The Root solution to the multi–marginal embedding problem: an optimal stopping and time–reversal approach††thanks: We are grateful to many who have commented on this research project. In particular, we thank the participants of the BIRS Workshop Mathematical Finance: Arbitrage and Portfolio Optimization in May 2014 and HIM Workshop Optimal Transport and Stochastics in March 2015 for their helpful comments and remarks.

Abstract

We provide a complete characterisation of the Root solution to the Skorokhod embedding problem (SEP) by means of an optimal stopping formulation. Our methods are purely probabilistic and the analysis relies on a tailored time-reversal argument. This approach allows us to address the long-standing question of a multiple marginals extension of the Root solution of the SEP. Our main result establishes a complete solution to the –marginal SEP using first hitting times of barrier sets by the time-space process. The barriers are characterised by means of a recursive sequence of optimal stopping problems. Moreover, we prove that our solution enjoys a global optimality property extending the one-marginal Root case. Our results hold for general, one-dimensional, martingale diffusions.

1 Introduction

The Skorokhod embedding problem (SEP) for Brownian motion consists of specifying a stopping time such that is distributed according to a given probability measure on . It has been an active field of study in probability since the original paper by Skorokhod, (1965), see Obłój, (2004) for an account. One of the most natural ideas for a solution is to consider as the first hitting time of some shape in time–space. This was carried out in an elegant paper of Root, (1969). Root showed that for any centred and square integrable distribution there exists a barrier , i.e. a subset of such that implies for all , for which , . The barrier is (essentially) unique, as argued by Loynes, (1970).

Root’s solution enjoys a fundamental optimality property, established by Rost, (1976), that it minimises the variance of the stopping time among all solutions to the SEP. More generally, for any convex function and any stopping time with . This led to a recent revival of interest in this construction in the mathematical finance literature, where optimal solutions to SEP are linked to robust pricing and hedging of derivatives, see Hobson, (1998, 2011). More precisely, optimality of the Root solution translates into lower bounds on prices of options written on the realised volatility.

In recent work Cox and Wang, 2013b show that the barrier may be written as the unique solution to a Free Boundary Problem (FBP) or, more generally, to a Variational Inequality (VI). This yields directly its representation by means of an optimal stopping problem. This observation was the starting point for our study here. Subsequently, Gassiat et al., (2014) used analytic methods based on the theory of viscosity solutions to extend Root’s existence result to the case of general, integrable starting and target measures satisfying the convex ordering condition. Using methods from optimal transport, Beiglböck et al., (2016) have also recently proved the existence and optimality of Root solutions for one-dimensional Feller processes and, under suitable assumptions on the target measure, for Brownian motion in higher dimensions.

The first contribution of our paper is to show that one can obtain the barrier directly from the optimal stopping formulation, and to prove the embedding property using purely probabilistic methods. This also allows us to determine a number of interesting properties of by means of a time-reversal technique. Our results will hold for a general one-dimensional diffusion.

Beyond the conceptual interest in deriving the Root solution from the optimal stopping formulation, the new perspective enables us to address the long–standing question of extending the Root solution of the Skorokhod embedding problem to the multiple-marginals case, i.e. given a non-decreasing (in convex order) family of probability measures on with finite first moment, and a diffusion started from the measure , find stopping times such that , and is uniformly integrable. Our second contribution, and the main result of the paper, provides a complete characterisation of such a solution to the SEP which extends the Root solution in the sense that it enjoys the following two properties:

-

•

first, the stopping times are defined as hitting times of a sequence of barriers, which are completely characterized by means of a recursive sequence of optimal stopping problems;

-

•

second, similar to the one-marginal case, we prove that our solution of the multiple marginal SEP minimizes the expectation of any non-decreasing convex function of among all families of stopping times , such that .

It is well known that solutions to the multiple marginal SEP exist if and only if the measures are in convex order, however finding optimal solutions to the multiple marginal SEP is more difficult. While many classical constructions of solutions to embedding problems can, in special cases, be ordered (see Madan and Yor, (2002)), in general the ordering condition is not satisfied except under strong conditions on the measures. The first paper to produce optimal solutions to the multiple marginal SEP was Brown et al., (2001), who extended the single marginal construction of Azéma and Yor, (1979) to the case where one intermediate marginal is specified. More recently, Obłój and Spoida, (2016) and Henry-Labordère et al., (2016) extended these results to give an optimal construction for an arbitrary sequence of marginals satisfying a mild technical condition.

There are also a number of papers which make explicit connections between optimal stopping problems and solutions to the SEP, including Peskir, (1999), Obłój, (2007) and Cox et al., (2008). In these papers, the key observation is that the optimal solution to the SEP can be closely connected to a particular optimal stopping problem; in all these papers, the same stopping time gives rise to both the optimal solution to the SEP, and the optimal solution to a related optimal stopping problem. In this paper, we will see that the key connection is not that the same stopping time solves both the SEP and a related optimal stopping problem, but rather that there is a time-reversed optimal stopping problem which has the same stopping region as the SEP, and moreover, the value function of the optimal stopping problem has a natural interpretation in the SEP. The first paper we are aware of to exploit this connection is McConnell, (1991), who works in the setting of the solution of Rost, (1971) and Chacon, (1985) to the SEP (see also Cox and Wang, 2013a ; Gassiat et al., (2014)), and uses analytic methods to show that Rost’s solution to the SEP has a corresponding optimal stopping interpretation. More recently111Indeed, we were made aware of this paper only in the final stages of completing this work. De Angelis, (2015) has provided a probabilistic approach to understanding McConnell’s connection, using a careful analysis of the differentiability of the value function to deduce the embedding properties of the SEP; both the papers of McConnell and De Angelis also require some regularity assumptions on the underlying measures in order to establish their results. In contrast, we consider the Root solution to the SEP. As noted above, a purely analytic connection between Root’s solutions to the SEP and a related (time-reversed) optimal stopping problem was observed in Cox and Wang, 2013b . In this paper, we are not only able to establish the embedding problems based on properties of the related optimal stopping problem, but we are also able to use our methods to prove new results (in this case, the extension to multiple marginal solutions, and characterisation of the corresponding stopping regions), without requiring any assumptions on the measures which we embed (beyond the usual convex ordering condition).

The paper is organized as follows. Section 2 formulates the multiple marginals Skorokhod embedding problem, reviews the Root solution together with the corresponding variational formulation, and states our optimal stopping characterization of the Root barrier. In Section 3, we report the main characterisation of the multiple marginal solution of the SEP, and we derive the corresponding optimality property. The rest of the paper is devoted to the proof of the main results. In Section 4, we introduce some important definitions relating to potentials, state the main technical results, and use these to prove our main result regarding the embedding properties. The connection with optimal stopping is examined in Section 5. Given this preparation, we report the proof of the main result in Section 6 in the case of locally finitely supported measures. This is obtained by means of a time reversal argument. Finally, we complete the proof in the case of general measures in Section 7 by a delicate limiting procedure.

Notation and Standing Assumptions: In the following, we consider a regular, time-homogenous, martingale diffusion taking values on an interval , defined on a filtered probability space satisfying the usual hypotheses. For , we write for expectations under the measure for which the diffusion departs from at time . We also write . We use both and to denote the diffusion process. While and denote the same object, the double notation allows us to distinguish between two interpretations: with a fixed reference time-space domain , we think of as starting in and running forward in time and of as starting in and running backwards in time. For a distribution on , we interpret .

