Abstract

We analyse the ruin probabilities for a renewal insurance risk process with inter-arrival time distributions depending on the claims that arrived within a fixed (past) time window. This dependence could be explained through a regenerative structure. The main inspiration of the model comes from the Bonus-Malus feature. We discuss first asymptotic results of ruin probabilities for different regimes of claim distributions. For numerical results, we recognise an embedded Markov additive process. Via an appropriate change of measure, ruin probabilities could be computed to a closed form formulae. Additionally, we present simulated results via the importance sampling method, which further permit an in-depth analysis of a few concrete cases.

keywords:

regenerative risk process ruin probability subexponential distribution Cramér asymptotics importance sampling Crude Monte Carlo Markov additive processx \doinum10.3390/—— \pubvolumexx \externaleditorAcademic Editor: name \historyReceived: date; Accepted: date; Published: date \TitleRuin probabilities with dependence on the number of claims within a fixed time window \AuthorCorina Constantinescu 1, Suhang Dai 1, Weihong Ni 1* and Zbigniew Palmowski 2 \AuthorNamesFirstname Lastname, Firstname Lastname and Firstname Lastname \corresW.Ni@liverpool.ac.uk; Tel.: +44 787 156 7797

1 Introduction

With the ever growing popularity of Bonus-Malus systems, one interesting question to study would be whether it really reduces the associated risk and with how much. A common measure to assess risks an insurer is exposed to is via the so-called ruin probabilities. Motivated by such kind of questions, we try to compute the probability of ruin for a simple Bonus system (also called no claim discount (NCD) system) in this paper. The main feature of such systems is that there is a premium discount when no claims are observed in the previous year. Inspired by this feature, we found a regenerative structure within inter claim times that could describe the dependence in a Bonus system equivalently.

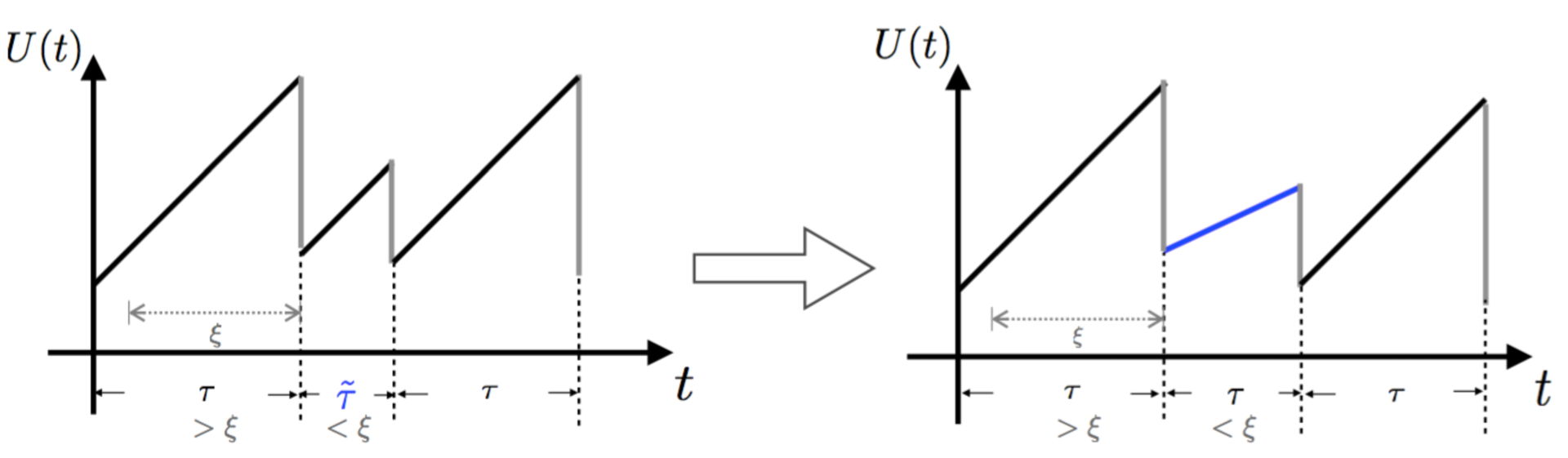

For the simplest case, there are only two classes - either a base or a discounted level in the NCD system under the consideration here. The discounted level implies a lower premium rate and occurs when no claim is witnessed in a past fixed time window . That is to say, the portfolio moves between these two classes. The switching condition relies on the history of arrived claims within the fixed time window . Theoretically speaking, it also works for a merely Malus system. Yet in practice, such systems do not exist as it probably sounds more tempting if an insurance company offers rewards rather than penalties. Therefore, the incorporation of such dependence in a risk model violates some of the classical assumptions, thus making it more difficult to calculate ruin probabilities. However, by equating the dependence between claim arrivals and premium rates with that between two consecutive inter arrival times (Figure 1), a regenerative structure can be identified so that further analysis could be carried out.

Looking into literature, one extension from a classical risk model is to relax the assumption of independence. Hence, dependence modelling has been introduced under a risk theory framework. There are several kinds of dependence to be considered. For a dependence within claims, Albrecher et al. albrecher2011explicit calculated ruin probabilities by using Archimedean survival copulas. Through a copulas method, Valdez and Mo valdez2002ruin also worked with risk models with dependence among claim occurrences focusing more on the simulation side. The dependence between claim sizes and inter-arrival times was also analysed. Albrecher and Boxma albrecher2004ruin first considered the case when the inter-claim time depends on the previous claim size with a random threshold. Due to the complexity of inverting Laplace Transform, they could only obtain the results in terms of Laplace Transforms. Kwan and Yang kwan2010dependent then studied such a dependence structure with a deterministic threshold and they were able to express ruin probability explicitly by solving a system of ordinary delay differential equations.

On the other hand, most of the work on Bonus-Malus systems mainly relied on a construction of a discrete Markov Chain in order to compute different levels of prices. See Lemaire . Due to the possibility of slow convergence to stationarity, asmussen2014 added an age-correction and implemented numerical analyses for various Bonus-Malus systems in different countries. Instead of considering premium levels depending only on claims in the previous period, it is alternatively suggested to take into account of the entire history where a Bayesian view could be adopted as in asmussen2014 . A recent work by Ni et al. ni2014 also applied the Bayesian approach to reflect this idea and obtained premiums in a closed form when claim severities are assumed to be Weibull distributed.

