Regret Lower Bound and Optimal Algorithm in Finite Stochastic Partial Monitoring

Abstract

Partial monitoring is a general model for sequential learning with limited feedback formalized as a game between two players. In this game, the learner chooses an action and at the same time the opponent chooses an outcome, then the learner suffers a loss and receives a feedback signal. The goal of the learner is to minimize the total loss. In this paper, we study partial monitoring with finite actions and stochastic outcomes. We derive a logarithmic distribution-dependent regret lower bound that defines the hardness of the problem. Inspired by the DMED algorithm (Honda and Takemura, 2010) for the multi-armed bandit problem, we propose PM-DMED, an algorithm that minimizes the distribution-dependent regret. PM-DMED significantly outperforms state-of-the-art algorithms in numerical experiments. To show the optimality of PM-DMED with respect to the regret bound, we slightly modify the algorithm by introducing a hinge function (PM-DMED-Hinge). Then, we derive an asymptotically optimal regret upper bound of PM-DMED-Hinge that matches the lower bound.

1 Introduction

Partial monitoring is a general framework for sequential decision making problems with imperfect feedback. Many classes of problems, including prediction with expert advice [1], the multi-armed bandit problem [2], dynamic pricing [3], the dark pool problem [4], label efficient prediction [5], and linear and convex optimization with full or bandit feedback [6, 7] can be modeled as an instance of partial monitoring.

Partial monitoring is formalized as a repeated game played by two players called a learner and an opponent. At each round, the learner chooses an action, and at the same time the opponent chooses an outcome. Then, the learner observes a feedback signal from a given set of symbols and suffers some loss, both of which are deterministic functions of the selected action and outcome.

The goal of the learner is to find the optimal action that minimizes his/her cumulative loss. Alternatively, we can define the regret as the difference between the cumulative losses of the learner and the single optimal action, and minimization of the loss is equivalent to minimization of the regret. A learner with a small regret balances exploration (acquisition of information about the strategy of the opponent) and exploitation (utilization of information). The rate of regret indicates how fast the learner adapts to the problem: a linear regret indicates the inability of the learner to find the optimal action, whereas a sublinear regret indicates that the learner can approach the optimal action given sufficiently large time steps.

The study of partial monitoring is classified into two settings with respect to the assumption on the outcomes. On one hand, in the stochastic setting, the opponent chooses an outcome distribution before the game starts, and an outcome at each round is an i.i.d. sample from the distribution. On the other hand, in the adversarial setting, the opponent chooses the outcomes to maximize the regret of the learner. In this paper, we study the former setting.

1.1 Related work

The paper by Piccolboni and Schindelhauer [8] is one of the first to study the regret of the finite partial monitoring problem. They proposed the FeedExp3 algorithm, which attains minimax regret on some problems. This bound was later improved by Cesa-Bianchi et al. [9] to , who also showed an instance in which the bound is optimal. Since then, most literature on partial monitoring has dealt with the minimax regret, which is the worst-case regret over all possible opponent’s strategies. Bartók et al. [10] classified the partial monitoring problems into four categories in terms of the minimax regret: a trivial problem with zero regret, an easy problem with regret111Note that ignores a polylog factor., a hard problem with regret, and a hopeless problem with regret. This shows that the class of the partial monitoring problems is not limited to the bandit sort but also includes larger classes of problems, such as dynamic pricing. Since then, several algorithms with a regret bound for easy problems have been proposed [11, 12, 13]. Among them, the Bayes-update Partial Monitoring (BPM) algorithm [13] is state-of-the-art in the sense of empirical performance.

Distribution-dependent and minimax regret: we focus on the distribution-dependent regret that depends on the strategy of the opponent. While the minimax regret in partial monitoring has been extensively studied, little has been known on distribution-dependent regret in partial monitoring. To the authors’ knowledge, the only paper focusing on the distribution-dependent regret in finite discrete partial monitoring is the one by Bartók et al. [11], which derived distribution-dependent regret for easy problems. In contrast to this situation, much more interest in the distribution-dependent regret has been shown in the field of multi-armed bandit problems. Upper confidence bound (UCB), the most well-known algorithm for the multi-armed bandits, has a distribution-dependent regret bound [2, 14], and algorithms that minimize the distribution-dependent regret (e.g., KL-UCB) has been shown to perform better than ones that minimize the minimax regret (e.g., MOSS), even in instances in which the distributions are hard to distinguish (e.g., Scenario 2 in Garivier et al. [15]). Therefore, in the field of partial monitoring, we can expect that an algorithm that minimizes the distribution-dependent regret would perform better than the existing ones.