We suppose that the diffusion coefficient is , so , where is locally Lipschitz, , for some constant , and strictly positive on , where we write , and without loss of generality, assume that ; in addition, we use for the closure of , and for the boundary, so . We assume that the corresponding endpoints are either absorbing (in which case they are in ), or inaccessible (in which case, if for example is inaccessible and finite, then ). The measures we wish to embed will be assumed to be supported on , and in the case where , it may be possible to embed mass at by taking a stopping time which takes the value . We define . We note also222See the proof of Lemma 5.1 below for a suitable argument. that as a consequence of the assumption on , we have , and we further write for suitable measures .

We will also frequently want to restart the space-time process, given some stopped distribution in both time and space, and we will write for a general probability measure on , with typically for some stopping time . With this notation, we have, and we denote the random starting point, which then has law . Since may put mass on , we interpret the process started at such a point as the constant process. For each of these processes, denotes the (semimartingale) local time at corresponding to the process , with the convention that for . In addition, given a barrier , we define the corresponding hitting time of by under by:

Similarly, given a stopping time we write

Finally, we observe that, as a consequence of the (local) Lipschitz property of , we know there exists a continuous transition density, , so that

whenever is supported in (see e.g. (Rogers and Williams,, 2000, Theorem V.50.11)). We observe that we then have the following useful identities for the local time (see e.g. (Karatzas and Shreve,, 1991, Theorem 3.7.1)):

and

| (1.1) |

2 The Root solution of the Skorokhod embedding problem

2.1 Definitions

Throughout this paper, we consider a sequence of centred probability measures on :

| and | (2.1) |

We similarly denote for all . We say that is in convex order, and we denote , if

| for all convex functions | (2.2) |

The lower and the upper bounds of the support of relative to are denoted by

| and | (2.3) |

We exclude the case where as a trivial special case, and so we always have for all , as a consequence of the convex ordering. The potential of a probability measure is defined by

| (2.4) |

see Chacon, (1977). For centred measures in convex order, we have

| and | (2.5) |

Recall that is a martingale diffusion. A stopping time (which may take the value with positive probability) is said to be uniformly integrable (UI) if the process is uniformly integrable under . We denote by the collection of all UI stopping times.

The classical Skorokhod embedding problem with starting measure and target measure is:

| (2.6) |

We consider the problem with multiple marginals:

| (2.7) |

In this paper, our interest is in a generalisation of the Root, (1969) solution of the Skorokhod embedding problem so that each stopping time is the first hitting time, after , by of some subset in . Further, and crucially, we require that is a barrier in the following sense:

Definition 2.1.

A set is called a barrier if

is closed;

if then for all ;

if is finite, .

Given a barrier , for , we define the corresponding barrier function:

| (2.8) |

Since is closed it follows, as observed by Root, (1969) and Loynes, (1970), that is lower semi–continuous on . Also, from the second property, we see that a barrier is the epigraph of the corresponding barrier function in the -plane:

Definition 2.2.

(i) We say that a barrier is regular if is an open interval containing zero.

(ii) For a probability measure on , we say that a barrier is -regular if

| for all |

i.e. the barrier cannot be enlarged without altering the stopping distribution of the space-time diffusion started with law and run to the hitting of .

Observe that a regular barrier is a -regular barrier. We have the following characterisation:

Remark 2.3.

A barrier is -regular if and only if for all .

Lemma 2.4.

Let be a probability measure on and a barrier such that . Then or -a.s. Further, if is not -regular then there exists a -regular barrier such that -a.s.

Proof.

For some , we have and . If then and and it is clear that -a.s. Otherwise . If is not -regular then by definition the set of all barriers for which -a.s. is not a singleton. Then for any two such barriers their union is also such a barrier, as shown by Loynes, (1970). It follows that there exists a minimal such barrier with respect to the inclusion which then necessarily has to be -regular. ∎

It follows that, without loss of generality, we may restrict our attention to -regular barriers. Henceforth, whenever a barrier is given it is assumed that it is a -regular barrier, where the measure will be clear from the context.

2.2 Root’s solution and its PDE characterisation

The main result of Root, (1969) is the following.

Theorem 2.5 (Root, (1969)).

Let , , and be a centred probability measure on with a finite second moment. Then there exists a barrier such that is a solution of SEP.

The first significant generalisation of this result is due to Rost, (1976) who showed that the result generalised to transient Markov processes under certain conditions. The condition that the probability measure has finite second moment has only very recently been further relaxed to the more natural condition that the measure has a finite first moment. This was first achieved by Gassiat et al., (2014), who have extended Root’s result to the case of one-dimensional (time-inhomogeneous) diffusions using PDE methods. The result was also obtained by Beiglböck et al., (2016) using methods from Optimal Transport theory.

Remark 2.6.

We next recall the recent work of Cox and Wang, 2013b and Gassiat et al., (2014). For a function , we denote by the derivative, the first and second spacial derivatives, i.e. with respect to the -variable, and we introduce the (heat) second order operator

| (2.9) |

Consider the variational inequality or obstacle problem:

| and | (2.10) |

Then, based on the existence result of Root, (1969), Cox and Wang, 2013b proved the following result.

Theorem 2.7 (Theorem 4.2, Cox and Wang, 2013b ; Theorem 2, Gassiat et al., (2014)).

Let be centred probability measures on in convex order. Then, there is a unique solution of (2.10) which extends continuously to , and the Root solution of the SEP is induced by the regular barrier

Moreover, we have the representation for all .

In Cox and Wang, 2013b , the solution to the variational inequality was determined as a solution in an appropriate Sobolev space, while Gassiat et al., (2014) show that the solution can be understood in the viscosity sense.

2.3 Optimal stopping characterisation

The objective of this paper is to provide a probabilistic version of the last result, and its generalisation to the multiple marginal problem. Our starting point is the classical probabilistic representation of the solution to (2.10) as an optimal stopping problem. Define now

| with | (2.11) |

where is the collection of all –stopping times . Then, using classical results, see e.g. Bensoussan and Lions, (1982), when properly understood, in (2.11) is a solution to (2.10). Uniqueness, in an appropriate sense, of solutions to (2.10), then allows to deduce that the characterisation of the Root barrier given in Theorem 2.7 corresponds to the stopping region of the optimal stopping problem (2.11)

| (2.12) |

The probabilistic approach we develop in this paper provides a self-contained construction of the Root solution, and does not rely on the existence result of Root, (1969) or PDE results. Indeed, these follow from the following direct characterisation which is a special case of Theorem 3.1 below.

3 Multiple Marginal Root Solution of the SEP: main results

3.1 Iterated optimal stopping and multiple marginal barriers

In order to extend the Root solution to the multiple marginals SEP, we now introduce the following natural generalisation of the previous optimal stopping problem. Denote

| and |

The main ingredient for our construction is the following iterated sequence of optimal stopping problems:

| where | (3.1) |

The stopping regions corresponding to the above sequence of optimal stopping problems are given by:

| with | (3.2) |

and the optimal stopping time which solves (3.1) is the first entry to by the time space process starting in and running backwards in time: .

Our main result shows that the same barriers used to stop the process running forward in time:

| (3.3) |

give the multiple marginals Root solution of SEP. It is important to note that the barriers in (3.2) are not necessarily nested – both and may contain points which are not in the other barrier.

