Mode jumping MCMC for Bayesian variable selection in GLMM

Abstract

Generalized linear mixed models (GLMM) are used for inference and prediction in a wide range of different applications providing a powerful scientific tool. An increasing number of sources of data are becoming available, introducing a variety of candidate explanatory variables for these models. Selection of an optimal combination of variables is thus becoming crucial. In a Bayesian setting, the posterior distribution of the models, based on the observed data, can be viewed as a relevant measure for the model evidence. The number of possible models increases exponentially in the number of candidate variables. Moreover, the space of models has numerous local extrema in terms of posterior model probabilities. To resolve these issues a novel MCMC algorithm for the search through the model space via efficient mode jumping for GLMMs is introduced. The algorithm is based on that marginal likelihoods can be efficiently calculated within each model. It is recommended that either exact expressions or precise approximations of marginal likelihoods are applied. The suggested algorithm is applied to simulated data, the famous U.S. crime data, protein activity data and epigenetic data and is compared to several existing approaches.

keywords:

Bayesian variable selection; Bayesian model averaging; Generalized linear mixed models; Auxiliary variables MCMC; Combinatorial optimization; High performance computations.draft \pdfcommentsetupcolor=1.0 1.0 0.0, open=true

1 Introduction

In this paper we study variable selection in generalized linear mixed models (GLMM) addressed in a Bayesian setting. Being one of the most powerful modeling tools in modern statistical science (Stroup, 2013) these models have proven to be efficient in numerous applications including simple banking scoring problems (Grossi and Bellini, 2006), insurance claims modeling (David, 2015), studies on the course of illness in schizophrenia, linking diet with heart diseases (Skrondal and Rabe-Hesketh, 2003), analyzing sophisticated astrophysical data (de Souza et al., 2015), and inferring on genomics data (Lobréaux and Melodelima, 2015). In many of these applications, the number of candidate explanatory variables (covariates) is large, making variable selection a difficult problem, both conceptually and numerically. In this paper we will focus on efficient Markov chain Monte Carlo (MCMC) algorithms for such variable selection problems. Our focus will be on posterior model probabilities although other model selection criteria can also easily be adopted within the algorithm.

Algorithms for variable selection in the Bayesian settings have been previously addressed, but primarily in the combined space of models and parameters. George and McCulloch (1997) describe and compare various hierarchical mixture prior formulations for Bayesian variable selection in normal linear regression models. They outline computational methods including Gray Code sequencing and standard MCMC for posterior evaluation and exploration of the space of models. They also comment on the infeasibility of exhaustive exploration of the space of models for moderately large problems as well as the inability of standard MCMC techniques to escape from local optima efficiently. Al-Awadhi et al. (2004) consider using several MCMC steps within a new model to obtain good proposals within the combined parameter and model domain while Yeh et al. (2012) propose local annealing approaches. Ghosh (2015) also addresses MCMC algorithms to estimate the posterior distribution over models. She observes that estimates of posterior probabilities of individual models based on MCMC output are often not reliable because the number of MCMC samples is typically considerably smaller than the size of the model space. As a consequence she considers the median probability model of Barbieri et al. (2004) instead and shows that this algorithm can, under some conditions, outperform standard MCMC. Yet another approach for Bayesian model selection is addressed by Bottolo et al. (2011), who propose the moves of MCMC between local optima through a permutation based genetic algorithm that has a pool of solutions in a current generation suggested by parallel tempered chains. A similar idea is considered by Frommlet et al. (2012). Multiple try MCMC methods with local optimization have been described by Liu et al. (2000). Song and Liang (2015) address the case when there is by far more explanatory variables than observations. They suggest a split and merge Bayesian model selection algorithm that first splits the set of covariates into a number of subsets, then finds relevant variables from these subsets and in the second stage merges these relevant variables and performs a new selection from the merged set. This algorithm in general cannot guarantee convergence to a global optimum or find the true posterior distribution of the models, however under some strict regularity conditions it does so asymptotically.

For an increasing number of model classes, marginal likelihoods for specific models can be efficiently calculated, either exactly or approximately. This makes the exploration of models much easier. Bové and Held (2011) consider an MCMC algorithm within the model space, but only allow local moves. This might be a severe limitation in cases where multiple sparsely located modes are present in the model space. Bivand et al. (2014) combine approximations of marginal likelihood with Bayesian model averaging within spatial models. Clyde et al. (2011) suggest a Bayesian adaptive sampling (BAS) algorithm as an alternative to MCMC allowing for perfect sampling without replacement.

In the general MCMC literature, various algorithms for exploration of model spaces with multiple sparse modes have been suggested. These approaches can be divided into two groups: methods based on exploration of the tempered target distributions (allowing to flatten or increase multimodality for different temperatures) and methods based on utilization of local gradients. The first group of algorithms was initialized with the parallel tempering approach (Geyer, 1991), which further had numerous modifications (Liang, 2010; Miasojedow et al., 2013; Salakhutdinov, 2009). One of the most prominent extensions is the equi-energy sampling approach (Kou et al., 2006), which utilizes the physical duality between temperature and energy. This approach targets directly the former to flatten or tighten the parameter spaces. Another extension is the multi domain sampling approach (Zhou, 2011), which first uses the target distribution tempering idea to find the set of local modes and then uses local MCMC to explore the regions around them for further global inference. The second group of algorithms uses auxiliary variables combined with gradients of the extended distribution to explore the state space accurately (Neal et al., 2011; Chen et al., 2014; Sengupta et al., 2016, and many others). Both groups of algorithms are mainly developed for exploration of continuous parameter spaces. All of these algorithms can in principle be adapted to discrete space problems. The approach in this article will be to adapt the mode jumping MCMC idea of Tjelmeland and Hegstad (1999) to the variable selection problem, utilizing the existence of marginal likelihoods for models of interest.

Different approaches can be applied for calculation of marginal likelihoods. For linear models with conjugate priors, analytic expressions are available (Clyde et al., 2011). In more general settings, MCMC algorithms combined with e.g. Chib’s method (Chib, 1995) can be applied, giving however computationally expensive procedures. See also Friel and Wyse (2012) for alternative MCMC based methods. For Gaussian latent variables, the computational task can be efficiently solved through the integrated nested Laplace approximation (INLA) approach (Rue et al., 2009). Hubin and Storvik (2016) compare INLA with MCMC based methods, showing that INLA based approximations are extremely accurate and require much less computational effort than the MCMC approaches for within-model calculations.

In this paper we introduce a novel MCMC algorithm for search through the model space, the mode jumping MCMC (MJMCMC). The focus will be on Gaussian latent variable models, for which efficient approximations to marginal likelihoods are available. The algorithm is based on the idea of mode jumping within MCMC - resulting in an MCMC algorithm which manages to efficiently explore the model space by means of mode jumping, applicable through large jumps combined with local optimization. Mode jumping MCMC methods within a continuous space setting were first suggested by Tjelmeland and Hegstad (1999). We modify the algorithm to the discrete space of possible models, requiring both new ways of making large jumps and of performing local optimization. We include mixtures of proposal distributions and parallelization to further improve the performance of the algorithm. A valid acceptance probability within the Metropolis-Hastings setting is constructed based on the use of backward kernels.

2 The generalized linear mixed model

We consider the following generalized linear mixed model:

| (1) | ||||

| (2) | ||||

| and | ||||

| (3) | ||||

Here is the response variable while are the covariates. We assume is a density/distribution from the exponential family with corresponding link function . The latent indicators define if covariate is to be included into the model () or not () while are the corresponding regression coefficients. We are also addressing the unexplained variability of the responses and the correlation structure between them through random effects with a specified parametric covariance matrix structure defined through , where are parameters describing the correlation structure.

In order to put the model into a Bayesian framework, we assume

| (4) | ||||

| and | ||||

| (5) | ||||

where is the prior probability of including a covariate into the model. For different priors are possible, see the applications in section 4.

Let , which uniquely defines a specific model. Assuming the constant term is always included, there are different models to consider. We want to find a set of the best models with respect to posterior model probabilities , where . We assume that marginal likelihoods are available for a given , and then use MCMC to explore . By Bayes formula

| (6) |

In order to calculate we have to iterate through the whole model space , which becomes computationally infeasible for large . The ordinary MCMC based estimate is based on a number of MCMC samples :

| (7) |

where is the indicator function. An alternative, named the renormalized model (RM) estimates by Clyde et al. (2011), is

| (8) |

where now is the set of visited models during the MCMC run. Although both (8) and (7) are asymptotically consistent, (8) will often be the preferable estimator since convergences of the MCMC based approximation (7) is much slower, see Clyde et al. (2011).

We aim at approximating by means of searching for some subspace of making the approximation (8) as precise as possible. Models with high values of are important to be addressed. This means that modes and near modal values of marginal likelihoods are particularly important for construction of reasonable and missing them can dramatically influence our estimates. Note that these are aspects just as important if̃ the standard MCMC estimate (7) is to be used. A main difference is that while for using (7) the number of times a specific model is visited is important, for (8) it is enough that a model is visited at least once. In this context the denominator of (8), which we would like to be as high as possible, becomes an extremely relevant measure for the quality of the search in terms of being able to capture whether the algorithm visits all of the modes, whilst the size of should be low in order to save computational time.

The posterior marginal inclusion probability can be approximated by

| (9) |

giving a measure for assessing importance of the covariates. Other parameters can be estimated similarly.

Algorithms for estimating are described in section 3. In practice may not be available analytically. We then rely on some precise approximations . Such approximations introduce additional errors in (8) and (9), but we assume them to be small enough to be ignored. This is further discussed in section 3.4.

3 Mode jumping Markov chain Monte Carlo

MCMC algorithms (Robert and Casella, 2005) have been extremely popular for the exploration of model spaces for model selection, being capable of providing samples from the posterior distribution of the models. In our setting, the most important aspect becomes building a method to explore the model space in a way to efficiently switch between potentially sparsely located modes, whilst avoiding visiting models with a low too often.

3.1 Standard Metropolis-Hastings

Metropolis-Hastings algorithms (Robert and Casella, 2005) are a class of MCMC methods for drawing from a complicated target distribution living on some space , which in our setting will be . Given some proposal distribution , the Metropolis-Hastings algorithm accepts the proposed with probability

| (10) |

and otherwise remains in the old state . This will generate a Markov chain which, given the chain is irreducible and aperiodic, will have as stationary distribution. Theoretical results related to convergence of MCMC based estimates can be found in e.g. Tierney (1996). Note that the discrete finite space of models make these results easily applicable in our case.

