Inference for High-dimensional Differential Correlation Matrices

111The research was supported in part by NSF Grant DMS-1208982 and NIH Grant R01 CA127334.

T. Tony Cai and Anru Zhang222Corresponding author. E-mail: anrzhang@wharton.upenn.edu Department of Statistics

The Wharton School

University of Pennsylvania

Abstract

Motivated by differential co-expression analysis in genomics, we consider in this paper estimation and testing of high-dimensional differential correlation matrices. An adaptive thresholding procedure is introduced and theoretical guarantees are given. Minimax rate of convergence is established and the proposed estimator is shown to be adaptively rate-optimal over collections of paired correlation matrices with approximately sparse differences. Simulation results show that the procedure significantly outperforms two other natural methods that are based on separate estimation of the individual correlation matrices. The procedure is also illustrated through an analysis of a breast cancer dataset, which provides evidence at the gene co-expression level that several genes, of which a subset has been previously verified, are associated with the breast cancer.

Hypothesis testing on the differential correlation matrices is also considered. A test, which is particularly well suited for testing against sparse alternatives, is introduced.

In addition, other related problems, including estimation of a single sparse correlation matrix, estimation of the differential covariance matrices, and estimation of the differential cross-correlation matrices, are also discussed.

Statistical inference on the correlation structure has a wide array of applications, ranging from gene co-expression network analysis (Carter et al., 2004; Lee et al., 2004; Zhang et al., 2008; Dubois et al., 2010; Fuller et al., 2007) to brain intelligence analysis (Shaw et al., 2006). For example, understanding the correlations between the genes is critical for the construction of the gene co-expression network. See Kostka and Spang (2004), Lai et al. (2004), and Fuller et al. (2007). Driven by these and other applications in genomics, signal processing, empirical finance, and many other fields, making sound inference on the high-dimensional correlation structure is becoming a crucial problem.

In addition to the correlation structure of a single population, the difference between the correlation matrices of two populations is of significant interest.

Differential gene expression analysis is widely used in genomics to identify disease-associated genes for complex diseases. Conventional methods mainly focus on the comparisons of the mean expression levels between the disease and control groups. In some cases, clinical disease characteristics such as survival or tumor stage do not have significant associations with gene expression, but there may be significant effects on gene co-expression related to the clinical outcome (Shedden and

Taylor (2005); Hudson et al. (2009); Bandyopadhyay

et al. (2010)). Recent studies have shown that changes in the correlation networks from different stages of disease or from case and control groups are also of importance in identifying dysfunctional gene expressions in disease. See, for example, de la Fuente (2010).

This differential co-expression network analysis has become an important complement to the original differential expression analysis as differential correlations among the genes may reflect the rewiring of genetic networks between two different conditions (See Shedden and

Taylor (2005); Bandyopadhyay

et al. (2010); de la Fuente (2010); Ideker and Krogan (2012); Fukushima (2013)).

Motivated by these applications, we consider in this paper optimal estimation of the differential correlation matrix. Specifically, suppose we observe two independent sets of -dimensional i.i.d. random samples with mean , covariance matrix , and correlation matrix , where and 2.

The goal is to estimate the differential correlation matrix . A particular focus of the paper is on estimating an approximately sparse differential correlation matrix in the high dimensional setting where the dimension is much larger than the sample sizes, i.e., . The estimation accuracy is evaluated under both the spectral norm loss and the Frobenius norm loss.

A naive approach to estimating the differential correlation matrix is to first estimate the covariance matrices and separately and then normalize to obtain estimators and of the individual correlation matrices and , and finally take the difference

as the estimator of the differential correlation matrix . A simple estimate of a correlation matrix is the sample correlation matrix. However, in the high-dimensional setting, the sample correlation matrix is a poor estimate. Significant advances have been made in the last few years on optimal estimation of a high-dimensional covariance matrix. Regularization methods such as banding, tapering, and thresholding have been proposed. In particular, Cai et al. (2010) established the optimal rate of convergence and Cai and Yuan (2012) developed an adaptive estimator of bandable covariance matrices. For sparse covariance matrices where each row and each column has relatively few nonzero entries, Bickel and Levina (2008) introduced a thresholding estimator and obtained rates of convergence; Cai and Liu (2011) proposed an adaptive thresholding procedure and Cai and Zhou (2012) established the minimax rates of convergence for estimating sparse covariance matrices.

