Meanfield games and model predictive control

Abstract.

Mean-Field Games are games with a continuum of players that incorporate the time-dimension through a control-theoretic approach. Recently, simpler approaches relying on the Best Reply Strategy have been proposed. They assume that the agents navigate their strategies towards their goal by taking the direction of steepest descent of their cost function (i.e. the opposite of the utility function). In this paper, we explore the link between Mean-Field Games and the Best Reply Strategy approach. This is done by introducing a Model Predictive Control framework, which consists of setting the Mean-Field Game over a short time interval which recedes as time moves on. We show that the Model Predictive Control offers a compromise between a possibly unrealistic Mean-Field Game approach and the sub-optimal Best Reply Strategy.

AMS subject classifications: 90B30, 35L65

Keywords: mean–field games, multi–agent systems

1. Introduction

According to the definition of the Handbook [21], systemic risk is the risk of a disruption of the proper functioning of the market which results in the reduction of the growth of the world’s Gross Domestic Product (GDP). In economics, a system such as a market can be described by a game, i.e. a set of agents endowed with strategies (and possibly other attributes) that they may play upon to maximize their utility function. In a game, the utility function depends on the other agents’ strategies. The proper functioning of a market is associated to a Nash equilibrium of this game, i.e. a set of strategies such that no agent can improve on his utility function by changing his own strategy, given that the other agents’ strategies are fixed. At the market scale, the number and diversity of agents is huge and it is more effective to use games with a continuum of players. Games with a continuum of players have been widely explored [4, 27, 31, 32].

To study systemic risk and its induced catastrophic changes in the economy, it is of primary importance to incorporate the time-dimension into the description of the system. A possible framework to achieve this is by means of a control-theoretic approach, where the optimal goal is not a simple Nash equilibrium, but a whole set of optimal trajectories of the agents in the strategy space. Such an approach has been formalized in the seminal work of [26] and popularized under the name of ’Mean-Field Game (MFG)’. It has given rise to an abundant literature, among which (to cite only a few) [8, 7, 6, 24, 12]. The MFG approach offers a promising route to investigate systemic risk. For instance, in the recent work [13], the MFG framework has been proposed to model systemic risk associated with inter-bank borrowing and lending strategies.

However, the fact that the agents are able to optimize their trajectory over a large time horizon in the spirit of physical particles subjected to the least action principle can be seen as a bit unrealistic. A related but different approach has been proposed in [19] and builds on earlier work on pedestrian dynamics [16]. It consists in assuming that agents perform the so-called ’Best-Reply Strategy’ (BRS): they determine a local (in time) direction of steepest descent (of the cost function, i.e. minus the utility function) and evolve their strategy variable in this direction. This approach has been applied to models describing the evolution of the wealth distribution among interacting economies, in the case of conservative [17] and nonconservative economies [18]. However, the link between MFG and BRS was still to be elaborated. This is the object of the present paper. We show that the BRS can be obtained as a MFG over a short interval of time which recedes as times evolves. This type of control is known as Model Predictive Control (MPC) or as Receding Horizon Control. The fact that the agents may be able to optimize the trajectories in the strategy space over a small but finite interval of time is certainly a reasonable assumption and this MPC strategy could be viewed as an improvement over the BRS and some kind of compromise between the BRS and a fully optimal but fairly unrealistic MFG strategy. We believe that MPC can lead to a promising route to model systemic risk. In this paper though, we propose a general framework to connect BRS to MFG through MPC and defer its application to specific models of systemic risk to future work.