Given that the ’s are binary, changes correspond to swaps between the values 0 and 1. One can address various options for generating proposals. A simple proposal is to first select the number of components to change, e.g. , followed by a sample of size without replacement from . This implies that in (10) the proposal probability for switching from to becomes symmetric, simplifying calculation of the acceptance probability. Other possibilities for proposals are summarized in Table 1, allowing, among others, different probabilities of swapping for the different components. Such probabilities can for instance be associated with marginal inclusion probabilities from a preliminary MCMC run.

Type

Proposal

Label

1

Random change with random size of the neighborhood

2

Random change with fixed size of the neighborhood

3

Swap with random size of the neighborhood

4

Swap with fixed size of the neighborhood

5

Uniform addition of a covariate

6

Uniform deletion of a covariate

3.2 MJMCMC - the mode jumping MCMC

The main problem with the standard Metropolis-Hastings algorithms is the trade-off between possibilities of large jumps (by which we understand proposals with a large neighborhood) and high acceptance probabilities. Large jumps will typically result in proposals with low probabilities. In a continuous setting, Tjelmeland and Hegstad (1999) solved this by introducing local optimization after large jumps, which results in proposals with higher acceptance probabilities. We adapt this approach to the discrete model selection setting by the following algorithm:

| (11) |

Here a large jump corresponds to changing a large number of ’s while the local optimization will be some iterative procedure based on, at each iteration, changing a small number of components until a local mode is reached.

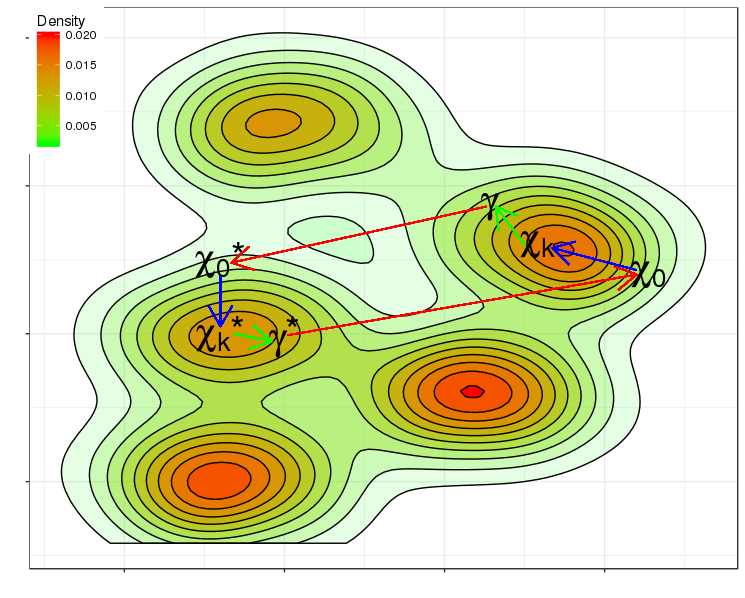

The procedure is illustrated in Figure 1 where the backward sequence , needed for calculating the acceptance probability, is included. For this algorithm, three proposals need to be specified; specifying the first large jump, specifying the local optimizer, and specifying the last randomization, all to be described in more details below.

-invariance of the MJMCMC procedures is given by the following theorem (based on similar arguments as in Storvik, 2011; Chopin et al., 2013):

Theorem 1.

Assume and is generated according to Algorithm 1. Then .

Proof.

Since and we have that

We may now consider as a proposal in the extended space, generated according to the distribution . An ordinary Metropolis-Hastings iteration with respect to is then to accept with probability where

proving the algorithm has as invariant distribution. Since this distribution has as marginal distribution it follows that . ∎

Note that neither the large jump distribution nor the optimization distribution (which can be both deterministic and stochastic) are involved in the acceptance probability. This gives great flexibility in the choice of these distributions.

Large jumps are not performed at each iteration, but rather through a composition of standard Metropolis-Hastings steps with local moves and large jumps. As a rule of thumb, based on suggestions of Tjelmeland and Hegstad (1999) and our own experience, we recommend that in not more than of the iterations large jumps are performed. This is believed to provide a global Markov chain with both good mixing between the modes and accurate exploration of the regions around the modes. This in turn induces good performance of the algorithm in terms of the captured posterior mass for a given number of iterations. However, some tuning might well be required for the particular practical applications.

The mode jumping MCMC steps can be modified to include a mixture of different proposal kernels , and and parallelized using the multiple try MCMC idea. Technical details are given in A.

An illustrative example

Assume 10 covariates and thus 1024 possible models. We generated with correlated binary covariates (see supplementary code for details) and 1000 observations. We used a Gaussian linear regression with a Zellner’s g-prior (Zellner, 1986) with . This model has tractable marginal likelihoods described in detail in section 4. We consider an MJMCMC step with a large jump swapping randomly 4 components of and a local greedy search, changing only one component at a time, as optimization routine. The last randomization changes each component of independently with probability equal to 0.1. A typical MJMCMC step with locally optimized proposals is illustrated in Table 2.

Forward

Backward

Model

Model

Initial mode

1010110111

1606.21

1101100001

1612.27

Large jump

1001110001

1541.51

1110100111

1608.55

Optimize

1101100000

1616.16

1010100110

1612.00

Randomize

1101100001

1612.27

1010110111

1606.21

Acceptance probability: , accept 1101100001

Large jumps

A change is defined by the components that are to be swapped. A simple choice is to give all components an equal probability to be swapped and independence between components, in which case

where is a binary variable equal to 1 if component is to be swapped and is the number of components to be swapped. An alternative is to first draw the number of components, , to swap according to a distribution and thereafter choose (uniformly) among the possible changes of size . Table 1 describes different ways of making large jumps where tuning parameters should be chosen such that the probability of a high value of is large.

Optimization

In order to increase the quality of proposals and consequently both improve the acceptance ratio and increase the probability of escaping from local optima, the large jump is followed by a local optimization step. Typically, contains many iterations, generating intermediate states but none of these intermediate states are needed for the final evaluation. Different local learning and optimization routines can be applied for the generation of , both deterministic and stochastic ones, see A.2 for further details. We will consider several feasible computationally options: local greedy optimization, local simulated annealing (SA) optimization, and local MCMC methods.

Randomization

A last randomization step defined through is needed in order to make the move back from to feasible. We typically use randomizing kernels with a high mass on a small neighborhood around the mode but with a positive probability for any change. The two possible appropriate kernels from Table 1 are the random change of either random or deterministic number of components with reasonably small but positive probabilities . This guarantees that the MJMCMC procedure is irreducible in .

Symmetric large jumps

In order for the acceptance probability to be high, it is crucial that the auxiliary variables in the reverse sequence make plausible ( should be large in (11)). This may be difficult to achieve because the backwards large jump has no guarantee to be close to the current state. One way to achieve this is to choose to be symmetric, increasing the probability of returning close to the initial mode in the reverse large jump. The symmetry is achieved by swapping the same set of ’s in the large jumps in the forward simulation as in the backwards simulation. We record the components that have been swapped. In our current implementation we require that only the components that do not correspond to can be changed in optimization transition kernels. The following algorithm is a modification of Algorithm 1 taking a symmetric large jump into account.

| (12) |

The following theorem shows that also this algorithm also is -invariant.

Theorem 2.

Assume and is generated according to Algorithm 2. Then .

Proof.

The stochastic auxiliary components are now and where and are deterministic functions of and , respectively. We have

We may now consider as a proposal in the extended space, generated according to the distribution . An ordinary Metropolis-Hastings iteration with respect to is then to accept with probability where

proving the algorithm has as invariant distribution. Since this distribution has as marginal distribution it follows that . ∎

3.3 Delayed acceptance

The most computationally demanding parts of the MJMCMC algorithms are the forward and backward optimizations. In many cases, the proposal generated through the forward optimization may lead to a very small value of resulting in a low acceptance probability regardless of the way the backwards auxiliary variables are generated. In such cases, one would like to reject directly without the need for performing the backward optimization. Such a scheme can be constructed by the use of the delayed acceptance procedure (Christen and Fox, 2005; Banterle et al., 2015). We then have:

Theorem 3.

Proof.

We have that

| where | ||||

Since for , it follows by the general results in Banterle et al. (2015) that we obtain an invariant kernel with respect to . ∎

In general the total acceptance rate will be smaller than without delayed acceptance (Banterle et al., 2015, remark 1), but the gain by avoiding a backwards optimization step if not accepted in the preliminary step can compensate on this.

3.4 Calculation of marginal densities

In practice exact calculation of the marginal density can only be performed in simple models such as linear Gaussian ones, so alternatives need to be considered. One approach is to use estimators that are accurate enough to neglect the approximation errors involved. Such approximative approaches have been used in various settings of Bayesian variable selection and Bayesian model averaging. Laplace’s method (Tierney and Kadane, 1986) has been widely used, but is based on rather strong assumptions. The harmonic mean estimator (Newton and Raftery, 1994) is an easy to implement MCMC based method but can give high variability in the estimates. Chib’s method (Chib, 1995), and its extension (Chib and Jeliazkov, 2001), have gained increasing popularity and can be very accurate provided enough MCMC iterations are performed. Approximate Bayesian Computation (Marin et al., 2012) has also been considered in this context, being much faster than MCMC alternatives, but also giving cruder approximations. Variational methods (Jordan et al., 1999) provide lower bounds for the marginal likelihoods and have been used for model selection in e.g. mixture models (McGrory and Titterington, 2007). Integrated nested Laplace approximation (INLA, Rue et al., 2009) provides accurate estimates of marginal likelihoods within the class of latent Gaussian models. In the context of generalized linear models, BIC type approximations can be used.

An alternative is to insert unbiased estimates of into the Metropolis-Hastings acceptance probabilities. Andrieu and Roberts (2009) name this the pseudo-marginal approach and show that this leads to exact algorithms (in the sense of converging to the right distribution). Importance sampling (Beaumont, 2003) and particle filter (Andrieu et al., 2010) are two approaches that can be used within this setting. In general, the convergence rate will depend on the amount of Monte Carlo effort that is applied. Doucet et al. (2015) provide some guidelines.

Our implementation of the MJMCMC algorithm allows for all of the available possibilities for calculation of marginal likelihoods and assumes that the approximation error can be neglected. For the experiments in section 4 we have applied exact evaluations in the case of linear Gaussian models, approximations based on the assumed informative priors in case of generalized linear models (Clyde et al., 2011), and INLA (Rue et al., 2009) in the case of latent Gaussian models. Bivand et al. (2015) also apply INLA within an MCMC setting, but then concentrating on hyperparameters that (currently) can not be estimated within the INLA framework. Friel and Wyse (2012) performed comparison of some of the mentioned approaches for calculation of marginal likelihoods, including Laplace’s approximations, harmonic mean approximations, Chib’s method and others. Hubin and Storvik (2016) reported some comparisons of INLA and other methods for approximating marginal likelihood. There it is demonstrated that INLA provides extremely accurate approximations on marginal likelihoods in a fraction of time compared to Monte Carlo based methods. Hubin and Storvik (2016) also demonstrated that by means of adjusting tuning parameters within the algorithm (the grid size and threshold values within the numerical integration procedure, Rue et al., 2009) one can often make the difference between INLA and unbiased methods of estimating of the marginal likelihood arbitrary small.

