Several new tail index estimators

00footnotemark: 000footnotetext: The research was supported by Research Council of Lithuania, grant

No. MIP-076/2013

Vygantas Paulauskas, Marijus Vaičiulis

Department of Mathematics and Informatics,Vilnius University, Naugarduko st. 24, LT-03225 Vilnius, Lithuania

Institute of Mathematics and Informatics, Vilnius University, Akademijos st. 4, LT-08663 Vilnius, Lithuania

Abstract

In the paper we propose some new class of functions which is used to

construct tail index estimators. Functions from this new class is non-monotone in general, but presents a product of two monotone functions: the power function and the logarithmic function, which plays

essential role in the classical Hill estimator. Introduced new

estimators have better asymptotic performance comparing with the

Hill estimator and other popular estimators over all range of the

parameters present in the second order regular variation condition.

Asymptotic normality of the introduced estimators is proved, and

comparison (using asymptotic mean square error) with other

estimators of the tail index is provided. Some preliminary simulation results are presented.

1 Introduction and formulation of results

From the first papers of Hill and Pickands (see [15] , [21]), devoted to the estimation of the tail index (or, more generally, extreme value index), most of statistics constructed for this aim were based on order statistics and logarithmic function. Suppose we have a sample , considered as independent, identically distributed (i.i.d.) random variables with a distribution function

d.f. satisfying the following relation for large :

(1.1)

Parameter is called extreme value index (EVI) and is called the tail index, , for all

, and is a slowly varying at infinity function:

In the paper we consider the case only.

Denote

, ,

where is the left continuous inverse function of a monotone

function , defined by the relation

, . It is well-known that in the case assumption (1.1) is equivalent to the following one: for all ,

(1.2)

i.e., the quantile function varies regularly with index .

Let denote the order statistic of Taking some part of the largest values from the sample and the logarithmic function a statistician can form various statistics. In this way one can get Hill and Pickands estimators, moment and moment ratio estimators which are well-known and deeply investigated. The heuristic behind this approach (the threshold-over-peaks (TOP) phenomenon and maximum likelihood) is also given in many papers and monographs, therefore we do not provide it here.

There were estimators, based on a little bit different idea: the sample is divided into blocks and in each block the ratio of two largest values is taken. Then the linear function instead of logarithmic one is applied to these ratios. Estimators, based on this idea were constructed in [17] and [18].

The next step was to include the linear and logarithmic functions into some parametric family of functions, and, considering estimators based on block scheme, this was done in [19], taking the family of functions, defined for

(1.3)

In [20] this family of functions was applied for order statistic. This was done by introducing the statistics

and some combinations, formed from these statistics.

Here is some number satisfying , and in the EVI

estimation is chosen as a function of (thus, strictly speaking

we should denote it by ). In this way the generalizations of the Hill, the moment, and the moment ratio estimators (we shall write the expressions of these estimators a little bit later; to denote these estimators we shall use the letters and for generalizations we add the letter ) were obtained, for example, the generalized Hill estimator (GHE) is defined as

(1.4)

and the Hill estimator is obtained by taking .

The main goal of this paper is to introduce another parametric family of functions, which has the same property that includes logarithmic function, and to construct new estimators using this family.

For let us consider functions

where parameters and can be arbitrary real numbers, but for our purposes, connected with consistency, we shall require and .

Moreover, mainly we shall consider only integer values of parameter . The family , similarly to , contains logarithmic function (with ), but, contrary to , contains logarithmic function for any value of parameter (if ). Also let us note that for function is monotone for all values of , while for and there is no monotonicity.

Using these functions we can form statistics, similar to :

The above mentioned Hill estimator, moment estimator (introduced in [6]) and the moment ratio estimator (introduced in [3])

can be expressed via statistics , as follows

Let us note, that, due to the expressions of functions and , we can express statistic via statistics :

(1.5)

and there is continuity with respect to in this relation, since it is easy to see that

Taking into account that can be expressed via (see (3.2) in [20]), all estimators, which were introduced in [20], can be written by means of statistics only.

One more estimator of the parameter , which can be written as a function of statistics , therefore also by statistics

very recently was introduced in [1] (see also [16] and [22]).

