\titlealternative

Systemic risk in multiplex networks with asymmetric coupling and threshold feedback

\authoralternativeR. Burkholz, M.V. Leduc, A. Garas & F. Schweitzer

References

Rebekka Burkholz

Matt V. Leduc

Antonios Garas & Frank Schweitzer

Chair of Systems Design, ETH Zurich, Weinbergstrasse 58, 8092

Zurich, Switzerland

Systemic risk in multiplex networks

with asymmetric coupling and threshold feedback

Rebekka Burkholz

Matt V. Leduc

Antonios Garas & Frank Schweitzer

Chair of Systems Design, ETH Zurich, Weinbergstrasse 58, 8092

Zurich, Switzerland

Abstract

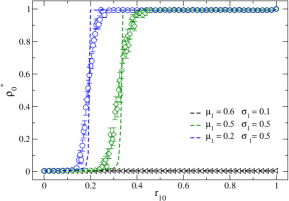

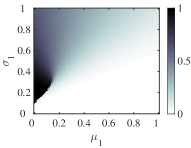

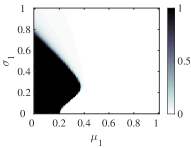

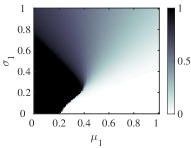

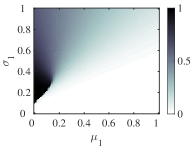

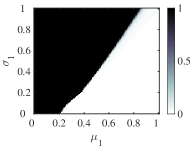

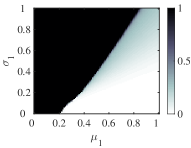

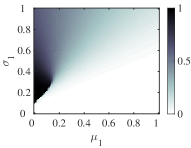

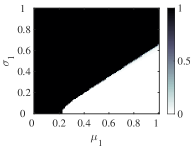

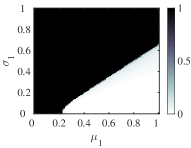

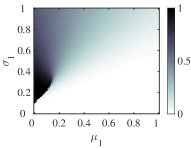

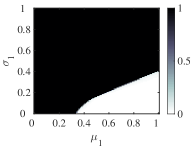

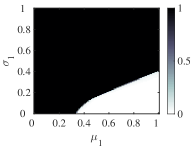

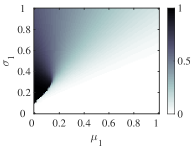

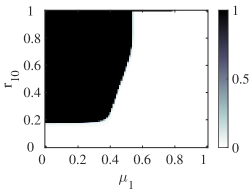

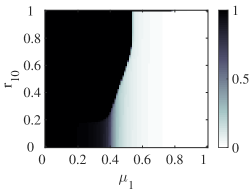

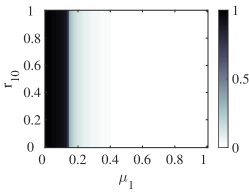

We study cascades on a two-layer multiplex network, with asymmetric feedback that depends on the coupling strength between the layers.

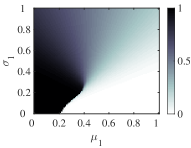

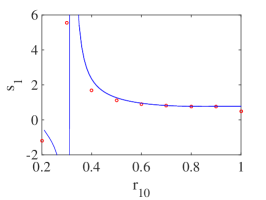

Based on an analytical branching process approximation, we calculate the systemic risk measured by the final fraction of failed nodes on a reference layer.

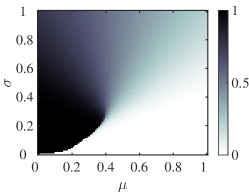

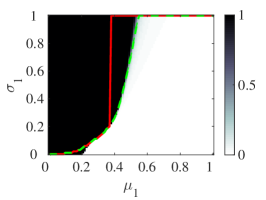

The results are compared with the case of a single layer network that is an aggregated representation of the two layers.

We find that systemic risk in the two-layer network is smaller than in the aggregated one only if the coupling strength between the two layers is small.

Above a critical coupling strength, systemic risk is increased because of the mutual amplification of cascades in the two layers.

We even observe sharp phase transitions in the cascade size that are less pronounced on the aggregated layer.

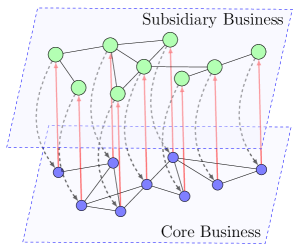

Our insights can be applied to a scenario where firms decide whether they want to split their business into a less risky core business and a more risky subsidiary business. In most cases, this may lead to a drastic increase of systemic risk, which is underestimated in an aggregated approach.

(4)

(5)

(6)