IMEX schemes for a Parabolic-ODE system of European Options with Liquidity Shocks

W. Mudzimbabwe, Lubin G. Vulkov

(Department of Applied Mathematics, Ruse University, Studentska str. 8, 7017 Ruse)

Abstract

The coupled system, where one is a degenerate parabolic equation and the other has not a diffusion term arises in the modeling

of European options with liquidity shocks.

Two implicit-explicit (IMEX) schemes

that preserve the positivity of the differential problem solution

are constructed and analyzed.

Numerical experiments confirm the theoretical results and illustrate the

high accuracy and efficiency of the schemes in combination with Richardson extrapolation

Key words Parabolic-ordinary system, European options, finite difference scheme, comparison principle, positivity

1 Introduction

We study numerically a parabolic-ODE system modelling option pricing liquidity shocks . The presence of liquidity shocks is a source of

non-liquidity risk and makes this market incomplete.

Ludkowsky and Shen [5] investigate a nonlinear pricing mechanism based on utility

maximization.

They consider the investor whose utility is described by an exponential utility function

where is the coefficient of risk aversion. The investor seeks to maximise utility of both terminal wealth and option payoff at

time horisont , which is chosen to coincide with the expiration date of all securities in market model.

Properties of the exponential utility function (1) imply that the value functions can be expressed as

where

is the wealth process and the functions

are related to the price of options in the two states, see (7) below.

Then the pair is the unique viscosity solutions of the coupled semi-linear system,

(5)

The terminal conditions are:

Here is volatility of the underlying, are transition intensities from state (0) to state (1) and vice versa, respectively, is drift of the underlying and , see [5] for more details.

Using and , the buyer’s indifference price (initial state 0) and (initial state

1) are defined via

where are the optimal solutions for terminal wealth with and without options respectively.

The value functions are given by

and the functions by,

where

Then, we obtain from (2), (5), (6)

and from (3), (4) the parabolic-ordinary system for and

with terminal conditions

The numerical solution of the system (8) is the main object of the present paper. The numerical treatment of the boundary layer effect for small values of and , the degeneracy at of the parabolic equation and the exponential nonlinearity lead to challenging problems [10].

The introduction of exponential nonlinear terms is an available assumption based on the financial nature of the model system (8).

There are many numerical schemes to solve nonlinear parabolic and hyperbolic equations. However, very few have dealt with an exponential

nonlinear term. The special nature of the nonlinear exponential term for a hyperbolic problem is discussed in [10].

A possible way to build an efficient numerical solution of (8), (9) is to implement an

IMEX method [1,9] . In this procedure the diffusion term is discretized implicitly in time and the reaction terms are discretized explicitly.

An IMEX method for numerical solution of reaction-diffusion equation with pure Neumann boundary conditions is developed in [3].

IMEX schemes, by applying explicit approximation both integral term and the convection term and an implicit approximation for

the second differential term are developed for integro-differential equations of finance in [2].

The rest of the paper is organized as follows. In the next section some results concerning well-posedness of Cauchy problem for (5)

and a comparison principle, obtained in [4] , are discussed . Also, two lemmas concerning discrete maximum principle [6,7] are formulated.

In Section 3 an implicit-explicit linear scheme is introduced. Comparison discrete principle and convergence of the scheme are

proved. Similar results are obtained for an IMEX

linearized scheme in Section 4. The computational experiments

in Section 5

confirm the applicability of our schemes and the theoretical results.

Finally, Section 6 summarizes our conclusions.

Notation

Let be a bounded interval in and let

denote the space of continuous functions on with the norm of any defined by

. For each

integer , let denote the space of - times differentiable functions on , with

continuous derivatives up to and including those of order , with the norm of any defined by

.

The notational conventions are adopted . The explicit reference to is dropped whenever the domain question is evident.

For any mesh functions on arbitrary mesh

,

the discrete maximum norm is defined by

Maximum norms and semi-norms for smooth functions of two variables are introduced in a similar way. Let

. Then

and if is the space of all functions on

with continuous derivatives then

2 Preliminaries

In this section we will describe some properties of the solution to system (8) using results obtained in [4].

Also

, following [6,7],

two lemmas , concerning discrete maximum principle (DM) are formulated.

We will consider solutions of (8)

satisfying

for some positive constants and .

In [4], well-posedness in weighted Sobolev spaces and comparison principle for the corresponding Cauchy problem (8), (9)

are established. With sufficient smoothness of the initial data the weak solutions

are classical ones.

In this paper we use the comparison principle for classical solutions of the problem (8), (9), i.e

.

Proposition 1 ([4])Let and be two classical solution of problem (8),(9) corresponding

to terminal data and , respectively.

If there exists some positive constants and such that and

satisfy conditions (10), then

In particular, let be bounded from below (or from above) by a constant

(resp. and the pair be a classical solution of the

terminal problem (8),(9).