There have been a few papers investigating ruin probabilities for a Bonus-Malus system recently. Working with real data, Alfredo1 ; Alfredo2 calculated ruin probabilities under a realistic Bonus-Malus framework. The idea in their work is that they first analyse ruin probabilities for a single year conditioning on the reserve levels at the beginning and the end of the year. Since premium rate is kept constant within a year, a classical technique could be borrowed. Then they use approximations and estimate ruin probabilities numerically. On the other hand, the incorporation of the feature of a Bonus-Malus system into a risk model is similar to a variation in the premium rates after a claim arrival. For such a dependence, by employing a Bayesian estimator in a risk model and using a comparison method with the classical case, Dubey Dubey and Li et al. Li2015 could interpret ruin probabilities in terms of a classic one. In this paper, we follow a similar idea. However, our work here is to model the dependence between premium rates and the claim arrivals within a fixed time window. In our opinion it mimics better the key feature of a Bonus system. The consequence of this approach is that it implies modelling the dependence between two consecutive inter-claim times based on a fixed threshold, which is explained by Figure 1. This serves as the main goal of this work. Furthermore, the allowance of such dependence obviously violates the renewal property as in the classical model. Nevertheless, a regenerative structure can be identified so that anlayses are possible. For literature on regenerative processes, we refer to BP1 ; BP2 .

In Figure 1, Let us denote the inter claim time by . The graph on the right shows a two-level Bonus system where the premium rate decreases after a relatively long wait which exceeds a fixed number . In reality, this fixed window could be understood as a calendar year for instance, because many insurances companies charge different premiums based only on yearly claim histories. After that, since the second waiting interval is less than , the premium rate returns to its original value and so on and so forth. Equivalently, this could be transferred to a model where the adjustment on premium rates is reflected in inter arrival times switching between two different random variables, as long as the increment of the surplus process in this time interval is kept the same. That is to say, whenever a large inter arrival time which is above is witnessed, the next inter claim time will switch to a random variable with a different distribution. As we work with the ruin probabilities under an infinite-time horizon, such transformation would not affect the results. could be assumed to have a smaller mean than for a more ’realistic’ interpretation, resulting from the effect of the drop in the premium rate. Additionally, for computational reasons, we make the assumption that the inter-exchange of the randomness of inter arrival times only happens after a jump rather than precisely at the end of the fixed window.

Aiming at studying the ruin probability of a Bonus system, we try to investigate this model under a regenerative framework using various methods. We start by looking at some asymptotic results via adopting theories developed for general regenerative processes in BP1 ; BP2 . For the Cramér case, it still shows exponential tails for the probability of ruin. All asymptotic results are shown for a general situation where the distribution for each random variable is not specified. Then, by constructing an appropriate Markov Additive Process and using the Importance Sampling method we can run simulations to get numerical results for the case where inter claim times and claims are exponentially distributed. In the end, we employ the crude Monte Carlo simulations to compare the underlying ruin probability with a classic one as a case analysis. In addition, we look at the influence of claim distributions on the ruin probabilities, where we found that there is no significant differences in ruin probabilities when altering between Exponential and Pareto claims. In general, results suggest that the use of Bonus systems may not act in favour of the reduction on ruin probabilities. That is probably because premium discounts generally decrease the risk reserves. However, if the insurer is able to gain more market share by providing a Bonus system, although ruin probabilities could not be improved, their revenues and profits could possibly experience a positive effect.

2 The model

Let us start from describing the model that we will work in this paper with. We denote by the amount of surplus of an insurance portfolio at time :

| (1) |

In the above classical model (1), represents the constant rate of premiums inflow, is a arrival process that counts the number of claims incurred during the time interval and is a sequence of independent and identically distributed (i.i.d.) claim sizes with distribution function and density (also independent of the claim arrival process ). We assume that a.s. as . One of the crucial quantities to investigate in this context is the probability that the surplus in the portfolio will not be sufficient to cover the claims for the first time, which is called the probability of ruin

Here is the initial reserve in the portfolio and

is the time of ruin for an initial surplus . We specify the counting process which in the classical models is a Poisson process. Let be the sequence of inter-claim times. In this paper we analyse the model when the distribution of depends on the number of claims that appeared within a fixed past time window as follows,

It is true that when such dependence structure is introduced, a direct use of renewal theory is no longer applicable here. However, taking a second look, even though it is not renewal at each jump epoch, the process in fact renews after several jumps and we call this a ’regeneration’. Thus, we define the regenerative epochs for our model in the following way.

Definition 1.

Regeneration epochs are defined as

with .

Roughly speaking, at these epoch (being the arrival times with zero number of arrivals within the last time window lagged by )

the risk process loses his ’memory’ and starting at these epochs the stochastic evolution remains the same.

A formal definition of a regenerative process can be found in Appendix A1 in RP . It easy to observe that

the risk process is indeed regenerative with regeneration epochs . In this case, . Notice that we define the regenerative epochs in such a way that the concern only lies in whether there are claims or not in the past fixed window rather than how many of them.