Contribution: the contributions of this paper lie in the following three aspects. First, we derive the regret lower bound: in some special classes of partial monitoring (e.g., multi-armed bandits), an regret lower bound is known to be achievable. In this paper, we further extend this lower bound to obtain a regret lower bound for general partial monitoring problems. Second, we propose an algorithm called Partial Monitoring DMED (PM-DMED). We also introduce a slightly modified version of this algorithm (PM-DMED-Hinge) and derive its regret bound. PM-DMED-Hinge is the first algorithm with a logarithmic regret bound for hard problems. Moreover, for both easy and hard problems, it is the first algorithm with the optimal constant factor on the leading logarithmic term. Third, performances of PM-DMED and existing algorithms are compared in numerical experiments. Here, the partial monitoring problems consisted of three specific instances of varying difficulty. In all instances, PM-DMED significantly outperformed the existing methods when a number of rounds is large. The regret of PM-DMED on these problems quickly approached the theoretical lower bound.

2 Problem Setup

This paper studies the finite stochastic partial monitoring problem with actions, outcomes, and symbols. An instance of the partial monitoring game is defined by a loss matrix and a feedback matrix , where . At the beginning, the learner is informed of and . At each round , a learner selects an action , and at the same time an opponent selects an outcome . The learner suffers loss , which he/she cannot observe: the only information the learner receives is the signal . We consider a stochastic opponent whose strategy for selecting outcomes is governed by the opponent’s strategy , where is a set of probability distributions over an -ary outcome. The outcome of each round is an i.i.d. sample from .

The goal of the learner is to minimize the cumulative loss over rounds. Let the optimal action be the one that minimizes the loss in expectation, that is, , where is the -th row of . Assume that is unique. Without loss of generality, we can assume that . Let and be the number of rounds before the -th in which action is selected. The performance of the algorithm is measured by the (pseudo) regret,

which is the difference between the expected loss of the learner and the optimal action . It is easy to see that minimizing the loss is equivalent to minimizing the regret. The expectation of the regret measures the performance of an algorithm that the learner uses.

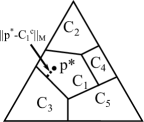

For each action , let be the set of opponent strategies for which action is optimal:

We call the optimality cell of action . Each optimality cell is a convex closed polytope. Furthermore, we call the set of optimality cells the cell decomposition as shown in Figure 1. Let be the set of strategies with which action is not optimal.

The signal matrix of action is defined as , where if is true and otherwise. The signal matrix defined here is slightly different from the one in the previous papers (e.g., Bartók et al. [10]) in which the number of rows of is the number of the different symbols in the -th row of . The advantage in using the definition here is that, is a probability distribution over symbols that the algorithm observes when it selects an action . Examples of signal matrices are shown in Section 5. An instance of partial monitoring is globally observable if for all pairs of actions, . In this paper, we exclusively deal with globally observable instances: in view of the minimax regret, this includes trivial, easy, and hard problems.

3 Regret Lower Bound

A good algorithm should work well against any opponent’s strategy. We extend this idea by introducing the notion of strong consistency: a partial monitoring algorithm is strongly consistent if it satisfies for any and given and .

In the context of the multi-armed bandit problem, Lai and Robbins [2] derived the regret lower bound of a strongly consistent algorithm: an algorithm must select each arm until its number of draws satisfies , where is the KL divergence between the two one-parameter distributions from which the rewards of action and the optimal action are generated. Analogously, in the partial monitoring problem, we can define the minimum number of observations.

Lemma 1.

For sufficiently large , a strongly consistent algorithm satisfies:

where and is the KL divergence between two discrete distributions, in which we define .