It is named as the harmonic moment tail index estimator (HME, this abbreviation is used in [1]),

and for it is defined by formula

(1.6)

while for it is defined as a limit as . It is easy to see that

i.e., we get the Hill estimator. But very simple transformation shows that, denoting , we have

This means, that the HME is exactly the GHE, only additional (tuning) parameters (for HME) and (for GHE) have different ranges.

It is strange why there is requirement in the definition of HME, which corresponds to the condition for GHE. Of course, both statistics can be

defined for all real and , but in order to have consistent estimators of the parameter we must have some restrictions on these tuning parameters.

In [20] the consistency of GHE is proved under condition (or ), which is equivalent to condition , while in [1]

the consistency of HME is stated (there is only the sketch of the proof) without any additional condition on , so one can think that HME is consistent for

all . In [20] it was explained why the GHE is not consistent if , and from the expression (1.6) intuitively it is clear that for

we have . This discussion even shows that the requirement is not natural: for we have , thus for

we still have consistency of HME, while if , then in the interval there is no consistency. The asymptotic normality of HME in [1] is proved under the requirement , which is equivalent to the requirement , used in [20].

Our first result shows what quantities are estimated by the introduced statistics .

Theorem 1.1

Suppose that are i.i.d. nonnegative random variables whose quantile function satisfies

condition (1.2). Let and . Let us suppose that a sequence satisfies conditions

(1.7)

Then we have

(1.8)

Here stands for the convergence in probability and denotes Euler’s gamma function.

The following corollary allows to proof the consistency of estimators, expressed as a function of statistics with different and

Corollary 1.1

Suppose that are i.i.d. nonnegative random variables whose quantile function satisfies

condition (1.2). Let and , . Let us suppose that a sequence satisfies (1.7).

Let be a continuous function. Then

(1.9)

as .

The relation (1.9) gives us many possibilities to form consistent estimators of using

statistics with different .

Since it is not clear which combinations are good ones, we decided to restrict ourselves with two most simple statistics (that is, and )and to consider the following three estimators of

(1.12)

(1.13)

(1.16)

One can note, that the estimator is exactly the GHE, given in (1.4), only expressed via statistics . For us it will be convenient to use this notation for GHE, since we shall compare these two new constructed estimators not with the Hill estimator (which earlier was like a ”benchmark” for other estimators), but with the GHE . Since , the second estimator presents another generalization of the Hill estimator, while the third estimator gives us the generalized moment ratio estimator.

The main step in proving asymptotic normality of the introduced estimators is to prove asymptotic normality for statistics . As usual, in order to get asymptotic normality for estimators the so-called second-order regular variation (SORV) condition, in one or another form, is assumed. In this paper we shall use the SORV condition formulated by means of the function . We assume that there exists a measurable

function with the constant sign near infinity, which is not identically zero, and as ,

such that

(1.17)

for all . Here is the so-called second order parameter. It is known that (1.17)

implies that the function varies regularly with index .

Let us denote .

Theorem 1.2

Suppose that are i.i.d. nonnegative random variables whose quantile function satisfies

condition (1.17). Suppose that and that the sequence satisfies

(1.7) and

(1.18)

Then, as ,

(1.19)

where stands for the convergence in distribution and quantities are as follows

(1.20)

Here is zero mean Gaussian random vector with variances

, and covariance , where

(1.21)

From Theorem 1.2 we derive the main result of the paper.

Having asymptotic normality of the introduced estimators in Section 2 we compare the asymptotic mean square error (AMSE) of these estimators. In [20] we showed that the GHE dominates the Hill estimator in all region of the parameters and : Although this domination is rather small (see Fig. 2, the right graph ), but theoretically it is important, since, as far as we know, this is the first estimator, which asymptotically performs better than the Hill estimator in all region of possible range of two parameters and . Now we compare estimators with , and the results are promising. First of all, GMRE substantially outperforms MRE in all region of the parameters see Fig. 2, the left graph. Fig. 3, the right graph presents comparison of GMRE with GHE, and asymptotic result (solid line) shows that no one estimator dominates in all region (the ratio of AMSE does not depend on ),

while simulation results (points) demonstrates the domination of GMRE for all values of , for which the simulation was performed.

