Support recovery without incoherence:

A case for

nonconvex regularization

| Po-Ling Loh1 | Martin J. Wainwright2 | |

|---|---|---|

| loh@wharton.upenn.edu | wainwrig@berkeley.edu | |

| Department of Statistics1 | Department of Statistics2 | |

| The Wharton School | Department of EECS | |

| University of Pennsylvania | UC Berkeley | |

| Philadelphia, PA 19104 | Berkeley, CA 94720 |

December 2014

Abstract

We demonstrate that the primal-dual witness proof method may be used to establish variable selection consistency and -bounds for sparse regression problems, even when the loss function and/or regularizer are nonconvex. Using this method, we derive two theorems concerning support recovery and -guarantees for the regression estimator in a general setting. Our results provide rigorous theoretical justification for the use of nonconvex regularization: For certain nonconvex regularizers with vanishing derivative away from the origin, support recovery consistency may be guaranteed without requiring the typical incoherence conditions present in -based methods. We then derive several corollaries that illustrate the wide applicability of our method to analyzing composite objective functions involving losses such as least squares, nonconvex modified least squares for errors-in-variables linear regression, the negative log likelihood for generalized linear models, and the graphical Lasso. We conclude with empirical studies to corroborate our theoretical predictions.

1 Introduction

The last two decades have generated a significant body of work involving convex relaxations of nonconvex problems arising in high-dimensional sparse regression (e.g., see the papers [10, 36, 7, 5, 3, 40] and references therein). In broad terms, the underlying goal is to identify a relatively sparse solution from among a set of candidates that also yields a good fit to the data. A hard sparsity constraint is most directly encoded in terms of the -“norm,” which counts the number of nonzero entries in a vector. However, this produces a nonconvex optimization problem that may be NP-hard to solve or even approximate [27, 38]. As a result, much work has focused instead on a slightly different problem, where the -based constraint is replaced by the convex -norm. There is a relatively well-developed theoretical understanding of the conditions under which such -relaxations produce good estimates of the underlying parameter vector (e.g., see the papers [3, 37, 25] and references therein).

Although the -norm encourages sparsity in the solution, however, it differs from the -norm in a crucial aspect: Whereas the -norm is constant for any nonzero argument, the -norm increases linearly with the absolute value of the argument. This linear increase leads to a bias in the resulting -regularized solution, and noticeably affects the performance of the estimator in finite-sample settings [11, 4, 21]. Motivated by this deficiency of -regularization, several authors have proposed alternative forms of nonconvex regularization, including the smoothly clipped absolute deviation (SCAD) penalty [11], minimax concave penalty (MCP) [44], and log-sum penalty (LSP) [6]. These regularizers may be viewed as a hybrid of - and -regularizers—they resemble the -norm in a neighborhood of the origin, but become (asymptotically) constant at larger values. Although the nonconvexity of the regularizer causes the overall optimization problem to be nonconvex, numerous empirical studies have shown that gradient-based optimization methods, while only guaranteed to find local optima, often produce estimators with consistently smaller estimation error than the estimators produced by the convex -penalty [11, 16, 46, 4, 21].

In recent years, several important advances have been made toward developing a theoretical framework for nonconvex regularization. Zhang and Zhang [43] provide results showing that global optima of nonconvex regularized least squares problems are statistically consistent for the true regression vector, leaving open the question of how to find such optima efficiently. Fan et al. [13] show that one step of a local linear approximation (LLA) algorithm, initialized at a Lasso solution, results in a local optimum of the nonconvex regularized least squares problem that satisfies oracle properties; Wang et al. [41] establish similar guarantees for the output of a particular path-following algorithm. Our own past work [20] provides a general set of sufficient conditions under which all stationary points of the nonconvex regularized problem are guaranteed to lie within statistical precision of the true parameter, which substantially simplifies the optimization problem to one of finding stationary points. Our work also establishes bounds on the -norm and prediction error that agree with the well-known bounds for the convex -regularizer, up to constant factors.

Despite these advances, however, an important question has remained: Are stationary points of such nonconvex problems also consistent for variable selection? In other words, does the support set of a stationary point agree with the support of the true regression vector, with high probability, and at what rate does the error probability tend to zero? In addition to providing a natural venue for establishing bounds on the -error, support recovery results furnish a much better understanding of when stationary points of nonconvex objectives are actually unique. For convex objectives, various standard proof techniques for variable selection consistency now exist, including approaches via Karush-Kuhn-Tucker optimality conditions and primal-dual witness arguments (e.g., [45, 40, 18]). However, these arguments, as previously stated, have relied crucially on convexity of both the loss and regularizer.

The first main contribution of our paper is to show how the primal-dual witness technique may be modified and extended to a certain class of nonconvex problems. Our proof hinges on the notion of generalized gradients from nonsmooth analysis [8], and optimization-theoretic results on norm-regularized, smooth, but possibly nonconvex functions [14]. Our main result is to establish sufficient conditions for variable selection consistency when both the loss and regularizer are allowed to be nonconvex, provided the loss function satisfies a form of restricted strong convexity and the regularizer satisfies suitable mild conditions. These assumptions are similar to the conditions required in our earlier work on - and -consistency [20], with an additional assumption on the minimum signal strength that allows us to derive stronger support recovery guarantees. Remarkably, our results demonstrate that for a certain class of regularizers—including the SCAD and MCP regularizers—we may dispense with the usual incoherence conditions required by -based methods, and still guarantee support recovery consistency for all stationary points of the resulting nonconvex program. This provides a strong theoretical reason for why certain nonconvex regularizers might be favored over their convex counterparts. In addition, we establish that for the same class of nonconvex regularizers, the unique stationary point is in fact equal to the oracle solution.

Several other authors have mentioned the potential for nonconvex regularizers to deliver estimation and support recovery guarantees under weaker assumptions than the -norm. The same line of work introducing nonconvex penalties such as the SCAD and MCP and developing subsequent theory [11, 12, 46, 42, 13] demonstrates that in the absence of incoherence conditions, nonconvex regularized problems possess local optima that are statistically consistent and satisfy an oracle property. Since nonconvex programs may have multiple solutions, however, these papers have focused on establishing theoretical guarantees for the output of specific optimization algorithms. More recently, Wang et al. [41] propose a path-following homotopy algorithm for obtaining solutions to nonconvex regularized -estimators, and show that iterates of the homotopy algorithm converge at a linear rate to the oracle solution of the -estimation problem. In contrast to theory of this type—applicable to a particular algorithm—the theory in our paper is purely statistical and does not concern iterates of a particular optimization algorithm. Indeed, the novelty of our theoretical results is that they establish support recovery consistency for all stationary points and, moreover, shed light on situations where such stationary points are actually unique. Finally, Pan and Zhang [29] provide results showing that under restricted eigenvalue assumptions on the design matrix that are weaker than the standard restricted eigenvalue conditions, a certain class of nonconvex regularizers yield estimates that are consistent in -norm. They provide bounds on the sparsity of approximate global and approximate sparse (AGAS) solutions, a notion also studied in earlier work [43]. However, their theoretical development stops short of providing conditions for recovering the exact support of the underlying regression vector.

The remainder of our paper is organized as follows: In Section 2, we provide basic background material on regularized -estimators and set up notation for the paper. We also outline the primal-dual witness proof method. Section 3 is devoted to the statements of our main results concerning support recovery and -bounds, followed by corollaries that specialize our results to linear regression, generalized linear models, and the graphical Lasso. In each case, we contrast our conditions for nonconvex regularizers to those required by convex regularizers and discuss the implications of our significantly weaker assumptions. We provide proofs of our main results in Appendices A and B, with supporting results and more technical lemmas contained in later appendices. Finally, Section 4 contains convergence guarantees for the composite gradient descent algorithm and a variety of illustrative simulations that confirm our theoretical results.

Notation:

For functions and , we write to mean that for some universal constant , and similarly, when for some universal constant . We write when and hold simultaneously. For a vector and a subset , we write to denote the vector restricted to . For a matrix , we write and to denote the spectral and Frobenius norms, respectively, and write to denote the elementwise -norm of . For a function , we write to denote a gradient or subgradient, if it exists. Finally, for , we write to denote the -ball of radius centered around 0.

2 Problem formulation

In this section, we briefly review the theory of regularized -estimators. We also outline the primal-dual witness proof technique that underlies our proofs of variable consistency for nonconvex problems.

