Confidence Regions for Entries of A Large Precision Matrix

Abstract

We consider the statistical inference for high-dimensional precision matrices. Specifically, we propose a data-driven procedure for constructing a class of simultaneous confidence regions for a subset of the entries of a large precision matrix. The confidence regions can be applied to test for specific structures of a precision matrix, and to recover its nonzero components. We first construct an estimator for the precision matrix via penalized node-wise regression. We then develop the Gaussian approximation to approximate the distribution of the maximum difference between the estimated and the true precision coefficients. A computationally feasible parametric bootstrap algorithm is developed to implement the proposed procedure. The theoretical justification is established under the setting which allows temporal dependence among observations. Therefore the proposed procedure is applicable to both independent and identically distributed data and time series data. Numerical results with both simulated and real data confirm the good performance of the proposed method.

JEL classification: C12, C13, C15.

Keywords: Bias correction; Dependent data; High dimensionality; Kernel estimation; Parametric bootstrap; Precision matrix.

1 Introduction

With an ever-increasing capacity of collecting and storing data, industry, business and government offices all encounter the task of analyzing the data of unprecedented size arisen from various practical fields such as panel studies of economic, social and natural (such as weather) phenomena, financial market analysis, genetic studies and communications engineering. A significant feature of these data is that the number of variables recorded on each individual is large or extremely large. Meanwhile, in many empirical studies, observations taken over different times are dependent with each other. Therefore, many well-developed statistical inference methods for independent and identically distributed (i.i.d.) data may no longer be applicable. Those features of modern data bring both opportunities and challenges to statisticians and econometricians.

The entries of covariance matrix measure the marginal linear dependence of two components of a random vector. There is a large body of literature on estimation and hypothesis testing of high-dimensional covariance matrices with i.i.d. data, including Bickel and Levina (2008a, b), Qiu and Chen (2012), Cai et al. (2013), Chang et al. (2017b) and references within. In order to capture the conditional dependence of two components of a random vector conditionally on all the others, the Gaussian graphical model (GGM) has been widely used. Under GGM, conditional independence of two components is equivalent to the fact that the correspondent entry of the precision matrix (i.e. the inverse of the covariance matrix) is zero. Therefore, the conditional dependence among components of a random vector can be well understood by investigating the structure of its precision matrix. Beyond GGM, the bijection relationship between the conditional dependence and the precision matrix may not hold. Nevertheless, the precision matrix still plays an important role in, among others, linear regression (van de Geer et al., 2014), linear prediction and kriging, and partial correlation graphs (Huang et al., 2010). See also Examples 1–3 in Section 2 below.

Let denote a precision matrix and be large. With i.i.d. observations, Yuan and Lin (2007) and Friedman et al. (2008) adopted graphical Lasso to estimate by maximizing the likelihood with an penalty. Meinshausen and Bühlmann (2006) introduced a neighborhood selection procedure which estimates by finding the nonzero regression coefficients of each component on all the other components using Lasso (Tibshirani, 1996) or Dantzig method (Candes and Tao, 2007). Also see Cai et al. (2011), Xue and Zou (2012) and Sun and Zhang (2013) for other penalized estimation methods. Chen et al. (2013) investigated the theoretical properties of the graphical Lasso estimator for with dependent observations. Though these methods provide consistent estimators for under some structural assumptions (for example, sparsity) imposed on , they cannot be used for statistical inference directly due to the non-negligible estimation biases, caused by the penalization, which are of order slower than .

The bias issue has been successfully overcome with i.i.d. Gaussian observations by, for example, Liu (2013) based on node-wise regressions method. Furthermore, Ren et al. (2015) proposed a novel estimator for each entry of based on pairwise penalized regression, and showed that their estimators achieved the minimax optimal rate with no bias terms. In spite of pairs among components, their method in practice only requires at most pairwise penalized regressions, where is the average size of the selected node-wise regression models.

The major contribution of this paper is to construct the confidence regions for subsets of the entries of . To our best knowledge, this is the first attempt of this kind. Furthermore we provide the asymptotic justification under the setting which allows dependent observations, and, hence, includes i.i.d. data as a special case. See also Remark 2 in Section 3.2 below. More precisely, let be a given index set of interest, whose cardinality can be finite or grow with . Let be the vector consisting of the entries of with their indices in . We propose a class of data-driven confidence regions for such that when both , where denotes the sample size. The potential application of is wide, including, for example, testing for some specific structures of , and detecting and recovering nonzero entries of consistently.

For any matrix , let be its element-wise -norm. We proceed as follows. First we propose a bias corrected estimator for via penalized node-wise regressions, and develop an asymptotic expansion for without assuming Gaussianity. As the leading term in the asymptotic expansion is a partial sum, we approximate the distribution of by that of the -norm of a high-dimensional normal distributed random vector with mean zero and covariance being an estimated long-run covariance matrix of an unobservable process. This normal approximation, inspired by Chernozhukov et al. (2013, 2014), paves the way for evaluating the probabilistic behavior of by parametric bootstrap.

It is worth pointing out that the kernel estimator for long-run covariances, initially proposed by Andrews (1991) for the problem with fixed dimension (i.e. fixed), also works under our setting with without requiring any structural assumptions on the underlying long-run covariance matrix. Owning to the form of this kernel estimator, the parametric bootstrap sampling can be implemented in an efficient manner in terms of both computational complexity and the required storage space; see Remark 4 in Section 3.2 below.

The rest of the paper is organized as follows. Section 2 introduces the problem to be solved and its background. The proposed procedure and its theoretical properties are presented in Section 3. Section 4 discusses the applications of our results. Simulation studies and a real data analysis are reported in Sections 5 and 6, respectively. All the technical proofs are relegated to the Appendix. We conclude this section by introducing some notation that is used throughout the paper. We write to mean . We say uniformly over if as . Let and denote, respectively, the - and -norm of a vector.

2 Preliminaries

Let be observations from an -valued time series, where and each has the constant first two moments, i.e. and for each . Let be the precision matrix. We assume that is -mixing in the sense that as , where

Here and are the -fields generated respectively by and . -mixing is a mild condition for time series. It is known that causal ARMA processes with continuous innovation distributions, stationary Markov chains under some mild conditions and stationary GARCH models with finite second moments and continuous innovation distributions are all -mixing. We refer to Section 2.6 of Fan and Yao (2003) for the further details on -mixing condition.

For a given index set , recall denotes the vector consisting of the entries of with their indices in . We are interested in constructing a class of confidence regions for such that

| (1) |

We also allow , the length of vector , either to be fixed or to go to infinity together with . The largest can be . We first give several motivating examples.

Example 1.

(High-dimensional linear regression) Consider linear regression with , where consists of explanatory variables and is large, and are true regression coefficients. In order to identify non-zero regression coefficients, we test the hypotheses

| (2) |

where is a given index set of interest. Let , and be the precision matrix of . It can be shown that , where . Thus, (2) can be equivalently expressed as

| (3) |

where . We reject at the significance level if does not contain the origin of with .

Example 2.

(Linear prediction and kriging) In the context of predicting a random variable based on an observed -dimensional vector , the best linear predictor in the sense of minimizing the mean squared predictive error is , where is the precision matrix of . Here we assume the means of both and are zero, to simplify the notation. We also assume that any redundant components of have been removed by applying the techniques described in Example 1 above.

To obtain a consistent estimate for when is large, it is necessary to impose some structural assumptions on . In the context of kriging (i.e. linear prediction in the context of spatial or spatial-temporal statistics), some lower-dimensional factor structures have been explored. See Huang et al. (2017) and the references within. Bandness/bandableness is another popular structural assumption often used in estimating large covariance or precision matrices (Bickel and Levina, 2008a). To investigate a banded structure for , one may test the hypotheses

| (4) |

where is a prespecified integer. We reject if confidence region does not contain the origin , where and .

Example 3.

(Partial correlation network) Given a precision matrix , we can define an undirected network where the vertex set represents the components of and the edge set are the pairs of variables with non-zero precision coefficients. Let be the partial correlation between the -th and the -th components of for any , where and are the errors of the best linear predictors of and given , respectively. From Lemma 1 of Peng et al. (2009), it is known that . Therefore, the network also represents the partial correlation graph of . The vertices if and only if and are partially uncorrelated. The GGM assumes in addition that is multivariate normal. Then depicts the conditional dependence among the vertices of the network, i.e. is the conditional correlation between the -th and -th vertices given all the others.