Finally, we formulate some results concerning the robustness of the introduced estimators. We follow the paper [1], where robustness was considered for the HME (or in our notation, for ).

To define the robustness measure for the estimator , instead of

we will use the notation .

Let us define

Then, following [1], for fixed and we take a quantity

which measures the worst effect of one arbitrarily large

contamination on the estimator . For fixed and these quantities are random variables, but it turns out that asymptotically they become constants, depending on and (here it is appropriate to note, that results on robustness are based on Theorem 1.1, thus there is no dependence on ).

Let us denote by the limit in probability of , , as and (1.7) holds.

Theorem 1.4

Suppose that are i.i.d. nonnegative random

variables whose quantile function satisfies condition

(1.2). Let .

Then we have

Assuming the SORV condition (1.17) we were able to find optimal values of for , (see formulas (2.7) and (2.8) in Section 2), therefore, for the generalized Hill estimator we get . For the generalized moment ratio estimator the situation is even better, since optimal value , therefore ,

while .

At first it seemed for us little bit strange, that for all three estimators we get the same value of , but looking more carefully to the construction of this measure of robustness, we realized that it is quite natural and even the proof is almost trivial. Since the second term in the expression of is independent of , moreover, it tends to , we have

(1.23)

Thus, robustness of the given estimator depends essentially on this first limit, which can be zero, infinity of finite,

depending on the term . For all classical estimators ()

this term tends to infinity, therefore we get infinite value for robustness, while for all three generalizations we are getting that this limit

as is , if and is , if , thus we are getting result of Theorem 1.4. Moreover, the proof of this theorem shows that we can contaminate the sample

not by one large value, but by several, and the asymptotic result will be the same - generalized estimators will remain (asymptotically) robust.

The rest of the paper is organized as follows. In the next section we investigate asymptotic mean square error of the introduced estimators, and compare these estimators with the generalized Hill estimator, using the same methodology as in [12], and provide some simulation results. Then there are formulated conclusions, and the last section is devoted to the proofs of the results. At the end of the proof of Theorem 1.3 we discuss the alternative proof of this result based on the paper [7].

2 Theoretical Comparison of the Estimators and Monte-Carlo simulations

As in [12] we can write the following relation for the asymptotic mean squared error

of the estimator

(2.1)

where a sequence satisfies (1.18). Here and below we write if as .

As in [20], assuming that is fixed, we perform the minimization of

with respect to . We will obtain optimal value of for the

estimator , which will be denoted by . Then we minimize asymptotic mean squared error

with respect to .

Thus, let us assume that is fixed. We define the function by the following relation:

(2.2)

By applying Lemma 2.8 in [5]

we get that minimum of right hand side of (2.1) is achieved with

(2.3)

Following the lines in [12] and using assumption (1.18), we get

Now we minimize (more precisely, the right-hand side of (2.5)) with respect to , and for this it is sufficient to

minimize the product with respect to .

Let us note that asymptotic parameters , depend on parameters and , while

quantities , depend on the product only. Therefore, it is convenient

to introduce notation and to consider minimization of the function

with respect to satisfying inequality . Equating the derivative of this function to zero, we get

(2.6)

By substituting the values of and into equation (2.6)

we get the equation

Whence it follows that the optimal value of for the

estimator is

(2.7)

since the second root of the quadratic equation does not satisfies the relation . As for the estimator , the optimal value of the parameter was found in [20], and in our notation (it is necessary to note, that SORV condition in [20] was used with different parametrization, see (1.3) therein) the optimal value of is

(2.8)

Unfortunately, the situation with the estimator is more complicated.

By substituting the expressions of and into (2.6)

we get the equation

For a fixed given value of this equation of -th order was solved with ”Wolfram Mathematica 6.0”.

It turns out that depending on the parameter it has 3 real roots and three pairs of conjugate roots or

5 real roots and two pairs of conjugate roots. All real roots were substituted into the function and optimal value was found in this way.