Structural assumptions on the individual correlation matrices and are crucial for the good performance of the difference estimator. These assumptions, however, may not hold in practice. For example, gene transcriptional networks often contain the so-called hub nodes where the corresponding gene expressions are correlated with many other gene expressions. See, for example, (Barabási and

Oltvai, 2004; Barabási et al., 2011). In such settings, some of the rows and columns of and have many nonzero entries which mean that and are not sparse. In genomic applications, the correlation matrices are rarely bandable as the genes are not ordered in any particular way.

In this paper, we propose a direct estimation method for the differential correlation matrix without first estimating and individually. This direct estimation method assumes that is approximately sparse, but otherwise does not impose any structural assumptions on the individual correlation matrices and . An adaptive thresholding procedure is introduced and analyzed. The estimator can still perform well even when the individual correlation matrices cannot be estimated consistently. For example, direct estimation can recover the differential correlation network accurately even in the presence of hub nodes in and as long as the differential correlation network is approximately sparse. The key is that sparsity is assumed for and not for or .

Theoretical performance guarantees are provided for direct estimator of the differential correlation matrix. Minimax rates of convergence are established for the collections of paired correlation matrices with approximately sparse differences. The proposed estimator is shown to be adaptively rate-optimal. In comparison to adaptive estimation of a single sparse covariance matrix considered in Cai and Liu (2011), both the procedure and the technical analysis of our method are different and more involved. Technically speaking, correlation matrix estimators are harder to analyze than those of covariance matrices and the two-sample setting in our problem further increases the difficulty.

Numerical performance of the proposed estimator is investigated through simulations. The results indicate significant advantage of estimating the differential correlation matrix directly.

The estimator outperforms two other natural alternatives that are based on separate estimation of and . To further illustrate the merit of the method, we apply the procedure to the analysis of a breast cancer dataset from the study by van de Vijver et al. (2002) and investigate the differential co-expressions among genes in different tumor stages of breast cancer.

The adaptive thresholding procedure is applied to analyze the difference in the correlation alternation in different grades of tumor.

The study provides evidence at the gene co-expression level that several genes, of which a subset has been previously verified, are associated with the breast cancer.

In addition to optimal estimation of the differential correlation matrix, we also consider hypothesis testing of the differential correlation matrices, versus . We propose a test which is particularly well suited for testing again sparse alternatives. The same ideas and techniques can also be used to treat other related problems. We also consider estimation of a single sparse correlation matrix from one random sample, estimation of the differential covariance matrices as well as estimation of the differential cross-correlation matrices.

The rest of the paper is organized as follows. Section 2 presents in detail the adaptive thresholding procedure for estimating the differential correlation matrix. The theoretical properties of the proposed estimator are analyzed in Section 3.

In Section 4, simulation studies are carried out to investigate the numerical performance of the thresholding estimator and Section 5 illustrates the procedure through an analysis of a breast cancer dataset. Hypothesis testing on the differential correlation matrices is discussed in Section 6.1, and other related problems

are considered in the rest of Section 6. All the proofs are given in the Appendix.

2 Estimation of Differential Correlation Matrix

We consider in this section estimation of the differential correlation matrix and introduce a data-driven adaptive thresholding estimator. The theoretical and numerical properties of the estimator are investigated in Sections 3 and 4 respectively.

Let be a -variate random vector with mean , covariance matrix , and correlation matrix , for and 2.

Suppose we observe two i.i.d. random samples, from and from , and the two samples are independent. The goal is to estimate the differential correlation matrix under the assumption that is approximately sparse.

Given the two random samples, the sample covariance matrices and sample correlation matrices are defined as, for and 2,

(1)

(2)

where and is the diagonal matrix with the same diagonal as .

We propose a thresholding estimator of the differential correlation matrix by individually thresholding the entries of the difference of the two sample correlation matrices with the threshold adaptive to the noise level of each entry. A key to the construction of the procedure is the estimation of the noise levels of the individual entries of , as these entries are random variables themselves.

We first provide some intuition before formally introducing the estimate of the noise levels of the individual entries of . Note that and . Define

(3)

Then one can intuitively write

(4)

where is approximately normal with mean 0 and variance 1. Hence, measures the uncertainty of the sample covariance . Based on the first order Taylor expansion of the 3-variate function for and ,

(5)

the entries of the sample correlation matrix can be approximated by

where the random variables and are approximately normal with mean 0 and variance 1, but not necessarily independent for .