Recently, many contributions on meanfield games and control mechanisms for particle systems have been made. For more details on meanfield games we refer to [8, 7, 6, 24, 12, 26]. Among the many possible meanfield games to consider we are interested in differential (Nash) games of possibly infinitely many particles (also called players). Most of the literature in this respect treats theoretical and numerical approaches for solving the Hamilton–Jacobi Bellmann (HJB) equation for the value function of the underlying game, see e.g. [12] for an overview. Solving the HJB equation allows to determine the optimal control for the particle game. However, the associated HJB equation posses several theoretical and numerical difficulties among which the need to solve it backwards in time is the most severe one, at least from a numerical perspective. Therefore, recently model predictive control (MPC) concepts on the level particles or of the associated kinetic equation have been proposed [16, 15, 20, 11, 1, 18, 17, 11]. While MPC has been well established in the case of finite–dimensional problems [23, 33, 28], and also in engineering literature under the term receding horizon control, contributions to systems of infinitely many interacting particles and/or game theoretic questions related to infinitely many particles are rather recent. It has been shown that MPC concepts applied to problems of infinitely many interacting particles have the advantage to allow for efficient computation [1, 17]. However, by construction MPC only leads to suboptimal solutions, see for example [25] for a comparison in the case of simple opinion formation model. Also, the existing approaches mostly for alignment models do not necessarily treat game theoretic concepts but focus on for example sparse global controls [15, 20, 11], time–scale separation and local mean–field controls [18] called best–reply strategy, or MPC on very short time–scales [1] called instantaneous control. Typically the MPC strategy is obtained solving an auxiliary problem (implicit or explicit) and the resulting expression for the control is substituted back into the original dynamics leading to a possibly modified and new dynamics. Then, a meanfield description is derived using Boltzmann or a macroscopic approximation. This requires the action of the control to be local in time and independent of future states of the system contrary to solutions of the HJB equation. Usually in MPC approaches independent optimal control problems are solved where particles do not anticipate the optimal control choices other particles contrary to meanfield games [26].

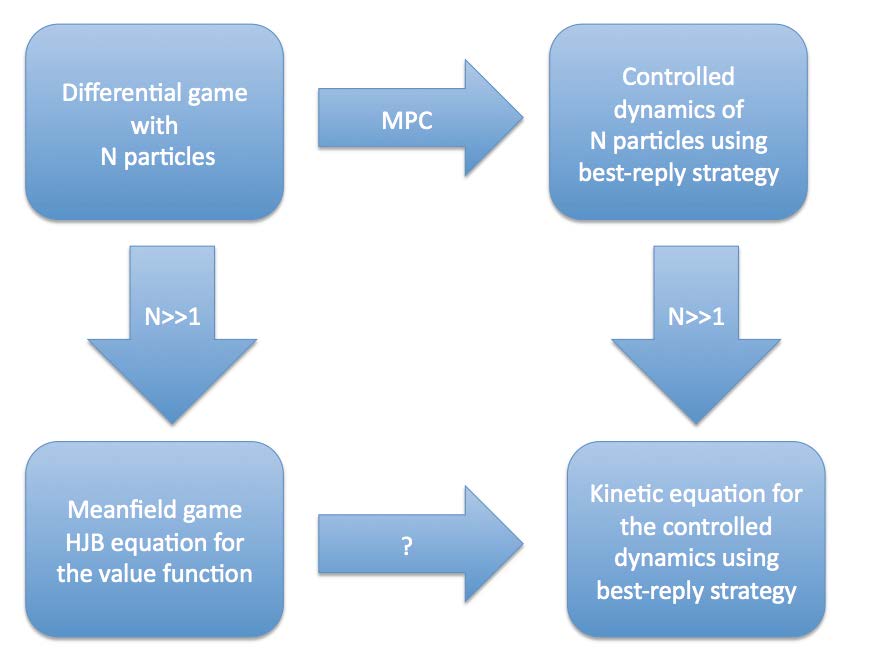

In this paper we contribute to the recent discussion by formal computations leading to a link between meanfield games and MPC concepts proposed on the level of particle games and associated kinetic equations. The relationship we plan to establish is highlighted in Figure 1.1. More precisely, we want to show that the MPC concept of the best–reply strategy [17] may be at least formally be derived from a meanfield games context.

2. Setting of the problem

We consider particles labeled by where each particle has a state We denote by the state of all particles and by the states of all particles except Further, we assume that each particle’s dynamics is governed by a smooth function depending on the state and we assume that each particle may control its dynamics by a control The dynamics for the particles is then given by

| (2.1) |

and initial conditions

| (2.2) |

We will drop the time–dependence of the variables whenever the intention is clear. Examples of models of the type (2.1) are alignment models in socio–ecological context, microscopic traffic flow models, production and many more, see e.g. the recent survey [29, 30, 34]. In recent contributions to control theory for equation (2.1) the case of a single control variable for all has been considered [1, 2, 11]. Here, we allow each particle to chose its own control strategy . We suppose a control horizon of be given. As in [12] we suppose that particle minimizes its own objective functional and determines therefore the optimal by