Lemma 1 can be interpreted as follows: for each round , consistency requires the algorithm to make sure that the possible risk that action is optimal is smaller than . Large deviation principle [16] states that, the probability that an opponent with strategy behaves like is roughly . Therefore, we need to continue exploration of the actions until holds for any to reduce the risk to .

The proof of Lemma 1 is in Appendix B in the supplementary material. Based on the technique used in Lai and Robbins [2], the proof considers a modified game in which another action is optimal. The difficulty in proving the lower bound in partial monitoring lies in that, the feedback structure can be quite complex: for example, to confirm the superiority of action over , one might need to use the feedback from action . Still, we can derive the lower bound by utilizing the consistency of the algorithm in the original and modified games.

We next derive a lower bound on the regret based on Lemma 1. Note that, the expectation of the regret can be expressed as . Let

where denotes a closure. Moreover, let

the optimal solution of which is

The value is the possible minimum regret for observations such that the minimum divergence of from any is larger than . Using Lemma 1 yields the following regret lower bound:

Theorem 2.

The regret of a strongly consistent algorithm is lower bounded as:

From this theorem, we can naturally measure the harshness of the instance by , whereas the past studies (e.g., Vanchinathan et al. [13]) ambiguously define the harshness as the closeness to the boundary of the cells. Furthermore, we show in Lemma 5 in the Appendix that : the regret bound has at most quadratic dependence on , which is defined in Appendix D as the closeness of to the boundary of the optimal cell.

4 PM-DMED Algorithm

In this section, we describe the partial monitoring deterministic minimum empirical divergence (PM-DMED) algorithm, which is inspired by DMED [17] for solving the multi-armed bandit problem. Let be the empirical distribution of the symbols under the selection of action . Namely, the -th element of is . We sometimes omit from when it is clear from the context. Let the empirical divergence of be , the exponential of which can be considered as a likelihood that is the opponent’s strategy.

The main routine of PM-DMED is in Algorithm 1. At each loop, the actions in the current list are selected once. The list for the actions in the next loop is determined by the subroutine in Algorithm 2. The subroutine checks whether the empirical divergence of each point is larger than or not (Eq. (3)). If it is large enough, it exploits the current information by selecting , the optimal action based on the estimation that minimizes the empirical divergence. Otherwise, it selects the actions with the number of observations below the minimum requirement for making the empirical divergence of each suboptimal point larger than .

Unlike the -armed bandit problem in which a reward is associated with an action, in the partial monitoring problem, actions, outcomes, and feedback signals can be intricately related. Therefore, we need to solve a non-trivial optimization to run PM-DMED. Later in Section 5, we discuss a practical implementation of the optimization.

| (1) |

| (2) |

| (3) |

| (4) |

Necessity of exploration: PM-DMED tries to observe each action to some extent (Eq. (2)), which is necessary for the following reason: consider a four-state game characterized by

The optimal action here is action , which does not yield any useful information. By using action , one receives three kinds of symbols from which one can estimate , , and , where is the -th component of . From this, an algorithm can find that is not very small and thus the expected loss of actions and is larger than that of action . Since the feedback of actions and are the same, one may also use action in the same manner. However, the loss per observation is and for actions and , respectively, and thus it is better to use action . This difference comes from the fact that . Since an algorithm does not know beforehand, it needs to observe action , the only source for distinguishing from . Yet, an optimal algorithm cannot select it more than times because it affects the factor in the regret. In fact, observations of action with some are sufficient to be convinced that with probability . For this reason, PM-DMED selects each action times.

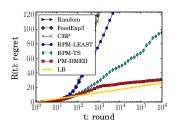

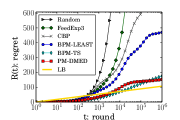

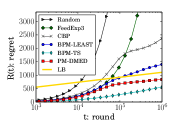

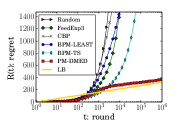

5 Experiment

Following Bartók et al. [11], we compared the performances of algorithms in three different games: the four-state game (Section 4), a three-state game and dynamic pricing. Experiments on the -armed bandit game was also done, and the result is shown in Appendix C.1.