Then

and (respectively

and ).

for any and any .

By making the substitutions ,

and , the system (3)

becomes

(14)

where . In accordance with (9) we take the initial conditions to be

(15)

For a call option,

(16)

We assume ground conditions for of the form (10).

In the next sections, the analysis of the difference approximations

of problem(12)-(14)

will use the following comparison principle that follows from those one for :

Proposition 2Let be two pairs of classical solutions of (12)-(14)

corresponding to the initial data and , respectively and such that conditions

of the type (10) hold. If the following inequalities also hold:

(15)

then

Hereinbelow we will use the following canonical form of writing a 3-point difference scheme

The discrete comparison principle for problem (16) was proved in [6,7] and is

formulated in the following way.

Lemma 2.1.

Let the conditions

be fulfilled. Then the solution of the difference scheme (15) satisfies the inequalities

Lemma 2.2.

Let the conditions

be met. Then for the solution the problem (16) the estimate holds

3 Implicit-Explicit Linear Scheme

In this section, we develop a linear IMEX scheme to solve the coupled semi-linear parabolic-ordinary system problem (11)-(12).

For call option one possible pair of boundary conditions is, see e.g. [10,11]

(18)

The left natural boundary condition for is

(19)

On we introduce the uniform

mesh

On the discrete domain we approximate the problem

(12)-(14)

by the difference scheme

The natural boundary condition can be approximated as follows

On the -th,

time level

the scheme (20)-(23) has the form

(28)

where

For the truncation error corresponding to (20)

we find

For the truncation error corresponding to (21) we get

In accordance with

Notation

we define the strong norms on the meshes and , respectively,

Let denote

Theorem 1Suppose that there exists classical solution of problem (10)-(14).

Then for sufficiently small

and the following

error estimate holds:

where the constant doesn’t depend of

and .

Proof

Define the errors by

Then satisfy the linear system of algebraic

equations:

where

and

Here and are the local truncation errors corresponding to the difference

equations (20) and (21), respectively. They will be estimated as follows.

Let us derive the truncation error corresponding to nonlinear (right) part:

For the nonlinear, right hand side of the first equation we obtain

and another one form

Now, taking into account the Tr1, we have

In a similar way, we find

Applying Lemma 2.1 we get

where is the strong norms as defined above.

We estimate

Next,

Therefore,

For we have

and

then

Since , we get

Therefore, by induction we have

which implies that

The following discrete comparison principle for the is crucial for the positivity of

the discrete approximations of the indeference prices and on the base of the scheme (20)-(24).

Theorem 2Let the assumptions of Theorem 1 hold

Let also ,

be grid functions defined on

and the inequalities hold:

Then for sufficiently small and we have

Proof. Let introduce

Then, from (26) we obtain

Using the mean-value theorem we get

We rewrite (30) in the form

Next, we rewrite (31) in the form

We apply the method of mathematical induction with respect to

to prove that

From (16), (17), we have

Assuming that (32) holds when , we will show that for

the above inequalities are

true.

On the base of Theorem 1 we can confirm that

for sufficiently small

there exists constants , such that

Then, if it necessary, we choose

in additional smaller such that

By induction, and using (Lemma 2.1)

we conclude that . Now Lemma 2.1

implies . It is clear from (32) and (34) that

4 Implicit-Explicit Linearised Scheme

Let us consider first the implicit scheme:

with boundary and initial approximations (22)-(24).

By Taylor expansion we get

We drop the -terms

and the results we insert in (36) and (37) to obtain:

(38)

(39)

where

Since , the diagonal domination can significally increase in

comparison with IMEX linear scheme, see system (20),(21).

Theorem 3Let the assumptions of Theorem 1 hold.Then

suppose that there exists classical solution of problem (10).

Then for sufficiently small

and the following

error estimate holds:

where the constant doesn’t depend of

and .

Proof.

Substituting from (37)

into (36) the first one we get

with and given by (22),(23) and (24).

For the error we have the linear system of algebraic equations

Further we follow the line of Theorem 1 to complete the proof.

The scheme (36), (37) also has similar

comparison properties of the linear IMEX scheme described in Theorem 2.

5 Numerical Experiments

In the section we perform numerical experiments to illustrate the accuracy, effectiveness and convergence of the implicit-explicit

linear scheme (20)-(24) (Scheme 1) and implicit-explicit linearized scheme (38),(39) (Scheme 2) developed in this article. We

provide experiments both with uniform and non-uniform meshes. Also, we present results of numerical experiments using Richardson

extrapolation in time.

The Tables (presented results) show the

accuracy in maximal discrete norm and convergence rate at final time , using

two consecutive meshes with formulas

where and are the exact and

the corresponding numerical solutions, respectively. In our case is or .

In Tables 1, 2,

we give the results from the computations

IMEX linear Scheme 1.