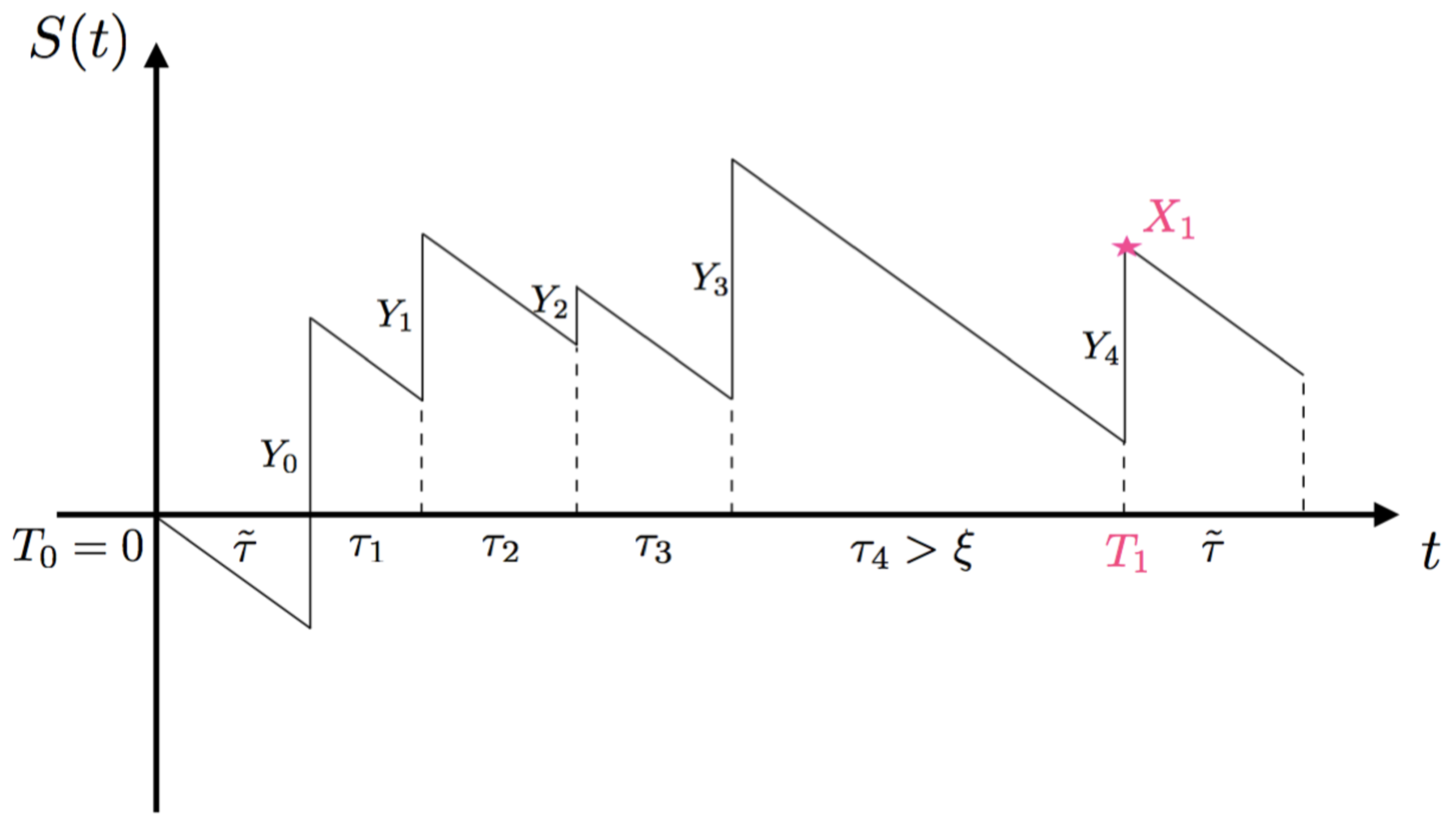

Moving into details, let us consider the claim surplus process denoted by

Moreover, let

and

| (2) |

Then due to the regenerative structure of the claim surplus process , the discrete-time process () is a random walk. The crucial observation used in this paper is:

| (3) |

The simplest case that we focus on is the one with inter claim times following two random variables and . The first one we choose when in a past time-window of length there is at least one claim. Otherwise we choose as the inter arrival time. Hence

It is a natural choice since usually in insurance company a long "silence" translates into a different behaviour of the arrival process just right after it. To rephrase it, our current model incorporates a dependence structure between each pair of consecutive inter-arrival times. Whenever an inter-arrival time exceeds , the next one would have the same distribution as . Otherwise, it conforms to .

More interestingly, as mentioned earlier, such model set-up would fit into a basic Bonus system, i.e., a system where policyholders enjoy discounts when they do not file claims for a certain period (but with no penalties). Without loss of generality, Figure 1 plots an example of such risk processes and demonstrate how our model reflects the feature of a Bonus system.

An example of sample path of the claim surplus process we will be working with is given in Figure 2 (where we assume starting from ).

Recall from (2) that is the end value at the first regenerative epoch. Then it is not difficult to observe that it has the same law as

| (4) |

where is a geometrical random variable with parameter . Here , and , .

The paper is organized as follows. Section 3 presents asymptotic results about ruin probabilities under three different regimes for claim distributions, using asymptotics derived for general regenerative processes as in BP1 ; BP2 . Section 4 demonstrates some numerical results via simulations and discusses a case analysis including comparison with ruin in a classical risk model. The simulations used in this section are based on the embedded Markov additive process within our model and rely on the importance sampling method via a change of measure. Our work will be concluded in Section 5.

3 Asymptotic results

In this section, we look at three different situations for claim distributions and analyse the asymptotic ruin probability associated with each of them. Inter arrival times considered in this section are general random variables if not mentioned specifically.

3.1 The heavy-tailed case

Let us first discuss the heavy-tailed case. We start with the assumption that the distribution of generic belongs to the class of subexponential distribution functions, where a distribution function on if and only if , for all , and

| (5) |

(where is the convolution of with itself). Here denotes the tail distribution given by . More generally, a distribution function on is subexponential if and only if is subexponential, where and is the indicator function of a set . We further assume throughout that are strong subexponential distributions. According to Definition 3.22 in FKZ , a distribution function on belongs to the class , i.e., G is strong subexponential, if and only if , for all , and

| (6) |

where

is the mean of . It is again known that the property depends only on the tail of . Further, if then and also where

is the integrated, or second-tail, distribution function determined by . See FKZ for details.

Theorem 2.

If and then

| (7) |

as , with .

Note that

Assume now that and are light-tailed, that is there exists such that and and that

| (8) |

Then from Foss et al. FKZ we have that

| (9) |

and by (4) and Corollary 3.40 in FKZ we have that

| (10) | |||||

where is a generic claim size. Moreover,

with

Remark 1.

Reducing to the classical model

Removal of the dependence in our setting would reduce to the classical model. An independent case is referring to the situation when . Substituting this into (10) yields,

In addition, it simplifies to

According to (7),

If we assume , and the safety loading to be i.e., . Also, we know that . The above identity could be reduced to,

| (11) |

which coinsides with the approximated ruin probability for the classic risk model with subexponential claims as shown by Theorem 1.36 in embrechts1997 .

3.2 The intermediate case

We now consider the case where satisfies

| (12) |

for every fixed , as , and

| (13) |

This is equivalent to the condition that . The case is treated in Section 2.1 so we assume . Another assumption we make is that

| (14) |

which implies that Cramér condition is not satisfied. Finally, we specify the tail behavior of . The case where has a heavier tail than is already covered in the previous subsection. Motivated by this, we assume that

| (15) |

(we allow the limit to equal 0). Furthermore, we assume that there exists a bounded function such that

| (16) |

for all real values of .

Proof.