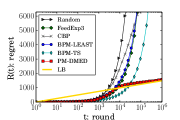

The three-state game, which is classified as easy in terms of the minimax regret, is characterized by:

The signal matrices of this game are,

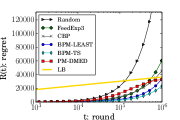

Dynamic pricing, which is classified as hard in terms of the minimax regret, is a game that models a repeated auction between a seller (learner) and a buyer (opponent). At each round, the seller sets a price for a product, and at the same time, the buyer secretly sets a maximum price he is willing to pay. The signal is “buy” or “no-buy”, and the seller’s loss is either a given constant (no-buy) or the difference between the buyer’s and the seller’s prices (buy). The loss and feedback matrices are:

where signals and correspond to no-buy and buy. The signal matrix of action is

Following Bartók et al. [11], we set , and .

In our experiments with the three-state game and dynamic pricing, we tested three settings regarding the harshness of the opponent: at the beginning of a simulation, we sampled 1,000 points uniformly at random from , then sorted them by . We chose the top 10%, 50%, and 90% harshest ones as the opponent’s strategy in the harsh, intermediate, and benign settings, respectively.

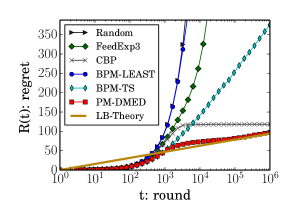

We compared Random, FeedExp3 [8], CBP [11] with , BPM-LEAST, BPM-TS [13], and PM-DMED with . Random is a naive algorithm that selects an action uniformly random. FeedExp3 requires a matrix such that , and thus one cannot apply it to the four-state game. CBP is an algorithm of logarithmic regret for easy games. The parameters and of CBP were set in accordance with Theorem 1 in their paper. BPM-LEAST is a Bayesian algorithm with regret for easy games, and BPM-TS is a heuristic of state-of-the-art performance. The priors of two BPMs were set to be uninformative to avoid a misspecification, as recommended in their paper.

The computation of in (1) and the evaluation of the condition in (3) involve convex optimizations, which were done with Ipopt [18]. Moreover, obtaining in (4) is classified as a linear semi-infinite programming (LSIP) problem, a linear programming (LP) with finitely many variables and infinitely many constraints. Following the optimization of BPM-LEAST [13], we resorted to a finite sample approximation and used the Gurobi LP solver [19] in computing : at each round, we sampled 1,000 points from , and relaxed the constraints on the samples. To speed up the computation, we skipped these optimizations in most rounds with large and used the result of the last computation. The computation of the coefficient of the regret lower bound (Theorem 2) is also an LSIP, which was approximated by 100,000 sample points from .

The experimental results are shown in Figure 2. In the four-state game and the other two games with an easy or intermediate opponent, PM-DMED outperforms the other algorithms when the number of rounds is large. In particular, in the dynamic pricing game with an intermediate opponent, the regret of PM-DMED at is ten times smaller than those of the other algorithms. Even in the harsh setting in which the minimax regret matters, PM-DMED has some advantage over all algorithms except for BPM-TS. With sufficiently large , the slope of an optimal algorithm should converge to LB. In all games and settings, the slope of PM-DMED converges to LB, which is empirical evidence of the optimality of PM-DMED.

6 Theoretical Analysis

| (5) |

| (6) |

| (7) |

| (8) |

| (9) |

| (10) |

Section 5 shows that the empirical performance of PM-DMED is very close to the regret lower bound in Theorem 2. Although the authors conjecture that PM-DMED is optimal, it is hard to analyze PM-DMED. The technically hardest part arises from the case in which the divergence of each action is small but not yet fully converged. To circumvent this difficulty, we can introduce a discount factor. Let

| (11) |

where . Note that in (11) is a natural generalization of in Section 4 in the sense that . Event means that the number of observations is enough to ensure that the “-discounted” empirical divergence of each is larger than . Analogous to , we define

and its optimal solution by

We also define , the optimal region of action with margin. PM-DMED-Hinge shares the main routine of Algorithm 1 with PM-DMED and lists the next actions by Algorithm 3. Unlike PM-DMED, it (i) discounts from the empirical divergence . Moreover, (ii) when is close to the cell boundary, it encourages more exploration to identify the cell it belongs to by Eq. (6).