2.1 Regularized -estimators

The analysis of this paper applies to regularized -estimators of the form

| (1) |

where denotes the empirical loss function and denotes the penalty function, both assumed to be continuous. In our framework, both of these functions are allowed to be nonconvex, but the theory applies a fortiori when only one function is convex. The prototypical example of a loss function to keep in mind is the least squares objective, . We include the side constraint, , in order to ensure that a global minimum exists.111In the sequel, we will give examples of nonconvex loss functions for which the global minimum fails to exist without such a side constraint (cf. Section 2.3 below). For modeling purposes, we have also allowed for an additional constraint, , where is an open convex set; note that we may take when this extra constraint is not needed.

The analysis of this paper is restricted to the class of coordinate-separable regularizers, meaning that is expressible as the sum

| (2) |

Here, we have engaged in some minor abuse of notation; the functions appearing on the right-hand side of equation (2) are univariate functions acting upon each coordinate. Our results are readily extended to the inhomogenous case, where different coordinates have different regularizers , but we restrict ourselves to the homogeneous case in order to simplify our discussion.

From a statistical perspective, the purpose of solving the optimization problem (1) is to estimate the vector that minimizes the expected loss function:

| (3) |

where we assume that is unique and independent of the sample size. Our goal is to develop sufficient conditions under which a minimizer of the composite objective (1) is a consistent estimator for . Consequently, we will always choose , which ensures that is a feasible point.

2.2 Class of regularizers

In this paper, we study the class of regularizers that are amenable in the following sense.

Amenable regularizers:

For a parameter , we say that is -amenable if:

-

(i)

The function is symmetric around zero (i.e., for all ), and .

-

(ii)

The function is nondecreasing on .

-

(iii)

The function is nonincreasing on .

-

(iv)

The function is differentiable, for .

-

(v)

The function is convex, for some .

-

(vi)

.

We say that is -amenable if, in addition:

-

(vii)

There is some scalar such that , for all .

Conditions (vi) and (vii) are also known as the selection and unbiasedness properties, respectively, and the MCP regularizer [42] described below minimizes the maximum concavity of subject to (vi)–(vii). Note that the usual -penalty is -amenable, but it is not -amenable, for any . The notion of -amenability was also used in our past work on -bounds for nonconvex regularizers [20], with the exception of the selection property (vi). Since the goal of the current paper is to obtain stronger conclusions, in terms of variable selection and -bounds, we will also require to satisfy the selection and unbiasedness properties.

Note that if we define , the conditions (iv) and (vi) together imply that

is everywhere differentiable. Furthermore, if

is -amenable, we have , for all . In

Appendix F.1, we provide some other useful results concerning amenable regularizers.

Many popular regularizers are either -amenable or -amenable. Let us consider a few examples to illustrate.

Smoothly clipped absolute deviation (SCAD) penalty:

This penalty, due to Fan and Li [11], takes the form

| (4) |

where is a fixed parameter. A straightforward calculation show

that the SCAD penalty is -amenable, with and .

Minimax concave penalty (MCP):

This penalty, due to Zhang [42], takes the form

| (5) |

where is a fixed parameter. The MCP regularizer is -amenable, with and .

Finally, let us consider some examples of penalties that are -amenable, but not -amenable, for any .

Standard Lasso penalty:

As mentioned previously, the -penalty is -amenable, but not -amenable, for any .

Log-sum penalty (LSP):

This penalty, studied in past work [6], takes the form

| (6) |

For , we have , and . In particular, the LSP regularizer is -amenable, but not -amenable, for any .

2.3 Nonconvexity and restricted strong convexity

Next, we consider some examples of the types of nonconvex loss functions treated in this paper. At a high level, we consider loss functions that are differentiable and satisfy a form of restricted strong convexity, as used in large body of past work on analysis of high-dimensional sparse -estimators (e.g., [1, 3, 37, 20, 25]). In order to provide intuition before stating the formal definition, note that for any convex and differentiable function that is globally convex and locally strongly convex around a point , there exists a constant such that

| (7) |

for all . The notion of restricted strong convexity (with respect to the -norm) weakens this requirement by adding a tolerance term that penalizes non-sparse vectors. In particular, for positive constants , we have the following definition:

Restricted strong convexity:

Given any pair of vectors , the loss function satisfies an -RSC condition, if:

| (8a) | |||||

| (8b) |

where are strictly positive constants, and

are nonnegative constants.

As noted in inequality (7), any locally strongly convex function that is also globally convex satisfies the RSC

condition with tolerance parameters . For

, the RSC

condition imposes strong curvature only in certain directions of

-dimensional space—namely, those nonzero directions for which the ratio

is relatively small; i.e., less than a constant multiple of

. Note that for any -sparse

vector , we have , so that the RSC definition guarantees a form of strong

convexity for all -sparse vectors when .

Standard linear regression:

Consider the standard linear regression model, in which we observe i.i.d. pairs , linked by the linear model

and the goal is to estimate . A standard loss function in this case is the least squares function , where is the vector of responses and is the design matrix with as its row. In this special case, for any , we have

Consequently, for the least squares loss function, the RSC condition is essentially equivalent to lower-bounding sparse restricted eigenvalues [37, 3].

Linear regression with errors in covariates:

Let us now turn to a simple extension of the standard linear regression model. Suppose that instead of observing the covariates directly, we observe the corrupted vectors , where is some type of noise vector. This setup is a particular instantiation of a more general errors-in-variables model for linear regression. The standard Lasso estimate (applied to the observed pairs ) is inconsistent in this setting.

As studied previously [19], it is natural to consider a corrected version of the Lasso, which we state in terms of the quadratic objective,

| (9) |

Our past work [19] shows that as long as are unbiased estimates of , any global minimizer of the appropriately regularized problem (1) is a consistent estimate for . In the additive corruption model described in the previous paragraph, a natural choice for the pair is given by

where the covariance matrix is assumed to be known. However, in the high-dimensional setting (), the random matrix is not positive semidefinite, so the quadratic objective function (9) is nonconvex. (This is also a concrete instance where the objective function (1) requires the constraint in order to be bounded below.) Nonetheless, our past work [19, 20] shows that under certain tail conditions on the covariates and noise vectors, the loss function (9) does satisfy a form of restricted strong convexity.

Generalized linear models:

Moving beyond standard linear regression, suppose the pairs are drawn from a generalized linear model (GLM). Recall that the conditional distribution for a GLM takes the form

| (10) |

where is a scale parameter and is the cumulant function. The loss function corresponding to the negative log likelihood is given by

| (11) |

and it is easy to see that equation (11) reduces to equation (9) with the choice . Using properties of exponential families, we may also check that equation (3) holds. Negahban et al. [25] show that a form of restricted strong convexity holds for a broad class of generalized linear models.

Graphical Lasso:

Now suppose that we observe a sequence of -dimensional random vectors with mean 0. Our goal is to estimate the inverse covariance matrix , assumed to be relatively sparse. In the Gaussian case, sparse inverse covariance matrices arise from imposing a Markovian structure on the random vector [35]. Letting denote the sample covariance matrix, consider the loss function

| (12) |

which we refer to as the graphical Lasso loss. Taking derivatives, it is easy to check that , which verifies the population-level condition (3). As we show in Section 3.5, the graphical Lasso loss is locally strongly convex, so it satisfies the restricted strong convexity condition with .

2.4 Primal-dual witness proof technique

We now outline the main steps of the primal-dual witness (PDW) proof technique, which we will use to establish support recovery and -bounds for the program (1). Such a technique was previously applied only in situations where is convex and is the -penalty, but we show that this machinery may be extended via a careful analysis of local optima of norm-regularized functions based on generalized gradients.

As stated in Theorem 1 below, the success of the PDW construction guarantees that stationary points of the nonconvex objective are consistent for variable selection consistency—in fact, they are unique. Recall that is a stationary point of the optimization program (1) if we have , for all in the feasible region [2]. Due to the possible nondifferentiability of at 0, we abuse notation slightly and denote

(see, e.g., Clarke [8] for a more comprehensive treatment of such generalized gradients). The set of stationary points includes all local/global minima of the program (1), as well as any interior local maxima.

The key steps of the PDW argument are as follows:

-

(i)

Optimize the restricted program

(13) where we enforce the additional constraint that . Establish that ; i.e., is an interior point of the feasible set.

-

(ii)

Define , and choose to satisfy the zero-subgradient condition

(14) where , , and . Establish strict dual feasibility of ; i.e., .

- (iii)

Note that the output of the PDW construction depends implicitly on the choice of and .

