Harn (2003), so that obeys the probability law of a Gamma distribution:

| (12) | |||||

| (13) |

Here Eq. (12) and Eq. (13) define the properties of the exponential noise in the same manner as Eq. (7) and Eq. (8), respectively, determine the properties of the white noise.

We concluded Sec. III by pointing out, that the white noise also emerges in models of a random flight, where the length of the particle’s displacements is sampled at each step from a symmetric probability distribution. Similarly, the random walk considered in this section can be generalized to a random flight with steps of a variable length. If the length of each displacement is sampled from an exponential probability distribution, the Gamma distribution of the particle’s total displacement arises again as the sum of independent exponentially distributed random variables, a property already used above to deduce Eq. (12).

The analogy between the random walk problems of this and of the previous section is now complete. In Sec. III the Wiener process was obtained as the continuous limit of the symmetric random walk problem. By a similar argument, above we deduced the Gamma process from the continuous limit of an asymmetric random walk.

Finally, we conjecture that the generalization of the Langevin equation Eq. (1) to systems with a preferred spatial direction, induced by an external force, is given by Eq. (4). The new third term of that equation, i.e. , is proportional to the exponential noise, defined by Eqs. (12) and (13). If instead of the coordinate space we considered the velocity space of a Brownian particle, would have a physical meaning of the mean external force, as discussed in the next section.

V Solution of the extended Langevin equation

The extended Langevin equation (4), can be solved by a straightforward generalization of the method used in Ref. (Chandrasekhar, 1943, Chapter II) for Eq. (1). To do this, we first denote by the sum of the folowing two stochastic terms

| (14) |

so that Eq. (4) can be rewritten as

| (15) |

A formal solution of Eq. (15) was already given in Ref. (Chandrasekhar, 1943, Chapter II), which we repeat here in our notation:

| (16) |

where is an initial value condition.

Since in this paper we do not need a solution of Eq. (15) for a particular physical system, we will focus our attention on the Steady-State (SS) solution . This will suffice for our interest in the statistical nature of the fluctuations described by Eq. (4), as wa anticipated in Introduction. Taking the steady-state limit of Eq. (16) we have

The decomposition of in Eq. (14) splits the integral on the right hand side of Eq. (V) into a sum of two terms:

| (18) |

The first integral in Eq. (18) is given by Lemma I of Ref. (Chandrasekhar, 1943, Chapter II). The result of integration is a normally distributed random variable , with a zero mean and a variance

which in the steady-state limit becomes

For the second integral in Eq. (18) we need another result, which is analogous to the above cited Lemma I of Ref. (Chandrasekhar, 1943, Chapter II) but for the exponential noise, is established by Lemma 1 in Appendix B. There we show, that the second integral in Eq. (18) is a random variable, given by a Gamma-mixture distribution, and compute its mean, variance and skewness. From now on we will denote this random variable by .

In summary, we found that is a sum of two independent random variables, a Gaussian and a Gamma-mixture . Therefore the cumulant-generating function, cf. Sec. A, of is a sum of the Gaussian cumulant-generating function (Krishnamoorthy, 2015, Chapter 10) and the Gamma-mixture distribution, obtained in Appendix B. This allows us to calculate the mean, variance () and the skewness () of . Omitting straightforward computational details, we write immediately the final results for the steady-state solution

| (19) | |||||

| (20) | |||||

| (21) | |||||

| (22) |

where stands for the -th cumulant.

Since the skewness of the steady-state solution does not vanish for , cf. Eq. (21), the structure of the fluctuations is non-Gaussian. Moreover, the skewness has the same sign as , which is consistent with the experimental observations of Ref. Belousov et al. (2016). Higher order statistics, than those in Eqs. (19)-(21), can also be computed from the cumulant-generating function.