Theorem 3.

Assume the following regularity conditions hold for . (1) is unique at . Moreover, (2) for , it holds that for all in some neighborhood of , where and denote the closure and the interior, respectively. Then,

We prove this theorem in Appendix D. Recall that is the set of optimal solutions of an LSIP. In this problem, KKT conditions and the duality theorem apply as in the case of finite constraints; thus, we can check whether Condition 1 holds or not for each (see, e.g., Ito et al. [20] and references therein). Condition 2 holds in most cases, and an example of an exceptional case is shown in Appendix A.

Theorem 3 states that PM-DMED-Hinge has a regret upper bound that matches the lower bound of Theorem 2.

Corollary 4.

(Optimality in the -armed bandit problem) In the -armed Bernoulli bandit problem, the regularity conditions in Theorem 3 always hold. Moreover, the coefficient of the leading logarithmic term in the regret bound of the partial monitoring problem is equal to the bound given in Lai and Robbins [2]. Namely, , where is the KL-divergence between Bernoulli distributions.

Corollary 4, which is proven in Appendix C, states that PM-DMED-Hinge attains the optimal regret of the -armed bandit if we run it on an -armed bandit game represented as partial monitoring.

Asymptotic analysis: it is Theorem 6 where we lose the finite-time property. This theorem shows the continuity of the optimal solution set of , which does not mention how close is to if for given . To obtain an explicit bound, we need sensitivity analysis, the theory of the robustness of the optimal value and the solution for small deviations of its parameters (see e.g., Fiacco [21]). In particular, the optimal solution of partial monitoring involves an infinite number of constraints, which makes the analysis quite hard. For this reason, we will not perform a finite-time analysis. Note that, the -armed bandit problem is a special instance in which we can avoid solving the above optimization and a finite-time optimal bound is known.

Necessity of the discount factor: we are not sure whether discount factor in PM-DMED-Hinge is necessary or not. We also empirically tested PM-DMED-Hinge: although it is better than the other algorithms in many settings, such as dynamic pricing with an intermediate opponent, it is far worse than PM-DMED. We found that our implementation, which uses the Ipopt nonlinear optimization solver, was sometimes inaccurate at optimizing (5): there were some cases in which the true satisfies , while the solution we obtained had non-zero hinge values. In this case, the algorithm lists all actions from (7), which degrades performance. Determining whether the discount factor is essential or not is our future work.

Acknowledgements

The authors gratefully acknowledge the advice of Kentaro Minami and sincerely thank the anonymous reviewers for their useful comments. This work was supported in part by JSPS KAKENHI Grant Number 15J09850 and 26106506.

References

- [1] Nick Littlestone and Manfred K. Warmuth. The weighted majority algorithm. Inf. Comput., 108(2):212–261, February 1994.

- [2] T. L. Lai and Herbert Robbins. Asymptotically efficient adaptive allocation rules. Advances in Applied Mathematics, 6(1):4–22, 1985.

- [3] Robert D. Kleinberg and Frank Thomson Leighton. The value of knowing a demand curve: Bounds on regret for online posted-price auctions. In FOCS, pages 594–605, 2003.

- [4] Alekh Agarwal, Peter L. Bartlett, and Max Dama. Optimal allocation strategies for the dark pool problem. In AISTATS, pages 9–16, 2010.

- [5] Nicolò Cesa-Bianchi, Gábor Lugosi, and Gilles Stoltz. Minimizing regret with label efficient prediction. IEEE Transactions on Information Theory, 51(6):2152–2162, 2005.

- [6] Martin Zinkevich. Online convex programming and generalized infinitesimal gradient ascent. In ICML, pages 928–936, 2003.

- [7] Varsha Dani, Thomas P. Hayes, and Sham M. Kakade. Stochastic linear optimization under bandit feedback. In COLT, pages 355–366, 2008.