Neighborhood and community are two basic features in a network. The neighborhood of the -th vertex, denoted by , is the set of all the vertices directly connected to it. For most of the spatial data, it is believed that the partial correlation neighborhood is related to the spatial neighborhood. Let be the set including the first closest vertices to the -th vertex in the spatial domain. It is of great interest to test vs. for some pre-specified positive constant . A community in a network is a group of vertices that have heavier connectivity within the group than outside the group. For graph estimation, we want to maximize the within-community connectivity and reduce the between-community connectivity. Therefore, it is of practical importance to explore the connectivity between different communities. Assume the components of are decomposed into disjoint communities . We are interested in recovering .

3 Main results

3.1 Estimation of

We first recall the relationship between a precision matrix and node-wise regressions. For a random vector with mean and covariance , we consider node-wise regressions

| (5) |

Let . The regression error is uncorrelated with if and only if for any . Under this condition, for any and . Let and . Then ; see Lemma 1 of Peng et al. (2009). This relationship between and provides a way to learn by the regression errors in (5).

Since the error vector in (5) is unobservable in practice, its “proxy” – the residuals of the node-wise regressions – can be used to estimate . Let . For each , we may fit the high-dimensional linear regression

| (6) |

by Lasso (Tibshirani, 1996), Dantzig estimation (Candes and Tao, 2007) or scaled Lasso (Sun and Zhang, 2012). For the case , the regression (6) will be conducted on the centered data , where is the sample mean. For simplicity, we adopt Lasso estimation. Let be the Lasso estimator of defined as follows:

| (7) |

where and is the tuning parameter. For each , the residual

| (8) |

provides an estimate of . Write and let be the sample covariance of , where . It is well known that is an unbiased estimator of , however, replacing by will incur a bias term. Specifically, as shown in Lemma 3 in Appendix, under Conditions 1–3 and some mild restrictions on the sparsity of and the growth rate of with respect to , it holds that

| (9) |

Here the higher order term is uniform over all and . Since is -consistent for , (9) implies that is also -consistent for . However, for any , due to the slow convergence rates of the Lasso estimators and , is no longer -consistent for . To eliminate the bias, we employ an estimator for :

| (10) |

By noticing that , we estimate by

| (11) |

for any and . We need to point out that the asymptotic expansion (9) is still valid for other penalized methods such as Dantzig estimation (Candes and Tao, 2007) and scaled Lasso (Sun and Zhang, 2012). Hence, we can also estimate and as (10) and (11), respectively, based on the residuals obtained by other penalized methods. To study the theoretical properties of this estimator , we need the following regularity conditions.

Condition 1.

There exist constants , , and independent of and such that for each ,

Condition 2.

The eigenvalues of are uniformly bounded away from zero and infinity.

Condition 3.

There exist constants and independent of and such that for any positive .

Condition 1 implies and for any and . It ensures the exponential upper bounds for the tail probabilities of the statistics concerned (see for example Lemma 1 in Appendix), which makes our procedure work for diverging at some exponential rate of . Condition 2 implies the bounded eigenvalues of and , which is commonly assumed in the literatures of high-dimensional data analysis. Condition 3 for the -mixing coefficients of is mild. Causal ARMA processes with continuous innovation distributions are -mixing with exponentially decaying . So are stationary Markov chains satisfying certain conditions. See Section 2.6.1 of Fan and Yao (2003) and the references therein. In fact, stationary GARCH models with finite second moments and continuous innovation distributions are also -mixing with exponentially decaying ; see Proposition 12 of Carrasco and Chen (2002). If we only require and for any in Condition 1 and in Condition 3 for some and , we can apply Fuk-Nagaev-type inequalities to construct the upper bounds for the tail probabilities of the statistics if diverges at some polynomial rate of . We refer to Section 3.2 of Chang et al. (2018) for the implementation of Fuk-Nagaev-type inequalities in such a scenario. The -mixing condition can be replaced by the -mixing condition, under which we can justify the proposed method for diverging at some polynomial rate of by using Fuk-Nagaev-type inequalities. However, it remains an open problem to establish the relevant properties under -mixing for diverging at some exponential rate of .

Proposition 1.

We see from Proposition 1 that is centered at the true parameter with a standard deviation at the order . Since is proportional to , it follows from that is sparse. When the maximum number of nonzero elements in each row of is of the order smaller than , Proposition 1 holds even when is of an exponential rate of . Similar to the asymptotic expansion for in Proposition 1, Liu (2013) gave an asymptotic expansion for with . More specifically, with i.i.d. data, he showed that for specified in Proposition 1 and , where is a remainder term with the convergence rate faster than . It follows from the central limit theorem that converges to standard normal distribution with some suitable scale , which indicates that can be used as the testing statistic to test or not. Notice that which implies . Hence, the magnitude of will be large if . This indicates that the asymptotic expansion given in Liu (2013) is enough for identifying non-zero entries of . However, it is not enough for constructing the confidence interval for due to the fact that it does not contain the asymptotic expansion of .

3.2 Confidence regions

Let . It follows from Proposition 1 that

where . Restricted on a given index set with , we have

| (12) |

Based on (12), we consider two kinds of confidence regions:

| (13) |

where is an diagonal matrix, specified in Remark 5 below, of which the elements are the estimated standard deviations of the components in . Here and are two critical values to be determined. and represent the so-called “non-Studentized-type” and “Studentized-type” confidence regions for , respectively. The Studentized-type confidence regions perform better than the non-Studentized-type ones when the heteroscedasticity exists, however, the performance of the non-Studentized-type confidence regions is more stable when the sample size is fairly small. See Chang et al. (2017a).

In the sequel, we mainly focus on estimating the critical value in (13), as can be estimated in the similar manner; see Remark 5 below. To determine , we need to first characterize the probabilistic behavior of . Since is a higher order term, will behave similarly as when is large. Notice that each element of is asymptotically normal distributed. Following the idea of Chernozhukov et al. (2013), it can be proved that the limiting behavior of can be approximated by that of the -norm of a certain multivariate normal vector. See Theorem 1 below. More specifically, for each , let be an -dimensional vector whose -th element is where is a bijective mapping from to such that . Then, we have

Denote by the long-run covariance of , namely,

| (14) |

Let where . Then specified in (14) can be written as

| (15) |

where . To study the asymptotical distribution of the average of the temporally dependent sequence and its long-run covariance , we introduce the following condition on .

Condition 4.

There exists constant such that

for each .

Condition 4 is for the validity of the Gaussian approximation for dependent data. Under Conditions 1 and 3, Davydov inequality (Davydov, 1968) entails for some universal constant . Together with Condition 4, they match the requirements of Gaussian approximation imposed on the long-run covariance of for and . See Theorem B.1 of Chernozhukov et al. (2014). If is stationary, . Under the stationarity assumption on each sequence , Condition 4 is equivalent to for any . Now we are ready to state our main result.

Theorem 1.

Remark 1.

Theorem 1 shows that the Kolmogorov distance between the distributions of and converges to zero. More specifically, as shown in the proof of Theorem 1 in Appendix, this convergence rate is for some constant without requiring any structural assumption on the underlying covariance . Note that may converge weakly to an extreme value distribution, which however requires some more stringent assumptions on the structure of . Furthermore the slow convergence to the extreme value distribution, i.e. typically slower than , entails an less accurate approximation than that implied by Theorem 1. We need to point out that there is also a requirement imposed on the diverging rate of such as for some constant in the proof of Theorem 1. Since , such requirement is satisfied automatically when the requirements on in Theorem 1 are required.

Theorem 1 provides a guideline to approximate the distribution of . To implement it in practice, we need to propose an estimator for . Denote by the matrix sandwiched by ’s on the right-hand side of (15), which is the long-run covariance of . Notice that defined in (10) is -consistent to , we can estimate by

| (16) |

Let for , and define

Based on the ’s, we propose a kernel estimator suggested by Andrews (1991) for as

| (17) |

where is the bandwidth, is a symmetric kernel function that is continuous at 0 and satisfying , for any , and . Given and defined respectively in (16) and (17), an estimator for is given by

| (18) |

Theorem 2 below shows that we can approximate the distribution of by that of for .

Remark 2.