The physical meaning of the parameters , and depends on the problem, modeled by the extended Langevin dynamics. For instance, for a Brownian particle, is the friction constant, while the parameter can be computed from the kinetic temperature 888 The kinetic temperature is proportional to the variance of the particle’s linear momentum distribution, cf. Eq. (20). once and are known. Finally, as explained further, is the average magnitude of the external force. This can be seen, if we take the steady-state average of both sides in Eq. (15), which corresponds to the macroscopic dynamics:

| (23) |

where the left hand side must vanish in the steady state by definition. From Eqs. (14) and (23) one finds:

| (24) | |||||

since the average effect of the white noise, vanishes. Finally, , because

| (25) |

Combining Eqs. (23)-(25), we have

which relates the terminal value to the external force and the friction coefficient . For the complete description of the extended Langevin dynamics, the time scale parameter , which is a new characteristic of a system, needs to be found as well.

In other words, all constants , and are physical observables, which can be determined by measurements. In fact, these quantities are used to characterize physical systems in steady states, as was shown in the example of a Brownian motion above.

VI Conclusion

The Langevin dynamics of Eq. (1) was extended by a new term to obtain Eq. (4), which generalizes the theory of Brownian motion, as well as the Onsager-Machlup theory of fluctuations, from spatially symmetric equilibrium systems to equilibrium and nonequilibrium steady-state systems with a preferred spatial direction. We also provided statistical arguments in Sec. IV, which allowed us to deduce the form of the new term.

A method of solving the extended Langevin equation was demonstrated in Sec. V. In particular, we showed how the statistical properties of its steady-state solution can be computed from macroscopic physical observables. The steady-state probability distribution of the fluctuations is also characterized by the cumulant-generating function, which can be expressed using the dilogarithm, a special mathematical function, cf. Appendix B. The corresponding probability density function, which apparently can not be expressed in terms of elementary functions, can be in principle approximated by the Modulated Gaussian distribution Belousov et al. (2016) for practical applications.

The theory, presented in this paper, should be applicable to a variety of physical systems in classical statistical mechanics, such as an equilibrium fluid system in a gravitational potential or an electric current driven by a voltage difference. Applications of Eq. (4) to particular systems opens new perspectives for the future research in equilibrium and nonequilibrium statistical physics.

Finally, we would like to make a remark about the equilibrium systems in the magnetic field. The vector of a magnetic field has an axial nature, which means that it does not select a preferred direction, but rather determines a sense of rotation in its normal plane. As discussed in Sec. I, such systems have a symmetry of the Curie’s limiting point group , which does not admit a preferred spatial direction Shubnikov (1988). This is in contrast to the forces, described by polar vectors considered here, e.g. the electric field, which belongs to the symmetry group Shubnikov (1988). For this reason, systems subject to a magnetic field bear more similarity with the rotating systems, which still may need a further generalization of the Langevin equation.

Appendix A Gamma approximation of the binomial distribution

In this Appendix we provide a formal mathematical argument for the Gamma approximation Eq. (10) of the binomial distribution Eq. (9). For this we will compare a cumulant-generating function (Berberan-Santos, 2006; Abramowitz and Stegun, 1964, Section 26.1) of the Gamma distribution ( with that of the Binomial distribution ().

We recall that a probability distribution of a random variable is uniquely determined by its probability mass (or density) function or, equivalently, by its cumulant-generating function :

| (26) |

where is the dual of , while the angle brackets denote the average value. The Taylor coefficients in Eq. (26) are the cumulants of .

The first and second cumulants of a probability distribution are equal to its mean and its variance, respectively. The mean and the variance of the binomial distribution Eq. (9) are equal to those of the Gamma distribution Eq. (10), respectively, if , cf. (Krishnamoorthy, 2015, Chapter 3 and 15). It follows then, that their cumulant-generating functions agree up to the third order term in , i.e.

because the first two cumulants cancel each other in the series expansion Eq. (26) for and , respectively.

For the binomial distribution Eq. (9), there are no asymptotic formulae of an accuracy higher than with the support on the half real line 999 However, there may exist approximations of Eq. (9) with the same order of accuracy as Eq. (10). . The error of the third order is due to the skewness of the Gamma distribution. This property is inherent in all distributions, which have the support on the half real line, as a consequence of their obvious asymmetry. In other words, any asymptotic formula of Eq. (9) acquires skewness in the limit , if its support spreads over all non-negative reals , as considered in Sec. IV.

