Quantifying Distributional Model Risk via Optimal Transport

Abstract.

This paper deals with the problem of quantifying the impact of model

misspecification when computing general expected values of

interest. The methodology that we propose is applicable in great

generality, in particular, we provide examples involving

path-dependent expectations of stochastic processes. Our approach

consists in computing bounds for the expectation of interest

regardless of the probability measure used, as long as the measure

lies within a prescribed tolerance measured in terms of a flexible

class of distances from a suitable baseline model. These distances,

based on optimal transportation between probability measures,

include Wasserstein’s distances as particular cases. The proposed

methodology is well-suited for risk analysis, as we demonstrate with

a number of applications. We also discuss how to estimate the

tolerance region non-parametrically using Skorokhod-type embeddings

in some of these applications.

Keywords. Model risk, distributional robustness,

transport metric, Wasserstein distances, duality, Kullback-Liebler

divergences, ruin probabilities, diffusion approximations.

MSC 60G07, 60F99, and 62P05.

1. Introduction.

One of the most ubiquitous applications of probability is the evaluation of performance or risk by means of computations such as for a given probability measure , a function , and a random element . In classical applications, such as in finance, insurance, or queueing analysis, is a stochastic process and is a path dependent functional.

The work of the modeler is to choose a probability model which is both descriptive and, yet, tractable. However, a substantial challenge, which arises virtually always, is that the model used, , will in general be subject to misspecification; either because of lack of data or by the choice of specific parametric distributions.

The goal of this paper is to develop a framework to assess the impact of model misspecification when computing .

The importance of constructing systematic methods that provide performance estimates which are robust to model misspecification is emphasized in the academic response to the Basel Accord 3.5, Embrechts et al. (2014): In its broadest sense, robustness has to do with (in)sensitivity to underlying model deviations and/or data changes. Furthermore, here, a whole new field of research is opening up; at the moment, it is difficult to point to the right approach.

The results of this paper allow the modeler to provide a bound for the expectation of interest regardless of the probability measure used as long as such measure remains within a prescribed tolerance of a suitable baseline model.

The bounds that we obtain are applicable in great generality, allowing us to use our results in settings which include continuous-time stochastic processes and path dependent expectations in various domains of applications, including insurance and queueing.

Let us describe the approach that we consider more precisely. Our starting point is a technique that has been actively pursued in the literature (to be reviewed momentarily), which involves considering a family of plausible models , and computing distributionally robust bounds as the solution to the optimization problem

| (1) |

over all probability measures in . The motivation, as mentioned earlier, is to measure the highest possible risk regardless of the probability measure in used. A canonical object that appears naturally in specifying the family is the neighborhood where is a chosen baseline model and is a non-negative tolerance level. Here, is a metric that measures discrepancy between probability measures, and the tolerance interpolates between no ambiguity and high levels of model uncertainty ( large). The family of plausible models, , can then be specified as a single neighborhood (or) a collection of such plausible neighborhoods. In this paper, we choose in terms of a transport cost (defined precisely in Section 2), and analyze the solvability of (1) and discuss various implications.

Being a flexible class of distances that include the popular Wasserstein distances as a special case, transport costs allow easy interpretation in terms of minimum cost associated with transporting mass between probability measures, and have been widely used in probability theory and its applications (see, for example, Rachev and Rüschendorf (1998a, b); Villani (2008); Ambrosio and Caffarelli (2003) for a massive collection of classical applications and Barbour and Xia (2006); Gozlan and Leonard (2016); Nguyen (2013); Wang and Guibas (2012); Fournier and Guillin (2014); Canas and Rosasco (2012); Solomon et al. (2014); Frogner et al. (2015) for a sample of growing list of new applications).

Relative entropy (or) Kullback-Liebler (KL) divergence, despite not being a proper metric, has been the most popular choice for , thanks to the tractability of (1) when is chosen as relative entropy or other likelihood based discrepancy measures (see Breuer and Csiszár (2013); Lam (2013); Glasserman and Xu (2014); Atar et al. (2015) for the use in robust performance analysis, and Hansen and Sargent (2001); Iyengar (2005); Nilim and El Ghaoui (2005); Lim and Shanthikumar (2007); Jain et al. (2010); Ben-Tal et al. (2013); Wang et al. (2015); Jiang and Guan (2015); Hu and Hong (2012); Bayraksan and Love (2015) and references therein for applications to distributionally robust optimization). Our study in this paper is directly motivated to address the shortcoming that many of these earlier works acknowledge: the absolute continuity requirement of relative entropy; there can be two probability measures and that produce the same samples with high probability, despite having the relative entropy between and as infinite. Such absolute continuity requirements could be very limiting, particularly so when the models of interest are stochastic processes defined over time. For instance, Brownian motion, because of its tractability in computing path-dependent expectations, is used as approximation of piecewise linear or piecewise constant processes (such as random walk). However, the use of the relative entropy would not be appropriate to accommodate these settings because the likelihood ratio between Brownian motion and any piecewise differentiable process is not well defined.

Another instance which shows the limitations of the KL divergence arises when using an Itô diffusion as a baseline model. In such case, the region contains only Itô diffusions with the same volatility parameter as the underlying baseline model, thus failing to model volatility uncertainty.

The use of a distance based on an optimal transport cost (or) Wasserstein’s distance, as we do here, also allows to incorporate the use of tractable surrogate models such as Brownian motion. For instance, consider a classical insurance risk problem in which the modeler has sufficient information on claim sizes (for example, in car insurance) to build a non-parametric reserve model. But the modeler is interested in path-dependent calculations of the reserve process (such as ruin probabilities), so she might decide to use Brownian motion based approximation as a tractable surrogate model which allows to compute easily. A key feature of the Wasserstein’s distances, is that it is computed in terms of a so-called optimal coupling. So, the modeler can use any good coupling to provide a valid bound for the tolerance parameter .

The use of tractable surrogate models, such as Brownian motion, diffusions, and reflected Brownian motion, etc., has enabled the analysis of otherwise intractable complex stochastic systems. As we shall illustrate, the bounds that we obtain have the benefit of being computable directly in terms of the underlying tractable surrogate model. In addition, the calibration of the tolerance parameter takes advantage of well studied coupling techniques (such as Skorokhod embedding). So, we believe that the approach we propose naturally builds on the knowledge that has been developed by the applied probability community.

We summarize our main contributions in this paper below:

a) Assuming that takes values in a Polish space, and using a wide range of optimal transport costs (that include the popular Wasserstein’s distances as special cases) we arrive at a dual formulation for the optimization problem in (1), and prove strong duality – see Theorem 8.

b) Despite the infinite dimensional nature of the optimization problem in (1), we show that the dual problem admits a one dimensional reformulation which is easy to work with. We provide sufficient conditions for the existence of an optimizer that attains the supremum in (1) – see Section 5. Using the result in a), for upper semicontinuous , we show how to characterize an optimizer in terms of a coupling involving and the chosen transport cost – see Remark 2 and Section 2.4.

c) We apply our results to various problems such as robust evaluation of ruin probabilities using Brownian motion as a tractable surrogate (see Section 3), general multidimensional first-passage time probabilities (see Section 6.1), and optimal decision making in the presence of model ambiguity (see Section 6.2).

d) We discuss a non-parametric method, based on a Skorokhod-type embedding, which allows to choose (these are particularly useful in tractable surrogate settings discussed earlier). The specific discussion of the Skorokhod embedding for calibration is given in Appendix A. We also discuss how can be chosen in a model misspecification context, see the discussion at the end of Section 6.1.