Andrews (1991) systematically investigated the theoretical properties for the kernel estimator for the long-run covariance matrix when is fixed. It shows that the Quadratic Spectral kernel

is optimal in the sense of minimizing the asymptotic truncated mean square error. In our numerical work, we adopt this quadratic spectral kernel with the data-driven selected bandwidth proposed in Section 6 of Andrews (1991), though our theoretical analysis applies to general kernel functions. Both our theoretical and simulation results show that this kernel estimator still works when is large in relation to . There also exist other estimation methods for long-run covariances, including the estimation utilizing moving block bootstrap (Lahiri, 2003; Nordman and Lahiri, 2005). Also see den Haan and Levin (1997) and Kiefer et al. (2000). Compared to those methods, an added advantage of using the kernel estimator is the computational efficiency in terms of both speed and storage space especially when is large; see See Remark 4 below. When the observations are i.i.d., a special case of our setting, as in (14) is degenerated to , the marginal covariance of . We can apply to estimate , and then use to estimate with as in (16).

Theorem 2.

Remark 3.

In practice, we approximate the distribution of by Monto Carlo simulation. Specifically, let be i.i.d. -dimensional random vectors drawn from . Then the conditional distribution of given can be approximated by the empirical distribution of , namely,

Then, specified in (13) can be estimated by

| (19) |

To improve computational efficiency, we propose the following Kernel based Multiplier Bootstrap (KMB) procedure to generate , which is much more efficient when is large.

-

Step 1.

Generate from , where is the matrix with as its -th element.

-

Step 2.

Let , where is defined in (16).

Remark 4.

The standard approach to draw a random vector consists of three steps: (i) perform the Cholesky decomposition on the matrix , (ii) generate independent standard normal random variables , (iii) perform transformation . Thus, it requires to store matrix and , which amounts to the storage costs and , respectively. The computational complexity is , mainly due to computing and the Cholesky decomposition. Note that could be in the order of . In contrast the KMB scheme described above only needs to store and , and draw an -dimensional random vector in each parametric bootstrap sample. This amounts to total storage cost . More significantly, the computational complexity is only which is independent of and .

Remark 5.

For the Studentized-type confidence regions defined in (13), we can choose the diagonal matrix for specified in (18). Correspondingly, for , it can be proved, in the similar manner as that for Thorem 2, that

To approximate the distribution of , we only need to replace the Step 2 in the KMB procedure by

-

Step 2′.

Let where is defined in (16).

Based on the i.i.d. random vectors generated by Steps 1 and , we can estimate via , which is calculated the same as in (19). We call the procedure combining Steps 1 and as Studentized Kernel based Multiplier Bootstrap (SKMB).

4 Applications

4.1 Testing structures of

Many statistical applications require to explore or to detect some specific structures of the precision matrix . Given an index set of interest and a set of pre-specified constants , we test the hypotheses

Recall that is a bijective mapping from to such that . Let and . A usual choice of is the zero vector, corresponding to the test for non-zero structures of . Given a prescribed level , define for specified in (13). Then, we reject the null hypothesis at level if . This procedure is equivalent to the test based on the -type statistic that rejects if . The -type statistics are widely used in testing high-dimensional means and covariances. See, for example, Cai et al. (2013) and Chang et al. (2017a, b). The following corollary gives the empirical size and power of the proposed testing procedure .

Corollary 1.

Corollary 1 implies that the empirical size of the proposed testing procedure will converge to the nominal level under . The condition specifies the maximal deviation of the precision matrix from the null hypothesis for any , which is a commonly used condition for studying the power of the -type test. See Cai et al. (2013) and Chang et al. (2017a, b). Corollary 1 shows that the power of the proposed test will approach 1 if such condition holds for some constant . A “Studentized-type” test can be similarly constructed via replacing and by and in (13), respectively.

4.2 Support recovering of

In studying partial correlation networks or GGM, we are interested in identifying the edges between nodes. This is equivalent to recover the non-zero components in the associated precision matrix. Let be the set of indices with non-zero precision coefficients. Choose . Note that provides simultaneous confidence regions for all the entries of . To recover the set consistently, we choose those precision coefficients whose confidence intervals do not include zero. For any -dimensional vector , let be the support set of . Recall is a bijective mapping from to such that . For any , let

be the estimate of .

In our context, note that the false positive means estimating the zero as non-zero. Let FP be the number of false positive errors conducted by the estimated signal set . Let the family wise error rate (FWER) be the probability of conducting any false positive errors, namely, . See Hochberg and Tamhane (2009) for various types of error rates in multiple testing procedures. Notice that . This shows that the proposed method is able to control family wise error rate at level for any . The following corollary further shows the consistency of .

Corollary 2.

From Corollary 2, we see that the selected set can identify the true set consistently if the minimum signal strength satisfies for some constant . Notice from Corollary 1 that only the maximum signal is required in the power analysis of the proposed testing procedure. Compared to signal detection, signal recovery is a more challenging problem. The full support recovery of requires all non-zero larger than a specific level. Similarly, we can also define via replacing by its “Studentized-type” analogue in (13).

5 Numerical study

In this section, we evaluate the performance of the proposed KMB and SKMB procedures in finite samples. Let be i.i.d. -dimensional samples from . The observed data were generated from the model and for . The parameter was set to be and , which captures the temporal dependence among observations. We chose the sample size and , and the dimension , and in the simulation. Let based on a positive definite matrix . The following two settings were considered for .

-

A.

Let for any .

-

B.

Let for any , for , where , and otherwise.

Structures A and B lead to, respectively, the banded and block diagonal structures for the precision matrix . Note that, based on such defined covariance , the diagonal elements of the precision matrix are unit. For each of the precision matrices, we considered two choices for the index set : (i) all zero components of , i.e. , and (ii) all the components excluded the ones on the main diagonal, i.e. . Notice that the sets of all zero components in for structures A and B are and , respectively. As we illustrate in the footnote222It follows from Proposition 1 that , where the term holds uniformly over . Recall and , if which is equivalent to , then it holds that Since ’s are i.i.d., together with , we have for any , which implies for any such that . On the other hand, based on the Gaussian assumption, since , we know the two normal distributed random variables and are independent, which leads to . Therefore, for any such that . Notice that in our setting for any , then . Hence, the variances of for any such that are almost identical. , the index sets in the setting (i) and (ii) mimic, respectively, the homogeneous and heteroscedastic cases for the variances of among .

For each of the cases above, we examined the accuracy of the proposed KMB and SKMB approximations to the distributions of the non-Studentized-type statistic and the Studentized-type statistic , respectively. Denote by and the distribution functions of and , respectively. In each of the 1000 independent repetitions, we first draw a sample with size following the above discussed data generating mechanism, and then computed the associated values of and in this sample. Since and are unknown, we used the empirical distributions of and over 1000 repetitions, denoted as and , to approximate them, respectively. For each repetition , we applied the KMB and SKMB procedures to estimate the quantiles of and , denoted as and , respectively, with , and then computed their associated empirical coverages and . We considered and in the simulation. We report the averages and standard deviations of and in Tables 1–3. Due to the selection of the tuning parameter in (7) depends on the standard deviation of the error term , we adopted the scaled Lasso (Sun and Zhang, 2012) in the simulation which can estimate the regression coefficients and the variance of the error simultaneously. The tuning parameters in scale Lasso were selected according to Ren et al. (2015).

It is worth noting that in order to accomplish the statistical computing for large under the R environment in high speed, we programmed the generation of random numbers and most loops into C functions such that we utilized “.C()” routine to call those C functions from R. However, the computation of the two types of statistics involves the fitting of the node-wise regressions. As a consequence, the simulation for large still requires a large amount of computation time. In order to overcome this time-consuming issue, the computation in this numerical study was undertaken with the assistance of the supercomputer Raijin at the NCI National Facility systems supported by the Australian Government. The supercomputer Raijin comprises 57,864 cores, which helped us parallel process a large number of simulations simultaneously.

From Tables 1–3, we observe that, for both KMB and SKMB procedures, the overall differences between the empirical coverage rates and the corresponding nominal levels are small, which demonstrates that the KMB and SKMB procedures can provide accurate approximations to the distributions of and , respectively. Also note that the coverage rates improve as increases. And, our results are robust to the temporal dependence parameter , which indicates the proposed procedures are adaptive to time dependent observations.