| (2.3) |

Herein, is the solution to (2.1) and equation (2.2). The optimal control and the corresponding optimal trajectory will from now on be denoted with superscript The minimization is performed on all sufficiently smooth functions . There is no restriction on the control similar to [26]. The objective related to particle is also supposed to be sufficiently smooth. The weights of the control and under additional conditions convexity of each optimization problem (2.3) is guaranteed. As seen in Section 3 a challenge in solving the problem (2.3) relies on the fact that the associated HJB has to be solved backwards in time. Contrary to [1, 11] problem (2.3) are in fact optimization problems that need to be solved simultaneously due to the dependence of on through equation (2.1). This implies that each particle anticipates the optimal strategy of all other particles when determining its optimal control . Obviously, the problem (2.3) simplifies when each particle anticipates an a priori fixed strategy of all other particles Then, the problem (2.3) decouples (in ) and the optimal strategy is determined independent of the optimal strategies It has been argued that this is the case for reaction in pedestrian motions [18]. In fact, therein the following best–reply strategy has been proposed as a substitute for problem (2.1)

| (2.4) |

As in the meanfield theory presented in [26, 12] we need to impose assumptions (A) on and before passing to the limit The assumption (B) will be used in Section 3.

-

(A)

For all and any permutation we have

for a smooth function and where Further we assume that for each the function enjoys the same properties as stated for

-

(B)

We assume that for all and all

Under additional growth conditions sequences of symmetric functions in many variables have a limit in the space of functions defined on probability measures, see e.g. [12, Theorem 2.1], [8, Theorem 4.1]. The corresponding result is recalled as Theorem A.1 in the appendix for convenience.

To exemplify computations later on we will use a basic wealth model [9, 14, 19, 18] where

| (2.5) |

for some bounded, non–negative and smooth function Clearly, fulfills (A). As objective function we use a measure depending only on aggregated quantities as in [17]. An example fulfilling (A) is

| (2.6) |

for some smooth function

Finally, we introduce some additional notation. We denote by the space of Borel probability measures over . The empirical discrete probability measure concentrated at a positions is denoted by

We also use this notation if is time dependent, i.e., , leading to the family of probability measures If the intention is clear we do not explicitly denote the dependence on of the measure (and on time if is time-dependent).

Based on the assumption (A) we will frequently use Theorem [12, Theorem 2.1]. This theorem is repeated for convenience in the appendix as Theorem A.1: let such that is symmetric where and any permutation . We may extend to a function such that Under assumptions given in Theorem A.1 the family is equicontinuous and there exists a limit such that up to a subsequence The result can be extended to a family of functions fulfilling assumption (A), see [8, Theorem 4.1]. We obtain an equicontinuous family with such that with limit and such that for any and a compact set we have for any fixed

| (2.7) |

In equation (2.7) we have the empirical measure on points in the argument of even so is defined on the empirical measure , i.e., we have

This is true since in the definition of the contribution of the empirical measure is for each point More details are given in [8] and [12, Section 7]. Since in the following it is often of importance to highlight the dependence on the empirical measure we introduce the following notation: we write

whenever equation (2.7) holds true.

2.1. From differential games to controlled particle dynamics

The best–reply strategy (2.4) is obtained also from a MPC approach [28] applied to equations (2.1) and (2.3). In order to derive the best–reply strategy we consider the following problem: suppose we are given the state of the system (2.1) at time . Then, we consider a control horizon of the MPC of and supposedly small. We assume that the applied control on is constant. For particle we denote the unknown constant by Instead of solving the problem (2.3) now on the full time interval we consider the objective function only on the receding time horizon Further, we discretize the dynamics (2.1) on using an explicit Euler discretization for the initial value We discretize the objective function by a Riemann sum. A naive discretization leads to a penalization of the control of the type Since the explicit Euler discretization in equation (2.8) is only accurate up to order we additionally require to have to obtain a meaningful control in the discretization (2.8) and also in the limit for . Therefore, in the MPC problem we need to scale the penalization of the control accordingly by This leads to a MPC problem associated with equation (2.3) and given by

| (2.8) | ||||

| (2.9) |

Solving the minimization problem (2.9) leads to

Now, we obtain a of order by Taylor expansion of at time Within the MPC approach the control for the time interval is therefore given by equation (2.10).

| (2.10) |

Usually, the dynamics (2.8) is then computed with the computed control up to Then, the process is repeated using the new state Substituting (2.10) into (2.8) and letting we obtain

| (2.11) |

This dynamics coincide with the dynamics generated by the best–reply strategy (2.4) provided that Therefore, on a particle level the controlled dynamics (2.11) of the best–reply strategy [17] is equivalent to a MPC formulation of the problem (2.3). For the toy example we obtain

| (2.12) |

2.2. From controlled particle dynamics (2.11) to kinetic equation

The considerations herein have essentially been studied for the best–reply strategy in the series of papers [19, 17, 18] and it is only repeated for convenience. The starting point is the controlled dynamics given by equation (2.11) which slightly extends the best–reply strategy. In order to pass to the meanfield limit we assume that (A) and (B) holds true. Then the particles are governed by

| (2.13) |

Associated with the trajectories the discrete probability measure is given by Using the weak formulation for a test function we compute the dynamics of over time as