In a recent paper, Esfahani and Kuhn (2015), the authors also consider distributionally robust optimization using a very specific Wasserstein’s distance. Similar formulations using Wasserstein distance based ambiguity sets have been considered in Pflug and Wozabal (2007); Wozabal (2012) and Zhao and Guan (2015) as well. The form of the optimization problem that we consider here is basically the same as that considered in Esfahani and Kuhn (2015), but there are important differences that are worth highlighting. In Esfahani and Kuhn (2015), the authors concentrate on the specific case of baseline measure being empirical distribution of samples obtained from a distribution supported in and the function possessing a special structure. In contrast, we allow the baseline measure to be supported on general Polish spaces and study a wide class of functions (upper semicontinuous and integrable with respect to ). The use of the Skorokhod embeddings that we consider here, for calibration of the feasible region, is also novel and not studied in the present literature.

Another recent paper, Gao and Kleywegt (2016), (which is an independent contribution made public a few days after we posted the first version of this paper in arXiv), presents a very similar version of the strong duality result shown in this paper. One difference that is immediately apparent is that the authors in Gao and Kleywegt (2016) concentrate on the case in which a specific cost function used to define transport cost is of the form for some and metric whereas we only impose that is lower semicontinuous. Allowing for general lower semicontinuous cost functions that are different from is useful, as demonstrated in applications towards distributionally robust optimization and machine learning in Blanchet et al. (2016). Another important difference is that, as far as we understand, the proof given in Gao and Kleywegt (2016) appears to implicitly assume that the space in which the random element of interest takes values is locally compact. For example, the proof of Lemma 2 in Gao and Kleywegt (2016) and other portions of the technical development appear to use repeatedly that a closed norm ball is compact. However, this does not hold in any infinite dimensional topological vector space111see, for example, Example 3.100 and Theorem 5.26 in Aliprantis and Border (1999), thus excluding important function spaces like and (denoting respectively the space of continuous and càdlàg functions on interval ), that are at the center of our applications. As mentioned earlier, our focus in this paper is on stochastic process applications, whereas the authors in Gao and Kleywegt (2016) put special emphasis on stochastic optimization in

The rest of the paper is organized as follows: In Section 2 we shall introduce the assumptions and discuss our main result, whose proof is given in Section 4. The proof is technical due to the level of generality that is considered. More precisely, it is the fact that the cost functions used to define optimal transport costs need not be continuous, and the random elements that we consider need not take values in a locally compact space (like ) which introduces technical complications, including issues like measurability of a key functional appearing in the dual formulation. In preparation to the proof, and to help the reader gain some intuition of the result, we present a one dimensional example first, in Section 3. Then, after providing the proof of our main result in Section 4 and conditions for existence of the worst-case probability distribution that attains the supremum in (1) in Section 5, we discuss additional examples in Section 6.

2. Our Main Result.

In order to state our main result, we need to introduce some notation and define the optimal transport cost between probability measures.

2.1. Notation and Definitions.

For a given Polish space we use to denote the associated Borel -algebra. Let us write and respectively, to denote the set of all probability measures and finite signed measures on . For any let denote the completion of with respect to the unique extension of to that is a probability measure is also denoted by and the measure in is to be interpreted as this extension defined on whenever is not measurable, but instead, is measurable. We shall use to denote the space of bounded continuous functions from to and to denote the support of a probability measure For any and denotes the collection of Borel measurable functions such that The universal algebra is defined by We use to denote the extended real line, and to denote the collection of measurable functions As for every any is also measurable when and are equipped, respectively, with the -algebras and Consequently, the integral is well-defined for any non-negative In addition, for any we say that is concentrated on a set if

Optimal transport cost.

For any two probability measures and in , let denote the set of all joint distributions with and as respective marginals. In other words, the set represents the set of all couplings (also called transport plans) between and Throughout the paper, we assume that

Assumption 1 (A1).

is a nonnegative lower semicontinuous function satisfying if and only if

Then the optimal transport cost associated with the cost function is defined as,

| (2) |

Intuitively, the quantity specifies the cost of transporting unit mass from in to another element of Given a lower semicontinuous cost function and a coupling the integral represents the expected cost associated with the coupling (or transport plan) For any non-negative lower semi-continuous cost function it is known that the ‘optimal transport plan’ that attains the infimum in the above definition exists (see Theorem 4.1 of Villani (2008)), and therefore, the optimal transport cost corresponds to the lowest transport cost that is attainable among all couplings between and

If the cost function is symmetric (that is, for all ), and it satisfies triangle inequality, one can show that the minimum transportation cost defines a metric on the space of probability measures. For example, if is a Polish space equipped with metric then taking the cost function to be renders the transport cost to be simply the Wasserstein distance of first order between and Unlike the Kullback-Liebler divergence (or) other likelihood based divergence measures, the Wasserstein distance is a proper metric on the space of probability measures. More importantly, Wasserstein distances do not restrict all the probability measures in the neighborhoods such as to share the same support as that of (see, for example, Chapter 6 in Villani (2008) for properties of Wasserstein distances).

2.2. Primal Problem.

Underlying our discussion we have a Polish space , which is the space where the random elements of the given probability model takes values. Given the objective, as mentioned in the Introduction, is to evaluate

for any function that satisfies the assumption that

Assumption 2 (A2).

is upper semicontinuous.

As the integral may equal for some satisfying only for the purposes of interpreting the supremum above, we let 222This is because, under the assumption that for every probability measure such that and one can identify a probability measure satisfying and see Corollary 3 in Appendix B for a simple construction of such a measure from measure Consequently, when computing the supremum of it is meaningful to restrict our attention to probability measures satisfying and interpret as The notation, simply facilitates this interpretation in this context. . The value of this optimization problem provides a bound to the expectation of regardless of the probability measure used, as long as the measure lies within distance (measured in terms of ) from the baseline probability measure In applied settings, is the probability measure chosen by the modeler as the baseline distribution, and the function corresponds to a risk functional (or) performance measure of interest, for example, expected losses, probability of ruin, etc.

As the infimum in the definition of the optimal transport cost is attained for any given non-negative lower semicontinuous cost function (see Theorem 4.1 of Villani (2008)), we rewrite the quantity of interest as below:

which, in turn, is an optimization problem with linear objective function and linear constraints. If we let

for brevity, then

| (3) |

is the quantity of interest.

2.2.1. The Dual Problem and Weak Duality.

Define to be the collection of all pairs such that is a non-negative real number, and

| (4) |

For every such consider

As is finite and whenever satisfies (4), the integral in the definition of avoids ambiguities such as for any Next, for any and see that

Consequently, we have

| (5) |

Following the tradition in optimization theory, we refer to the above infimum problem that solves for in (5) as the dual to the problem that solves for in (3), which we address as the primal problem. Our objective in the next section is to identify whether the primal and the dual problems have same value (that is, do we have that ?).

2.3. Main Result: Strong Duality Holds.

Recall that the feasible sets for the primal and dual problems, respectively, are:

| (6a) | ||||

| (6b) | ||||

| The corresponding primal and dual problems are | ||||

| For brevity, we have identified the primal and dual objective functions as and respectively. As the identified primal and dual problems are infinite dimensional, it is not immediate whether they have same value (that is, is ?). The objective of the following theorem is to verify that, for a broad class of performance measures indeed equals | |||

Theorem 1.

Under the Assumptions (A1) and (A2),

(a) . In other

words,

(b) For any define as follows:

There exists a dual optimizer of the form for some In addition, any feasible and are primal and dual optimizers, satisfying , if and only if

| (8a) | |||

| (8b) | |||

As the measurability of the function is not immediate, we establish that in Section 4, where the proof of Theorem 8 is also presented. Sufficient conditions for the existence of a primal optimizer satisfying are presented in Section 5. For now, we are content discussing the insights that can be obtained from Theorem 8.

Remark 1 (on the value of the dual problem).

First, we point out the following useful characterization of the optimal value, as a consequence of Theorem 8:

| (9) |

where the right hand side333As there is no ambiguity, such as the form in the definition of integral is simply a univariate reformulation of the dual problem. This characterization of follows from the strong duality in Theorem 8 and the observation that for every The significance of this observation lies in the fact that the only probability measure involved in the right-hand side of (9) is the baseline measure which is completely characterized, and is usually chosen in a way that it is easy to work with (or) draw samples from. In effect, the result indicates that the infinite dimensional optimization problem in (3) is easily solved by working on the univariate reformulation in the right hand side of (9).

