The pilgrim process

Probability distributions on cladograms.

Advances in Statistical Modeling and Inference. Essays in honor of K. Doksum

Poisson Processes.

Gibbs fragmentation trees.

Abstract

Pilgrim’s monopoly is a probabilistic process giving rise to a non-negative sequence that is infinitely exchangeable, a natural model for time-to-event data. The one-dimensional marginal distributions are exponential. The rules are simple, the process is easy to generate sequentially, and a simple expression is available for both the joint density and the multivariate survivor function. There is a close connection with the Kaplan-Meier estimator of the survival distribution. Embedded within the process is an infinitely exchangeable ordered partition processes connected to Markov branching processes in neutral evolutionary theory. Some aspects of the process, such as the distribution of the number of blocks, can be investigated analytically and confirmed by simulation. By ignoring the order, the embedded process can be considered as an infinitely exchangeable partition process, shown to be closely related to the Chinese restaurant process. Further connection to the Indian buffet process is also provided. Thus we establish a previously unknown link between the well-known Kaplan-Meier estimator and the important Ewens sampling formula.

keywords:

and

1 Introduction

A fundamental principle underlying statistical modeling is that arbitrary choices such as sample size or observation labels should not affect the sense of a model and meaning of parameters. For example, a priori the labels assigned to observations (unit , , …) carry no meaning other than to distinguish among units. This guiding precept gives rise to the study of exchangeable distributions. Infinite exchangeability captures the idea that the data generating process should not be affected by arbitrary relabeling of the sample. Here we are concerned with infinitely exchangeable non-negative sequences , which arise in survival analysis where the observations are event times. Pilgrim’s monopoly is a sequential description of such a process. Restriction to the subsample yields . For and , the probability of equality can be non-negative, implying the number of unique times in the set may be less than . In this paper, we outline both existing and new theoretical results concerning the associated asymptotic behavior of the process. For example, the number of unique times grows asymptotically at a rate proportional to . An argument is given as to why the pilgrim’s monopoly is the most fitting model for applied work when such ties may be the result of numerical rounding.

Research on nonparametric Bayesian survival analysis has been based around the de Finnetti approach to constructing exchangeable survival processes by generating survival times conditionally independent and identically distributed given a completely independent hazard measure, i.e. the cumulative conditional hazard is a Lévy process (Cornfield and Detre, 1977; Kalbfleisch, 1978; Hjort, 1990; Clayton, 1991). Such processes are sometimes called neutral to the right (Doksum, 1974; James, 2006). Pilgrim’s monopoly corresponds to a particular choice of Lévy process and thus fits naturally within the existing literature. However, the probability density can be computed using the characteristic index, and the process can be simulated directly from the predictive distributions, allowing us to bypass the Lévy process entirely.

While connections to survival analysis were expected, we find that the pilgrim process provides a fundamental link among seemingly disparate areas of statistics. The connections arise due to the embedding of two processes within the pilgrim’s monopoly. First the ties of generate a partial ranking (or ordered partition) of the units. That is, generates a sequence of unique times for some . This induces a clustering of units by unique times (i.e. ). The partial ranking of the blocks is obtained by the ordering of the associated unique times. The embedded ordered partition process is infinitely exchangeable as it only depends on block order and block size.

The embedded ordered partitions are characterized by a splitting rule , which only depends on the total number individuals at risk leading up to the next failure time, , and the number of those who fail at that time, . An interesting connection to Markov branching models in neutral evolutionary theory is shown, in particular the family of beta-splitting models (Aldous, 1996). These contain several important models, namely the symmetric binary tree model, Yule model, and uniform model. We explain how the beta-splitting model corresponding to the pilgrim process may be most fitting in the study of phylogenetic trees.

Infinitely exchangeable partition processes are important in cluster analysis, serving as a natural prior for the partition of sampled units. More recently there has been interest in a generalization to feature allocation models (Broderick, Pitman, and Jordan, 2013). Each infinitely exchangeable process on non-negative sequences induces an infinitely exchangeable partition process by the relation if . We show how this induced partition process contains the well-known Chinese restaurant process. Moreover, a generalization of the pilgrim process to doubly indexed sequences is shown to be connected with the Indian buffet process.

1.1 Outline

The goal of this paper is to highlight existing and new results related to the pilgrim process. We establish a fundamental connection between this process and models in seemingly unrelated areas of statistics. In particular, we provide a previously unknown connection between the Kaplan-Meier estimator and the Ewens sampling formula.

We organize our discussion as follows. In Section 2, we provide a description of the pilgrim’s monopoly. In Section 3, we investigate the behavior of the process via simulation, providing some intuition to the key features. In Section 4, we summarize the known theoretical behavior of the process as well as establish several new results. In particular we argue that the pilgrim process is the natural choice for survival analysis as it is the unique subfamily of processes with weakly continuous predictive distributions. In Section 5, we review the connections with previous literature, in particular the study of neutral to the right processes used in Bayesian survival analysis and Markov branching models in the study of probability distributions on cladograms. In Section 6, we discuss extensions of the pilgrim process to a richer set of time-to-event models with various asymptotic behavior, as well as to the setting of recurrent events. In Section 7, we provide an explicit connection between the various processes and the Chinese restaurant process and Indian buffet process. The connection yields alternate methods for producing exchangeable random partition and feature allocation processes.

2 Pilgrim’s monopoly

Although not as simple as the Chinese restaurant process (Pitman, pp. 57–62, 2006) or the Indian buffet process (Griffiths and Ghahramani, 2005), the rules of pilgrim’s monopoly are straightforward and reminiscent of the board game even though the available real estate is an infinite straight line rather than a square loop. Pilgrim’s monopoly is a novel description of a process first described by Dempsey and McCullagh (2015) in the more general study of Markov survival processes. It is a process involving a sequence of pilgrims or travellers who pay toll fees and hotel taxes as they go, proceeding until their funds are depleted. The initial funds for each pilgrim are distributed independently according to the exponential distribution with unit mean. Toll fees are paid continuously at the posted per-mile rate , which is reduced after each passing traveller, and taxes are levied by each hotel encountered on the route. If his funds are exhausted, the traveller establishes a new hotel at the point of exhaustion, and collects taxes from subsequent passers-by. If he arrives at a hotel where his remaining funds are insufficient to pay the tax, the funds are forfeit, and he remains at the hotel as a resident.

Initially, there are no hotels, the toll rate is uniform dollars per mile, so the first traveller setting out from the origin proceeds to the point where he establishes the first hotel. At that stage, the toll rate at point is reduced to , the rate at is unchanged, and the hotel tax is the log ratio of the upstream toll rate to the downstream rate. Upstream is the direction of travel.

After pilgrims have set out from the origin and reached their destinations, , hotels have been established at unique points with . Hotel contains pilgrims, so that . Let be the number of travellers who have proceeded beyond point , i.e., , so that is the number of travellers whose destination lies in . The toll rate is right-continuous and piecewise constant, increasing from immediately before hotel to immediately after. As always, the hotel tax is the log ratio of upstream to downstream toll rates. Thus, the sequence of tolls and taxes faced by pilgrim on the first three legs of his journey are as follows:

where . The destination is the point of maximum progress permitted by the funds available, i.e., the total tolls and taxes are such that . If , the pilgrim establishes a new hotel at ; otherwise he pays the full toll for the segment . If his remaining funds are sufficient to cover the hotel tax at , he does so, and his pilgrimage continues in the same way until his funds are exhausted. Otherwise, his destination is .

3 Illustration by simulation

The pilgrim process takes an input sequence , and produces an output sequence such that is a deterministic function of , though not an invertible one. The following is an example of a 10-component pair generated with :

where is exact and is given to two decimal places. In other words, the transformation is non-stochastic, the only random element being the stochastic nature of the inputs.