- [8] Antonio Piccolboni and Christian Schindelhauer. Discrete prediction games with arbitrary feedback and loss. In COLT, pages 208–223, 2001.

- [9] Nicolò Cesa-Bianchi, Gábor Lugosi, and Gilles Stoltz. Regret minimization under partial monitoring. Math. Oper. Res., 31(3):562–580, 2006.

- [10] Gábor Bartók, Dávid Pál, and Csaba Szepesvári. Minimax regret of finite partial-monitoring games in stochastic environments. In COLT, pages 133–154, 2011.

- [11] Gábor Bartók, Navid Zolghadr, and Csaba Szepesvári. An adaptive algorithm for finite stochastic partial monitoring. In ICML, 2012.

- [12] Gábor Bartók. A near-optimal algorithm for finite partial-monitoring games against adversarial opponents. In COLT, pages 696–710, 2013.

- [13] Hastagiri P. Vanchinathan, Gábor Bartók, and Andreas Krause. Efficient partial monitoring with prior information. In NIPS, pages 1691–1699, 2014.

- [14] Peter Auer, Nicoló Cesa-bianchi, and Paul Fischer. Finite-time Analysis of the Multiarmed Bandit Problem. Machine Learning, 47:235–256, 2002.

- [15] Aurélien Garivier and Olivier Cappé. The KL-UCB algorithm for bounded stochastic bandits and beyond. In COLT, pages 359–376, 2011.

- [16] Amir Dembo and Ofer Zeitouni. Large deviations techniques and applications. Applications of mathematics. Springer, New York, Berlin, Heidelberg, 1998.

- [17] Junya Honda and Akimichi Takemura. An Asymptotically Optimal Bandit Algorithm for Bounded Support Models. In COLT, pages 67–79, 2010.

- [18] Andreas Wächter and Carl D. Laird. Interior point optimizer (IPOPT).

- [19] Gurobi Optimization Inc. Gurobi optimizer.

- [20] S. Ito, Y. Liu, and K. L. Teo. A dual parametrization method for convex semi-infinite programming. Annals of Operations Research, 98(1-4):189–213, 2000.

- [21] Anthony V. Fiacco. Introduction to sensitivity and stability analysis in nonlinear programming. Academic Press, New York, 1983.

- [22] T.L. Graves and T.L. Lai. Asymptotically efficient adaptive choice of control laws in controlled Markov chains. SIAM J. Contr. and Opt., 35(3):715–743, 1997.

- [23] Emilie Kaufmann, Olivier Cappé, and Aurélien Garivier. On the complexity of A/B testing. In COLT, pages 461–481, 2014.

- [24] Sébastien Bubeck. Bandits Games and Clustering Foundations. Theses, Université des Sciences et Technologie de Lille - Lille I, June 2010.

- [25] William W. Hogan. Point-to-set maps in mathematical programming. SIAM Review, 15(3):591–603, 1973.

- [26] Thomas M. Cover and Joy A. Thomas. Elements of Information Theory, Second Edition (Wiley Series in Telecommunications and Signal Processing). Wiley-Interscience, 2006.

Appendix A Case in which Condition 2 Does Not Hold

Figure 3 is an example that Theorem 3 does not cover. The dotted line is , which (accidentally) coincides with a line that makes the convex polytope of . In this case, Condition 2 does not hold because whereas (two starred points), which means that a slight modification of changes the set of cells that intersects with the dotted line discontinuously. We exclude these unusual cases for the ease of analysis.

The authors consider that it is quite hard to give the optimal regret bound without such regularity conditions. In fact, many regularity conditions are assumed in Graves and Lai [22], where another generalization of the bandit problem is considered and the regret lower bound is expressed in terms of LSIP. In this paper, the regularity conditions are much simplified by the continuity argument in Theorem 6 but it remains an open problem to fully remove them.

Appendix B Proof: Regret Lower Bound

Proof of Lemma 1.