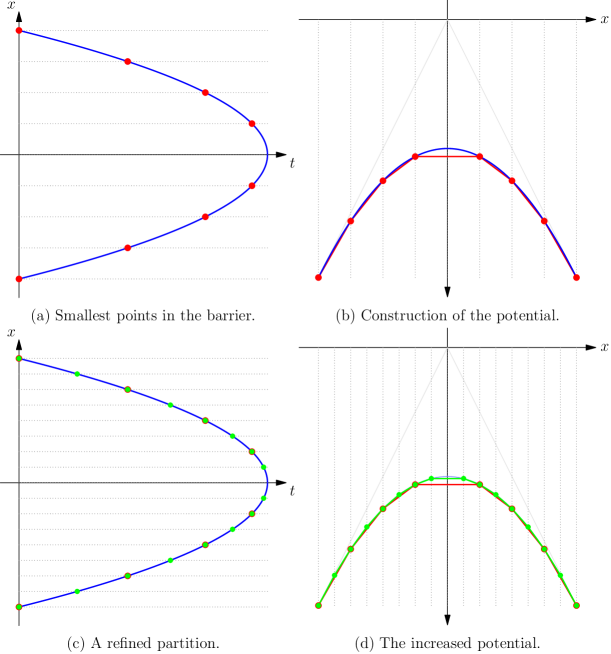

An example of a possible sequence of stopping times is depicted in Figure 1. Since the barriers are not necessarily nested, in general will not be equal to the first entry time to the barrier, only the first entry time after . It may also be the case that . Both cases are shown in Figure 1.

Finally, it will be useful to introduce the (time-space) measures on defined for all Borel subsets of by:

We are now ready to state our main result, which includes Theorem 2.8 as a special case.

Theorem 3.1.

Let be a vector of centred probability measures on in convex order. Then is a -regular barrier for all , and solves SEP. Moreover, we have

| for all | (3.4) |

Our proof will proceed by induction. Its main ingredients will be summarised in Section 4.

3.2 Optimality

In this section, we show optimality of the constructed -fold Root solution of the multiple marginal Skorokhod embedding problem. We recall the main ingredients of our embedding defined in (3.1)–(3.3). We also denote . Define the set of all solutions to SEP in (2.7):

For a given function we consider the optimal -fold embedding problem:

| (3.5) |

Theorem 3.2.

The above remains true for any stopping times which embed since if is not uniformly integrable then it is not minimal, see (Obłój,, 2004, Section 8), and we can find smaller stopping times for which the above bound is already satisfied.

Similar to many proofs of optimality of particular solutions to SEP, see e.g. Hobson, (1998); Cox et al., (2008); Henry-Labordère et al., (2016), at the heart of our argument lies identification of a suitable pathwise inequality. Interpreting (3.5) as an iterated Martingale Optimal Transport problem, the pathwise inequality amounts to an explicit identification of the dual optimiser in the natural Kantorovich-type duality. Our inequality is inspired by the one developed by Cox and Wang, 2013b .

For all and , we introduce the functions

Our main result below involves the following functions:

| (3.6) |

Lemma 3.3.

Let be a non-negative non-decreasing function. Then for all , with , we have:

| (3.7) |

and equality holds if for .

The proof of the above inequality is entirely elementary, even if not immediate, and is reported in Appendix A. The optimality in Theorem 3.2 then essentially follows by evaluating the above on stopped paths and taking expectations. Technicalities in the proof are mainly related to checking suitable integrability of various terms and the proof is also reported in Appendix A.

Finally, we note that the above pathwise inequality could be evaluated on paths of arbitrary martingale and, after taking expectations, would lead to a martingale inequality. The inequality would be sharp in the sense that we have equality for stopped at in (3.3). This method of arriving at martingale inequalities is linked to the so-called Burkholder method, see e.g. Burkholder, (1991), and has been recently exploited in number of works, see e.g. Acciaio et al., (2013); Beiglböck and Nutz, (2014); Obłój et al., (2015).

4 The inductive step

In this section we outline the main ideas behind the proof of Theorem 3.1. The proof proceeds by induction. At the end of each step in the induction, we will determine a stopping time , and the time-space distribution , which corresponds to the distribution of the stopped process under the starting measure . This measure will be the key part of the subsequent definitions. Given this stopping time, and a new law , we proceed to determine a new stopping time , and the corresponding time-space distribution . This stopping time will embed the law . This inductive step is summarised in Theorem 4.1 below.

This stopping time is constructed as the solution of an optimal stopping problem , introduced below, with obstacle function appropriately defined by combining the potential function of the stopped process and the difference of potentials between the starting distribution – the spatial marginal of denoted – and the target distribution . We will also show that the function is equal to the potential function , allowing us to iterate the procedure.

We now introduce the precise definitions. The measure will be a fixed integrable measure throughout, and so we will typically not emphasise the dependence of many terms on this measure.

Let be the time-space distribution of for some UI stopping time . The stopped potential is defined as the potential of :

| (4.1) |

Motivated by the iterative optimal stopping problems (3.1), we also introduce, for any probability measure on , the difference of potentials

| where |

and is equivalent to . Moreover, since is UI, we have

| (4.2) |

The optimal stopping problem which will serve for our induction argument is:

| (4.3) |

We also introduce the corresponding stopping region

| (4.4) |

and we set

| (4.5) |

Theorem 4.1.

Let with corresponding time-space distribution , and an integrable measure such that . Then is a UI stopping time embedding and . Moreover, is a -regular barrier.

Proof of Theorem 3.1.

Consider the first marginal. Let so that , , and let . Then and in (4.3)–(4.4) are equal to, respectively, in (3.1)-(3.2). It follows from Theorem 4.1 that the stopping time induced by is a UI stopping time solving SEP and , as required. We next iterate the arguments. Given the UI stopping time from the step with its space-time measure we know that so that, with , we have and . Applying Theorem 4.1 we get that embeds , is UI and as required. The proof finishes after iterations. ∎

The rest of this paper is dedicated to the proof of Theorem 4.1. The following result isolates the main steps needed for this.

Lemma 4.2.

Let with corresponding time-space distribution , and . Assume further that , pointwise as , and . Then, is a UI stopping time embedding .

Proof.

From the assumptions and the definition of we obtain

where the inequality follows from Fatou’s Lemma. This in particular implies that is an integrable probability measure on , for all , and as , where . Since also as , we deduce from the above inequality that , and therefore as . Then for , it follows from the dominated convergence theorem that

In particular, for some , for all , and by the above, sending , we see that . We conclude that , i.e. , which is the required embedding property. Moreover, it follows from the Tanaka formula together with the monotone convergence theorem that

The uniform integrability of the stopping time now follows from (Elworthy et al.,, 1999, Corollary 3.4). ∎

The pointwise convergence of towards , as will be stated in Lemma 5.5 (iii), while the equality is more involved and will be shown through a series of results, see Lemma 7.3.

Remark 4.3.

We have if and only if , for all . Indeed, by the Tanaka formula,

Recalling that, under , , and (under ), . Recall that, under , the local time is set to for , by convention. Then from the strong Markov property, we have , and therefore:

| (4.6) |

justifying the claimed equivalence.

Remark 4.4.

Observe that the regularity of the barrier can now be seen as an easy consequence of Lemma 4.2. Suppose (in the setting of Theorem 4.1), we have and pointwise as . From (4.6), (4.2) and applying monotone convergence to as , we deduce that

Now suppose that . Then , by (4.6). In view of Remark 2.3, this shows that is regular.

5 Stopped potential and the optimal stopping problem

5.1 Properties of the stopped potential function

The following lemma provides some direct properties of the stopped potential. Recall the definition .

Lemma 5.1.

Let with corresponding time-space distribution . Then, is concave and -Lipschitz-continuous in , and non-increasing, and is (uniformly in ) -Hölder continuous on for all . In addition

and the following identity holds in the distribution sense:

by which we mean that, for any stopping time , we have

| (5.1) | ||||

where is the space-time density of the process (started at and running backwards in time) up to the stopping time .