3.5 Parallelization and tuning parameters of the search

With large number of potential explanatory variables it is important to be able to utilize multiple cores and GPUs of either local machines or clusters in parallel. General principles of utilizing multiple cores in local optimization are provided in Eksioglu et al. (2002). At every step of the local optimization within the large jump steps we allow to simultaneously draw several proposals with respect to a certain transition kernel during the optimization procedure and then sequentially calculate the transition probabilities as the proposed models are evaluated by the corresponding CPUs, GPUs or clusters in the order they are returned. In those iterations where no large jumps are performed, we are utilizing multiple cores by means of addressing multiple try MCMC to explore the solutions around the current mode. The parallelization strategies are described in detail in A.

In practice, tuning parameters of the local optimization routines such as the choice of the neighborhood, generation of proposals within it, the cooling schedule for simulated annealing (Michiels et al., 2010) or number of steps in greedy optimization also become crucially important and it yet remains unclear whether we can optimally tune them before or during the search. Mixing of proposals from Table 1 and of optimizers is also possible. Tuning the probabilities of addressing these different options can be beneficial. Such tuning is a sophisticated mathematical problem, which we are not trying to resolve optimally within this paper, however we suggest a simple practical idea for obtaining reasonable solutions. Within the BAS algorithm, an important feature was to utilize the marginal inclusion probabilities of different covariates. We have introduced this in our algorithms as well by allowing insertion of estimates of the ’s in proposals given in Table 1 based on some burn-in period. They then correspond to the marginal inclusion probabilities after burn-in shifted with some small from 0 and 1 if necessary in order to guarantee irreducibility. Additional literature review on search parameter tuning can be found in Luo (2016).

4 Experiments

In this section we are going to apply the MJMCMC algorithm to different data sets and analyze the results in relation to other algorithms. Linear regression is addressed through the U.S. Crime Data (Raftery et al., 1997) and a protein activity data (Clyde et al., 1998). Logistic regression is considered in a simulated example based on a data set and through an Arabidopsis epigenetic data set. The Arabidopsis example also includes random effects.

We compare the performance of our approach to competing MCMC methods such as the MCMC model composition algorithm (, Madigan et al., 1995; Raftery et al., 1997) and the random-swap (RS) algorithm (Clyde et al., 2011) as well as the BAS algorithm (Clyde et al., 2011). Both and RS are simple MCMC procedures based on the standard Metropolis-Hastings algorithm with proposals chosen correspondingly as an inversion or a random change of one coordinate in at a time (Clyde et al., 2011). BAS carries out sampling without repetition from the space of models with respect to the adaptively updated marginal inclusion probabilities. For one of the examples, also a comparison with the ESS++ software (evolutionary stochastic search, Bottolo et al., 2011) is made. For the cases when full enumeration of the model space is possible we additionally compare all of the aforementioned approaches to the benchmark TOP method that consists of the best quantile of models in terms of the posterior probability for the corresponding number of addressed models and can not by any chance be outperformed in terms of the posterior mass captured.

The different algorithms that are compared are implemented in different programming languages, making it difficult to compare CPU time fairly. We have therefore focused on both the total number of visited models and the number of unique models visited, since this is the main computational burden (marginal likelihood values of visited models can be stored). The number of models visited for MJMCMC includes all of the models visited during global and local moves as well as local combinatorial optimization, hence the comparison on the same number of totally visited and uniquely visited models is fair.

Following Clyde et al. (2011), approximations for model probabilities (8) and marginal inclusion probabilities (9) based on a subspace of models are further referred to as RM (renormalized) approximations, whilst the corresponding MCMC based approximations (7) are referred to as MC approximations. The validation criteria addressed include root mean squared errors and bias of parameters of interest based on multiple replications of each algorithm, similar to Clyde et al. (2011). In addition to marginal inclusion probabilities, we also include a global measure

| (13) |

describing the fraction of probability mass contained in the subspace . This measure allows us to address how well the search works in terms of capturing posterior mass within a given model space. By formula (8) maximization of automatically induces minimization of the bias in terms of posterior marginal model probabilities, which vanishes gradually when .

Mixtures of different proposals from Table 1 and local optimizers mentioned in section 3.2 were used in the studied examples in the MJMCMC algorithm. A validation of the gain in using such mixtures is given in example 4.1, where we address both MJMCMC with mixtures and a simpler version where only one choice of proposal distributions is used (the details are given in the example). The details on the choices and frequencies of different proposals for the other examples are given in Tables 1-5 in B. The choices are based on some tuning on a simulated data example, reported in section C.1. Further small adaptations were made in some of the examples. Generally speaking, we can not claim that the choices of the tuning parameters are optimal. It is rather some subjectively rational choice.

4.1 Example 1

Here we address the U.S. Crime data set, first introduced by Vandaele (1978) and stated to be a test bed for evaluation of methods for model selection (Raftery et al., 1997). The data set consists of observations on 15 covariates and the responses, which are the corresponding crime rates. We will compare performance of the algorithms based on a linear Bayesian regression model using a Zellner’s g-prior (Zellner, 1986) with . This implies that the marginal likelihood is of the following form:

| (14) |

where is the usual coefficient of determination of a linear regression model. With this scaling, the marginal likelihood of the null model (the model containing no covariates) is 1.0.

This is a sophisticated example with a total of potential models and with several local modes. As a result, all simple MCMC methods easily get stuck and have extremely poor performances in terms of the captured mass and precision of both the marginal posterior inclusion probabilities and the posterior model probabilities. Table 3 shows the RMSE (scaled by ) for the model parameters over 100 repeated runs for each algorithm. The True column contains the true marginal inclusion probabilities (obtained from full enumeration) while the TOP column shows the RMSE results based on the 3276 models with highest posterior probabilities (about 10% of the total number of models). The MJMCMC columns show the results based on using mixtures of proposals and optimizers (see Tables 1 and 2 for details) while the MJMCMC∗ results are based on one specific choice of proposals with swaps of 4 components at a time for the large jumps (Type 4 in Table 1) and a local greedy optimizer changing two components at a time with a last randomization of type 2 (Table 1). For the standard MCMC steps, a type 4 with two changing components was used.

For this example, both the MC3 and the RS methods got stuck in some local modes and for the 3276 models only 829/1071 unique models where visited. These algorithms did not reach 3276 unique models within a reasonable time for this example (most likely the algorithm could not escape from local extrema), hence such a scenario is not reported. For this example MJMCMC gives a much better performance than the other MCMC methods in terms of both MC and RM based estimations with respect to the posterior mass captured, . With a total of 3276 visited, BAS slightly outperforms MJMCMC. However, when running MJMCMC so that the number of unique models visited () are comparable with BAS, MJMCMC gives better results (columns marked with MJMCMC2 in Table 3). The comparison is performed in terms of posterior mass captured, biases and root mean squared errors for both posterior model probabilities and marginal inclusion probabilities (Table 3).

BAS has the property of always visiting new unique models, whilst all MCMC based procedures tend to do revisiting with respect to the corresponding posterior probabilities. When generating a proposal is much cheaper than estimating marginal likelihoods of the model (which is usually the case, also in this example) and we are storing the results for the already visited models, having generated a bit more models by MJMCMC does not seem to be a serious issue. Those unique models that are visited have a higher posterior mass than those suggested by BAS (for the same number of models visited). Furthermore MJMCMC (like BAS) can escape from local modes.

Also the results based on no mixture of proposals (MJMCMC* in the table) are much better than standard MCMC methods, however the results obtained by the MJMCMC algorithm with a mixture of proposals were even better. We have tested this on some other examples too and the use of mixtures was always beneficial and thus recommended. For this reason only the cases with mixtures of proposals are addressed in other experiments.

| Par | True | TOP | MJMCMC | MJMCMC2 | BAS | RS | MJMCMC* | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| - | RM | MC | RM | MC | RM | MC | RM | MC | RM | RM | MC | |||||

| 0.16 | 3.51 | 6.57 | 10.68 | 5.11 | 10.29 | 5.21 | 6.49 | 3.49 | 5.87 | 3.31 | 6.23 | 9.06 | ||||

| 0.16 | 3.34 | 7.46 | 10.54 | 5.60 | 10.19 | 6.26 | 8.62 | 3.39 | 8.83 | 3.05 | 6.38 | 10.54 | ||||

| 0.19 | 3.24 | 8.30 | 12.43 | 6.30 | 12.33 | 6.20 | 6.58 | 2.55 | 6.22 | 2.46 | 7.15 | 10.91 | ||||

| 0.22 | 3.27 | 6.87 | 13.61 | 5.57 | 13.64 | 3.10 | 5.81 | 6.23 | 4.93 | 5.27 | 5.29 | 10.93 | ||||

| 0.23 | 2.56 | 6.30 | 13.45 | 4.59 | 13.65 | 1.84 | 6.07 | 13.05 | 5.13 | 12.77 | 5.39 | 10.90 | ||||

| 0.23 | 3.27 | 9.49 | 16.21 | 7.40 | 16.21 | 9.27 | 5.99 | 2.99 | 5.70 | 2.60 | 7.68 | 11.06 | ||||

| 0.29 | 2.31 | 4.37 | 13.63 | 3.45 | 12.73 | 2.28 | 4.74 | 9.61 | 3.46 | 9.70 | 3.91 | 10.10 | ||||

| 0.30 | 1.57 | 6.18 | 19.22 | 3.79 | 17.31 | 0.99 | 13.24 | 21.84 | 13.53 | 21.48 | 4.63 | 13.22 | ||||

| 0.33 | 1.92 | 8.61 | 19.71 | 6.14 | 19.49 | 3.11 | 10.19 | 7.47 | 10.99 | 7.12 | 5.87 | 15.43 | ||||

| 0.34 | 2.51 | 11.32 | 22.68 | 7.29 | 20.50 | 8.43 | 22.89 | 25.19 | 23.63 | 24.71 | 7.58 | 12.97 | ||||

| 0.39 | 0.43 | 3.95 | 11.13 | 2.38 | 6.99 | 5.02 | 21.48 | 30.24 | 21.39 | 29.94 | 2.99 | 12.66 | ||||

| 0.57 | 1.58 | 5.92 | 13.21 | 3.82 | 9.03 | 13.78 | 30.81 | 37.57 | 29.27 | 37.15 | 5.11 | 14.04 | ||||

| 0.59 | 0.58 | 3.57 | 13.49 | 2.37 | 15.94 | 4.04 | 11.88 | 21.79 | 11.16 | 21.31 | 2.77 | 12.77 | ||||

| 0.77 | 3.25 | 7.62 | 7.28 | 5.97 | 4.78 | 15.45 | 21.83 | 19.18 | 20.53 | 19.65 | 6.41 | 14.27 | ||||

| 0.82 | 3.48 | 9.23 | 4.45 | 6.89 | 5.85 | 14.50 | 69.68 | 76.81 | 69.19 | 76.30 | 6.75 | 14.76 | ||||

| 1.00 | 0.86 | 0.58 | 0.58 | 0.71 | 0.71 | 0.66 | 0.10 | 0.10 | 0.10 | 0.10 | 0.60 | 0.60 | ||||

| Eff | 3276 | 1909 | 1909 | 3237 | 3237 | 3276 | 829 | 829 | 1071 | 1071 | 3264 | 3264 | ||||

| Tot | 3276 | 3276 | 3276 | 5936 | 5936 | 3276 | 3276 | 3276 | 3276 | 3276 | 4295 | 4295 | ||||

