Kriging Metamodels and Experimental Design for Bermudan Option Pricing

Abstract.

We investigate two new strategies for the numerical solution of optimal stopping problems within the Regression Monte Carlo (RMC) framework of Longstaff and Schwartz. First, we propose the use of stochastic kriging (Gaussian process) meta-models for fitting the continuation value. Kriging offers a flexible, nonparametric regression approach that quantifies approximation quality. Second, we connect the choice of stochastic grids used in RMC to the Design of Experiments paradigm. We examine space-filling and adaptive experimental designs; we also investigate the use of batching with replicated simulations at design sites to improve the signal-to-noise ratio. Numerical case studies for valuing Bermudan Puts and Max-Calls under a variety of asset dynamics illustrate that our methods offer significant reduction in simulation budgets over existing approaches.

1. Introduction

The problem of efficient valuation and optimal exercise of American/Bermudan options remains one of intense interest in computational finance. The underlying timing flexibility, which is mathematically mapped to an optimal stopping objective, is ubiquitous in financial contexts, showing up both directly in various derivatives and as a building block in more complicated contracts, such as multiple-exercise opportunities or sequential decision-making. Since timing optionality is often embedded on top of other features, ideally one would have access to a flexible pricing architecture to easily import optimal stopping sub-routines. While there are multiple alternatives that have been proposed and investigated, most existing methods are not fully scalable across the range of applications, keeping the holy grail of such “black-box” optimal stopping algorithm out of reach111By black-box we mean a “smart” framework that automatically adjusts low-level algorithm parameters based on the problem setting. It might still require some high-level user input, but avoids extensive fine-tuning or, at the other extreme, a hard-coded, non-adaptive method.. This is either due to reliance on approaches that work only for a limited subset of models, (e.g. one-dimensional integral equations, various semi-analytic formulas, etc.) or due to severe curses of dimensionality that cause rapid deterioration in performance as model complexity increases.

Within this landscape, the regression Monte Carlo framework or RMC (often called Least Squares Monte Carlo, though see our discussion on this terminology in Section 2.2) has emerged as perhaps the most popular generic method to tackle optimal stopping. The intrinsic scalability of Monte Carlo implies that if the problem is more complex one simply runs more simulations, with the underlying implementation essentially independent of dimensionality, model dynamics, etc. However, the comparatively slow convergence rate of RMC places emphasis on obtaining more accurate results with fewer simulated paths, spurring an active area of research, see e.g. [1, 4, 14, 20, 21, 29, 41].

In this article, we propose a novel marriage of modern statistical frameworks and the optimal stopping problem, making two methodological contributions. First, we examine the use of kriging meta-models as part of a simulation-based routine to approximate the optimal stopping policies. Kriging offers a flexible non-parametric method (with several additional convenient features discussed below) for approximating the continuation value, and as we demonstrate is competitive with existing basis-expansion setups. To our knowledge this is the first article to use kriging models in optimal stopping. Second, we investigate the experimental design aspect of RMC. We propose several alternatives on how to generate and customize the respective stochastic grids, drawing attention to the accompanying performance gains. Among others, we investigate adaptive generation of the simulation designs, extending the ideas in Gramacy and Ludkovski [16] who originally proposed the use of sequential design for optimal stopping. Rather than purely targeting speed savings, our strategies explore opportunities to reduce the simulation budget of RMC through “smart” regression and design approaches. In particular, the combination of kriging and improved experimental design brings up to an order-of-magnitude savings in simulation costs, which can be roughly equated to memory requirements. While there is considerable overhead added, these gains indicate the potential of these techniques to optimize the speed-memory trade-off. They also show the benefits of approaching RMC as an iterated meta-modeling/response-surface modeling problem.

Our framework is an outgrowth of the recent work by the author in [16]. In relation to the latter paper, the present article makes several modifications that are attractive for the derivative valuation context. First, while [16] suggested the use of piecewise-defined Dynamic Trees regression, the kriging meta-models are intrinsically continuous. As such, they are better suited for the typical financial application where the value function is smooth. Second, to reduce computational overhead, we introduce a new strategy of batching by generating multiple scenarios for a given initial condition. Third, in contrast to [16] that focused on sequential designs, we also provide a detailed examination and comparison of various static experimental designs. Our experiments indicate that this already achieves significant simulation savings with a much smaller overhead, and is one of the “sweet spots” in terms of overall performance.

The rest of the paper is organized as follows. Section 2 sets the notation we use for a generic optimal stopping problem, and the RMC paradigm for its numerical approximation. Along the way we recast RMC as a sequence of meta-modeling tasks. Section 3 introduces and discusses stochastic kriging meta-models that we propose to use for empirical fitting of the continuation value. Section 4 then switches to the second main thrust of this article, namely the issue of experimental designs for RMC. We investigate space-filling designs, as well as the idea of batching or replication. Section 5 marries the kriging methodology with the framework of sequential design to obtain an efficient approach for generating designs adapted to the loss criterion of RMC. In Section 6 we present a variety of case studies, including a classical bivariate GBM model, several stochastic volatility setups, and multivariate GBM models with multiple stopping regions. Finally, Section 7 summarizes our proposals and findings.

2. Model

We consider a discrete-time optimal stopping problem on a finite horizon. Let , be a Markov state process on a stochastic basis taking values in some (usually uncountable) subset . The financial contract in question has a maturity date of and can be exercised at any earlier date with payoff . Note that in the financial applications this corresponds to a Bermudan contract with a unit of time corresponding to the underlying discretization of early exercise opportunities. The dependence of on is to incorporate interest rate discounting.

Let , be the information filtration generated by and the collection of all -stopping times bounded by . The Bermudan contract valuation problem consists of maximizing the expected reward over all . More precisely, define for any ,

| (2.1) |

where denotes -expectation given initial condition . We assume that is such that for any , for instance bounded.

Using the tower property of conditional expectations and one-step analysis,

| (2.2) |

where we defined the continuation value and timing-value via

| (2.3) | ||||

| (2.4) |

Since for all and , the smallest optimal stopping time for (2.1) satisfies

| (2.5) |

Thus, it is optimal to stop immediately if and only if the conditional expectation of tomorrow’s reward-to-go is less than the immediate reward. Rephrasing, figuring out the decision to stop at is equivalent to finding the zero level-set (or contour) of the timing value or classifying the state space into the stopping region and its complement the continuation region. By induction, an optimal stopping time is

| (2.6) |

From the financial perspective, obtaining the exercise strategy as defined by is often even more important than finding the present value of the contract.

The representation (2.6) suggests a recursive procedure to estimate the optimal policy as defined by . To wit, given a collection of subsets of which are stand-ins for the stopping regions, define the corresponding exercise strategy pathwise for a scenario :

| (2.7) |

Equipped with , we obtain the pathwise payoff

| (2.8) |

Taking expectations, is the expected payoff starting at , not exercising immediately at step and then following the exercise strategy specified by ; our notation highlights the latter (path-) dependence of on future stopping regions ’s. If for all , we can use (2.8) to recover . Indeed, the expected value of in this case is precisely the continuation value . Consequently, finding (and hence the value function via (2.2)) is reduced to computing conditional expectations of the form . Because analytic evaluation of this map is typically not tractable, this is the starting point for Monte Carlo approximations which only require the ability to simulate -trajectories. In particular, simulating independent scenarios , emanating from yields the estimator via

| (2.9) |

A key observation is that the approximation quality of (2.9) is driven by the accuracy of the stopping sets that determine the exercise strategy and control the resulting errors (formally we should thus use a double-hat notation to contrast the estimate in (2.9) with the true expectation ). Thus, for the sub-problem of approximating the conditional expectation of , there is a thresholding property, so that regression errors are tolerated as long as they do not affect the ordering of and . This turns out to be a major advantage compared to value function approximation techniques as in [42], which use (2.2) directly and do not explicitly make use of pathwise payoffs. See also [40] for a recent comparison of value-function and stopping-time approximations.

2.1. Meta-Modeling

In (2.9) the estimate of was obtained pointwise for a given location through a plain Monte Carlo approach. Alternatively, given paths , emanating from different initial conditions , one may borrow information cross-sectionally by employing a statistical regression framework. A regression model specifies the link

| (2.10) |

where is the mean-zero noise term with variance . This noise arises from the random component of the pathwise payoff due to the internal fluctuations in and hence . Letting be a vector of obtained pathwise payoffs, one regresses against to fit an approximation . Evaluating at any then yields the predicted continuation value from the exercise strategy conditional on .