Proof can be found in BP1 . ∎

We discuss now when conditions (12)-(16) are satisfied. Assume that

that is satisfies assumptions (12), (13) and (14). Then by representation (4) we can easily check that also satisfies

| (17) |

and

| (18) |

We additionally assume that satisfies

(see (25) for the representation of ). Note that the assumption (15) is always satisfied in our case since similarly to (17) we have:

Finally, conditioning on , using representation (4) and property (12) gives:

for , where

3.3 The Cramér case

In this subsection, we review the extension of the classical Cramér case from random walks to perturbed random walks and regenerative processes.

Theorem 4.

Assume that there exists a solution to the equation

Assume furthermore that is non-lattice and that . Then

with for independent of and .

Proof.

See goldie . ∎

It is easy to see that is bounded from above by

| (19) |

In fact it is even bounded above by

| (20) |

Note that by (4) the Cramér adjustment coefficient solves

for

| (21) | |||||

where . The above calculations shows also that the m.g.f. of has the following representation:

| (22) |

We can now identify constant :

| (23) | |||||

under assumption that

Example 1.

A special example of exponentially distributed , and would lead to

| (25) | |||||

and

This gives that

Moreover, since

the NPC condition is equivalent to

| (26) |

Furthermore, as a connection with Section 4, it is worth mentioning here that the above identity should coincide with

| (27) |

where

| (28) | |||||

| (29) |

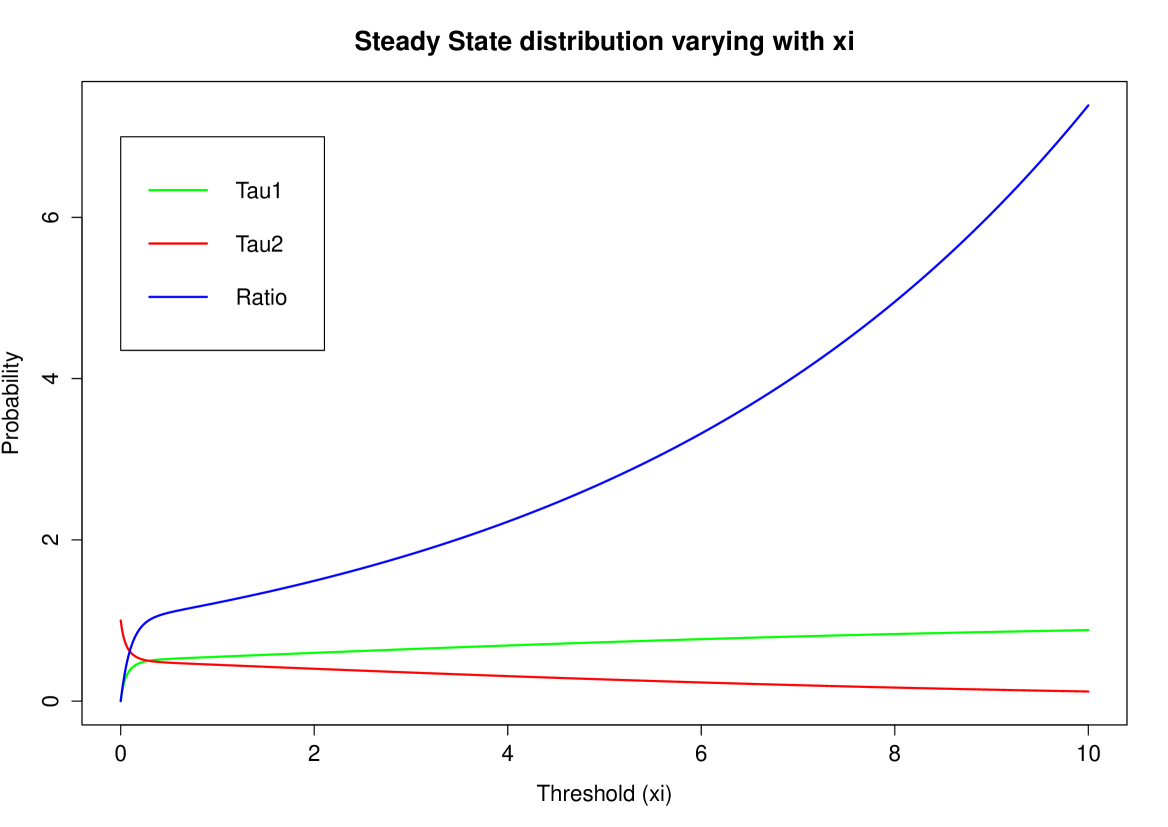

denote the steady state distribution in the Markovian environment of and , which is precisely defined in Section 4.2. That is to say, when the process becomes stationary, the probability to have an inter-arrival time less or equal to (State 1) would be while that for it being larger than (State 2) is represented by . The graph depicted in Figure 3 below shows an example of this distribution. It could be seen that the probability for State 1 in our case is monotonically increasing with . The blue line represents the ratio of probabilities between State 1 and State 2 thus having the same monotonicity as the green line. This will be analysed further via simulation.

4 Numerical Results

In this section, we explain several methods to simulate the ruin probabilities for our model. Initially, we tried the crude Monte Carlo simulation, but as in the classical case, several issues remain including determining a maximum time range so that it approximates an infinite time ruin probability. Then we employed the Importance Sampling technique, which allows us to simulate ruin probabilities under a new measure where ruin happens for sure. However, this does not give us the ruin probability as defined in our original problem. Hence, after a deeper analysis, the construction of a Markov additive further assists in developing a more sophisticated importance sampling technique for our model when the inter claim times as well as claims are exponentially distributed. Using this method, ruin probabilities could be simulated via a closed form formulae. At the end of this section, we present a case study using the crude Monte Carlo simulation where ruin probabilities for our model are compared with the ones under a classical setting, aiming at answering the question which originated this work. We also investigate the influence of two different claim distributions on simulated ruin probabilities.

4.1 Importance Sampling and Change of Measure

One cause of the drawback of using the crude Monte Carlo simulation is that ruin probabilities are inefficient, i.e., ruin probability tends to zero very quickly, when the initial reserve is large. This has been explained by the Cramér theorem that asymptotically ruin probability has an exponentially decay with respect to . The other reason of not simply adopting a crude Monte Carlo simulation is that we are anyway trying to simulate an infinite time ruin probability under a finite time horizon. In order to overcome this effect, the importance sampling technique has been brought in. The key idea behind is to find an equivalent probability measure under which the process has a probability of ruin equal to 1.