4.2 Example 2

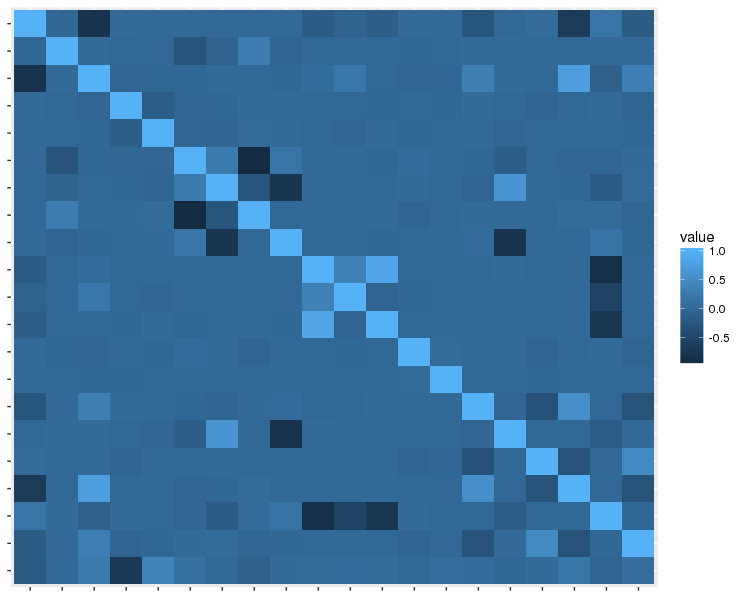

In this example we are considering a new simulated data set for logistic regression. We generated covariates as a mixture of binary and continuous variables. The correlation structure is shown in Figure 2 while the full details of how the data was generated is given in B.1.

A total of potential models need to be considered in this case. Additionally, in this example , which makes estimation of a single model significantly slower than in the previous example. For we use the binomial prior (4) with . We are in this case using the BIC-approximation for the marginal likelihood,

| (15) |

where is the maximum likelihood (or MAP) estimate for the ’s involved and is the number of parameters. This choice was made in order to compare the results with implementations of BAS, RS and MC3 available in the supplementary to Clyde et al. (2011), where this approximation is considered. In that way, the model search procedures are compared based on the same selection criterion.

| Par | True | TOP | MJMCMC | MJMCMC2 | BAS | BAS-RS | RS | |||

| - | RM | MC | RM | MC | RM | RM | RM | MC | ||

| 0.29 | 0.00 | 7.38 | 15.54 | 4.54 | 16.62 | 6.47 | 3.67 | 6.01 | 2.11 | |

| 0.31 | 0.00 | 6.23 | 15.50 | 3.96 | 16.94 | 5.58 | 3.02 | 5.37 | 2.55 | |

| 0.35 | 0.00 | 4.86 | 14.62 | 2.78 | 13.66 | 4.22 | 2.12 | 3.91 | 2.37 | |

| 0.35 | 0.00 | 4.55 | 15.24 | 2.56 | 15.45 | 4.66 | 1.64 | 3.40 | 2.56 | |

| 0.36 | 0.00 | 4.90 | 16.52 | 2.92 | 17.39 | 5.42 | 2.45 | 3.65 | 2.61 | |

| 0.37 | 0.00 | 4.82 | 14.35 | 2.66 | 14.08 | 3.32 | 1.80 | 4.15 | 2.18 | |

| 0.40 | 0.00 | 9.25 | 20.93 | 5.65 | 22.18 | 9.75 | 4.82 | 6.76 | 2.83 | |

| 0.44 | 0.00 | 3.14 | 17.54 | 1.58 | 16.24 | 3.73 | 1.30 | 1.33 | 2.93 | |

| 0.44 | 0.00 | 4.60 | 18.73 | 2.29 | 17.90 | 4.87 | 1.30 | 1.51 | 2.42 | |

| 0.46 | 0.00 | 3.10 | 17.17 | 1.53 | 16.97 | 4.06 | 1.51 | 1.09 | 2.85 | |

| 0.61 | 0.00 | 3.68 | 16.29 | 1.63 | 13.66 | 3.89 | 1.39 | 2.19 | 2.35 | |

| 0.88 | 0.00 | 5.66 | 6.70 | 3.74 | 6.26 | 6.60 | 5.57 | 7.61 | 2.15 | |

| 0.91 | 0.00 | 5.46 | 6.81 | 3.95 | 6.90 | 4.66 | 3.14 | 4.32 | 1.57 | |

| 0.97 | 0.00 | 1.90 | 1.74 | 1.35 | 1.34 | 2.43 | 1.96 | 2.30 | 1.1 | |

| 1.00 | 0.00 | 0.00 | 0.43 | 0.00 | 0.32 | 0.00 | 0.00 | 0.00 | 0.37 | |

| 1.00 | 0.00 | 0.00 | 0.57 | 0.00 | 0.41 | 0.00 | 0.00 | 0.00 | 0.33 | |

| 1.00 | 0.00 | 0.00 | 0.41 | 0.00 | 0.33 | 0.00 | 0.00 | 0.00 | 0.23 | |

| 1.00 | 0.00 | 0.00 | 0.43 | 0.00 | 0.39 | 0.00 | 0.00 | 0.00 | 0.23 | |

| 1.00 | 0.00 | 0.00 | 0.47 | 0.00 | 0.35 | 0.00 | 0.00 | 0.00 | 0.24 | |

| 1.00 | 0.00 | 0.00 | 0.52 | 0.00 | 0.36 | 0.00 | 0.00 | 0.00 | 0.41 | |

| 1.00 | 1.00 | 0.72 | 0.72 | 0.85 | 0.85 | 0.74 | 0.85 | 0.68 | 0.68 | |

| Eff | 10000 | 5148 | 5148 | 9988 | 9988 | 10000 | 10000 | 1889 | 1889 | |

| Tot | 10000 | 9998 | 9998 | 19849 | 19849 | 10000 | 10000 | 10000 | 10000 | |

Some of the covariates involved have large correlations. This induces both multimodality within the space of models and sparsity of the locations of the modes and creates an interesting example for comparison of different search strategies. As one can see in Table 4, MJMCMC outperformed pure BAS by far both in terms of posterior mass captured and in terms of root mean square errors of marginal inclusion probabilities when based on the same number of unique models. MJMCMC outperformed RS as well. The latter got stuck in some local modes and could only reach 1889 unique models for the 10000 models visited. We could not reach 10000 unique models for the RS algorithm within a reasonable time for this example either (again most likely the algorithm could not escape from local extrema), hence such a scenario is not reported. Even for almost two times less originally visited models in , comparing to BAS, MJMCMC gives almost the same results in terms of the posterior mass captured and errors. MJMCMC, for the given number of unique models visited, did not outperform a combination of MCMC and BAS (BAS-RS), which is recommended by Clyde et al. (2011) for larger model spaces; both of them gave approximately identical results.

4.3 Example 3

This experiment is based on a much larger model space in comparison to all of the other examples. We address the protein activity data (Clyde et al., 1998) and consider all main effects together with the two-way interactions and quadratic terms of the continuous covariates resulting in 88 covariates in total. This corresponds to a model space of cardinality , a number far to high to perform full search through all models. This model space is additionally multimodal, which is the result of having high correlations between numerous of the addressed covariates (17 pairs of covariates have correlations above 0.95).

We analyzed the data set using Bayesian linear regression with the binomial prior (4) with for and a Zellner’s g-prior with for (the data has observations). We then compared the performance of MJMCMC, BAS and RS. For this example we have also addressed the ESS++ algorithm (Bottolo et al., 2011).