The advantage of regression is that it replaces pointwise estimation (which requires re-running additional scenarios for each location ) with a single step that fuses all information contained in to fit . Armed with the estimated , we take the natural estimator of the stopping region at ,

| (2.11) |

which yields an inductive procedure to approximate the full exercise strategy via (2.7). Note that (2.11) is a double approximation of – due to the discrepancy between and the true expectation from (2.8), as well as due to partially propagating the previous errors in relative to the true .

The problem of obtaining based on (2.10) is known as meta-modeling or emulation in the machine learning and simulation optimization literatures [25, 3, 38]. It consists of two fundamental steps: first a design (i.e. a grid) is constructed and the corresponding pathwise payoffs are realized via simulation. Then, a regression model (2.10) is trained to link the ’s to ’s via an estimated . In the context of (2.3), emulation can be traced to the seminal works of Tsitsiklis and van Roy [42] and Longstaff and Schwartz [30] (although the idea of applying regression originated earlier, with at least Carrière [8]). The above references pioneered classical least-squares regression (known by the acronyms Least Squares Method, Least Squares Monte Carlo and more generally as Regression Monte Carlo and Regression Based Schemes) for (2.10), i.e. the use of projection onto a finite family of basis functions ,

The projection was carried out by minimizing the distance between and the manifold spanned by the basis functions (akin to the definition of conditional expectation):

| (2.12) |

where the loss function is a weighted norm based on the distribution of ,

| (2.13) |

Motivated by the weights in (2.13), the accompanying design is commonly generated by i.i.d. sampling from . As suggested in the original articles [30, 42] this can be efficiently implemented by a single global simulation of -paths , although at the cost of introducing further -dependencies among ’s.

Returning to the more abstract view, least-squares regression (2.12) is an instance of a meta-modeling technique. Moreover, it obscures the twin issue of generating . Indeed, in contrast to standard statistical setups, in meta-modeling there is no a priori data per se; instead the solver is responsible both for generating the data and for training the model. These two tasks are intrinsically intertwined. The subject of Design of Experiments (DoE) has developed around this issue, but has been largely absent in RMC approaches. In the next Section we re-examine existing RMC methods and propose novel RMC algorithms that build on the DoE/meta-modeling paradigm by targeting efficient designs .

2.2. Closer Look at the RMC Regression Problem

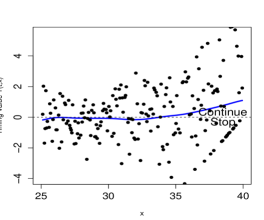

Figure 1 shows the distribution of in a 1-D Geometric Brownian motion Bermudan Put option problem (see Section 4.4), the archetype of a financial application. The left plot shows a scatterplot of as varies, and the right panel gives a histogram of for a fixed initial value . Two features become apparent from these plots. First, the noise variance is extremely large, swamping the actual shape of . Second, the noise distribution is highly non-standard. It involves a potent brew of (i) heavy-tails; (ii) significant skewness; (iii) multi-modality. In fact, does not even have a smooth density as the nonnegativity of the payoff , implies that has a point mass at zero.

Moreover, as can be observed in the left panel of Figure 1, the distribution of is heteroscedastic, with a state-dependent conditional skew and state-dependent point mass at zero. These phenomena violate the assumptions of ordinary least squares regression, making the sampling distribution of fitted ill-behaved, i.e. far from Gaussian. More robust versions of (2.12), including regularized (such as Lasso) or localized (such as Loess or piecewise linear models) least squares frameworks have therefore been proposed, see [27, 28]. Further structured regression proposals can be found in [24, 29]. Alternatively, a range of variance reduction methods, such as control variates, have been suggested to ameliorate the estimation of in (2.12), see for example [1, 4, 20, 21, 23].

The parametric constraints placed by the LSMC approach (2.12) on the shape of the continuation value , make its performance highly sensitive to the distance between the manifold and the true [39]. Moreover, when using (2.12) a delicate balance must be observed between the number of scenarios and the number of basis functions . These concerns highlight the inflexible nature of parametric regression and become extremely challenging in higher dimensional settings with unknown geometry of . One work-around is to employ hierarchical representations, for example by partitioning into disjoint bins and employing independent linear hyperplane fits in each bin, see e.g. Bouchard and Warin [6]. Nevertheless, there remain ongoing challenges in adaptive construction of .

Another limitation of the standard LSMC approach is its objective function. As discussed, least squares regression can be interpreted as minimizing a global weighted mean-squared-error loss function. However, as shown in (2.5), the principal aim in optimal stopping is not to learn globally in the sense of its mean-squared-error, but to rank it vis-a-vis . Indeed, recalling the definition of the timing function, the correct loss function (cf. [16]) is

| (2.14) |

Consequently, the loss criterion is localized around the contour . Indeed, a good intuition is that optimal stopping is effectively a classification problem: in some regions of , the sign of is easy to detect and the stopping decision is “obvious”, while in other regions is close to zero and resolving the optimal decision requires more statistical discrimination. For example, in Bermudan options it is a priori clear that out-of-the-money (OTM) , and so it is optimal to continue at such . This observation was already stated in [30] who suggested to only regress in-the-money (ITM) trajectories. However, it also belies the apparent inefficiency in the corresponding design— the widely used LSMC implementation first “blindly” generates a design that covers the full domain of , only to discard all OTM scenarios. This dramatically shrinks the effective design size, up to 80% in the case of an OTM option. The mismatch between (2.14) and (2.13) makes the terminology of “least-squares” Monte Carlo that exclusively emphasizes the -criterion unfortunate.

While one could directly use (2.14) during the cross-sectional regression (for example to estimate the coefficients in (2.12), which however would require implementing an entirely new optimization problem), a much more effective approach is to take this criterion into account during the experimental design. Intuitively, the local accuracy of any approximation of is limited by the amount of observations in the neighborhood, i.e. the density of around . The form of (2.14) therefore suggests that the ideal approach would be to place along the stopping boundary in analogue to importance sampling. Of course the obvious challenge is that knowing is equivalent to solving the stopping problem. Nevertheless, this perspective suggests multiple improvements to the baseline approach which is entirely oblivious to (2.14) when picking .

2.3. Outline of Proposed Approach

Motivated by the above discussion, we seek efficient meta-models for learning that can exploit the local nature of (2.14). This leads us to consider non-parametric, kernel-based frameworks, specifically Gaussian process regression, also known as kriging [3, 25, 45]. We then explore a range of Design of Experiments approaches for constructing . Proposed design families include (i) uniform gridding; (ii) random and deterministic space-filling designs; (iii) adaptive sequential designs based on expected improvement criteria. While only the last choice is truly tailored to (2.14), we explain that reasonably well-chosen versions of (i) and (ii) can already be a significant improvement on the baseline.

To formalize construction of , we rephrase (2.10) as a response surface (aka meta-) modeling (RSM) problem. RSM is concerned with the task of estimating an unknown function that is noisily observed through a stochastic sampler,

| (2.15) |

where we remind the reader to substitute in their mind and ; is treated as a parameter. Two basic requirements in RSM are a flexible nonparametric approximation architecture that is used for searching for the outputted fit , and global consistency, i.e. convergence to the ground truth as number of simulations increases without bound. The experimental design problem then aims to maximize the information obtained from samples towards the end of minimizing the specified loss function .

The pathwise realizations of involve simulation noise which must be smoothed out and as we saw is often highly non-Gaussian. To alleviate this issue, we mimic the plain Monte Carlo strategy in (2.9) that uses the classical Law of Large Numbers to obtain a local estimate of , by constructing batched or replicated designs. Batching generates multiple independent samples , at the same , which are used to compute the empirical average . Clearly, follows the same statistical model (2.15) but with a signal-to-noise ratio improved by a factor of , . This also reduces the post-averaged design size , which speeds-up and improves the training of the meta-model.

To recap, kriging gives a flexible non-parametric representation for . The fitting method automatically detects the spatial structure of the continuation value obviating the need to specify the approximation function-class. While the user must pick the kernel family, extensive experiments suggest that these have a second-order effect. Also, the probabilistic structure of kriging offers convenient goodness-of-fit diagnostics after is obtained, yielding a tractable quantification of posterior uncertainty. This can be exploited for DoE, see Section 5.