Using [12, Theorem 2.1] and denoting by a family of empirical measures on we obtain from the previous equation

for some function . Assume and fulfill the assertions of [8, Theorem 4.1]. Then, we obtain in the sense of equation (2.7) that for any and sufficiently large and and therefore in the sense of equation (2.7)

This is the weak form of the kinetic equation for a probability measure

| (2.14) |

For the toy example the corresponding function is given by

and Therefore, we obtain

We summarize the previous findings in the following lemma.

Lemma 2.1.

Consider a fixed time horizon and consider particles governed by the dynamics (2.1) and initial conditions (2.2). Assume (A) and (B) hold true. Assume each particle , chooses its control at time by

| (2.15) |

Assume that for Then, the meanfield limit of the particle dynamics (2.1) and (2.15) is given by

| (2.16) |

for initial data

Finally, we summarize the MPC approach. Consider a time interval , an equidistant discretization such that and a first–order numerical discretization of particle dynamics (2.1) given by

| (2.17) |

for and Let in equation (2.17) be the control is piecewise constant. The constants obtained as discretization in time of equation (2.15) are given by

| (2.18) |

Then, each coincides up to with optimal control on the time interval of the minimization problems (2.19). For each and each fixed value we have up

| (2.19) |

where is given by equation (2.17).

3. Results related to meanfield games

In this paragraph we consider the limit of the problem (2.3) for a large number of particles. This has been investigated for example in [26] and derivations (in a slightly different setting) have been detailed in [12, Section 7]. In order to show the links presented in Figure 1.1 we repeat the formal computations in [12].

A notion of solution to the competing optimization problem (2.3) is the concept of Nash equilibrium. If it exists it may be computed for the differential games using the HJB equation. We briefly present computations leading to the HJB equation. Then, we discuss the large particle limit of the HJB equation and derive the best–reply strategy.

3.1. Derivation of the finite–dimensional HJB equation

The HJB equation describes the evolution of a value function of the particle The value function is defined as the future costs for a particle trajectory governed by equation (2.1) and starting at time , position and control

| (3.20) |

where is the solution to equation (2.1) with control and initial condition

| (3.21) |

Among all possible controls we denote by the optimal control that minimizes . We investigate the relation of the value function of particle to the optimal control . To this end assume that the coupled problem (2.3) has a unique solution denoted by . Each for each , is hence a solution to

The corresponding particle trajectories are denoted by and are obtained through (2.1) for an initial condition

Since depends on minimizing the value function (3.20) leads to the computation of formal derivatives of with respect to The optimal control is then found as formal point (in function space) where the derivative of with respect to vanishes. We have as Gateaux derivative of in an arbitrary direction

| (3.22) |

The derivative is not easily computed due to the unknown derivative of each state with respect to the acting control However, choosing a set of suitable co-states for and we may simplify the previous equation (3.22): we test equation (2.1) by functions for such that and integrate on with and initial data at to obtain

| (3.23) |

The derivative with respect to in an arbitrary direction is then

| (3.24) |

The previous equation can be equivalently rewritten as

| (3.25) |

Let for fulfill the coupled linear system of adjoint equations (or co-state equations), solved backwards in time,

| (3.26) |

Then, formally for every we have

Since for all we have

it follows that

for At optimality the necessary condition is

for all which implies that thanks to equation (3.22) we obtain for a.e.

This leads to the following equation a.e. in

| (3.27) |

Equations

| (3.28) |

and (3.26) for and equation (3.27) comprise the optimality conditions for the minimization of the value function given by equation (3.20). Due to equation (3.28) this system is a coupled system of ordinary differential and algebraic equations in the unknowns Solving for all those unknowns yields in particular the optimal control for the value function for all The adjoint equation (3.26) is posed backwards in time such that the system is two–point boundary value problem and due to the strong coupling of and it is not easy to solve. The derived system is a version of Pontryagins maximum principle (PMP) for sufficient regular and unique controls. We refer to [22, 33, 10] for more details. From now on we assume that equation (3.27) where solves equation (3.26) is necessary and sufficient for optimality of for minimizing the value function The corresponding optimal trajectory and co-state is denoted by introduced above. We formally derive the HJB based on the previous equations of PMP and refer to [22, Chapter 8] for a careful theoretical discussion.