The process is straightforward to simulate, but a simple algorithm with minimal book-keeping is likely to be considerably less efficient than an algorithm that keeps track of hotel positions and occupancy numbers, updating them as needed. For greater generality, one may include a second parameter such that the toll rate is , which does not affect the taxes. Although not entirely obvious, the transformation is such that , so the effect is merely multiplicative. A reasonable argument may be made for taking as the default. In particular, the toll after the final hotel would be and limits as tends to or become well-defined. However, unless otherwise stated, we take .

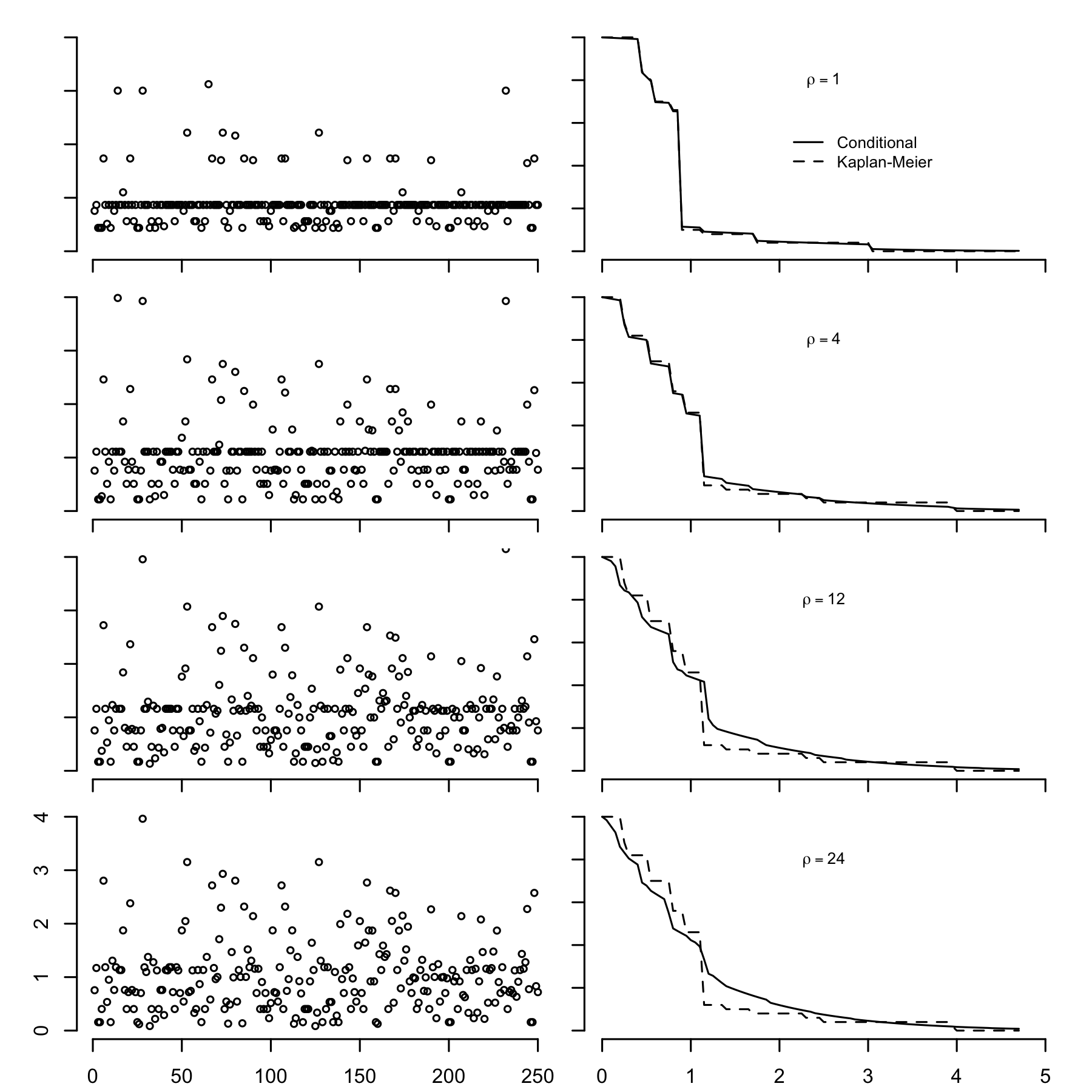

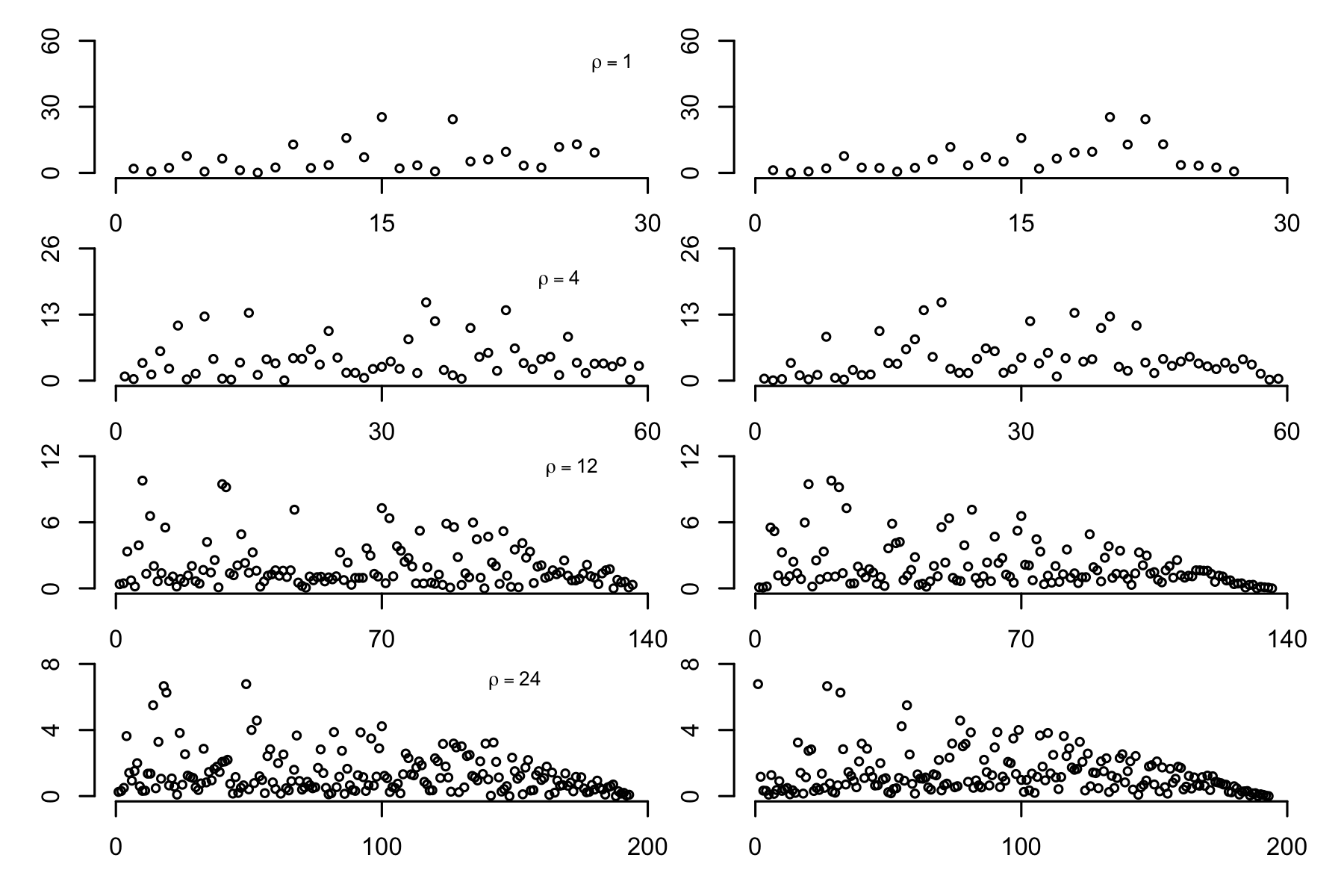

The left panels of Figure 1 show four realizations of the process with the same input sequence, , and parameters respectively. The right panels show the conditional survival distribution (solid line) for which

is the sum of the posted tolls and taxes to be levied on one pilgrim, , travelling from the origin to .