Proof.

The definition of in (4.1) immediately shows that is concave, Lipschitz in , and non-increasing in . As in Remark 4.3 above, using Tanaka’s formula and the strong Markov property we obtain

| (5.2) |

We now consider continuity properties of . First observe that, by the martingale property of , we have

Using the fact that and the martingale property of , we deduce

where the first inequality follows via localisation and limiting argument using Fatou’s lemma and monotone convergence. It now follows by Grönwall’s lemma that

from which we deduce that

| (5.3) |

Writing for , we see that

and we deduce that is -Hölder continuous on . Equation (5.3) also provides the inequality

It remains to compute . First, since is non-increasing in and concave in , the partial derivatives and are well-defined as distributions on , so makes sense in terms of measures.

We first consider the case where is suitably differentiable (say smooth). Note that by a monotone convergence argument, we can restrict to the case where remains in a compact subinterval of up to , and hence is bounded. Let be the transition density for the diffusion and recall that . It follows that for an arbitrary starting measure , we have , and we directly compute (using Kolmogorov’s Forward Equation, which holds due to the smoothness assumption on ) that

Suppose in addition that has a smooth density with respect to Lebesgue measure (which we also denote by ). We then compute from (5.2) and the equation above that

Applying Itô’s lemma, we see that

| (5.4) | ||||

We now argue that our results hold for an arbitrary, locally Lipschitz function . Keeping fixed as above, with a smooth density, let be a sequence of Lipschitz functions obtained from by mollification. Note that since we are on a compact interval, and hence are all bounded and from the mollification, we may assume that there exists such that are all -Lipschitz; moreover is bounded on the corresponding compact time-space set.

Write for the solution to the SDE , and note in particular, by standard results for SDEs (e.g. (Protter,, 2005, Theorem V.4.15)) that almost surely (possibly after restricting to a subsequence), and in as . Hence, by bounded convergence, we get convergence of the corresponding expectations on the right-hand side of (5.4), as . In addition, writing for the functions corresponding to the diffusions , we see from the first half of the proof that the functions are 1-Lipschitz in , and uniformly Hölder continuous in , for some common Hölder coefficient. It follows from the Arzelà-Ascoli theorem that converge uniformly (possibly down a subsequence) to . We deduce that (5.1) holds for general and smooth .

Finally, approximating the measure by smooth measures through a mollification argument, and observing that the local times for the diffusion are jointly continuous in and (by (1.1) and the discussion preceeding this equation) we conclude that we can pass to the limit on the right-hand side of (5.2), and hence on the left-hand side of (5.1). On the other hand, when is continuous, we can also pass to the limit on the right-hand side of (5.1). Moreover we can approximate by a sequence of stopping times such that has a continuous density, and this gives us the required result after a monotone convergence argument. ∎

For the next statement, we introduce the processes

| (5.5) |

where is defined through as in (4.2), i.e. .

Lemma 5.2.

Let with corresponding time-space distribution . Then the processes and are -supermartingales for all , and .

Proof.

In this proof we will want to take expectations with respect to both the and processes at the same time; we will assume that these are defined on a product space, where the processes are independent. Then we will denote expectation with respect to the process alone by , etc, and the filtrations generated by the respective processes by and .

We first prove the supermartingale property for the process . The case is an immediate consequence of the Jensen inequality. Next, fix , and recall that for . Then we need to show, for ,

Using Hunt’s switching identity we have

Using the Strong Markov property, and to denote independent copies of etc., we deduce

where, in the final line, we used Jensen’s inequality and the fact that .

Now suppose , and consider for . A similar calculation to that above shows that for ,

where . Note that for any , the process is a supermartingale for . It follows that, since ,

∎

5.2 The optimal stopping problem

In this section we derive some useful properties of the function . We first state some standard facts from the theory of optimal stopping. Introduce

| for all | (5.6) |

Proposition 5.3.

Let with corresponding time-space distribution , and . Then, for all , is an optimal stopping rule for the problem in (4.3):

| (5.7) |

and the process is a -martingale for and a -supermartingale for .

Proof.

Recall that under the diffusion , departs from at time , and when , we write . Then we have for :

| (5.8) |

Notice that is a classical optimal stopping problem with maturity , and obstacle , , satisfying the condition of upper semicontinuity under expectation, i.e. for any monotone sequence of stopping times converging to . Under this condition, it is proved in El Karoui, (1981) that the standard theory of optimal stopping holds true. In particular, the process satisfies the announced martingale and supermartingale properties, and an optimal stopping time for the problem is

which is exactly . ∎

Remark 5.4.

Note that, taking in (4.3), . Suppose then, from (5.7), for all . We now consider the cases where , , and a finite interval separately.

In the case where , we have as , for any . As for all as , it is impossible that for all and all . So there always exists with and hence .

Similarly consider the case where . From the properties of the diffusion, we know that almost surely as . Moreover, since and , for some , we must have as for . Since is centred, as , and hence we cannot have for all and all . Hence there always exists with and hence .

Finally consider the case where . Hence , and a similar argument to above gives as , for . This limit corresponds to , where is the centred measure supported on , and it is easy to check that this potential is strictly smaller than the potential of any other centred measure supported on , and so for any other measure, there always exists with and hence . The case of the measure is trivial, and we exclude this from subsequent arguments.

Lemma 5.5.

Let with corresponding time-space distribution , and . Then:

-

(i)

the function is -Lipschitz-continuous in , non-increasing and is -Hölder-continuous in , and there is a constant which is independent of such that ;

-

(ii)

is non-increasing in ; in particular, is non-increasing in and concave in ;

-

(iii)

, , and pointwise as .

Proof.

(i) The -Lipschitz-continuity of in follows directly from the Lipschitz continuity of and in . Then, the Hölder continuity in follows by standard arguments using the dynamic programming principle (for example, as a simple modification of the proof of Proposition 2.7 in Touzi, (2012)).

(ii) Let , fix , and let be such that

Recall from Lemma 5.2 the supermartingale properties of the process introduced in (5.5). Then

In addition, since , we have:

Putting these together, we conclude that

By the arbitrariness of , this shows is non-increasing in , and implies that inherits from the non-increase in . By the supermartingale property of the process in Proposition 5.3, this in turns implies that is concave in .

(iii) By definition, . Since , we have . On the other hand, since , we have by the supermartingale property of established in the previous Lemma 5.2.

In the rest of this proof, we show that as for all . We consider three cases:

- Suppose for some . Then, for any , and which converges to , as .

- Suppose that for some sequence with . Then it follows from the previous case that , and therefore by the Lipschitz-continuity of .

- Otherwise, suppose that does not intersect for some . Let over all such that does not intersect . By Remark 5.4, we may assume is not empty and hence . In the subsequent argument, we assume that is finite, the case where is finite follows by the same line of argument. The optimal stopping time in (5.6) satisfies and , -almost surely. If both and are finite, we use the inequality , together with Fatou’s Lemma, Lemmas 5.1 and 5.2, and bounded convergence, to see that

| (5.9) | ||||

Hence , and is linear on .

For the general case where may be infinite, a more careful argument is needed. Since as , it follows that . Fix and choose sufficiently large that . Let and note that as . Then by the martingale property of on , and the fact that , we have

where we wrote . Taking limits as , and using Fatou as above, it follows from the definition of that:

| (5.10) |

Taking and using concavity of we get that , and is linear on . Letting we conclude that is linear on . ∎

5.3 Existence and basic properties of the barrier

We denote the barrier function corresponding to the regular barrier defined in (4.4) with . It will be used on many occasions in our proofs. Recall from (2.3) the definition of the support of a measure in terms of the measure . In what follows, we write for the bounds of the support of in terms of the measure .