Table 1: Convergence results for at the money ( and ) and

based on Scheme 1

Value

Difference

Ratio

Value

Difference

Ratio

30

0.246669

0.235165

60

0.247438

7.70e-04

0.235917

7.52e-04

120

0.247749

3.11e-04

2.48 (1.31)

0.236218

3.01e-04

2.50 (1.32)

240

0.247887

1.38e-04

2.25 (1.17)

0.236349

1.31e-04

2.30 (1.20)

480

0.247952

6.50e-05

2.12 (1.09)

0.236410

6.10e-05

2.15 (1.10)

960

0.247983

3.10e-05

2.10 (1.07)

0.236439

2.90e-05

2.10 (1.07)

Table 2: Convergence results for at the money ( and ) and taking and using nonuniform Tavella-Randal grid with based on Scheme 1

Value

Difference

Ratio

Value

Difference

Ratio

30

0.247196

0.235660

60

0.247863

6.67e-04

0.236305

6.45e-04

120

0.248124

2.61e-04

2.56 (1.35)

0.236552

2.47e-04

2.61 (1.38)

240

0.248238

1.14e-04

2.29 (1.20)

0.236657

1.05e-04

2.35 (1.23)

480

0.248291

5.30e-05

2.15 (1.10)

0.236706

4.90e-05

2.14 (1.10)

960

0.248322

3.10e-05

1.71 (0.77)

0.236735

2.90e-05

1.69 (0.76)

Table 2

is based on a non-uniform grid and also shows that the scheme is first order in time. Here we use Tavella-Randal [8] mesh:

In this case, we choose to concentrate mesh points around the strike price since we expect the error to be largest there.

In Table 3 we list the results from computation with Scheme 2

that for this non-uniform grid the results are still first order accurate in time as in the uniform case.

Table 3: Convergence results for at the money ( and ) and taking based on Scheme 2

Value

Difference

Ratio

Value

Difference

Ratio

30

0.246685

0.234952

60

0.247444

7.59e-04

0.235812

8.60e-04

120

0.247752

3.08e-04

2.46 (1.30)

0.236165

3.53e-04

2.44 (1.28)

240

0.247889

1.37e-04

2.25 (1.17)

0.236323

1.58e-04

2.23 (1.16)

480

0.247953

6.40e-05

2.14 (1.10)

0.236397

7.40e-05

2.14 (1.09)

960

0.247984

3.10e-05

2.06 (1.05)

0.236433

3.60e-05

2.06 (1.04)

Table 4: Convergence results for at the money ( and ) and taking and using nonuniform Tavella-Randal grid with based on scheme 2

Value

Difference

Ratio

Value

Difference

Ratio

30

0.248722

0.237005

60

0.249432

7.10e-04

0.237812

8.07e-04

120

0.249715

2.83e-04

2.51 (1.33)

0.238139

3.27e-04

2.47 (1.30)

240

0.249839

1.24e-04

2.28 (1.19)

0.238283

1.44e-04

2.27 (1.18)

480

0.249897

5.80e-05

2.14 (1.10)

0.238351

6.80e-05

2.12 (1.08)

960

0.249928

3.10e-05

1.87 (0.90)

0.238387

3.60e-05

1.89 (0.92)

Now, we improve the convergence in time applying

Richardson extrapolation [4].

To this aim

we use the formula

where is order of numerical solution (1 in our case) and is the solution obtained using time step

and is the solution obtained using time step . The resulting solution has order of accuracy [4].

Table 5 shows the result of applying this technique to the Scheme 1. The order of accuracy in time is now two. Similarly this technique is applied to Scheme 2, see Table 6.

Hence the convergence is much slower but smoother compared to the explicit based Scheme 1 due the

error of linearisation.

The tables shows second order in time.

Table 5: Convergence results for at the money ( and ) and taking based on Scheme 1 using Richardson extrapolation

Difference

Ratio (order)

10

0.2451080

20

0.2465578

0.2480075

40

0.2472811

0.2480045

3.02e-6

80

0.2476431

0.2480051

5.79e-7

5.22 (2.38)

160

0.2478242

0.2480053

1.96e-7

2.96 (1.56)

320

0.2479148

0.2480053

5.13e-8

3.82 (1.93)

640

0.2479600

0.2480053

1.27e-8

4.05 (2.02)

1280

0.2479827

0.2480053

3.08e-9

4.12 (2.04)

2560

0.2479940

0.2480053

7.45e-10

4.13 (2.05)

Table 6: Convergence results for at the money ( and ) and taking based on Scheme 2 using Richardson extrapolation.