Let us start from something trivial. For the moment, we only consider the "ruin probability" when the time between regenerative epochs is ignored. In other words, we now look at our process from a macro perspective and it is renewal at each regenerative time epoch, so we omit the situations where ruin happens within these intervals. We refer to it as the "macro" process which coincides with a classical risk process and its corresponding ruin probability as the "macro" ruin probability in the sequel. We can then define the macro ruin time as

| (30) |

Consequently, the macro ruin probability denoted by should be smaller or equal than the ruin probability associated with our actual risk process . But for illustration purposes, it is worth covering the nature of change of measure under the framework of this macro process first before we dig into more complex scenarios.

Theorem 5.

Assume that there exists a such that . Consider a new measure such that:

with and defined in a similar way. Then we could establish the same relation as in the classical case for the m.g.f. of ,

| (31) |

Proof.

Rewriting the equation (25) we derive:

| (32) | |||||

First, we note that

| (33) |

Thus for ,

| (34) | |||||

| (35) |

Note that have the same form. Then the equation (32) could be modified into:

Now let,

Then,

∎

To analyse (31) further, can be considered as if the function shifted to the left by . We know that the net profit condition for the macro process requires , i.e., . Additionally, (22) should have a positive root if the tail of the claim cost distribution is exponentially bounded. That is to say, would result in a positive drift of the macro claim surplus process and then cause a macro ruin to happen for certain. The new m.g.f. makes this true. Hence we can write for a macro ruin probability as

with . For a strict and detailed proof please refer to RP (Chapter IV. Theorem 4.3). Moreover, from (31) it follows that

| (36) |

and is absolutely continuous with respect of (up to time ) with a likelihood ratio:

| (37) |

Define a new stopping time . Note that the event is equivalent to . From the Optional Stopping Theorem it follows that for any set we have

See (RP, , Chapter III. Theorem 1.3) for more details.

This means that we could simulate macro ruin probabilities under the new measure where the ruin happens with probability . We do it using new law of given in (36) and to each ruin even we add weight where is the observed macro ruin time. Summing all events with weights produces the ruin probability . In this way we can avoid infinite time simulations. For the case when everything is exponentially distributed as it was considered in Example 1 we have that under the simulation should be made according to new parameters:

In this case has the law of

| (38) |

where and .

4.2 Embedded Markov additive process

To get more precise simulation results avoiding the macro ruin probability giving lower estimate only, we have to understand the structure of our process better.

To implement this, we will use the theory of discrete-time Markov Additive Processes. For simplicity, we assume everything to be exponential distributed with , and , respectively.

Recall our process described by (2), note that ruin happens only at claim arrivals and . From time to , the distribution of the increment is only dependents on the relation between and . Hence, we could transfer the original model given in (3) into a new one () by adding a Markov state process defined on . The index represents the occupying state of at time . For instance, state describes a status where the current inter-arrival time is less or equal than while state refers to the opposite situation. For convenience, we construct based on the choice of : implies and otherwise. Note that the two state Markov chain has a transition probability matrix as follows with the element being .

where and . We also define a new process whose increment is governed by . More specifically, two scenarios could be analysed to explain this process. Given , scenario 1 is when , i.e., and . Then comparing with , there is a chance of obtaining given , and having given , with the corresponding increment being and , respectively. On the contrary, scenario 2 represents the situation where the current state is , i.e., and . Thus, all the variables above are presented in the same way only with a tilde sign added on , and .

is a discrete time bivariate Markov process also referred to as a discrete-time Markov additive process (MAP). The moment of ruin is the first passage time of over level , defined by

Without loss of generality, assume that . Then the event is equivalent to . This implies that

To perform simulation we will derive now the special representation of the underlying ruin probability using new change of measure. We start from identifying a kernel matrix with the entry given by . Here and denotes the probability measure conditional on the event and its corresponding expectation, respectively. Then for , a m.g.f of the measure is with

Additionally, based on the additive structure of the process for we have:

We will now present few facts that will be used in the main construction.

Lemma 6.

We have,

| (41) |

where is the eigenvalue of and is the corresponding right eigenvector.

Proof.

Note that

where is a standard basis vector. This completes the proof. ∎

Lemma 7.

The following sequence

| (42) |

is a discrete-time martingale.

Proof.

Let Then,

which gives the assertion of the lemma. ∎

Define now a new conditional probability measure using Randon-Nikodym derivative as follows:

Lemma 8.

Under the new measure process is again MAP specified by the Laplace transform of its kernel in the following way:

| (43) |

where is a diagonal matrix with on the diagonal.

Proof.

Note that the kernel of can be written as:

This shows that the new measure is exponentially proportional to the old one, which ensures that is absolutely continuous with respect to . Further transferring it into the matrix m.g.f. form yields the desired result. ∎

Corollary 9.

Under the new measure , the MAP consists of a Markov state process which has a transition probability matrix

| (46) |

where

and an additive component with random variables with laws given in Theorem 31 where should be chosen everywhere instead of .

In fact, when , coincides with defined by Theorem 31. Recall from (30) and . Since , then implies . Now the main representation used in simulations follows straightforward from above lemmas and Optional Stopping Theorem as it was already done in the previous section and it is given in the next theorem.

Theorem 10.

The ruin probability for the underlying process (2) equals:

| (47) |

where denotes the overshoot at the time of ruin .

Now we will simulate ruin events using new parameters of the model identified in Lemma 9. We start from state of . We will run our risk process until ruin event. With each ruin event we will associate its weight . Summing and averaging all weights gives the estimate of the ruin probability .

Remark 3.

In addition, it has been discovered that has an eigenvalue equal to 1 and

is the corresponding right eigenvector.

Proof.

Indeed, let denote the eigenvalue of . Thus we can write,

Recall (21), clearly is a solution to the above equation. That directly leads to and one can obtain

Plugging in the parameters completes the proof. ∎

Example 2.

