Smoothed Hierarchical Dirichlet Process: A Non-Parametric Approach to Constraint Measures

Abstract

Time-varying mixture densities occur in many scenarios, for example, the distributions of keywords that appear in publications may evolve from year to year, video frame features associated with multiple targets may evolve in a sequence. Any models that realistically cater to this phenomenon must exhibit two important properties: the underlying mixture densities must have an unknown number of mixtures; and there must be some “smoothness” constraints in place for the adjacent mixture densities. The traditional Hierarchical Dirichlet Process (HDP) may be suited to the first property, but certainly not the second. This is due to how each random measure in the lower hierarchies is sampled independent of each other and hence does not facilitate any temporal correlations. To overcome such shortcomings, we proposed a new Smoothed Hierarchical Dirichlet Process (sHDP). The key novelty of this model is that we place a temporal constraint amongst the nearby discrete measures in the form of symmetric Kullback-Leibler (KL) Divergence with a fixed bound . Although the constraint we place only involves a single scalar value, it nonetheless allows for flexibility in the corresponding successive measures. Remarkably, it also led us to infer the model within the stick-breaking process where the traditional Beta distribution used in stick-breaking is now replaced by a new constraint calculated from . We present the inference algorithm and elaborate on its solutions. Our experiment using NIPS keywords has shown the desirable effect of the model.

Key-words: Bayesian non-parametric, smoothed HDP, Bayesian inference, particle filtering, truncated Beta distribution.

1 Introduction

The Hierarchical Dirichlet Process (HDP) is an extension to the traditional Dirichlet process (DP), which essentially is comprised of a set of measures responsible for generating observations in each of its respective groups. The model allows the lower hierarchies of different groups to share “atoms” of their parents. They allow practitioners to apply the model to scenarios where independent mixture densities (of each group) share certain mixture components amongst its siblings which are inherited from their parents.

HDP is proposed by [17] and further studied by [18][19][14][8] and many other literatures in various disciplines have used it as an infinite version of Latent Dirichlet Allocation (LDA) [3]. In order to perform inference, [17] proposed three Monte-Carlo Markov Chain (MCMC) methods, two of which adopted collapsed Gibbs with and integrated out while the third one instantiated and integrated . The other works focus on the variational inference of HDP.

HDP has been successfully extended to model sequential data, in the form of so called HDP-HMM [17][19][8] and infinite HMM [2]. In these models, it is assumed that there exists a set of “time invariant measures”; A series of latent states are then drawn from these time invariant measures. The index for which a measure is to be used at time , is determined by the state of the previous state, i.e., . In order to cater for a “smooth” transition of states, [7] proposed the so-called ‘sticky’ HDP-HMM method. This approach adds a weight for the self-transition bias and places a separate prior on this prior. While such methods can be simpler in terms of inference, and may make more sense in situations where the states distributions may repeat at some point in time, they are not suitable for scenarios where the underlying distribution does not repeat in cycles, i.e., there is a need for a unique distribution to be assigned at each time . One example of this is the distribution of topics for a scientific journal, it is highly unlikely that its topic distributions will “come” back at some years in the future.

In order to generate a set of non-repeating and time-varying measures associated with observations at time , [12] proposed a Bayesian non-parametric approach in the form of Dependent Dirichlet processes. Based on an initial Dirichlet process, successive measures can be formed through three operations: superposition, subsampling and point transition. However, each of its operations can be very restrictive. For example, in sub-sampling, the “next” measure must have a fewer number of “sticks” than the first. The full flexibilities can only be achieved using combinations of all three operations, which makes the method very complex.

In this paper, we propose an alternative method to construct a time-varying dependent Dirichlet processes. Our model uses a very simple constraint in which the “smoothness” of the mixing measures in the second layer of HDP is achieved by simply placing a symmetric KL divergence constraint between them which is bounded by some fixed value . The key motivation is achieved through the following observation: Using our KL constraint, we can achieve our intended outcome by substituting the Beta distribution with a truncated Beta while still using the stick-breaking paradigm. The new truncation is calculated from any valued placed, and we observed that there are only a finite number of possible solution spaces for the truncations. Subsequently, we developed a sampling method using a Gibbs Sampling framework, where one of the Gibbs steps is achieved using particle filtering. We named our method Smoothed HDP (sHDP). Since we only applied a simple scalar value for its constraint, we argue it is the non-parametric approach to place constraints amongst Dirichlet Processes.

This rest of the paper is organised as follows: The second section describes the background of our model, and for completeness we include the related inference method. The third section is the elaborated description of our model. In section 4 we give the details of the inference method. In section 5, we test the model using synthetic data sets and the PAMI article key words. Section 6 provides a conclusion and some further discussions.

2 Background

To make this paper self-contained, we describe in this paper, some of the related models and their associated inference methods. We adopt the stick breaking paradigm for the representation of a Dirichlet process for both and . In terms of inference, given both and , particle filtering is used instead of Gibbs sampling to infer since the conditional distribution, cannot be obtained analytically. We use the slice sampling proposed by [4] for the sampling of the truncated Beta distribution.