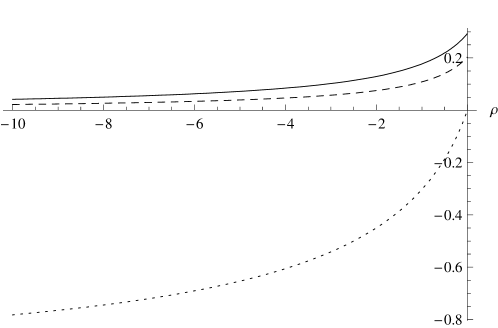

Numerical values of optimal value as a function of are provided in Fig.1. Although we got explicit and very simple expressions for the optimal values and , we provide these two functions (as functions of ) in the same Fig.1.

Figure 1: Graph of the functions (solid line), (dashed line) and (dotted line),

Let denote optimal value of the parameter .

From this picture we see that the first two functions has comparatively small range of values (for the range is ), this means that optimal value of parameters and are not sensitive to the parameter , but more sensitive to .

Now we are able compare the generalized Hill estimator

with the another generalization of the Hill estimator and

generalized moment ratio estimator .

But before performing comparison of these estimators, at first we demonstrate that

generalized moment ratio estimator

outperforms the initial moment ratio estimator in the whole

area . Denoting

it is not difficult to get that

where . Since we must investigate this function on negative half-line , it is convenient to denote and to write

with

where .

Taking logarithm of , using the fact that is product of several elementary functions, and using the simple relation

, one can get

In a similar way one can get

As a matter of fact, , but considering asymptotic normality and AMSE of estimators under consideration we excluded the case

therefore we calculate this last limit. More difficult is to show that the function is

monotone and increasing (or is decreasing), we skip these considerations, only we mention that we use the fact that

the logarithmic derivative of a product of functions is a sum of logarithmic derivatives of these functions.

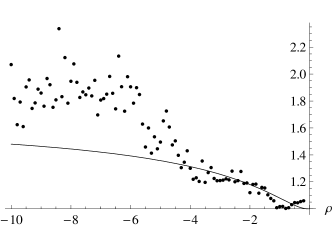

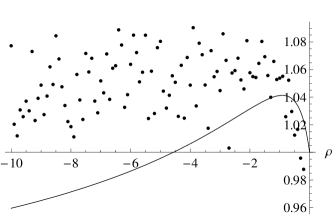

The graph of the function , is provided in Fig.2 in left. In the same picture we gave also results (in form of separate points) of simulations, which will be explained below. Surprisingly, simulation results are even better than theoretical asymptotical result - most points are above the graph of .

Figure 2: Graph of the functions

(solid line, in left), (solid line, in right) and results of Monte-Carlo simulations (points)

Now we can compare this result with the analogous comparison of

the generalized Hill estimator with the Hill estimator. If we

denote

then we have

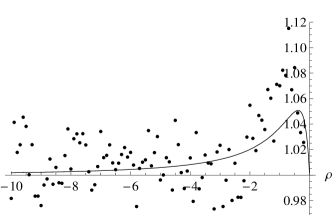

In [20] it was shown that the improvement of the

generalized Hill estimator over the Hill estimator is important only

theoretically since the maximal value of the function is

, see Fig.2 in right (this is the same graph as in Figure 2 in

[20], only now we added results of simulation; in this case

simulation results are in good correspondence with theoretical

ones).

Thus, comparing with the generalized Hill estimator, we have

substantial improvement of the moment ratio estimator, since in a

big range of the parameter the function is bigger

than 1.3, and the maximal value is close to .

Now we return to comparison of estimators and

with the generalized Hill estimator , and we must investigate the following two functions:

It is important to note that both functions are independent of and depend only on .

In view of (2.5) we have

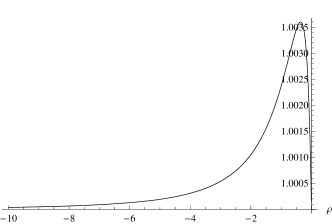

Since we were able to obtain the optimal value of only numerically, we can provide only a numerically obtained graph of the function , see Fig.3 on the left, therefore, in this case we did not provide simulation results.

Figure 3: Graph of the functions (on the left), (solid line, on the right) and

results of Monte-Carlo simulations (points)

Although this graph allow to believe that the new generalization of the Hill estimator dominates the generalized Hill estimator (which is the same as HME) in all region of parameters , but without explicit expression of the function we can not prove this.