Comparing the simulation results indicated by KMB and SKMB in the category of Tables 1–3, when the dimension is less than the sample size (, ), we can see that the SKMB procedure has better accuracy than the KMB procedure if the heteroscedastic issue exists. This finding also exists when the dimension is over the sample size and both of them are large (, ). For the homogeneous case , the KMB procedure provides better accuracy than the SKMB procedure when sample size is small (). However, when the sample size becomes larger , the accuracy of the SKMB procedure can be significantly improved and it will outperform the KMB procedure. The phenomenon that the SKMB procedure sometimes cannot beat the KMB procedure might be caused by incorporating the estimated standard deviations of ’s in the denominator of the Studentized-type statistic, which suffers from high variability when the sample size is small. The simulation results suggest us that: (i) when the dimension is less than the sample size or both the dimension and the sample size are very large, the SKMB procedure should be used to construct the confidence regions of if the heteroscedastic issue exists; (ii) if the sample size is small, and we have some previous information that there does not exist heteroscedastic issue, then the KMB procedure should be used to construct the confidence regions of . However, even in the homogeneous case, the SKMB procedure should still be employed when the sample size is large.

6 Real data analysis

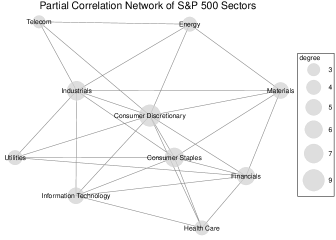

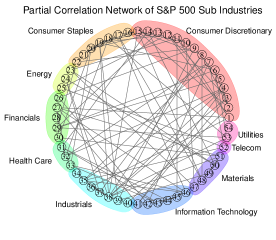

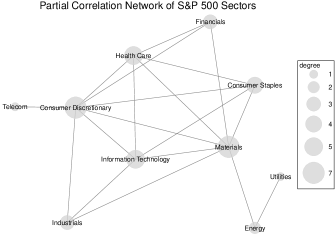

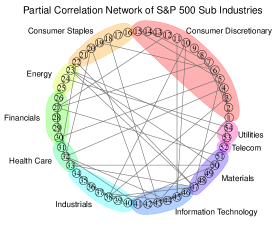

In this section, we follow Example 3 in Section 2 to study the partial correlation networks of the Standard and Poors (S&P) 500 Component Stocks in 2005 (252 trading days, preceding the crisis) and in 2008 (253 trading days, during the crisis), respectively. The reason to analyze those two periods is to understand the structure and dynamic of financial networks affected by the global financial crisis (Schweitzer et al., 2009). Aït-Sahalia and Xiu (2015) analyzed the data in 2005 and 2008 as well in order to investigate the influence of the financial crisis.

We analyzed the data from http://quote.yahoo.com/ via the R package tseries, which contains the daily closing prices of S&P 500 stocks. The R command get.hist.quote can be used to acquire the data. We kept 402 stocks in our analysis whose closing prices were capable of being downloaded by the R command and did not have any missing values during 2005 and 2008.

Let be the -th stock price at day . We considered the log return of the stocks, which is defined by . As kindly pointed out by a referee that the log return data usually exhibit volatility clustering, we utilized the R package fGarch to obtain the conditional standard deviation for the mean centered log return of each stock via fitting a GARCH(1,1) model, and then we standardized the log return by its mean and conditional standard deviation. Ultimately, we had the standardized log returns of all the 402 assets at day .

Let be the precision matrix of . By the relationship between partial correlation and precision matrix, the partial correlation network can be constructed by the non-zero precision coefficients as demonstrated in Example 3 in Section 2. To learn the structures of , we focused on the Global Industry Classification Standard (GICS) sectors and their sub industries of the S&P 500 companies, and aimed to discover the sub blocks of which had nonzero entries. Those blocks could help us build the partial correlation networks of the sectors and sub industries for the S&P 500 stocks in 2005 and 2008, respectively.

The advantage of investigating the complex financial network system by partial correlation is to overcome the issue that the marginal correlation between two stocks might be a result of their correlations to other mediating stocks (Kenett et al., 2010). For example, if two stocks and are both correlated with some stocks in the set , the partial correlation can suitably remove the linear effect of on and . Hence, it measures a “direct” relationship between and (de la Fuente et al., 2004). The partial correlation analysis is widely used in the study of financial networks (Shapira et al., 2009; Kenett et al., 2010), as well as the study of gene networks (de la Fuente et al., 2004; Reverter and Chan, 2008; Chen and Zheng, 2009).

Based on the information on bloomberg and “List of S&P 500 companies” on wikipedia, we identified 10 major sectors with 54 sub industries of the S&P 500 companies (see Tables 4 and 5 for detailed categories). The 10 sectors were Consumer Discretionary, Consumer Staples, Energy, Financials, Health Care, Industrials, Information Technology, Materials, Telecommunication Services and Utilities. There were one company with the unidentified sector and eight companies with unidentified sub industries due to acquisition or ticket change (represented by “NA” in Tables 4 and 5).

To explore the partial correlation networks of different sectors and sub industries, we were interested in a set of hypotheses

| (20) |

for disjoint index sets , which represented different sub industries. For each of the hypotheses in (20), we calculated the Studentized-type statistic in (13) with and apply the SKMB procedure to obtain parametric bootstrap samples . The P-value of the hypothesis (20) was

To identify the significant blocks, we applied the Benjamini and Hochberg (1995)’s multiple testing procedure that controls the false discovery rate (FDR) of (20) at the rate . Let be the ordered P-values and be the corresponding null hypotheses, where is the number of hypotheses under our consideration. Note that we had for testing sub industry blocks. We rejected in (20) for .

We constructed the partial correlation networks based on the significant blocks from the above multiple testing procedure. The estimated partial correlation networks of the 54 sub industries, labeled by numbers from 1 to 54, are shown in the right panels of Figures 1 and 2, corresponding to 2005 and 2008, respectively. The name of each sub industry and the stocks included can be found in Tables 4 and 5. The shaded areas with different colors represent the 10 major sectors, respectively. The left panels in Figures 1 and 2 give the partial correlation networks of the sectors, where the nodes represent the 10 sectors, and two nodes (sectors) and are connected if and only if there exists a connection between one of sub industries belonging to sector and one of sub industries belonging to sector in the right panel.

We observed from the left panel of Figure 1 that preceding the crisis in 2005, the Consumer Discretionary sector was likely to be a hub connecting to all the other 9 sectors. It was the most influential sector with the largest degree, i.e., the total number of directed links connecting to the Consumer Discretionary sector in the network. During the crisis in 2008, the Consumer Discretionary sector was still the most influential sector as shown by the left panel of Figure 2, but it had less connections compared to 2005. The Financials sector was a little bit separated from the other sectors in 2008, with only half connections in contrast with the network connectivity in 2005. The similar situation also appeared in the partial correlations networks of S&P 500 sub industries as shown in the right panels of Figures 1 and 2. More specifically, both the numbers of the edges within and between most sectors for the network of S&P 500 sub industries in 2008 were significantly less than those in 2005 (see Table 6 for details), which indicated that the market fear in the crisis broke the connections of stock sectors and sub industries. From the perspective of financial network studies, the above analysis confirmed that fear froze the market in the 2008 crisis (Reavis, 2012).

Acknowledgments

The authors are grateful to the Co-Editor, an Associate Editor and two anonymous referees for constructive comments and suggestions. This research was undertaken with the assistance of resources provided at the NCI National Facility systems at the Australian National University through the ANU Allocation Scheme supported by the Australian Government. The authors would like to thank Pauline O’Shaughnessy for her great help in getting us started with the supercomputer Raijin. Jinyuan Chang was supported in part by the Fundamental Research Funds for the Central Universities (Grant No. JBK1802069, JBK171121), NSFC (Grant No. 11501462), the Center of Statistical Research at SWUFE, and the Joint Lab of Data Science and Business Intelligence at SWUFE. Qiwei Yao was supported in part by an EPSRC research grant.

Appendix

Throughout the Appendix, let denote a generic positive constant depending only on the constants specified in Conditions 1–4, which may be different in different cases. Let , , and . Define and .

Lemma 1.

Proof: For any given and , based on the first part of Condition 1, Lemma 2 of Chang et al. (2013) leads to

Hence, for any such that , Theorem 1 of Merlevède et al. (2011) leads to

By Bonferroni inequality, we have

Let , we obtain the first conclusion. Following the same arguments, we can establish the other inequalities.

Proof: Define

for some , where is given in Lemma 1. Selecting for any , Theorem 6.1 and Corollary 6.8 of Bühlmann and van de Geer (2011) imply that, restricted on , we have

| (21) |

and

| (22) |

with probability approaching 1. By Bonferroni inequality and Lemma 1,

For suitable selection of , we have as . Thus, from (21), it holds that

| (23) |

On the other hand, notice that

by Condition 2, Lemma 1, (22) and (23), we have

Hence, we complete the proof.