2.1 The hierarchical Dirichlet process

Let be a diffusion measure (a measure having no atoms a.s.) [11] and be a scalar, and a discrete measure is sampled from [16]. Setting as the base measure and be the concentration parameter, we sample for . Obviously, should be discrete and some of the activated atoms for different are shared. We the adopt stick-breaking paradigm for the representation of a Dirichlet process, and denote

| (1) |

where is the Dirac function,

and and are mutually independent. As proposed by [17], can be formulated as

| (2) |

where

| (3) |

This formulation has an advantage in that the atoms in (2) are distinct.

2.2 Posterior sampling of the GEM distribution

The Chinese restaurant process is famous in the posterior sampling of the Dirichlet process. However, since our model requires to sample and explicitly, we use the method proposed by [9]. Denoting by the number of observations equal to , the posterior of is drawn as

| (4) | ||||

2.3 Slice sampling of a truncated Beta distribution

For the sampling of the truncated Beta distribution, we use slice sampling proposed by [4]. Let and be scalars and the density of is

where is the Dirac function.To sample from this truncated Beta distribution, we add auxiliary variable and construct a joint density of as

The method of drawing of and is:

-

1.

Sampling conditional on

-

2.

Sampling conditional on using inverse transform

-

(a)

if

-

(b)

if

-

(a)

2.4 Particle filtering

Particle filtering is used to sample the posterior distribution of sequential random variables. The advantage of particle filtering is that sampling is possible when the posterior density cannot be stated analytically. Let be latent random variables and be observed random variables. The joint distribution of them is

Let be a positive integer large enough, and the posterior sampling method is:

-

1.

For , propose from prior , and compute weights .

-

2.

Resample with weights , where denotes the vector of and denotes .

-

3.

For ,

-

(a)

propose from , and compute weights .

-

(b)

resample with weights .

-

(a)

The empirical posterior distribution of is

| (5) |

For a fully description of particle filtering please refer to [5].

3 The model of the smoothed HDP

In this section, we will give a full description of our model. In the traditional HDP, the discrete measures in the lower level, i.e., , are independent given the concentration parameter and the base measure . Separately from this independent assumption, we force the successive mixing measures and to be alike in terms of their symmetric KL divergence. Since both and are discrete measures with infinite many atoms, the computation of symmetric KL divergence between them is intractable. As a substitution, we propose an aggregated form of symmetric KL divergence that is computable. It can be proved that our aggregated symmetric KL divergence has the same expectation as the original form although they are not equal all the time.

3.1 The aggregated symmetric KL divergence

Let be scalars and be a diffusion measure, we sample a discrete base measure distributed as . Then the mixing measures () in the lower level are sampled from

with a constraint that the symmetric KL divergence for some fixed positive scalar . Suppose and have the following expression

The symmetric KL divergence between and is defined to be

| (6) |

Our problem is summarised as

Problem 1.

Given and ,

| sample | |||||

| subject to |

where is a scalar.

However, since (6) is a sum of infinite terms, the direct computation of (6) is intractable. Alternatively, for every atom , we define an aggregated symmetric KL divergence as

| (7) | ||||

Hence Problem 1 changes to

Problem 2.

Given and , for

| sample | (8) | |||||

| subject to |

where is a scalar.

The simplest way to set the value of is letting . But this does not make sense unless . However, direct algebraic calculation shows that the these two symmetric KL divergences are not agree at all times. Fortunately, the next theorem shows that the two terms, and , take the same value on average.

Theorem 1.

The expectation of and agrees with respect to , where and .

Proof.

In light of Theorem 1, we are safe to set . The details of sampling is given in the next subsection.

3.2 How to sample conditional on

Suppose , and is known, and we want to sample . Observe (7) and with a few algebraic calculation, the aggregated symmetric KL divergence constraint can be restated as

| (10) | ||||

where is a constant with respect to , which is

Note the function

is convex in the interval , the equality

| (11) |

has at most two roots. Showing in Figure 1, inequality (10) has solution of form

According to the relationship of and shown in (2), the truncating boundary for are and , where is the lower bound and is the upper bound and they can be or . Combine this constraint and the sampling method of in (2)(3) gives the solution of Problem 2 in Algorithm 1.

4 Inference

Note in Algorithm 1 we sample directly without the explicit likelihood, hence we cannot compute the posterior of analytically. Consequently, we have to use particle filtering to sample the posterior distribution of for .

4.1 Initialization

According to the definition of Dirichlet process [6], given concentration parameter and base measure , the expectation of distributions sampled from is . Let be an observation in phase , then the distribution of is modeled as

| (12) |

Followed by the deduction above and integrate out , the distribution of is

| (13) |

Hence the posterior distribution of can be sampled with help of (4). Suppose the prior of is a Dirichlet process and has the form of (1). Let be a set of the observations taking on cluster and , then the posterior of is

and the posterior of is

The posterior of is

where denote all the observations in phase and is the likelihood function.