Considering only the taxes, we find that

so that the limit as is the Kaplan-Meier survival curve. In other words, is the limit as of the sum of the hotel taxes posted for pilgrim in . This is also shown in Fig. 1 for comparison, using only the first 50 values. The sample size was kept sufficiently small to make the differences visible. The Kaplan-Meier distribution has mass only at the hotels, and the limiting tax at the final hotel is infinite. (In the presence of censoring, the total mass or tax may be finite, i.e., the Kaplan-Meier distribution may have positive mass at infinity, and the Kaplan-Meier curve then differs from the limiting conditional survival distribution only in the final interval following the last hotel.)

Exchangeability is apparent in the sense that any fixed permutation of the sequence would look much the same. It is also apparent that the process for small is much more grainy than the process for large . The number of distinct values, i.e., the number of hotels, in the four simulations is 15, 32, 74, and 100 respectively.

Simulation allows us to keep track not only of hotel development and hotel occupancy, but also the collection of tolls and taxes. The th pilgrim travelling through the sector contributes in tolls, so the total toll collected in this sector is , where and . The total collected in tolls from all pilgrims passing through the inter-hotel zone is , and the sum of these tolls is . The remainder is distributed in taxes and forfeits to the various hotels. In other words, the process generates not only a partition of into blocks which are ordered in space, but also a partition of by tolls and taxes into parts that are also linearly ordered along the route.

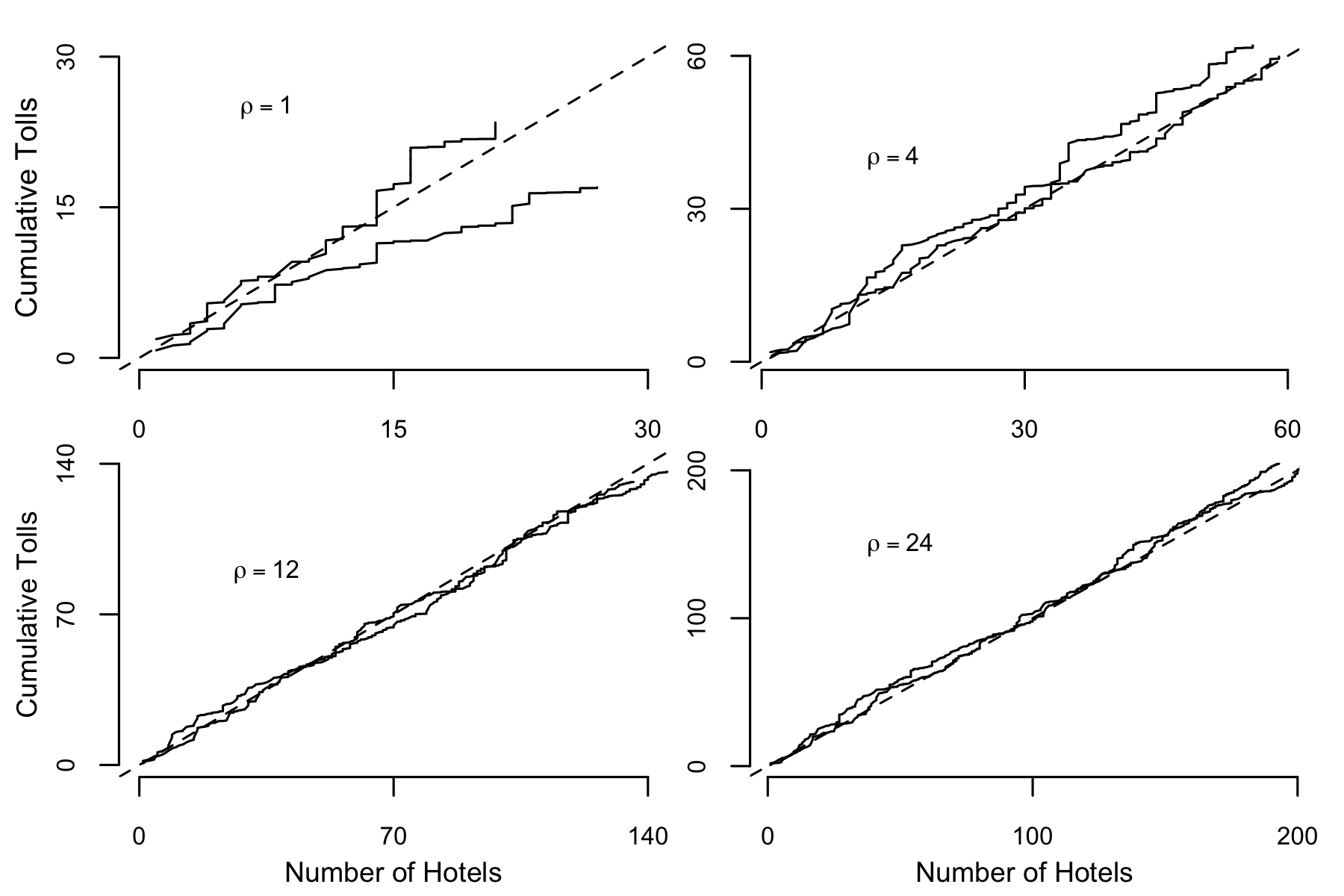

It is of some interest to examine the relationship between the number of hotels, , and the total paid in tolls. Both are increasing in . Figure 2 suggests that they are essentially proportional for large , with limiting ratio one independent of . Specifically, the limiting ratio is equal to the parameter .

