Tail fitting for truncated and non-truncated

Pareto-type distributions

Beirlant J.a111Corresponding author: Jan Beirlant, KU Leuven, Dept of Mathematics and LStat, Celestijnenlaan 200B, 3001 Heverlee, Belgium; Email: jan.beirlant@wis.kuleuven.be , Fraga Alves, M.I.b, Gomes, M.I.b,

a Department of Mathematics and Leuven Statistics Research Center, KU Leuven

b Department of Statistics and Operations Research, University of Lisbon

Abstract

Recently some papers, such as Aban, Meerschaert and Panorska (2006), Nuyts (2010) and Clark (2013), have drawn attention to possible truncation in Pareto tail modelling.

Sometimes natural upper bounds exist that truncate the probability tail, such as the Maximum Possible Loss in insurance treaties. At other instances ultimately at the largest data, deviations from a Pareto tail behaviour become apparent.

This matter is especially important when extrapolation outside the sample is required.

Given that in practice one does not always know whether the distribution is truncated or not, we consider estimators for extreme quantiles both under truncated and non-truncated Pareto-type distributions.

Hereby we make use of the estimator of the tail index for the truncated Pareto distribution first proposed in Aban et al. (2006).

We also propose a truncated Pareto QQ-plot and a formal test for truncation in order to help deciding between a truncated and a non-truncated case.

In this way we enlarge the possibilities of extreme value modelling using Pareto tails, offering an alternative scenario by adding a truncation point that is large with respect to the available data.

In the mathematical modelling we hence let at different speeds compared to the limiting fraction () of data used in the extreme value estimation.

This work is motivated using practical examples from different fields of applications, simulation results, and some asymptotic results.

Considering positive data, the Pareto (Pa) distribution is a simple and very popular model with power law probability tail.

Using the notation from Aban et al. (2006), the right tail function (RTF)

(1)

is considered as the standard example in the max domain of attraction of the Fréchet distribution. For instance, losses in property and casualty insurance often have a heavy right tail

behaviour making it appropriate for including large events in applications such as excess-of-loss pricing and enterprise risk management (ERM). There might be some practical problems with the use of

the Pa distribution and its generalization to the Pa-type model, because some probability mass can still be assigned to loss amounts that are unreasonable large or even physically impossible. In ERM this corresponds to the concept of maximum possible loss. Here we will consider specific data sets on earthquake fatalities and forest fires. For other applications of natural truncation, such as probable maximum precipitation, see Aban et al. (2006). These authors considered the upper-truncated Pareto distribution with RTF

(2)

for , where . Next to the RTF, for any given distribution, we make use

of the tail quantile function defined by () where () denotes the upper quantile function corresponding to . Henceforth, and , respectively and , denote the RTF and the tail quantile function of the underlying Pa distribution, respectively of the Pa distribution truncated at from which the data are observed with . Note the following relations between the RTFs and the tail quantile functions:

(3)

(4)

(5)

where equals the odds ratio of the truncated probability mass under the untruncated Pa-type distribution , and .

Aban et al. (2006) derived the conditional maximum likelihood estimator (MLE) based on the () largest order statistics representing only the portion of the tail where the truncated Pareto (TPa) approximation holds. They showed that, with denoting the order statistics of an independent and identically distributed sample of size from , the MLE’s obtained under this conditioning model are given by

where solves the equation

(6)

where is the Hill (1975) statistic and .

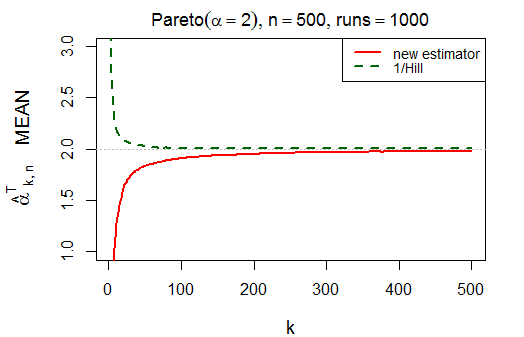

This estimator can be considered as an extension of Hill’s (1975) estimator to the case of a TPa distribution, while was introduced as an estimator of when .

Independently, Nuyts (2010) considered truncation of Pa distributions and obtained an adaptation of the Hill (1975) estimator through the estimation of for some finite, taking to be the strict Pa in (1). Then replacing by the truncation point and by some appropriate threshold , as commonly considered in extreme value methodology, we obtain in the spirit of Nuyts (2010) that

(7)

Estimating by the maximum of the sample, by an order statistic , and by ,

we find (6) again.

The estimator proposed in Nuyts (2010) differs slightly from , but can be shown to be asymptotically equivalent to . Nuyts (2010) also considered trimming the estimator by deleting the () top data, leading to the generalization of (6)

The estimator provides a way to make the Hill (1975) estimator robust against outliers, but it will be less efficient than the estimator without trimming. While robustness under Pa models has received quite some attention in the literature (see for instance Hubert et al., 2013, and the references therein), we confine ourselves to the case .

The solution of (6) can be approximated using Newton-Raphson iteration on the equation

to get

(8)

where for instance Hill’s estimator can serve as an initial approximation: .

The main purpose of this paper is to consider tail estimation for truncated and non-truncated distributions in case the Pa behaviour starts to set in from an intermediate threshold on. In case of no truncation, this setting has been formalized mathematically by the concept of Pa-type distributions, defined by

(9)

where is a slowly varying function at infinity, i.e. for every . Hence, under this model, with denoting a peak over a threshold with ,

It is well-known that then also

(10)

where is again a slowly varying function.

In extreme value statistics the parameter is referred to as the extreme value index (EVI). The EVI is the shape parameter in the generalized extreme value distribution

This class of distributions is the set of the unique non-degenerate limit distributions of a sequence of maximum values, linearly normalized. In case the class of distributions for which the maxima are attracted to corresponds to the Pa-type distributions in (9). Note that for a given fixed truncated Pa models are known to exhibit an EVI , see for instance Figure 2.8 in Beirlant et al. (2004).

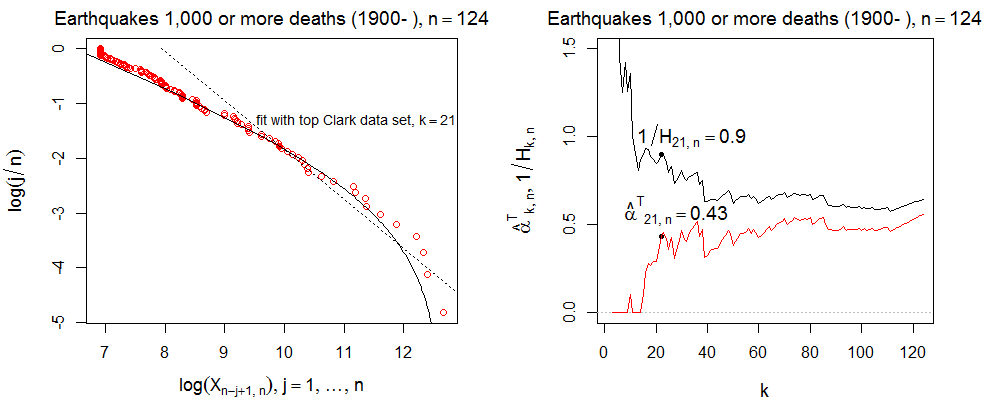

To illustrate the practical importance of the present setting, we consider the data set containing fatalities due to large earthquakes as published by the U.S. Geological Survey on http://earthquake. usgs.gov/earthquakes/world/, which were also used in Clark (2013).

It contains the estimated number of deaths for the 124 events between 1900 and 2011 with at least 1000 deaths.

In Figure 1 the Pa QQ-plot (or log-log plot)

(11)

is given. It exhibits a linear or Pa pattern for a large section of the data, while the final end of the plot is curved. The plot of as the classical estimates of based on an untruncated Pa distribution indeed bends upwards towards smaller values of . This indicates that the unbounded Pareto pattern could be violated in this example. On this plot the extrapolations using a Pa distribution (1) respectively the TPa model (2) (with the linear respectively the curved extrapolation) are plotted based on the largest 21 data points as it was proposed in Clark (2013) such that and .

In section 3 tail extrapolation based on the TPa model will indeed appear to be appropriate in this case.