4.2 Update of

Given , and , we use particle filtering to sample the posterior of . With the help of Algorithm 1, we give a proposal . The weight of this proposal is a product of probabilities

| (14) |

where is the number of observations in phase that take cluster . Using particle filtering, our sampling algorithm of is given in Algorithm 2.

4.3 Update of

The latent variable is used to indicate which cluster the observation is from. By the definition of , the probability of is . Given and , the likelihood is . Combining these together gives the posterior probability of , which is proportional to

where is the weight of the atom in .

4.4 Update of the hyper-parameters

For hyper-parameters and , we simply put Gamma distribution as priors on them, namely, and . The posterior of and are

respectively, where is the number of observations and is the number of distinct atoms. By adding auxiliary variable , it renders a mixture of Gammas for and . For details of the sampling method please refer to [20].

5 Experiments

We validate our smoothed HDP model using both synthetic and real dataset. MATLAB code of our experiments are available in the following website: https://github.com/llcc402/MATLAB-codes.

We assume the number of activated atoms is at most , hence the definition of the symmetric KL divergence (6) becomes:

| (15) |

In case some weights of become close to zero, causing the KL to become arbitrarily large, we set a minimum lower bound for every component weight to be .

5.1 Simulations on synthetic data set

Since the computation of the symmetric KL divergence only requires the knowledge of weights of the discrete measures, we discard the positions and sample instead. In our experiments, we set . Conditioning on , we sample , we then sample using our sHDP. We compare our model with HDP in order to show its smoothness effect. In HDP, while having and sampled in the same way as sHDP, is instead to be generated independently, i.e., . In all the experiments we set .

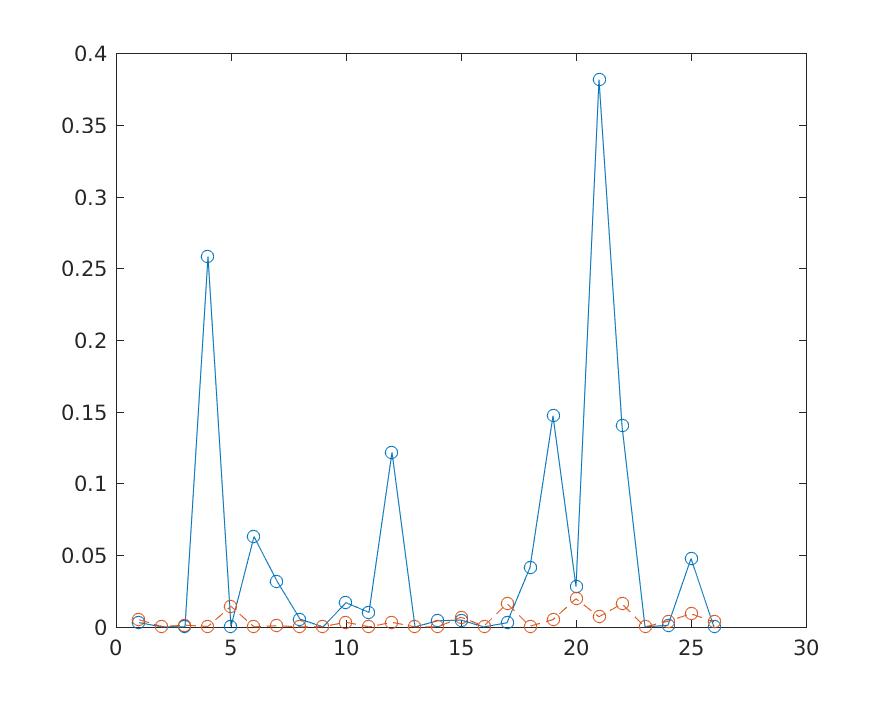

In sHDP, we set the KL bound , and compare the symmetric KL divergence between and . We repeat this procedure for times and compare the symmetric KL divergence by (15), and the result is shown in Figure 2(a). From this figure, we can see that the symmetric KL divergence of successive measures are much smaller than the traditional model. The mean of the values of sHDP is about , just as Theorem 1 illustrated, while the mean of traditional HDP is about .

In the second experiment, we show how the mean of KL varies with the bound we choose. By setting from to , we sample times and compute the symmetric KL divergence between them. This is shown in Figure 2(b). We show that the average symmetric KL divergence of the two distributions have increased when the bound value increases, which leads to an expected outcome.