Appendix B Gamma-mixture probability distribution

When solving the extended Langevin equation in Sec. V, we had to evaluate a steady-state limit for a definite stochastic integral of the form:

| (27) |

where and is the exponential noise with the time scale parameter .

Below we will consider a more general function . We will obtain the cumulant-generating function of the random variable (Berberan-Santos, 2006; Abramowitz and Stegun, 1964, Section 26.1), cf. Sec. A, and compute some of its statistical moments, i.e. mean, variance, and skewness.

Lemma 1.

Let be a random variable given by

where is some integrable function and is the exponential noise with the time scale parameter . Then has a Gamma-mixture distribution, which is described by a cumulant-generating function

where is the dual of in the reciprocal Laplace space.

Proof.

Partitioning the domain of integration into subintervals of length , so that , we express as the limit of the following discrete sum :

| (28) |

where the index runs through all subintervals.

By virtue of Eqs. (12-13), each term of the summation in Eq. (28) is an independent Gamma-distributed random variable. In other words, the probability distribution of is a discrete mixture of Gamma-distributed random variables or, equivalently, a discrete Gamma-mixture distribution. The shape and scale parameters (Krishnamoorthy, 2015, Chapter 15) of each component are, respectively, and , while the cumulant-generating function of their sum is:

| (29) |

where is the dual of .

The cumulants , and hence the statistical moments of , can be obtained either by differentiation of the cumulant-generating function given by Lemma 1, cf. Eq. (26), or by using the calculus of cumulants. While the latter method was adopted in Sec. V to compute the skewness of the steady-state solution , cf. Eq. (21), in this section the former approach is more convenient.

Differentiating Eq. (30) with respect to we find:

| (31) |

from which the skewness can be computed using its definition in terms of cumulants .

Now, returning to Eq. (27), we need to use in Eqs. (30)-(B). Then the cumulant-generating function, given by Eq. (30), becomes 101010 We evaluated the integral in Eq. (30) for using a software for symbolic computations Wolfram Research, Inc. (2016). :

| (32) |

where stands for a dilogarithm function (Abramowitz and Stegun, 1964, Section 27.7). So that the steady-state limit of Eq. (32) yields

| (33) |

To evaluate Eq. (B) for the form of , chosen above, it is convenient to consider first a general integral of the following form

| (34) | |||||

for any integer .

References

- Onsager and Machlup (1953) L. Onsager and S. Machlup, Phys. Rev. 91, 1505 (1953).

- Machlup and Onsager (1953) S. Machlup and L. Onsager, Phys. Rev. 91, 1512 (1953).

- Coffey and Kalmykov (2012) W. T. Coffey and Y. P. Kalmykov, The Langevin equation: with applications to stochastic problems in physics, chemistry and electrical engineering, Vol. 27 (World Scientific, 2012).

- Kanazawa et al. (2015a) K. Kanazawa, T. G. Sano, T. Sagawa, and H. Hayakawa, Phys. Rev. Lett. 114, 090601 (2015a).

- Kanazawa et al. (2015b) K. Kanazawa, T. G. Sano, T. Sagawa, and H. Hayakawa, Journal of Statistical Physics 160, 1294 (2015b).

- Morgado and Queirós (2016) W. A. M. Morgado and S. M. D. Queirós, Phys. Rev. E 93, 012121 (2016).

- Note (1) The differential equation (1) is of the first order with respect to time. A second order version of the Langevin equation was considered in Ref. Machlup and Onsager (1953) for systems, in which the fluctuations of the currents should be taken into account. This modifies merely the deterministic character of the resulting dynamics, while the steady-state probability of the fluctuations, studied in this paper, remain unchanged, cf (Chandrasekhar, 1943, Section II.3).

- Gustavsson et al. (2006) S. Gustavsson, R. Leturcq, B. Simovič, R. Schleser, T. Ihn, P. Studerus, K. Ensslin, D. C. Driscoll, and A. C. Gossard, Phys. Rev. Lett. 96, 076605 (2006).

- Utsumi and Saito (2009) Y. Utsumi and K. Saito, Phys. Rev. B 79, 235311 (2009).