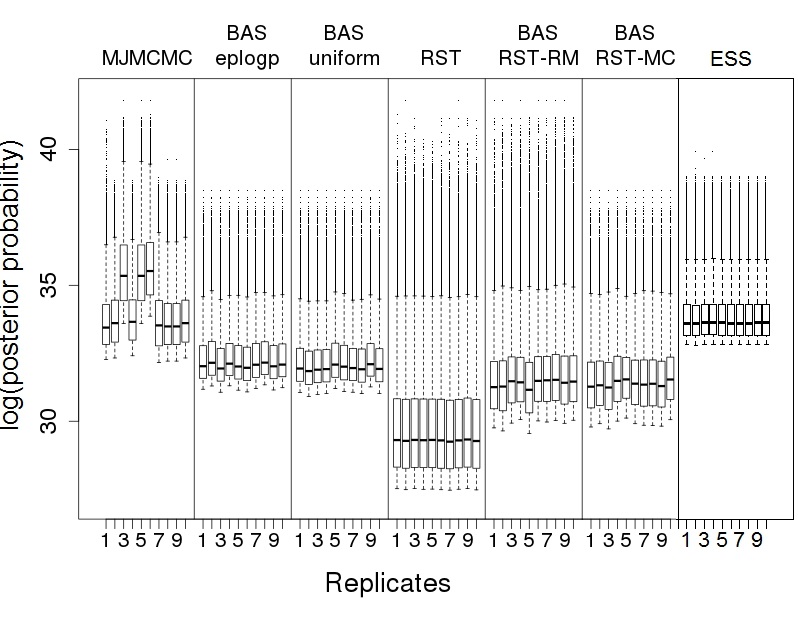

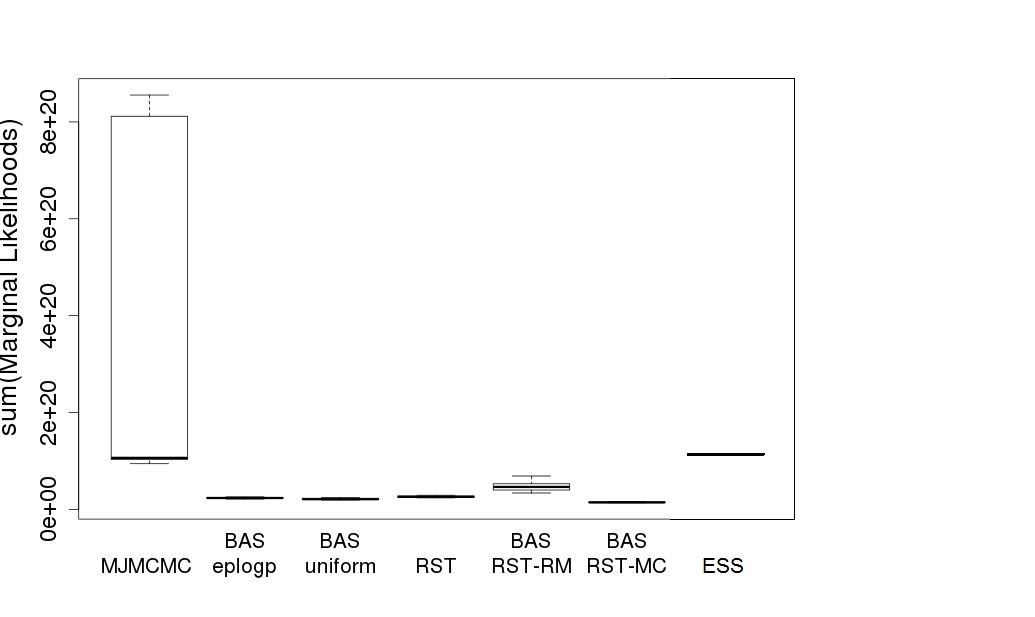

The reported RS results are based on the RS algorithm run for iterations and a thinning rate of (named RST in Clyde et al. (2011)). BAS was run with several choices of initial sampling probabilities such as uniformly distributed within the model space one, eplogp adjusted (Clyde et al., 2011), and those based on RM and MC approximations obtained by the RST algorithm. For the first two initial sampling probabilities BAS was run for iterations. For the two latter (the BAS-RST-RM and BAS-RST-MC) algorithms) first RS was run for iterations providing models for estimating initial sampling probabilities and then BAS was run for the other iterations based on RM or MC estimates of the marginal inclusion probabilities. MJMCMC was run until unique models were obtained. ESS++ was run with default search settings until unique models were visited. All of the algorithms were replicated 10 times.

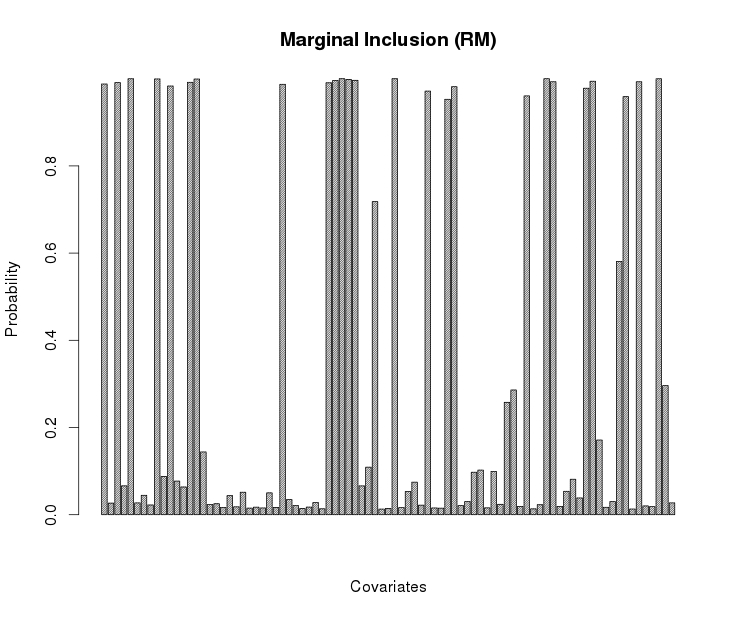

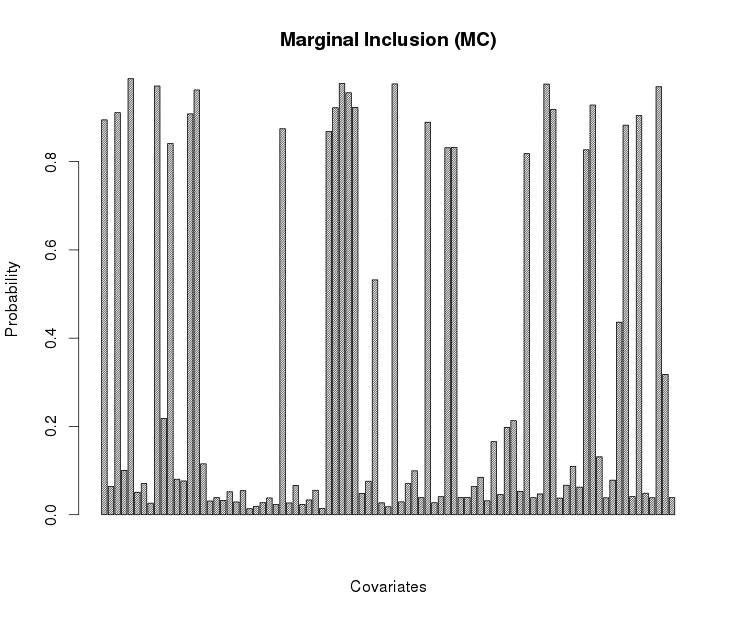

In Figure 3 box-plots of the best 100000 models captured by the corresponding replications of the algorithms as well as posterior masses captured by them are displayed. BAS with both uniform and eplogp initial sampling probabilities performed rather poorly in comparison to other methods, whilst BAS combined with RM approximations from RST did slightly better. ESS++ as well as MJMCMC show the most promising results. BAS with RM initial sampling probabilities usually managed to find models with the highest posterior probabilities, however MJMCMC in general captured by far higher posterior mass within the same amount of unique models addressed. Marginal inclusion probabilities obtained by the best run of MJMCMC with respect to mass (denominator of (8) with value in Figure 3) are reported in Figure 4, whilst those obtained by other methods can be found in Clyde et al. (2011). Since MJMCMC obtained the highest posterior mass, we expect that the corresponding RM estimates of the marginal inclusion probabilities are the least biased, moreover they perfectly agree with the MC approximations. Although MJMCMC in all of the obtained replications outperformed most of the competitors in terms of the posterior mass captured, it itself exhibited significant variation between the runs (right panel of Figure 3). The latter issue can be explained by that we are only allowing visiting of the total model space in the addressed replications, which might be not enough to always converge to the same posterior mass captured. Note however that the variability in the results obtained from different runs of MJMCMC clearly indicates that more iterations are needed, while the other methods may indicate (wrongly) that sufficient iterations have been performed.

4.4 Example 4

In this example we illustrate how MJMCMC works for GLMM models. As illustration, we address genomic and epigenomic data on Arabadopsis. Arabadopsis is a plant model organism with a lot of genomic/epigenomic data easily available (Becker et al., 2011). At each position on the genome, a number of reads are allocated. At locations with a nucleotide of type cytosine (C), reads are either methylated or not. Our focus will be on modeling the amount of methylated reads through different covariates including (local) genomic structures, gene classes and expression levels. The studied data was obtained from the NCBI GEO archive (Barrett et al., 2013).

We model the number of methylated reads per loci , where is the number of reads, through (1)-(3) by a Poisson distribution for the response and . Since in general the ratio of methylated bases is low, we have preferred the Poisson distribution of the responses to the binomial. The mean is modeled via the log link to the chosen covariates, including an offset defined by per location, and a spatially correlated random effect which is modeled via an process with parameter , namely with , . Thus, we take into account spatial dependence structures of methylation rates along the genome as well as the variance of the observations not explained by the covariates. We use the binomial prior (4) with for and the Gaussian prior for the regression coefficients:

For the parameters within the random effects, we first reparametrize to , and assume

| (16) | ||||

| and | ||||

| (17) | ||||

Marginal likelihoods were for this example calculated through the INLA package (www.r-inla.org).

Par

True

TOP

MJMCMC

RS MCMC

RM

RM

MC

RM

MC

0.0035

0.0005

0.0022

2.0416

0.0198

1.9768

0.0048

0.0006

0.0051

2.0899

0.0257

1.9352

0.0065

0.0006

0.0056

2.3459

0.0353

0.6887

0.0076

0.0007

0.0017

3.3660

0.0353

1.2374

0.0076

0.0007

0.0079

2.3279

0.0344

1.6163

0.0096

0.0007

0.0075

2.3342

0.0455

1.7170

0.0813

0.0007

0.0200

3.6851

0.1679

2.8022

0.0851

0.0006

0.0134

2.7179

0.0766

1.9136

0.1185

0.0008

0.0184

3.3149

0.1773

3.0463

0.3042

0.0006

0.0071

9.4926

0.1106

3.7344

0.9827

0.0002

0.0063

2.5350

0.0638

1.5681

1.0000

0.0007

0.0000

4.7091

0.0000

1.2258

1.0000

0.0000

0.0000

2.7343

0.0000

0.9971

1.0000

1.0000

0.9998

0.9998

0.9977

0.9977

Eff

8192

385

1758

1758

155

155

Tot

8192

385

3160

3160

10000

10000

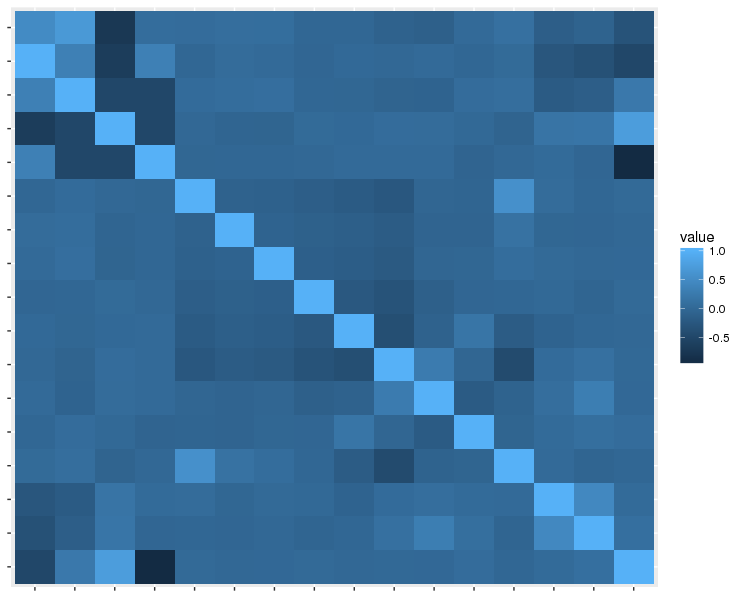

We have addressed different covariates in addition to the intercept. We have considered a factor with 3 levels corresponding to whether a location belongs to a CGH, CHH or CHG genetic region, where H is either A, C or T and thus generating two covariates and corresponding to whether a location is CGH or CHH. A second factor indicates whether a distance to the previous cytosine nucleobase (C) in DNA is 1, 2, 3, 4, 5, from 6 to 20 or greater than 20 inducing the binary covariates . A third factor corresponds to whether a location belongs to a gene from a particular group of genes of biological interest, these groups are indicated as , , or inducing 3 additional covariates . Finally, we have considered two binary covariates and represented by expression levels exceeding 3000 and 10000, respectively. The cardinality of our search space is for this example. The correlation structure between these 13 covariates is represented in Figure 5.