Under the restricted strong convexity condition, the restricted problem (13) minimized in step (i) is actually a convex program. Hence, if , the zero-subgradient condition (14) must hold at for the restricted problem (13). Note that when is convex and is the -penalty as in the conventional setting, the additional -constraint in the programs (1) and (13) is omitted. If also , the vector is automatically a zero-subgradient point if it is a global minimum of the restricted program (13), which greatly simplifies the analysis. Our refined analysis shows that under suitable restrictions, global optimality still holds for and , and the convexity of the restricted program therefore implies uniqueness.

In the sections to follow, we show how the primal-dual witness technique may be used to establish support recovery results for general nonconvex regularized -estimators, and then derive sufficient conditions under which stationary points of the program (1) are in fact unique.

3 Main statistical results and consequences

We begin by stating our main theorems concerning support recovery and -bounds, and then specialize our analysis to particular settings of interest.

3.1 Main results

Our main statistical results concern stationary points of the regularized -estimator (1), where the loss function satisfies the RSC condition (8b) with parameters , and the regularizer is -amenable with . Our first theorem concerns the success of the PDW construction described in Section 2.4. The theorem guarantees support recovery provided two conditions are met, the first involving an appropriate choice of and , and the second involving strict dual feasibility of the dual vector . Note that it is through validating the second condition that the incoherence assumption arises in the usual -analysis, but we demonstrate in our corollaries to follow that strict dual feasibility may be guaranteed under weaker conditions when a -amenable regularizer is used, instead. (See Appendix C for a technical discussion.) The proof of Theorem 1 is contained in Appendix A.

Theorem 1 (PDW construction for nonconvex functions).

Suppose is an -RSC function and is -amenable, for some . Suppose that:

-

(a)

The parameters satisfy the bounds

(15a) (15b) -

(b)

For some , the dual vector from the PDW construction satisfies the strict dual feasibility condition

(16)

Then for any -sparse vector , the program (1) with a sample size has a unique stationary point, given by the primal output of the PDW construction.

Remark:

Of course, Theorem 1 is

vacuous unless proper choices of , and exist. In

the corollaries to follow, we show that , with

high probability, in many settings of interest. In particular, we may

choose to satisfy

inequality (15a) when the sample size satisfies . Note that then causes

inequality (15b) to be satisfied under the same sample size

scaling. Indeed, if the RSC parameters were known, we could simply

take and then

focus on tuning . Finally, note that the inequality

is satisfied as long as , which is guaranteed by the

preceding choice of and the scaling . In this way, the existence of an appropriate choice of

is guaranteed.222An important observation is that the parameter

does not actually appear in the statistical estimation

procedure and is simply a byproduct of the PDW analysis. Hence, it

is not necessary to know or estimate a valid value of .

Note also that our results require the assumption , where a smaller gap of translates into a larger sample size requirement. This consideration may motivate an advantage of using the LSP regularizer over a regularizer such as SCAD or MCP; as discussed in Section 2.2, the SCAD and MCP regularizers have equal to a constant value, whereas for the LSP. On the other hand, the LSP is not -amenable, which as discussed later, allows us to remove the incoherence condition for SCAD and MCP when establishing strict dual feasibility (16). Indeed, the MCP is designed so that is minimal subject to unbiasedness and selection of the regularizer [44]. This suggests that for more incoherent designs, the LSP may be preferred for variable selection, whereas for less incoherent designs, SCAD or MCP may be better. In the simulations of Section 4, however, the LSP regularizer only performs negligibly better than the -penalty in situations where the incoherence condition holds and the same regularization parameter is chosen.

Finally, we note that although the conditions of Theorem 1 are already relatively mild, they are nonetheless sufficient conditions. Indeed, as confirmed experimentally, there are many situations where the condition does not hold, yet the stationary points of the program (1) still appear to be supported on and/or unique. Two feasible explanations for this phenomenon are the following: First, it is possible that in cases where , the composite objective function is not convex over the entire feasible set, yet is still sufficiently close to and the positive definite condition

| (17) |

holds at the point . Examining the proof of

Theorem 1, we may see that

equation (17), together with strict dual feasibility, is

sufficient for establishing that is a local minimum of the

program (1); Lemma 3 in

Appendix A then implies that all stationary points

are supported on . Nonetheless, since the restricted

program (13) is no longer guaranteed to be convex,

multiple stationary points may exist. Second, we note that although

strict convexity of the objective and a zero-subgradient

condition are certainly sufficient conditions to guarantee a unique

global minimum, a function may have diverse regions of

convexity/concavity and still possess a unique global minimum. In such cases, we

may still be lucky in simulation studies and obtain the global optimum.

Our second general theorem provides control on the -error between any stationary point and , and shows that the local/global optimum of a nonconvex regularized program agrees with the oracle result when the regularizer is -amenable. We define the oracle estimator according to

and write . In other words, the oracle estimator is the unpenalized estimator obtained from minimizing over the true support set . As shown in the proof, under the assumed RSC conditions, the restricted function is strictly convex and is uniquely defined. With this notation, we have the following result:

Theorem 2.

Suppose the assumptions of Theorem 1 are satisfied and strict dual feasibility (16) holds. Then the unique stationary point of the program (1) has the following properties:

-

(a)

Let . Then

(18) -

(b)

Moreover, if is -amenable and the minimum value is lower-bounded as

(19a) then agrees with the oracle estimator , and we have the tighter bound (19b)

Remark:

Theorem 2 underscores the strength of -amenable regularizers. Indeed, with the addition of a

beta-min condition (19a), which provides a lower bound on the minimum signal strength, the unbiasedness property

allows us to remove the second term in inequality (18)

and obtain a faster oracle rate (19b). As described

in greater detail in the corollaries below, we may show that the

right-hand expression in inequality (19b) is bounded

by , with high

probability, provided the spectrum of is bounded appropriately.

3.2 Ordinary least squares linear regression

Our first application focuses on the setting of ordinary least squares, together with the nonconvex regularizers introduced in Section 2.2: SCAD, MCP, and LSP. We compare the consequences of Theorems 1 and 2 for each of these regularizers with the corresponding results for the convex -penalty. Our theory demonstrates a clear advantage of using nonconvex regularizers such as SCAD and MCP that are -amenable; whereas support recovery based on -based methods is known to require fairly stringent incoherence conditions, our corollaries show that methods based on nonconvex regularizers will guarantee support recovery even in the absence of incoherence conditions.

The -regularized form of least squares regression may be written in the form

| (20) |

Note that the Hessian of the loss function is given by . While the sample

covariance matrix is always positive semidefinite, it has rank at most

. Hence, in high-dimensional settings where , the Hessian of

the loss function has at least zero eigenvalues, implying that

any nonconvex regularizer makes the overall

program (20) nonconvex.

In analyzing the family of estimators (20), we assume throughout that , for a sufficiently large constant . By known information-theoretic results [39], this type of lower bound is required for any method to recover the support of a -sparse signal, hence is not a limiting restriction. With this setup, we have the following result, proved in Appendix D.1:

Corollary 1.

Suppose and are sub-Gaussian, and regularization parameters are chosen such that and , for some constants and . Also suppose the sample covariance matrix satisfies the condition

| (21) |

-

(a)

Suppose is -amenable, with , and also satisfies the incoherence condition

(22) Then with probability at least , the nonconvex objective (20) has a unique stationary point (corresponding to the global optimum). Furthermore, , and

(23) -

(b)

Suppose the regularizer is -amenable, with . Also suppose

Then with probability at least , the nonconvex objective (20) has a unique stationary point given by the oracle estimator , and

(24)

Note that if we also have the beta-min condition in part (a), then is still a sign-consistent estimate of

; however, the guaranteed bound (23) is looser than the oracle bound (24) derived in part (b).

The proof of Corollary 1 is provided in Appendix D.1. Here, we make some comments about its consequences. Regularizers satisfying the conditions of part (b) include the SCAD and MCP penalties. Recall that for the SCAD penalty, we have ; and for the MCP, we have . Hence, the lower-eigenvalue condition translates into and , respectively. The LSP penalty is an example of a regularizer that satisfies the conditions of part (a), but not part (b): with this choice, we have , so the condition is satisfied asymptotically whenever is bounded below by a constant. A version of part (a) also holds for the -penalty, as shown in past work [40].