Lemma 3.

Proof: Notice that and for any , then

Condition 2, Lemmas 1 and 2 imply that

Meanwhile, by Lemma 1, we have which implies that

Therefore, we have

| (24) |

Here the remainder term is uniform over any and . On the other hand, By the fourth result of Lemma 1, it yields that Here the remainder term is uniform over all . Together with (24), we have

Here the remainder term is also uniform over all and . Hence,

We complete the proof.

Proof of Proposition 1: Notice that , and for any and , Lemma 3 implies that

for any . Recall . It follows from Lemma 1 that Recall , if for specified in Lemma 1 and , it holds that

for any . Meanwhile, by the same arguments, for each , it holds that This proves Proposition 1.

Proof of Theorem 1: Define For any and , it yields that

On the other hand, notice that , following the same arguments, we have

| (25) |

By the Anti-concentration inequality for Gaussian random vector [Corollary 1 of Chernozhukov et al. (2015)], it holds that

| (26) |

for any . From the proofs of Lemmas 2 and 3, we know . Thus, if , we can select a suitable to guarantee and . Therefore, for such selected , (25) leads to

| (27) |

To prove Theorem 1, it suffices to show as . We will show this below.

Write where and . Given a , define and Write and for each . The diverging rate of will be specified later. Let be a positive integer satisfying , and . We decompose the sequence to the following blocks where and is the integer truncation operator: and . Additionally, let be two positive integers such that , and . We decompose each to a “large” block with length and a “small” block with length . Specifically, and for any , and . Assume is a centered normal random vector such that

Our following proof includes two steps. The first step is to show

| (28) |

And the second step is to show

| (29) |

We first show (28). Define Notice that , by the triangle inequality, it holds that Similar to (25), we have

| (30) |

for any . For each , it follows from Davydov inequality (Davydov, 1968) that

Applying Lemma 2 of Chang et al. (2013), Conditions 1 and 4 imply that for any . Then

| (31) |

By the triangle inequality and Jensen’s inequality,

| (32) |

which implies that

Thus, it follows from Markov inequality that

Similar to (26), it holds that for any . If we choose and for some sufficiently large , then Therefore, (30) implies . To show (28) that , it suffices to prove .

Let and . To prove , it is equivalent to show . From Theorem B.1 of Chernozhukov, Chetverikov and Kato (2014), if . Notice that , thus to show , it suffices to show

By Theorem B.1 of Chernozhukov et al. (2014), it holds that provided that

| (33) |

for some . As we mentioned above, . To make diverge as fast as possible, we can take for some . Then (33) becomes

Therefore, Notice that takes the supremum when . Hence, if , it holds that . Then we construct the result (28).

Analogously, to show (29), it suffices to show . Write as the covariance of . Recall denotes the covariance of . Lemma 3.1 of Chernozhukov et al. (2013) leads to

| (34) |

We will specify the convergence rate of below. Notice that, for any , we have

The triangle inequality yields

For each , the following identities hold:

Together with the triangle inequality, Davydov inequality and Cauchy-Schwarz inequality, we have

From (32), it holds that

By the proof of Lemma 2 in Chang et al. (2015), we can prove that

| (35) |

Specifically, notice that

| (36) |

where we set . By Cauchy-Schwarz inequality and Davydov inequality, we have

Similarly, we can bound the other terms in (36). Therefore, we have (35) holds which implies that . For and specified above, (34) implies . Then we construct the result (29). Hence, we complete the proof of Theorem 1.

Lemma 4.

Proof: We first construct an upper bound for . For any and , it holds that

| (37) |

for any , where . Following Lemma 2 of Chang et al. (2013), it holds that

| (38) |

for any . Notice that , we have if . Then, (38) leads to

| (39) |

We will specify the upper bound for below. Similar to (38), we have that

| (40) |

for any . Denote by the event . For each , let for . Write , then

| (41) |

From (40), we have . Similar to (31), we have

If , then (41) yields that

| (42) |

For each , we first consider . By Markov inequality, it holds that

| (43) |

for any . Let be a positive integer such that and for specified in (37). We decompose the sequence to the following blocks where : and . Additionally, let and . We then decompose each to a block with length and a block with length . Specifically, and for any , and . Based on these notations and Cauchy-Schwarz inequality, it holds that

By Lemma 2 of Merlevède et al. (2011), noticing that , we have

| (44) |

Following the inequality for any , we have that

Together with (44), following the inequality for any , and , it holds that

Similarly, we can obtain the same upper bound for . Hence,

We restrict . Notice that , then

Together with (43), notice that and , it holds that

| (45) |

To make the upper bound in above inequality decay to zero for some and , we need to require For the first term on the right-hand side of above inequality, the optimal selection of is . Therefore, (45) can be simplified to

if . The same inequality also hold for . Combining with (37), (39) and (42),

for any such that . Notice that above inequality is uniformly for any and , thus

To make the upper bound of above inequality converge to zero, and should satisfy the following restrictions:

| (46) |

Notice that , (46) implies that where To make can decay to zero and can diverge at exponential rate of , we need to assume and Let and . We select and , then

Hence, we complete the proof of Lemma 4.

Proof of Theorem 2: Similar to the proof of (29), it suffices to prove . By Lemmas 1 and 3, we have . Notice that ’s are uniformly bounded away from zero, then ’s are uniformly bounded away from infinity with probability approaching one. Thus,

| (47) |

We will show below.

Define

where

We will specify the convergence rates of and , respectively. Notice that

For any , it holds that

which implies

| (48) |

We will prove the -norm of the last three terms on the right-hand side of above identity are . We only need to show this rate for one of them and the proofs for the other two are similar. For any and ,

Here the term is uniform for any and . Then the -th component of is

| (49) |

where

Here the term is uniform for any and . Following the same arguments, we have

Therefore, the -th component of can be bounded by where the last identity in above equation is based on (23). Therefore, from (48), by Lemma 4, we have

Analogously, we can prove the same result for . Therefore, Repeating the the proof of Proposition 1(b) in Andrews (1991), we know the convergence in Proposition 1(b) is uniformly for each component of . Thus, . Then Similar to (34), we complete the proof.

Proof of Corollary 1: From Theorem 2, it holds that . Therefore, which establishes part (i). For part (ii), the following standard results on Gaussian maximum hold:

and

for any . Then, Let for some . Restricted on , Let . Without lose of generality, we assume . Therefore,

Restricted on , if , it holds that for some , which implies

From Lemma 4, we know that which also implies that . Then we can choose suitable such that . Hence, we complete part (ii).

Proof of Corollary 2: Our proof includes two steps: (i) to show , and (ii) to show . Result (i) is equivalent to . The latter one is equivalent to . Notice that , it holds that

which implies . Then we construct result (i). Result (ii) is equivalent to . Let . Without lose of generality, we assume . Notice that

we can construct result (ii) following the arguments for the proof of Corollary 1.

References

- Aït-Sahalia and Xiu (2015) Aït-Sahalia, Y. and Xiu, D. (2015). Principal component analysis of high frequency data. National Bureau of Economic Research, working paper, No. w21584.

- Andrews (1991) Andrews, D. W. K. (1991). Heteroskedasticity and autocorrelation consistent covariance matrix estimation. Econometrica, 59, 817–858.

- Benjamini and Hochberg (1995) Benjamini, Y. and Hochberg, Y. (1995). Controlling the false discovery rate: a practical and powerful approach to multiple testing. Journal of the Royal Statistical Society, B, 57, 289–300.

- Bickel and Levina (2008a) Bickel, P. and Levina, E. (2008a). Regularized estimation of large covariance matrices. The Annals of Statistics, 36, 199–227.

- Bickel and Levina (2008b) Bickel, P. and Levina, E. (2008b). Covariance regularization by thresholding. The Annals of Statistics, 36, 2577–2604.

- Bühlmann and van de Geer (2011) Bühlmann, P. and van de Geer, S. (2011). Statistics for High-Dimensional Data: Methods, Theory and Applications. Springer, Heidelberg.

- Cai et al. (2011) Cai, T. T., Liu, W. and Luo, X. (2011). A constrained minimization approach to sparse precision matrix estimation. Journal of the American Statistical Association, 106, 594–607.

- Cai et al. (2013) Cai, T. T., Liu, W. and Xia, Y. (2013). Two-sample covariance matrix testing and support recovery in high-dimensional and sparse settings. Journal of the American Statistical Association, 108, 265–277.