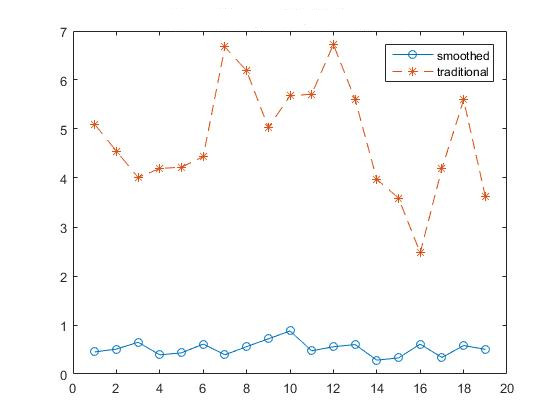

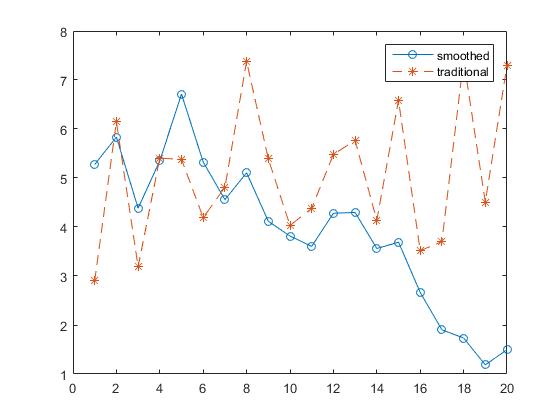

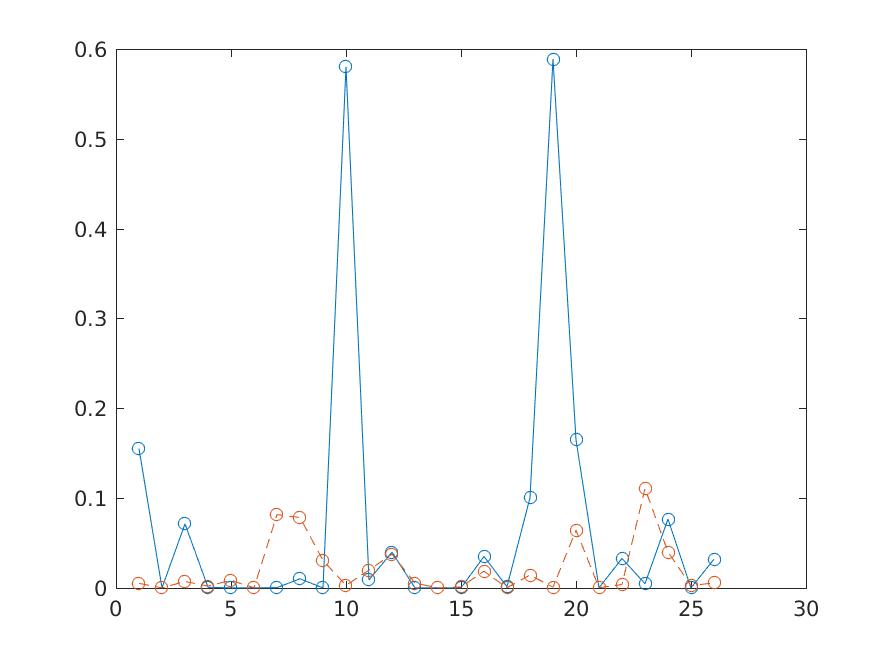

The last simulation is about using the time series data with the following setting: We first set , and , then we generate using sHDP. After that, we add Gamma noise to the distributions . The noise is simulated as follows. First generate independent random variables distributed as , then add them to . Lastly, we normalize the distributions. With these noisy distributions, we generate positive integers from each of them representing the component indices which are seen as the observations of the model in order to infer the posterior of . We sample the posterior from both HDP and sHDP. The symmetric KL divergence of successive distributions is shown in Figure 3(a). It can be seen that the symmetric KL values of sHDP are below while that of HDP are much larger, from about to . We also compared the distance between the theoretical value of and the posterior of both models in which the symmetric KL divergence is used as the measure of distance. It can be seen that in the first time intervals, the distances are similar, however, in the last sHDP results much smaller KL distance than that of the HDP.

5.2 Applications on real data set

We parsed the web page of PAMI and collected keywords from approximately papers published from 1990 to 2015. The keywords from one paper is seen as a document and the years are considered to be the phases. Similarly to [12], we transform each of the documents into a dimensional vector using the method proposed by [10]. We compute the similarity between two documents, which is the number of shared words divided by the total number of words in these two documents. Then we derive eigen vectors for the normalized graph Laplacian [15] and the column matrix of the eigen vectors are seen as the data set. For pre-processing, we change the standard deviation of the columns to be .

We assume the likelihood of the data is normally distributed with fixed variance and performed a hierarchical clustering of the data set. The clusters are considered to be the topics of the corpus. In the experiment, we set , and the KL bound , and we sample the posterior for iterations. The mixing measures represents the weights of the keyword clusters for each year.