Finally, comparing two generalizations of the Hill and moment ratio estimators (which, in our opinion are the most successful, since for both of them we have quite simple expression for optimal value of )we have

where . As can be seen

from Fig. 3 in right, generalized moment ratio estimator

dominates

the generalized Hill estimator for , where

. It is not difficult to show that

And empirical results, as in the case of function in

Fig. 2 (in left), are somehow unexpected - almost all empirical points in the

figure are not only above the graph of , but they are

bigger than 1, this means that the empirical MSE of generalized moment ratio

estimator is smaller than the empirical MSE of the generalized Hill estimator for

all values of in the interval , not only for

, as gives asymptotic theoretical

result.

Now we shall provide some results of Monte-Carlo simulations (part of these results are given in Figures 2 and 3 together with theoretical results). We must admit that these results are very preliminary, since for practical application of the proposed estimators still we are facing with problems of estimating the parameters and , and the main problem is with estimation of (and this problem is for almost all estimators, if we want to have asymptotic normality of the estimator), since optimal value of is expressed as a function of . We intend to return to this problem in a separate paper.

For simulations we shall use a little bit more restrictive condition than (1.17), namely, we assume that the distribution function

under consideration belongs to the Hall’s class of Pareto type distributions

([13],[14]), i.e.

(2.9)

where , and . This assumption is assumed for the following reason. Taking the ratio of AMSE of two estimators we do not need to know the function , but for simulations, having given sample size , we must calculate the value of in (2.3) and the empirical MSE of estimators, and for this we must have the function . Assuming (2.9),

we have that the second order condition (1.17) holds with

and from (2.2) it follows that

. Now we

can rewrite (2.3) as follows:

In fact, quantities , depend on , and only, thus replacing

and by some estimators and , we obtain the empirical values of the parameter

for the Hill and the moment ratio estimators:

(2.10)

(2.11)

For corresponding generalized estimators we have additionally to take estimators of optimal parameter therefore we have

(2.12)

(2.13)

Thus, in our simulations the comparison is made between the Hill estimator

, the generalized Hill estimator

, the moment ratio estimator

and the generalized moment ratio estimator

, with parameters given in (2.10)-(2.13).

We generated 1000 times samples of i.i.d. random variables of size with the following two d. f. with the extreme value

index , parameter and satisfying (2.9):

(i) the Burr d.f. , ;

(ii) the Kumaraswamy generalized exponential d.f. , .

The parameter which is present in (2.9) for the Burr distribution is and for the Kumaraswamy distribution - , and for both distributions.

To calculate the Hill and the generalized Hill estimators we used the following algorithm:

1. Estimate the parameter by the following estimator proposed in [8]:

where

with , and

To decide which values of parameters ( or ) and to take in the above written estimator we realized the algorithm provided in [11].

2. To estimate the parameter use the estimator , where

and , . This estimator was introduced in [10]. Also, as in the step 1 to choose the parameter we applied algorithm from [11].

3. By using (2.10) estimate parameter for the Hill estimator and then obtain ;

4. Estimate and ;

5. By using (2.12) estimate parameter for the generalized Hill estimator and find

estimate .

We used the similar algorithm (with obvious changes) for the moment ratio estimator and the generalized moment ratio estimator . Having values of the estimators we calculate MSE and bias of these estimators and also the ratios of some pairs of MSE.

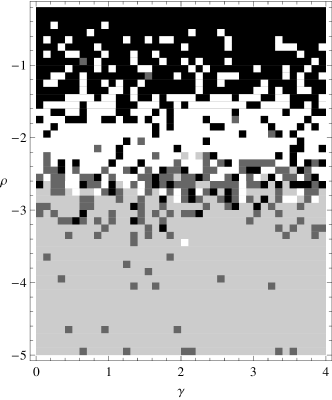

The results of simulations are summarized in Fig. 4 (for the Burr distribution) and in Fig. 5 (for the Kumaraswamy distribution).