A valuable consequence of Corollary 1 is that it establishes conditions under which stationary points are unique and variable selection consistency holds, when using certain nonconvex regularizers. The distinguishing point between parts (a) and (b) of the corollary is that using -amenable regularizers allow us to do away with an incoherence assumption (22) and guarantee that the unique stationary point is in fact equal to the oracle estimator.

Furthermore, a great deal of past work on nonconvex regularizers [11, 44, 42, 43] has focused on the ordinary least squares regression objective (20); hence, it is instructive to interpret the results of Corollary 1 in light of this existing work. Zhang [42] shows that the two-step MC+ estimator (beginning with a global optimum of the program (20) with the MCP regularizer) is guaranteed to be consistent for variable selection, under only a sparse eigenvalue assumption on the design matrix. Our result shows that the global optimum obtained in the MCP step is actually already guaranteed to be consistent for variable selection, provided we have only slightly stronger assumptions about lower- and upper-eigenvalue bounds on the design matrix. In another related paper, Wainwright [39] establishes necessary conditions for support recovery in a linear regression setting when the covariates are drawn from a Gaussian distribution. As remarked in that paper, the necessary conditions only require eigenvalue bounds on the design matrix, in contrast to the more stringent incoherence conditions appearing in necessary and sufficient conditions for the success of the Lasso [40, 45]. Using standard matrix concentration results for sub-Gaussian variables, it may be shown that the inequalities (21) and (22) hold, with high probability, when the population-level bounds are satisfied:

| (25) |

However, the second inequality (25) is a fairly strong assumption on the covariance matrix , and as we explore in the simulations of Section 4 below, simple covariance matrices such as the class (43) defined in Section 4.2 fail to satisfy the latter condition. Hence, Corollary 1 shows clear advantage of using the SCAD or MCP regularizers over the -penalty or LSP when is not incoherent.

3.3 Linear regression with corrupted covariates

We now shift our focus to an application where the loss function

itself is nonconvex. In particular, we analyze the situation when the

general loss function is defined according to

equation (9). To simplify our discussion, we only

state an explicit corollary for the case when is the

convex -penalty; the most general case, involving a nonconvex

quadratic form and a nonconvex regularizer, is simply a hybrid of the

analysis below and the arguments of the previous section. Our goal is

to illustrate the applicability of the primal-dual witness technique

for nonconvex loss functions.

Let us recall the problem of linear regression with corrupted covariates, as previously introduced in Section 2.3. The pairs are drawn according to the standard linear model . While the response vector is assumed to be observed, suppose we observe only the corrupted versions of the covariates. Based on the observed variables , we may then compute the quantities

| (26) |

and estimate based on the following nonconvex program:

| (27) |

Also suppose and , for a sufficiently large constant .

Corollary 2.

Suppose are sub-Gaussian, , and are chosen such that and . If in addition,

and

| (28) |

then with probability at least , the nonconvex objective (27) has a unique stationary point (corresponding to the global optimum) such that , and

| (29) |

Note that if in addition, we have a lower bound of the form

, then we are guaranteed

that is sign-consistent for .

Corollary 2 may be understood as an extension of part (a) of Corollary 1: it shows how the primal-dual witness technique may be used even in a setting where the loss function is nonconvex. Under the same incoherence assumption (28) and the familiar sample size scaling of the usual Lasso, stationary points of the modified (nonconvex) Lasso program (27) are also support-recovery consistent. Corollary 2 also implies the rather surprising result that, although the objective (27) is indeed nonconvex whenever and , it nonetheless has a unique stationary point that is in fact equal to the global optimum. This result further clarifies the simulation results appearing in Loh and Wainwright [19]. Indeed, those simulations are performed with the setting , so the incoherence condition (28) holds, with high probability, with close to 0. A careful inspection of the plots in Figure 2 of Loh and Wainwright [19] confirms the theoretical conclusion of Corollary 2; more detailed simulations for non-identity assignments of appear in Section 4 below. The proof of Corollary 2 is provided in Appendix D.2.

3.4 Generalized linear models

To further illustrate the power of nonconvex regularizers, we now move to the case where the loss function is the negative log likelihood of a generalized linear model. We show that the incoherence condition may again be removed if the regularizer is -amenable (as is the case for the SCAD and MCP regularizers).

For drawn from a GLM distribution (10), we take and construct the composite objective

| (30) |

We impose the following conditions on the covariates and the link function:

Assumption 1.

-

(i)

The covariates are uniformly bounded as , for all .

-

(ii)

There are positive constants and , such that and .

The conditions of Assumption 1, although somewhat stringent, are nonetheless satisfied in various settings of interest. In particular, for logistic regression, we have , so

and we may verify that the boundedness conditions in Assumption 1(ii) are satisfied with and . Also note that the uniform bound on is used implicitly in the proof for support recovery consistency in the logistic regression analysis of Ravikumar et al. [31], whereas the uniform bound on also appears in the conditions for - and -consistency in other past work [25, 20]. The uniform boundedness condition in Assumption 1(i) is somewhat less desirable: although it always holds for categorical data, it does not hold for Gaussian covariates. We suspect that is possible to relax this constraint, but since our main goal is to illustrate the more general theory, we keep it here. In what follows, let denote the Fisher information matrix.

Corollary 3.

It is worthwhile to compare Corollary 3 with the analysis of -regularized logistic regression given in Ravikumar et al. [31] (see Theorem 1 in their paper). Both results require that the sample size is lower-bounded as , but Ravikumar et al. [31] also require to satisfy the incoherence condition

| (32) |

As noted in their paper and by other authors, the incoherence condition (32) is difficult to interpret and verify for general GLMs. In contrast, Corollary 3 shows that by using a properly chosen nonconvex regularizer, this incoherence requirement may be removed entirely. In addition, Corollary 3 is attractive in its generality, since it applies to more than just the logistic case with an -penalty and extends to various nonconvex problems where the uniqueness of stationary points is not evident a priori. The proof of Corollary 3 is contained in Appendix D.3.

3.5 Graphical Lasso

Finally, we discuss the consequences of our theorems for the graphical Lasso, as previously described in Section 2.3. Recall that for the graphical Lasso, the observations consist of a collection of -dimensional vectors, and the goal is to recover the support of the inverse covariance matrix . The analysis here is different and more subtle, because we seek a high-dimensional result in which the sample size scales only with the row sparsity of the inverse covariance matrix, as opposed to the total number of of nonzero parameters (which grows linearly with the matrix dimension, for any connected graph).

In order to prove such a result, we consider the constrained estimator

| (33) |

where denotes the convex cone of symmetric, strictly positive definite matrices, and we impose the spectral norm bound on the estimate.333We denote the constraint radius by rather than , in order to emphasize the difference from previous situations.

A more standard choice would be to use the -norm bound as the side-constraint, as done in our past work on Frobenius norm bounds for the graphical Lasso with nonconvex regularizers [20]. However, as we will show here, the formulation (33) actually leads to variable selection consistency results under the milder scaling , rather than the scaling obtained in our analysis on Frobenius norm bounds [20]. Here, we use to denote the maximum number of nonzeros in any row/column of , and to denote the total number of nonzero entries.

A few remarks are in order. First, when is the convex -penalty and , the program (33) is identical to the standard graphical Lasso (e.g., [9, 32, 15, 33]). However, since we are interested in scenarios where is allowed to be nonconvex, we include an additional spectral norm constraint governed by . As a technical comment, note that our original assumptions required to be an open subset of . In the analysis to follow, we handle the symmetry constraint by treating the program (33) as an optimization problem over the space , and then take to be the open subset of corresponding to positive definite matrices. Doing so makes the program (33) consistent with the framework laid out earlier in our paper. In this case, the oracle estimator is defined by

| (34) |

With this setup, we have the following guarantee:

Corollary 4.

Given a sample size , suppose the ’s are drawn from a sub-Gaussian distribution, and the regularizer is -amenable. Also suppose that

Then with probability at least , the program (33) with has a unique stationary point given by the oracle estimator , and

| (35) |

Moreover, as shown in the proof in Appendix D.4, the support containment condition and elementwise bound (35) also imply bounds on the Frobenius and spectral norms of the error, namely

| (36) |

We reiterate that Corollary 4 does not involve any restrictive incoherence assumptions on the matrix . As remarked in past work [22, 32], such incoherence conditions for the graphical Lasso are very restrictive—much more so than the corresponding incoherence conditions for graph recovery using neighborhood regression [23, 45, 40]. Thus, in this setting, our corollary illustrates another distinct advantage of nonconvex regularization.

4 Simulations

In this section, we report the results of various simulations that we ran in order to verify our theoretical results.