Remark 2 (on the structure of primal optimal transport plan444In the literature of optimal transportation of probability measures, it is common to refer joint probability measures alternatively as transport plans, and the integral as the cost of transport plan We follow this convention to allow easy interpretations.).

It is evident from the characterisation of an optimal measure

in Theorem 8(b) that if

exists, it is concentrated on

Thus, a worst-case

joint probability measure gets identified with a

transport plan that transports mass from to the optimizer(s) of

the local optimization problem

According to

the complementary slackness conditions (8a) and

(8b), such a transport plan satisfies one

of the following two cases:

Case 1: the transport plan

necessarily costs

Case 2: the transport plan

satisfies (follows from primal

feasibility of ) and equals the constant

almost surely (follows from

(8a) assuming that

exists). Recall from (9) that

which is in agreement with the

structure described for the primal optimizer here when

The interpretation is that the budget for

quantifying ambiguity, is sufficiently large to move all

the probability mass to thus making

as large as possible.

Remark 3 (On the uniqueness of a primal optimal transport plan).

Suppose that there exists a primal optimizer and a dual optimizer satisfying In addition, suppose that for almost every there is a unique that attains the supremum in Then the primal optimizer is unique because of the following reasoning: For every if we let denote the unique maximizer, then it follows from Proposition 7.50(b) of Bertsekas and Shreve (1978) that the map is measurable. If is a pair jointly distributed according to , then due to complementarity slackness condition (8a), we must have that almost surely. As any primal optimizer must necessarily assign entire probability mass to the set (due to complementarity slackness condition (8a)), the primal optimizer is unique.

Remark 4 (on optimal transport plans).

Given and a dual optimal pair any is primal optimal if and only if

| (10) |

where both the summands in the above expression are necessarily nonnegative. This follows trivially by substituting the following expressions for and in

As both the summands in (10) are nonnegative, for any such that we have,

| (11) |

where for any

Remark 5.

If (for example, if grows to at a rate faster than the rate at which the transport cost function grows) for every in a set such that then This is because, for every and and consequently, for very therefore as a consequence of Theorem 8. Requiring the objective to not grow faster than the transport cost may be useful from a modeling viewpoint as it offers guidance in understanding choices of transport cost functions that necessarily yield as the robust estimate .

We next discuss an important special case of Theorem 8, namely, computing worst case probabilities. The applications of this special case, in the context of ruin probabilities, is presented in Section 3 and Section 6.1. Other applications of Theorem 8, broadly in the context of distributionally robust optimization, are available in Esfahani and Kuhn (2015); Zhao and Guan (2015), Gao and Kleywegt (2016) and Blanchet et al. (2016), and as well in Example 4 in Section 6.2 of this paper.

2.4. Application of Theorem 8 for computing worst-case probabilities.

Suppose that we are interested in computing,

| (12) |

where is a nonempty closed subset of the Polish space Since is closed, the indicator function is upper semicontinuous and therefore we can apply Theorem 8 to address (12). In order to apply Theorem 8, we first observe that

where is the lowest cost possible in transporting unit mass from to some in the set and denotes the positive part of the real number Consequently, Theorem 8 guarantees that the quantity of interest, , in (12), can be computed by simply solving,

| (13) |

If the infimum in the above expression for is attained at then merely by substituting in , we obtain In addition, due to complementary slackness conditions (8a) and (8b), we have and for any optimal transport plan satisfying Here, as we have

Next, as we turn our attention towards the structure of an optimal transport plan when let us assume, for ease of discussion, that for every Unless indicated otherwise, let us assume that in the rest of this discussion. For every and observe that

Then, Part (b) of Theorem 8 allows us to conclude that, an optimal transport plan satisfying if it exists, is concentrated on

Next, let denote the set of probability measures with as marginal for the first component, and satisfying In other words,

Recall that for any and for any Therefore, for a pair distributed jointly according to some it follows from the definition of the collection that

almost surely. Then, as is non-negative, satisfies,

Since the marginal distribution of is (refer the definiton of above), it follows that satisfies where

| (14) |

Further, as any optimal measure satisfying is a member of it follows from the complementary slackness condition (8b) that has to equal whenever and consequently, whenever a primal optimizer satisfying exists. The observation that holds regardless of whether a primal optimizer exists or not, and this is the content of Lemma 2 below, whose proof is provided towards the end of this section in Subsection 2.4.1.

Lemma 2.

If and any coupling in is primal optimal (because it satisfies the complementary slackness conditions (8a) and (8b) in addition to the primal feasibility condition that ). In particular, one can describe a convenient optimal coupling satisfying as follows: First, sample with distribution and let be any universally measurable map such that -almost surely. We then write,

to obtain distributed according to Such a universally measurable map always exists, assuming that is lower semicontinuous and that is not empty555The assumption that holds, for example, when is compact and nonempty (as is lower semi-continuous), or when has compact sub-level sets for each (recall that is a closed set in the discussion) for -almost every (see, for example, Proposition 7.50(b) of Bertsekas and Shreve (1978)). In this case,

The second equality follows from the observation that for the described coupling distributed according to we have, if and only if almost surely.

The reformulation that is extremely useful, as it re-expresses the worst-case probability of interest in terms of the probability of a suitably inflated neighborhood, evaluated under the reference measure which is often tractable (see Section 3 and 6.1 for some applications). However, as the reasoning that led to this reformulation relies on the existence of a primal optimal transport plan, we use optimal transport plans in Theorem 15 below to arrive at the same conclusion. The proof of Theorem 15 is presented towards the end of this section in Subsection 2.4.1.

Theorem 3.

Recall from Lemma 2 that if it is strictly positive, is such that To arrive at the characterization (15), we had assumed that the integral

| (16) |

is continuous at and consequently However, if this is not the case, for example, because is atomic, then In this scenario, one can identify an optimal coupling by randomizing between the extreme cases and Remark 6 below provides a characterization of the primal optimizer when

Remark 6.

Suppose that is such that and that all the assumptions in Theorem 15, except the condition that are satisfied. Let be an independent Bernoulli random variable with success probability, As before, sample with distribution and let be any universally measurable map such that -almost surely. Then,

is such that (thus satisfying complementary slackness condition (8a)), and

This verifies the complementary condition (8b) as well, and hence the marginal distribution of in the coupling attains the supremum in

All the examples considered in this paper have the function as continuous, and hence we have the characterization (15) which offers an useful reformulation for computing worst-case probabilities. For instance, let us take the cost function as a distance metric (as in Wasserstein distances), and let the baseline measure and the set be such that defined in (16), is continuous. Then (15) provides an interpretation that the worst-case probability in the neighborhood of is just the same as where denotes the -neighborhood of the set Thus, the problem of finding a probability measure with worst-case probability in the neighborhood of measure amounts to simply searching for a suitably inflated neighborhood of the set itself. For example, if then

for any where is the solution to the univariate optimization problem in (13). Alternatively, due to Lemma 2, one can characterize as where is the monotonically increasing right-continuous function (with left limits) defined in (16). If does not admit a closed-form expression, one approach is to obtain samples of under the reference measure and either solve the sampled version of (13), or compute a Monte Carlo approximation of the integral to identify the level as

2.4.1. Proofs of Lemma 2 and Theorem 15.

We conclude this section with proofs for Lemma 2 and Theorem 15. Given and define where

In addition, define

and The above definitions yield, and when

Lemma 4.

Suppose that Assumption (A1) is in force, and is a nonempty closed subset of the Polish space In addition, suppose that attains the infimum in (13). Then, there exists a collection of probability measures such that and

Proof.