For the Burr distribution we took parameters and in the intervals and respectively. In Fig. 4 (left) we divided

this rectangle into

squares , , . By taking true values of parameters and

as coordinates of the center

of the rectangle , we performed Monte-Carlo simulations. We colored the square in black if

empirical MSE of the estimator

is the smallest among all four estimators under consideration, while

areas of domination of the estimators ,

and

are in dark grey, grey and in white, respectively. In Fig. 4 (right) there are given

the areas of domination of absolute value of the bias using the same colors as in the left picture.

Figure 4: Empirical comparison of the estimators by using Burr distribution

We faced with serious difficulties while estimating the second order parameter

when samples are simulated from Kumaraswamy distribution with (for many samples computer was getting infinite value of sums

involved in the estimator of ), thus we restrict our simulations

in the rectangle . The corresponding areas of domination of MSE and bias for this distribution are presented in Fig.5.

Figure 5: Empirical comparison of the estimators by using Kumaraswamy distribution

Fig. 4 and 5 demonstrates that areas of domination almost do not depend on parameter and essentially depend only on .

This corresponds well to theoretical results that functions , ,

, and depend on only.

Therefore, taking the particular value and the hundred of values of in the interval for the

Burr distribution we obtained ratios of empirical MSE’s to complement theoretical comparison

and included these ratios (as separate points) in Fig. 2 and 3.

From Fig. 2 (right) we see that empirical results on comparison of MSE of the generalized Hill estimator with MSE of the Hill

estimator reflects quite well theoretical (asymptotic) function - points are on both sides of this function.

Little bit unexpectedly, Fig. 2 (left) and 3 (right) reveals that empirical results differ from theoretical ones.

In Fig. 2 (left), where generalized moment ratio estimator is compared with the moment ratio estimator, in the interval

empirical points are very close to the theoretical function , but in the interval all points are above the theoretical curve,

this means that the moment ratio estimator has MSE almost two times bigger that MSE of the generalized moment ratio estimator.

Empirical results in Fig. 3 (right) shows that the generalized moment ratio estimator performs better than GHE for all values of in the

interval , while theoretical result predict such result only for .

3 Conclusions

We introduced a new parametric class of functions which allows to construct many new generalizations of well-known estimators, including such as the Hill, the moment, and the moment ratio estimators. We prove asymptotic normality of all these generalized estimators in a unified way and demonstrate that in the sense of AMSE new estimators are better than the classical ones, especially promising looks GMR estimator. We hope that this new parametric class of functions will be useful in the difficult problem of estimating the second order parameter .

Preliminary simulation results show quite good correspondence with the obtained theoretical results, but we admit that future work on the behavior of new estimators for middle size samples is needed.

4 Proofs

Proof of the Theorem 1.1. There is nothing to prove in the trivial case . Keeping in mind

relation (1.5), conclusion (1.8) is the immediate consequence of the Theorem 1 in [20] in the case and . The case was investigated in [9].

Consider the case and , . Let us recall that the

function varies regularly at infinity with the

index , thus, by applying Potter’s bound we have: for

arbitrary there exits , such that, for

and ,

(4.1)

In order to apply (4.1) for the function it is

convenient to introduce the notation , where

, if , and ,

if . Then we get

(4.2)

Similarly we get the following inequalities

(4.3)

By multiplying inequalities (4.2) and (4.3), we

obtain

where

Let be i.i.d. random variables with distribution

function , . Taking

(4.4)

for we get

(4.5)

(4.6)

Note that , , thus

(4.7)

From this equality, by summing inequalities (4.5)

and(4.6), we get

(4.8)

(4.9)

By means of the standard argument (see e.q. [4]) one can

deduce that the left-hand side of (4.8) equals (in

distribution) to the sum

The expectation of this quantity equals to , where

One can verify that

(4.10)

By using the last identity, assumptions

, and the fact that we get

Whence we get , as .

Consider a quantity now. If , then and

we use the following inequality which holds for any real numbers and : . We have

Now it follows that , as . In the case we have , and since , applying the same inequality as above, we get

Now we take small such that , for example, one can take .

Keeping in mind that , we can estimate

Collecting the last two estimates we get

This allows to deduce that , as .

Let . By using inequality , which holds for

any real numbers and , we get

which implies , .

Thus, by applying the Khintchine weak law of large numbers, left-hand side of (4.8) converges to zero in probability.