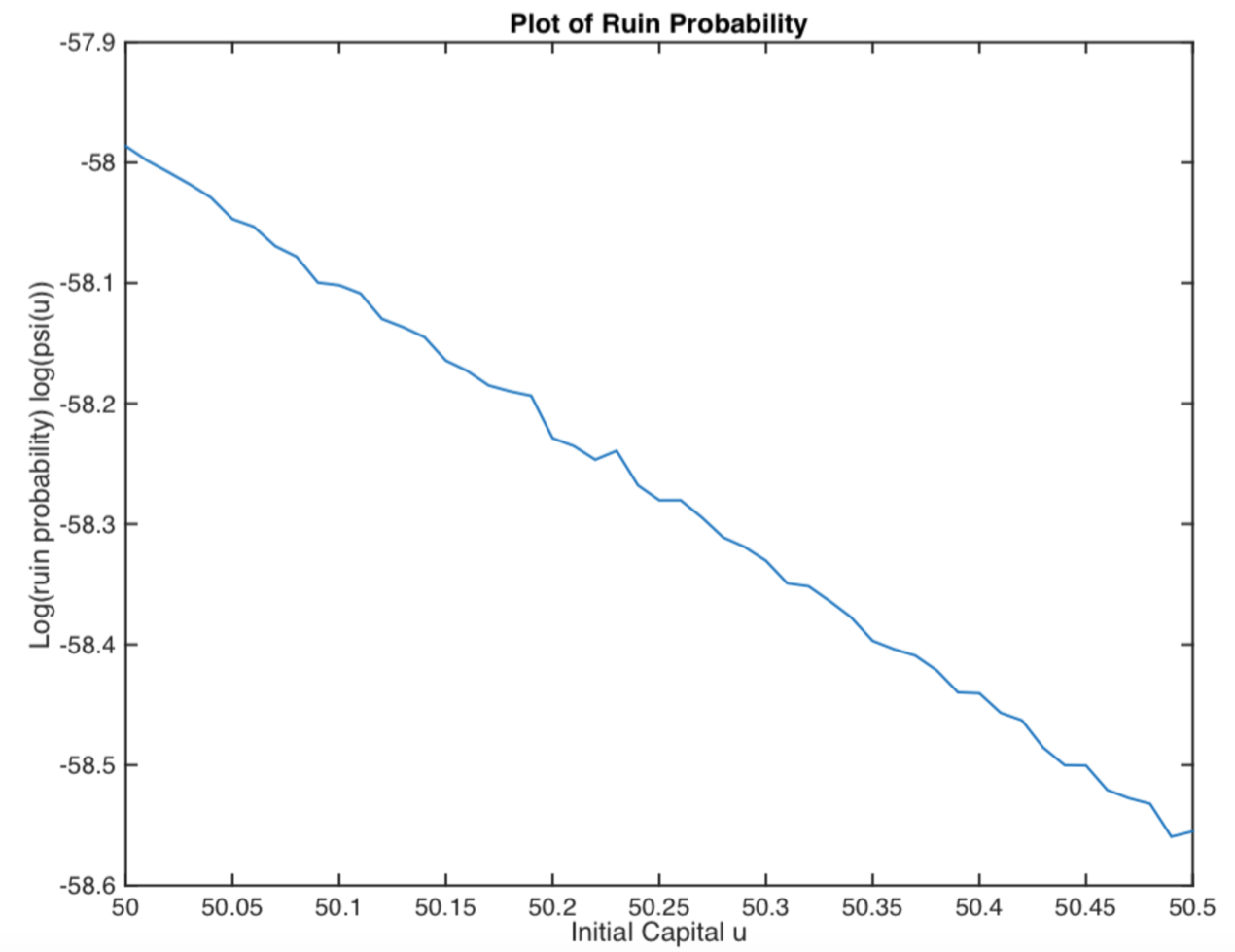

Assume that , and have exponential distribution with parameters , and , respectively. The smallest positive real root of Equation (21) is calculated for and its corresponding right eigenvector is . Then the ruin probability is plotted in Figure 8. It shows an exponential decay as we expected.

4.3 Case Study

In this subsection, we show some results via a crude Monte Carlo simulation method. The key idea is to simulate the process according to the model setting and simply counting the number of paths that gets to ruin. Due to the nature of this approach, a ’maximum’ time should be set beforehand, which means we are in fact simulating a finite time ruin probability. However, the drawback of it may be ignored for now as long as we are not getting a lot of zeros.

Our task is to compare the simulated results with a classical analytical ruin function when exponential claims are considered.

Just to prepare for later explanation, a system of integral equations for our model could actually be written,

| (49) | |||||

| (50) |

where correspond to the ruin probabilities with the first inter-arrival time being and respectively, and

with being the density function of the claim sizes.

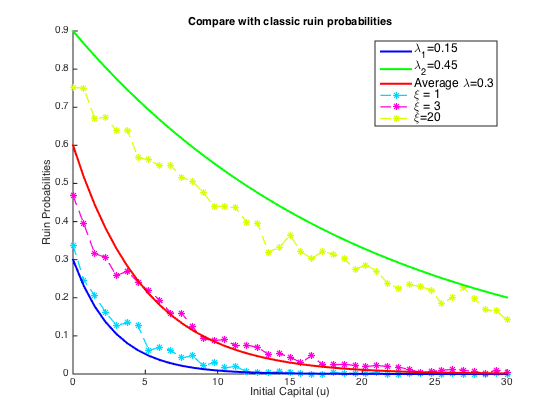

Hence, for the simplest case of exponentially distributed claim costs, we plotted both the classic ruin probabilities and our simulated ones on the same graph as shown below (see Figure 5).

It could be concluded that under two given parameters for Poisson intensity, simulated finite ruin probabilities in our model lie between two extreme but have many possibilities in-between. The comparison depends extensively on the value of . These results also confirmed Theorem 4 that the tail of the ruin function in our case still has an exponential decay and is strongly related to the solution for . In other words, when the dependence is introduced, it is not for sure that ruin probabilities would see an improvement.

Moving into details, solid lines show classical ruin probabilities (infinite-time) as a function of initial reserve , and each of them denotes an individual choice of Poisson parameters (, ) with the middle one being the average of the other two (). It is clear that the larger the Poisson parameter, the higher is the ruin probability. On the other hand, those dotted lines are simulated results from our risk model with dependence for the same given pair of Poisson parameters and . The four layers here correspond to four different choices of values for , i.e., . If , the simulated ruin probability (in fact finite-time) tends to a classical case with the lower claim arrival intensities ( here), which explains the blue dotted line lying around the dark blue solid line. On the contrary, if , simulated ruin probabilities approach the other end. This phenomenon is also theoretically supported by the integral equations (49) and (50) if either of these limits ( and ) is taken. This then triggered us to search for a such that the simulated ruin probability coincides with a classical one. Let us see an example here, if based on the parameters we chose in Figure 5. That implies the choice of our fixed window is the average length of the two kinds of inter-arrival times. However, as can be seen from Figure 5, the dotted line with lies closer than the one with to the red solid line. This suggests that the choice of will influence the simulated ruin probabilities and thus the comparison with a classical one. It is also very likely that there exists a such that our simulated ruin probabilities concur with the classic one.