Figure 1: Earthquake fatalities data set. Left: Pa QQ-plot with extrapolations anchored at based on a non-truncated Pa model in (1) (dotted line) and a truncated Pareto model in (2) (full line) as proposed in Clark (2013). Right: plot of and for .

As suggested in Clark (2013) could also be taken to be zero or negative. For instance formally setting in (2), one obtains the tail of a uniform type distribution. Finite tail distributions following (2) with negative value of show a fast rate of convergence to for small and when is a big number, due to the presence of in this expression. In the applications we have in mind here, as we allow to be large, convergence to is slow and hence a positive value of is appropriate. Closely related to this paper, Chakrabarty and Samorodnitsky (2012) considered a different truncation model, whereby a heavy tailed random variable is truncated at a high value added by exponentially tailed random variables , and where the probability mass under behind is set at . These authors show the consistency of Hill’s estimator and provide a test for this kind of truncation. They did not consider the estimation of extreme quantiles however.

In the next sections we specify the truncation models and provide estimators for extreme quantiles and for . In section 4 we consider the problem of deciding between a Pa-type case in (9) and a TPa-type case in (12), or, between light and rough truncation. To this end we construct a TPa QQ-plot, provide a new significance test and compare it with the test proposed in Aban et al. (2006).

In section 5 we study the finite sample behaviour of the proposed estimators using simulations and practical examples. The asymptotic properties of and the extreme quantile estimators under rough and light truncation are discussed in a final section. Proofs will be deferred to the supplementary material.

2 Rough and light truncation of Pareto-type distributions

Truncation of a Pa-type distribution at a value necessarily requires and

One can now consider two cases as :

•

Rough truncation when , and by Karamata’s uniform convergence theorem for regularly varying functions (Seneta, 1976),

(12)

This corresponds to situations where the deviation from the Pa behaviour due to truncation at a high value will be visible in the data, and an adaptation of the

classical Pa tail extrapolation methods appears appropriate.

•

Light truncation when

(13)

and hardly any truncation is visible in the data, and the Pa-type model (9) without truncation and the existing extreme value methods for Pa-type tails are appropriate.

Since and , we now obtain that if is bounded away from 0

(15)

where as using Karamata’s uniform convergence theorem. Note that in case satisfies (1).

In case it follows similarly from (4) that

(16)

Hence, with playing the role of , and choosing , the conditions of rough and light truncation are rephrased as follows, in accordance with (15) and (16):

•

Rough truncation when

and

(17)

•

Light truncation when

and

The estimation of and (or , ) will now constitute important steps in order to arrive at estimators of extreme quantiles and .

Given the fact that our model is only defined choosing , jointly with the corresponding conditions for rough and light truncation, the underlying model depends on and a triangular array formulation of the observations should be used in order to emphasize the nature of the model. However, in statistical procedures as presented here, when a single sample is given, the notation is more natural and will be used throughout.

3 Estimation of extreme quantiles

From (15) it is clear that the estimation of is an intermediate step in important estimation problems following the estimation of , namely of extreme quantiles and of the endpoint .

From (15)

as an estimator for in case of truncated and non-truncated Pa-type distributions.

In practice we will make use of the admissible estimator

In case , in order to construct estimators of and extreme quantiles ,

as in (18) we find that

(20)

Then taking logarithms on both side of (20) and estimating by we find an estimator of :

(21)

Note that can also be rewritten as

(22)

(23)

An estimator of follows from letting ,

taking the maximum with in order for this endpoint estimator to be admissible.

Equation (23) for constitutes an adaptation to the TPa case of the Weissman (1978) estimator

(24)

which is valid under (9). Expression (23) is more adapted to the case of light truncation or . Version (22) can be linked to the case of rough truncation or .

Version (21) can be applied in all cases. However in section 5, in case of light truncation will be shown to be consistent only when . When this condition is not satisfied under light truncation we propose to use

(25)

Note that such alternative expressions do not exist for the estimation of the endpoint as in case no finite endpoint exists.

4 Goodness-of-fit and testing for truncated Pareto-type distributions

From the preceeding sections the need for goodness-of-fit and test for truncated Pa distributions became apparent.

Based on a chosen value for particular , we propose the TPa QQ-plot to verify the validity of (15):

(26)

Note that when or the TPa QQ-plot agrees with the classical Pareto QQ-plot (11).

Under (15) an ultimately linear pattern should be observed to the right of some anchor point, i.e. at the points with indices for some . From this, we propose to choose the value of in practice

as the value that maximizes the correlation between and for and . This choice can be improved in future work since the covariance structure of the deviations of the points on the TPa QQ-plot from the reference line are neither independent nor identically distributed. This issue was addressed for the Pa QQ-plot in Beirlant et al. (1996) and Aban and Meerschaert (2004) and should be considered in the truncated case too.

Aban et al. (2006) already proposed a test for versus under the strict Pa and TPa models, rejecting at asymptotic level when

(27)

for some and where in (1). In (27), is estimated by the maximum likelihood estimator under based on the Hill (1975) estimator

while

(28)

Note that the rejection rule (27) can be rewritten as

(29)

and the p-value is given by .

Here we also consider the problem of testing light versus rough truncation, i.e.

In the next sections we inspect the finite sample and asymptotic properties of the test (27) under and .

We propose also a different test rejecting when an appropriate estimator of is significantly different from 0. Here we construct such an estimator generalizing with an average of ratios , which then possesses an asymptotic normal distribution under the null hypothesis. Observe that under (15) as

Estimating by

leads now to

(30)

as an estimator of , with an appropriate estimator of .

Under the reciprocal of the Hill (1975) estimator is an appropriate estimator of . Moreover, in the final section it will be stated that under some regularity assumptions on the underlying Pa-type distribution, we have under for and , that is asymptotically normal with mean 0 and variance 1/12.

Moreover, it is then also shown that under rough truncation

as , and

so that an asymptotic test based on rejects on asymptotic level when

(31)

with . The p-value is then given by .

Both tests (27) and (31) will further be compared below.

5 Practical examples and simulations

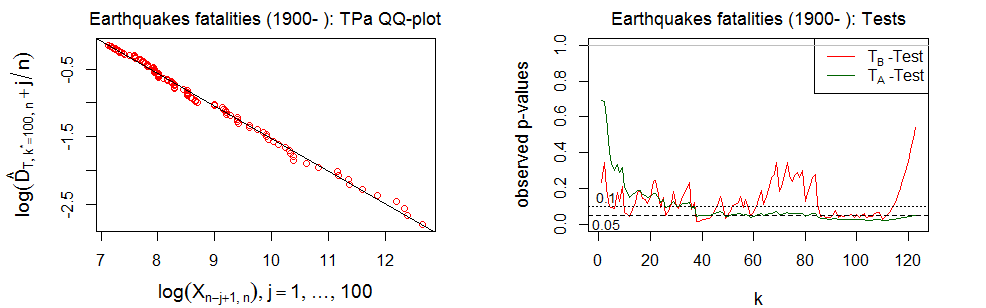

First we retake the data set containing fatalities due to large earthquakes from Figure 1.

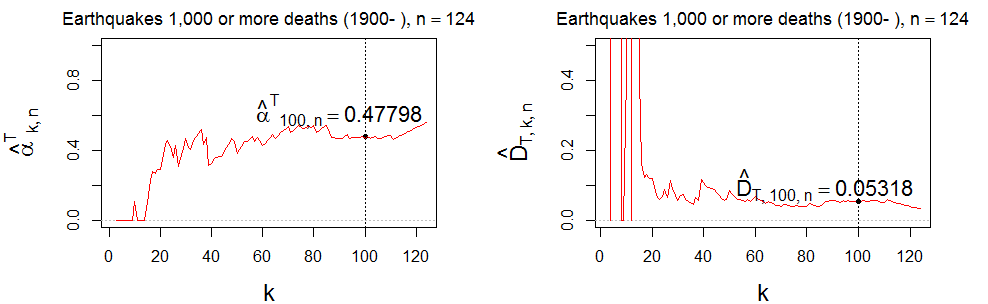

In Figure 2 (middle) the estimates and are plotted against . Here we have chosen as a typical value where both plots are horizontal in .

The TPa QQ-plot in (26) is given in Figure 2 (top left), using the above mentioned value . Next, the p-values as a function of , both for the and tests are given (top right).