Consider the function evaluated along the optimal trajectory i.e., let Then, by definition of and we have

Using the necessary condition (3.27) we obtain

| (3.29) | |||

The trajectory of depends on the initial condition . Computing the variation of with respect to for and evaluating at yields (since does not dependent on ):

From the weak form of the state equation (3.23) we obtain after differentiation with respect to the initial condition for

Similarly to the computations before we use the equation for given by equation (3.26) to express

Therefore, provided that is a solution to equation (3.26). Now, along we may express in equation (3.29) the co–state by the derivative of with respect to Replacing we obtain

By definition we have for all Therefore, instead of solving the PMP equation we may ask to solve the HJB for on for given by the reformulation of the previous equation:

| (3.30) | |||

with terminal condition

| (3.31) |

Remark 3.1.

Since does not contain terminal costs of the type the terminal condition for is zero. In case of terminal costs we obtain and terminal constraints for the co-state as in equation (3.26).

The aspect of the game theoretic concept is seen in the HJB equation (3.30) in the mixed terms If we model particles that do not anticipate the optimal choice of the control of other particles then minimization problems for in equation (3.20) are independent. Therefore the corresponding HJB for and with decouple and all mixed terms vanish. In a different setting this situation has been studied in [1, 2] where only a single control for all particles is present.

Assume we have a (sufficiently regular) solution with . Then, we obtain the optimal control and the optimal trajectory for minimizing by

| (3.32) |

where fulfills equation (3.28). This is an implicit definition of However, in view of the dynamics (3.28) it is not necessary to solve equation (3.32) for Similar to the discussion in Section 2.1 we obtain a controlled systems dynamic provided we have a solution to the HJB equation. The associated controlled dynamics are given by

| (3.33) |

and initial conditions (2.2). Comparing the HJB controlled dynamics with equation (2.11) we observe that in the best–reply strategy the full solution to the HJB is not required. Instead, is approximated by This approximation is also obtained using a discretization of equation (3.30) in a MPC framework. Since the equation for is backwards in time we may use a semi discretization in time on the interval given by

Using the terminal condition we obtain that for all

The derivation of the equation for the HJB equation for allows for an arbitrary choice of Hence we may set the terminal time also to This implies to consider the value function

where fulfills (3.28) and where we indicate the dependence on by a superscript on Applying the explicit Euler discretization as shown before leads therefore to

Hence, the best–reply strategy applied at time for a finite–dimensional problem of interacting particles coincides with an explicit Euler discretization of the HJB equation for a value function given by where is the state of the particle system at time

3.2. Meanfield limit of the HJB equation (3.30)

Next, we turn to the meanfield limit of equation (3.30) for To this end we assume that (A) and (B) holds. We further recall and introduce some notation;

We obtain the following set of equations for and

| (3.34) | |||

We show that a solution to the previous set of equations is obtained by considering the equation (3.35) below. Suppose that a function fulfills

| (3.35) | |||

and terminal condition Suppose a solution to equation (3.35) exists and fulfills the previous equation pointwise a.e. Then, we define

| (3.36) |

By definition therefore the partial derivatives of are computed as follows where

Due to assumption (A) we have that

for any The same is true for the argument of Therefore,

and Therefore, fulfills equation (3.34). Hence, instead of studying equation (3.34) we may study the limit for of equations (3.35). In view of Theorem A.1 a limit exists provided is symmetric (and fulfills uniform bound and uniform continuity estimates).

Note that, as a solution to equation (3.35) is symmetric with respect to the argument This holds true, since and are symmetric with respect to for any Hence, in the following we may assume to have a solution to equation (3.35) with the property that for any permutation we have

| (3.37) |

In view of Theorem A.1 we expect to converge for for to a limit function in the sense of Theorem A.1, i.e., up to a subsequence and for

Similar to equation (2.7) we obtain that the limit fulfills the convergence if the measure is replaced by the empirical measure for any Using the introduced notation in Section 2 we may therefore write

Similarly, we obtain the following meanfield limits for sufficiently large (and provided the assumptions of Theorem A.1 and [8, Theorem 4.1] are fulfilled.