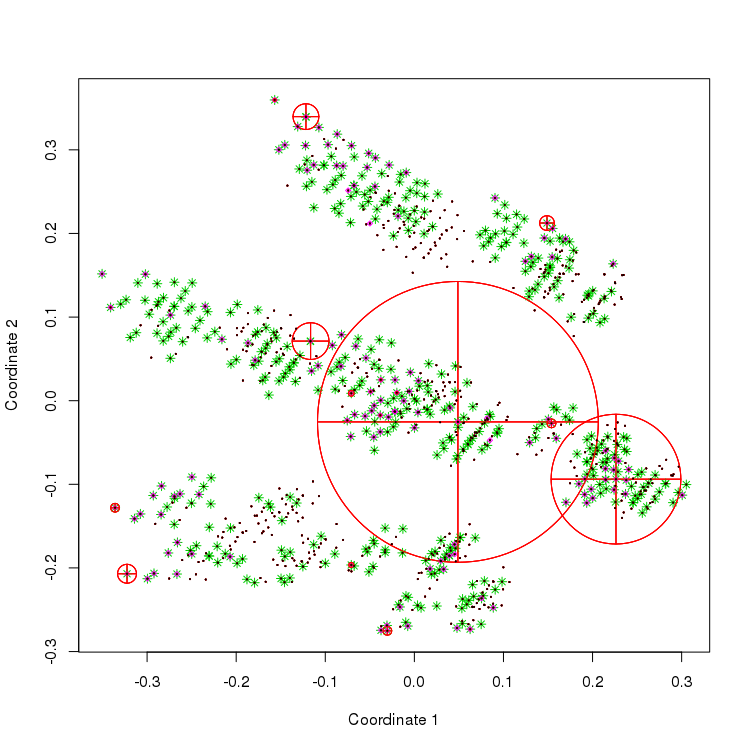

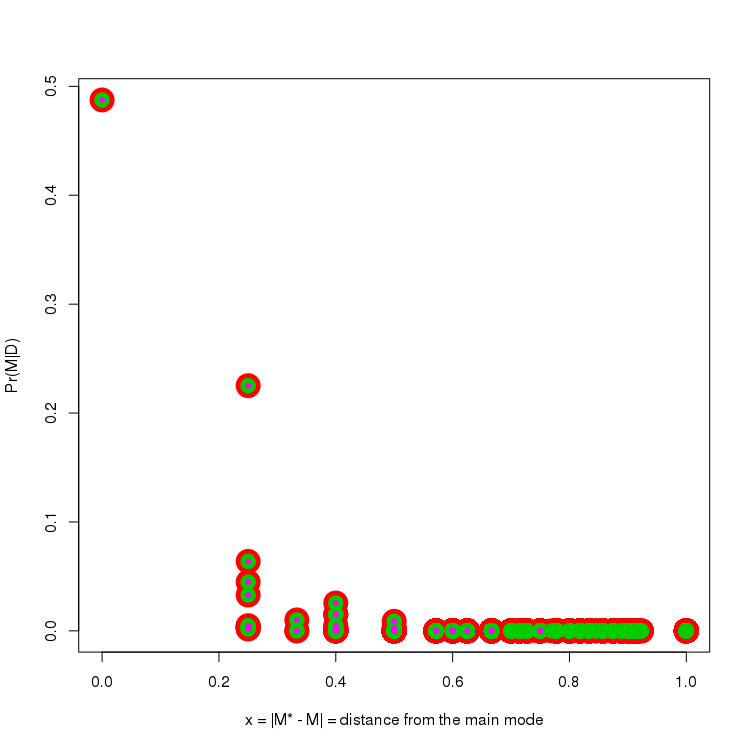

As seen from Table 5 (TOP column), within just the 385 best unique models (2.35% of the total model space) we were able to capture almost full posterior mass for this problem. The model space, as shown in Figure 6, has very few sparsely located modes in a quite large model space. In this example we compared MJMCMC and a simple MCMC algorithm, the latter was allowed to only swap one component per iteration (similar to the RS algorithm within the BAS package). This example contains most of the mass in just two closely located models as can be seen in Figure 6. This is why a simple RS MCMC can capture essentially most of the mass after 10000 iterations. At the same time there are a few small modes that lie a bit further from the region of the high concentration of mass, which the simple RS MCMC algorithm did not capture. Essentially, RS MCMC stayed within a few modes for most of the time, never being able to travel to the more remote parts of the model space and generated very few (155 on average) unique models. This number is here very low compared to the total number of models visited (10000). If there were more sparsely located remote modes, the simple RS MCMC algorithm would run into the problems similar to those discussed in the previous examples and miss a significant amount of mass. For MJMCMC, we ran the algorithm until 3160 models where visited, resulting in 1758 unique models. MJMCMC was able to capture the mass also from the remote small modes, adding a bit to the captured mass, slightly outperforming the simple RS MCMC algorithm. As can be seen in Table 5, MJMCMC outperformed the simple RS MCMC algorithm in terms of the errors of marginal model probabilities. Marginal inclusion probabilities in terms of RM are also more precise when MJMCMC is used. MC based approximations are also in this case worse than the RM versions, in this case with MJMCMC slightly worse.

According to marginal inclusion probabilities ( column in Table 5, obtained from full enumeration), factors of whether the location is CGH or CHH ( and ) are both extremely significant, as well as the higher cut off for the level of expression (). Additionally, factors for and groups of genes ( ad ) have non-zero marginal inclusion probabilities and reasonably high significance. In future it would be of interest to obtain additional covariates such as whether a nucleobase belongs to a particular part of the gene like the promoter or a coding region. Furthermore, it is of interest to address factors whether a base is located within a CpG island (regions with a high frequency of C bases) or whether it belongs to a transposone. Moreover, interactions of these covariates may be interesting. Alternative choices of the response distributions (e.g. binomial or negative binomial) and/or other types of random effects (, ) might also be of an interest.

5 Summary and discussion

In this paper we have introduced the mode jumping MCMC (MJMCMC) approach for calculating posterior model probabilities and performing Bayesian model averaging and selection. The algorithm incorporates the ideas of MCMC with the possibility of large jumps combined with local optimizers to generate proposals in the discrete space of models. Unlike standard MCMC methods applied to variable selection, the developed procedure avoids getting stuck in local modes and manages to iterate through all of the important models much faster. In many cases it also outperforms Bayesian Adaptive Sampling (BAS), having the tendency to capture a higher posterior mass within the same amount of unique models visited. This can be explained by that for problems with numerous covariates BAS requires good initial marginal inclusion probabilities to perform well. Clyde et al. (2011) demonstrated that estimates of marginal inclusion probabilities obtained from preliminary MCMC runs could largely improve BAS. A combination of MJMCMC with BAS could possibly improve both algorithms even further.

The EMJMCMC R-package is developed and currently available from the Git Hub repository: http://aliaksah.github.io/EMJMCMC2016/. The methodology depends on the possibility of calculating marginal likelihoods within models accurately. The developed package gives a user high flexibility in the choice of methods to obtain marginal likelihoods. Whilst the default choice for marginal likelihood calculations is based on INLA (Rue et al., 2009), we also have adopted efficient C based implementations for exact calculations in Bayesian linear regression and approximate calculations in Bayesian logistic and Poisson regressions in combination with g-priors as well as other priors. Several model selection criteria for the class of methods are also addressed. Extensive parallel computing for both MCMC moves and local optimizers is available within the developed package. Within a standard call, a user specifies how many threads are addressed within the in-build mclapply function or snow based parallelization. An advanced user can specify his own function to parallelize computations on both the MCMC and local optimization levels, using, for instance, modern graphical processing units - GPUs, which in turn allows additional efficiency and flexibility.

Whilst the renormalized model estimators (8) are Fisher consistent (Clyde et al., 2011), they remain generally speaking biased; although their bias reduces to zero asymptotically (with respect to the number of iterations). Standard MCMC based estimators such as (7), which are both consistent and unbiased, are also available through our procedure; these estimators however tend to have a much higher variance than the aforementioned ones. As one of the further developments it would be of interest to combine knowledge available from both groups of estimators to adjust for bias and variance, which is vital for higher dimensional problems.

Another aspect that requires being discussed is the model selection criterion. Different criteria can sometimes disagree about the results of model selection. In order to avoid confusion, the researcher should be clear about the stated goals. If the goal is prediction rather than inference one should adjust for that and use AIC, WAIC (Watanabe, 2009) or DIC (Spiegelhalter et al., 2002) rather than BIC or posterior model probability as selection criterion in MJMCMC. These choices are possible within the EMJMCMC package as well.

Based on several experiments, we claim MJMCMC to be a rather competitive algorithm that is addressing the wide class of Generalized Linear Mixed Models (GLMM). In particular, for this class of models one can incorporate a random effect, which both can model the variability unexplained by the covariates and can introduce dependence between observations, creating additional modeling flexibility. Estimation of parameters for such models becomes significantly harder in comparison to simple GLM. This creates the necessity to address parallel computing extensively. We have enabled the latter within our package by means of combining methods for calculating marginal likelihoods, such as the INLA methodology, and parallel MJMCMC algorithm.

Currently, we only consider choice of covariates to be included into the model. However, the mode jumping procedure can easily be extended to more general cases. In the future it would be of interest to extend the procedure to model selection and model averaging jointly across covariates, link functions, random effect structures and response distributions. Such extensions will require even more accurate tuning of control parameters of the algorithm, introducing another important direction for further research.