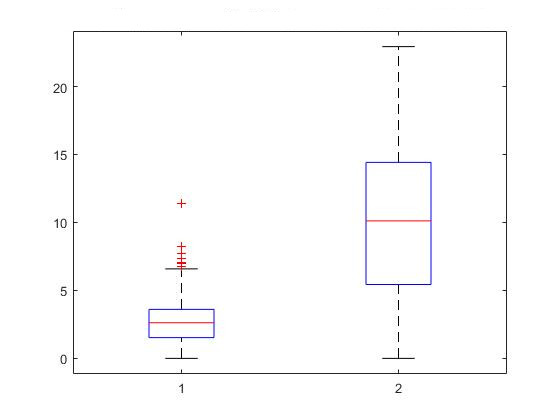

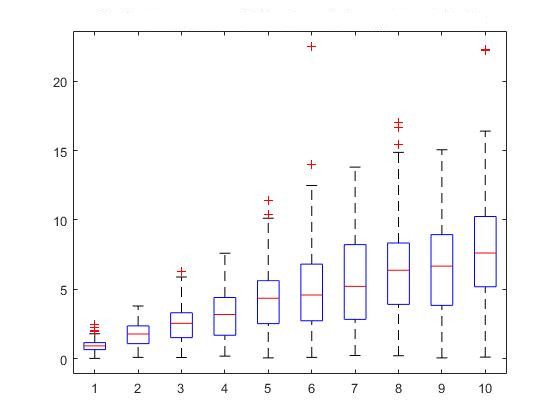

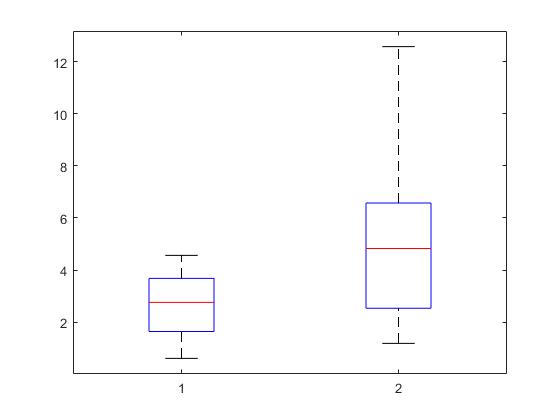

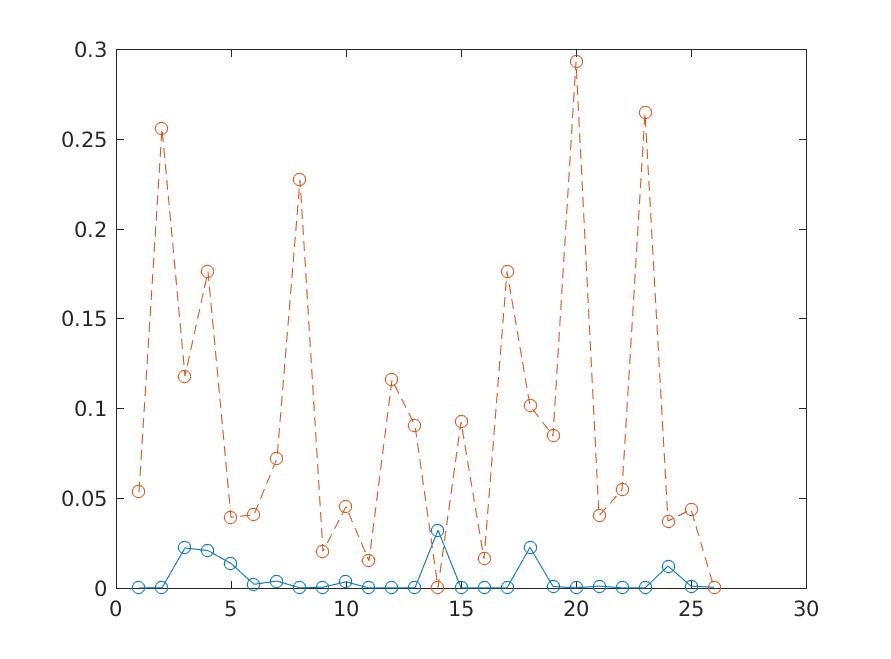

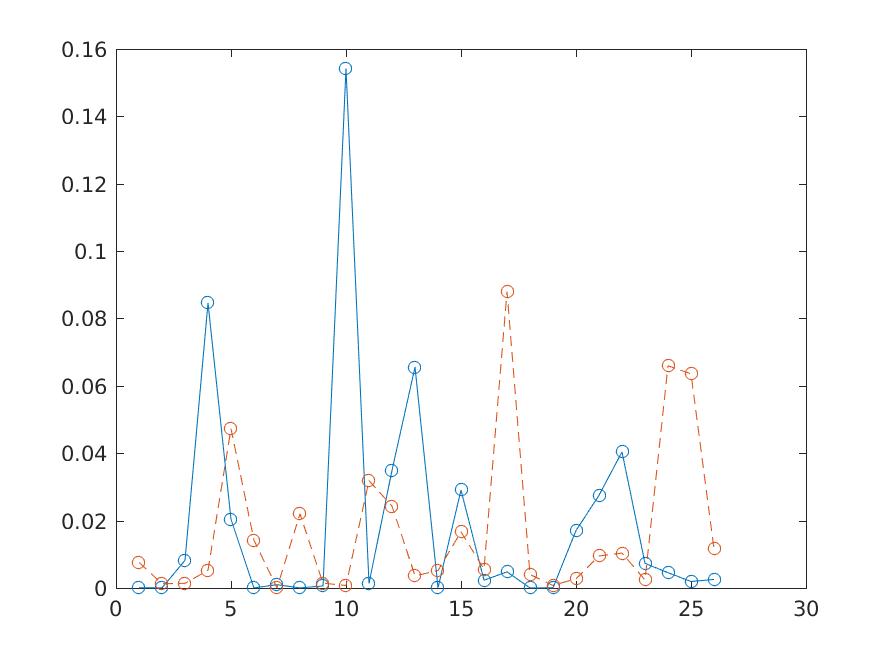

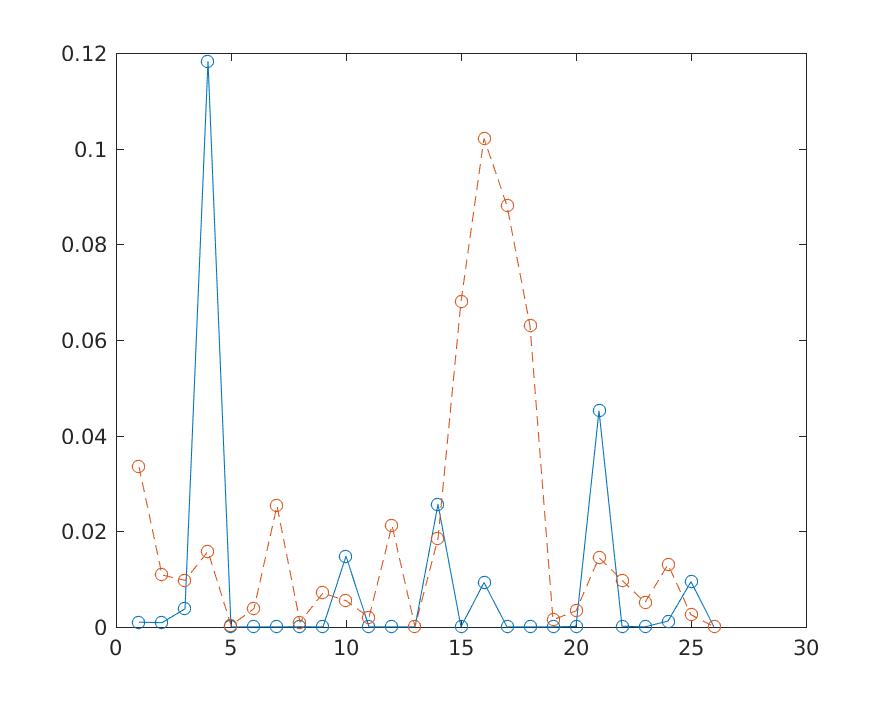

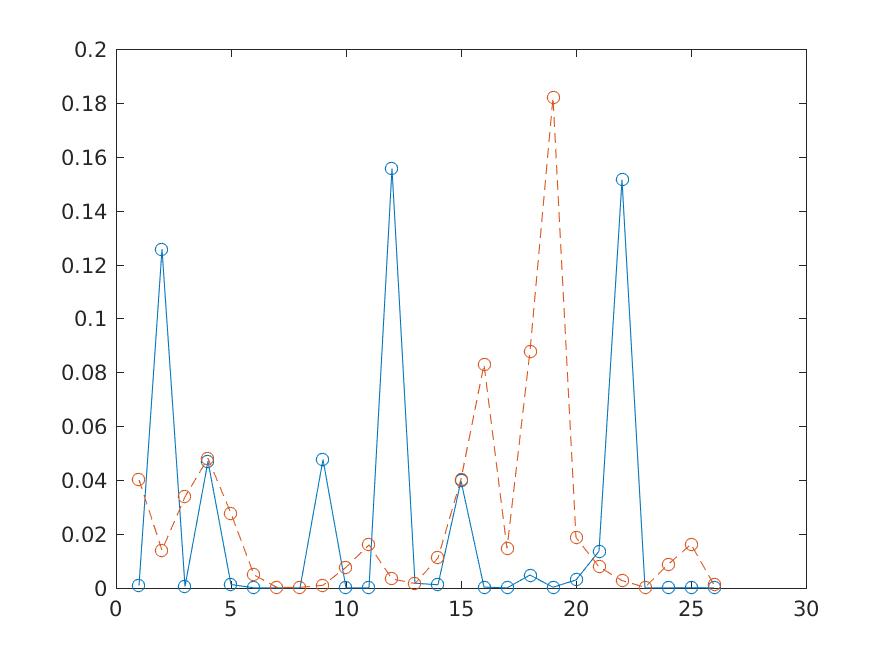

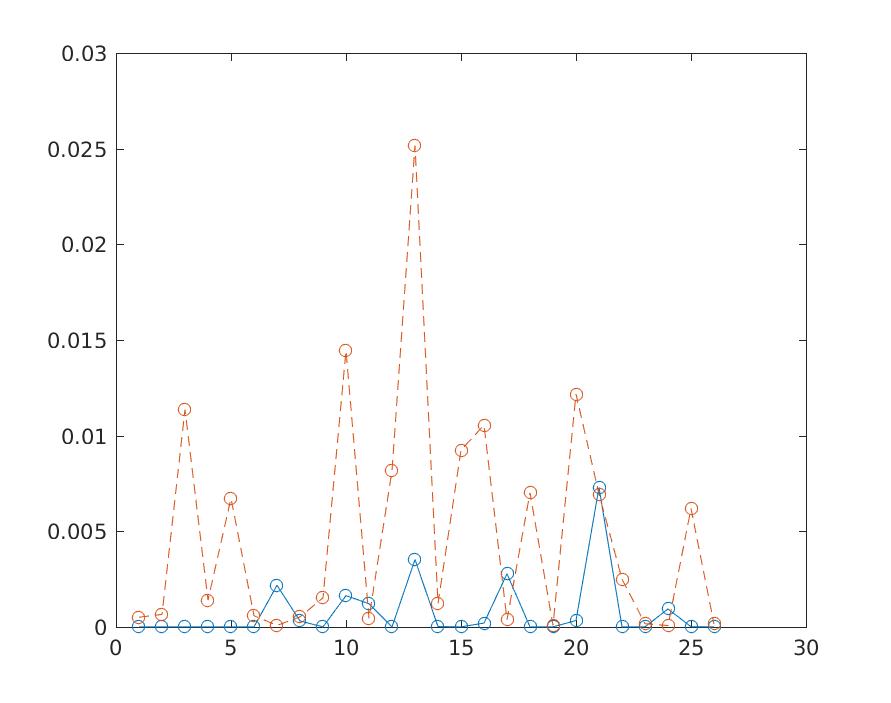

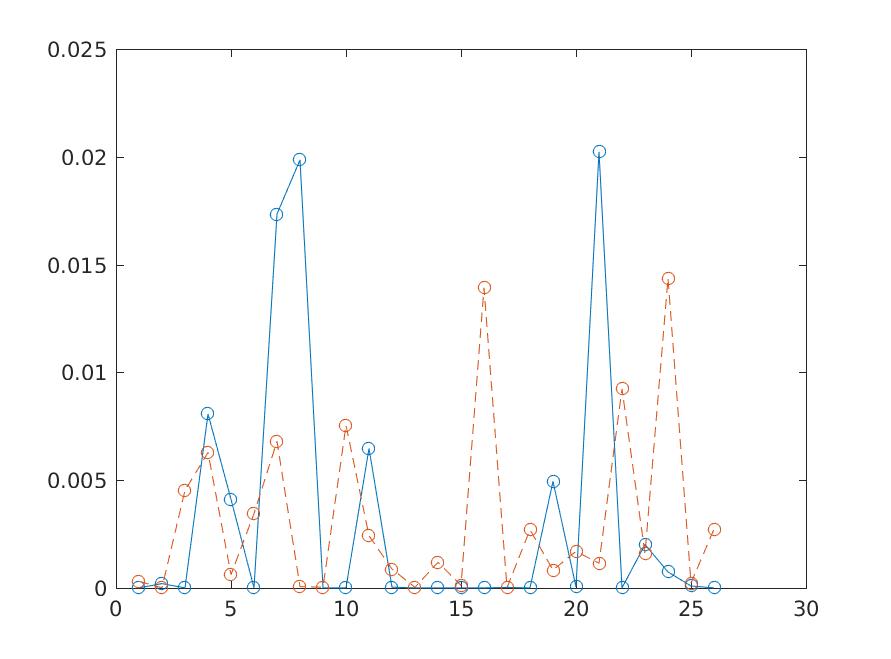

When we compare the outcomes from both sHDP and HDP, we found that the clusters for each year are similar for both models, but the value of successive symmetric KL divergence can be quite different. The mean of the successive symmetric KL of sHDP is mostly blow while the mean of HDP is around . The boxplot of the symmetric KL divergence is shown in Figure 4. Moreover, we track the components weights for the most significant clusters of through to in figure 5. In this figure, we can see that when the weights of are large (the first sub-figures in Figure 5), both HDP and sHDP show similar degree of fluctuation in its KL divergence. However, for less significant weight components of , (the last few figures), the smoothing effect of sHDP can be more obviously shown. This illustrates the fact that sHDP can suppress smaller components over times, and hence help achieve smoothness.

6 Conclusion and discussion

We proposed a smoothed Hierarchical Dirichlet Process (sHDP), in which we add a smoothness constraint to the lower layer of a Dirichlet Process (DP), in order to cater to many settings where temporal and/or spatial smoothness between the underlying measures is required. We used symmetric KL divergence for this constraint. Although it is conceptually sound, the traditional symmetric KL in its original form can not be practically applied since the symmetric KL divergence between two countable discrete measures is an infinite sum of real numbers. For this reason, in our paper, we proposed to use aggregated symmetric KL divergence as an alternative measure. We proved that this substitution has the same expectation of the original symmetric KL divergence, and hence can be used appropriately as an alternative bound.