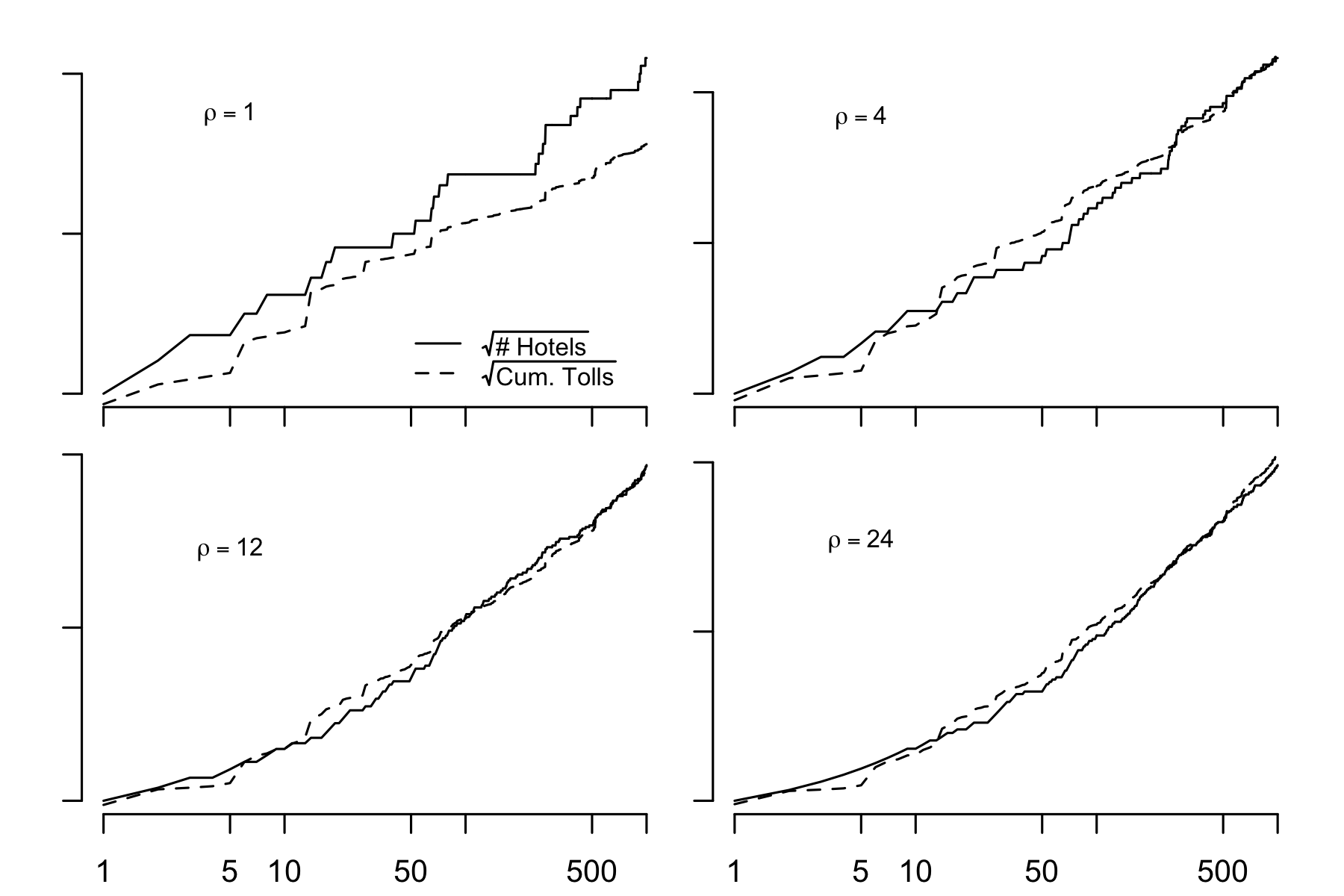

Figure 3 is a plot of against , i.e., the square root of the number of hotels against the log of the number of pilgrims, one panel for each parameer value . Also plotted is the square root of the accumulated tolls against . The simulation is in agreement with the claim that , at least for sufficiently large .

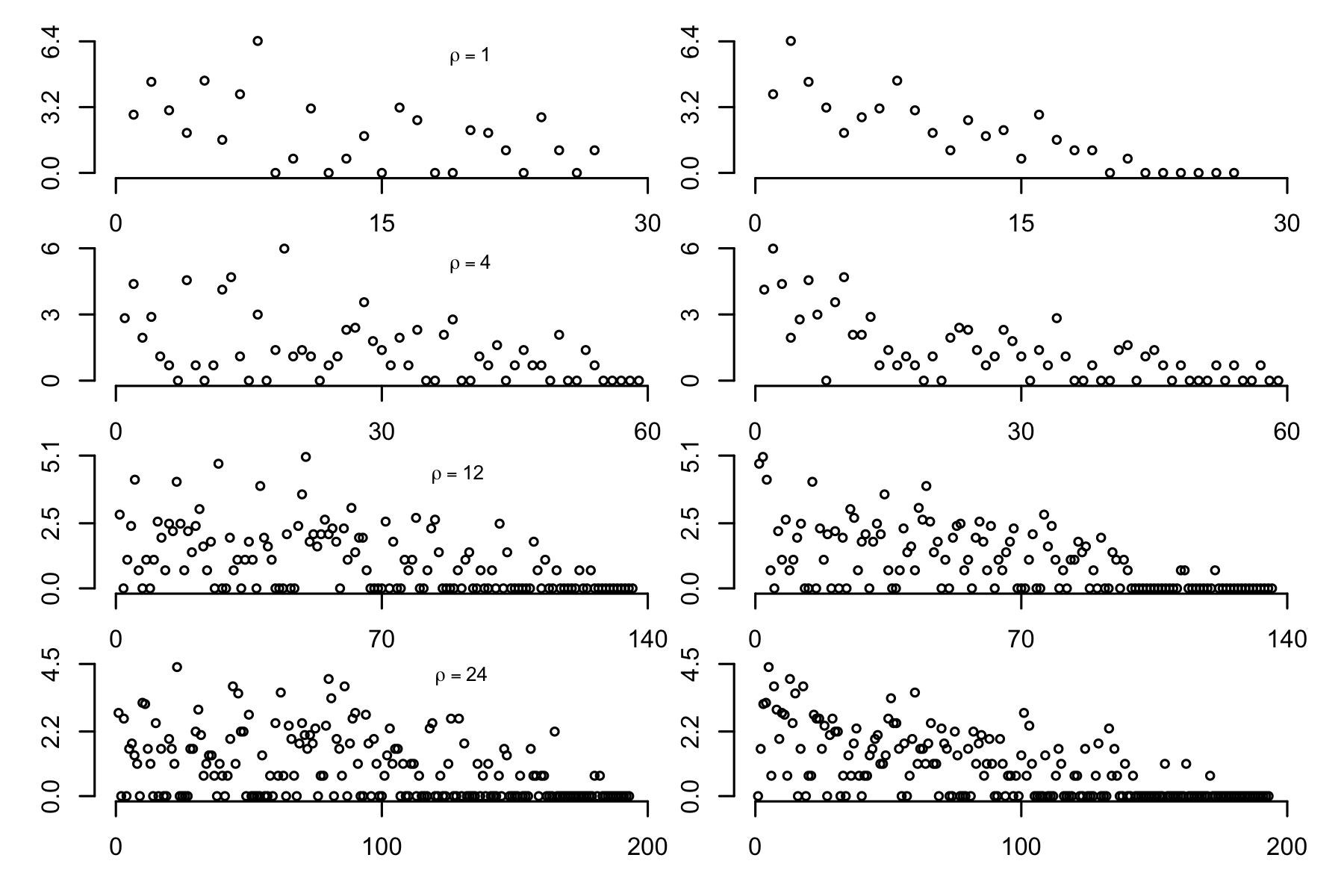

Simulations also allow us to monitor the accumulated wealth of hotel proprietors, either in temporal order of establishment or in spatial order relative to the origin. The wealth of a hotel is the sum of the forfeits of its occupants plus the taxes paid by passers-by. Figure 4 shows the total tax collected by each proprietor in temporal order of establishment (left) and spatial order (right). In each case, there is an upper boundary linearly decreasing in the index. The distribution of total tax collected is approximately uniform under temporal ordering from zero to the upper boundary. Figure 5 shows the total tax when wealth is distributed among occupants. In this case, the maximal wealth per occupant appears to grow initially and then decrease, reaching its peak at the median index independent of .