3. Kriging Metamodels

Kriging models have emerged as perhaps the most popular framework for DoE over continuous input spaces . In kriging the cross-sectional interpolation is driven by the spatial smoothness of and essentially consists of aggregating the observed values of in the neighborhood of . Book-length treatment of kriging can be found in [45], see also [25, Ch. 5] and [3]. To be precise, in this article we deal with stochastic kriging under heterogeneous sampling noise.

Stochastic kriging meta-models follow a Bayesian paradigm, treating in (2.15) as a random object belonging to a function space . Thus, for each , is a random variable whose posterior distribution is obtained based on the collected information from samples and its prior distribution . Let be the information generated by the design , i.e. . We then define the posterior distribution of ; the global map is called the surrogate surface (the terminology is a misnomer, since is in fact measure-valued). Its first two moments are the surrogate mean and variance respectively,

| (3.1) | ||||

| (3.2) |

Note that in this function-view framework, a point estimate of the unknown is replaced with a full posterior distribution over the space ; tractability is achieved by imposing and maintaining Gaussian structure. The surrogate mean surface is then the natural proxy (being the maximum a posteriori probability estimator) for , and the surrogate variance is the proxy for the standard error of .

To model the relationship between and at different locations kriging uses the Reproducing Kernel Hilbert Space (RKHS) approach, treating the full as a realization of a mean-zero Gaussian process. If necessary, is first “de-trended” to justify the mean-zero assumption. The Gaussian process generating is based on a covariance kernel , with . The resulting function class forms a Hilbert space. The RKHS structure implies that both the prior and posterior distributions of given are multivariate Gaussian.

By specifying the correlation behavior, the kernel encodes the smoothness of the response surfaces drawn from the GP which is measured in terms of the RKHS norm . Two main examples we use are the squared exponential kernel

| (3.3) |

and the Matern-5/2 kernel

| (3.4) |

which both use the weighted Euclidean norm . The length-scale vector controls the smoothness of members of , the smaller the rougher. The variance parameter determines the amplitude of fluctuations in the response. In the limit , elements of concentrate on the linear functions, effectively embedding linear regression; if , elements of are constants. For both of the above cases, members of the function space can uniformly approximate any continuous function on any compact subset of .

The use of different length-scales for different coordinates of allows anisotropic kernels that reflect varying smoothness of in terms of its different input coordinates. For example, in Bermudan option valuation, continuation values would typically be more sensitive to the asset price than to a stochastic volatility factor , which would be reflected in .

Let denote the observed noisy samples at locations . Given the data and the kernel , the posterior of again forms a GP; in other words any collection is multivariate Gaussian with means , covariances , and variances , specified by the matrix equations [45, Sec. 2.7]:

| (3.5) | ||||

| (3.6) |

with , and the positive definite matrix , . The diagonal structure of is due to the assumption that independent simulations have uncorrelated noise, i.e. use independent random numbers. Note that the uncertainty, , associated with the prediction at has no direct dependence on the simulation outputs ; all response points contribute to the estimation of the local error through their influence on the induced correlation matrix . Well-explored regions will have lower , while regions with few or no observations (in particular regions beyond the training design) will have high .

3.1. Training a Kriging Metamodel

To fit a kriging metamodel requires specifying , i.e. fixing the kernel family and then estimating the respective kernel hyper-parameters, such as in (3.4) that are plugged into (3.5)-(3.6). The typical approach is to use a maximum likelihood approach which leads to solving a nonlinear optimization problem to find the MLEs defining . Alternatively, cross-validation techniques or EM-type algorithms are also available.

While the choice of the kernel family is akin to the choice of orthonormal basis in LSMC, in our experience they play only a marginal role in performance of the overall pricing method. As a rule of thumb, we suggest to use either the Matern-5/2 kernel or the squared-exponential kernel. In both cases, the respective function spaces are smooth (twice-differentiable for Matern-5/2 family (3.4) and for the squared exponential kernel), and lead to similar fits. The performance is more sensitive to the kernel hyper-parameters, which are typically estimated in a frequentist framework, but could also be inferred from a Bayesian prior, or even be guided by heuristics.

Remark 3.1.

One may combine a kriging model with a classical least squares regression on a set of basis functions . This is achieved by taking where is a trend term as in (2.12), ’s are the trend coefficients to be estimated, and is the “residual” mean-zero Gaussian process. The Universal Kriging formulas, see [34] or [45, Sec. 2.7], then allow simultaneous computation of the kriging surface and the OLS coefficients . For example, one may use the European option price, if one is explicitly available, as a basis function to capture some of the structure in .

Inference on the kriging hyperparameters requires knowledge of the sampling noise . Indeed, while it is possible to simultaneously train and infer a constant simulation variance (the latter is known as the “nugget” in the machine learning community [38]), with state-dependent noise is not identifiable. Batching allows to circumvent this challenge by providing empirical estimates of . For each site , we thus sample independent replicates and estimate the conditional variance as

| (3.7) |

is the batch mean. We then use as a proxy to the unknown to estimate . One could further improve the estimation of by fitting an auxiliary kriging meta-model from ’s, cf. [25, Ch 5.6] and references therein. As shown in [33, Sec 4.4.2], after fixing we can then treat the samples at as the single design entry with noise variance . The end result is that the batched dataset has just rows that are fed into the kriging meta-model.

For our examples below, we have used the R package DiceKriging [37]. The software takes the input locations , the corresponding simulation outputs and the noise levels , as well as the kernel family (Matern-5/2 (3.4) by default) and returns a trained kriging model. One then can utilize a predict call to evaluate (3.5)-(3.6) at given s. The package can also implement universal kriging. Finally, in the cases where the design is not batched or the batch size is very small (below 20 or so), we resort to assuming homoscedastic noise level that is estimated as part of training the kriging model (an option available in DiceKriging). The advantage of such plug-and-play functionality is access to an independently tested, speed-optimized, debugged, and community-vetted code, that minimizes implementation overhead and future maintenance (while perhaps introducing some speed ineffiencies).

Remark 3.2.

The kriging framework includes several well-developed generalizations, including treed GP’s [18], local GP’s [15], monotone GP’s [36], and particle-based GP’s [17] that can be substituted instead of the vanilla method described above, similar to replacing plain OLS with more sophisticated approaches. All the aforementioned extensions can be used off-the-shelf through public R packages described in the above references.

3.2. Approximation Quality

To quantify the accuracy of the obtained kriging estimator , we derive an empirical estimate of the loss function . To do so, we integrate the posterior distributions vis-a-vis the surrogate means that are proxies for using (2.14):

| (3.8) |

where are the standard Gaussian cumulative/probability density functions. The quantity is precisely the Bayesian posterior probability of making the wrong exercise decision at based on the information from , so lower indicates better performance of the design in terms of stopping optimally. Integrating over then gives an estimate for :

| (3.9) |

Practically, we replace the latter integral with a weighted sum over , .

3.3. Further RKHS Regression Methods

From approximation theory perspective, kriging is an example of a regularized kernel regression. The general formulation looks for the minimizer of the following penalized residual sum of squares problem

| (3.10) |

where is a chosen smoothing parameter and is a RKHS. The summation in (3.10) is a measure of closeness of to data, while the right-most term penalizes the fluctuations of to avoid over-fitting. The representer theorem implies that the minimizer of (3.10) has an expansion in terms of the eigen-functions

| (3.11) |

relating the prediction at to the kernel functions based at the design sites ; compare to (3.5). In kriging, the function space is , , and the corresponding norm has a spectral decomposition in terms of differential operators [45, Ch. 6.2].

Another popular version of (3.10) are the smoothing (or thin-plate) splines that take where denotes the Euclidean norm in . In this case, the RKHS is the set of all twice continuously-differentiable functions [19, Chapter 5] and

| (3.12) |

This generalizes the one-dimensional penalty function . Note that under and (3.12) the optimization in (3.10) reduces to the traditional least squares linear fit since it introduces the constraint A common parametrization for the smoothing parameter is through the effective degrees of freedom statistic dfλ; one may also select adaptively via cross-validation or MLE [19, Chapter 5]. The resulting optimization of (3.10) based on (3.12) gives a smooth response surface which is called a thin-plate spline (TPS), and has the explicit form

| (3.13) |

See [26] for implementation of RMC via splines.