4.1 Optimization algorithm

We begin by describing the algorithm we use to optimize the program (1). We rewrite the program as

| (37) |

and apply the composite gradient descent algorithm due to Nesterov [26]. The updates of the composite gradient procedure are given by

| (38) |

where is the stepsize.

In the particular simulations of this section, we take . Then the iterates (38) have the convenient closed-form expression

| (39) |

The following proposition guarantees the computational efficiency of the general composite gradient descent algorithm (38). For ease of analysis, we assume that , and the Taylor error satisfies the following restricted strong convexity condition, for all :

| (40a) | |||||

| (40b) |

as well as the restricted smoothness condition

| (41) |

We also assume for simplicity that is convex, as is the case for all the regularizers studied in this paper.

In the following statement, we let be the unique global optimum of the program (37). Also denote .

Proposition 1.

Suppose satisfies the RSC (40b) and RSM (41) conditions, and assume the regularizer is -amenable with , and is convex. Let the scalars be chosen to satisfy the bounds and . Then for any stepsize parameter and tolerance , the iterates of the composite gradient descent algorithm (38) satisfy the -bound

where .

We sketch the proof of Proposition 1 in Appendix E.1. It establishes that the composite gradient descent algorithm (38) converges geometrically up to tolerance ; moreover, only iterations are necessary.

Since we are interested in -error bounds, we state a simple corollary to Proposition 1 that ensures convergence of the iterates in -norm, up to accuracy , assuming statistical consistency of the global optimum and the scaling :

Corollary 5.

Suppose, in addition to the assumptions of the previous proposition, that , and the sample size is lower-bounded as . Then the iterates of the composite gradient descent algorithm (38) satisfy the -bound

| (42) |

The proof of Corollary 5 is a simple consequence of Proposition 1 and is supplied in Appendix E.2. Note that the bound holds, with high probability, as a consequence of Lemma 9 in Appendix F.2. Corollary 5 has a natural consequence for support recovery: Suppose the estimate satisfies an -bound of the form , as guaranteed by Theorem 2. Combining the -bound (42) on iterate with the triangle inequality, we are then guaranteed that

so the composite gradient descent algorithm converges to a vector with the correct support, provided .

4.2 Classes of matrices

Next, we describe two classes of matrices to be used in our simulations. The first class consists of matrices that do not satisfy the incoherence conditions, although the maximum and minimum eigenvalues are bounded by constants. We define

| (43) |

Hence, is a matrix with 1’s on the diagonal, ’s in the first positions of the row and column, and 0’s everywhere else. The following lemma, proved in Appendix E.3, provides the incoherence parameter and eigenvalue bounds for as a function of :

Lemma 1.

With the shorthand notation and , the incoherence parameter is given by , and the minimum and maximum eigenvalues are given by and .

In particular, if , Lemma 1 ensures that

has bounded eigenvalues but does not satisfy the

incoherence condition.

The second class of matrices is known as the spiked identity model [17] or constant correlation model [45]. We define the class according to

| (44) |

where and denotes the all ’s vector. An easy calcuation shows that and , whereas the incoherence parameter is given by (see Corollary 1 of the paper [45]).

4.3 Experimental results

We ran experiments with the loss function coming from (a) ordinary

least squares linear regression, (b) least squares linear regression

with corrupted covariates, and (c) logistic regression. For all our

simulations, we used the regularization parameters and , and we set

the SCAD and MCP parameters to be and ,

respectively. Note that although the covariates in our simulations for

logistic regression do not satisfy the boundedness

Assumption 1(i) imposed in our corollary, the generated plots

still agree qualitatively with our predicted theoretical results.

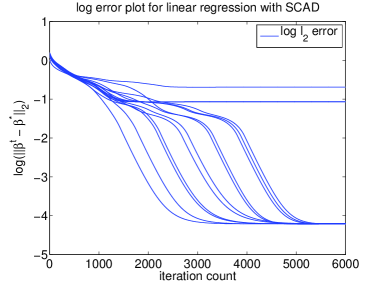

In our first set of simulations, we show that using the SCAD or MCP

regularizer in situations where the design matrix does not satisfy

incoherence conditions still results in an estimator that is variable

selection consistent. We generated i.i.d. covariates , where was obtained from the

family of non-incoherent matrices (43), with . We chose and , the unit vector with the first components equal to

, and generated response variables according to

the linear model , where

. In addition, we generated corrupted

covariates , where , and . We then ran the composite gradient descent algorithm

with updates given by equation (39), where the loss

function is given by equation (9), and are defined as in

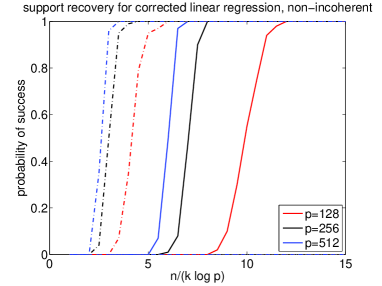

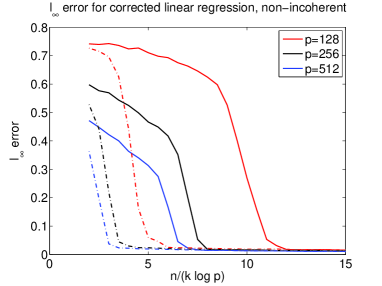

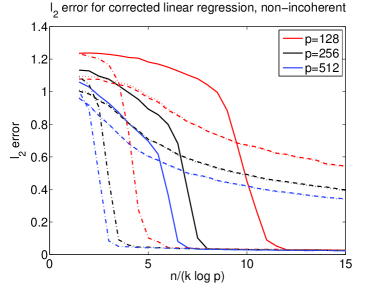

equation (26). Figure 1 shows the

results of our simulations for the problem sizes , and

. In panel (a), we see that the probability of correct support

recovery transitions sharply from 0 to 1 as the sample size increases

and is the SCAD or MCP regularizer. In contrast, the probability

of recovering the correct support remains at 0 when is

the -penalty or LSP—by the structure of ,

regularization with the -penalty or LSP results in an

estimator that puts nonzero weight on the

coordinate, as well. Note that we have rescaled the horizontal axis

according to in order to match the scaling prescribed by

our theory; the three sets of curves for each regularizer roughly

align, as predicted by Theorem 1. Panel (b)

confirms that the -error decreases to 0 when using the SCAD and MCP, as predicted by

Theorem 2. Finally, we plot the -error

of the SCAD and MCP regularizers

alongside the -error for the -penalty and LSP in panel

(c). Although the -error is noticeably smaller for SCAD and

MCP than for the -penalty and LSP, as noted by previous

authors [11, 4, 21], all four regularizers are

nonetheless consistent in -error, since a lower-eigenvalue

bound on the covariance matrix of the design is sufficient for

-consistency [20]. For our choice of regularization

parameters, where the same value of is shared between the

-penalty and LSP, the two sets of curves for the

-penalty and LSP nearly agree; as shown in Candes et

al. [6], the relative improvement of the LSP in

comparison to the -penalty may vary widely depending on the

regularization parameter.

|

|

| (a) | (b) |

|

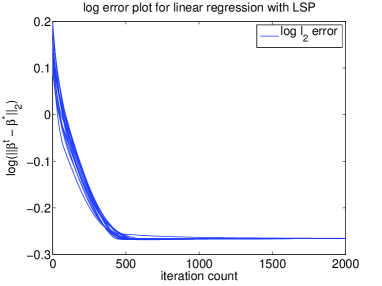

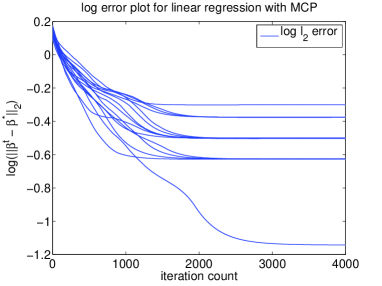

In our second set of simulations, we explore the uniqueness of stationary points of the composite objectives. We focus on settings where the loss function comes from either linear regression with ordinary least squares, or logistic regression. Our theory guarantees that stationary points are unique when , but when , multiple stationary points may emerge. In fact, when , convergence of the composite gradient descent algorithm and consistent support recovery are no longer guaranteed. In practice, we observe that multiple initializations of the composite gradient descent algorithm still appear to converge to a single stationary point with the correct support, when is slightly larger than ; however, when that condition is violated more severely, the composite gradient descent algorithm indeed terminates at several distinct stationary points. Figure 2 shows the result of multiple runs of the composite gradient descent algorithm with different regularizers in the cleanly-observed linear regression setting. We generated observations , with coming from the family of spiked identity models (44), for and , and independent additive noise, . We set the problem dimensions to be , , and , and generated to have nonzero values with equal probability for each sign. When using the SCAD or MCP regularizers (panels (b) and (d)), distinct stationary points emerge and the recovered support is incorrect, since . In contrast, the -penalty and LSP still continue to produce unique stationary points with the correct support (panels (a) and (b)). Observe from the plots in Figure 2 that the error decreases at a rate that is linear on a log scale, as predicted by Theorem 3 of Loh and Wainwright [20], until it reaches the threshold of statistical accuracy. Further note the significant increase in overall precision from using SCAD or MCP, as seen by comparing the vertical axes in panels (a) & (b) and panels (c) & (d).