Corollary 5.6.

Let with corresponding time-space distribution , and . Then, the set is a (closed) barrier, and moreover

-

(i)

;

-

(ii)

if and only if and on ;

-

(iii)

if and only if .

Proof.

For , we have and it is then immediate from (iii) and (ii) of Lemma 5.5 that and so , for all . By the continuity of and , established in Lemmas 5.1 and 5.5, we conclude that is a closed barrier.

(i) For , we have and hence . It follows from Lemma 5.5 (iii) that and hence for all so that .

(ii) In the proof of Lemma 5.5 (iii), it was shown that the condition implies that is linear on , i.e. , see (5.10). Moreover, the last argument in (i) above also implies that for all whenever . This provides the implication .

Suppose now that and on . For fixed , we have:

Here we have used the strict inequality for all to get the second line. To get the final line, we use Lemma 5.2 to deduce that , and hence that is a submartingale up to , given that is linear on .

This shows that , and hence , for all , and .

(iii) If then for all ,

by (iii) of Lemma 5.5, and so for

all . Recalling that , we conclude that only if .

∎

Remark 5.7 (On having rays for arbitrary large ).

We can now deduce from the proof of the convergence , as in Lemma 5.5 (iii), that for any there exist such that and . In the proof, we show that for any point such that either there exists points such that or there exists an less than such that for any large enough is linear on . Letting , and using the fact that , we conclude that for all . Then implies . In particular, , and by Corollary 5.6 we contradict the initial assumption that is not in the barrier.

Remark 5.8 (On the structure of the stopping region).

Let be integrable measures in convex order. It follows from Corollary 5.6 that the barrier can be divided into at most countably many (possibly infinite) non-overlapping open intervals such that , for , on which for all and .

Observing that in both the embedding, and the optimal stopping perspectives, the process started from never exits each interval , it is sufficient to consider each interval separately, noting that in such a case, for all , and all . In the subsequent argument, we will assume that we are on a single such interval , which may then be finite, semi-infinite, or equal to . In addition, if the measures are in convex order, then their restrictions to each are also in convex order.

Remark 5.9 (On for atomic measures).

Let be integrable measures in convex order. Bearing in mind Remark 5.8, we suppose that is a probability measure on such that for some integer , and some ordered scalars , we have and for all . From the representation of the optimal stopping time , see Proposition 5.3 above, and the form of the set implied by Corollary 5.6, it follows that

| (5.11) |

where is the set of stopping times such that and a.s.

6 Locally finitely supported measures

A probability measure is said to be locally finitely supported if its support intersects any compact subset of at a finite number of points. The measure is finitely supported if its support intersects at a finite number of points. Throughout, will be fixed, so we will typically only refer to (locally) finitely supported measures. Observe that an integrable, centred measure can only be finitely supported if and are both finite — indeed, in this case a locally finitely supported measure is finitely supported if and only if and are both finite.

6.1 Preparation

We start with two preliminary results which play crucial roles in the next section where we establish the main result for finitely supported measures. The first result is the key behind the time-reversal methodology which underpins the main results, see Section 3.1. Here, we give a natural proof in the case where is a Brownian motion, when the proof has a simple intuition333Given its importance, we have discussed this result with many colleagues. Our first proof used an explicit formula for the density in , see Proposition 2.8.10 p.98 in Karatzas and Shreve, (1991). The current proof uses a clever coupling trick devised by Tigran Atoyan.. In Appendix B we give a PDE proof which works in the more general diffusion setting.

To understand the importance of the result, it is helpful to think of the local time of and of on the two sides of the announced equality. This result is then used to obtain the key equality in a “box” setting where the barrier is locally composed of two rays. The case of finitely supported measures is then obtained with an inductive argument in Section 6.2.

Lemma 6.1.

Let be the local time of a Brownian motion . For any and we have

Proof.

Without loss of generality we suppose and introduce two additional points and so that with . Note that by translation invariance and symmetry of Brownian motion we have

Using this in the desired equality, and subtracting , we see that it suffices to show that

Finally, by shift invariance, we may suppose without loss of generality that . Consider three independent Brownian motions starting from and denote the hitting times for . Further, let . Define two new processes

| (6.1) |

and observe these are standard Brownian motions. This construction is depicted in Figure 2. We denote the local time of at level .

Recall that and consider . For this quantity to be non-zero the following have to happen prior to : first has to hit without reaching , then it has to come back to and continue to without ever reaching . This happens at time and from then onwards the local time is counted before time and we see that it simply corresponds to . With a similar reasoning for , we see that our construction gives us the desired coupling:

and taking expectations gives the required result. ∎

We now prove an important consequence of the above result, which will form the basis of an induction argument.

Lemma 6.2.

Let with corresponding time-space distribution , and . Let and be such that , , and on . Then on .

Proof.

In view of Remark 4.3, and the continuity of , it is sufficient to show that

| (6.2) |

We fix . Since , , we have the decomposition

| (6.3) | |||||

where we introduced the measure , and used the fact that, conditional on starting in , the stopping times and are equal (and starting on , we never hit before ). Observe that for , we have

| (6.4) | |||||

since by the assumptions on . Moreover, since is a UI embedding of , it follows from the Tanaka formula that for , we have

where the last equality follows from the assumption that on together with Remark 4.3. Since , this provides by substituting in (6.4) that for :

Plugging this expression in (6.3), we get

The required result now follows from the following claims involving :

| (6.5) | |||||

| (6.6) | |||||

| (6.7) |

which we now prove.

(i) To prove (6.5), we use Itô’s formula (possibly after mollification) to get

Using Lemma 5.1 and writing , this provides:

(ii) We next prove (6.6). Since is concave by Lemma 5.1, it follows from the Itô-Tanaka formula that:

where the last equality follows from Lemma 6.1 together with a coordinate shift.

(iii) Finally we turn to (6.7). Recall that on . Then, since on , we have:

We next use the fact that does not intersect to compute for that

by application of the Itô-Tanaka formula, due to the concavity of the function , as established in Lemma 5.5. We finally conclude from Lemma 6.1/B.1 that

∎

6.2 The case of finitely supported measures

We now start the proof of Theorem 4.1 for a (relatively) finitely supported probability measure . Recall from Lemma 4.2 and Lemma 5.5 (iii) that we need to prove that . When there is no risk of confusion we write for . In the sequel, we will say that is -supported on points if the measure restricted to is a discrete measure, supported on points.

Proposition 6.3.

Let with corresponding time-space distribution , and an –finitely supported measure such that . Then and Theorem 4.1 holds for .

The proof proceeds by induction on the number of points in the support of . The case where is trivial, since it follows immediately from (iii) of Corollary 5.6 that . Hence we suppose that . We start with the case where contains no points, and therefore all mass starting in under will be embedded at the two points .

Lemma 6.4.

Let with corresponding time space distribution , and with . Then holds for all .

Proof.

The proof of Proposition 6.3 will be complete when we establish that the following induction step works.

Lemma 6.5.

Let with time-space distribution . Assume for any which is -supported on points. Then, for any measure which is -supported on points.

Proof.

Let be a centred probability measure -supported on the ordered points , with for all . By Remark 5.9, the set is of the form

| for some |

Let be such that , so that is a horizontal ray in starting farthest away from zero. Define a centred probability measure –supported on by conveniently distributing the mass of at among the closest neighboring points:

1. Let . We first prove that

| (6.8) |

By a direct calculation, we see that for , and is affine and strictly smaller than on . Consider first . Recall (5.7) with the optimal stopping time being the minimum of and the first entry to for the diffusion started in and running backward in time. However since it follows that on . In consequence, we can rewrite (5.11) as

An analogous argument shows for and and for and . By continuity of we also have .