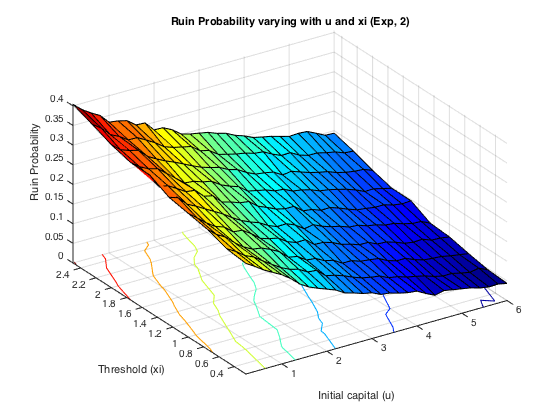

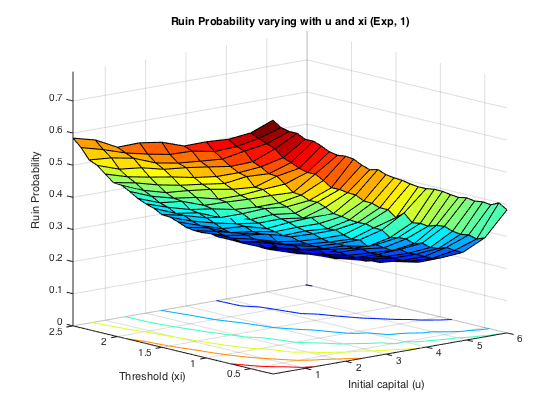

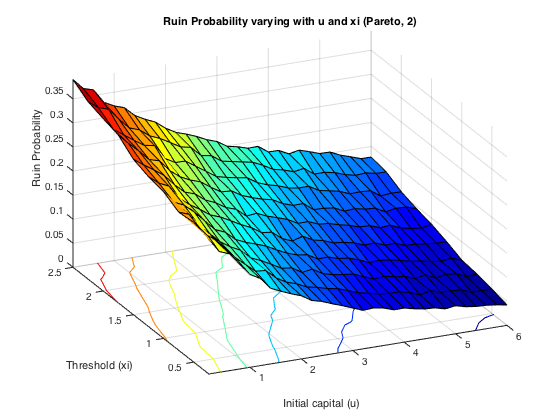

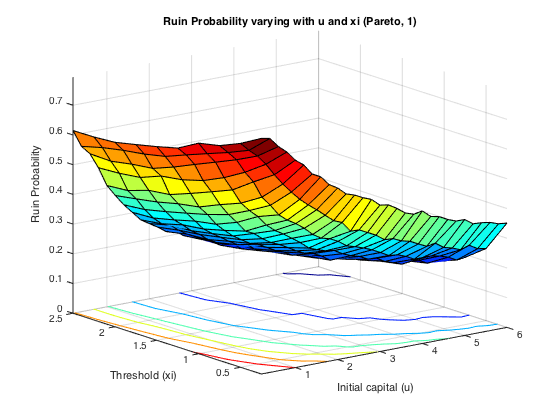

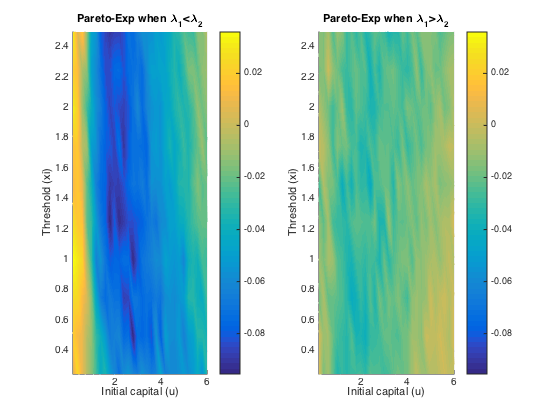

While the first half of the Monte Carlo simulation looked at the influence of on simulated ruin probabilities, the second step is to see the effects of claim sizes. Typical representation of light-tailed and heavy-tailed distributions - Exponential and Pareto - were assumed for claim severities and inter arrival times were switching between two different exponentially distributed random variables with parameters and . Two cases were simulated - either or . It is expected that the effects from claim severity distributions on infinite time ruin probabilities would be tiny as they normally affects more severely in the deficit at ruin. Here, since we simulate finite-time ruin probabilities, we are curious whether the same conclusion can be drawn.

Figure 6 displays the two cases for Exponential claims while Figure 7 does that for Pareto claims. All of these four graphs demonstrate a decreasing trend for simulated finite-time ruin probabilities over the amount of initial surplus, which is as expected. In general, the differences between ruin probabilities for Exponentially distributed claim costs and those for Pareto ones are not significant. To be more precise, the exact values of these disparities are plotted in Figure 8. The color bar shows the scale of the graph, and yellow represents values around 0. Indeed, the differences are very small. Furthermore, it can be seen that the disparities behave differently when and when . For the former case, ruin probabilities for Pareto claims tend to be smaller than those for Exponential claims when the initial reserve is not little, whereas there seems to be no distinction between the two claim distributions in the latter case. One way to explain this is that claim distributions would have more impact on the deficit at ruin because the claim frequency is not affected, the same as in an infinite-time ruin case. However, this is just a sample simulated result from which we cannot draw a general conclusion.

On the other hand, it could be seen from the projections on the plane that the magnitude of and causes different monotonicity of ruin probabilities with respect to the fixed window . If , the probability of ruin is monotonically increasing with the increase of . If , it appears to be the opposite monotonicity. This conclusion for monotonicity is true for both models with heavy-tailed claims and those with light-tailed ones. Such behaviour could also be theoretically verified if we look at the stationary distribution of the Markov Chain created by the exchange of inter claim times given by (28) and (29). The increase of will raise the probability of getting an inter-claim time smaller than at steady state, i.e.,

Then that directly leads to an increasing number of . The ruin probability is associated with

for any fixed time , where and denote the number of times and appearing in the process. Notice that stays the same even though the value of alters. So now the magnitude of depends only on and the distribution of i.i.d . The change of alters only the former value. Intuitively, a rise in indicates an increase in and a decrease in whose amount is denoted by and , respectively. Since the sum of s and s is kept constant, we have

If , then , which implies . That is to say, the increase of is more than the drop in so that sees a rise in the end. Thus, it leads to a higher ruin probability. On the contrary, when , i.e., , as goes up, ruin probabilities would experience a monotone decay. This reasoning is visually reflected in Figure 6-7 shown above and it could also be noticed that the distribution of claims does not affect such monotonicity.