Proof of Lemma 4. Since we consider a collection such that For every if we let

as a consequence of Markov’s inequality and the characterization (11) in Remark 4, we obtain,

For every given a pair jointly distributed with law we define a new jointly distributed pair defined as follows,

Our objective now is to show that the collection where satisfies the desired properties. We begin by verifying that here: As and it is immediate that In addition, as because it follows from the non-negativity of and that Next, as for every we have that and Finally, for every is also immediate once we observe that

thus verifying all the desired poperties of the collection ∎

Proof.

Proof of Lemma 2. Consider a collection such that and Such a collection exists because of Lemma 4. We first observe that because Next, recalling the definitions of subsets introduced before stating Lemma 4, we use to observe that,

Case 1: Let us first restrict ourself to the case where Then can be bounded from above and below as follows:

Next, as and we use the second part of (11) to reason that

| (17) | ||||

| (18) |

for every The next few steps are dedicated towards re-expressing the integrals in the left hand side of (17) and right hand side of (18) in terms of and to obtain,

| (19) |

As every satisfies we have

thus establishing the first inequality in (19) as a consequence of bounded convergence theorem. Next, as is contained in the union of and we obtain,

thus verifying the second inequality in (19). Now that we have verified both the inequalities in (19), the conclusion that is automatic if we send in (17), (18) and use (19).

Case 2: When It follows from the definitions of sets and that and when Recall that and are such that Let and As and for any we have Next, as we have

| (20) |

as a consequence of monotone convergence theorem. Further, as for every it follows from (20) that This concludes the proof. ∎

Proof.

Proof of Theorem 15. Consider a collection such that and Such a collection exists because of Lemma 4. Similar to the proof of Lemma 2, we recall the definitions of subsets introduced before stating Lemma 4, to observe that and consequently,

As a result, Combining this with the observation that we obtain,

| (21) |

for every Similar to the proof of Lemma 2, the rest of the proof is dedicated towards proving

| (22) |

when The first inequality is immediate when we observe that every is such that and therefore,

which equals due to bounded convergence theorem. This verifies the first inequality in (21). Next, as the probability equals,

Since and we obtain that

Further, as we have and therefore, thus verifying the inequality in the right hand side of (22). Now that both the inequalities in (22) are verified, we combine (21) with (22) to obtain that ∎

3. Computing ruin probabilities: A first example.

In this section, we consider an example with the objective of computing a worst-case estimate of ruin probabilities in a ruin model whose underlying probability measure is not completely specified. As mentioned in the Introduction, such a scenario can arise for various reasons, including the lack of data necessary to pin down a satisfactory model. A useful example to keep in mind would be the problem of pricing an exotic insurance contract (for example, a contract covering extreme climate events) in a way the probability of ruin is kept below a tolerance level.

Example 1.

In this example, we consider the celebrated Cramer-Lundberg model, where a compound Poisson process is used to calculate ruin probabilities of an insurance risk/reserve process. The model is specified by 4 primitives: initial reserve safety loading the rate at which claims arrive, and the distribution of claim sizes with first and second moments and respectively. Then the stochastic process

specifies a model for the reserve available at time Here, denotes the size of the -th claim, and the collection is assumed to be independent samples from the distribution Further, is the rate at which a premium is received, and is taken to be a Poisson process with rate Then one of the important problems in risk theory is to calculate the probability

that the insurance firm runs into bankruptcy before a specified duration

Despite the simplicity of the model, existing results in the literature do not admit simple methods for the computation of (see Asmussen and Albrecher (2010), Embrechts et al. (1997), Rolski et al. (1999) and references therein for a comprehensive collection of results). In addition, if the historical data is not adequately available to choose an appropriate distribution for claim sizes, as is typically the case in an exotic insurance situation, it is not uncommon to use a diffusion approximation

that depends only on first and second moments of the claim size distribution Here, the stochastic process denotes the standard Brownian motion, and

is to serve as a diffusion approximation based substitute for ruin probabilities See the seminal works of Iglehart and Harrison (Iglehart (1969); Harrison (1977)) for a justification and some early applications of diffusion approximations in computing insurance ruin. Such diffusion approximations have enabled approximate computations of various path-dependent quantities, which may be otherwise intractable. However, as it is difficult to verify the accuracy of the Brownian approximation of ruin probabilities, in this example, we use the framework developed in Section 2 to compute worst-case estimates of ruin probabilities over all probability measures in a neighborhood around the baseline Brownian motion driving the ruin model

For this purpose, we identify the Polish space where the stochastic processes of our interest live as the Skorokhod space equipped with the topology. In other words, is simply the space of real-valued right-continuous functions with left limits (rcll) defined on the interval equipped with the -metric Please refer Lemma 11 in Appendix B for an expression of and Chapter 3 of Whitt (2002) for an excellent exposition on the space . Next, we take the transportation cost (corresponding to -th order Wasserstein distance) as

for some and the baseline measure as the probability measure induced in the path space by the Brownian motion In addition, if we let

then the following observations are in order: First, the Brownian approximation for ruin probability equals Next, the set is closed (verified in Lemma 10 in Appendix B), and hence the function is upper semicontinuous. Further, it is verified in Lemma 11 in Appendix B that

| (23) |

As is continuous, for any given it follows from Theorem 15 that

| (24) |

where, the level is identified as As admits a simple form as in (23), following (24), the problem of computing becomes as elementary as

| (25) |

with Thus, the computation of worst-case ruin probability remains the problem of evaluating the probability that a Brownian motion with negative drift crosses a positive level, smaller than the original level In other words, the presence of model ambiguity has manifested itself only in reducing the initial capital to a new level Apart from the tractability, such interpretations of the worst-case ruin probabilities in terms of level crossing a modified ruin set is an attractive feature of using Wasserstein distances to model distributional ambiguities.

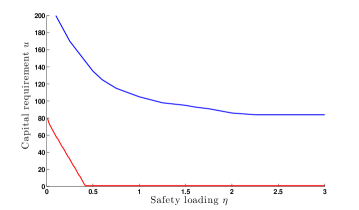

Numerical illustration: To make the discussion concrete, we consider a numerical example where and the safety loading The claim sizes are taken from a distribution that is not known to the entire estimation procedure. Our objective is to compute the Brownian approximation to the ruin probability and its worst-case upper bound The estimation methodology is data-driven in the following sense: we derive the estimates of moments and from the observed realizations of claim sizes. While obtaining estimates for moments and are straightforward, to compute we use the claim size samples to embed realizations of compound Poisson risk process in a Brownian motion, as in Khoshnevisan (1993). Specific details of the algorithm that estimates can be found in Appendix A. The estimate of obtained is such that the compensated compound Poisson process of interest that models risk in our setup lies within the -neighborhood with high probability. Next, given the knowledge of Lagrange multiplier the evaluation of and (with are straightforward, because of the closed-form expressions for level crossing probabilities of Brownian motion. Computation of is also elementary, and can be accomplished in multiple ways. We resort to an elementary sample average approximation scheme that solves for The estimates of Brownian approximation to ruin probability and the worst-case ruin probability for various values of are plotted in Table 1. To facilitate comparison, we have used a large deviation approximation of the ruin probabilities that satisfy as as a common denominator to compare magnitudes of the Brownian estimate and the worst-case bound In particular, we have drawn samples of claim sizes from the Pareto distribution While the Brownian approximation remarkably underestimates the ruin probability , the worst-case upper bound appears to yield estimates that are conservative, yet of the correct order of magnitude.

For further discussion on this toy example, let us say that an insurer paying for the claims distributed according to has a modest objective of keeping the probability of ruin before time at a level below 0.01. The various combinations of initial capital and safety loading factors that achieve this objective are shown in Figure 1. While the combinations that work for the Brownian approximation model is drawn in red, the corresponding combinations that keep is shown in blue.