A further RKHS approach, applied to RMC in [41] is furnished by the so-called (Gaussian) radial basis functions. These are based on the already mentioned Gaussian kernel , but substitute the penalization in (3.10) with ridge regression, reducing the sum in (3.11) to terms by identifying/optimizing the “prototype” sites .

4. Designs for Kriging RMC

Fixing the meta-modeling framework, we turn to the problem of generating the experimental design . We work in the fixed-budget setting, with a pre-specified number of simulations to run. Optimally constructing the respective experimental design requires solving a -dimensional optimization problem, which is generally intractable. Accordingly, in this section we discuss heuristics for generating near-optimal static designs. Section 5 then considers another work-around, namely sequential methods that utilize a divide-and-conquer approach.

4.1. Space Filling Designs

A standard strategy in experimental design is to spread out the locations to extract as much information as possible from the samples . A space-filling design attempts to distribute ’s evenly in the input space , here distinguished from the theoretical domain of . While this approach does not directly target the objective (2.14), assuming is reasonably selected, it can still be much more efficient than traditional LSMC designs. Examples of space-filling approaches include maximum entropy designs, maximin designs, and maximum expected information designs [25]. Another choice are quasi Monte Carlo methods that use a deterministic space-filling sequence such as the Sobol for generating . The simplest choice are gridded designs that pick on a pre-specified lattice, see Figure 2 below. Quasi-random/low-discrepancy sequences have already been used in American option pricing but for other purposes; in [7] for approximating one-step value in a stochastic mesh approach and in [9] for generating the trajectories of . Here we propose to use quasi-random sequences directly for constructing the simulation design; see also [46] for using a similar strategy in a stochastic control application.

One may also generate random space-filling designs which is advantageous in our context of running multiple response surface models (indexed by ) by avoiding any grid-ghosting effects. One flexible procedure is Latin hypercube sampling (LHS) [32]. In contrast to deterministic approaches that are generally only feasible in hyper-rectangular ’s, LHS can be easily combined with an acceptance-rejection step to generate space-filling designs on any finite subspace.

Typically the theoretical domain of is unbounded (e.g. ) and so the success of a space-filling design is driven by the judicious choice of an appropriate . This issue is akin to specifying the domain for a numerical PDE solver and requires structural knowledge. For example, for a Bermudan Put with strike , we might take , covering a wide swath of the in-the-money region, while eschewing out-of-the-money and very deep in-the-money scenarios. Ultimately, the problem setting determines the importance of this choice (compare the more straightforward setting of Section 6.3 below vs. that of Section 6.2 where finding a good is much harder).

4.2. Probabilistic Designs

The original solution of Longstaff and Schwartz [30] was to construct the design using the conditional density of , i.e. to generate independent draws , . This strategy has two advantages. First, it permits to implement the backward recursion for estimating on a fixed global set of scenarios which requires just a single (albeit very large) simulation and hence saves simulation budget. Second, a probabilistic design automatically adapts to the dynamics of , picking out the regions that is likely to visit and removing the aforementioned challenge of specifying .

Moreover, empirical sampling of reflects the density of which helps to lower the weighted loss (2.14). Assuming that the boundary is not in a region where is very low, this generates a well-adapted design, which partly explains why the experimental design of LSMC is not entirely without its merits. Compared to a space-filling design that is sensitive to , a probabilistic design is primarily driven by the initial condition . This can be a boon as above, or a limitation; for example with OTM Put contracts, the vast majority of empirically sampled sites would be out-of-the-money, dramatically lowering the quality of an empirical . A good compromise is to take i.e. to condition on being in-the-money.

4.3. Batched Designs

As discussed, the design sites need not be distinct and the macro-design can be replicated. Such batched designs offer several benefits in the context of meta-modeling. First, averaging of simulation outputs dramatically improves the statistical properties of the averaged compared to the raw ’s. In most cases once , the Gaussian assumption regarding the respective noise becomes excellent. Second, batching raises the signal-to-noise ratio and hence simplifies response surface modeling. Training the kriging kernel with very noisy samples is difficult, as the likelihood function to be optimized possesses multiple local maxima. Third, as mentioned in Section 3.1, batching allows empirical estimation of heteroscedastic sampling noise . Algorithm 1 summarizes the steps for building a kriging-based RMC solver with a replicated design.

Batching also connects to the general bias-variance tradeoff in statistical estimation. Plain (pointwise) Monte Carlo offers a zero bias / high variance estimator of , which is therefore computationally expensive. A low-complexity model such as parametric least squares (2.12), offers a low variance/high bias estimator (since it requires constraining ). Batched designs coupled with kriging interpolate these two extremes by reducing bias through flexible approximation classes, and reducing variance through batching and modeling of spatial response correlation.

Remark 4.1.

The batch sizes can be adaptive. By choosing appropriately one can set to any desired level. In particular, one could make all averaged observations homoscedastic with a pre-specified intrinsic noise . The resulting regression model for would then conform very closely to classical homoscedastic Gaussian assumptions regarding the distribution of simulation noise.

As the number of replications becomes very large, batching effectively eliminates all sampling noise. Consequently, one can substitute the empirical average from (3.7) for the true , an approach first introduced in [43]. It now remains only to interpolate these responses, reducing the meta-modeling problem to analysis of deterministic experiments. There is a number of highly efficient interpolating meta-models, including classical deterministic kriging (which takes in (3.5)-(3.6)), and natural cubic splines. Assuming smooth underlying response, deterministic meta-models often enjoy very fast convergence. Application of interpolators offers a new perspective (which among others is nicer to visualize) on the RMC meta-modeling problem. To sum up, batching offers a tunable spectrum of methods that blend smoothing and interpolation of .

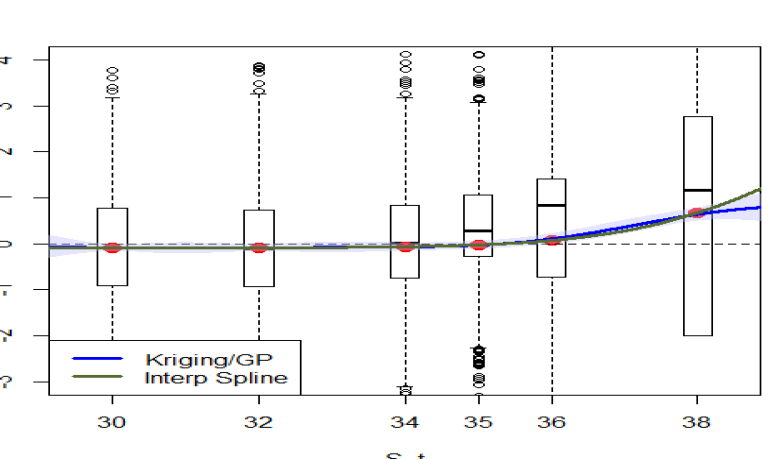

Figure 2 illustrates the above idea for a 1-D Bermudan Put in a GBM model, see Section 4.4. We construct a design of macro size which uses just six distinct sites , and replications at each site. We then interpolate the obtained values using (i) a deterministic kriging model; and a (ii) natural cubic spline. We observe that the resulting fit for shown in the Figure looks excellent and yields an accurate approximation of the exercise boundary.

4.4. Illustration

To illustrate different simulation designs we revisit the classical example of a 1-D Bermudan Put option in a Geometric Brownian motion model. More extensive experiments are given in Section 6. The log-normal -dynamics are

| (4.1) |

and the Put payoff is . The option matures at , and we assume 25 exercise opportunities spaced out evenly with . This means that with a slight abuse of notation, the RMC algorithm is executed over . The rest of the parameter values are interest rate , dividend yield , volatility , and at-the-money strike . In this case , cf. [30]. In one dimension, the stopping region for the Bermudan Put is an interval so there is a unique exercise boundary .

We implement Algorithm 1 using a batched LHS design with , so at each step there are distinct simulation sites . The domain for the experimental designs is the in-the-money region . To focus on the effect of various ’s, we freeze the kriging kernel across all time steps as a Matern-5/2 type (3.4) with hyperparameters , which were close to the MLE estimates obtained. This choice is maintained for the rest of this section, as well as for the following Figures 4-5. Our experiments (see in particular Table 3) imply that the algorithm is insensitive to the kernel family or the specific software/approach used for training the kriging kernels.