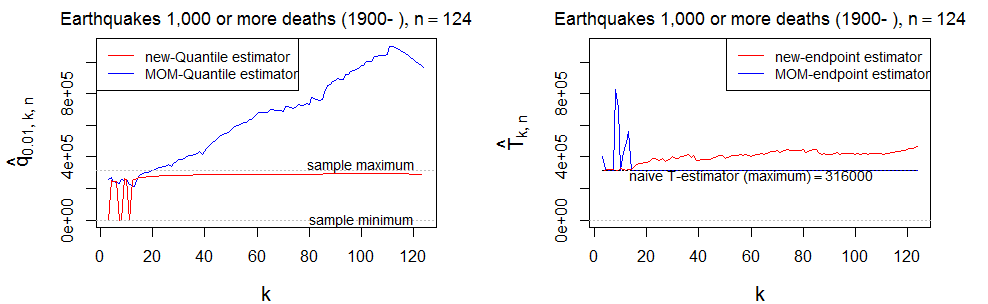

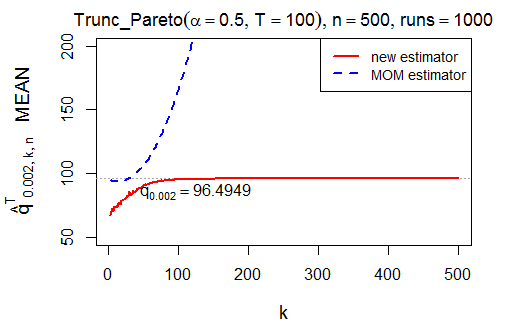

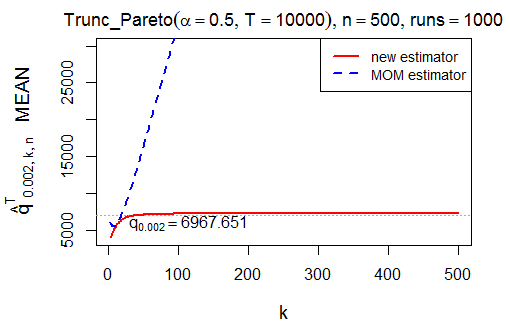

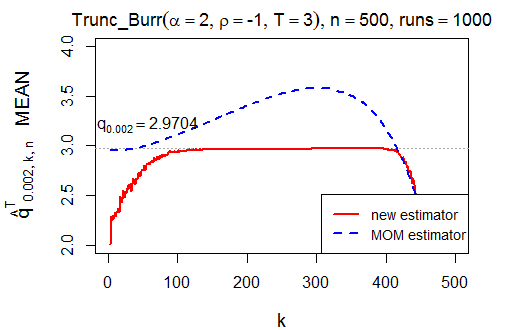

Finally in Figure 2 (bottom) the estimates of the extreme quantile using (21) and the endpoint (obtained by letting ) are presented as a function of . They are contrasted with the values obtained by the classical method of moment estimates as introduced in Dekkers et al. (1989) illustrating the slow convergence of the classical extreme value methods in the TPa-type model we study here.

For any real EVI, the classical moment -estimator is defined by

(32)

with , , which constitutes a consistent estimator for . The Hill estimator is .

The MOM-estimators for high quantiles and right endpoint, based on the moment estimator , are defined by

(see de Haan and Ferreira, 2006, , for details)

(33)

and

(34)

Notice that in (34) corresponds to the admissible version of the moment endpoint estimator , since the latter can return values below the sample maximum.

Concerning the high quantile estimation, the chosen value is directly related to the modest sample size here of . The quantile estimates reveal a stable pattern on , in Figure 2 (bottom left).

While on the basis of Figure 2, is only border significant for small values of , the TPa-type model with a truncation point around 400,000 deaths offers a convincing fit, and leads to a useful estimator for extreme quantiles.

Figure 2: Earthquake fatalities data set. Top: TPa QQ-plot (left) for the earthquake fatalities data set using ; plot of p-values based on and . Middle: plots of Pareto index (left)

and odds ratio estimates () (right) marking the values at . Bottom: quantile estimates (left) and endpoint estimates (right) contrasted with the method of moments quantile and endpoint estimators, in (33) and (34), respectively.

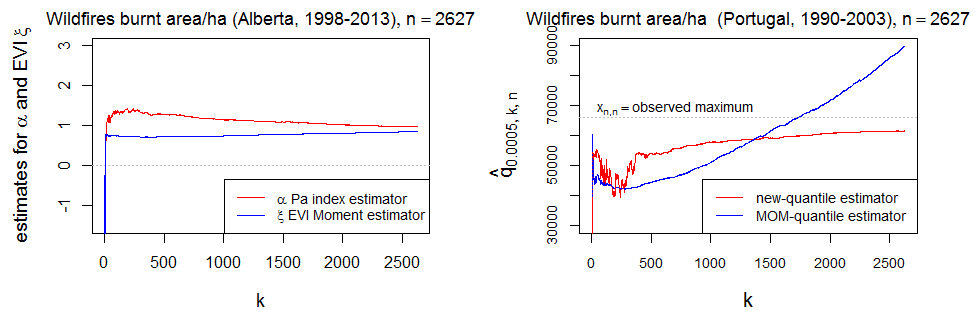

Another application can be found in statistical modelling of size distributions of forest fires. Power law distributions have appeared in literature for modelling such sizes, while Reed and McKelvey (2002) provided evidence that in some circumstances this is too simple to describe such distributions over their full range. We consider here two data sets with sizes of wild fires from Alberta (Canada) from 1998-2013 () that can be found on

http://wildfire.alberta.ca/wildfire-maps/historical-wildfire-information/spatial-wildfire-data.aspx, together with a data set, recently considered in Gomes et al. (2012) and in Brilhante et al. (2013), containing the number of hectares, exceeding 100 ha, burnt during wildfires recorded in Portugal from 1990 till 2003 ().

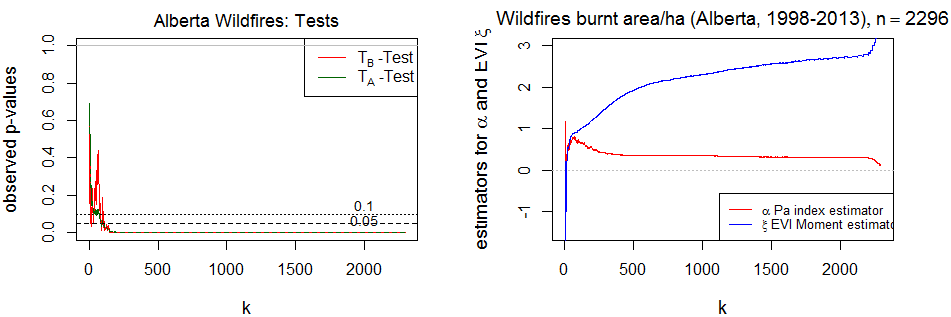

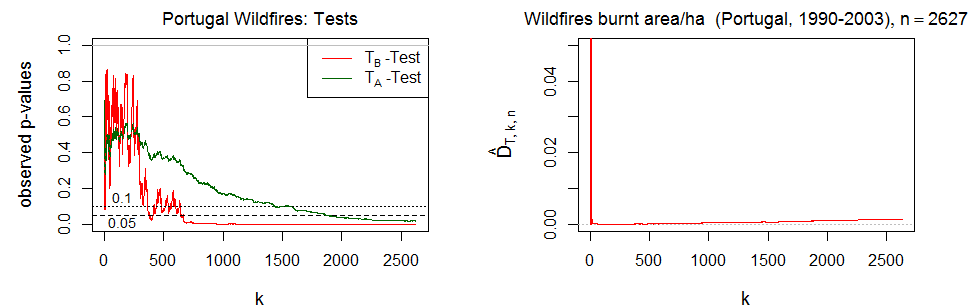

Both tails are analyzed in Figure 3 for the Alberta data set and in Figure 4 for the Portuguese data. While for the Portugal case study light truncation or Pareto-type behaviour cannot be rejected, the rough truncation model fits the Alberta wildfires data much better than the unbounded model.