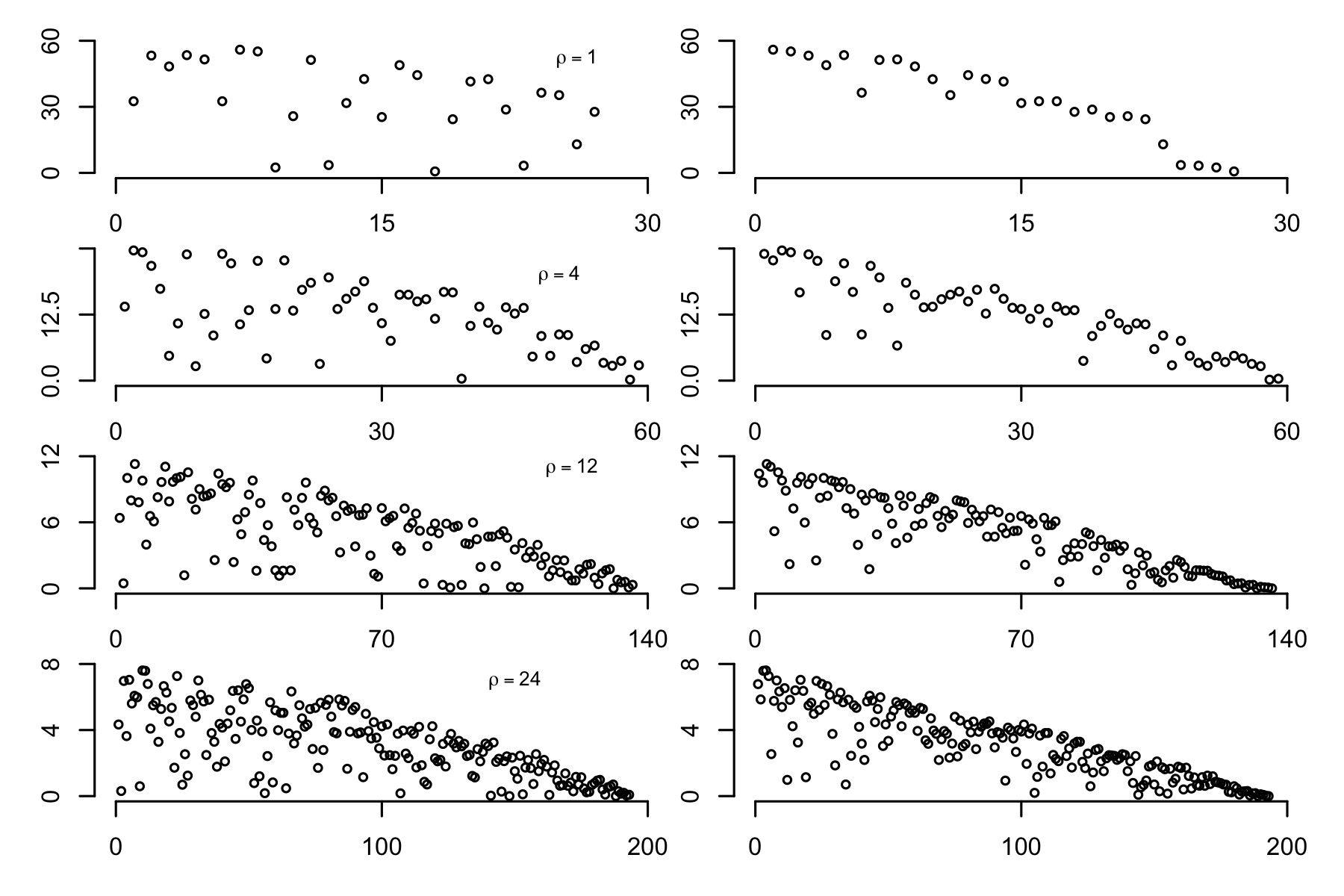

Finally, we investigate the size of hotels in both spatial and temporal order. Figure 6 is a plot of the total number of residents in each hotel on a log-scale for various choices of under both orderings. As tends to infinity, the number of residents in each hotel tends to one. At the other extreme, as tends to zero, all individuals occupy the same hotel. For intermediate values, there tends to be few large hotels with the remainder of moderate size. The number of hotels of size is approximately Poisson with rate proportional to . Under the spatial order relative to the origin, the larger hotels tend to exist closer to the origin. Under temporal ordering, the larger hotels occur earlier; however, the bunching around early indices is less pronounced under this ordering. The number of hotels is independent of the parameter .

4 Key behavior

The pilgrim process is a mathematical exercise that can be studied at various levels and in various ways. The questions of interest are mostly related to the behaviour of the sequence both for finite and the limit as . Some very natural questions are related to the number and the sizes of the blocks, i.e., the hotel occupancy numbers , possibly, but not necessarily, ignoring order. Other questions are concerned with expenditures, particularly the expenditure on taxes and forfeits versus the expenditure on tolls. The total expenditure on tolls, , is a function of , but the remainder is not. As a function of , it appears that is closely related to the number of blocks.

Here we review some of the key existing results found in Dempsey and McCullagh (2015).

Lemma 4.1.

The joint density function for the non-negative sequence is

| (4.1) |

where and where is the th unique time of ( with ).

Remark 1.

The conditional distribution of given has discrete atoms at each of the hotels , plus a remainder that is continuous on . In particular, the conditional distribution is such that

Moreover, the conditional distribution given is such that where are conditionally independent, is distributed continuously as a function of the tolls, and is distributed on as a function of taxes.

4.1 Weak continuity of predictions

The conditional distribution of given the sequence of previous failures has an atom at each distinct failure time, and is continuous elsewhere. The predictive distribution is weakly continuous if a small perturbation of the failure times gives rise to a small perturbation of the predictive distribution. In other words, for each , and for each non-negative vector ,

at each continuity point, i.e., not equal to one of the failure times.

Remark 2.

Consider two adjacent hotels that are -apart. Suppose they are at located at and for some with and occupants respectively. Then as , we say the hotels “merge” and there is one hotel at with occupants. Weak continuity implies as hotels merge, the total taxes collected is the same as the sum of the taxes collected at each hotel individually.

Remark 2 shows that the pilgrim process has weakly continuous predictive distributions as hotel taxes are the log ratio of upstream and downstream toll rates. Theorem 4.2 shows that among a large class of exchangeable survival processes, this property is unique to the pilgrim process.

Theorem 4.2 (Dempsey and McCullagh, 2015).

A Markov survival process has weakly continuous predictive distributions if and only if it is a pilgrim process: for some . The iid exponential model is included as a limit point.

4.2 Number of blocks & block sizes

Lemma 4.3 proves the relationship between the mean number of hotels and the number of pilgrims.

Lemma 4.3 (Dempsey and McCullagh, 2015).

The number of blocks, i.e., the number of distinct components in , is a random non-decreasing function of whose mean satisfies the recursion

| (4.2) |

In particular, for large .

Remark 3.

The total expenditure on tolls by the first pilgrims is , so that is the tax levied by hotels. The mean value, , also satistifes equation (4.2). Therefore, as tends to infinity.

A question of interest is how the number of hotels of a given size grows as a function of the number of pilgrims. Below is a new result highlighting this fact for the pilgrim process.

Lemma 4.4.

The number of hotels of size is approximately Poisson with asymptotic rate proportional to .

The proof can be found in Appendix A.3.

5 Connections with the literature

5.1 Bayesian survival analysis

The output of the pilgrim process is an infinitely exchangeable sequence, which automatically has a de Finetti representation as a conditionally independent and identically distributed sequence. It is in fact one of a large class of similar survival processes investigated in detail by Hjort (1990), in which is a stationary, completely independent, measure on , and are conditionally independent given , with distribution

This means that is a Lévy process with infinitely divisible increments, which are necessarily stationary if the marginal distributions are to be exponential. Processes of this type have been investigated by Doksum (1974), Ferguson and Phadia (1979), Kalbfleisch (1978), Clayton (1991) and James (2006). They are sometimes called neutral to the right. In general, the increments need not be stationary, there may be individual-specific weights such that , and the observations may be subject to censoring. It is important that these matters be accommodated in applied work, and the processes in this class have the virtue that inhomogeneities and right-censoring are easily accommodated. We have chosen not to emphasize this aspect of things because it tends to obscure the underlying process.

Each process in the class is associated with an infinitely divisible distribution which has a characteristic exponent for , and an associated Lévy measure. This means that the multivariate survival function is

For example, the characteristic exponent and the Lévy measure for the gamma process considered by Kalbfleisch (1978) and Clayton (1991) are

The characteristic exponent and the Lévy measure for the pilgrim process are

where is the derivative of the log gamma function. These two pairs and are very alike and they produce very similar processes, but the limits as are not exactly the same. The obvious attraction of the pilgrim process is that it has joint and conditional distributions that are simple to evaluate, which does not, in itself, make it more suited for applied work than any of the other processes in the class. Other processes in the same class include for , which is quite different because it is not analytic at the origin.