- Candes and Tao (2007) Candes, E. and Tao, T. (2007). The Dantzig selector: Statistical estimation when is much larger than . The Annals of Statistics, 35, 2313–2351.

- Carrasco and Chen (2002) Carrasco, M. and Chen, X. (2002). Mixing and moment properties of various GARCH and stochastic volatility models. Econometric Theory, 18, 17–39.

- Chang et al. (2015) Chang, J., Chen, S. X. and Chen, X. (2015). High dimensional generalized empirical likelihood for moment restrictions with dependent data. Journal of Econometrics, 185, 283–304.

- Chang et al. (2018) Chang, J., Guo, B. and Yao, Q. (2018). Principal component analysis for second-order stationary vector time series. The Annals of Statistics, in press.

- Chang et al. (2013) Chang, J., Tang, C. Y. and Wu, Y. (2013). Marginal empirical likelihood and sure independence feature screening. The Annals of Statistics, 41, 2123–2148.

- Chang et al. (2017a) Chang, J., Zheng, C., Zhou, W.-X. and Zhou, W. (2017a). Simulation-based hypothesis testing of high dimensional means under covariance heterogeneity. Biometrics, 73, 1300–1310.

- Chang et al. (2017b) Chang, J., Zhou, W., Zhou, W.-X. and Wang, L. (2017b). Comparing large covariance matrices under weak conditions on the dependence structure and its application to gene clustering. Biometrics, 73, 31–41.

- Chen and Zheng (2009) Chen, L. and Zheng, S. (2009). Studying alternative splicing regulatory networks through partial correlation analysis. Genome biology, 10, R3.

- Chen et al. (2013) Chen, X., Xu, M. and Wu, W. B. (2013). Covariance and precision matrix estimation for high-dimensional time series. The Annals of Statistics, 41, 2994–3021.

- Chernozhukov et al. (2013) Chernozhukov, V., Chetverikov, D. and Kato, K. (2013). Gaussian approximations and multiplier bootstrap for maxima of sums of high-dimensional random vectors. The Annals of Statistics, 41, 2786–2819.

- Chernozhukov et al. (2014) Chernozhukov, V., Chetverikov, D. and Kato, K. (2014). Testing many moment inequalities. arXiv:1312.7614.

- Chernozhukov et al. (2015) Chernozhukov, V., Chetverikov, D. and Kato, K. (2015). Comparison an anti-concentration bounds for maxima of Gaussian random vectors. Probability Theory and Related Fields, 162, 47–70.

- Davydov (1968) Davydov, Y. A. (1968). Convergence of distributions generated by stationary stochastic processes. Theory of Probability Its Applications, 13, 691–696.

- de la Fuente et al. (2004) de la Fuente, A., Bing, N., Hoeschele, I. and Mendes, P. (2004). Discovery of meaningful associations in genomic data using partial correlation coefficients. Bioinformatics, 20, 3565–3574.

- den Haan and Levin (1997) den Haan, W. J. and Levin, A. (1997). A practitioner’s guide to robust covariance matrix estimation, Handbook of Statistics 15, Chapter 12, 291–341.

- Fan and Yao (2003) Fan, J. and Yao, Q. (2003). Nonlinear Time Series. Springer, New York.

- Friedman et al. (2008) Friedman, J., Hastie, T. and Tibshirani, R. (2008). Sparse inverse covariance estimation with the graphical lasso. Biostatistics, 9, 432–441.

- Huang et al. (2017) Huang, D., Yao, Q. and Zhang, R. (2017). Krigings over space and time based on latent low-dimensional structures. A preprint.

- Huang et al. (2010) Huang, S., Li, J., Sun, L., Liu, J., Wu, T., Chen, K. and Reiman, E. (2010). Learning brain connectivity of Alzheimer’s disease by sparse inverse covariance estimation. Neuroimage, 50, 935–949.

- Hochberg and Tamhane (2009) Hochberg, Y. and Tamhane, A. C. (2009). Multiple Comparison Procedures. Wiley, New York.

- Kenett et al. (2010) Kenett, D. Y., Tumminello, M., Madi, A., Gur-Gershgoren, G., Mantegna, R. N. and Ben-Jacob, E. (2010). Dominating clasp of the financial sector revealed by partial correlation analysis of the stock market. PloS One, 5, e15032.

- Kiefer et al. (2000) Kiefer, N. M., Vogelsang, T. J. and Bunzel, H. (2000). Simple roubust testing of regression hypothesis. Econometrica, 68, 695–714.

- Lahiri (2003) Lahiri, S. N. (2003). Resampling Methods for Dependent Data. Springer, Berlin.

- Liu (2013) Liu, W. (2013). Gaussian graphical model estimation with false discovery rate control. The Annals of Statistics, 41, 2948–2978.

- Meinshausen and Bühlmann (2006) Meinshausen, N. and Bühlmann, P. (2006). High-dimensional graphs and variable selection with the Lasso. The Annals of Statistics, 34, 1436–1462.

- Merlevède et al. (2011) Merlevède, F., Peligrad, M. and Rio, E. (2011). A Bernstein type inequality and moderate deviations for weakly dependent sequences. Probability Theory and Related Fields, 151, 435–474.

- Nordman and Lahiri (2005) Nordman, D. J. and Lahiri, S. N. (2005). Validity of sampling window method for linear long-range dependent processes. Econometric Theory, 21, 1087–1111.

- Peng et al. (2009) Peng, J., Wang, P., Zhou, N. and Zhu, J. (2009). Partial correlation estimation by joint sparse regression models. Journal of the American Statistical Association, 104, 735–746.

- Qiu and Chen (2012) Qiu, Y. and Chen, S. X. (2012). Test for bandedness of high-dimensional covariance matrices and bandwidth estimation. The Annals of Statistics, 40, 1285–1314.

- Reavis (2012) Reavis, C. (2012). The global financial crisis of 2008: The role of greed, fear, and oligarchs. MIT Sloan Management Review, 16, 1–22.

- Ren et al. (2015) Ren, Z., Sun, T., Zhang, C. H. and Zhou, H. (2015). Asymptotic normality and optimalities in estimation of large Gaussian graphical models. The Annals of Statistics, 43, 991–1026.

- Reverter and Chan (2008) Reverter, A. and Chan, E. K. F. (2008). Combining partial correlation and an information theory approach to the reversed engineering of gene co-expression networks. Bioinformatics, 24, 2491–2497.

- Schweitzer et al. (2009) Schweitzer, F., Fagiolo, G., Sornette, D., Vega-Redondo, F., Vespignani, A. and White, D. R. (2009). Economic networks: The new challenges. Science, 325, 422–425.

- Shapira et al. (2009) Shapira, Y., Kenett, D. Y. and Ben-Jacob, E. (2009). The index cohesive effect on stock market correlations. The European Physical Journal B-Condensed Matter and Complex Systems, 72, 657–669.

- Sun and Zhang (2012) Sun, T. and Zhang, C. H. (2012). Scaled sparse linear regression. Biometrika, 99, 879–898.

- Sun and Zhang (2013) Sun, T. and Zhang, C. H. (2013). Sparse matrix inversion with scaled Lasso. Journal of Machine Learning Research, 14, 3385–3418.

- Tibshirani (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the Lasso. Journal of the Royal Statistical Society, B, 58, 267–288.

- van de Geer et al. (2014) van de Geer, S., Bühlmann, P., Ritov, Y. and Dezeure, R. (2014). On asymptotically optimal confidence regions and tests for high-dimensional models. The Annals of Statistics, 42, 1166–1202.

- Xue and Zou (2012) Xue, L. and Zou, H. (2012). Regularized rank-based estimation of high-dimensional nonparanormal graphical models. The Annals of Statistics, 40, 2541–2571.