- Belousov et al. (2016) R. Belousov, E. G. D. Cohen, C.-S. Wong, J. A. Goree, and Y. Feng, Phys. Rev. E 93, 042125 (2016).

- Note (2) Skewness is related to the third moment of a probability distribution, so that symmetric distributions, like the Gaussian, have zero skewness.

- Shubnikov (1988) A. Shubnikov, Computers & Mathematics with Applications 16, 357 (1988).

- Curie, P. (1894) Curie, P., J. Phys. Theor. Appl. 3, 393 (1894).

- Note (3) “C’est la dissymétrie qui crée le phénomène” (It is the dissymetry, which creates the phenomenon) Curie, P. (1894).

- Note (4) To reverse the evolution of such systems, the sign of the external force should be changed together with that of the velocities and of the time Bertini et al. (2015).

- Bertini et al. (2015) L. Bertini, A. De Sole, D. Gabrielli, G. Jona-Lasinio, and C. Landim, Rev. Mod. Phys. 87, 593 (2015).

- Bonella et al. (2014) S. Bonella, G. Ciccotti, and L. Rondoni, EPL (Europhysics Letters) 108, 60004 (2014).

- Stratonovich (1967) R. L. Stratonovich, Topics in the theory of random noise, Vol. 1 (CRC Press, 1967).

- Blanter and Büttiker (2000) Y. Blanter and M. Büttiker, Physics Reports 336, 1 (2000).

- Note (5) The Gamma process is characterized by statistically independent increments, each having a Gamma probability distribution (Frenk and Nicolai, 2007; Dufresne et al., 1991; Steutel and Van Harn, 2003, Chapter I).

- Frenk and Nicolai (2007) J. Frenk and R. P. Nicolai, ERIM Report Series Reference No. ERS-2007-031-LIS (2007).

- Dufresne et al. (1991) F. Dufresne, H. U. Gerber, and E. S. W. Shiu, ASTIN Bulletin: The Journal of the International Actuarial Association 21, 177 (1991).

- Steutel and Van Harn (2003) F. W. Steutel and K. Van Harn, Infinite divisibility of probability distributions on the real line (CRC Press, 2003).

- Chandrasekhar (1943) S. Chandrasekhar, Rev. Mod. Phys. 15, 1 (1943).

- Ilienko (2013) A. Ilienko, Annales Univ. Sci. Budapest., Sect. Comp. 39, 137 (2013).

- Codling et al. (2008) E. A. Codling, M. J. Plank, and S. Benhamou, Journal of The Royal Society Interface 5, 813 (2008).

- Note (6) The Gaussian approximation is accurate only around the mean value of , cf. Keller (2004). Nonetheless, the original theory of Langevin equation is not concerned with corrections for the large deviations from the mean, which have vanishingly small probabilities.

- Note (7) The probability mass function is the discrete analogue of the probability density function for continuous random variables.

- Keller (2004) J. B. Keller, Proceedings of the National Academy of Sciences of the United States of America 101, 1120 (2004).

- Good (1986) I. J. Good, Statistical Science 1, 157 (1986).

- Durrett (2010) R. Durrett, Probability: theory and examples (Cambridge university press, 2010).

- Krishnamoorthy (2015) K. Krishnamoorthy, Handbook of statistical distributions with applications (CRC Press, 2015).

- Note (8) The kinetic temperature is proportional to the variance of the particle’s linear momentum distribution, cf. Eq. (20).

- Berberan-Santos (2006) M. N. Berberan-Santos, Journal of Mathematical Chemistry 41, 71 (2006).

- Abramowitz and Stegun (1964) M. Abramowitz and I. A. Stegun, Handbook of mathematical functions: with formulas, graphs, and mathematical tables, Vol. 55 (Courier Corporation, 1964).

- Note (9) However, there may exist approximations of Eq. (9) with the same order of accuracy as Eq. (10).

- Note (10) We evaluated the integral in Eq. (30) for using a software for symbolic computations Wolfram Research, Inc. (2016).

- Wolfram Research, Inc. (2016) Wolfram Research, Inc., “Mathematica,” (2016).