The technique here is mostly inspired from Theorem 1 in Lai and Robbins [2]. The use of a term is inspired from Kaufmann et al. [23]. Let and be the optimal action under the opponent’s strategy . We consider a modified partial monitoring game with its opponent’s strategy is .

Notation: Let is the signal of the -th observation of action . Let

and . Let and be the probability and the expectation with respect to the modified game, respectively. Then, for any event ,

| (12) |

holds. Now, let us define the following events:

First step (): from (12),

By using this we have

| (13) |

Since this algorithm is strongly consistent, for any . Therefore, the RHS of the last line of (13) is , which, by choosing sufficiently small , converges to zero as . In summary, .

Second step (): we have

Note that

is the maximum of the sum of positive-mean random variables, and thus converges to is average (c.f., Lemma 10.5 in [24]). Namely,

almost surely. Therefore,

almost surely. By using this fact and , we have

In summary, we obtain .

Last step: we here have

where we used the fact that for in the last line. Note that, by using the result of the previous steps, . By using the complementary of this fact,

Using the Markov inequality yields

| (14) |

Because is subpolynomial as a function of due to the consistency, the second term in LHS of (14) is and thus negligible. Lemma 1 follows from the fact that (14) holds for sufficiently small and arbitrary . ∎

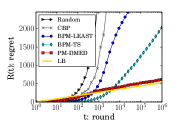

Appendix C The -armed Bandit Problem as Partial Monitoring

In Section 6, we have introduced PM-DMED-Hinge, an asymptotically optimal algorithm for partial monitoring. In this appendix, we prove that this algorithm also has an optimal regret bound of the -armed bandit problem when we run it on an -armed bandit game represented as an instance of partial monitoring.

In the -armed bandit problem, the learner selects one of actions (arms) and receives a corresponding reward. This problem can be considered as a special case of partial monitoring in which the learner directly observes the loss matrix. For example, three-armed Bernoulli bandit can be represented by the following loss and feedback matrices, and the strategy:

| (15) |

where , and are the expected rewards of the actions. Signals and correspond to the rewards of and generated by the selected arm, respectively. More generally, -armed Bernoulli bandit is represented as an instance of partial monitoring in which the loss and feedback matrices are the same matrix

where mod denotes the modulo operation. This problem is associated with parameters that correspond to the expected rewards of the actions. For the ease of analysis, we assume are in and different from each other. Without loss of generality, we assume , and thus action is the optimal action. The opponent’s strategy is

Note that .

Proof of Corollary 4.

In the following, we prove that the regularity conditions in Theorem 3 are always satisfied in the case of the -armed bandit. During the proof we also show that is equal to the optimal constant factor of Lai and Robbins [2].

Because signal corresponds to the reward of , we can define , and thus

First, we show the uniqueness of at . It is easy to check

where is the KL divergence between two Bernoulli distributions with parameters and . Then

| (16) |

where the last inequality follows from the fact that

By Eq. (16), the regret minimizing solution is

and

which is unique.

Second, we show that for sufficiently small . Note that,

and

To prove

| (17) |

it suffices to show that, an open ball centered at any position in

contains a point in . This holds because we can make a slight move towards the direction of increasing : we can always find in an open ball centered at such that and because of (i) the fact that there always exists such that for arbitrary and (ii) the continuity of the operator. Therefore, any open ball centered at contains an element of , by which we obtain (17). By using (17), we have

| (18) |

where we used the fact that . Combining (18) with the fact that yields .

Therefore, in the -armed Bernoulli bandit problem, the regularity conditions are always satisfied and matches the optimal coefficient of the logarithmic regret bound. From Theorem 3, if we run PM-DMED-Hinge in this game, its expected regret is asymptotically optimal in view of the -armed bandit problem. ∎

C.1 Experiment

We also assessed the performance of PM-DMED and other algorithms in solving the three-armed Bernoulli bandit game defined by (15) with parameters , , and . The settings of the algorithms are the same as that of the main paper. The results of simulations are shown in Figure 4. LB-Theory is the regret lower bound of Lai and Robbins [2], that is, . The slope of PM-DMED quickly approaches that of LB-Theory, which is empirical evidence that PM-DMED has optimal performance in -armed bandits.