ACKNOWLEDGMENTS

The authors gratefully acknowledge the CELS project at the University of Oslo, http://www.mn.uio.no/math/english/research/groups/cels/index.html, for giving the opportunity, inspiration and motivation to write this paper. The authors also thank the editor, the associate editor, and the referees for helpful comments and suggestions which significantly improved the manuscript. We would also like to acknowledge Paul Grini, Ole Christian Lingjærde and Melinka Butenko for the valuable discussions on the design of Example 4. Furthermore we want to gratitude Ole Christian Lingjærde for the final proofreading.

References

References

- (1)

- Al-Awadhi et al. (2004) Al-Awadhi, F., Hurn, M. and Jennison, C. (2004), ‘Improving the acceptance rate of reversible jump MCMC proposals’, Statistics and Probability Letters 69(2), 189 – 198.

- Andrieu et al. (2010) Andrieu, C., Doucet, A. and Holenstein, R. (2010), ‘Particle Markov chain Monte Carlo methods’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 72(3), 269–342.

- Andrieu and Roberts (2009) Andrieu, C. and Roberts, G. O. (2009), ‘The pseudo-marginal approach for efficient Monte Carlo computations’, The Annals of Statistics (2), 697–725.

- Banterle et al. (2015) Banterle, M., Grazian, C., Lee, A. and Robert, C. P. (2015), ‘Accelerating Metropolis-Hastings algorithms by delayed acceptance’, arXiv preprint arXiv:1503.00996 .

- Barbieri et al. (2004) Barbieri, M. M., Berger, J. O. et al. (2004), ‘Optimal predictive model selection’, The annals of statistics 32(3), 870–897.

- Barrett et al. (2013) Barrett, T., Wilhite, S. E., Ledoux, P., Evangelista, C., Kim, I. F., Tomashevsky, M., Marshall, K. A., Phillippy, K. H., Sherman, P. M., Holko, M. et al. (2013), ‘NCBI GEO: archive for functional genomics data sets - update’, Nucleic acids research 41(D1), D991–D995.

- Beaumont (2003) Beaumont, M. A. (2003), ‘Estimation of population growth or decline in genetically monitored populations’, Genetics 164(3), 1139–1160.

- Becker et al. (2011) Becker, C., Hagmann, J., Müller, J., Koenig, D., Stegle, O., Borgwardt, K. and Weigel, D. (2011), ‘Spontaneous epigenetic variation in the Arabidopsis thaliana methylome’, Nature 480(7376), 245–249.

- Bivand et al. (2015) Bivand, R., Gómez-Rubio, V., Rue, H. et al. (2015), ‘Spatial Data Analysis with R-INLA with Some Extensions’, Journal of Statistical Software 63(i20).

- Bivand et al. (2014) Bivand, R. S., Gómez-Rubio, V. and Rue, H. (2014), ‘Approximate Bayesian inference for spatial econometrics models’, Spatial Statistics 9, 146–165.

- Blum and Roli (2003) Blum, C. and Roli, A. (2003), ‘Metaheuristics in combinatorial optimization: Overview and conceptual comparison’, ACM Computing Surveys (CSUR) 35(3), 268–308.

- Bottolo et al. (2011) Bottolo, L., Chadeau-Hyam, M., Hastie, D. I., Langley, S. R., Petretto, E., Tiret, L., Tregouet, D. and Richardson, S. (2011), ‘ESS++: a C++ objected-oriented algorithm for Bayesian stochastic search model exploration’, Bioinformatics 27(4), 587–588.

- Bové and Held (2011) Bové, D. S. and Held, L. (2011), ‘Bayesian fractional polynomials’, Statistics and Computing 21(3), 309–324.

- Chen et al. (2014) Chen, T., Fox, E. and Guestrin, C. (2014), Stochastic gradient Hamiltonian Monte Carlo, in ‘International Conference on Machine Learning’, pp. 1683–1691.

- Chib (1995) Chib, S. (1995), ‘Marginal likelihood from the Gibbs output’, Journal of the American Statistical Association 90(432), 1313–1321.

- Chib and Jeliazkov (2001) Chib, S. and Jeliazkov, I. (2001), ‘Marginal likelihood from the Metropolis–Hastings output’, Journal of the American Statistical Association 96(453), 270–281.

- Chopin et al. (2013) Chopin, N., Jacob, P. E. and Papaspiliopoulos, O. (2013), ‘SMC2: an efficient algorithm for sequential analysis of state space models’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 75(3), 397–426.

- Christen and Fox (2005) Christen, J. A. and Fox, C. (2005), ‘Markov chain Monte Carlo using an approximation’, Journal of Computational and Graphical statistics 14(4), 795–810.

- Clyde et al. (2011) Clyde, M. A., Ghosh, J. and Littman, M. L. (2011), ‘Bayesian adaptive sampling for variable selection and model averaging’, Journal of Computational and Graphical Statistics 20(1), 80–101.

- Clyde et al. (1998) Clyde, M., Parmigiani, G. and Vidakovic, B. (1998), ‘Multiple shrinkage and subset selection in wavelets’, Biometrika 85(2), 391–401.

- David (2015) David, M. (2015), ‘Auto insurance premium calculation using generalized linear models’, Procedia Economics and Finance 20, 147 – 156.

- de Souza et al. (2015) de Souza, R., Cameron, E., Killedar, M., Hilbe, J., Vilalta, R., Maio, U., Biffi, V., Ciardi, B. and Riggs, J. (2015), ‘The overlooked potential of generalized linear models in astronomy, i: Binomial regression’, Astronomy and Computing 12, 21 – 32.

- Doucet et al. (2015) Doucet, A., Pitt, M. K., Deligiannidis, G. and Kohn, R. (2015), ‘Efficient implementation of Markov chain Monte Carlo when using an unbiased likelihood estimator’, Biometrika 102(2), 295.

- Eksioglu et al. (2002) Eksioglu, S. D., Pardalos, P. M. and Resende, M. G. (2002), Parallel metaheuristics for combinatorial optimization, in R. Corrêa, I. Dutra, M. Fiallos and F. Gomes, eds, ‘Models for Parallel and Distributed Computation’, Vol. 67 of Applied Optimization, Springer US, pp. 179–206.

- Friel and Wyse (2012) Friel, N. and Wyse, J. (2012), ‘Estimating the evidence – a review’, Statistica Neerlandica 66(3), 288–308.

- Frommlet et al. (2012) Frommlet, F., Ljubic, I., Arnardóttir Helga, B. and Bogdan, M. (2012), ‘QTL Mapping Using a Memetic Algorithm with Modifications of BIC as Fitness Function’, Statistical Applications in Genetics and Molecular Biology 11(4), 1–26.

- George and McCulloch (1997) George, E. I. and McCulloch, R. E. (1997), ‘Approaches for Bayesian variable selection’, Statistica Sinica 7(2), 339–373.

- Geyer (1991) Geyer, C. J. (1991), ‘Markov chain Monte Carlo maximum likelihood’.

- Ghosh (2015) Ghosh, J. (2015), ‘Bayesian model selection using the median probability model’, Wiley Interdisciplinary Reviews: Computational Statistics 7(3), 185–193.

- Grossi and Bellini (2006) Grossi, L. and Bellini, T. (2006), Credit risk management through robust generalized linear models, in S. Zani, A. Cerioli, M. Riani and M. Vichi, eds, ‘Data Analysis, Classification and the Forward Search’, Studies in Classification, Data Analysis, and Knowledge Organization, Springer Berlin Heidelberg, pp. 377–386.

- Hubin and Storvik (2016) Hubin, A. and Storvik, G. (2016), ‘Estimating the marginal likelihood with Integrated nested Laplace approximation (INLA)’. arXiv:1611.01450v1.

- Jordan et al. (1999) Jordan, M. I., Ghahramani, Z., Jaakkola, T. S. and Saul, L. K. (1999), ‘An introduction to variational methods for graphical models’, Machine learning 37(2), 183–233.

- Kou et al. (2006) Kou, S., Zhou, Q. and Wong, W. H. (2006), ‘Discussion paper equi-energy sampler with applications in statistical inference and statistical mechanics’, The annals of Statistics pp. 1581–1619.

- Liang (2010) Liang, F. (2010), ‘A double Metropolis–Hastings sampler for spatial models with intractable normalizing constants’, Journal of Statistical Computation and Simulation 80(9), 1007–1022.

- Liu et al. (2000) Liu, J. S., Liang, F. and Wong, W. H. (2000), ‘The Multiple-Try Method and Local Optimization in Metropolis Sampling’, Journal of the American Statistical Association 95(449), 121–134.

- Lobréaux and Melodelima (2015) Lobréaux, S. and Melodelima, C. (2015), ‘Detection of genomic loci associated with environmental variables using generalized linear mixed models’, Genomics 105(2), 69 – 75.

- Luo (2016) Luo, G. (2016), ‘A review of automatic selection methods for machine learning algorithms and hyper-parameter values’, Network Modeling Analysis in Health Informatics and Bioinformatics 5(1), 1–16.

- Madigan et al. (1995) Madigan, D., York, J. and Allard, D. (1995), ‘Bayesian graphical models for discrete data’, International Statistical Review/Revue Internationale de Statistique pp. 215–232.

- Marin et al. (2012) Marin, J.-M., Pudlo, P., Robert, C. P. and Ryder, R. J. (2012), ‘Approximate Bayesian computational methods’, Statistics and Computing 22(6), 1167–1180.

- McGrory and Titterington (2007) McGrory, C. A. and Titterington, D. (2007), ‘Variational approximations in Bayesian model selection for finite mixture distributions’, Computational Statistics & Data Analysis 51(11), 5352–5367.

- Miasojedow et al. (2013) Miasojedow, B., Moulines, E. and Vihola, M. (2013), ‘An adaptive parallel tempering algorithm’, Journal of Computational and Graphical Statistics 22(3), 649–664.

- Michiels et al. (2010) Michiels, W., Aarts, E. and Korst, J. (2010), Theoretical Aspects of Local Search, 1st edn, Springer Publishing Company, Incorporated.

- Neal et al. (2011) Neal, R. M. et al. (2011), ‘MCMC using Hamiltonian dynamics’, Handbook of Markov Chain Monte Carlo 2(11).

- Newton and Raftery (1994) Newton, M. A. and Raftery, A. E. (1994), ‘Approximate Bayesian inference with the weighted likelihood bootstrap’, Journal of the Royal Statistical Society. Series B (Methodological) pp. 3–48.

- Raftery et al. (1997) Raftery, A. E., Madigan, D. and Hoeting, J. A. (1997), ‘Bayesian model averaging for linear regression models’, Journal of the American Statistical Association 92(437), 179–191.

- Robert and Casella (2005) Robert, C. P. and Casella, G. (2005), Monte Carlo Statistical Methods, Springer Texts in Statistics, Springer-Verlag New York, Inc., Secaucus, NJ, USA.