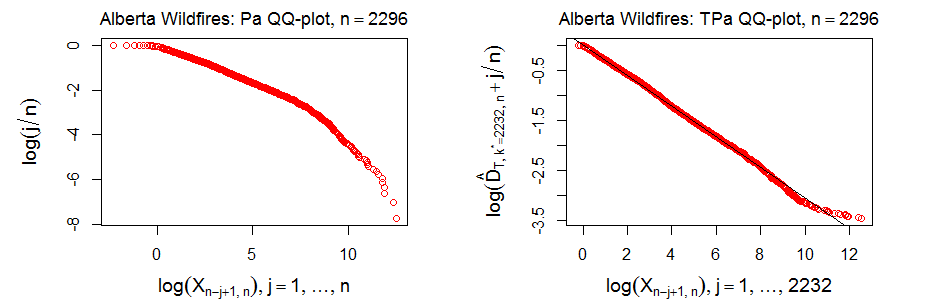

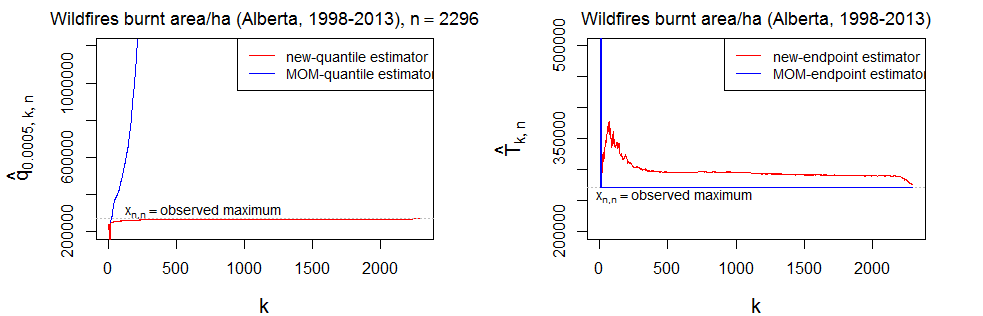

Figure 3: Alberta wildfires. Top: Pa QQ-plot (left); TPa QQ-plot (right) using the top data. Middle: plots of p-values for and tests (left), and Pa index (right) estimates contrasted with the method of moments estimates in (32). Bottom: quantile estimates (left) and endpoint estimates (right) contrasted with the method of moments quantile and endpoint estimators, in (33) and (34), respectively.

For the Alberta data set, in Figure 3 (top right), the TPa QQ-plot in (26), associated with the validity of (15), has been built on the chosen value , which maximizes the correlation between and , , for . For the Pareto index , high quantile and right endpoint estimation in Figure 3 we get conclusions similar to the ones of the earthquake fatalities data set.

Figure 4: Portugal wildfires. Top: Pa QQ-plot. Middle: plots of p-values for and tests (left) , and odds ratio estimates (right). Bottom: Pa index estimates (left) and quantile estimates (right) contrasted with the method of moments index and quantile estimators, in (32) and (33), respectively.