2. We now prove that holds for all .

2.1. From the fact that , for , together with , it follows that . Consequently, for all and all ,

| and |

It follows from the induction hypothesis that holds for all , and for all .

2.2.

It remains to consider and . For , we now know that holds at , and places no points in . Then, it follows from Lemma 6.2 that on . The same argument applies for .

∎

6.3 The case of locally finitely supported measures

In this subsection, we consider the case of measures which are –finitely supported on any compact subset of , but could have an accumulation of atoms at or . We will establish Theorem 4.1 for such by suitably approximating with a sequence of measures with finite support. Recall that , and similarly for . The desired result has already been shown when , see Proposition 6.3, so we consider the case where at least one of these is infinite. For simplicity, we suppose that both are infinite (and hence ), the case where only one is being similar. The approximation is depicted graphically in Figure 3.

For , we observe that we can define a new measure , and constants such that for , , and . In particular, to construct such a measure, we can set for , and extend linearly to the right of , with gradient until the function meets , at the point , from which point on, we take ; a similar construction follows from . The existence of the point follows from the fact that as , which in turn is a consequence of the convex ordering property. This construction guarantees

In particular, is a sequence of atomic measures with finite support. Hence, by Proposition 6.3, Theorem 4.1 holds for these measures. Moreover, we can prove the following:

Lemma 6.6.

Let with corresponding time-space distribution , and a locally finitely supported measure such that . Let be the sequence of measures constructed above. Then the sequence is non-decreasing, and

Proof.

We proceed in two steps:

1. We first show that is non-decreasing and . Recall that for . Then, by definition of the optimal stopping problem, we see that . However, we have for by construction, and so if it is optimal to stop for , it is also optimal to stop for and for . It follows that, for , implies and . The desired monotonicity follows instantly and follows since is closed.

2. It remains to show the reverse inclusion .

First, observe that for the points where or the inclusion

holds. This is an immediate consequence of Corollary 5.6 together with the relation between the measures and .

The rest of the proof is devoted to showing that for a point in the support of with , we have for all . We first carry our preparatory computations which follow two cases. Then we combine the two to give the final result.

2.1. Since Theorem 4.1 holds for , we have

. It then follows from Remark

4.4 that and for our .

Denote . Then, for

sufficiently large , we have for all . Note that .

Letting , we conclude that

This means that, for all with sufficiently small there is a positive probability under that the process reaches before hitting (and hence also ) or exiting . In particular, considering possible paths, we can reverse this: for any such , running backwards, there exists a positive probability that we will reach the support of before hitting or exiting a bounded interval. More specifically, writing , and , for some sufficiently small at least one of the following two cases described below is true. We refer to Figure 4 for a graphical interpretation of the two cases, and a number of the important quantities described below.

-

Case 1

The only points of the support of which can be reached from without exiting are in . Let be a closed and bounded interval such that . Observe that the measures are -finitely supported, and hence for some , and all . Moreover, we may assume that is also sufficiently small that .

For such an , write

and note that .

Our aim is now to use the expression of in Lemma 5.1, to show that is a strict supermartingale on . Recall that and define

and

Recall the family of supermartingales defined in (5.5). We want to show that for some constant which is independent of . Since for all , the event is -measurable. Hence it is sufficient to show that . Using the supermartingale property of , we can further reduce this to showing that

Note that on we have and . We now write for the space-time density of the process killed when it leaves , i.e.

for smooth functions . Then from the form of , we know that is bounded away from zero on , and applying Lemma 5.1 we have

by the assumption on the support of under consideration. By the assumption on , and the fact that is bounded below on , this final term is strictly positive, and independent of , so:

(6.9) for some independent of .

-

Case 2

There exists a bounded rectangle such that , all points of can be reached from via a continuous path which does not enter , and the process spends a strictly positive time in . More specifically, for all sufficiently small , we can choose , such that , , and the set

satisfies . Further, recalling the definitions of and above, we have -a.s.. In a similar manner to above, we now write for the space-time density of the process killed when it leaves , and observe that is bounded away from zero on the set . It follows from Lemmas 5.1 and 5.2 that:

where in the last line we applied Lemma 5.1 and the fact that for

It follows that we can choose independent of such that

which, by an application of Itô’s formula, implies that

(6.10)

Observe finally that, in view of the supermartingale properties of Lemma 5.2, we can combine (6.9) and (6.10) to get:

| (6.11) |

for some independent of , and for any satisfying the

conditions of the lemma.

2.2. We are now ready to exploit the above to establish that for . Take the values of determined above, and consider the

following calculation:

Here we use (6.11) for the first two terms in the second inequality; the third term in the second inequality is at least 0 using the fact that implies that , and . It then follows, since is non-increasing in , that

We now use the fact that independently of , and as to deduce that . In particular, it is not optimal to stop immediately

for the optimal stopping problem at

with , whenever .

∎

Proposition 6.7.

Let with corresponding time-space distribution , and a locally finitely supported measure such that . Then and Theorem 4.1 holds for .

Proof.

It follows from Lemma 6.6 that decreases to , and converges to in probability, and therefore . Finally, if we write , we also have

where we used (4.6) and monotone convergence. It follows from Remark 4.3 that .

Since and , and as , by monotone convergence, we have , and hence by (Elworthy et al.,, 1999, Corollary 3.4), is a UI stopping time. Finally, we deduce that is -regular by observing from (4.4) and taking limits in the equation above that if and only if . From Remark 2.3, it follows that is -regular. ∎

7 The general case

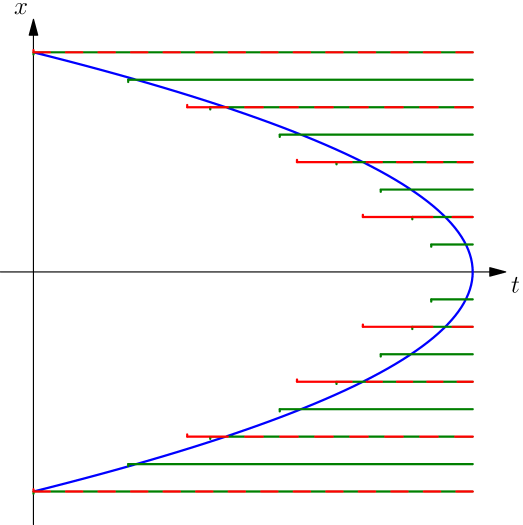

In this section, we complete the proof of Theorem 4.1. We fix with its corresponding time-space distribution , and let be an arbitrary integrable measure such that . We start by approximating with a sequence of locally finitely supported measures. Let

| and | (7.1) |

We set when there are no points of in , see Corollary 5.6 for a characterisation. The existence of a minimizer follows from the lower semicontinuity of the barrier function which, in turn, is implied by the closedness property of the barrier . If there exists more than one minimiser, we choose the smallest: , so that if , then for some . Note that .

We now determine a sequence of approximating measures defined as follows: the measure is defined through its potential function, , and we set to be the smallest concave function such that for all . In particular, we deduce that ; moreover, has the same mean as , and as for each . This approximation is depicted in Figure 5.

Each is locally finitely supported, and so we can apply Proposition 6.7 to each . Write for the corresponding barrier. A typical sequence of barriers are depicted in Figure 6.