A discussion on regulatory capital requirement. For the safety loading we have considered, the Brownian approximation model requires that the initial capital be at least to achieve . On the other hand, to keep the robust ruin probability estimates below it is required that roughly 3 times more than the capital requirement of the Brownian model. From the insurer’s point of view, due to the model uncertainty the contract is faced with, it is not uncommon to increase the premium income (or) initial capital by a factor of 3 or 4 (referred as “hysteria factor”, see Embrechts et al. (1998), Lewis (2007)). This increase in premium can be thought of as a guess for the price for statistical uncertainty. Choosing higher premium and capital (larger and ), along the blue curve in Figure 1, as dictated by the robust estimates of ruin probabilities instead provides a mathematically sound way of doing the same. Unlike the Brownian approximation model, the blue curve demonstrates that one cannot decrease the probability of ruin by arbitrarily increasing the premium alone, the initial capital also has to be sufficiently large. This prescription is consistent with the behaviour of markets with heavy-tailed claims where, in the absence of initial capital, a few initial large claims that occur before enough premium income gets accrued are enough to cause ruin. The minimum capital requirement prescribed according to the worst-case estimates can be thought of as the regulatory minimum capital requirement.

Remark 7.

Defining the candidate set of ambiguous probability measures via KL-divergence (or) other likelihood based divergence has been the most common approach while studying distributional robustness (see, for example, Hansen and Sargent (2001); Ben-Tal et al. (2013); Breuer and Csiszár (2013)). This would not have been useful in this setup, as the compensated Poisson process that models risk is not absolutely continuous with respect to Brownian motion. In general, it is normal to run into absolute continuity issues when we deal with continuous time stochastic processes. In such instances, as demonstrated in Example 1, modeling via optimal transport costs (or) Wasserstein distances not only offers a tractable alternative, but also yields insightful equivalent reformulations.

4. Proof of the duality theorem.

4.1. Duality in compact spaces.

We prove Theorem 8 by first proving the following progressively strong duality results in Polish spaces that are compact. Proofs of all the technicalities that are not central to the argument are relegated to Appendix B.

Proposition 5.

Suppose that is a compact Polish space, and satisfies Assumption (A2). In addition to satisfying Assumption (A1), suppose that is continuous. Then and a primal optimizer satisfying exists.

Proposition 6.

Suppose that is a compact Polish space, satisfies Assumption (A2), and satisfies Assumption (A1). Then and a primal optimizer satisfying exists.

As in the proof of the standard Kantorovich duality in compact spaces in Villani (2003), we use Fenchel duality theorem (see Theorem 1 in Chapter 7, Luenberger (1997)) to prove Proposition 5. However, the similarity stops there, owing to the reason that the set of primal feasible measures is not tight when is non-compact (contrast this with Kantorovich duality, where the collection of feasible measures the set of all joint distributions between any two probability measures and is tight).

Proof of Proposition 5.

As a preparation for applying Fenchel duality theorem, we first let and identify as its topological dual. Here, the spaces and representing the vector space of bounded continuous functions and finite Borel measures on respectively, are equipped with the supremum and total variation norms. The fact that is the dual space of is a consequence of Riesz representation theorem (see, for example, Rudin (1986)). Next, let be the collection of all functions in that are of the form

for some and In addition, let denote the collection of all functions in that satisfy for every Every in the convex subset is defined by the pair which, in turn, can be uniquely identified by,

for some in such that Keeping this invertible relationship in mind, define the functionals and as below:

Evidently, the functional is convex, is concave, and we are interested in

| (26) |

The next task is to identify the conjugate functionals and their respective domains as below:

The conjugate functionals and are defined accordingly as,

First, to determine we see that for every

Therefore,

Next, to identify we show in Lemma 15 in Appendix B that if a measure is not non-negative. On the other hand, if is non-negative, then

This is because, being an upper semicontinuous function that is bounded from above, it can be approximated pointwise by a monotonically decreasing sequence of continuous functions666Let be an upper semicontinuous function, that is bounded from above, defined on a Polish space If is a function that metrizes the Polish space then, for instance, the choice is continuous, and satisfies pointwise. Then the above equality follows as a consequence of monotone convergence theorem. As a result,

Then, on As is defined to equal it follows that

| (27) |

As the set contains points in the relative interiors of and (consider, for example, the candidate where because is upper semicontinuous and is compact) and the epigraph of the function has non-empty interior, it follows as a consequence of Fenchel’s duality theorem (see, for example, Theorem 1 in Chapter 7, Luenberger (1997)) that

where the supremum in the right is achieved by some In other words (see (26) and (27)),

As it follows from the definition of that

However, due to weak duality (5), we have Therefore,

Proof of Proposition 6.

First, observe that is a nonnegative lower semicontinuous function defined on the Polish space Therefore, we can write where is a nondecreasing sequence of continuous cost functions 777For instance, one can choose where the function metrizes the Polish space Then is continuous, and satisfies if and only if With as cost function, define the corresponding primal and dual problems,

Here, the feasible sets and are obtained by suitably modifying the cost function in sets and (defined in (6a) and (6b)) as below:

As the cost functions are continuous, due to Proposition 5, there exists a sequence of measures such that

| (28) |

As is compact, the set is automatically tight, and due to Prokhorov’s theorem, there exists a subsequence weakly converging to some First, we check that is feasible:

where the second and third equalities, respectively, are consequences of monotone convergence and weak convergence. In addition, since is a nondecreasing sequence of functions,

Therefore, Again as a simple consequence of weak convergence, we have for every Therefore, and is indeed feasible. Next, as is upper semicontinuous and is compact, is bounded from above. Then, due to the weak convergence , the objective function satisfies

because as in (28). Further, as it follows that is a subset of and hence for all As a result, we obtain,

Since never exceeds (see (5)), it follows that

4.2. A note on additional notations and measurability.

Given that we have established duality in compact spaces, the next step is to establish the same when is not compact. For this purpose, we need the following additional notation. For any probability measure let

where and denote the respective supports of marginals and As every probability measure defined on a Polish space has -compact support, the set which is a subset of is -compact. As we shall see in the proof of Proposition 7, can be written as the union of an increasing sequence of compact subsets It will then be easy to make progress towards strong duality in noncompact sets such as by utilizing the strong duality results derived in Section 4.1 (which are applicable for compact sets ) via a sequential argument; this is accomplished in Section 4.3 after introducing additional notation as follows. For any closed let

| (29) |

where is used to denote the collection of measurable functions with denoting the universal algebra of the Polish space With this notation, the dual feasible set is nothing but The next issue we address is the measurability of functions of the form For any

which is analytic, because projections of any Borel measurable set are analytic (see, for example, Proposition 7.39 in Bertsekas and Shreve (1978)). As analytic subsets of lie in (see Corollary 7.42.1 in Bertsekas and Shreve (1978)), the function is measurable (that is, universally measurable; refer Chapter 7 of Bertsekas and Shreve (1978) for an introduction to universal measurability and analytic sets).

4.3. Extension of duality to non-compact spaces.

Proposition 7, presented below in this section, is an important step towards extending the strong duality results proved in Section 4.1 to non-compact sets.

Proposition 7.

Suppose that Assumptions (A1) and (A2) are in force. Let be a probability measure satisfying

(a)

(b) and

(c) for every Then

Proof of Proposition 7.