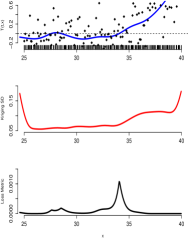

Figure 3 illustrates the effect of various experimental designs on the kriging meta-models. We compare three different batched designs with a fixed overall size : (a) an LHS design with small batches ; (b) an LHS design with a large , and (c) a probabilistic density-based design also with ; recall that the latter generates paths of and then creates sub-simulations initiating at each . The resulting at are shown in the top panels of Figure 3, along with the obtained estimates . The middle row of Figure 3 shows the resulting surrogate standard deviations . The shape of is driven by the local density of the respective , as well as by the simulation noise . Here, is highly heteroscedastic, being much larger near at-the-money than deep ITM. This is because in-the-money one is likely to stop soon and so the variance of is lower. For LHS designs, the roughly uniform density of leads to the posterior variance being proportional to the simulation noise, ; on the other hand the empirical design reflects the higher density of closer to , so that is smallest there. Moreover, because there are very few design sites for (just 5 in Figure 3), the corresponding surrogate variance has the distinctive hill-and-valley shape. In all cases, the surrogate variance explodes along the edges of , reflecting lack of information about the response there.

|

|

|

| LHS | LHS | Emp |

The bottom panels of Figure 3 show the local loss metric for the corresponding designs. We stress that is a function of the sampled , and hence will vary across algorithm runs. Intuitively is driven by the respective surrogate variance , weighted in terms of the distance to the stopping boundary. Consequently, large is fine for regions far from the exercise boundary. Overall, we can make the following observations:

-

(i)

Replicating simulations does not materially impact surrogate variance at any given , and hence makes little effect on . Consequently, there is minimal loss of fidelity relative to using a lot of distinct design sites in .

-

(ii)

The modeled response surfaces tend to be smooth. Consequently, the kernel should enforce long-range spatial dependence (sufficiently large lengthscale) to make sure that is likewise smooth. Undesirable fluctuations in can generate spurious stopping/continuation regions, see e.g. the left-most panel in Figure 3 around .

-

(iii)

Probabilistic designs tend to increase because they fail to place enough design sites deep ITM, leading to extreme posterior uncertainty there, cf. the right panel in the Figure.

-

(iv)

Due to very low signal-to-noise ratio that is common in financial applications, replication of simulations aids in seeing the “shape” of and hence simplifies the meta-modeling task, see point (ii).

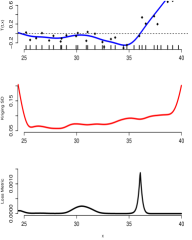

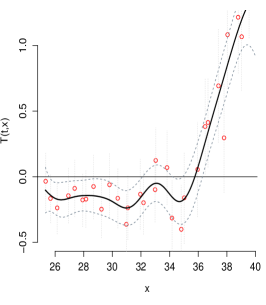

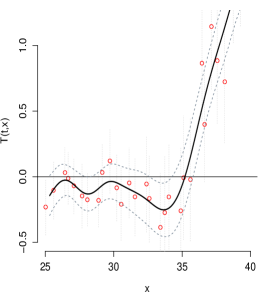

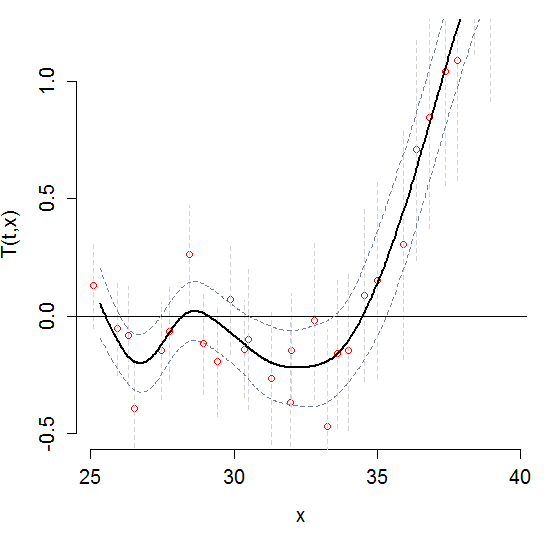

To give a sense regarding the aggregate quality of the meta-models, Figure 4 shows the estimated at three different steps as the RMC implements backward recursion. The overall shape of remains essentially the same, being strongly positive close to the strike , crossing zero at and remaining slightly negative deep ITM. As decreases, the exercise boundary also moves lower. The Figure shows how the cross-sectional borrowing of information (modeled by the GP correlation kernel ) reduces the surrogate variance compared to the raw (cf. the corresponding 95% CIs). We also observe that there is some undesirable “wiggling” of , which can generate spurious exercise boundaries such as in the extreme left of the panel in Figure 4. However, with an LHS design this effect is largely mitigated compared to the performance of the empirical design in Figure 3. This confirms the importance of spacing out the design . Indeed, for the LHS designs the phenomenon of spurious exercising only arises for and very small, whereby the event that would lead to the wrong exercise strategy has negligible probability of occurring.

|

|

|

5. Sequential Designs

In this section we discuss adaptive designs that are generated on the fly as the meta-model learns . Sequential design captures the intuition of focusing the sampling efforts around the exercise boundary , cf. the loss function (2.14). This makes learning the response intrinsic to constructing the experimental design. In particular, Bayesian procedures embed sequential design within a dynamic programming framework that is naturally married to statistical learning. Algorithmically, sequential design is implemented at each time step by introducing an additional loop over that grows the experimental designs now indexed by their size ( is the number of distinct sites, with batching possibly applied in the inner loop as before). As the designs are augmented, the corresponding surrogate surfaces and stopping regions are re-estimated and refined. The final result is a sequence of adaptive designs and corresponding exercise policy.

5.1. Augmenting the Experimental Design

Fixing a time step , the sequential design loop is initialized with , generated for example using LHS. New design sites are then iteratively added by greedily optimizing an acquisition function that quantifies information gains via Expected Improvement (EI) scores. The aim of EI scores is to identify locations which are most promising in terms of lowering the global loss function from (2.14). In our context the EI scores are based on the posterior distributions which summarize information learned so far about . The seminal works of [12, 31] showed that a good heuristic to maximize learning rates is to sample at sites that have high surrogate variance or high expected surrogate variance reduction, respectively. Because we target (2.14), a second objective is to preferentially explore regions close to the contour . This is achieved by blending the distance to the contour with the above variance metrics, in analogue to the Efficient Global Optimization approach [22] in simulation optimization.

A greedy strategy augments with the location that maximizes the acquisition function:

| (5.1) |

Two major concerns for implementing (5.1) are (i) the computational cost of optimizing over and (ii) the danger of myopic strategies. For the first aspect, we note that (5.1) introduces a whole new optimization sub-problem just to augment the design. This can generate substantial overhead that deteriorates the running time of the entire RMC. Consequently, approximate optimality is often a pragmatic compromise to maximize performance. For the second aspect, myopic nature of (5.1) might lead to undesirable concentration of the design interfering with the convergence of as grows. It is well known that many greedy sequential schemes can get trapped sampling in some subregion of , generating poor estimates elsewhere. For example, if there are multiple exercise boundaries, the EI metric might over-prefer established boundaries, and risk missing other stopping regions that were not yet found. A common way to circumvent this concern is to randomize (5.1), which ensures that grows dense uniformly on . In the examples below we follow [16] and replace in (5.1) with where is a finite candidate set, generated using LHS over some domain again. LHS candidates ensure that potential new locations are representative and well spaced out over .

Kriging meta-models are especially well-suited for sequential design thanks to availability of simple updating formulas that allow to efficiently assimilate new data points into an existing fit. If a new sample is added to an existing design and keeping the kernel fixed, the surrogate mean and variance at location are updated via

| (5.2) | ||||

| (5.3) |

where is a weight function (that is available analytically) specifying the influence of the new -sample on , conditional on existing design locations . Note that (5.2) and (5.3) only require the knowledge of the latest surrogate mean/variance and ; previous simulation outputs do not need to be stored. Moreover, the updated surrogate variance is a deterministic function of which is independent of . In particular, the local reduction in surrogate standard deviation at is proportional to the current [11]:

| (5.4) |

Remark 5.1.