Since the potentials of the measures are increasing, we have ; in addition, the function is piecewise linear, and so implies , for some , and . In consequence, for such an we have

| (7.2) |

and it follows from the optimal stopping formulation that — i.e. new spikes may appear, but existing spikes get smaller. Taking a sequence such that for all , for some , we see that increases to a limit. We now establish that this limit is equal to .

Lemma 7.1.

Let

| (7.3) |

Then and for any of the form , for some sequence of indices , .

Proof.

We first show . Let . Then, for all , there is such that , i.e. . However as , and so , proving that . This shows that , and therefore by the closeness of .

We now show the reverse inclusion, . For , and , choose so that . Then there exists such that and for some and by our choice of points . Further, as argued above, so that for all . It follows that .

The above shows , or equivalently . As observed above, for , we have is an increasing sequence in and hence converges to some limit which we denote . By the barrier property of each and the definition of we see that . It follows that and hence all three are equal. ∎

Proposition 7.2.

Consider the approximation sequence above and define . Then:

-

(i)

the process is uniformly integrable under ;

-

(ii)

;

-

(iii)

.

Proof.

(i) By definition and, from Proposition 6.7, the same process stopped at is uniformly integrable, which implies the result.

(ii) Suppose that does not converge a.s. to . Take such that, possibly passing to a subsequence, we have that for some . Then necessarily for large enough. This gives

We take limits on both sides. The left-hand side converges to by continuity of and joint continuity of , see (5.2). For the right-hand side we use -Lipschitz continuity of each and -Hölder continuity in as given in Lemma 5.5. This shows, with , that

for a constant independent of , and hence

which then shows that and hence which gives the desired contradiction.

(iii) Using the above, together with Proposition 6.7 and Remark 4.3, we deduce that

∎

Lemma 7.3.

We have and is a UI stopping time embedding .

Proof.

It suffices to show the first equality as the rest follows from Lemma 5.5 (iii) and Lemma 4.2. Given (iii) of Proposition 7.2 and Remark 4.3, it remains only to show that . We consider the alternative approximating sequence: . Recall from above that if then from which it follows that is an increasing sequence of barriers. Moreover, from the definition of the points , we have , since when we hit , we are guaranteed to hit as soon as we have travelled at least in both directions. However , and therefore:

But also and the result follows. ∎

Appendix A Proofs of the optimality results

We prove here the results announced in Section 3.2. We start with establishing the required pathwise inequality.

Proof of Lemma 3.3.

We proceed in three steps.

1. We first observe that for all , and on . Indeed, notice that , where is the first time we enter , having previously entered the barriers in sequence. Then , -a.s. implying that by the non-decrease of .

2. We next compute that:

| (A.1) |

Then, for , by Step 1. Next, notice that if and only if for all , and that in this case -a.s., implying that . Hence:

| (A.2) |

3. By the previous steps, we have:

where we used (A.1) and . ∎

To be able to take expectations in the pathwise inequality when applied to the stopped diffusion, we need to establish suitable (sub)martingale properties. These are isolated in the following lemma.

Lemma A.1.

Let be bounded non-negative and non-decreasing, and assume

| is a martingale for all | (A.3) |

Then, for all , the process is a -submartingale, and a -martingale on .

Proof.

First, applying the Itô-Tanaka formula to the second term in the definition of , we have

Since , (A.3) shows that differs from a martingale by a bounded random variable and in particular is integrable.

We now proceed in two steps.

1. For , using the above decomposition and (A.3), we have

where . We shall prove in Step 2 below that

| (A.4) | |||||

| (A.5) |

and

| equality holds in (A.4)–(A.5) if | (A.6) |

Then,

with equality if .

2. (i) We first argue, for all , that

| (A.7) |

The martingale property is immediate from the definition of . The submartingale property follows from the following induction. First, the claim is obvious for by the fact that is non-decreasing. Next, suppose that the submartingale property in (A.7) holds for some . Introduce the stopping times , and notice that for . Then, denoting by independent copies of the same objects, and using the induction hypothesis, we see that:

(ii) We now prove (A.4). For , it follows from (A.7) that

(iii) We next prove (A.5). For , using again (A.7), we see that:

(iv) Finally, to prove (A.6), we observe that the equality was lost in (A.4) and (A.5) only because of the inequalities in (A) and (A), which in turn become equalities provided that does not enter for . The condition that ensures this is true. ∎

Proof of Theorem 3.2.

Finally, we complete the proof of the main result in Section 3.2. First, by monotone convergence arguments and since is convex, note that

| (A.10) |

is the same for all so that adding a constant to does not change the problem. We shall normalise by taking and exclude the trivial case . If the quantities in (A.10) are equal to then there is nothing to prove. We thus assume that (A.10) is finite. Note that this might be so even if for each . More generally, thanks to the convex ordering of measures, one can define the integral for a convex and . This is done by considering which are convex, equal to on a compact set and affine on the complement. Further, if with and convex with finite integrals against then the integral is also well defined and finite, see Beiglböck et al., (2016) for details. We shall use this fact below repeatedly together with which follows from (A.10).

Without loss of generality, we may assume that is bounded, the general case follows from a direct monotone convergence argument. Then for all , and in particular, . We define , and observe that is then a non-negative, convex function with so that is a non-negative convex function. We conclude that , . Moreover, we have for all since , as argued above.

The aim is now to take expectations in (3.7) for , where . To do this, we need to check that the expectations under of individual terms on the right-hand side of (3.7) are well defined.

We can rewrite the first two terms on the right-hand side of (3.7) as:

where we used that so that and . The expectation of the first two terms is then equal to

The integrals in the second sum are well defined and finite by the discussion above. As for the first sum, observe that

Using , and integrability properties of we see that the local martingale

is a martingale on . It then follows from Lemma A.1 that

with equality if . Taking expectations under in (3.7), we deduce that

with equality when we replace with . ∎

Appendix B Extension to continuous Markov local martingales

The following statement extends Lemma 6.1 to a class of continuous Markov local martingales.

Lemma B.1.

Let be a local martingale with , for some locally Lipschitz function , and let be fixed points in , and the first exit time of from the interval . Then

| for all |

Proof.

Le be fixed, and denote . We decompose the proof in three steps.

Step 1: By dominated convergence the function is continuous, and it follows from classical argument using the tower property that is a viscosity solution of the equation

| (B.1) |

Step 2: Similarly, the function is a continuous function, and is in addition convex in the variable. Denote by the local time of the continuous martingale . Using the Itô-Tanaka formula, we see that:

By the density occupation formula, this provides for all Borel subset of :

where denotes the distribution function of . Notice that . Then:

Let be a molifier, and set . Then, is smooth, and it follows from the last equality that

where . Since is Lipschitz on , and is bounded, we see that

By the arbitrariness of and the Borel subset of , this shows that

| and |

Since , locally uniformly, it follows from the stability result of viscosity solutions that is a viscosity solution of on . We also directly see that and . Hence is also a viscosity solution of (B.1).

Step 3: To conclude that , we now use the fact that equation (B.1) has a unique viscosity solution. Indeed the corresponding equation satisfied by , for an arbitrary , satisfies the conditions of Theorem 8.2 of Crandall et al., (1992).

∎

References

- Acciaio et al., (2013) Acciaio, B., Beiglböck, M., Penkner, F., Schachermayer, W., and Temme, J. (2013). A trajectorial interpretation of Doob’s martingale inequalities. The Annals of Applied Probability, 23(4):1494–1505.

- Azéma and Yor, (1979) Azéma, J. and Yor, M. (1979). Une solution simple au problème de Skorokhod. In Séminaire de Probabilités, XIII (Univ. Strasbourg, Strasbourg, 1977/78), volume 721 of Lecture Notes in Math., pages 90–115. Springer, Berlin.