|

|

| (a) | (b) |

|

|

| (c) | (d) |

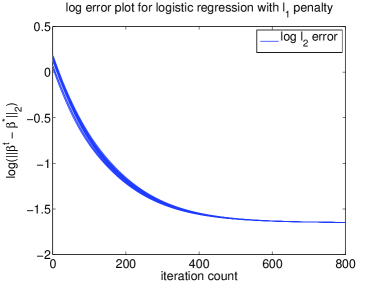

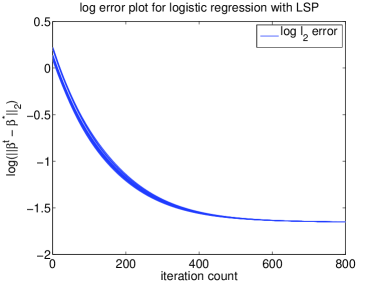

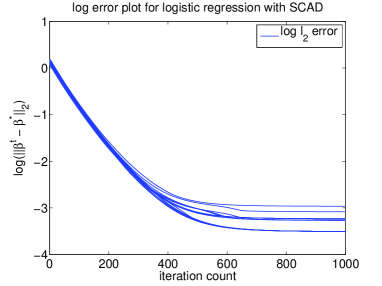

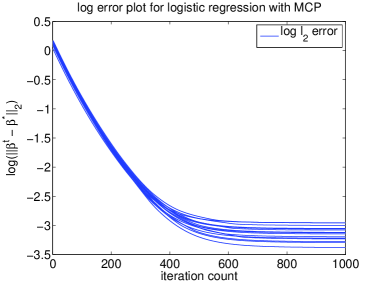

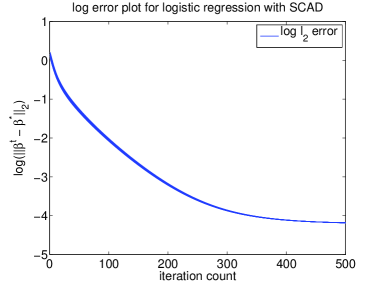

Finally, we present a third set of simulations, analogous to the second, with the OLS loss function replaced by the maximum likelihood loss function for logistic regression:

We generated , with , and set the problem dimensions to be , , and . We generated to have nonzero values with equal probability for each sign, and generated response variables according to

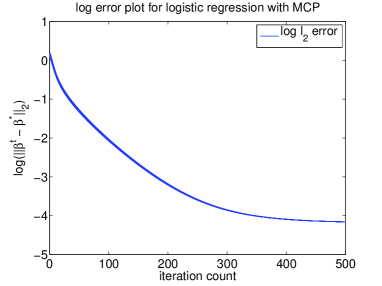

Figure 3 shows the results of our simulations. Panels (a)–(d) plot the log -error as a function of iteration number, when . Note that in this case, an empirical evaluation shows that , so we expect and . As in the plots of Figure 2, multiple stationary points emerge in panels (c) and (d) when is the SCAD or MCP regularizer; in contrast, we see from panels (a) and (b) that all 15 runs of composite gradient descent converge to the same stationary point when is the -penalty or LSP. In panels (e) and (f), we repeat the simulations with . In this case, , and we see from our plots that although the condition is still violated, the larger value of is enough to make the stationary points under SCAD or MCP regularization unique. We may again observe the geometric rate of convergence of the -error in each plot, up to a certain small threshold. The improved performance from using the SCAD and MCP regularizers may be observed empirically by comparing the vertical axes in the panels of Figure 3.

|

|

| (a) | (b) |

|

|

| (c) | (d) |

|

|

| (e) | (f) |

5 Discussion

We have developed an extended framework for analyzing a variety of nonconvex problems via the primal-dual witness proof technique. Our results apply to composite optimization programs where both the loss and regularizer function are allowed to be nonconvex, and our analysis significantly generalizes the machinery previously established to study convex objective functions. As a consequence, we have provided a powerful reason for using nonconvex regularizers such as the SCAD and MCP rather than the convex -penalty: In addition to being consistent in -error, the nonconvex regularizers actually produce an overall estimator that is consistent for support recovery when the design matrix is non-incoherent and the usual -regularized program fails in recovering the correct support. We have also established a similar strong result for the graphical Lasso objective function with nonconvex regularizers, which eliminates the need for complicated incoherence conditions on the inverse covariance matrix.

Future directions of research include devising theoretical guarantees when the condition is only mildly violated, since the condition does not appear to be strictly necessary based on our simulations, and establishing a rigorous justification for why the SCAD and MCP regularizers perform appreciably better than the -penalty even in terms of -error, in situations where the assumptions are not strong enough for an oracle result to apply. It is also an open question as to how generally the restricted strong convexity condition may hold for various other nonconvex loss functions of interest, or whether a local RSC condition is sufficient to guarantee good behavior with proper initializations of a gradient descent algorithm. Finally, it would be useful to be able to compute the RSC constants empirically from data, so as to assign a nonconvex regularizer with the proper amount of curvature.

Acknowledgments

The work of PL was partly supported from a Hertz Foundation Fellowship, an NSF Graduate Research Fellowship and a PD Fellowship while studying at Berkeley. MJW and PL were also partially supported by grants NSF grant DMS-1107000, NSF grant CIF-31712-23800, and Air Force Office of Scientific Research Grant AFOSR-FA9550-14-1-0016.

Appendix A Proof of Theorem 1

In this Appendix, we provide the proof of Theorem 1. We begin with the main body of the argument, with the proofs of some more technical lemmas deferred to later subsections.

A.1 Main part of proof

We follow the outline of the primal-dual witness construction described in Section 2.4. For step (i) of the construction, we use Lemma 9 in Appendix F, where we simply replace by and by , which is the function restricted to . It follows that as long as , we are guaranteed that , whence

Here, the final inequality follows by the lower bound in inequality (15b). We conclude that must be in the interior of the feasible region.

Moving to step (ii) of the PDW construction, we define the shifted objective function . Since is an interior point, it must be a zero-subgradient point for the restricted program (13), so , where is the dual vector. By the chain rule, this implies that , where . Accordingly, we may define the subvector such that

| (45) |

where is the extended subgradient. Under the assumption (16), this completes step (ii) of the construction.

For step (iii), we first establish that is a local minimum for the program (1) by verifying the sufficient conditions of Lemma 10 in Appendix F, with , , and . Note that Lemma 8(b) from Appendix F.1 ensures the concavity and differentiability of . Since , condition (100a) is trivially satisfied. Furthermore, condition (100b) holds by equation (45). Hence, it remains to verify the condition (100c).

We first show that . Supposing the contrary, consider a vector such that . Fixing some index such that , by the definition of , we have

| (46) |

However, if denotes the vector with entry replaced by , we clearly still have , but

where the strict inequality holds because ,

by our assumption. We have thus obtained a contradiction to

equation (46); consequently, our initial assumption was

false, and we may conclude that .

The following lemma, proved Appendix A.2, guarantees that a shifted form of the loss function is strictly convex over an -dimensional subspace:

Lemma 2.

Consider any -RSC loss function and -amenable regularizer , with . If , the function is strictly convex on , and the restricted program (13) is also strictly convex.

In particular, since and , Lemma 2 immediately implies

condition (100c) of Lemma 10. We

conclude that is indeed a local minimum of the

program (1).

The following lemma, proved in Appendix A.3, show that all stationary points of the program (1) are supported on :

Lemma 3.

Turning to the uniqueness assertion, note that since all stationary points are supported in , any stationary point of the program (1) must satisfy , where is a stationary point of the restricted program (13). By Lemma 2, the restricted program is strictly convex. Hence, the vector , and consequently also , is unique.