In principle, the hyperparameters of the kernel ought to be re-estimated as more data is collected, which makes updating non-sequential. However, since we expect the estimated to converge as grows, it is a feasible strategy to keep frozen across sequential design iterations, allowing the use of (5.2)-(5.3).

Algorithm 2 summarizes sequential design for learning at a given time-step ; see also Algorithm 1 for the overall kriging-based RMC approach to optimal stopping.

Remark 5.2.

The ability to quickly update the surrogate as simulation outputs are collected lends kriging-models to “online” and parallel implementations. This can be useful even without going through a full sequential design framework. For example, one can pick an initial budget , implement RMC with simulations, and if the results are not sufficiently accurate, add more simulations without having to completely restart from scratch. Similarly, batching simulations is convenient for parallelizing using GPU technology.

5.2. Acquisition Functions

In this section we propose several acquisition functions to guide the sequential design sub-problem (5.1). Throughout we are cognizant of the loss function (2.14) that is the main criterion for learning .

One possible proposal for an EI metric is to sample at locations that have a high (weighted) local loss defined in (3.8), i.e.

| (5.5) |

The superscript ZC stands for zero-contour, since intuitively measures the weighted distance between and exercise boundary, see [16]. targets regions with high or close to the exercise boundary, .

A more refined version, dubbed ZC-SUR, attempts to identify regions where can be quickly lowered through additional sampling. To do so, ZC-SUR incorporates the expected difference which can be evaluated using the updating formulas (5.2)-(5.3). This is similar in spirit to the stepwise uncertainty reduction (SUR) criterion in stochastic optimization [34]. Plugging-in (2.14) we obtain

| (5.6) | ||||

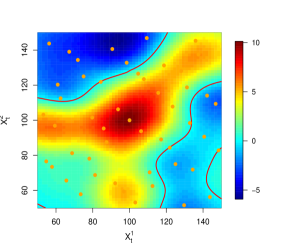

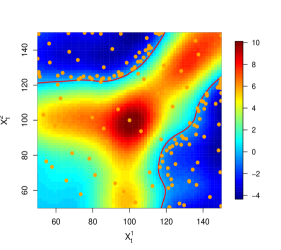

Figure 5 illustrates the ZC-SUR algorithm in a 2D Max-Call setting of Section 6.2. The left panel shows the initial Sobol macro design of sites. The right panel shows the augmented design . At each site, a batch of replications is used to reduce intrinsic noise. We observe that the algorithm aggressively places most of the new design sites around the zero-contour of , primarily lowering the surrogate variance (i.e. maximizing accuracy) in that region.

|

|

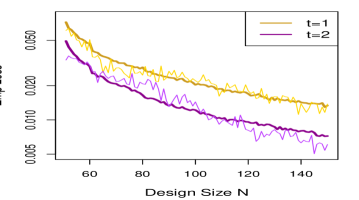

The empirical integrated local loss from (3.9) provides an indicator of algorithm performance by quantifying the accuracy of . This is particularly relevant for the sequential design approach, where one is able to track as the designs are augmented. Figure 6 shows the evolution of as function of the macro-design size for two different time steps and the same 2D Max-Call contract. We observe that is generally decreasing in ; the SUR criterion intuitively makes the latter a random walk with negative drift given by . Also, we observe that approximation errors are larger for later time steps, i.e. is increasing. This is because is based on the underlying distribution of ; for larger the volume of the effective support of the latter grows, lowering the density of the design sites. This increases surrogate variance and in turn raises the local loss in (3.8).

While the values of are not sufficient on their own to yield a confidence interval for the option price (due to the complex error propagation), self-assessment allows the possibility of adaptive termination of Algorithm 1. For example, one could implement Algorithm 1 until for a pre-specified tolerance level. From above discussion, this would lead to larger experimental designs for close to which in particular would counteract error propagation.

6. Numerical Experiments

We proceed to implement our RMC methods on three different types of Bermudan options in dimensions . Our examples are based on previously published parameter sets, allowing direct comparison of relative accuracy. To benchmark our approach, we compare against two implementations of the conventional LSMC, namely global polynomial bases, and local piecewise-linear bases from the method of Bouchard and Warin [6]. The latter consists of sub-dividing into equi-probable rectangular sub-domains and separately regressing against in each cell. This strategy does not require user-specified basis function selection for (2.12), although it is sensitive to the chosen number of sub-domains. In each case study, to enable “apples-to-apples” comparison of different RMC methods, all approximations of are evaluated on a fixed out-of-sample set of paths of .

6.1. Benchmarked Examples

While our first visualizations were in 1-D, to offer more realistic setups we use as benchmarks two-dimensional and 3-dimensional models. In both cases we work with independent and identically distributed geometric Brownian motion factors . As a first example we consider a two-dimensional basket Put where each asset follows the GBM dynamics (4.1) under same parameters as in Section 4.4, namely , . The payoff is with and , leading to option value of . For our second example, we consider a three-dimensional rainbow or max-Call payoff . The parameters are from Andersen and Broadie [2]: , , , , with option value of .

As a first step, Tables 1-2 show the impact of different experimental designs. We concentrate on the space-filling designs, evaluating the randomized LHS design, as well as two low-discrepancy sequences (Halton and Sobol), varying the batch sizes . For completeness, we also compare them against the Probabilistic density-based design, and a Sequential (namely ZC-SUR) DoE strategies. For the basket Put (see Table 1), the designs operate with the triangular input space which covers the relevant in-the-money region of the contract and we use (the QMC sequences were generated in a cube and then restricted to the triangular subset). For the max-Call (see Table 2), the designs are on the rectangular region with . In both examples we purposely choose a very limited simulation budget ( for the 2-D Put and for the 3-D Call) to accentuate the difference between the methods.

Not surprisingly, fully capturing the shape of the exercise boundary with just a handful of design sites (even in the idealized setting where one obtains a noise-free sample of at an optimal collection ) is impossible. Nevertheless, compared to having tens of thousands of design sites in LSMC, being able to get away with a couple hundred macro-sites is almost magical. In this example we also see that the probabilistic design performs very well, partly because the Put is ATM originally. At the same time the performance of an LHS design is a little bit off, and the two low-discrepancy sequences perform essentially the same. We stress that differences of less than 0.1 cents in are essentially negligible, so that the main conclusion from Table 1 is that the precise structure of a space-filling DoE design seems to play only a minor role.

Relative to conventional LSMC, the more sophisticated kriging meta-model introduces significant regression overhead. In standard RMC, about 95% of simulation time is spent on path-generation and the rest on regression; in our approach this allocation is turned on its head with of time devoted to regression. This becomes even more extreme in sequential methods, where the time cost of simulations becomes essentially negligible. The regression cost arises due to the complexity of making predictions (3.5) with the kriging model; as the size of the macro design increases, this becomes the dominant expense of the whole algorithm. As a result, the running time of our method is very sensitive to . For comparison, at , a single run for the 2-D Put problem took 8 seconds in our computing environment, took 20 seconds, and took 190 seconds. The situation is even more acute for the sequential DoE that is an order of magnitude slower; for that reason we have not run (which takes many minutes) in that case. The above facts indicate that batching is essential to adequate performance of the kriging RMC. A full investigation into the optimal amount of batching (the choice of in (3.7)) is beyond the scope of this paper. However, based on our experience, we suggest that would be appropriate in a typical financial context, offering a good trade-off between computational speed-up from replication and maintaining an adequate number of distinct design sites.

Table 3 illustrates the effect of choosing different kriging kernels ; we consider the Matern-5/2 (3.4), Gaussian/squared-exponential (3.3) and Matern-3/2 families [37]. In each case kernel hyper-parameters are fitted in a black-box manner by the DiceKriging software and underlying design was space-filling using the Sobol sequence. As expected, optimizing the kernel gives more accurate results, improving the previous, fixed-kernel answers in Tables 1-2 above; it also adds about 20% additional time. The other conclusion is that the choice of the kernel family has a negligible effect on performance. Hence, for the rest of the experiments we work with the default choice of a squared-exponential kernel.

From the above experiments, the following guidance can be given for implementing kriging RMC: pick in the range 50–100 which is sufficient to estimate reasonably well, and reduce macro design size significantly; use whatever kernel family and hyper-parameter optimization the software recommends. As a goodness-of-fit check, examine posterior variance along the estimated stopping boundary —it should not be too large.