- Beiglböck et al., (2016) Beiglböck, M., Cox, A. M. G., and Huesmann, M. (2016). Optimal transport and Skorokhod embedding. Inventiones mathematicae. (online first).

- Beiglböck and Nutz, (2014) Beiglböck, M. and Nutz, M. (2014). Martingale Inequalities and Deterministic Counterparts. Electron. J. Probab., 19(95):1–15.

- Beiglböck et al., (2016) Beiglböck, M., Nutz, M., and Touzi, N. (2016). Complete duality for martingale optimal transport on the line. Ann. Probab. to appear.

- Bensoussan and Lions, (1982) Bensoussan, A. and Lions, J.-L. (1982). Applications of variational inequalities in stochastic control, volume 12 of Studies in Mathematics and its Applications. North-Holland Publishing Co., Amsterdam–New York.

- Brown et al., (2001) Brown, H., Hobson, D., and Rogers, L. C. G. (2001). The maximum maximum of a martingale constrained by an intermediate law. Probab. Theory Related Fields, 119(4):558–578.

- Burkholder, (1991) Burkholder, D. L. (1991). Explorations in martinagle theory and its applications. In École d’Été de Probabilités de Saint Flour XIX – 1989, volume 1464 of Lecture Notes in Math., pages 1–66. Springer Berlin.

- Chacon, (1985) Chacon, P. (1985). The filling scheme and barrier stopping times. PhD thesis, Univ. Washington.

- Chacon, (1977) Chacon, R. V. (1977). Potential processes. Trans. Amer. Math. Soc., 226:39–58.

- Cox et al., (2008) Cox, A. M. G., Hobson, D. G., and Obłój, J. (2008). Pathwise inequalities for local time: applications to Skorokhod embeddings and optimal stopping. Ann. Appl. Probab., 18(5):1870–1896.

- (12) Cox, A. M. G. and Wang, J. (2013a). Optimal robust bounds for variance options. arXiv: 1308.4363.

- (13) Cox, A. M. G. and Wang, J. (2013b). Root’s barrier: Construction, optimality and applications to variance options. Annals of Applied Probability, 23(3):859–894.

- Crandall et al., (1992) Crandall, M., Ishii, H., and Lions, P.-L. (1992). User’s guide to viscosity solutions of second order partial differential equations. Bull. Amer. Math. Soc., 27(1):1–67.

- De Angelis, (2015) De Angelis, T. (2015). From optimal stopping boundaries to Rost’s reversed barriers and the Skorokhod embedding. arXiv: 1505.02724.

- El Karoui, (1981) El Karoui, N. (1981). Les aspects probabilistes du contrôle stochastique. In Hennequin, P., editor, Ecole d’été de Probabilités de Saint-Flour IX-1979, volume 876 of Lecture Notes in Mathematics, pages 73–238. Springer Berlin Heidelberg.

- Elworthy et al., (1999) Elworthy, K. D., Li, X.-M., and Yor, M. (1999). The importance of strictly local martingales; applications to radial Ornstein–Uhlenbeck processes. Probability Theory and Related Fields, 115(3):325–355.

- Gassiat et al., (2014) Gassiat, P., Oberhauser, H., and dos Reis, G. (2014). Root’s barrier, viscosity solutions of obstacle problems and reflected FBSDEs. arXiv:1301.3798v4.

- Henry-Labordère et al., (2016) Henry-Labordère, P., Obłój, J., Spoida, P., and Touzi, N. (2016). The maximum maximum of a martingale with given marginals. Ann. Appl. Prob, 26(1):1–44.

- Hobson, (2011) Hobson, D. (2011). The Skorokhod Embedding Problem and Model-Independent Bounds for Option Prices. In Carmona, R., Çinlar, E. amd Ekeland, I., Jouini, E., Scheinkman, J., and Touzi, N., editors, Paris-Princeton Lectures on Mathematical Finance 2010, volume 2003 of Lecture Notes in Math., pages 267–318. Springer.

- Hobson, (1998) Hobson, D. G. (1998). Robust hedging of the lookback option. Finance Stoch., 2(4):329–347.

- Karatzas and Shreve, (1991) Karatzas, I. and Shreve, S. E. (1991). Brownian motion and stochastic calculus, volume 113 of Graduate Texts in Mathematics. Springer-Verlag.

- Loynes, (1970) Loynes, R. M. (1970). Stopping times on Brownian motion: Some properties of Root’s construction. Z. Wahrscheinlichkeitstheorie und Verw. Gebiete, 16:211–218.

- Madan and Yor, (2002) Madan, D. and Yor, M. (2002). Making Markov martingales meet marginals: with explicit constructions. Bernoulli, 8(4):509–536.

- McConnell, (1991) McConnell, T. R. (1991). The two-sided Stefan problem with a spatially dependent latent heat. Trans. Amer. Math. Soc., 326(2):669–699.

- Obłój, (2004) Obłój, J. (2004). The Skorokhod embedding problem and its offspring. Probab. Surv., 1:321–390 (electronic).

- Obłój, (2007) Obłój, J. (2007). The Maximality Principle Revisited: On Certain Optimal Stopping Problems. In Donati-Martin, C., Émery, M., Rouault, A., and Stricker, C., editors, Séminaire de Probabilités, XL, number 1899 in Lecture Notes in Mathematics, pages 309–328. Springer Berlin Heidelberg.

- Obłój and Spoida, (2016) Obłój, J. and Spoida, P. (2016). An iterated Azéma-Yor type embedding for finitely many marginals. Ann. Probab. to appear.

- Obłój et al., (2015) Obłój, J., Spoida, P., and Touzi, N. (2015). Martingale inequalities for the maximum via pathwise arguments. In Donati-Martin, C., Lejay, A., and Rouault, A., editors, In Memoriam Marc Yor - Séminaire de Probabilités XLVII, volume 2137 of Lecture Notes in Mathematics, pages 227–247. Springer Berlin Heidelberg.

- Peskir, (1999) Peskir, G. (1999). Designing options given the risk: the optimal Skorokhod-embedding problem. Stochastic Process. Appl., 81(1):25–38.

- Protter, (2005) Protter, P. E. (2005). Stochastic Integration and Differential Equations. Springer Science & Business Media, second edition edition. Google-Books-ID: mJkFuqwr5xgC.

- Rogers and Williams, (2000) Rogers, L. C. G. and Williams, D. (2000). Diffusions, Markov processes, and martingales. Vol. 2. Cambridge Mathematical Library. Cambridge University Press, Cambridge. Itô calculus, Reprint of the second (1994) edition.

- Root, (1969) Root, D. H. (1969). The existence of certain stopping times on Brownian motion. Ann. Math. Statist., 40:715–718.

- Rost, (1971) Rost, H. (1971). The stopping distributions of a Markov Process. Invent. Math., 14:1–16.

- Rost, (1976) Rost, H. (1976). Skorokhod stopping times of minimal variance. In Séminaire de Probabilités, X (Première partie, Univ. Strasbourg, Strasbourg, année universitaire 1974/1975), pages 194–208. Lecture Notes in Math., Vol. 511. Springer, Berlin.

- Skorokhod, (1965) Skorokhod, A. V. (1965). Studies in the theory of random processes. Translated from the Russian by Scripta Technica, Inc. Addison-Wesley Publishing Co., Inc., Reading, Mass.

- Touzi, (2012) Touzi, N. (2012). Optimal Stochastic Control, Stochastic Target Problems, and Backward SDE, volume 29. Springer Science & Business Media.