- Rohde (2002) Rohde, D. L. T. (2002), ‘Methods for binary multidimensional scaling’, Neural Comput. 14(5), 1195–1232.

- Rue et al. (2009) Rue, H., Martino, S. and Chopin, N. (2009), ‘Approximate Bayesian inference for latent Gaussian models by using integrated nested Laplace approximations’, Journal of the Royal Statistical Sosciety 71(2), 319–392.

- Salakhutdinov (2009) Salakhutdinov, R. R. (2009), Learning in Markov random fields using tempered transitions, in ‘Advances in neural information processing systems’, pp. 1598–1606.

- Sengupta et al. (2016) Sengupta, B., Friston, K. J. and Penny, W. D. (2016), ‘Gradient-based MCMC samplers for dynamic causal modelling’, NeuroImage 125, 1107–1118.

- Skrondal and Rabe-Hesketh (2003) Skrondal, A. and Rabe-Hesketh, S. (2003), ‘Some applications of generalized linear latent and mixed models in epidemiology: Repeated measures, measurement error and multilevel modeling’, Norwegian Journal of Epidemology 13(2), 265–278.

- Song and Liang (2015) Song, Q. and Liang, F. (2015), ‘A split-and-merge Bayesian variable selection approach for ultrahigh dimensional regression’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 77(5), 947–972.

- Spiegelhalter et al. (2002) Spiegelhalter, D. J., Best, N. G., Carlin, B. P. and Van Der Linde, A. (2002), ‘Bayesian measures of model complexity and fit’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 64(4), 583–639.

- Storvik (2011) Storvik, G. (2011), ‘On the flexibility of Metropolis-Hastings acceptance probabilities in auxiliary variable proposal generation’, Scandinavian Journal of Statistics 38, 342–358.

- Stroup (2013) Stroup, W. W. (2013), Generalized linear mixed models : Modern concepts, methods and applications, CRC Press, Taylor & Francis, Boca Raton.

- Tierney (1996) Tierney, L. (1996), ‘Introduction to general state-space Markov chain theory’, Markov chain Monte Carlo in practice pp. 59–74.

- Tierney and Kadane (1986) Tierney, L. and Kadane, J. B. (1986), ‘Accurate approximations for posterior moments and marginal densities’, Journal of the american statistical association 81(393), 82–86.

- Tjelmeland and Hegstad (1999) Tjelmeland, H. and Hegstad, B. K. (1999), ‘Mode jumping proposals in MCMC’, Scandinavian journal of statistics 28, 205–223.

- Vandaele (1978) Vandaele, W. (1978), ‘Participation in illegitimate activities: Ehrlich revisited’, Deterrence and Incapacitation 1, 270–335.

- Watanabe (2009) Watanabe, S. (2009), ‘An introduction to algebraic geometry and statistical learning theory’.

- Yeh et al. (2012) Yeh, Y. T., Yang, L., Watson, M., Goodman, N. and Hanrahan, P. (2012), ‘Synthesizing open worlds with constraints using locally annealed reversible jump MCMC’, ACM Transactions on Graphics 31(4), 56–58.

- Zellner (1986) Zellner, A. (1986), ‘On assessing prior distributions and Bayesian regression analysis with g-prior distributions’, Bayesian inference and decision techniques: Essays in Honor of Bruno De Finetti 6, 233–243.

- Zhou (2011) Zhou, Q. (2011), ‘Multi-domain sampling with applications to structural inference of Bayesian networks’, Journal of the American Statistical Association 106(496), 1317–1330.

Appendix A Details of the MJMCMC algorithm

A.1 Multiple try MCMC algorithm

In addition to ordinary MCMC steps and mode jump MCMC, also multiple-try Metropolis (Liu et al., 2000) is considered. Multiple-try Metropolis is a sampling method that is a modified form of the Metropolis-Hastings method, designed to be able to properly parallelize the original Metropolis-Hastings algorithm. The idea of the method is to allow generating trial proposals in parallel from a proposal distribution . Then, is selected with probabilities proportional to some importance weights where . In the reversed move are generated from the proposal while . Finally, the move is accepted with probability

| (A-1) |

In the implementation of the algorithm, ordinary MCMC is considered as a special case of multiple try MCMC with . We recommend ordinary or multiple try MCMC steps are used in at least of the iterations with proposals of large jumps for the remaining 5%.

A.2 Choice of proposal distributions

The implementation of MJMCMC allows for great flexibility in the choices of proposal distributions for the large jumps, the local optimization and the last randomization.

-

1.

Table 1 lists the current possibilities for drawing indexes to swap in the first large jump. One should choose distributions where a large number of components are swapped.

-

2.

An important ingredient of the MJMCMC algorithm is the choice of local optimizer. In the current implementation of the algorithm, several choices are possible; simulated annealing, greedy optimizers based on best neighbor optimization or first improving neighbor (Blum and Roli, 2003) which is another variant of greedy local search accepting the first randomly selected solution better than the current. For each alternative the neighbors are defined through swapping a few of the ’s in the current model.

-

3.

For the last randomization, again Table 1 lists the possibilities, but in this case a small number of swaps will be preferable.

Different possibilities to combine the optimizers and proposals in a hybrid setting are also possible. Then, at each iteration, which proposal distributions and which optimizers to use are randomly drawn from the set of possibilities, see Robert and Casella (2005, sec 10.3) for the validity of such procedures.

A.3 Parallel computing in local optimizers

General principles of utilizing multiple cores in local optimization are provided in Eksioglu et al. (2002). Given a current state in the optimization routine, one can simultaneously draw several proposals with respect to a certain transition kernel and, if necessary, calculate the transition probabilities as the proposed models are evaluated. This step can be performed by parallel CPUs, GPUs or clusters. Consider an optimizer with the acceptance probability function , which either changes over the time (iterations) or remains unchanged. For the greedy local search . For the implemented version of the simulated annealing algorithm we consider , where is the SA temperature (Blum and Roli, 2003) parameter at iteration . The proposed parallelization strategy is given in detail in Algorithm 3.

A.4 Parallel MJMCMC with a mixture of proposals

Here we described the full version of our algorithm based on a combination of Algorithm 2 and the multiple try idea. The suggested MJMCMC approach allows to both jump between local modes efficiently and to explore the solutions around the modes simultaneously whilst keeping the desired ergodicity of the MJMCMC procedure. This implementation allows for mixtures of both local optimizers and proposals to be addressed within MJMCMC. Both the local optimization and the multiple try steps utilize multiple CPUs and GPUs of a single machine or a cluster of nodes. The pseudo-code of the algorithm is given in Algorithm 4 below. In this pseudo-code we consider the following notation:

-

1.

- the probability for a large jump;

-

2.

- the distribution for the choice of the local optimizers, a discrete distribution over a finite number of possibilities;

-

3.

- the distribution for the choice of large jump transition kernel, a discrete distribution over the possibilities in Table 1 with high probabilities on a large number of swaps;

-

4.

- the distribution for the choice of the randomizing kernel, a discrete distribution over a finite number of possibilities, also from Table 1, but with a small number of changes;

-

5.

- the distribution for the choice of proposals within the multiple try MCMC, a discrete distribution over the possibilities in Table 1 with a high probability on a small number of swaps.

The essential ingredients of the parallel version of the MJMCMC with a mixture of proposals (Algorithm 4) are as follows:

-

1.

Multiple try MCMC steps are performed for the steps with no mode jumps;

-

2.

At the iterations with mode jumps the large jump proposals , the optimization proposals , and the randomizing kernels are chosen randomly;

-

3.

At the iterations with no mode jumps the proposal is chosen randomly as ;

-

4.

The optimization steps are parallelized as described in A.3.

-

5.

The multiple-try steps are parallelized.

Appendix B Supplementary materials for the experiments

Table 1 describes some of the tuning parameters used for the different examples. Here, MTMCMC refers to the multiple try MCMC steps. The remaining tuning parameters, describing the mixture distributions and are specified in tables 2 (example 1), 3 (example 2), 4 (example 3) and 5 (example 4).

Example

CPU

SA

Greedy

MT

No

Num

S

LS

FI

Size

Steps

1

4

4

3

10

14

15

F

T

4

15

2

2

5

3

10

14

20

F

T

2

20

3

10

18

3

10

14

88

F

T

10

88

4

1

3

3

10

14

13

F

T

2

13

S.1

4

4

3

10

14

15

F

T

4

15

| Proposal | Optimizer | Frequency | Type 1 | Type 4 | Type 3 | Type 5 | Type 6 | Type 2 | |

| - | 0.1176 | 0.3348 | 0.2772 | 0.0199 | 0.2453 | 0.0042 | |||

| - | - | 2 | |||||||

| - | - | - | - | - | - | ||||

| - | 0.0164 | 0 | 1 | 0 | 0 | 0 | 0 | ||

| - | - | - | 4 | ||||||

| - | - | - | - | - | - | - | - | ||

| SA | 0.5553 | 0.0788 | 0.3942 | 0.1908 | 0.1928 | 0.1385 | 0.0040 | ||

| GREEDY | 0.2404 | 0.0190 | 0.3661 | 0.2111 | 0.2935 | 0.1046 | 0.0044 | ||

| MTMCMC | 0.2043 | 0.2866 | 0.1305 | 0.2329 | 0.1369 | 0.2087 | 0.0040 | ||

| - | - | 2 | |||||||

| - | - | - | - | - | - | ||||

| - | - | 0 | 0 | 0 | 0 | 0 | |||

| - | - | - | - | ||||||

| - | - | - | - | - | - | - |

| Proposal | Optimizer | Frequency | Type 1 | Type 4 | Type 3 | Type 5 | Type 6 | Type 2 | |

| - | 0.1179 | 0.3357 | 0.2779 | 0.0200 | 0.2459 | 0.0021 | |||

| - | - | 1 | |||||||

| - | - | - | - | - | - | ||||

| - | 0.0180 | 0 | 1 | 0 | 0 | 0 | 0 | ||

| - | - | - | 5 | ||||||

| - | - | - | - | - | - | - | - | ||

| SA | 0.5042 | 0.0636 | 0.3249 | 0.1571 | 0.2288 | 0.2246 | 0.0009 | ||

| GREEDY | 0.2183 | 0.0160 | 0.3085 | 0.1779 | 0.2474 | 0.2493 | 0.0007 | ||

| MTMCMC | 0.2774 | 0.2879 | 0.3016 | 0.1582 | 0.1107 | 0.1401 | 0.0013 | ||

| - | - | 1 | |||||||

| - | - | - | - | - | - | ||||

| - | - | 0 | 0 | 0 | 0 | 0 | |||

| - | - | - | - | ||||||

| - | - | - | - | - | - | - |