A.2 Proof of Lemma 2

We begin by establishing the bound , for all . Equivalently,

| (47) |

When this lower bound holds, we are guaranteed that

so is strictly convex on under the prescribed sample size.

In order to prove the bound (47), consider a fixed such that and . For this vector, we have , so

| (48) |

Furthermore, by the RSC assumption (8b) and the fact that , we have

| (49) |

Since , we also have . Combining this bound with equations (48) and (49) then gives the desired inequality (47).

Finally, we note the decomposition , showing that is the sum of a strictly convex and convex function over . Hence, is strictly convex, as claimed. The strict convexity of over follows immediately.

A.3 Proof of Lemma 3

Let . We first show that . Suppose on the contrary that . By inequality (8b), we have . Moreover, since is feasible, the first-order optimality condition gives

| (50) |

Summing the two preceding inequalities yields

| (51) |

Since is an interior local minimum, we have . Hence, inequality (51) implies that

where the bound holds by Lemma 8 in Appendix F.1. Rearranging, we then have

Since and by assumption, this implies that , as claimed.

Now, applying the RSC condition (8b), we have

which implies that

| (52) |

By inequality (50), we also have

| (53) |

where . From the zero-subgradient condition (14), we have . Combining with inequality (53) then yields

| (54) |

Rearranging, we have

| (55) |

where the second inequality comes from the fact that , and the third inequality comes from the bound (52). Finally, we need a lemma showing that lies in a cone set:

Lemma 4.

If for some and , then

Proof.

From inequality (54) together with the RSC bound (52), we have

| (56a) | ||||

| Note that since , we have | ||||

| (56b) | ||||

| Furthermore, we have | ||||

| (56c) | ||||

Combining inequalities (56a), (56b), and (56) then yields

| (57) |

Under the assumption on , we have , so that inequality (57) implies

Putting together the pieces, we then have

which establishes the claim. ∎

Appendix B Proof of Theorem 2

Note that by the fundamental theorem of calculus, satisfies

By the zero-subgradient condition (14) and the invertibility of , we then have

implying that

| (58) |

Lemma 8 in Appendix F.1 guarantees that , so

which is inequality (18).

To establish inequality (19b), we use the following lemma:

Lemma 5.

Suppose is -amenable, and the bound (19a) holds. Then for all , and in particular, .

Proof.

Lemma 5 implies that . Hence, the zero-subgradient condition (14) reduces to . Since is strictly convex on by Lemma 2, this zero-gradient condition implies that is the unique global minimum of , so we have the equalities and , as claimed. Finally, inequality (58) simplifies to inequality (19b), using the equality .

Appendix C Establishing strict dual feasibility

In this Appendix, we derive conditions that allow us to establish the strict dual feasibility conditions required in order to apply Theorem 1. We use these derivations to prove Corollaries 1–3.

By the zero-subgradient condition (14), we have

Defining , we then have

In block form, this means

| (59) |

By simple algebraic manipulations, we then have

| (60) |

Note that by the selection property (vi), we have , so the first term in equation (60) vanishes, giving

| (61) |

If the unbiasedness property (vii) also holds, we have the following result:

Proposition 2.

However, for regularizers that do not satisfy the unbiasedness property (vii), such as the LSP and the usual -norm, we impose slightly stronger conditions to ensure strict dual feasibility. The notion of an incoherence condition is taken from the Lasso literature [45, 40, 24]:

Assumption 2.

There exists such that , where denotes the -operator norm.

Based on this condition, we have the following result:

Proposition 3.

Proof.

Appendix D Proofs of corollaries in Section 3

In this section, we provide detailed proofs of the corollaries to Theorems 1 and 2 appearing in Section 3.

D.1 Proof of Corollary 1

As established in Corollary 1 of our previous work [20], the RSC condition (8b) holds w.h.p. with and , under sub-Gaussian assumptions on the variables.

D.1.1 Proof of part (a)

We now use the machinery developed in Appendix C. We use a slightly more direct analysis than the result stated in Proposition 3, which allows us to produce tighter bounds. Denoting , we have

| (64) |

so equation (61) takes the form

| (65) |

using the fact that , by Lemma 8. We now write

| (66) |

where is an orthogonal projection matrix. Note that for , we have

since is a sub-Gaussian vector with parameter , and is a projection matrix. Taking another expectation, we have

so is sub-Gaussian with parameter . Using sub-Gaussian tail bounds and a union bound, we conclude from equation (D.1.1) that

with probability at least , provided . Hence, strict dual feasibility holds, w.h.p., provided , and the variable selection consistency property follows by Theorem 1.

Turning to -bounds, we have

For , we may write . Furthermore,

with probability at least . Conditioned on , the variables are sub-Gaussian with parameter . Denoting

and applying a union bound, we then have

so

as well. We conclude that

and

with probability at least . Combining this with the assumption (21), we conclude by part (a) of Theorem 2 that the desired -bound holds.

D.1.2 Proof of part (b)

The proof of this corollary is nearly identical to the proof of part (a), except that equation (D.1.1) does not have the extra term ; by the assumption of -amenability, Lemma 5 implies that . Hence, equation (61) takes the form

Observe that the matrix concentration arguments from the proof of part (a) also imply that , w.h.p. The remainder of the proof follows by part (b) of Theorem 2.

D.2 Proof of Corollary 2

The expressions for and are as in equation (64), with defined in equation (26). Furthermore, as remarked in the proof of Corollary 1, Corollary 1 of our previous work [20] implies that the RSC condition (8b) holds w.h.p., when and .

We may verify using standard techniques that when the ’s and ’s are sub-Gaussian and , we have the bound , with probability at least [19]. Hence, if , the lower bound in inequality (15a) is satisfied w.h.p. We may then check that for the choice of regularization parameters and , and under the scaling , both bounds in condition (15a) hold.

We now use Proposition 3 to verify condition (a) in Theorem 1, establishing strict dual feasibility (16). From the bound (63b), and with the scaling , it suffices to show that

| (67) |

w.h.p. To this end, we have the following proposition, which we state in some generality to indicate its applicability to other types of corrupted linear models [19]:

Proposition 4.

Suppose satisfies the deviation bound

| (68) |

Also suppose satisfies the deviation bound

| (69) |

and suppose and are uniformly bounded. Under the scaling and , inequality (67) holds, with probability at least .

Proof.

First note that inequality (68) implies the following deviation bounds:

| (70a) | ||||

| (70b) | ||||

| (70c) | ||||

Inequality (70a) follows from from a discretization argument over the -ball in , and inequality (70b) is similar. Inequality (70c) follows by taking and a union bound over . Furthermore, by Lemma 11, inequality (70a) implies that

| (71) |

as well.

Note that by inequalities (70c) and (69), we have

| (72) |

with probability at least . Furthermore, the triangle inequality gives

| (73) |

and the first term is bounded above by , by inequality (72). For the second term, we write

| (74) |

where we have again used inequality (72) in the second inequality. Furthermore,

| (75) |

The terms in inequality (75) are bounded as

Combining the bounds with inequalities (70b) and (71), we conclude from inequality (75) that

| (76) |

with probability at least , under the scaling . Plugging inequality (76) into inequality (D.2) and combining with inequality (72), we conclude that

with probability at least . The desired result then follows under the scaling . ∎

It is easy to check that the bounds (68) and (69) hold when are defined by equation (26) and , and are sub-Gaussian. Hence, strict dual feasibility holds by Propositions 3 and 4, and the PDW technique succeeds.

Turning to -bounds, note that

We have the following result:

Proposition 5.

D.3 Proof of Corollary 3

Note that Corollary 2 of our previous work [20] establishes the RSC condition (8b) when is bounded and the ’s are again sub-Gaussian. We again proceed via the framework and terminology of Appendix C, particularly Proposition 2. Taking derivatives of the loss function (11), we have

To verify inequality (62a), we may use straightforward sub-Gaussian concentration techniques (cf. the proof of Corollary 2 in Loh and Wainwright [20]). For inequality (62b), note that

by the mean value theorem, where lies on the line segment between and .

For each pair , we write

| (78) |

where denotes the vector restricted to . Inequality (D.3) follows by two applications of the Cauchy-Schwarz inequality and the fact that . Furthermore, by Lemma 9 in Appendix F, we have

with probability at least . By Assumption 1(i), we also have . Hence, inequality (D.3) becomes

In particular, taking a supremum over unit vectors , we have

| (79) |

with probability at least , where the second inequality holds by a standard spectral norm bound on the sample covariance matrix.