In a similar way we can prove that the left-hand side of (4.9) tends to zero in probability, too. Theorem 1.1 is proved.

Proof of the Theorem 1.2. Let . Theorem 3.2.5 in [4] states

(4.11)

The relation (4.11), together with and Theorem 3.9 in [2], gives (1.19) for .

Consider now the case . Adjusting Potter’s type bounds (3.4) in [20] for our purposes

(such adjustment is needed since the second order condition (1.17) and the corresponding condition in [20] are slightly different),

we get

that for possibly different function with , as , and for each , there

exists a such that for , ,

(4.12)

where is defined in (1.3).

It is well-known that a similar Potter’s type bounds hold for the logarithmic function, see, e.g., inequalities (3.2.7) in [4]. Namely, for a possibly different function with , as , and for each , there

exists such that for , ,

(4.13)

Let . By multiplying inequalities (4.12) and (4.13) we get that for , ,

Suppose that is large enough that for , ,

Then, by applying inequalities (4.12) and (4.13) one more time we obtain

(4.14)

where

To prove two-dimensional Central Limit Theorem (1.19) we shall use the well-known Cramer-Wald method. Let . From (4.12) and (4.14) we get

where is the same as in (1.18), is proved in [20]. Now, by combining

(4.17)-(4.19) one can obtain (4.16).

Taking into account (4.16), substituting the values of and from (4.4) into (4.15) and performing summation

over we get distributional representation

(4.20)

where

By applying relations (4.17)-(4.19) one more time, we find

(4.21)

where , are defined in (1.20).

By using well-known Rényi’s representation (see e.g. Section 2 in [20] for details) we obtain

(4.22)

where

Keeping in mind equality (4.10)

one can deduce that

quantity presents normalized sum of zero mean random variables, which are i.i.d.. Moreover, under assumption ,

where , and are defined in (1.21). Thus, applying Lindeberg-Lévy central limit theorem we get the relation

. This, together with (4.22) gives

(4.23)

Applying Theorem 3.9 in [2], from (4.21) and (4.23) we get

Continuous Mapping Theorem gives us the relation

The last relation together with (4.20) gives (1.19). Theorem 1.2 is proved.

Proof of the Theorem 1.3. In the case the proof of the relation (1.22) can be found in [20] (proof of the Corollary 1) or

in [1] (proof of Theorem 2). But the asymptotic normality of all estimators

can be obtained in a unified way, expressing these estimators as functions of statistics and , and then combining Theorem 1.1, Theorem 1.2 and Continuous mapping Theorem. Namely, it is easy to see that

For the estimator we have

Multiplying the numerator and denominator of the right hand side by , we get

For the third estimator the following representation holds:

As it was said, it remains to combine Theorem 1.1, Theorem 1.2 and Continuous Mapping Theorem, and we deduce (1.22) with . For example, we have

with

From Theorems 1.1 and 1.2 and Theorem 3.9 from [2] we have

and now we apply Continuous Mapping Theorem (Theorem 2.7 in [2]).

As it was mentioned at the end of Introduction, there is possibility to use general approach in proving asymptotic normality of the introduced estimators, suggested in [7]. Let stands for the empirical d.f. based on the sample and let the empirical tail quantile function is defined as

Then almost all known estimators of the extreme value index that are based on some part of largest order statistics can be written as some functional

(defined on some functional space), applied to . Then, having estimator written as , the idea in [7] is to use invariance principle for the process in the functional space on which is defined and then requiring some smoothness (Hadamard differentiability in linear topological space) one can try to derive asymptotic normality of the estimator under consideration. For estimators, considered in the paper, it is possible to use this scheme, but the functionals are quite complicated. For example, one can write , but

and

For this complicated functional we must prove Hadamard differentiability on some linear topological space (to choose the appropriate space is also non trivial problem, usual space with Skorokhod topology is not a linear topological space). Thus, it seems that our approach is much more simple and we do not need more restrictive conditions (such that appears in [7]), since instead of invariance principle for tail quantile function we prove two-dimensional CLT for two particular statistics and then apply continuous mapping theorem in .

Proof of the Theorem 1.4. The expression of is given in [1], and at first we followed the pattern of the proof in [1], but, as it was noticed in Introduction, there is more simple proof.