As any Borel probability measure on a Polish space is concentrated on a -compact set (see Theorem 1.3 of Billingsley (1999)), the sets and are -compact, and therefore is -compact as well. Then, by the definition of -compactness, the set can be written as the union of an increasing sequence of compact subsets of If we let to be the union of the projections of over its two coordinates, then it follows that is an increasing sequence of subsets of satisfying As and are finite, one can pick the increasing sequence with to be satisfying,

| (30a) | ||||

| (30b) | ||||

| (30c) | ||||

where and is introduced while defining the primal feasibility set (recall that ) and the dual objective in Section 2.2. Having chosen the compact subsets define a joint probability measure and its corresponding marginal as below:

for every Additionally, let For every these new definitions can be used to define “restricted” primal and dual optimization problems and supported on the compact set

| (31) | ||||

| (32) |

To comprehend (32), refer the definition of in (29). As is compact, due to the duality result in Proposition 6, we know that there exists a that is feasible for optimization of and satisfies

| (33) |

Using this optimal measure one can, in turn, construct a measure by stitching it together with the residual portion of as below:

Having tailored a candidate measure next we check its feasibility that as follows: Since for some it is easy to check, as below, that has as its marginal for the first component: first, it follows from the definition of that

As it follows that and consequently,

Therefore, for some Further, as is a feasible solution for the optimization problem in (31),

which does not exceed To see this, refer (30b) and recall that Therefore, the stitched measure is primal feasible, that is Consequently,

As is chosen to satisfy (30c), we have Therefore, it is immediate from (33) that

| (34) |

which, if is a useful upper bound for all of See that the statement of Proposition 7 already holds when equals Therefore, let us take to be finite. Next, given and take an -optimal solution for that is, and

For any pair that belongs to we have from the definition of that is larger than for every

for every As combining the above expression with (34) results in

| (35) |

Since the integrand admits as a lower bound on further, as serves as a common integrable lower bound for all This has two consequences: First, because of the finite upper bound in (35), and are finite (recall that as well), and there exists a subsequence such that as for some The second consequence of the existence of a common integrable lower bound is that we can apply Fatou’s lemma in (35) along the subsequence to obtain

Here, we have used that as and the fact that is supported on a subset of The fact that is at least for every is carefully checked in Lemma 16, Appendix B. If we let then and as is arbitrary, it follows from the above inequality that This completes the proof.

Proof of Theorem 8(a).

If then as never exceeds equals as well, and there is nothing to prove. Next, consider the case where is finite: that is, Let denote the convex set of probability measures that satisfy conditions (a)-(c) of Proposition 7. Then, due to Proposition 7, for every

For any and define

As it is easy to see that Since for every one can rather restrict attention to the compact subset as follows:

| (36) |

Being a pointwise supremum of a family of affine functions, is a lower semicontinuous with respect to the variable Further, recall that Thus, for any due to Fatou’s lemma,

which means that is lower semicontinuous in Along with this lower semicontinuity, for every fixed is also convex in In addition, for any and

Therefore, is a concave function in for every fixed One can apply a standard minimax theorem (see, for example, Sion (1958)) to conclude

This observation, in conjunction with (36), yields

Lemma 8 below is the last piece of technicality that completes the proof of Part (a) of Theorem 8.

Lemma 8.

Suppose that Assumptions (A1) and (A2) are in force. Then, for any

Proof.

Proof of Lemma 8. For brevity, let and For any and define the sets,

Here, recall that for any The sequence also admits the following equivalent backward recursive definition,

that renders the collection disjoint. As the function is upper semicontinuous, it is immediate that the sets are Borel measurable and their corresponding projections are analytic subsets of Then, due to Jankov-von Neumann selection theorem888See, for example, Chapter 7 of Bertsekas and Shreve (1978) for an introduction to analytic subsets and Jankov-von Neumann measurable selection theorem, there exists, for each such that , an universally measurable function such that or, in other words,

| (37) |

Next, let us define the function as below:

This definition is possible because and the collection is disjoint. As each is universally measurable, the composite function is universally measurable as well, and satisfies that

for each Both sides of the inequality above can be inferred from (37) after recalling that Letting we see that

| (38) |

Next, define the family of probability measures as below:

with representing the dirac measure centred at As almost surely, we have that the functions and are integrable with respect to This means that (here, recall that is the set of probability measures satisfying conditions (a)-(c) in the statement of Proposition 7). Further, as

which is integrable with respect to the measure Therefore, due to Fatou’s lemma,

where the last inequality follows from (38). Since is a member of set for every it is then immediate that

As for every the inequality in the reverse direction is trivially true. This completes the proof of Lemma 8. ∎

Proof of Theorem 8(b).

To summarize, in the proof of Part (a) of Theorem 8, we established that

where is lower-semicontinuous in and is bounded by from below. Recall that is finite. If we let

then due to a routine application of Fatou’s lemma, we have that whenever In other words, is lower semicontinuous. In addition, as we have that if This means that the level sets are compact for every and therefore, attains its infimum. In other words, there exists a such that

Thus, we conclude that a dual optimizer of the form always exists. Next, if the primal optimizer satisfying also exist, then

which gives us complementary slackness conditions (8a) and (8b), as a consequence of equality getting enforced in the following series of inequalities:

Alternatively, if the complementary slackness conditions (8a) and (8b) are satisfied by any and then automatically,

thus proving that and are, respectively, the primal and dual optimizers. This completes the proof of Theorem 8.

5. On the existence of a primal optimal transport plan.

Unlike the well-known Kantorovich duality where an optimizer that attains the infimum in (2) exists if the transport cost function is nonnegative and lower semicontinuous (see, for example, Theorem 4.1 in Villani (2008)), a primal optimizer satisfying need not exist for the primal problem, that we have considered in this paper. The feasible set for the problem (2) in Kantorovich duality, which is the set of all joint distributions with given and as marginal distributions, is compact in the weak topology. On the other hand, the primal feasibility set for a given and that we consider in this paper is not necessarily compact, and the existence of a primal optimizer satisfying is not guaranteed. Example 2 below demonstrates a setting where there is no primal optimizer satisfying even if the transport cost is chosen as a metric defined on the Polish space

Example 2.

Consider Let the dirac measure at be the reference measure defined on Let and for all The primal problem of interest is where for the choice We first argue that here: As for every we have For recall the definition As Assumptions (A1) and (A2) hold, an application of Theorem 8(a) results in,

Since we had already verified that the above lower bound results in with the infimum being attained at However, as for every it is immediate that is necessarily smaller than 1 for all Therefore, there does not exist a primal optimizer such that A careful examination of Part (b) of Theorem 8 also results in the same conclusion: A primal optimizer, if it exists, is concentrated on which is empty in this example, because for every

Recall from Proposition 6 that a primal optimizer always exists whenever the underlying Polish space is compact. In the absence of compactness of Proposition 9 below presents additional topological properties (P-Compactness) and (P-USC) under which a primal optimizer exists. Corollary 1, that follows Proposition 9, discusses a simple set of sufficient conditions for which these properties listed in Proposition 9 are easily verified.

Additional notation.

Define For every it follows from Lemma 17 in Appendix B that there exists such that whenever is well-defined. As a result,

Throughout this section, we assume that is a dual-optimal pair satisfying As it follows that almost surely.

Proposition 9.

Suppose that the Assumptions (A1) and (A2) are in force. In addition, suppose that the functions and are such that the following properties are satisfied:

Property 1 (P-Compactness).

For any there exists a compact such that and the closure of the set, is compact, for some

Property 2 (P-USC).

For every collection such that for some we have

Then there exists a primal optimizer satisfying

It is well-known that upper semicontinuous functions defined on compact sets attain their supremum. As Property 1 (P-Compactness) and Property 2 (P-USC), respectively, enforce a specific type of compactness and upper semicontinuity requirements that are relevant to our setup, we use the suggestive labels (P-Compactness) and (P-USC), respectively, to identify Properties 1 and 2 throughout the rest of this section.

Proof.

Proof of Proposition 9. As consider a collection such that We first show that Property (P-Compactness) guarantees the existence of a weakly convergent subsequence of satisfying for some

Step 1 Verifying tightness of : As it follows from (11) that

| (39) |

for every For any Markov’s inequality results in,

which is at most Then, given any and for the choice specified in (P-Compactness), it follows from union bound that is at least,

because Consequently, As the closure of is compact for the choice of in (P-Compactness), we have is a compact subset of for given Therefore, for all we obtain that for any given thus rendering that the collection is tight.

Then, as a consequence of Prokhorov’s theorem, we have a subsequence such that for some

Step 2 Verifying : As we obtain as a consequence of the weak convergence (see that for all ). Further, as is a nonnegative lower semicontinuous function, it follows from a version of Fatou’s lemma for weakly converging probabilities (see Theorem 1.1 in Feinberg et al. (2014) and references therein) that Therefore,

Step 3 Verifying optimality of : As Property (P-USC) guarantees that , we obtain thus yielding The fact that follows from Theorem 8. ∎

The following assumptions imposing certain growth conditions on the functions and provide a simple set of sufficient conditions required to verify properties (P-Compactness) and (P-USC) stated in Proposition 9.