In general, the joint density of at times may be written in terms of the characteristic exponent

| (5.1) |

where are the distinct components of , are their multiplicities, and is the th order forward difference

The conditional density of given is most easily described in terms of the conditional hazard measure, which has an atom or tax

at each distinct component of , plus a continuous component with density at . A detailed description is provided by Dempsey and McCullagh (2015). In general, the hotel tax is not equal to the log ratio of upstream to downstream toll rates.

Expression (5.1) is also correct under right censoring provided that the product is restricted to failures. It is also correct under the inhomogeneous model with weights , provided that is replaced with , and the forward differences at are re-defined in the obvious way as an alternating sum over subsets of the residents at . It is also correct under monotone temporal transformation provided that the integral with respect to Lebesgue measure is transformed to an integral with respect to another measure , and the Jacobian is included. These modifications are sufficient to cover the great majority of the non-exchangeable or non-homogeneous processes in this class.

5.2 Neutral population genetics

The non-negative sequence generated by the pilgrim process can be thought of as a simple binary-tree embedded in continuous time. At each failure time the remaining units are split into those who fail, , and the set of units that remain alive, . The tree-like structure is reminiscent of evolutionary tree models studied in neutral evolutionary theory. In particular, the pilgrim process has much in common with the beta-splitting model (Aldous, 1996) introduced as a natural family for the study of probability distributions on cladograms.

A cladogram is a visual representation of the relations among various species. Unlike the trees associated with the pilgrim process, the cladogram has no distinction between right and left edges and are not embedded in continuous time. Figure 7 illustrates such a tree; the figure suggests and are more closely related compared to and among these and are more closely related.

The beta-splitting model assumes the probability of splitting individuals into two groups of size and respectively is given by

where is the normalizing constant and . The beta-splitting model contains several fundamental examples, notably the Yule model (), the uniform model (), and the symmetric binary model as a limit (). Examining equation (6.4) shows the obvious similarity to our setting. The key difference is that the splitting rule for non-negative sequences need not be symmetric. Moreover the number of failures at each failure time needs to be positive, but the risk set can be empty, .

A question of interest is the conditional distribution of a new particle given an existing cladogram. Given an existing split of particles into left and right particles, the probability of the new particle going right is

| (5.2) |

for . Now suppose starting with particles there are consecutive left-singleton splits, . Then the probability that the particle goes right at each of these splits is

| (5.3) |

for . Equations (5.2) and (5.3) are equal for , the latter smaller for and greater for .

We can embed such a cladogram in continuous time by associating with each edge a random holding time (see McCullagh, Pitman, and Winkel, 2008). Figure 7 illustrates the holding times until each subsequent split. Given particles, the holding time until the next fragmentation is distributed exponential with rate parameter . The sequence must satisfy

in order for the process to remain consistent and exchangeable.

To particle is associated the non-negative sequence of holding times . The cladogram on particles embedded in continuous time can be summarized by the set of these non-negative sequences . In Figure 7 both and are associated with the sequence , with , and both and with .

Here we translate Theorem 4.2 to the setting of probability distributions on cladograms embedded in continuous time. The weak continuity condition is slightly different in this setting as the distribution depends on the previous branch choices of the new particle. However, conditional on the branch up to a particular point, the predictive distribution is weakly continuous if a small perturbation of the future splitting times gives rise to a small perturbation in the predictive distribution. The theorem is a direct consequence of the equivalence of equations (5.2) and (5.3) only when (ie. the pilgrim process in this setting). Theorem 5.1 shows that in a large subclass of Markov branching models, an analogous result to Theorem 4.2 holds.

Theorem 5.1.

A Markov branching process with splitting rule of the form

for some sequence of weights , has weakly continuous predictive distributions if and only if it is either the beta-splitting model with or the comb model ().

The comb model is the maximally unbalanced model where only one particle splits from the rest at each time. This is analogous to the setting for Markov survival processes where ties do not occur with probability one. In the case of neutral evolutionary theory, the fragmentations are assumed to happen simultaneously. Consider the above example. The set is assumed to split from the set simultaneously. However, it may be the case that there are two splits occurring in close temporal proximity. As all other Markov branching models have discontinuous predictive distributions, the use of the beta-splitting model for in applications where simultaneous splits are likely the result of approximation seems natural. Even considering the cladogram when it is not embedded in continuous time, equality of equations (5.2) and (5.3) may seem an appropriate assumption for a neutral evolutionary tree model.

In a data example, Aldous (1996) finds the “fit to the model is strikingly better than to the usual models.” Blum and Francois (2006) support this claim with analysis of two additional datasets. Aldous asks if this “is just a fluke?” The above findings suggest not. Indeed they suggest the model analogous to the pilgrim process may be most fitting. It should be noted that the branching topology is a non-smooth function of the value of with particularly different behavior for . As many previous conclusions in neutral evolutionary theory assume a uniform branch split model () underlying the evolutionary tree, these claims may need to be revisited under this new paradigm.

6 Extensions of the pilgrim process

The pilgrim process can be extended to a three parameter family indexed by , , and . Here we continue to assume . For , the pilgrim process is recovered. The generalized pilgrim process exhibits different asymptotic behavior as a function of .

6.1 Generalized pilgrim process

Definition 6.1.

Considering only the taxes, the generalized pilgrim process assumes the hotel tax for the th hotel is given by

where . Note that yields the hotel tax for the pilgrim process. The toll fees, , now depend on the choice of .

-

1.

For ,

where is the beta function.

-

2.

For ,

While the taxes are no longer the ratio of upstream and downstream tolls, the toll choice preserves exchangeability of the joint distribution for the non-negative sequence for all .

Behavior of the generalized pilgrim process depends on the choice of (Dempsey and McCullagh, 2015). For , the number of hotels grows logarithmically. Moreover, the fraction of individuals occupying each hotel admits a stick-breaking representation. If denotes the fraction of individuals in hotel under spatial ordering, then

| (6.1) |

where and .

On the other hand, for , the number of hotels grows polynomially, . If denotes the number of occupants of the first hotel after pilgrims then

for large . So the number of occupants has a power law distribution of degree .

Lemma 6.2 gives new asymptotic results for the number of hotels of a given size for the generalized pilgrim process.

Lemma 6.2.

For , let be the number of hotels with occupancy for a generalized pilgrim process after pilgrims.

-

1.

For , as where is a Poisson random variable with . For this corresponds to condition .

-

2.

For , asymptotically for all fixed . Moreover, almost surely.

Proof of Lemma 6.2 can be found in Appendix A.4. When , it follows from Lindeberg’s theorem that

| (6.2) |

where . For we have . For , we have a similar asymptotic result. Namely, there exists such that

| (6.3) |

Equations (6.2) and (6.3) provide new asymptotic normality results for the number of blocks of the generalized pilgrim process.

6.2 Ordered partitions and splitting rules

A partial ranking of is an ordered list consisting of disjoint non-empty subsets of whose union is . The term partial ranking and ordered partition are used interchangeably. The elements are unordered within blocks, but is the subset ranked first, the subset ranked second, and so on. Let and denote the set of partial rankings of and respectively. An ordered partition process is a probability distribution on the infinite set .

Restriction of the generalized pilgrim process to the first pilgrims gives a joint distribution of the non-negative sequence . The non-negative sequence is in one-to-one correspondence with a pair of a partial ranking and interarrival times

where is the number of blocks.

Here we are only interested in the partial ranking determined by the temporal ordering of the hotels and the number of occupants of the generalized pilgrim process. It is completely determined by a splitting rule. The chance that pilgrims can pay the total tax of a hotel and cannot is given by

| (6.4) |

where is the normalizing constant. For example, if then the splitting rule becomes

| (6.5) |

where is the beta function. The splitting rule allow us to easily infer the induced probability distribution on partial rankings discussed in Section 7.

Using the associated splitting rules, the distribution of is given by

| (6.6) |

where and . Equation (6.6) is important in establishing the connection between the pilgrim process and Ewens sampling formula.