From the expression (1.23), given in the Introduction, we see that, in order to find ,

it is sufficient to find the limit , since , as and (1.7) holds. For all three estimators calculations are simple and similar, therefore we demonstrate the proof for the estimator , having the most complicated expression.

It is clear that, for sufficiently large value of , can be written as

(4.24)

where and is the sum of the rest summands from statistic and does not depend on .

If , then and the limit of the quantity in (4.24) is , while for , and the limit in (4.24) is

and this expression almost (this word is used for the reason that in the above written expression the sum is divided by , while for complete coincidence division should be by ) coincides with , therefore, passing to the limit as we get in limit . In the case only nominator contains function which grows unboundedly, therefore, we get infinite value for .

References

[1] J. Beran, D. Schell, and M. Stehlik. The harmonic

moment tail index estimator: asymptotic distribution and robustness.

Ann. Inst. Stat. Math., 66:193–220, 2014.

[2] P. Billingsley. Convergence of Probability

Measures.

Wiley, New York, 1968.

[3] J. Danielsson, D. W. Jansen, and C. G. De Vries. The method of moments ratio

estimator for the tail shape parameter. Communications in Statistics - Theory and

Methods, 25(4):711–720, 1996.

[4] L. de Haan and A. Ferreira. Extreme Value Theory: An Introduction. Springer, New

York, 2006.

[5] A.L.M. Dekkers and L. de Haan. Optimal choise of sample fraction in extreme-value

estimation. J. Multivar. Anal., 47:173–195, 1993.

[6] A.L.M. Dekkers, J.H.J. Einmahl, and L. de Haan. A moment estimator for the index

of an extreme-value distribution. Ann. Statist., 17:1833–1855, 1989.

[7] H. Drees. A general class of estimators of the extreme value index. J. Stat. Planing

and Inference, 66:95–112, 1998.

[8] M.I. Fraga Alves, M. I. Gomes, and L. de Haan. A new class of semi-parametric

estimators of the second order parameter. Portugaliae Mathematica, 60:193–214, 2003.

[9] M.I. Gomes and M.J. Martins. Alternatives to Hill’s estimator - asymptotic versus

finite sample behaviour. J. Stat. Planning and Inference, 93:161–180, 2001.

[10] M.I. Gomes and M.J. Martins. Asymptotically unbiased estimators of the tail index

based on external estimation of the second order parameter. Extremes, 5:5–31, 2002.

[11] M.I. Gomes, D. Pestana, and F. Caeiro. A note on the asymptotic variance at optimal

levels of a bias-corrected Hill estimator. Stat. Probab.Lett., 79:295–303, 2009.

[12] L.de Haan and L. Peng. Comparison of tail index estimators. Statist. Nederlandica,

52:60–70, 1998.

[13] P. Hall. On some simple estimates of an exponent of regular variation. J. Roy. Statist.

Soc. Ser. B, 44:37–42, 1982.

[14] P. Hall and A.H. Welsh. Adaptive estimates of parameters of regular variation. Ann.

Statist., 13:331–341, 1985.

[15] B.M. Hill. A simple general approach to inference about the tail of a distribution.

Ann. Statist., 3:1163–1174, 1975.

[16] J.B. Henry III. A harmonic moment tail index estimator. J. Statistical Theor. Appl.,

8:141–162, 2009.

[17] V. Paulauskas. A new estimator for a tail index. Acta Appl. Math., 79:55–67, 2003.

[18] V. Paulauskas and M. Vaičiulis. Once more on comparison of tail index estimators.

Preprint, 2010.

[19] V. Paulauskas and M. Vaičiulis. Several modifications of DPR estimator of the tail

index. Lith. Math. J., 51:36–50, 2011.

[20] V. Paulauskas and M. Vaičiulis. On the improvement of Hill and some others estimators. Lith. Math. J., 53:336–355, 2013.

[21] J. Pickands. Statistical inference using extreme order statistics,. Ann. Stattist., 3:119–131, 1975.

[22] M. Stehlik, R. Potocký, H. Waldl, and Z. Fabián. On the favourable estimation of

fitting heavy tailed data. Computational Statistics, 25:485–503, 2010.