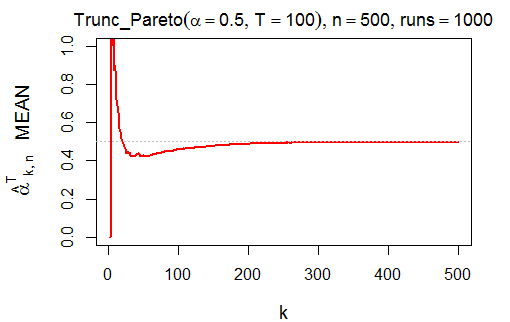

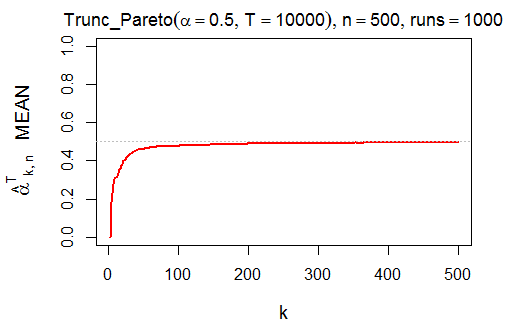

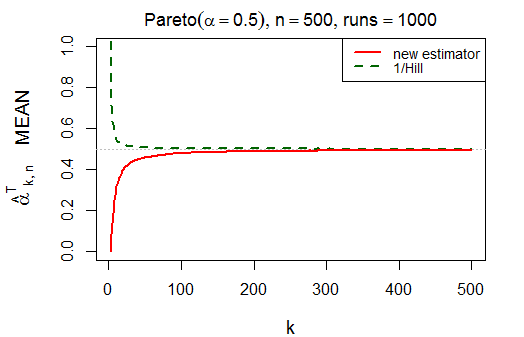

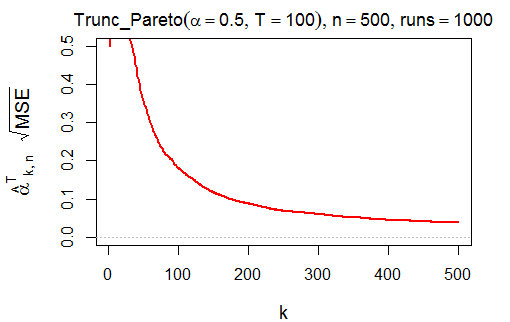

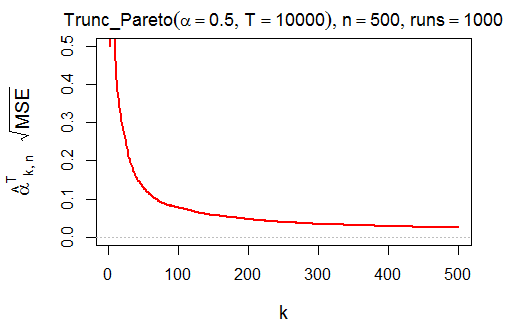

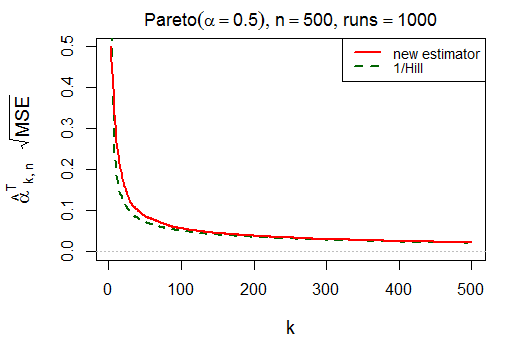

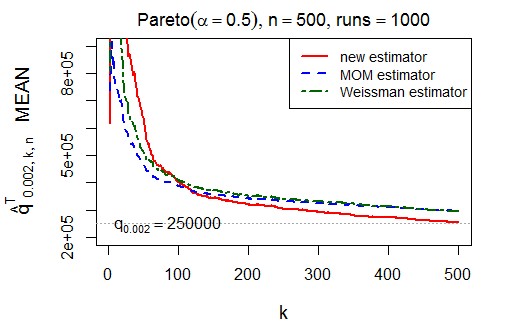

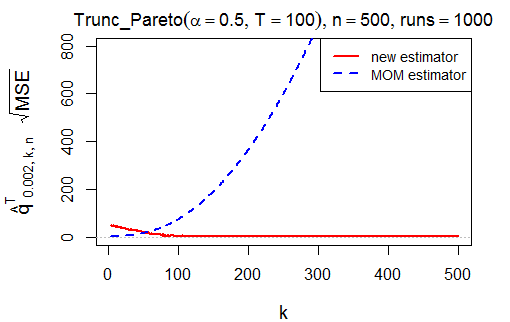

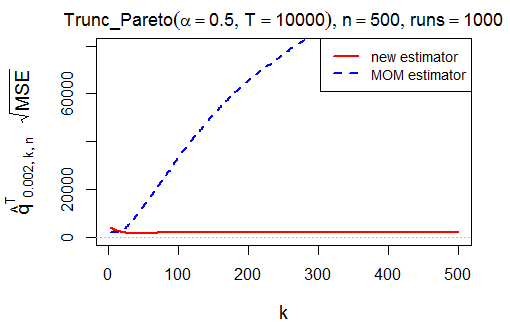

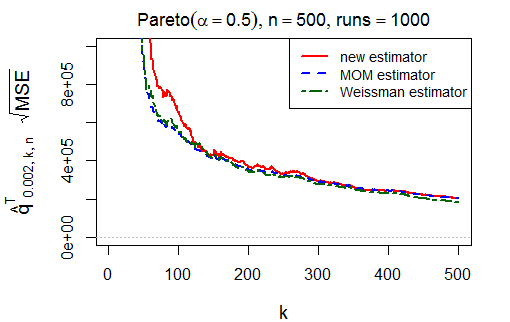

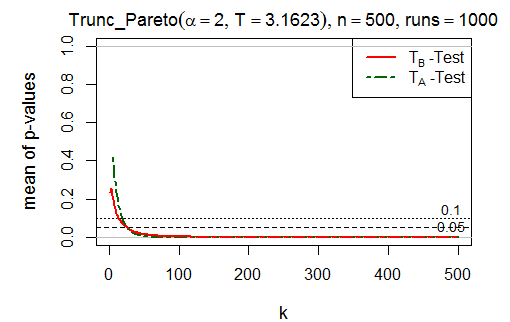

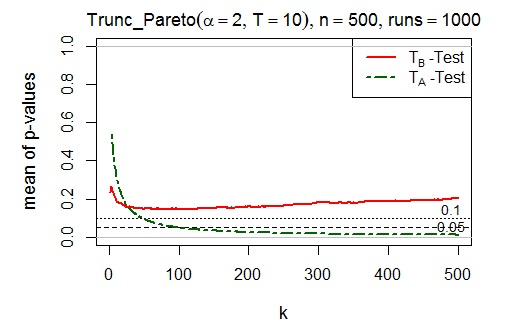

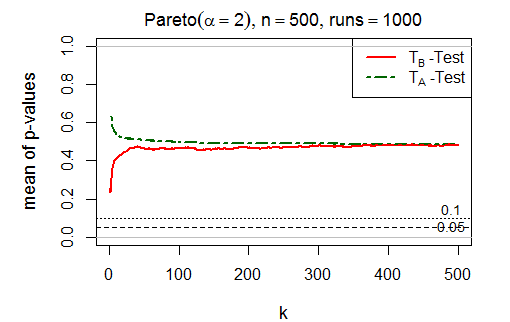

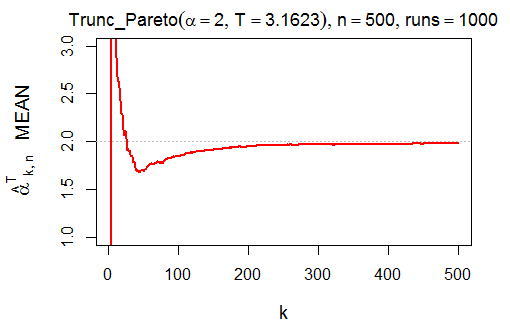

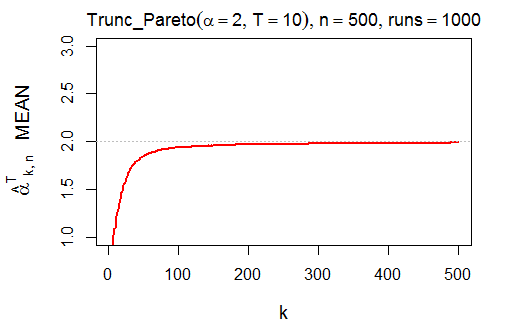

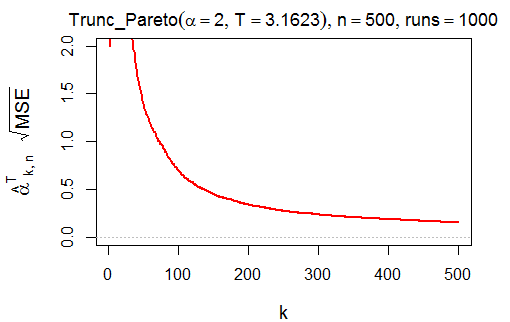

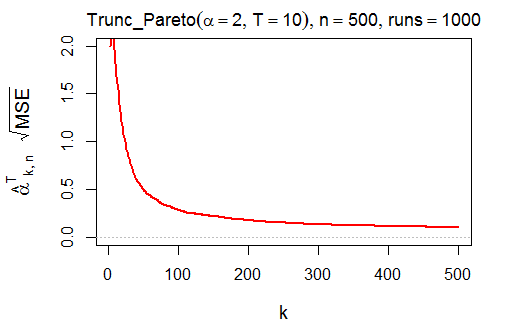

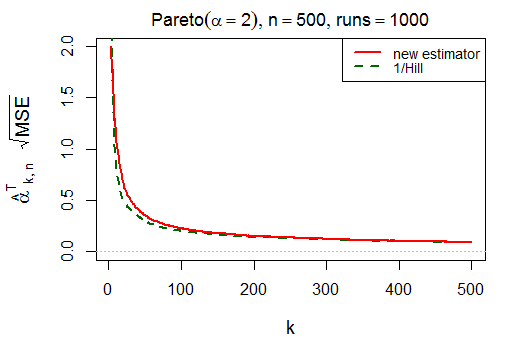

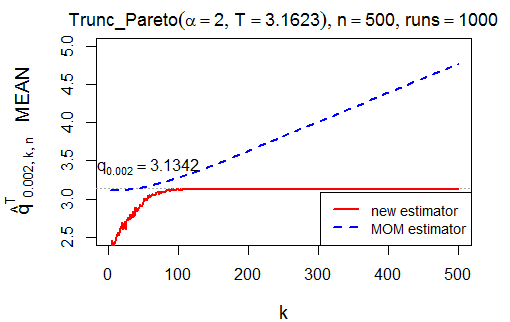

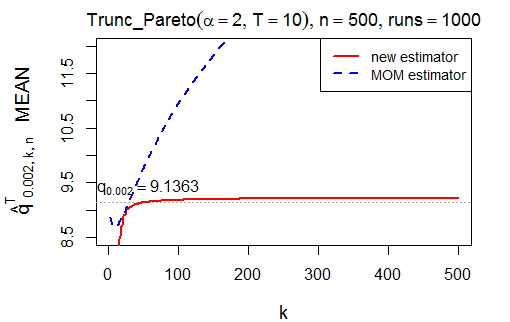

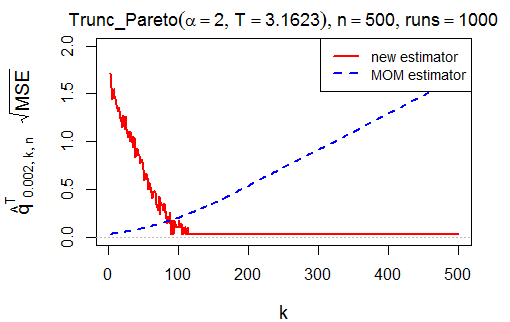

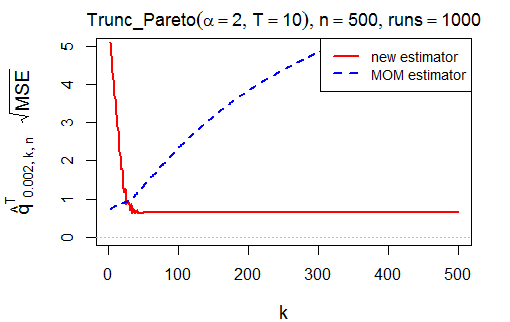

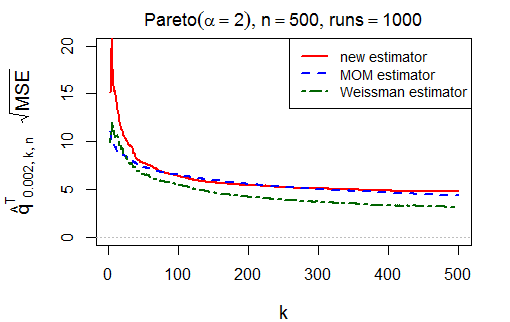

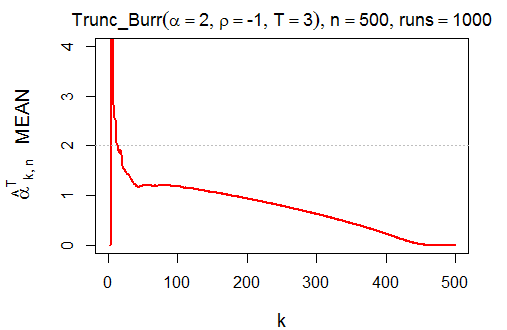