Appendix D Optimality of PM-DMED-Hinge

In this appendix we prove Theorem 3. First we define distances among distributions. For distributions of symbols we use the total variation distance

For distributions of outcomes, we identify with the set and define

For we define

In the following, we use Pinsker’s inequality given below many times.

Let

Note that these two constants are positive from the global observability.

D.1 Properties of regret lower bound

In this section, we give Lemma 5 and Theorem 6 that are about the functions and . In the following, we always consider these functions on , and , where denotes the support of the distribution.

We define

Lemma 5.

Let and be satisfying and for all . Then

| (19) |

Furtheremore, is nonempty and

Proof of Lemma 5.

Since , there exists for any such that

For this we have

Thus, by letting for all we have

which implies (19). On the other hand it holds for any from that

and therefore we have

∎

Theorem 6.

Assume that the regularity conditions in Theorem 3 hold. Then the point-to-set map is (i) nonempty near and (ii) continuous at .

See Hogan [25] for definitions of terms such as continuity of point-to-set maps.

Proof of Theorem 6.

Define

for

Note that for . From Lemma 5, near ,

and

hold. Since the function

is continuous in , is a closed set and therefore is nonempty near .

From the continuity of at any such that , we have

Thus, we have

| (20) |

Since the objective function is continuous in and , and (20) is compact, now it suffices to show that (20) is continuous in at to prove the theorem from [25, Corollary 8.1].

First we show that is closed at . Consider for a sequence which converges to as . We show that if as .

Take an arbitrary such that . Since and , there exists such that and . Thus, from , it holds for sufficiently large that . For this we have

that is, . Therefore for sufficiently large we have

and, letting ,

This means that , that is, is closed at .

Next we show that is open at . Consider and a sequence which converges to as . We show that there exists a sequence such that .

Consider the optimal value function

| (21) |

Since the feasible region of (21) is closed at and the objective function of (21) is lower semicontinuous in we see that is lower semicontinuous from [25, Theorem 2]. Therefore, for any there exists such that for all

since from . Thus, by letting we have

that is, . ∎

D.2 Regret analysis of PM-DMED-Hinge

Let be the empirical distribution of the symbols from the action when the action is selected times. Then we have . Let . Then, from the large deviation bound on discrete distributions (Theorem 11.2.1 in Cover and Thomas [26]), we have

| (22) |

We also define

For

| (23) |

define events

| (24) | ||||

where we write instead of for events and .

Proof of theorem 3.

Since , the whole sample space is covered by

| (25) | ||||

Let denote the event that action is newly added into the list at the -th round and denote the event that occurred by Step 6 of Algorithm 3. Note that if occurred then is equivalent to . Combining this fact with (25) we can bound the regret as

The following Lemmas 7–13 bound the expectation of each term and complete the proof. ∎

Lemma 7.

Let be the unique member of . Then there exists such that and for all

Lemma 8.

Lemma 9.

Lemma 10.

Lemma 11.

Lemma 12.

Lemma 13.

Proof of Lemma 7.

From we have

| (26) |

Here assume that . Then

which contradicts (26) and we obtain . Furthermore, from and we have

respectively. Since is continuous at from Theorem 6, for all where is the unique member of and we used the fact that implies .

We complete the proof by

∎

Proof of Lemma 8.

Proof of Lemma 9.

Let and be arbitrary. Consider the case that

| (28) |

for some . Then under events and we have

which implies that the condition (9) is satisfied. On the other hand from (10), satisfies

| (29) |

Eqs. (28) and (29) imply that there exists at least one such that . This action is selected within rounds and therefore never holds for all . Thus, under the condition (28) it holds that

By using this inequality we have

| (30) | ||||

Proof of Lemma 10.

Because , and imply

and imply

On the other hand, event occurs for at most twice since all actions are put into the list if occurred. Thus, we have

∎

Proof of Lemma 11.

On the other hand, occurs for at most twice since is put into the list under this event. Thus, we have

∎

Proof of Lemma 12.

implies

and therefore

Note that occurs for at most twice because all actions are put into the list if occurred. Thus, we have

∎