It remains to discuss the limit of the mixed term in equations (3.34) and (3.35), respectively.

| (3.38) |

In order to derive the meanfield limit for equation (3.38) we require to be symmetric in all variables, i.e.,

-

(C)

We assume for any permutation and for all

Under assumption (C) we have in particular for all and a permutation

Therefore, In the sense of equation (2.7) we further obtain for any However under assumption (C) we also obtain Assuming the limit in Theorem A.1 is unique we obtain that is therefore independent of

Now, consider the discrete measure and For each we denote by the push forward of the discrete measure with the flow field and Let the characteristic equations for for fixed be given by the flow field

| (3.39) |

Similarly to equation (1.58), we obtain the directional derivative of the measure of with respect to the measure in direction of the vectorfield at as

where denotes the space of square integrable functions for the measure . Performing the limits for in the sense of equation (2.7), replacing by , we obtain finally the meanfield equation for given by

| (3.40) | |||

The previous equation is reformulated using the concept of directional derivatives of measures outlined in the Appendix A. Denote by a field. If for each is obtained as push forward with the vector field then, fulfills in a weak sense the continuity equation (1.54). Therefore, fulfills

| (3.41) |

As seen from the previous equations and the computations in equation (1.58) we therefore have

This motivates the following definition. For a family of measures with , define by

| (3.42) |

Then, from equation (3.40) we obtain

| (3.43) |

and from equation (3.41) we obtain using the definition (3.42)

| (3.44) |

Provided we may solve the meanfield equations (3.43) and (3.44) for we obtain a solution along the characteristics in space by the implicit relation (3.42). In this sense and under the assumptions to the meanfield limit of equation (3.34) or respectively equation (3.35) is given by the system of the following equations (3.45) and (3.46) for and for all The terminal condition for is given by

| (3.45) | ||||

| (3.46) |

We may also express the control given by equation (3.32), i.e.,

in the meanfield limit. Under assumption (B) and using equation (3.36) and equation (3.42) For any we have

3.3. MPC and best reply strategy for the meanfield equation (3.45)–(3.46)

We obtain the best–reply strategy through a MPC approach. Note that the calculations leading to equation (3.45) are independent of the terminal time Now, let a time be fixed and let be sufficiently small. Consider the value function on the receding horizon with initial conditions given at and where we, as before, add as a superscript to indicate the dependence on the short time horizon:

| (3.47) |

Repeating the derivation of the meanfield limit computations for we obtain equation (3.45) defined only for Also, we obtain A first–order in approximation of the solution to the (backwards in time ) equation (3.45) is therefore given by

| (3.48) |

Substituting this relation in the equation for in (3.45) we obtain the MPC meanfield equation as

| (3.49) |

This equation is precisely the same as we had obtained for the controlled dynamics using the best–reply strategy derived in the previous section and given by equation (2.14).

Remark 3.2.

The best–reply strategy for a meanfield game corresponds therefore to considering at each time a value function measuring only the costs for a small next time step. Those costs may depend on the optimal choices of the other agents. However, for a small time horizon the derivative of the running costs (i.e. ) is a sufficient approximation to the otherwise intractable solution to the full system of meanfield equations (3.45)-(3.46).

We summarize the findings in the following Proposition.

Proposition 3.1.

Assume (A) to (C) holds true and let be given. Denote by and the meanfield limit for of and respectively. Assume that be such that and fulfill equation

| (3.50) |

and let

Then, for any and up to an error of order the function implicitly defined by

is a solution to the meanfield equation

The meanfield equation is the formal limit for of an particle game on the time interval and described by equation (2.1) for i.e.,

A solution to the associated th HJB equations for are given by for and the optimal control is

Appendix A Technical details

We collect some results of [12] for convenience. The Kantorowich–Rubenstein distance for measures is given defined by

| (1.51) |

Theorem A.1 (Theorem 2.1[12]).

Let be a compact subset of . Consider a sequence of functions with Assume each is a symmetric function in all variables, i.e.,

for any permutation on Denote by the Kantorowich–Rubenstein distance on the space of probability measures and let be a modulus of continuity independent of . Assume that the sequence is uniformly bounded . Further assume that for all and all we have

where is defined by .