Therefore, by observation, these results suggest that when , the larger choice of the fixed window , the smaller the ruin probability will be, and vice versa. On the contrary, when , the larger choice of the fixed window , the larger the ruin probability will be, and vice versa. In fact was mentioned in the introduction (Figure 1) to be an assumption for a Bonus system. Such observation suggests that if the insurer opts to investigate claims histories less frequently, i.e., choosing a larger , the ruin probability tends to be smaller. This potentially implies a smaller ruin probability if no premium discount is offered to policyholders. It seems that to minimise an insurer’s probability of ruin probably relies more on premium incomes. The use of Bonus systems may not help in decreasing such probabilities. The case of could be referred to as a Malus system which is unusual in the real world which leads to an opposite conclusion to the other case. This again addresses the significance of premium income to an insurer. In a system with purely maluses, the ruin probability could be reduced if the insurer reviews the policyholders’ behaviours more frequently indicating more premium incomes.

5 Conclusion

In this paper, we found that a simple Bonus system could be reflected by a dependence structure embedded in a risk model. For the simplest case, we made inter-arrival times switch between two random variables by comparing them with a fixed window . Such interchange was equivalently converted from the change of premium rates based on recent claims as shown by Figure 1 emulating a basic no claim discount (NCD) system where there are only two classes - either a base or discounted level. Theoretically speaking, it also works for a merely Malus system. Yet in practice, such system does not exist as it probably sounds more tempting if an insurance company offers rewards rather than a penalty.

Several different approaches have been undertaken to study the ruin probability under the framework of a regenerative process. It is not surprising under the Cramér assumption, the ruin function still has an exponential tail. Since asymptotic results are not exact, we conducted numerical analyses based on different approaches. As a main contribution, we explained how we could construct a discrete Markov additive process from the model under concern when everything is exponentially distributed. By a change of measure via exponential families, ruin probabilities were possible to be simulated through a better presented form (47). Furthermore, we attached a case study using Monte Carlo simulations. It has been discovered that the underlying probability has opposite monotonicity with respect to the fixed time window when two random variables for the inter claim times swap parameters. Additionally, it implies that the use of Bonus systems may not be helpful in reducing ruin probabilities as the premium incomes seem to be more important. However, Bonus systems could still be used as a means of attracting market share which is beneficial to the business in many ways.

Acknowledgements.

This work is under the support from the RARE-318984 project, a Marie Curie IRSES Fellowship within the 7th European Community Framework Programme. Z. Palmowski kindly acknowledges the support from the National Science Centre under the grant 2015/17/B/ST1/01102. \authorcontributionsZ.P. and S.D. conceived and designed the model; W.N. connected the work with the Bonus-Malus model; Z.P., W.N. and C.C. conducted analyses in details; S.D. introduced simulation methods; C.C. and W.N. interpreted the idea and wrote the paper. All authors substantially contributed to the work. \conflictofinterestsThe authors declare no conflict of interest. The founding sponsors had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript, and in the decision to publish the results.References

- (1) Afonso, L.B., Egídio dos Reis, A.D. and Waters, H.R., Calculating continuous time ruin probabilities for a large portfolio with varying premiums. ASTIN Bulletin, 2009, 39(01), 117–136.

- (2) Afonso, L.B., Rui, C., Egídio dos Reis, A.D., and Guerreiro, G., Bonus malus systems and finite and continuous time ruin probabilities in motor insurance. 2015, Preprint.

- (3) Albrecher, H. and Boxma, O.J., A ruin model with dependence between claim sizes and claim intervals. Insurance: Mathematics and Economics, 2004, 35(2), 245–254.

- (4) Albrecher, H., Constantinescu, C. and Loisel, S., Explicit ruin formulas for models with dependence among risks. Insurance: Mathematics and Economics, 2011, 48(2), 265–270.

- (5) Asmussen, S., Modeling and Performance of Bonus-Malus Systems: Stationarity versus Age-Correction. Risks, 2014, 2(1), 49–73.

- (6) Asmussen, S. and Albrecher, H., Ruin Probabilities, 2010, Vol. 14. World Scientific.

- (7) Blanchet, J. and Glynn, P., Efficient rare-event simulation for the maximum of heavy-tailed random walks, Ann. Appl. Probab. 2008, 18(4), 1351–1378.

- (8) Dubey, A., Probabilité de ruine lorsque le paramètre de Poisson est ajusté a posteriori, Mitteilungen der Vereinigung schweiz Versicherungsmathematiker, 1977, 2, 130–141.

- (9) Embrechts, P. and Kl uppelberg, C. and Mikosch, T., Modelling extremal events for insurance and finance, Berlin, 1997, Springer, c1997.

- (10) Foss, S., Korshunov, D. and Zachary S., An Introduction to Heavy-tailed and Subexponential Distributions, 2011, Springer.

- (11) Goldie, C.M., Implicit renewal theory and tails of solutions of random equations. The Annals of Applied Probability, 1991, 126–166.

- (12) Kwan, I.K. and Yang, H., Dependent insurance risk model: deterministic threshold. Communications in Statistics—Theory and Methods, 2010, 39(5), 765–776.

- (13) Lemaire, J., Bonus-malus systems in automobile insurance. 2012, Springer science & business media.

- (14) Li, B. and Ni, W. and Constantinescu, C., Risk models with premiums adjusted to claims number. Insurance: Mathematics and Economics, 2015, 65(2015), 94–102.

- (15) Ni, W., Constantinescu, C. and Pantelous, A.A., Bonus–Malus systems with Weibull distributed claim severities. Annals of Actuarial Science, 2014, 8(02), 217–233.

- (16) Palmowski, Z. and Zwart, B., Tail asymptotics for the supremum of a regenerative process, J. Appl. Probab. 2007, 44(2), 349–365.

- (17) Palmowski, Z. and Zwart, B., On perturbed random walks, J. Appl. Probab. 2010, 47(4), 1203–1204.

- (18) Rolski, T., Schmidli, H., Schmidt, V. and Teugles, J.L., Stochastic processes for insurance and finance. John Wiley and Sons, Inc., New York, 1999.

- (19) Valdez, E.A. and Mo, K., Ruin probabilities with dependent claims. Working paper, UNSW, Sydney, Australia, 2002.