- Yuan and Lin (2007) Yuan, M. and Lin, Y. (2007). Model selection and estimation in the Gaussian graphical model. Biometrika, 94, 19–35.

| Covariance Structure | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| KMB | SKMB | KMB | SKMB | KMB | SKMB | KMB | SKMB | |||

| A | 0.925 | 0.963(0.013) | 0.919(0.005) | 0.885(0.022) | 0.906(0.007) | 0.954(0.011) | 0.939(0.004) | 0.915(0.014) | 0.937(0.004) | |

| 0 | 0.950 | 0.978(0.008) | 0.949(0.007) | 0.913(0.016) | 0.941(0.007) | 0.972(0.007) | 0.956(0.002) | 0.941(0.011) | 0.954(0.002) | |

| 0.975 | 0.991(0.004) | 0.978(0.003) | 0.950(0.014) | 0.976(0.003) | 0.985(0.003) | 0.982(0.002) | 0.963(0.006) | 0.981(0.002) | ||

| 0.925 | 0.950(0.014) | 0.888(0.014) | 0.835(0.029) | 0.875(0.014) | 0.955(0.012) | 0.920(0.009) | 0.890(0.019) | 0.916(0.010) | ||

| 0.3 | 0.950 | 0.967(0.010) | 0.930(0.008) | 0.876(0.025) | 0.920(0.009) | 0.973(0.007) | 0.956(0.005) | 0.924(0.013) | 0.952(0.006) | |

| 0.975 | 0.987(0.006) | 0.966(0.004) | 0.923(0.017) | 0.958(0.005) | 0.987(0.004) | 0.979(0.003) | 0.956(0.010) | 0.978(0.003) | ||

| B | 0.925 | 0.953(0.016) | 0.927(0.005) | 0.812(0.036) | 0.874(0.008) | 0.950(0.009) | 0.931(0.003) | 0.894(0.014) | 0.917(0.004) | |

| 0 | 0.950 | 0.973(0.010) | 0.957(0.005) | 0.863(0.028) | 0.918(0.007) | 0.969(0.008) | 0.956(0.006) | 0.925(0.013) | 0.947(0.007) | |

| 0.975 | 0.986(0.004) | 0.979(0.002) | 0.918(0.020) | 0.965(0.004) | 0.989(0.004) | 0.981(0.004) | 0.961(0.008) | 0.978(0.004) | ||

| 0.925 | 0.950(0.019) | 0.898(0.011) | 0.772(0.039) | 0.815(0.018) | 0.950(0.011) | 0.933(0.005) | 0.880(0.017) | 0.915(0.007) | ||

| 0.3 | 0.950 | 0.971(0.011) | 0.930(0.007) | 0.826(0.031) | 0.873(0.012) | 0.968(0.007) | 0.956(0.003) | 0.913(0.012) | 0.943(0.004) | |

| 0.975 | 0.987(0.004) | 0.970(0.005) | 0.885(0.021) | 0.938(0.008) | 0.985(0.004) | 0.972(0.003) | 0.943(0.010) | 0.964(0.004) | ||

| Covariance Structure | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| KMB | SKMB | KMB | SKMB | KMB | SKMB | KMB | SKMB | |||

| A | 0.925 | 0.967(0.006) | 0.891(0.010) | 0.872(0.017) | 0.873(0.009) | 0.971(0.003) | 0.935(0.003) | 0.924(0.008) | 0.799(0.003) | |

| 0 | 0.950 | 0.978(0.004) | 0.934(0.007) | 0.903(0.011) | 0.923(0.009) | 0.977(0.002) | 0.954(0.002) | 0.939(0.006) | 0.822(0.004) | |

| 0.975 | 0.987(0.003) | 0.975(0.003) | 0.933(0.012) | 0.968(0.004) | 0.983(0.002) | 0.977(0.002) | 0.956(0.004) | 0.856(0.004) | ||

| 0.925 | 0.961(0.010) | 0.871(0.010) | 0.786(0.027) | 0.833(0.011) | 0.973(0.004) | 0.937(0.005) | 0.867(0.011) | 0.905(0.007) | ||

| 0.3 | 0.950 | 0.979(0.006) | 0.918(0.010) | 0.842(0.021) | 0.890(0.011) | 0.982(0.004) | 0.959(0.003) | 0.899(0.011) | 0.934(0.004) | |

| 0.975 | 0.991(0.004) | 0.966(0.005) | 0.890(0.014) | 0.949(0.006) | 0.991(0.001) | 0.973(0.003) | 0.936(0.007) | 0.950(0.003) | ||

| B | 0.925 | 0.961(0.007) | 0.884(0.009) | 0.713(0.027) | 0.746(0.015) | 0.966(0.006) | 0.921(0.005) | 0.884(0.011) | 0.814(0.007) | |

| 0 | 0.950 | 0.974(0.004) | 0.934(0.008) | 0.780(0.030) | 0.831(0.015) | 0.980(0.003) | 0.938(0.004) | 0.915(0.009) | 0.840(0.006) | |

| 0.975 | 0.985(0.003) | 0.974(0.004) | 0.869(0.019) | 0.912(0.010) | 0.988(0.002) | 0.970(0.003) | 0.952(0.006) | 0.887(0.007) | ||

| 0.925 | 0.954(0.007) | 0.856(0.014) | 0.641(0.034) | 0.673(0.019) | 0.964(0.005) | 0.928(0.004) | 0.853(0.016) | 0.850(0.007) | ||

| 0.3 | 0.950 | 0.968(0.006) | 0.908(0.008) | 0.716(0.036) | 0.767(0.018) | 0.979(0.004) | 0.950(0.003) | 0.900(0.012) | 0.889(0.006) | |

| 0.975 | 0.983(0.004) | 0.954(0.005) | 0.821(0.028) | 0.878(0.014) | 0.988(0.002) | 0.971(0.002) | 0.940(0.010) | 0.925(0.005) | ||

| Covariance Structure | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| KMB | SKMB | KMB | SKMB | KMB | SKMB | KMB | SKMB | |||

| A | 0.925 | 0.976(0.005) | 0.854(0.013) | 0.826(0.017) | 0.834(0.013) | 0.979(0.002) | 0.959(0.003) | 0.913(0.009) | 0.948(0.004) | |

| 0 | 0.950 | 0.987(0.003) | 0.908(0.010) | 0.866(0.011) | 0.892(0.010) | 0.991(0.002) | 0.974(0.001) | 0.945(0.007) | 0.963(0.001) | |

| 0.975 | 0.991(0.002) | 0.954(0.005) | 0.903(0.009) | 0.944(0.006) | 0.997(0.001) | 0.987(0.003) | 0.967(0.003) | 0.979(0.003) | ||

| 0.925 | 0.967(0.010) | 0.823(0.013) | 0.674(0.031) | 0.758(0.016) | 0.981(0.002) | 0.951(0.004) | 0.822(0.011) | 0.933(0.004) | ||

| 0.3 | 0.950 | 0.983(0.004) | 0.887(0.011) | 0.754(0.030) | 0.840(0.012) | 0.987(0.002) | 0.972(0.004) | 0.861(0.012) | 0.958(0.005) | |

| 0.975 | 0.994(0.002) | 0.952(0.010) | 0.841(0.019) | 0.922(0.011) | 0.996(0.001) | 0.988(0.002) | 0.926(0.010) | 0.978(0.003) | ||

| B | 0.925 | 0.964(0.008) | 0.852(0.013) | 0.638(0.031) | 0.631(0.019) | 0.973(0.004) | 0.944(0.005) | 0.882(0.010) | 0.912(0.006) | |

| 0 | 0.950 | 0.981(0.004) | 0.915(0.008) | 0.729(0.031) | 0.738(0.021) | 0.987(0.003) | 0.967(0.003) | 0.915(0.009) | 0.946(0.004) | |

| 0.975 | 0.991(0.002) | 0.961(0.007) | 0.831(0.017) | 0.860(0.015) | 0.995(0.001) | 0.984(0.001) | 0.952(0.006) | 0.968(0.003) | ||

| 0.925 | 0.958(0.008) | 0.781(0.025) | 0.528(0.047) | 0.417(0.031) | 0.978(0.003) | 0.930(0.006) | 0.813(0.015) | 0.867(0.010) | ||

| 0.3 | 0.950 | 0.977(0.006) | 0.870(0.009) | 0.643(0.040) | 0.564(0.023) | 0.985(0.002) | 0.956(0.005) | 0.866(0.013) | 0.912(0.009) | |

| 0.975 | 0.989(0.002) | 0.939(0.007) | 0.787(0.031) | 0.737(0.023) | 0.997(0.001) | 0.980(0.002) | 0.932(0.011) | 0.954(0.005) | ||

| Stock Symbols | Sectors | Sector No. | Sub Industries | Industry No. |

| IPG | Consumer Discretionary | 1 | Advertising | 1 |

| ANF, COH, NKE, TIF, VFC | Consumer Discretionary | 1 | Apparel, Accessories & Luxury Goods | 2 |