Assumption 3 (A3).

There exist a nondecreasing function satisfying as and a positive constant such that whenever

Assumption 4 (A4).

There exist an increasing function satisfying as and a positive constant such that In addition, given there exists a positive constant such that for every such that

The growth condition imposed in Assumption (A4) is similar to the requirement that the growth rate parameter defined in Gao and Kleywegt (2016), be equal to 0.

Corollary 1.

Let be locally compact when equipped with the topology induced by a norm defined on Suppose that the functions and satisfy Assumptions (A1) - (A4). Then, whenever the dual optimal pair satisfying is such that there exists a primal optimizer satisfying

Proof.

We verify the properties (P-Compactness) and

(P-USC) in the statement of Proposition

9 in order to establish the existence

of a primal optimizer.

Step 1 (Verification of

(P-Compactness)): As any Borel probability measure on a

Polish space is tight, there exists a compact

such that

for any Let

Given it follows from Assumption (A4) that

there exists large enough satisfying

for all such that

Then, for any

and

when

is large enough

such that

this is because,

when and

In particular, if

we

have for every

As it

follows that,

is a compact subset of Therefore,

is compact as well, thus verifying

Assumption (A3) in the statement of Proposition

9.

Step 2 (Verification of P-USC). Let

be such

that for some

Our objective is to show that

| (40) |

While (40) follows directly from the properties of weak convergence when is bounded upper semicontinuous, an additional asymptotic uniform integrability condition that,

is sufficient to guarantee (40) in the absence of boundedness (see, for example, Corollary 3 in Zapała (2008)). In order to demonstrate this asymptotic uniform integrability property, we proceed as follows: Given Assumption (A4) guarantees that for every satisfying Let and be subsets of defined as follows:

As for every (recall that it follows from the growth conditions in Assumption (A4) that

Further, as any satisfies it follows from the nondecreasing nature of that for every for every Combining this observation with the fact that we obtain,

As it follows from Markov’s inequality that, is at most,

Since we have -almost surely, for every Consequently, and therefore,

where and As a result, we obtain

| (41) |

Further, as is finite and when we have as Consequently, letting and in (41), we obtain

thus verifying the desired uniform integrability property. This observation, in conjunction with the upper semicontinuity of and weak convergence results in (40). As all the requirements stated in Proposition 9 are verified, a primal optimizer satisfying exists. ∎

Remark 8.

In addition to the assumptions made in Corollary 1, suppose that is a convex function in for every and is a concave function. Then, due to Corollary 1, a primal optimizer exists. Further, as the supremum in is attained at a unique maximizer for every it follows from Remark 3 that the primal optimizer is unique.

6. A few more examples.

6.1. Applications to computing general first passage probabilities.

Computing probabilities of first passage of a stochastic process into a target set of interest has been one of the central problems in applied probability. The objective of this section is to demonstrate that, similar to the one dimensional level crossing example in Section 3, one can compute general worst-case probabilities of first passage into a target set by simply computing the probability of first passage of the baseline stochastic process into a suitably inflated neighborhood of set The goal of such a demonstration is to show that the worst-case first passage probabilities can be computed with no significant extra effort.

Example 3.

Let model the financial reserve, at time of an insurance firm with two lines of business. Ruin occurs if the reserve process hits a certain ruin set within time In the univariate case, the ruin set is usually an interval of the form or its translations (as in Example 1). However, in multivariate cases, the ruin set can take a variety of shapes based on rules of capital transfers between the different lines of businesses. For example, if capital can be transferred between the two lines without any restrictions, a natural choice is to declare ruin when the total reserve becomes negative. On the other hand, if no capital transfer is allowed between the two lines, ruin is declared immediately when either or becomes negative. In this example, let us consider the case where the regulatory requirements allow only fraction of reserve, if positive, to be transferred from one line of business to the other. Such a restriction will result in a ruin set of the form

It is immediately clear that capital transfer is completely unrestricted when and altogether prohibited when The intermediate values of softly interpolates between these two extreme cases. Of course, one can take the fraction of capital transfer allowed from line to line to be different from that allowed from line to line 1, and various other modifications. However, to keep the discussion simple we focus on the model described above, and refer the readers to Hult and Lindskog (2006) for a general specification of ruin models allowing different rules of capital transfers between lines of businesses.

As in Example 1, we take the space in which the reserve process takes values to be the set of all -valued right continuous functions with left limits defined on the interval The space again, as in Example 1, is equipped with the standard -metric (see Chapter 3 of Whitt (2002)), and consequently, the cost function

| (42) |

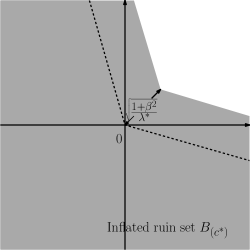

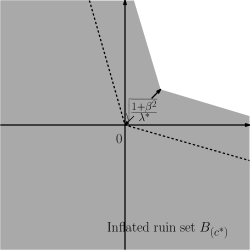

is continuous. Here, is the standard Euclidean norm for in and is the set of all strictly increasing functions such that both and are continuous. Let denote a baseline probability measure that models the reserve process in the path space. Given our objective is to characterize the worst-case first passage probability, of the reserve process hitting the ruin set As the set is not closed, we consider its topological closure

which, apart from the paths that hit ruin set also contains the paths that come arbitrarily close to without hitting due to the presence of jumps; the fact that is the desired closure is verified in Lemma 13 and Corollary 2 in Appendix B. Further, it is verified in Lemma 14 in Appendix B that

If the reference distribution is such that is continuous, then

| (43) | ||||

as an application of Theorem 15; here, as in Section 2.4, Following the expression for in Lemma 14, we also have that equals

| (44) |

Next, if we let and

| (45) |

as a family of sets parameterized by then it follows from (44) that

| (46) |

in words, the worst-case probability that the reserve process hits (or) comes arbitrarily close to the ruin set is simply equal to the probability under reference measure that the reserve process hits (or) comes arbitrarily close to an inflated ruin set where for any we define

This conclusion is very similar to (25) derived for 1-dimensional level crossing in Section 3. The original ruin set and the suitably inflated ruin set are respectively shown in the Figures 3(b)(a) and (b).

Next, as an example, let us take the reserve process satisfying the following dynamics as our baseline model:

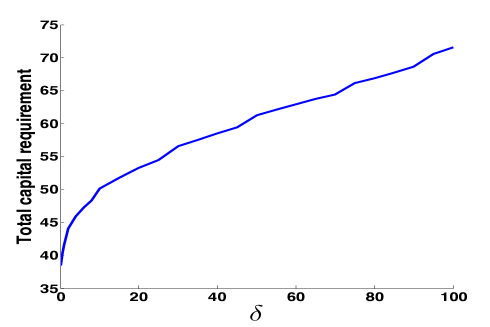

where is the drift vector with negative components, is a 2 2 positive definite covariance matrix, and a 2-dimensional standard Brownian motion. The real number denotes the total initial capital and such that denotes the proportion of initial capital set aside for the two different lines of businesses. The probability measure induced in the path space by the process is taken as the baseline measure Further, for purposes of numerical illustration, we take the identity matrix. Our aim is to find total initial capital such that (recall the definition of the ruin event in 45). This is indeed possible due to the equivalent characterization in (46), and the resulting capital requirement for various values of are displayed in Figure 3.

It may also be useful to note that one may as well choose the space of continuous functions taking values in as the underlying space to work with if the modeler decides to restrict the distributional ambiguities to continuous stochastic process; in that case, the first passage set itself is closed, and the inequality in (43) holds with equality.