6.3 Pilgrim’s voyage and recurrent events

We now consider the process where each pilgrim must reach a final destination, . Assume that pilgrim has access to a sequence of funds, .

Initially, there are no hotels, the toll rate is uniform dollars per mile, so the first traveller setting out from the origin proceeds to the point where he establishes the first hotel. He then embarks on a second voyage with funds and establishes a second hotel at . He continues in this manner until reaching the final destination, .

At this stage, the toll rate at all points is reduced to , and the hotel tax for all hotels is equal to the log ratio . After pilgrims have set out from the origin and reached the final destination, there are a set of established hotels which are the unique times of the set . Suppose hotel has been occupied by pilgrims, then for the st pilgrim the toll rate from is constant equal to , while the hotel tax is the log ratio

This generates an infinitely exchangeable doubly-indexed non-negative sequence .

The joint density function for the restriction of the sequence to is

The pilgrim’s voyage is useful for describing sequences of recurrent event times. The pilgrim’s voyage can be generalized in a similar way as the pilgrim’s monopoly. Moreover, can depend on time as well as the number of previous event times. This implies such a description can easily be extended to incorporate time-inhomogeneity as well as historical dependencies. Section 7.4 highlights the connection between the pilgrim’s voyage and the Indian buffet process.

7 Exchangeable clustering and feature allocation models

The goal of cluster analysis is to identify a set of mutually exclusive and exhaustive subsets of a finite set . The idea is points in the set will represent a homogeneous sub-population of the sample. The problem is an example of unsupervised learning where there is no external information to aid in the decision making process.

As labelling of elements and the blocks are completely arbitrary, it is natural to disregard the labels and focus solely on the underlying partition of the index set. To this end, exchangeable cluster processes have been developed. Below connects the current study of the pilgrim process to the study of exchangeable partition processes. A connection to the Ewens sampling formula is derived.

7.1 Partition processes and partition structures

A partition of is a set consisting of disjoint non-empty subsets of whose union is . The elements of are unordered within or among blocks. Let denote the set of partitions of , and the set of partitions on the infinitely countable set . Let denote the number of blocks, and the size of block . The alternative notation is commonly used.

The Chinese restaurant process is a sequential description of a particular infinitely exchangeable partition process.

Definition 7.1.

Let denote the restriction of a partition process to the . Then the Chinese restaurant process is defined sequentially. Imagine a restaurant with countably infinite tables indexed by . The tables are chosen accordingly:

-

1.

The first customer sits at the first table.

-

2.

The placement of the st customer is determined by the conditional distribution . The customer chooses a new table with probability or one of the occupied tables with probability proportional to the number of occupants.

The probability of a particular partition, , is given by

where is the ascending factorial. This is the celebrated Ewens sampling formula, which arises in a variety of settings (Crane, 2015).

7.2 From pilgrim process to Ewens sampling formula

Consider generating a random partition via the generalized pilgrim process by extracting the ordered partition from the non-negative sequence and then simply ignoring the ordering of blocks. The map is not reversible, however the resulting random partition is infinitely exchangeable.

| (7.1) |

The probability of the random partition is then

| (7.2) |

where is the group of permutations of items. Note the probabilities on the right-hand side are on partial rankings in while the left-hand side is a probability on partitions in .

Theorem 7.2 provides an interesting connection between the Ewens sampling formula and the generalized pilgrim process.

Theorem 7.2.

The random partition obtained from the generalized pilgrim process for and is equivalent in distribution to a random partition generated by the Ewens sampling formula for .

Proof.

The splitting rule for is given by equation (6.5). By equation (6.6), this implies the probability of a particular partial ranking is

where cancellation is a consequence of . Without loss of generality, we assume this is the canonical labeling ( identity) of the ordered partition. Applying equation (7.2), the proof is complete if we can show

where and .

Consider sampling without replacement from particles with weights proportional to . Then the probability of a given order of sampling of the particles, , is given by

Therefore by law of total probability we have the sum over all possible orderings is equal to one as desired. ∎

While the mapping given by equation (7.1) is noninvertible, the proof to equation (7.2) provides a means for taking a random partition from the Ewens sampling formula and generating a random ordered partition equivalent in distribution to that generated by the generalized pilgrim process by sampling without replacement from the blocks with probabilities proportional to the size of the blocks .

The stick-breaking representation given by equation (6.1) shows that asymptotic frequencies of the first block of the random ordered partition and the first block of the Chinese restaurant process with blocks in size-biased order are equal in distribution. However, sequential construction via the generalized pilgrim process shows that for each , there is a non-zero chance that the first block becomes a singleton. Therefore, while asymptotically equivalent the finite-dimensional distributions are not. We now state a straightforward corollary to Theorem 7.2.

Corollary 7.3.

The one-parameter Chinese restaurant process is a subfamily of the partition process induced by the generalized pilgrim process.

For , the two-parameter extension of the one-parameter Chinese restaurant process allows us to control the relative frequencies. That is, the expected asymptotic frequencies for the first and second blocks are and respectively. So the parameter controls the ratio of the expected asymptotic frequencies, .

For and , the construction is similar to the two-parameter Chinese restaurant process. For and , the two-parameter seating model has customers choosing a new table with probability proportional to or one of the occupied tables with probability proportional to . The number of blocks grows at the same asymptotic rate, . Lemma 7.4 is a consequence of Lemma 6.2 and Lemma 3.11 of Pitman (2005, pg. 71) which provides an asymptotic distribution for the proportion of blocks of size for the two-parameter seating model.

Lemma 7.4.

For and the induced partition from the generalized pilgrim process converges in distribution to the distribution of the random partition generated by the two-parameter Chinese restaurant process.

An interesting class of priors is now generated by looking at the pilgrim process (). The number of blocks grows at which does not correspond to any of the seating models discussed. Therefore, the pilgrim process provides a method for generating an exchangeable partition processes with intermediary behavior between the one-parameter Chinese restaurant process () and the two-parameter process (). We can think of the pilgrim process as an embedding in continuous time of a partition process. Clusters that are similar will be in close temporal proximity. Weak continuity of conditional distributions suggests that the difference between two clusters being arbitrarily close to one another versus one larger cluster on the predictive distribution is negligible at continuity points. In situations where such behavior is desired, the pilgrim process seems a viable candidate for cluster analysis.

7.3 Feature allocation processes

A feature allocation is a generalization of a partition that relaxes the constraint of mutual exclusivity of the blocks. In particular, a feature allocation of is a multiset consisting of non-empty subsets of . Like a partition the elements of are unordered within blocks, and blocks are unordered as well. Let denote the set of feature allocations of , and the set of feature allocations of . The Indian buffet process is a sequential description of a particular feature allocation process.

Definition 7.5.

Let denote the restriction of a feature allocation process to . Then the Indian buffet process is defined sequentially. Imagine a restaurant with countably infinite dishes indexed by . Each customer chooses a finite number of dishes according to the following :

-

1.

The first customer chooses dishes

-

2.

The number of dishes for the st customer is determined by the conditional distribution . For a previously sampled dish , the customer samples the dish with probability

where denotes the number of previous customers to have sampled the dish. The customer then chooses

new dishes. If the new dishes are labelled by order-of-appearance . Here represents the number of dishes sampled after customers, (with ).

7.4 Pilgrim’s voyage to random feature allocations

Consider the doubly-indexed non-negative sequence associated with the pilgrim’s voyage. Then similar to how the pilgrim process induces an ordered partition, , the pilgim’s voyage induces an ordered feature allocation, . The mapping defined by equation (7.1) extends naturally to this setting for feature allocation processes.

The feature allocation, , induced by the pilgrim’s voyage has a sequential description. For , the number of new hotels, , is a Poisson process with rate parameter . Given a final destination , .

For the st pilgrim, the chance he stays at a hotel is where denotes the number of previous occupants. The number of new hotels is given by a Poisson process with rate . Therefore .