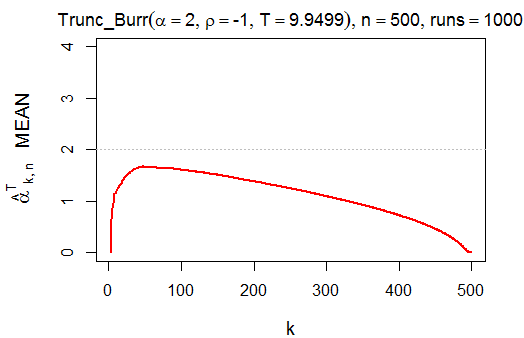

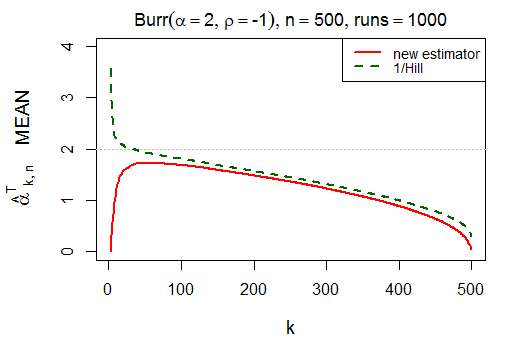

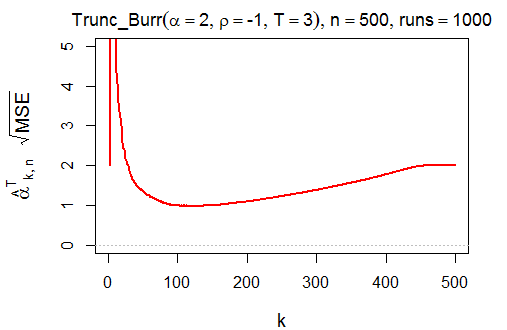

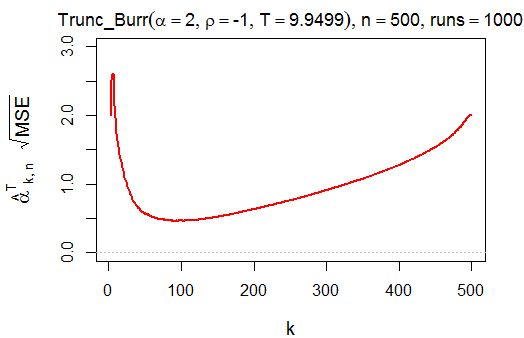

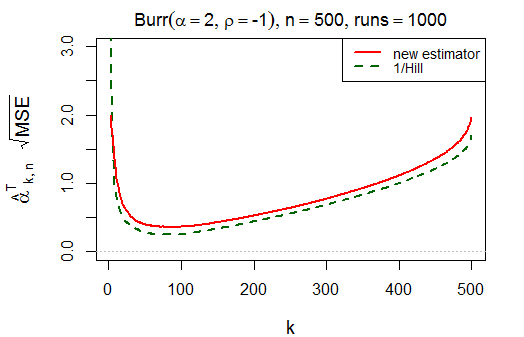

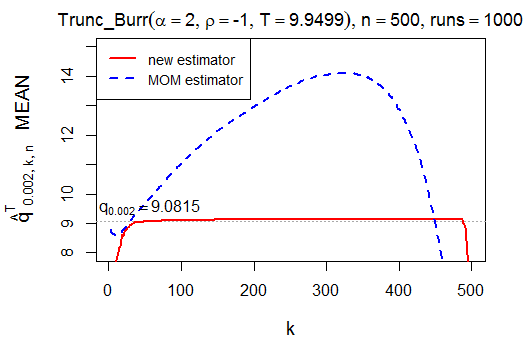

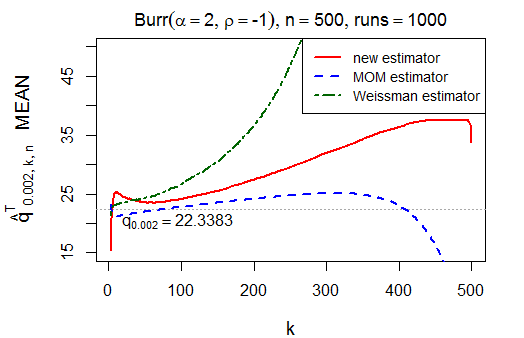

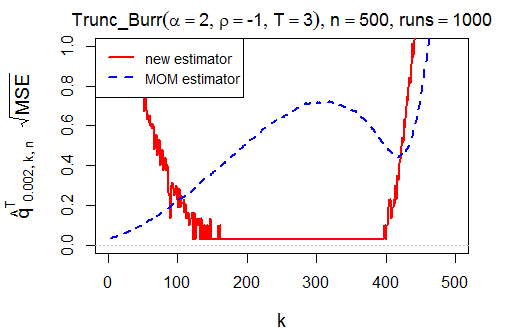

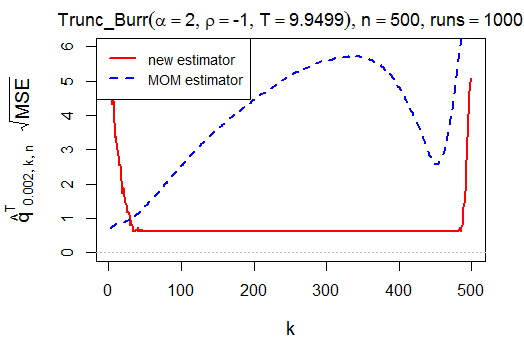

The finite sample behaviour of the proposed estimators based on (6) and (8), from (21), and from (23) has been studied through an extensive Monte Carlo simulation procedure with 1000 runs, both for truncated and non-truncated Pa-type distributions. Here we will only present results concerning Pa and Burr distributions, with truncated and non-truncated versions with sample size :

1.

Non-truncated models

(a)

Pareto(),

(35)

(b)

Burr(), ,

(36)

2.

Truncated models

(a)

Truncated-Pareto(), and a high quantile from the corresponding Pareto model (35)

(37)

(b)

Truncated-Burr(), , and a high quantile from the corresponding Burr model in (36)