6.2. Scalability in State Dimension

The max-Call setting is convenient for investigating scalability of our approaches in the dimension of the problem. In contrast to basket Put, the stopping region of a max-Call consists of several disconnected pieces. Namely, it is optimal to stop if exactly one asset is in-the-money while all other assets are below the strike . This generates disconnected stopping sub-regions in dimension . One consequence is that selecting a good domain for a space-filling design, such as one of the low-discrepancy sequences, is difficult since the continuation region is non-convex and the stopping region is disconnected. We use which encompasses the relevant parts of both stopping and continuation regions; hence, in this situation we build our metamodel for both in-the-money and out-of-the-money paths. The latter is rather large, hurting the accuracy of space-filling designs.

Following [2] we benchmark for . Table 4 shows the results from two different implementations of the LSMC algorithm (namely a global polynomial (“Poly”) basis, as well as the localized Bouchard-Warin (“BW11”) [6] scheme, and comparing them to two kriging metamodels, one using a space-filling design utilizing the low-discrepancy Sobol sequence (“Krig+Sobol”) and the other a sequential ZC-SUR design (“Krig+SUR”). To show the advantage of our approach, we use an order-of-magnitude smaller design for Krig+Sobol, and an even smaller one for the adaptive Krig+SUR method. For large , the standard LSMC approach requires hundreds of thousands of -trajectories which may impose memory constraints, so these savings are impressive.

In terms of overall simulation budget measured by the number of 1-step simulations of (see fourth column of Table 4), the use of better experimental designs and kriging meta-models enables a factor of 2-5 savings, which is smaller than the reduction in because we do not exploit the “global grid” trick of the conventional approach. In the last five-dim. example we also see the limitation of the kriging model due to excessive regression overhead as the macro-design size rises. As a result, despite using less than 20% of the simulation budget, the overall running time, is much longer than for LSMC. With the present implementation using DiceKriging, this overhead crowds out simulation savings around . Table 4 suggests that while attractive conceptually, the gains from a sequential design strategy are marginal in terms of memory, and are expensive in terms of additional overhead. Rephrasing, one can squeeze most of the savings via a space-filling design. This observation offers a pragmatic guidance for the DoE aspect, indicating that one must balance simulation-budget savings against regression/DoE overhead. Of course, this trade-off keeps changing as more efficient large-scale kriging/RSM software is developed/used (e.g. localized kriging, see [15]).

6.3. Stochastic Volatility Examples

Lastly, we discuss stochastic volatility (SV) models. Because there are no (cheap) exact methods to simulate the respective asset prices, discretization methods such as the Euler scheme are employed. This makes this class a good case study on settings where simulation costs are more significant. Our case study uses the mean-reverting SV model with a two-dimensional state :

| (6.1) |

where is the asset price and the log-volatility factor. Volatility follows a mean-reverting stationary Ornstein-Uhlenbeck process with mean reversion rate and base-level , with a leverage effect expressed via the correlation . Simulations of are done based on an Euler scheme with a time-step . We consider the asset Put ; exercise opportunities are spaced out by . Related experiments have been carried out in [35], and recently in [1].

Table 5 lists three different parameter sets. Once again we consider the kriging meta-models (here implemented with LHS for a change) against LSMC implementation based on the BW11 [6] algorithm. Table 5 confirms that the combination of kriging and thoughtful simulation design allows to reduce by an order of magnitude. Compare for the first parameter set a kriging model with LHS design that uses (and estimates option value at 16.06) relative to the LSMC model with (and estimates option value of 16.05). For the set of examples from [1] we observe that the space-filling design does not perform as well, which most likely is due to having the inefficient rectangular LHS domain . Still, the sequential design method wins handily.

Table 5 also showcases another advantage of building a full-scale metamodel for the continuation values. Because we obtain the full map , our method can immediately generate an approximate exercise strategy for a range of initial conditions. In contrast, in conventional LSMC all trajectories start from a fixed . In Table 5 we illustrate this capability by re-pricing the Put from [1] after changing to an out-of-the-money initial condition (keeping ). For the kriging approach we use the exact same metamodels that were built for the ITM case (), meaning the policy sets remain the same. Thus, all that was needed to obtain the reported Put values was a different set of test trajectories to generate fresh out-of-sample payoffs. We note that the obtained results (compare with budget of to with ) still beat the re-estimated LSMC solution by several cents.

7. Conclusion

We investigated the use of kriging meta-models for policy-approximation based on (2.11) for optimal stopping problems. As shown, kriging allows a flexible modeling of the respective continuation value, internally learning the spatial structure of the model. Kriging is also well-suited for a variety of DoE approaches, including batched designs that alleviate non-Gaussianity in noise distributions, and adaptive designs that refine local accuracy of the meta-model in the regions of interest (and demand a localized, non-parametric fit). These features translate into savings of 50-80% of simulation budget. While the time-savings are often negative, I believe that kriging is a viable, and attractive regression approach for RMC. First, in many commercial-grade applications, memory constraints are as important as speed constraints. Speed is generally much more scalable/parallelizable than memory. Second, as implemented, the main speed bottleneck comes from cost of building a kriging model; alternative formulations get around this scalability issue, and more speed-ups can be expected down the pike. Third, kriging brings a suite of diagnostic tools, such as a transparent credible interval for the fitted that can be used to self-assess accuracy. Fourth, through its analytic structure kriging is well suited for automated DoE strategies.

Yet another advantage of kriging, is a consistent probabilistic framework for joint modeling of and its derivatives. The latter is of course crucial for hedging: in particular Delta-hedging is related to the derivative of the value function with respect to . In the continuation region we have , so that a natural estimator for Delta is the derivative of the meta-model surrogate , see e.g. [44, 21]. For kriging metamodels, the posterior distribution of the response surface derivative is again Gaussian and thus available analytically, with formulas similar to (3.5)-(3.6). We refer to [10] for details, including an example of applying kriging for computing the Delta of European options. Application of this approach to American-style contracts will be explored separately.

The presented meta-modeling perspective modularizes DoE and regression, so that one can mix and match each element. Consequently, one can swap kriging with another strategy, or alternatively use a conventional LSMC with a space-filling design. In the opinion of the author, this is an important insight, highlighting the range of choices that can/need to be made within the broader RMC framework. In a similar vein, by adding a separate pre-averaging step that resembles a nested simulation or Monte Carlo forest scheme (see [5]), our proposal for batched designs highlights the distinction between smoothing (removing simulation noise) and interpolation (predicting at new input sites), which are typically lumped together in regression models. To this end, kriging meta-models admit a natural transition between modeling of deterministic (noise-free) and stochastic simulators and are well-suited for batched designs.

Kriging can also be used to build a classification-like framework that swaps out cross-sectional regression to fit with a direct approach to estimating . One solution is to convert the continuous-valued path payoffs into labels: and build a statistical classification model for ; for example a kriging probit model. Then . Modeling rather than might alleviate much of the ill-behavior in the observation noise . These ideas are left for future work.

By choice, in our experiments we used a generic DoE strategy with minimal fine-tuning. In fact, the DoE perspective suggests a number of further enhancements for implementing RMC. Recall that the original optimal stopping formulation is reduced to iteratively building meta-models across the time steps. These meta-models are of course highly correlated, offering opportunities for “warm starts” in the corresponding surrogates. The warm-start can be used both for constructing adaptive designs (e.g. a sort of importance sampling to preferentially target the exercise boundary of ) and for constructing the meta-model (e.g. to better train the kriging hyper-parameters ). Conversely, one can apply different approaches to the different time-steps, such as building experimental designs of varying size , or shrinking the surrogate domain as . These ideas will be explored in a separate forthcoming article.

As mentioned, ideally the experimental design is to be concentrated along the stopping boundary. While this boundary is a priori unknown, some partial information is frequently available (e.g. for Bermudan Puts one has rules of thumb that the stopping boundary is moderately ITM). This could be combined with an importance sampling strategy to implement the path-generation approach of standard LSM while generating a more efficient design. See [13, 23, 14] for various aspects of importance sampling for optimal stopping. Another variant would be a “double importance sampling” procedure of first generating a non-adaptive (say density-based) design, and then adding (non-sequentially) design points/paths in the vicinity of estimated .

Acknowledgment: I am grateful to the anonymous referee and the editor for many useful suggestions which have improved the final version of this work.