Difference

Ratio (order)

10

0.2451717

20

0.2465832

0.2479947

40

0.2472928

0.2480023

7.64e-6

80

0.2476486

0.2480045

2.14e-6

3.57 (1.84)

160

0.2478269

0.2480051

6.22e-7

3.44 (1.78)

320

0.2479161

0.2480053

1.78e-7

3.49 (1.81)

640

0.2479607

0.2480053

4.93e-8

3.62 (1.85)

1280

0.2479830

0.2480053

1.32e-8

3.73 (1.90)

2560

0.2479942

0.2480053

3.46e-9

3.81 (1.93)

5120

0.2479998

0.2480053

8.95e-10

3.87 (1.95)

10240

0.2480026

0.2480053

2.29e-10

3.91 (1.97)

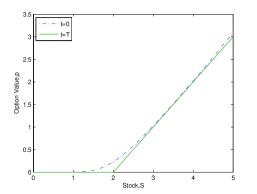

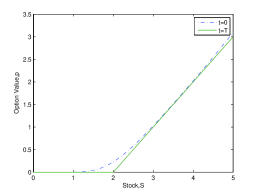

(a) at and

(b) at and

Figure 1: Comparing European option values at issue and maturity in the liquid and illiquid states for the IMEX Linear scheme

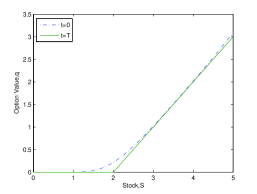

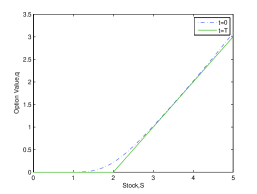

(a) at and

(b) at and

Figure 2: Comparing European option values at issue and maturity in the liquid and illiquid statesfor the IMEX Linearised scheme

In Figure 1 we compare options values and at issue and maturity in the liquid and illiquid states using the parameters , =0.3, , , , , and using the

Scheme 1

.

Figure 2

illustrate

the linearised scheme, using the same parameters.

Figures 1,2

illustrate

the positivity of the solution , using both schemes.

6 Conclusions

In this work we have considered one-dimensional problem of European options with liquidity shocks.

We have constructed and analyzed two IMEX finite difference schemes that preserve the positivity property

of the differential solution.

The second one(the IMEX linearized scheme) has better diagonal domination, respectively monotonicity.

It would be interesting to consider extensions of the IMEX schemes to the American options

with liquidity shocks. In this case one has to solve a free boundary problem. It could be written

as a linear complementary problem which could be discretized using the schemes given here. The

extension is beyond the scope of this paper, and we leave it for further work.

AcknowledgementThe authors thank to Prof.M.Koleva for the help at the numerical experiments. This research was supported

by the European Union under Grant Agreement number 304 617 (FP7 Marie Curie Action Project Multi-ITN Strike-Novel Methods in

Computational Finance) and Bulgarian National Fund of Science under Project DFNI I02/20-2014.

References

[1] U.M.Asher, S.J.Ruuth, B.T.Wetton, Implicit-explicit methods for time dependent partial

differential equations, SIAM J.Numer. Anal., 32(3) 797-823, (1995)

[2] M. Briani, R. Natalini, G.Russo, Implicit-explicit numerical

schemes for jump-diffusion processes, CALCOLO, 44 , 33-57, (2007)

[3] I.Farago, F. Izsak, T.Szabo, A. Kriston, An IMEX scheme for reaction-diffusion equations: applications for a PEM

fuel call model, Cent. Eur. J. Math. , v.11, N4, 746-759 (2013)

[4] T.Gyulov, L.Vulkov, Well-posedeness and comparison principle for

option pricing with switching liquidity, arXiv: 1502.07622 (2015)

[5] M. Ludkovski, Q. Shen, European option pricing

with liquidity shocks, Int. J. Theor. Appl. Finance16 (7) 135-143 (2013).

[6] P. Matus, The maximum principle and some of its applications, Comp. Methods, in Appl. Math.

V.2, No 1 , 50-91 (2002)

[7] A.A. Samarskii, Theory of Difference Scheme, Marcel Dekker, Inc., N.Y. (2001)

[8] D. Tavella, C. Randal, Pricing Financial Instruments: The Finite Difference Method, Wiley (2000).

[9]J.G. Verwer, J.G.Blom, W. Hundsdorter, An implicit-explicit approach for atmosphere transport-chemistry problems,

Appl. Num. Math. 20 , 191-209, (1996)

[10] L.Wang, W. Chen, C.Wang, An energy-conserving second order numerical

scheme for nonlinear hyperbolic equation with exponential nonlinear term, J. Comp. Appl. Math., V.280, 347-366 (2015)

[11] P. Wilmott, J. Dewynne, S. Howison, Option Pricing: Mathematical Models and Computations, Wiley, 1998

[12] H.Windcliff, P.A. Forssyth, K.R. Vetzal, Analysis of the stability of the linear boundary

condition for the Black-Sholes equation, J.Comp. Fin, 8:1, 65-92 (2004)