We showed that given a measure at time , i.e., , a base measure and the concentration parameter , the sampling of the weight of , i.e., can be derived by using a truncated Beta distribution; We show that the truncation boundaries can be solved as roots of a convex function. This has made the solution space easily obtainable.

We show empirically the effect of the bound over the distribution in figure 2(b): we vary the bound value from to for which we show that the average symmetric KL divergence of the sampled successive distributions have also increased accordingly, which is in line with our expectation. The application of our model to the real dataset shows the smoothness effect of our model, which can be illustrated in both figure 4 and 5. The box plot in 4 show that KL divergence between successive measures, and of our model is much less than that of the HDP.

We also have analysed the results further to gain some insights into the component-wise smoothness: We choose the eight most significant components of the base measure , and then tracked how its weight changes from to (as we have 26 years of data). The results are shown in figure 5. It is interesting to note that we have a gradual increase in smoothness when its corresponding base measure component is decreased in value.

We also like to point out that our proposed method actually violates de Finetti’s theorem about the exchangeable random variables [1]. According to de Finetti’s theorem, the prior exists only if the random variables are infinitely exchangeable. However, our assumption on the dependence of successive distributions actually made the prior/base measure non-existent.

In the current form, the non traceability of the conditional require us to use particle filter as its inference method. Although it suffices in the settings of our testing dataset which is comprised of only 26 time intervals, it nonetheless can be a computation bottleneck when the application requires us to have much more granular time intervals. Therefore, in our future work, we will experiment with stochastic inference methods for time sequences, similar to that of [13].

References

- [1] David J. Ardus. Exchangeability and related topics. Springer Berlin Heidelberg, 1985.

- [2] Matthew J Beal, Zoubin Ghahramani, and Carl Edward Rasmussen. The Infinite Hidden Markov Model. In Advances in Neural Information Processing Systems 14, pages 577–584, 2001.

- [3] David M Blei, Andrew Y Ng, and Michael I Jordan. Latent Dirichlet Allocation. Journal of Machine Learning Research, 3(4-5):993–1022, 2012.

- [4] Paul Damien and Stephen G. Walker. Sampling truncated normal, beta, and gamma densities. Journal of Computational and Graphical Statistics, 10(2):206–215, 2001.

- [5] Arnaud Doucet and Am Johansen. A tutorial on particle filtering and smoothing: fifteen years later. Handbook of Nonlinear Filtering, 12:656–704, 2009.

- [6] Thomas S. Ferguson. A Bayesian Analysis of Some Nonparametric Problems. The Annals of Statistics, 1(2):209–230, 1973.

- [7] Emily B Fox. The sticky HDP-HMM: Bayesian nonparametric hidden Markov models with persistent states. arXiv preprint, page 60, 2007.

- [8] Matt Hoffman, D M Blei, C Wang, and J Paisley. Stochastic variational inference. The Journal of Machine Learning Research, 14(1):1303–1347, 2013.

- [9] Hemant Ishwaran and Lancelot F James. Gibbs Sampling Methods for Stick-Breaking Priors. Journal of the American Statistical Association, 96(453):161–173, 2001.

- [10] Frbmi Jordan. Learning spectral clustering. Advances in Neural Information Processing Systems 16 (NIPS), pages 305–312, 2004.

- [11] Achiim Klenke. Probability Theory: A Comprehensive Course. Springer, 2008.

- [12] Dahua Lin, Eric Grimson, and John Fisher. Construction of Dependent Dirichlet Processes based on Poisson Processes. In Advances in Neural Information Processing Systems 23 (Proceedings of NIPS), pages 1–9, 2010.

- [13] Johnson Matthew and Alan Willsky. Stochastic variational inference for Bayesian time siries models. In Proceedings of the 31st International Conference on Machine Learning (ICML-14), pages 1854–1862, 2014.

- [14] John Paisley and Lawrence Carin. Hidden markov models with stick-breaking priors. IEEE Transactions on Signal Processing, 57(10):3905–3917, 2009.

- [15] Max Planck and Ulrike Von Luxburg. A Tutorial on Spectral Clustering A Tutorial on Spectral Clustering. Statistics and Computing, 17:395–416, 2006.

- [16] Jayaram Sethuraman. A constructive definition of Dirichlet priors. Statistica Sinica, 4(2):639–650, 1994.

- [17] Yee Whye Teh, Michael I Jordan, Matthew J Beal, and David M Blei. Hierarchical Dirichlet Processes. Journal of the American Statistical Association, 101(476):1566–1581, 2006.

- [18] Yee Whye Teh, Kenichi Kurihara, and Max Welling. Collapsed Variational Inference for HDP. In Advances in neural information processing systems, 2007.

- [19] Chong Wang and David M Blei. Online Variational Inference for the Hierarchical Dirichlet Process. In International Conference on Artificial Intelligence and Statistics, volume 2, pages 752–760, 2011.

- [20] Mike West. Hyperparameter estimation in Dirichlet process mixture models. ISDS discussion paper series, pages #92–03, 1992.