References

- [1] A. Agarwal, S. Juneja, and R. Sircar, American options under stochastic volatility: Control variates, maturity randomization & multiscale asymptotics, Quantitative Finance, 16 (2016), pp. 17–30.

- [2] L. Andersen and M. Broadie, A primal-dual simulation algorithm for pricing multi-dimensional American options, Management Science, 50 (2004), pp. 1222–1234.

- [3] B. Ankenman, B. L. Nelson, and J. Staum, Stochastic kriging for simulation metamodeling, Operations research, 58 (2010), pp. 371–382.

- [4] D. Belomestny, F. Dickmann, and T. Nagapetyan, Pricing Bermudan options via multilevel approximation methods, SIAM Journal on Financial Mathematics, 6 (2015), pp. 448–466.

- [5] C. Bender, A. Kolodko, and J. Schoenmakers, Enhanced policy iteration for American options via scenario selection, Quantitative Finance, 8 (2008), pp. 135–146.

- [6] B. Bouchard and X. Warin, Monte-Carlo valorisation of American options: facts and new algorithms to improve existing methods, in Numerical Methods in Finance, R. Carmona, P. D. Moral, P. Hu, and N. Oudjane, eds., vol. 12 of Springer Proceedings in Mathematics, Springer, 2011.

- [7] P. P. Boyle, A. W. Kolkiewicz, and K. S. Tan, Pricing Bermudan options using low-discrepancy mesh methods, Quantitative Finance, 13 (2013), pp. 841–860.

- [8] J. F. Carrière, Valuation of the early-exercise price for options using simulations and nonparametric regression, Insurance: Mathematics & Economics, 19 (1996), pp. 19–30.

- [9] S. K. Chaudhary, American options and the LSM algorithm: quasi-random sequences and Brownian bridges, Journal of Computational Finance, 8 (2005), pp. 101–115.

- [10] X. Chen, B. E. Ankenman, and B. L. Nelson, Enhancing stochastic kriging metamodels with gradient estimators, Operations Research, 61 (2013), pp. 512–528.

- [11] C. Chevalier, D. Ginsbourger, and X. Emery, Corrected kriging update formulae for batch-sequential data assimilation, in Mathematics of Planet Earth, Springer, 2014, pp. 119–122.

- [12] D. A. Cohn, Neural network exploration using optimal experiment design, Neural networks, 9 (1996), pp. 1071–1083.

- [13] P. Del Moral, P. Hu, and N. Oudjane, Snell envelope with small probability criteria, Applied Mathematics & Optimization, 66 (2012), pp. 309–330.

- [14] E. Gobet and P. Turkedjiev, Adaptive importance sampling in least-squares Monte Carlo algorithms for backward stochastic differential equations, Stochastic Processes and Applications, in press (2016).

- [15] R. Gramacy and D. Apley, Local Gaussian process approximation for large computer experiments, Journal of Computational and Graphical Statistics, 24 (2015), pp. 561–578.

- [16] R. Gramacy and M. Ludkovski, Sequential design for optimal stopping problems, SIAM Journal on Financial Mathematics, 6 (2015), pp. 748–775.

- [17] R. Gramacy and N. Polson, Particle learning of Gaussian process models for sequential design and optimization, Journal of Computational and Graphical Statistics, 20 (2011), pp. 102–118.

- [18] R. Gramacy and M. Taddy, Tgp, an R package for treed Gaussian process models, Journal of Statistical Software, 33 (2012), pp. 1–48.

- [19] T. Hastie, R. Tibshirani, and J. Friedman, The elements of statistical learning: data mining, inference and prediction, Springer, 2009.

- [20] P. Hepperger, Pricing high-dimensional Bermudan options using variance-reduced Monte Carlo methods, Journal of Computational Finance, 16 (2013), pp. 99–126.

- [21] S. Jain and C. W. Oosterlee, The stochastic grid bundling method: Efficient pricing of Bermudan options and their Greeks, Applied Mathematics and Computation, 269 (2015), pp. 412–431.

- [22] D. Jones, M. Schonlau, and W. Welch, Efficient global optimization of expensive black-box functions, Journal of Global optimization, 13 (1998), pp. 455–492.

- [23] S. Juneja and H. Kalra, Variance reduction techniques for pricing American options using function approximations, Journal of Computational Finance, 12 (2009), pp. 79–102.

- [24] K. H. Kan and R. M. Reesor, Bias reduction for pricing American options by least-squares Monte Carlo, Applied Mathematical Finance, 19 (2012), pp. 195–217.

- [25] J. P. Kleijnen, Design and analysis of simulation experiments, vol. 111, Springer Science & Business Media, 2 ed., 2015.

- [26] M. Kohler, A regression-based smoothing spline Monte Carlo algorithm for pricing American options in discrete time, Advances in Statistical Analysis, 92 (2008), pp. 153–178.

- [27] , A review on regression-based Monte Carlo methods for pricing American options, in Recent Developments in Applied Probability and Statistics, Springer, 2010, pp. 37–58.

- [28] M. Kohler and A. Krzyżak, Pricing of American options in discrete time using least squares estimates with complexity penalties, Journal of Statistical Planning and Inference, 142 (2012), pp. 2289–2307.

- [29] P. Létourneau and L. Stentoft, Refining the least squares Monte Carlo method by imposing structure, Quantitative Finance, 14 (2014), pp. 495–507.

- [30] F. Longstaff and E. Schwartz, Valuing American options by simulations: a simple least squares approach, The Review of Financial Studies, 14 (2001), pp. 113–148.

- [31] D. MacKay, Information-based objective functions for active data selection, Neural computation, 4 (1992), pp. 590–604.

- [32] M. McKay, R. Beckman, and W. Conover, Comparison of three methods for selecting values of input variables in the analysis of output from a computer code, Technometrics, 21 (1979), pp. 239–245.

- [33] V. Picheny and D. Ginsbourger, A nonstationary space-time Gaussian Process model for partially converged simulations, SIAM/ASA Journal on Uncertainty Quantification, 1 (2013), pp. 57–78.

- [34] V. Picheny, D. Ginsbourger, O. Roustant, R. T. Haftka, and N.-H. Kim, Adaptive designs of experiments for accurate approximation of a target region, Journal of Mechanical Design, 132 (2010), p. 071008.

- [35] B. R. Rambharat and A. E. Brockwell, Sequential Monte Carlo pricing of American-style options under stochastic volatility models, The Annals of Applied Statistics, 4 (2010), pp. 222–265.

- [36] J. Riihimäki and A. Vehtari, Gaussian processes with monotonicity information, in International Conference on Artificial Intelligence and Statistics, 2010, pp. 645–652.

- [37] O. Roustant, D. Ginsbourger, Y. Deville, et al., Dicekriging, Diceoptim: Two R packages for the analysis of computer experiments by kriging-based metamodeling and optimization, Journal of Statistical Software, 51 (2012), pp. 1–55.

- [38] T. J. Santner, B. J. Williams, and W. I. Notz, The design and analysis of computer experiments, Springer Science & Business Media, 2013.

- [39] L. Stentoft, Assessing the least squares Monte Carlo approach to American option valuation, Review of Derivatives Research, 7 (2004), pp. 129–168.

- [40] L. Stentoft, Value function approximation or stopping time approximation: a comparison of two recent numerical methods for American option pricing using simulation and regression, Journal of Computational Finance, 18 (2014), pp. 65–120.

- [41] S. Tompaidis and C. Yang, Pricing American-style options by Monte Carlo simulation: Alternatives to ordinary least squares, Journal of Computational Finance, 18 (2013), pp. 121–143.

- [42] J. Tsitsiklis and B. Van Roy, Regression methods for pricing complex American-style options, IEEE Transactions on Neural Networks, 12 (2001), pp. 694–703.

- [43] W. C. Van Beers and J. P. Kleijnen, Kriging for interpolation in random simulation, Journal of the Operational Research Society, 54 (2003), pp. 255–262.

- [44] Y. Wang and R. Caflisch, Pricing and hedging American-style options: a simple simulation-based approach, Journal of Computational Finance, 13 (2010), pp. 95–125.

- [45] C. K. Williams and C. E. Rasmussen, Gaussian processes for machine learning, the MIT Press, 2006.

- [46] C. Yang and S. Tompaidis, An iterative simulation approach for solving stochastic control problems in finance, tech. report, Available at SSRN 2295591, 2013.