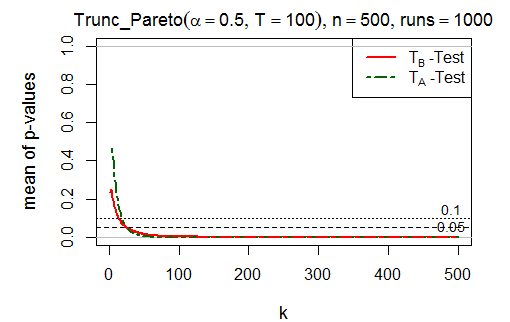

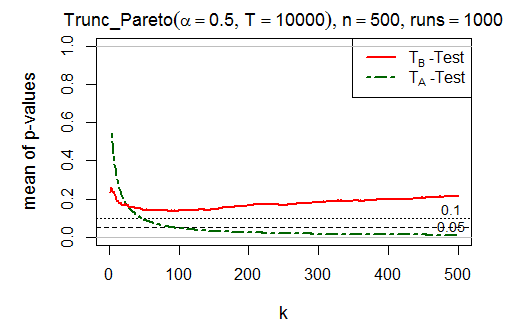

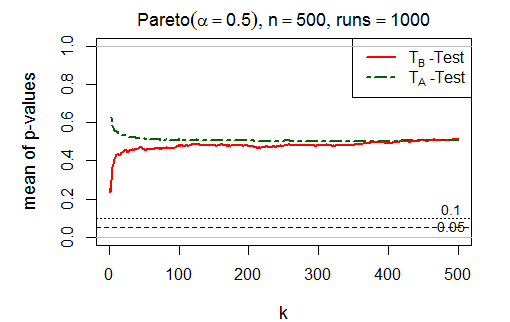

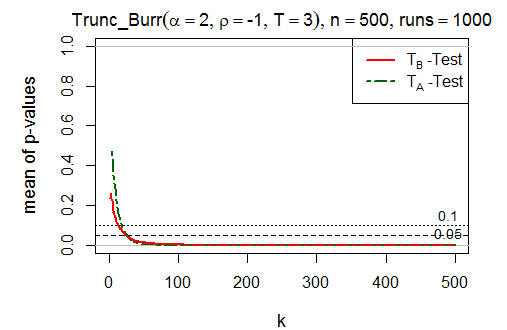

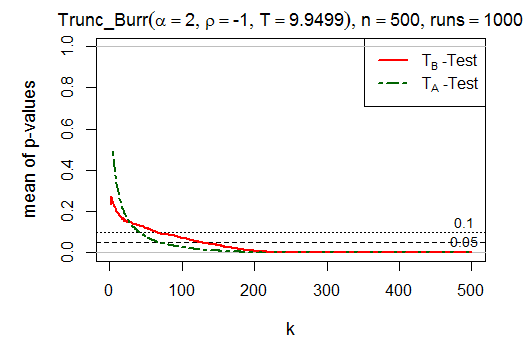

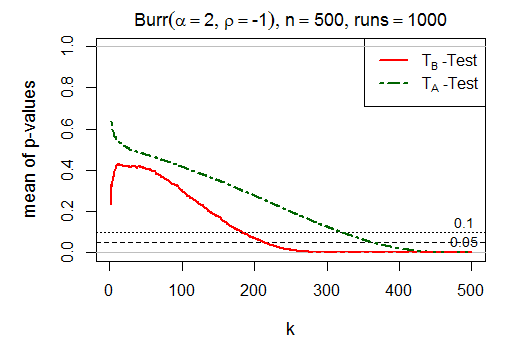

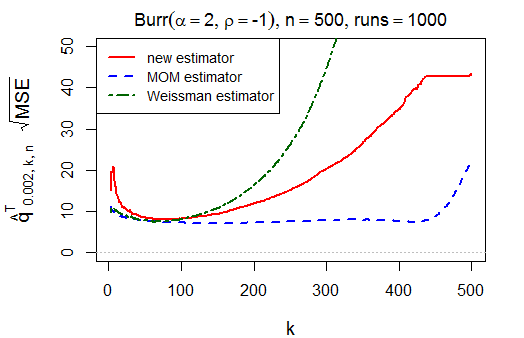

For a particular data set from an unknown but apparently heavy-tailed distribution, the practitioner does not know if the distribution comes from a truncated or a non-truncated Pa-type distribution and hence we have to study the behaviour of the tests and the proposed estimators under both cases, and compare them with the existing estimators where appropriate. Our simulation results illustrate this, using three columns in Figures 5-7, setting the cases where equals the 90 and 99 percentile of the corresponding non-truncated Pa random variable next to the case where . The case serves as an illustration of the rough truncation case, while is meant to represent light truncation.

Figure 5: Pa: Left column: ; Middle column: ; Right column: . Means of p-values of tests based on and (first row). Estimation of using the Newton-Raphson procedure with initial value : mean (second row) and (third row). Estimation of the high quantile using , , and (last column): means (fourth row) and (fifth row).

The mean of the p-values show that both tests and strongly reject the hypotheses and in case

. In the case test rejects more clearly in contrast to the test which then appears more appropriate to test . In case of a Burr distribution for with , rejects more often for as the deviation from the Pa-model begins to set in for this Pa-type distribution .

Figure 6: Pa: Left column: ; Middle column: ; Right column: . Means of p-values of tests based on and (first row). Estimation of using the Newton-Raphson procedure with initial value : mean (second row) and (third row). Estimation of the high quantile using , , and (last column): means (fourth row) and (fifth row).

The -estimator represented in Figures 5-7 is the solution of (6), approximated using the Newton-Raphson iteration as in (8), with an initial value . With finite samples and fixed , TPa-type distributions belong to the Weibull domain of attraction for maxima with EVI

so that the moment estimator in (32) almost surely converges to -1. Also, for these models, does not constitute a consistent estimator either for or for , since in case the Hill estimator almost surely tends to zero when as . Only when we have that and estimate the same value . In case of the truncated Burr distribution the Pareto

index estimator is underestimating , which is not uncommon in extreme value analysis, and is in fact comparable to the behaviour of in this case.

When estimating an extreme quantile the estimator in (33) based on the moment estimator is designed both for truncated and non-truncated cases and is to be compared with the estimation procedure defined in (23). Finally and the Weissman (1978) extreme quantile estimator from (24) are competitors in case of non-truncated Pa-type distributions only.

The convergence of the new quantile estimators seems to be attained at low thresholds (or high ) with high accuracy, contrasting with higher thresholds (or low ) for MOM class estimators. With quantile estimation an erratic behaviour appears under rough truncation in Figures 6-7 for some smaller values of . This is a consequence of the use of rather than in practice. If we assume that is finite then using simply rather than produces much smoother performance in extreme quantile estimation.

On the other hand in case of non-truncated models the use of instead of , leads to extreme quantile estimates that are quite sensitive with respect to the value of . While the stable parts in the plots of quantile estimates are readily apparent anyway, we here use in (21).

In case of non-truncated Pa-type models (right columns) concerning high quantile estimation,

taking into account that and are designed for this particular situation, we can conclude that the newly proposed estimators perform reasonably well at around if we compare with the classical Weissman and moment-type extreme quantile estimators. For instance in case of the Burr distribution in Figure 7 it appears that our quantile estimator is slightly worse than the moment estimator but better than the Weissman (1978) estimator. Finally note that for quantile estimators the relative values can be obtained dividing the presented absolute error by the exact value of .

Figure 7: Burr: Left column: ; Middle column: ; Right column: . Means of p-values of tests based on and (first row). Estimation of using the Newton-Raphson procedure with initial value : mean (second row) and (third row). Estimation of the high quantile using , , and (last column): means (fourth row) and (fifth row).

6 Asymptotics of estimators and tests

In this section we state the large sample distribution of and defined in (6) and (21) for TPa-type distributions both under rough (12) and light (13) truncation.

To this end we will make use of the expressions (15)-(14) and (16) for the upper quantile function both under rough and light truncation assuming that is continuous. We also make use of a second order slow variation condition on

specifying the rate of convergence of to 1 as , which is used typically in all asymptotic results in extreme value methods (see for instance Theorem 3.2.5 in de Haan and Ferreira, 2006):

(39)

with , , and regularly varying with index , i.e. as for every .

Finally represents a standard Wiener process.

Remark 1. In case the asymptotic result for is identical to that of the Hill estimator under a Pa-type distribution, as given for instance in Beirlant et al. (2004), section 4.2.

Theorem 2.

Suppose (39) holds and , , and such that . Moreover denotes a standard exponential random variable.

(a)

Let . Then

(b)

Let , , , and . Then

If then

Remark 2. In case both the asymptotic bias and the stochastic part of are of smaller order than in case of . This confirms the findings of the simulations where the

plots of the quantile estimators are found to be quite horizontal as a function of and show a small variance, compared to other extreme quantile estimators in this case.

In case , note that the quantile estimator is only consistent if , this is for quantiles situated maximally up to the border of the sample , using for instance a sequence of the type for some . The extra factor

in (23) compared to the Weissman estimator induces this restriction. The first term in the expansion of in Theorem 2(b) is indeed the asymptotic expansion of as given for instance in Beirlant et al. (2004), section 4.6. If and then the expansion of the Weissman estimator is dominant, while if and the second term in the expansion is to be retained.

From Theorem 2 it follows that it is important to be able to test if for a given case study rough or light truncation holds. Indeed, if rough truncation holds then in extreme quantile estimation from (21) should be used, while under light truncation the estimator from (25), or the classical Weissman estimator (24), or the moment type extreme quantile estimator can be used when extrapolating outside the sample. From Theorem 3(a) the consistency of both tests (27) and (31) follows directly, while the null distributions are conisdered in parts (b) and (c).

Note that the result in Theorem 3(b) needs a stronger condition on for the limit to hold under , meaning that for the test based on the truncation point has to lie higher than in case of in order to keep a given significance level. This yields a theoretical confirmation of the simulation results where the test was found to reject light truncation situations that deviate from the untruncated Pa-type distributions, sooner than the test.

7 Conclusion

We have extended the work on estimating the Pareto index under truncation from Aban et al. (2006) and Nuyts (2010) to extreme quantile estimation, and considered also truncation of regularly varying tails. The main proposals and findings are

•

The new estimator of the Pareto index is effective whether the underlying distribution is truncated or not, thus unifying previous approaches. Although based on a truncated model, the estimator of is competitive even when the underlying distribution is unbounded.

•

Our method leads to new quantile estimators which are especially effective in the case of rough truncation. In case the data come from a light truncated Pa-type distribution, which is the case when the Pa QQ-plot (11) is linear in the right tail, the extreme quantile estimator (21) should not be used for extrapolation far out of range of the available observations as discussed in Remark 2.