Here we have assumed . Otherwise, the sequential description changes as the rate of the Poisson process is multiplied by . Without loss of generality for the induced feature allocation process, we set and . Theorem 7.6 establishes the connection between the Indian buffet process and the pilgrim’s voyage.

Theorem 7.6.

The random feature allocation induced by the pilgrim’s voyage is equal in distribution to the random feature allocation generated by the Indian buffet process for , , and .

The proof is a direct consequence of the equivalence between the sequential descriptions of the random feature allocation processes. If we ignore the ordering of the pilgrim’s voyage for and we have the process that corresponds to the Indian buffet process. The pilgrim’s voyage can be generalized in the same way as the pilgrim process. The generalization is a three-parameter family with parameters such that and . By similar arguments via sequential descriptions one can prove the following lemma.

Lemma 7.7.

Given the Indian buffet process with parameters , , and , there exists , , and such that the random feature allocation induced by the generalized pilgrim’s voyage is equivalent in distribution to that obtained by the Indian buffet process.

In particular, the three-parameter Indian buffet process is a proper subset of the three-parameter family of feature allocation processes generated by the generalized pilgrim’s voyage.

8 Summary

In this paper, we presented the pilgrim process, a probabilistic process in which initial funds for each pilgrim gives rise to a non-negative sequence that is infinitely exchangeable. Simple expressions for a sequential description of the process, the joint density, and the multivariate survivor function are provided as well as a connection to the Kaplan-Meier estimator. Simulation allows investigation of the process’s properties; for example, we find that the number of hotels grows in tandem with the total expenditure on tolls, both growing at a rate proportional to . We connect the pilgrim process with the class of survival processes investigated by Hjort (1990), seeing that the pilgrim process is closely approximated by the gamma process originally considered by Kalbfelisch (1978) and Clayton (1991). Also, generalized pilgrim process is connected to the study of Markov branching models in neutral evolutionary theory. We end with exploration of extensions to the pilgrim process and its connection to exchangeable partition and feature allocation processes.

References

- [1] Aldous, D. (1996) In Random Discrete Structures 76, 1–18.

- [2] Blum, M. and Francois, O. (2006) Which Random Processes Describe the Tree of Life? A Large-Scale Study of Phylogenetic Tree Imbalance. Systematic Biology 55, 685–691.

- [3] Broderick, T., Jordan, M., and Pitman, J. (2013) Cluster and feature modeling from combinatorial stochastic processes. Statistical Science 28, 289–312.

- [4] Broderick, T., Jordan, M., and Pitman, J. (2013) Feature allocations, probability functions, and paintboxes. Bayesian Analysis 8, 801–836.

- [5] Clayton, D.G. (1991) A Monte Carlo method for Bayesian inference in frailty models. Biometrics 47, 467–485.

- [6] Crane, H. (2015) The ubiquitous Ewens sampling formula. Statistical Science, to appear.

- [7] Dempsey, W. and McCullagh, P. (2015) Weak continuity of predictive distribution for Markov survival processes. Unpublished.

- [8] Ferguson, T.S. (1973) A Bayesian analysis of some nonparametric problems. Annals of Statistics 1, 209–230.

- [9] Griffiths, T. and Ghahramani, Z. (2005) Infinite latent feature models and the Indian buffet process. Advances in Neural Information Processing Systems 18, Cambridge, MA, 2006. MIT Press.

- [10] Hjort, N.L. (1990) Nonparametric Bayes estimators based on beta processes in models for life history data. Annals of Statistics 18, 1259–1294.

- [11] James, L.F. (2007) Neutral-to-the-right species sampling mixture models. Chapter 21 in , 425-439, World Scientific Series in Biostatistics, vol 3.

- [12] Kalbfleisch, J.D. (1978) Nonparametric Bayesian analysis of survival time data. J. Roy. Statist. Soc. B 40, 214–221.

- [13] Kaplan, E. L. and Meier, P. (1958) Nonparametric estimation from incomplete observations. J. Amer. Statist. Assn. 53, 457–-481.

- [14] Kingman, J.F.C (1993) Oxford Scientific Publications.

- [15] McCullagh, P., Pitman, J., and Winkel, M. (2008) Bernoulli 14, 988–1002.

- [16] Pitman, J. (2006) Combinatorial Stochastic Processes. Lecture Notes Math. Springer, New York.

Appendix A Technical Arguments

A.1 Proof of Theorem 4.2

Here is presented the conditions for the conditional survival function, , to be a continuous function of the observed risk trajectory. To each consistent splitting rule there is an associated characteristic index defined by

The splitting rules can be described by th order differences

Then

For the conditional survival function to be right continuous, the atomic component of the conditional survival distribution must satisfy

for and . On the other hand, for the function to be left continuous, the atomic component must satisfy

Recursive substitution shows the two conditions to be equal and continuity holds if

| (A.1) |

It is now shown that such a condition is uniquely satisfied by the harmonic process.

Proposition A.1.

The harmonic process is the only Markov survival process with continuous conditional survival function. That is,

where is the risk set trajectory when for some if and only if is from a harmonic survival process.

Proof.

Recall the definition of the th order forward differences

which implies that this forward difference is a linear function of the set .

Start by considering the standardized characteristic index (). First, let be fixed.

Let and . Then equation (A.1) becomes

By definition, is a linear function of while is a function of . Therefore, the left hand side is a linear function of given . On the right hand side, , is a function of while is a function of . Since , both sides are linear in . Therefore solving for shows the characteristic index is a deterministic function of the previous characteristic index values .

The above argument holds if the coefficient of is nonzero. The coefficient is equivalently zero if . Now, suppose equality holds for all . By definition, the splitting rule satisfies

which implies that is again a function of the previous characteristic indices.

The above argument shows is a deterministic function of for . However, is constrained by choice of . In particular, the holding times satisfy . Moreover, the splitting rule must satisfy . Therefore

This translates to for some . It rests to show a correspondence between and the parameter controlling the harmonic process.

For the harmonic process,

so that . Then due to the normalization of the splitting rule

This establishes the correspondence between and and therefore between all that define continuous survival functions and the set of all harmonic processes with parameters and . ∎

Proposition A.2.

If for fixed and for all , then for all . Thus the only process with trivial forward differences is when are iid exponential.

Proof.

Consider the standardized sequence, , and start by showing that implies that for . Indeed, the condition implies that and . Consistency implies

This implies for which implies which is equivalent to . Recursively applying this argument yields for all .

It rests to show that for implies . The normalization condition of the splitting rule implies

Now study the th forward differences:

Plugging into the normalization condition yields

which completes the proof. ∎

Lemma A.3.

Proof.

First note and therefore

It was previously shown that which implies

Adding these together proves the lemma. ∎

A.2 Proof of Theorem 5.1

Theorem 2 from McCullagh, Pitman, and Winkel (2008) proves that the binary fragmentation trees of Gibbs type are identified with the Aldous’ beta-splitting model.

Among the beta-splitting models, the key continuity condition is exactly the same as stated in section A.1

which is only satisfied by the beta-splitting model with and as .

A.3 Proof of Lemma 4.4

The splitting rule for the harmonic process is

When is large, . Moreover, the number of blocks grows at a rate of . Therefore, by a Poissonization argument the number of blocks of size is approximately Poisson with rate parameter

where is a constant dependent on , and is the trigamma function.

A.4 Proof of Lemma 6.2

The splitting rule for is given by

Let and a fixed constant. Then define

Then

denotes the expected number of blocks of size where the random sequence satisfies . As , we want to show . By the ratio test

where we have used for . Therefore, the sequence converges almost surely and we have the expected number of blocks of size is proportional to .

Since the expected number of blocks is we see that the expected number of blocks of size is

In particular, for then we have the expected number of blocks is which is equivalent to the one parameter Chinese restaurant process.