Then there exists a subsequence of and a continuous map such that

| (1.52) |

An extension is found in [8, Theorem 4.1]. As toy example consider . If is compactly supported, bounded and for all then the assumptions of the previous theorem are fulfilled. Note that the assumption on implies that for each we have for all and all This condition implies the estimate on The corresponding limit is given by the function defined by We have

Derivatives in the space of measures are described for example in [3]. They may be motivated by the following formal computation. Let be a smooth function on and let for and We denote by a subindex the evaluation at of the corresponding expression and by a prime the derivative of Then,

Therefore, we may write

provided that . Further, where is the push forward operator, see below. Hence, for the family of measures the previous computation lead to a notion of derivatives. This can be formalized to a calculus for derivatives in measure space and we summarize in the following more general results from [3, Chapter II.8]. We consider the space of probability measures [3, Equation (5.1.22)]:

We assume is equipped with the Wasserstein distance [3, Chapter 7.1.1]. In the case and for bounded measures this distance is equivalent to defined in equation (1.51). For the case we refer to [5] for a different characterization.

We consider absolutely continuous curves The curve is called absolutely continuous if there exists a function such that for all we have

| (1.53) |

see [3, Definition 1.1.1]. For an absolutely continuous curve , i.e., and there exists a vector field with a.e. such that the continuity equation

| (1.54) |

holds in a distributional sense. Further, a.e. in Here, for is the metric derivative of the curve The precise statement is given in [3, Theorem 8.3.1] and the metric derivative is given in [3, Theorem 1.1.2] by

| (1.55) |

The limit exists a.e. in provided that is absolutely continuous (1.53). We have a.e. for each function fulfilling equation (1.53), see [3, Chapter 1]. Also, the converse result holds true: If fulfills in a weak sense equation (1.54) for some then is absolutely continuous. Furthermore, solutions to equation (1.54) can be represented using the methods of characteristics, see [3, Lemma 8.1.6, Proposition 8.1.8]. Under suitable assumptions on and we have that a weak solution to equation (1.54) is

| (1.56) |

provided that solves characteristic system for every and every

| (1.57) |

Here, is the initial position of the characteristic in phase space and is the push forward operator, i.e., if applied to the set we have Equation (1.54) may also be viewed as the directional derivative of the family of measures in direction

In Section 3 we need to discuss a term of the type for a symmetric function Now, consider a family of paths generated by where solves the characteristic equation and Let We have then

If we assume that fulfills the assumption of Theorem A.1, then, there exists and then in the sense of equation (2.7). The following computation similar to the motivation shows the expression of the unknown term for large

| (1.58) | |||

| (1.59) |

In order to make the link with the theory developed in [12], we note that the last derivative at can be interpreted as

with the space of square integrable functions with respect to the measure . This formula can either be seen as the definition of if one follows the approach of [3] (which is the route taken here) or as a consequence of its definition if one follows the approach of [12].

Acknowledgments

This work has been supported by KI-Net NSF RNMS grant No. 1107444, grants DFG Cluster of Excellence ’Production technologies for high–wage countries’, BMBF KinOpt and CNRS PEPS-HuMaI grant ’DEESSes’. MH and JGL are grateful for the opportunity to stay and work at Imperial College, London, UK, in the Department of Mathematics. PD is on leave from CNRS Institut de Mathématiques de Toulouse UMR 5219; F-31062 Toulouse, France.

References

- [1] G. Albi, M. Herty, and L. Pareschi, Kinetic description of optimal control problems and applications to opinion consensus, Comm. Math. Sci., (2014).

- [2] G. Albi, L. Pareschi, and M. Zanella, Boltzmann type control of opinion consensus through leaders, arXiv preprint arXiv:1405.0736, (2014).

- [3] L. Ambrosio, N. Gigli, and G. Savare, Gradient Flows in Metric Spaces of Probability Measures, Lectures in Mathematics, Birkhäuser Verlag, Basel, Boston, Berlin, 2008.

- [4] R. J. Aumann, Existence of competitive equilibria in markets with a continuum of traders, Econometrica: Journal of the Econometric Society, (1966), pp. 1–17.

- [5] J.-D. Benamou and Y. Brenier, A computational fluid mechanics solution to the monge-kantorovich mass transfer problem, Numer. Math., 84 (2000), pp. 375–393.

- [6] A. Bensoussan, J. Frehse, and P. Yam, Mean Field Games and Mean Field Type Control Theory, Series: SpringerBriefs in Mathematics, New York, 2013.

- [7] A. Bensoussan, J. Frehse, and P. Yam, The master equation in mean field theory, arXiv preprint arXiv:1404.4150, (2014).

- [8] A. Blanchet and G. Carlier, From nash to cournot-nash equilibria via the monge-kantorovich problem, arXiv preprint arXiv:1404.5485, (2014).

- [9] J.-P. Bouchaud and M. Mézard, Wealth condensation in a simple model of economy, Phys. A, 282 (2000), pp. 536–545.