•

A new TPa QQ-plot is constructed that can assist in verifying the validity of the TPa-type model. Moreover a new test is provided for testing light truncation against rough truncation which offers an extra

tool for practitioners.

Acknowledgment The authors thank Mark Meerschaert for helpful discussions and many suggestions that had a significant positive influence on the paper.

References

[1] Aban, I.B. and Meerschaert, M.M., 2004. Generalized least squares estimators for the thickness of heavy tails. Journal of Statistical Planning and Inference119, 341–352.

[2] Aban, I.B., Meerschaert, M.M. and Panorska, A.K., 2006. Parameter Estimation for the Truncated Pareto Distribution, Journal of the American Statistical Association: Theory and Methods101(473), 270–277.

[3]

Beirlant, J., Vynckier, P. and Teugels, J., 1996. Tail index estimation, Pareto quantile plots and regression diagnostics. J. Amer. Statist. Assoc., 91, 1659-1667.

[4]

Beirlant, J., Goegebeur, Y., Teugels, J. and Segers, J., 2004. Statistics of Extremes: Theory and Applications, Wiley, UK.

[5]

Brilhante, M.F., Gomes, M.I. and Dinis Pestana, D., 2013. A simple generalisation of the Hill estimator. Computational Statistics & Data Analysis, 57(1), 518-535.

[6]

Chakrabarty, A. and Samorodnitsky, G., 2012. Understanding heavy tails in a bounded world, or, is a truncated heavy tail heavy or not? Stochastic Models, 28, 109-143.

[7]

Clark, D.R., 2013. A note on the upper-truncated Pareto distribution. In Proc. of the Enterprise Risk Management Symposium, April 22-24, Chicago IL.

[8]

Dekkers, A., Einmahl, J. and de Haan, L., 1989. A moment estimator for the index of an extreme-value distribution. Ann. Statist., 17, 1795-1832.

[9]

de Haan, L. and Ferreira, A., 2006. Extreme Value Theory: an Introduction, Springer Science and Business Media, LLC, New York.

[10]

Hill, B.M., 1975. A simple general approach about the tail of a distribution. Annals of Statistics 3, 1163-1174.

[11]

Gomes, M.I., Figueiredo, F. and Neves, M.M., 2012. Adaptive estimation of heavy right tails: the bootstrap methodology in action. Extremes, 15:4, 463-489.

[12]

Hubert, M., Dierckx, G. and Vanpaemel, D., 2013. Detecting influential data points for the Hill estimator in Pareto-type distributions. Computational and Statistical Data Analysis 65, 13-28.

[13]

Nuyts, J., 2010. Inference about the tail of a distribution: improvement on the Hill estimator. International Journal of Mathematics and Mathematical Sciences, Article ID 924013.

[14]

Reed, W.J. and McKelvey, K.S., 2002. Power-law behaviour and parametric models for the size-distributions of forest fires. Ecological Modelling, 150, 239-254.

[15] Seneta, E., 1976. Regularly Varying Functions. Lecture Notes in Math.

508, Springer-Verlag, Berlin.

[16]

Weissman, I., 1978. Estimation of parameters and large quantiles based on the largest observations. Journal of the American Statistical Association 73, 812-815.

Tail fitting for truncated and non-truncated

Pareto-type distributions Supplementary material: Proofs of the asymptotic results

Beirlant J.a222Corresponding author: Jan Beirlant, KU Leuven, Dept of Mathematics and LStat, Celestijnenlaan 200B, 3001 Heverlee, Belgium; Email: jan.beirlant@wis.kuleuven.be , Fraga Alves, M.I.b, Gomes, M.I.b,

a Department of Mathematics and Leuven Statistics Research Center, KU Leuven

b Department of Statistics and Operations Research, University of Lisbon

Proof of Theorem 1

The mean value theorem implies that where is between and , with .

Then that the limit distribution of is found from the asymptotic distribution of

Hence the asymptotic behaviour of and constitute essential building blocks in the derivation of the asymptotics for . We consider these in the following Propositions.

For this we make use of the result (see de Haan and Ferreira, 2006, 7.2.12) that for some standard Wiener process (with ) we have uniformly over all , as ,

(S1)

Proposition 1.

Let (39) hold and let , , . Then

(a)

if ,

where

(b)

if ,

where the first two terms in this expansion are the limits for of the first two lines in the expansion in case (a).

Proof

Let

and let denote the order statistics from an i.i.d. sample of size from the uniform (0,1) distribution. Then using summation by parts and the fact that ()

Using (S1), can now be approximated as by the integral

Using the mean value theorem on the inner integral between and , followed by an integration by parts, we obtain the approximation

First, let . Then from (15) the approximation (LABEL:midH) of equals

Next, add and subtract from the second and fourth line respectively, and

use the approximations

with and between and , and

Finally, using partial integration we have

from which one obtains the stated result in (a).

Secondly, consider . Then using (16)

the proof follows the lines of proof of the asymptotic normality of the Hill estimator as for instance given in Mason and Turova (1994), except

for the extra term

appearing from the factor in (16). However, using

, one derives that

Condition in Theorem 1(b) entails that the bias term due to the factor in (16) is negligible with respect to the classical bias due to the last factor in (16).

∎

Proposition 2.

Let (39) hold and let , , . Then

(a)

if ,

where

(b)

if ,

where denotes the maximum of a sample of size from the standard exponential distribution.

Proof The proof of (a) follows similar lines as the proof of Proposition 1(a). Concerning part (b) remark that using (16)

The result then follows since , and by using (39).

∎

Proof of Theorem 1 (cont’d).

First we derive the consistency of under the conditions of Theorem 1, so that then .

Aban et al. (2006, see A.4) showed that is a decreasing function in . Moreover

and . Showing that asymptotically under the conditions of the theorem using Propositions 1 and 2 in both cases (a) and (b), we have then that there is a unique solution to the equation . Note with Propositions 1 and 2 that for the true value we have , since and asymptotically are equal, namely to

in case (a), and

in case (b). So the true value asymptotically is a solution from which the consistency follows.

From Propositions 1 and 2, (S4), (S5), and (S3) we find that the stochastic part in the development of is given by

Developing for , respectively , leads to the stated asymptotic variances in cases (a) and (b).

From (S4), (S5), and the asymptotic bias expressions in Propositions 1 and 2 one finds the asymptotic bias expressions of . For instance in case we find that

(S6)

∎

Proof of Theorem 2. First consider the case . Then from (22)

while

with the average of an i.i.d. sample from the standard exponential distribution so that .

Furthermore

Now it follows from Propositions 1(a) and 2(a) that

so that, with

from which (a) follows.

Next, in the case , starting from expression (23) and Proposition 1(b), we obtain

where under the given conditions

since, using Theorem 1(b) and Proposition 2(b), and the fact that asymptotically is standard exponentially distributed,

Furthermore,

Finally since under the given assumptions , , and

we find that

from which the result follows with Theorem 1(b).

∎

Proof of Theorem 3. The first statement in (a) and (b) follow readily from Propositions 1(b) and 2(b).

In order to prove (c) we first derive the asymptotic distribution of .

Note that

with

In Theorem A.1 in Beirlant et al. (2009) [1] it is stated that converges weakly in the space with and

the Banach space of continuous functions equipped with the topolgy of uniform convergence. The limit process is a Gaussian process with

From we have for that as , and thus by the continuous mapping theorem

converges weakly to .

From this it then follows that

Then also

from which the result (c) follows.

To prove the second statement in (a), we obtain from (15) that

Setting () we have that are distributed as the order statistics of a uniform () sample of size . Moreover for we have

. Following Proposition 1(a) it then follows that

Since

and

the result follows.

References

[S1]

Beirlant, J., Joossens, E., Segers, J., 2009. Second-order refined peaks-over-threshold modelling for heavy-tailed distribution.

Journal of Statistical Planning and Inference 139, 2800-2815.

[S2]

Mason, D.M., Turova, T.S., 1994. Weak convergence of the Hill estimator process. In: Extreme Value Theory and Applications: Proceedings of the Conference on Extreme Value Theory and Applications, Gaithersburg, 1993, Vol. 1. J. Galambos, J. Lechner and E. Simiu, eds. Kluwer, Dordrecht.