As a final remark, if the modeler believes that model ambiguity is more prevalent in one line of business over other, she can perhaps quantify that effect by instead choosing for in the cost function defined in (42). This would penalise moving probability mass in one direction more than the other and result in the ruin set being inflated asymmetrically along different directions. We identify studying the effects of various choices of cost functions, the corresponding and the appropriateness of the resulting inflated ruin set for real world ruin problems as an important direction towards applying the proposed framework in quantitative risk management. For example, suppose that the regulator has interacted with the insurance company, and both the company and the regulator have negotiated a certain level of capital requirement multiple times in the past. Then the insurance company can calibrate from these previous interactions with the regulator. That is, find the value of which implies that the negotiated capital requirement in a given past interaction is necessary for the bound on ruin probability to be lesser than a fixed (regulatory driven) acceptance level (for instance, we use 0.01 as the acceptance level for ruin probability in our earlier numerical illustration in this example). An appropriate quantile of these ‘implied’ values may be used to choose based on risk preference.

6.2. Applications to ambiguity-averse decision making.

In this section, we consider a stochastic optimization problem in the presence of model uncertainty. It has been of immense interest recently to search for distributionally robust optimal decisions, that is, to find a decision variable that solves

Here, is a performance/risk measure that depends on a random element and a decision variable that can be chosen from an action space The solution to the above problem minimizes worst-case risk over a family of ambiguous probability measures Such an ambiguity-averse optimal choice is also referred as a distributionally robust choice, because the performance of the chosen decision variable is guaranteed to be better than OPT irrespective of the model picked from the family

There has been a broad range of ambiguity sets that has been considered: For examples, refer Delage and Ye (2010); Goh and Sim (2010); Wiesemann et al. (2014) for moment-based uncertainty sets, Hansen and Sargent (2001); Iyengar (2005); Nilim and El Ghaoui (2005); Lim and Shanthikumar (2007); Jain et al. (2010); Ben-Tal et al. (2013); Wang et al. (2015); Jiang and Guan (2015); Hu and Hong (2012); Bayraksan and Love (2015) for KL-divergence and other likelihood based uncertainty sets, Pflug and Wozabal (2007); Wozabal (2012); Esfahani and Kuhn (2015); Zhao and Guan (2015); Gao and Kleywegt (2016) for Wasserstein distance based neighborhoods, Erdoğan and Iyengar (2006) for neighborhoods based on Prokhorov metric, Bandi et al. (2015); Bandi and Bertsimas (2014) for uncertainty sets based on statistical tests and Ben-Tal et al. (2009); Bertsimas and Sim (2004) for a general overview. As most of the works mentioned above assume the random element to be -valued, it is of our interest in the following example to demonstrate the usefulness of our framework in formulating and solving distributionally robust optimization problems that involve stochastic processes taking values in general Polish spaces as well.

Example 4.

We continue with the insurance toy example considered in Section 3. In practice, as the risk left to the first-line insurer is too large, reinsurance is usually adopted. In proportional reinsurance, one of the popular forms of reinsurance, the insurer pays only for a proportion of the incoming claims, and a reinsurer pays for the remaining fraction of all the claims received. In turn, the reinsurer receives a premium at rate from the insurer. Here, otherwise, the insurer could make riskless profit by reinsuring the whole portfolio. The problem we consider here is to find the reinsurance proportion that minimises the expected maximum loss that happens within duration In the extensive line of research that studies optimal reinsurance proportion, diffusion models have been particularly recommended for tractability reasons (see, for example Hojgaard and Taksar (1998); Schmidli (2001)). As in Example 1, if we take to be the diffusion process that approximates the arrival of claims, then

is a suitable model for losses made by the firm. Here, is the rate of payout for the reinsurance contract, and is the rate at which a premium income is received by the insurance firm. The quantity of interest is to determine the reinsurance proportion that minimises the maximum expected losses,

| (47) |

However, as we saw in Example 1, conclusions based on diffusion approximations can be misleading. Following the practice advocated by the rich literature of robust optimization, we instead find a reinsurance proportion that performs well against the family of models specified by In other words, we attempt to solve for

where is a random element in space following measure and Here, as in Section 2.4, we have taken and

For if we take

then due to the application of Theorem 8, we obtain

To keep this discussion terse, it is verified in Lemma 12 in Appendix B that the inner infimum evaluates simply to

As a result,

| (48) |

which is an optimization problem that involves the same effective computational effort as the non-robust counterpart in (47). For the specific numerical values employed in Example 1, if we additionally take the new parameter the Brownian approximation model evaluates to the optimal choice and the corresponding loss whereas the robust counterpart in (48) evaluates to worst-case for the ambiguity-averse optimal choice For a collection of various other examples of using Wasserstein based ambiguity sets in the context of distributionally robust optimization, refer Esfahani and Kuhn (2015); Zhao and Guan (2015) and Gao and Kleywegt (2016).

Acknowledgments.

The authors would like to thank the anonymous referees whose valuable suggestions have been immensely useful in supplementing the proof of the strong duality theorem with crisp arguments at various instances. The authors would also like to thank Garud Iyengar and David Goldberg for helpful discussions, and Rui Gao for providing a comment that led us to add Remark 6 in the paper. The authors gratefully acknowledge support from Norges Bank Investment Management and NSF grant CMMI 1436700.

References

- Aliprantis and Border (1999) C. Aliprantis and K. Border. Infinite Dimensional Analysis: A Hitchhiker’s Guide. Studies in Economic Theory. Springer, 1999. ISBN 9783540658542. URL https://books.google.com/books?id=6jjY2Vi3aDEC.

- Aliprantis and Burkinshaw (1998) C. D. Aliprantis and O. Burkinshaw. Principles of Real Analysis. Gulf Professional Publishing, 1998.

- Ambrosio and Caffarelli (2003) L. Ambrosio and L. A. Caffarelli. Optimal transportation and applications: Lectures given at the CIME summer school 2001. Springer Science & Business Media, 2003.

- Asmussen and Albrecher (2010) S. Asmussen and H. Albrecher. Ruin probabilities. World Scientific Publishing Co. Pvt. Ltd., 2010. ISBN 978-981-4282-52-9; 981-4282-52-9. doi: 10.1142/9789814282536. URL http://dx.doi.org/10.1142/9789814282536.

- Atar et al. (2015) R. Atar, K. Chowdhary, and P. Dupuis. Robust bounds on risk-sensitive functionals via Rényi divergence. SIAM/ASA J. Uncertain. Quantif., 3(1):18–33, 2015. ISSN 2166-2525. doi: 10.1137/130939730. URL http://dx.doi.org/10.1137/130939730.

- Bandi and Bertsimas (2014) C. Bandi and D. Bertsimas. Robust option pricing. European J. Oper. Res., 239(3):842–853, 2014. ISSN 0377-2217. doi: 10.1016/j.ejor.2014.06.002. URL http://dx.doi.org/10.1016/j.ejor.2014.06.002.

- Bandi et al. (2015) C. Bandi, D. Bertsimas, and N. Youssef. Robust queueing theory. Operations Research, 63(3):676–700, 2015. doi: 10.1287/opre.2015.1367. URL http://dx.doi.org/10.1287/opre.2015.1367.

- Barbour and Xia (2006) A. D. Barbour and A. Xia. On Stein’s factors for poisson approximation in wasserstein distance. Bernoulli, 12(6):943–954, 2006. ISSN 13507265. URL http://www.jstor.org/stable/25464848.

- Bayraksan and Love (2015) G. Bayraksan and D. K. Love. Data-driven stochastic programming using phi-divergences. The Operations Research Revolution, pages 1–19, 2015.

- Ben-Tal et al. (2009) A. Ben-Tal, L. El Ghaoui, and A. Nemirovski. Robust optimization. Princeton Series in Applied Mathematics. Princeton University Press, 2009. ISBN 978-0-691-14368-2. doi: 10.1515/9781400831050. URL http://dx.doi.org/10.1515/9781400831050.