| F, HOG, JCI | Consumer Discretionary | 1 | Auto Parts & Equipment | 3 |

| CBS, CMCSA, DIS, DTV, TWC, TWX | Consumer Discretionary | 1 | Broadcasting & Cable TV | 4 |

| IGT, WYNN | Consumer Discretionary | 1 | Casinos & Gaming | 5 |

| JCP, JWN, KSS, M | Consumer Discretionary | 1 | Department Stores | 6 |

| APOL, DV | Consumer Discretionary | 1 | Educational Services | 7 |

| DHI, KBH, LEN, LOW, PHM | Consumer Discretionary | 1 | Homebuilding | 8 |

| EXPE, HOT, MAR, WYN | Consumer Discretionary | 1 | Hotels, Resorts & Cruise Lines | 9 |

| BDK, NWL, SNA, SWK, WHR | Consumer Discretionary | 1 | Household Appliances | 10 |

| AMZN | Consumer Discretionary | 1 | Internet Retail | 11 |

| HAS, MAT, ODP, RRD | Consumer Discretionary | 1 | Printing Services | 12 |

| GCI, MDP, NYT | Consumer Discretionary | 1 | Publishing | 13 |

| DRI, SBUX, YUM | Consumer Discretionary | 1 | Restaurants | 14 |

| AN, AZO, BBBY, GPC, GPS, HAR, LTD, SPLS | Consumer Discretionary | 1 | Specialty Stores | 15 |

| FPL, WPO | Consumer Discretionary | 1 | NA | NA |

| ADM | Consumer Staples | 2 | Agricultural Products | 16 |

| CVS, SVU, SWY, WAG | Consumer Staples | 2 | Food & Drug Stores | 17 |

| AVP, CL, KMB | Consumer Staples | 2 | Household Products | 18 |

| TGT, FDO, WMT | Consumer Staples | 2 | Hypermarkets & Super Centers | 19 |

| CAG, CCE, CPB, DF, GIS, HNZ, HRL, HSY, K, KFT, | Consumer Staples | 2 | Packaged Food | 20 |

| KO, MKC, PBG, PEP, SJM, SLE, STZ, TAP, TSN | ||||

| EL, PG | Consumer Staples | 2 | Personal Products | 21 |

| MO, RAI | Consumer Staples | 2 | Tobacco | 22 |

| BTU, CNX, MEE | Energy | 3 | Coal Operations | 23 |

| APA, CHK, COG, COP, CTX, CVX, DNR, DO, DVN, | Energy | 3 | Oil & Gas Exploration & Production | 24 |

| EOG, EP, EQT, ESV, FO, HES, MRO, MUR, NBL, | ||||

| OXY, PXD, RRC, SE, SWN, TSO, VLO, WMB, XTO | ||||

| BHI, BJS, CAM, FTI, NBR, NOV, RDC, SII, SLB | Energy | 3 | Oil & Gas Equipment & Services | 25 |

| BAC, BBT, BK, C, CIT, CMA, COF, FHN, FITB, | Financials | 4 | Banks | 26 |

| HCBK, HRB, IVZ, KEY, LM, MI, MTB, NTRS, PNC, | ||||

| SLM, STI, USB, WFC | ||||

| CME, EFX, ICE, NYX, PFG, PRU, RF, STT, TROW, | Financials | 4 | Diversified Financial Services | 27 |

| UNM, VTR | ||||

| ETFC, FII, JNS, LUK, MS, SCHW | Financials | 4 | Investment Banking & Brokerage | 28 |

| AFL, AIG, AIZ, CB, CINF, GNW, HIG, L, LNC, | Financials | 4 | Property & Casualty Insurance | 29 |

| MBI, MET, MMC, PGR, TMK, TRV, XL | ||||

| AMT, AVB, BXP, CBG, HCN, HCP, HST, IRM, | Financials | 4 | REITs | 30 |

| KIM, PBCT, PCL, PSA, SPG, VNO, WY |

| Stock Symbols | Sectors | Sector No. | Sub Industries | Industry No. |

| AOC | Financials | 4 | NA | NA |

| AMGN, BIIB, CELG, FRX, GENZ, GILD, HSP, | Health Care | 5 | Pharmaceuticals | 31 |

| KG, LIFE, LLY, MRK, MYL, WPI | ||||

| ABC, AET, BMY, CAH, CI, DGX, DVA, ESRX, HUM, | Health Care | 5 | Health Care Supplies | 32 |

| MCK, MHS, PDCO, THC, UNH, WAT, WLP, XRAY | ||||

| ABT, BAX, BCR, BDX, ISRG, JNJ, MDT, MIL, | Health Care | 5 | Health Care Equipment & Services | 33 |

| PKI, PLL, STJ, SYK, TMO, VAR | ||||

| BA, RTN | Industrials | 6 | Aerospace & Defense | 34 |

| CHRW, EXPD, FDX, UPS | Industrials | 6 | Air Freight & Logistics | 35 |

| LUV | Industrials | 6 | Airlines | 36 |

| DE, FAST, GLW, MAS, MTW, PCAR | Industrials | 6 | Construction & Farm Machinery & Heavy Trucks | 37 |

| COL, EMR, ETN, GE, HON, IR, JEC, LEG, | Industrials | 6 | Industrial Conglomerates | 38 |

| LLL, MMM, PH, ROK, RSG, TXT, TYC | ||||

| CMI, DHR, DOV, FLS, GWW, ITT, ITW | Industrials | 6 | Industrial Machinery | 39 |

| CSX, NSC, UNP | Industrials | 6 | Railroads | 40 |

| ACS, CTAS, FLR, RHI | Industrials | 6 | NA | NA |

| CBE, MOLX, JBL, LXK | Information Technology | 7 | Office Electronics | 41 |

| ADBE, ADSK, BMC, CA, ERTS, MFE, MSFT, NOVL, | Information Technology | 7 | Application Software | 42 |

| ORCL, TDC | ||||

| CIEN, HRS, JDSU, JNPR, MOT | Information Technology | 7 | Communications Equipment | 43 |

| AAPL, AMD, HPQ, JAVA, QLGC, SNDK | Information Technology | 7 | Computer Storage & Peripherals | 44 |

| ADP, AKAM, CRM, CSC, CTSH, CTXS, CVG, EBAY, | Information Technology | 7 | Information Services | 45 |

| FIS, GOOG, IBM, INTU, MA, MWW, PAYX, TSS, | ||||

| XRX, YHOO, DNB | ||||

| ALTR, AMAT, BRCM, INTC, KLAC, LLTC, LSI, MCHP, | Information Technology | 7 | Semiconductors | 46 |

| MU, NSM, NVDA, NVLS, QCOM, TXN, XLNX | ||||

| ATI, BLL, FCX, NEM, OI | Materials | 8 | Metal & Glass Containers | 47 |

| DD, DOW, ECL, EMN, IFF, MON, PPG, PX, SHW, SIAL | Materials | 8 | Specialty Chemicals | 48 |

| BMS, MWV, PTV | Materials | 8 | Containers & Packaging | 49 |

| AKS, TIE, X | Materials | 8 | Iron & Steel | 50 |

| AVY, IP, SEE | Materials | 8 | Paper Packaging | 51 |

| VMC | Materials | 8 | NA | NA |

| CTL, EQ, FTR, Q, S, T, VZ, WIN | Telecommunications Services | 9 | Telecom Carriers | 52 |

| AEE, AEP, AES, AYE, CMS, CNP, D, DYN, ETR, | Utilities | 10 | MultiUtilities | 53 |

| FE, PEG, POM, PPL, SCG, SO, SRE, TE, WEC, XEL | ||||

| STR, TEG | Utilities | 10 | Utility Networks | 54 |

| RX | NA | NA | NA | NA |

| Sectors | 2005 | 2008 | ||

|---|---|---|---|---|

| Within | Between | Within | Between | |

| Consumer Discretionary | 13 | 37 | 9 | 12 |

| Consumer Staples | 4 | 16 | 1 | 6 |

| Energy | 0 | 8 | 1 | 4 |

| Financials | 3 | 14 | 5 | 5 |

| Health Care | 2 | 10 | 2 | 8 |

| Industrials | 5 | 19 | 3 | 5 |

| Information Technology | 5 | 13 | 6 | 9 |

| Materials | 2 | 12 | 2 | 10 |

| Telecommunication Services | 0 | 3 | 0 | 1 |

| Utilities | 0 | 4 | 1 | 2 |