- [10] A. Bressan, Noncooperative differential games, Milan Journal of Mathematics, 79 (2011), pp. 357–427.

- [11] M. Caponigro, M. Fornasier, B. Piccoli, and E. Trélat, Sparse stabilization and optimal control of the Cucker-Smale model., Math. Control Relat. Fields, 3 (2013), pp. 447–466.

- [12] P. Cardaliaguet, Notes on mean field games, from P.-L. Lions lectures at College de France, (2010).

- [13] R. Carmona, J.-P. Fouque, and L.-H. Sun, Mean field games and systemic risk, arXiv preprint arXiv:1308.2172 (to appear in Comm. Math. Sci.), (2013).

- [14] S. Cordier, L. Pareschi, and G. Toscani, On a kinetic model for a simple market economy, J. Stat. Phys., 120 (2005), pp. 253–277.

- [15] I. Couzin, J. Krause, N. Franks, and S. Levin, Effective leadership and decision-making in animal groups on the move, Nature, 433 (2005), pp. 513–516.

- [16] P. Degond, C. Appert-Rolland, M. Moussaid, J. Pettré, and G. Theraulaz, A hierarchy of heuristic-based models of crowd dynamics, J. Stat. Phys., 152 (2013), pp. 1033–1068.

- [17] P. Degond, J.-G. Liu, and C. Ringhofer, Evolution of the distribution of wealth in an economic environment driven by local nash equilibria, Journal of Statistical Physics, 154 (2014), pp. 751–780.

- [18] , Evolution of wealth in a nonconservative economy driven by local nash equilibria, Phl. Trans. Roy. Soc. A, 372 (2014).

- [19] , Large-scale dynamics of mean-field games driven by local nash equilibria, Journal of Nonlinear Science, 24 (2014), pp. 93–115.

- [20] M. Fornasier and F. Solombrino, Mean-field optimal control, submitted to ESAIM: Control, Optimization, and Calculus of Variations, (preprint arXiv:1306.5913), (2013).

- [21] J.-P. Fouque and J. A. Langsam, Handbook on Systemic Risk, Cambridge University Press, 2013.

- [22] A. Friedman, Differential games, American Mathematical Society, Providence, R.I., 1974. Expository lectures from the CBMS Regional Conference held at the University of Rhode Island, Kingston, R.I., June 4–8, 1973, Conference Board of the Mathematical Sciences Regional Conference Series in Mathematics, No. 18.

- [23] L. Grüne and J. Pannek, Nonlinear model predictive control, Communications and Control Engineering Series, Springer, London, 2011. Theory and algorithms.

- [24] O. Guéant, J.-M. Lasry, and P.-L. Lions, Mean field games and applications, in Paris-Princeton Lectures on Mathematical Finance 2010, Springer, 2011, pp. 205–266.

- [25] M. Herty, S. Steffensen, and L. Pareschi, Mean-field control and Riccati equations, preprint, (2014).

- [26] J.-M. Lasry and P.-L. Lions, Mean field games, Japanese Journal of Mathematics, 2 (2007), pp. 229–260.

- [27] A. Mas-Colell, On a theorem of schmeidler, Journal of Mathematical Economics, 13 (1984), pp. 201–206.

- [28] D. Q. Mayne and H. Michalska, Receding horizon control of nonlinear systems, IEEE Trans. Automat. Control, 35 (1990), pp. 814–824.

- [29] S. Motsch and E. Tadmor, Heterophilious dynamics enhances consensus, arXiv preprint arXiv:1301.4123, (2013).

- [30] G. Naldi, L. Pareschi, and G. Toscani, Mathematical Modeling of Collective Behavior in Socio-Economic and Life Sciences, Series: Modeling and Simulation in Science, Engineering and Technology, Birkhauser, Boston, 2010.

- [31] D. Schmeidler, Equilibrium points of nonatomic games, Journal of Statistical Physics, 7 (1973), pp. 295–300.

- [32] N. Z. Shapiro and L. S. Shapley, Values of large games, i: a limit theorem, Mathematics of Operations Research, 3 (1978), pp. 1–9.

- [33] E. D. Sontag, Mathematical control theory, vol. 6 of Texts in Applied Mathematics, Springer-Verlag, New York, second ed., 1998. Deterministic finite-dimensional systems.

- [34] T. Vicsek and A. Zafeiris, Collective motion, Physics Reports, 517 (2012), pp. 71–140.