Furthermore, for , the expression is an i.i.d. average of a product of sub-Gaussian random variables and , since the ’s are sub-Gaussian and is uniformly bounded by assumption. Defining , a standard discretization argument of -dimensional unit sphere yields

| (80) |

with probability at least . Hence, by inequalities (D.3) and (80), we have . Applying Lemma 11 in Appendix F yields

| (81) |

as well. A similar argument shows that

and

with probability at least . Putting together the pieces, we find that

| (82) |

with high probability. Returning to the expression (62b), we have the bound

where , and

| (83) |

Since the eigenspectrum of is bounded by assumption, standard techniques (cf. the proofs of Corollary 2 in Loh and Wainwright [20] and Lemma 6 in Negahban et al. [25]) guarantee that , with probability at least . Turning to the second term, we have

| (84) |

Now,

| (85) |

and by the triangle inequality,

| (86) |

where

By the bounds (81) and (82), we have

w.h.p., so combined with inequalities (84), (85), and (86), we have

Hence, by Proposition 2, strict dual feasibility holds under the scaling .

D.4 Proof of Corollary 4

In this section, we provide the proof of Corollary 4. Corollary 3 of our previous work [20] establishes the RSC condition (8b), with and scaling as and . Our proof strategy deviates mildly from the framework described in Section 2.4, in that we provide a slightly different way of constructing a matrix such that and is a zero-subgradient point of the restricted program (13). However, subject to this minor adjustment, the remainder of the primal-dual witness technique proceeds as before.

We begin with a simple lemma establishing the convexity of the program (33):

Lemma 6.

Suppose is -amenable. Then for the choice of parameter , the objective function in the program (33) is strictly convex over the constraint set.

Proof.

A simple calculation shows that for the graphical Lasso loss

we have . Note that is a deterministic quantity that does not depend on . Hence,

We see that for , we have , so is convex. Further note that by assumption, the quantity is also convex. Hence, the overall objective function is strictly convex over the feasible set, as claimed. ∎

In particular, if there exists a zero-subgradient point of the composite objective function within the feasible set, it must be the unique global minimum. Our strategy is to construct such a zero-subgradient point. Let denote the support of , where we remove redundant elements. We define the map according to

where is the symmetric matrix agreeing with on and having 0’s elsewhere, and . We analyze the behavior of over the -ball of radius to be specified later. In particular, note that for , we have

| (87) |

since has at most nonzero entries per row. Hence, when , we are guaranteed that the matrix is invertible, making a continuous map. We show that , so by Brouwer’s fixed point theorem [28], the function must have a fixed point, which we denote by . Defining the constants and , this insight is summarized in the following lemma:

Lemma 7.

Let , where is a constant depending only on the sub-Gaussian parameter of the ’s. Suppose

| (88) |

and suppose the sample size satisfies . Then with probability at least , there exists such that

| (89) |

Furthermore, if is -amenable and , we have , for all .

Proof.

We first establish that . Consider . We have

implying that

| (90) |

For the first term, we have

| (91) |

w.h.p., by the sub-Gaussian assumption on the ’s. Furthermore, by the matrix expansion

| (92) |

we have

By the triangle inequality, we then have

| (93) |

By Hölder’s inequality, we have

Using inequality (87) and plugging back into inequality (93), we then have

| (94) |

where the last inequality follows from our assumption (88). Combining inequalities (D.4), (91), and (94), and using the assumption that , we find that , as desired. Applying Brouwer’s fixed point theorem then yields the required fixed point . Defining , the third equality in line (89) follows. The operator norm bound in inequality (89) follows from the same argument as in inequality (87). Finally, by the triangle inequality and the assumption that is -amenable, we have . ∎

Equipped with Lemma 7, we now prove that is the (unique) global optimum of the program (33). Note that it suffices to show that is a zero-subgradient point of the objective function in the program (33); since the objective is strictly convex by Lemma 6, must be the global minimum. The same manipulations used in Appendix C and Proposition 2 reveal that is a zero-subgradient point satisfying dual feasibility, if inequalities (62a) and (62b) hold. In fact, we may take , since the convexity of the problem immediately implies uniqueness of a stationary point if it exists. We treat as a matrix operating on the -dimensional vector . For the graphical Lasso, we have , so we need to show that . It is straightforward to see that by the sub-Gaussianity of the ’s, setting for a suitably large constant is sufficient to satisfy inequality (62a).

Turning to inequality (62b), note that

Furthermore, for , we have

using Lemma 7. Lemma 11 in Appendix F then implies that

Hence, by Lemma 13 in Appendix F, we have

implying the bounds

and

Applying Lemma 11 in Appendix F yields

| (95) |

Next we define the pair according to

Note that we have , and moreover,

Combined with our earlier upper bound on , we conclude that , under the scaling .

Next, observe that

Hence, the primal-dual witness technique succeeds. Note that by inequality (95), we also have

By Theorem 2, we conclude that is the unique global minimum of the program (33) with the desired properties.

Finally, let us prove the claimed bounds on the Frobenius and spectral norms. Note that . Furthermore, since is a symmetric matrix, we also have

The bounds then follow from our earlier bound on the elementwise -norm.

Appendix E Proofs for Section 4

In this section, we provide details of proofs for the results in Section 4.

E.1 Proof of Proposition 1

This proof is a fairly straightforward modification of the proof of Theorem 3 in Loh and Wainwright [20], so we provide only a sketch of how the argument deviates from the proof supplied there.

The only substantial difference between the two settings is that rather than , and the side constraint is slightly tweaked. Nonetheless, we have , for all in the feasible region, which is the only property of the side constraint needed for the proofs of Loh and Wainwright [20]. Concerning the particular form of , we simply need to establish for the RSC relations that

| (96) |

still holds, where . Note that

| (97) |

By Lemma 8(b) in Appendix F.1, we have

implying that

| (98) |

Combining inequalities (97) and (98) yields the required inequality (96). Finally, note that by our assumption and equation (97), we have , so the RSM condition holds for with the same parameter . The remaining arguments proceed as before.

E.2 Proof of Corollary 5

We set in Proposition 1. Then

where the last inequality follows by the assumption of statistical consistency for . Under the scaling , the desired result follows.

E.3 Proof of Lemma 1

The computation of the incoherence parameter is straightforward. For the spectral properties, note that for any vector . Consequently, we have

We may write

where we have used the fact that . It is easy to see that the final expression is maximized when , so . Equality is achieved for the vector . The lower-eigenvalue bound follows by a similar argument, with equality achieved when .

Appendix F Some useful auxiliary results

Finally, we provide some useful auxiliary results, which we employ in

the proofs of our main theorems.

F.1 Properties of amenable regularizers

The following lemma is useful in various parts of our analysis. Part (a) is based on Lemma 4 of Loh and Wainwright [20].

Lemma 8.

Consider a -amenable regularizer . Then we have

-

(a)

, for all , and

-

(b)

The function is concave and everywhere differentiable.

Proof.

(a) Consider . By condition (iii), we have

. By conditions (iii) and (iv), we also

have . Putting

together the pieces, we find that . A similar argument holds when .

(b) If , we can write , which is concave since is convex, by condition (v). Similarly, is concave for . At , we have , by condition (vi). Then is a differentiable function with monotonically decreasing derivative, implying concavity of the function. ∎

F.2 Bounds on -errors of stationary points

The following result is taken from Loh and Wainwright [20]. It applies to any stationary point of the program , meaning a vector such that for all feasible .

F.3 Sufficient conditions for local minima

The following lemma is a minor extension of results from Fletcher and Watson [14]. It applies to functions and , such that is concave, for some .

Lemma 10.

Suppose is feasible for the program

| (99) |

and there exist , such that

| (100a) | ||||

| (100b) | ||||

| (100c) | ||||

where

Then is an isolated local minimum of the program (99).

Proof.

The proof of this lemma essentially follows the proof of Theorem 3 of Fletcher and Watson [14], except it allows for a composite function in the objective that is not in . Nonetheless, we include a full proof for clarty and completeness.

Suppose for the sake of contradiction that is not an isolated local minimum. Then there exists a sequence of feasible points with , where

Let ; then is a set of feasible directions. Since , the set must possess a point of accumulation , and we may extract a convergent subsequence. Relabeling the points as necessary, we assume that . We show that .

Since the feasible region is closed, is also a feasible direction at . In particular, if , we must have