Equation (7) suggests that estimation of is similar to the sparse covariance matrix estimation considered in Cai and Liu (2011), where it is proposed to adaptively threshold entries according to their individual noise levels. However, the setting here is more complicated as is not an unbiased estimate of and the noise levels are harder to estimate. These make the technical analysis more involved. The noise levels are unknown here but can be estimated based on the observed data. Specifically, we estimate and by the following data-driven quantities,

(8)

(9)

We are now ready to introduce the adaptive thresholding estimator of using data-driven threshold levels. Let be a thresholding function satisfying the following conditions:

(C1).

for all satisfying for some ;

(C2).

for ;

(C3).

, for all .

Note that the commonly used soft thresholding function and the adaptive lasso rule with satisfy these three conditions. See Rothman et al. (2009) and Cai and Liu (2011). Although the hard thresholding function does not satisfy Condition (C1), the technical arguments given in this paper still work with very minor changes.

We propose to estimate the sparse differential correlation matrix by the entrywise thresholding estimator defined as

where is a thresholding function satisfying (C1)-(C3) and the threshold level is given by with

(10)

Here are given by (9) and the thresholding constant can be chosen empirically through cross-validation. See Section 4.1 for more discussions on the empirical choice of .

3 Theoretical Properties

We now analyze the theoretical properties of the data-driven thresholding estimator proposed in the last section. We will establish the minimax rate of convergence for estimating the differential correlation matrix over certain classes of paired correlation matrices with approximately sparse difference under the spectral norm loss. The results show that is rate-optimal under mild conditions.

3.1 Rate Optimality of the Thresholding Estimator

We consider the following class of paired correlation matrices in with approximately sparse difference

(11)

for some . Here and mean that and are symmetric, semi-positive definite, and with all diagonal entries 1. For , their difference is approximately sparse in the sense that each row vector of lies in the ball with radius and .

When , this constraint becomes the commonly used exact sparsity condition.

Let

We assume that for each , is sub-Gaussian distributed, i.e. there exist constants such that for all and ,

(12)

In addition, we assume for some constant

(13)

The following theorem provides an upper bound for the risk of the thresholding estimator under the spectral norm loss.

Theorem 3.1 (Upper bound)

Suppose and (12) and (13) hold. Suppose the thresholding function satisfy Conditions (C1)-(C3). Then the thresholding estimator defined in (2) and (10) with satisfies

(14)

(15)

(16)

for some constant that does not depend on or .

Remark 3.1

Condition (13) holds naturally when are jointly Gaussian. To see this point, we suppose is the correlation between and . Then one can write , where are independently standard Gaussian. It is easy to calculate that , which implies (13) holds for .

Condition (13) is used in Lemma 6.1 to show that is a good estimate of and can be controlled by with high probability.

Theorem 3.1 gives the rate of convergence for the thresholding estimator . The following result provides the lower bound for the minimax risk of estimating the differential correlation matrix with .

Theorem 3.2 (Lower Bound)

Suppose

and

for some constant . Then minimax risk for estimating satisfies

(17)

(18)

(19)

for some constant .

Theorems 3.1 and 3.2 together yield the minimax rate of convergence

for estimating with under the spectral norm loss, and show that the thresholding estimator defined in (2) and (10) is adaptively rate-optimal.

Remark 3.2

The technical analysis here for the different of two correlation matrices is more complicated in comparison to the problem of estimating a sparse covariance matrix considered in Cai and Liu (2011). It can be seen in (7), i.e. the “signal + noise” expression of , the difference of the sample correlation matrices has six “noise terms”. It is necessary to deal with all these six terms in the theoretical analysis of Theorem 3.1.

4 Numerical Studies

We investigate in this section the numerical performance of the adaptive thresholding estimator of the differential correlation matrix through simulations. The method is applied to the analysis of a breast cancer dataset in the next section.

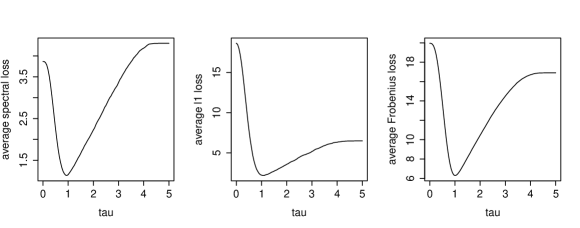

In the previous sections, we proposed the entrywise thresholding method for estimating and then studied the theoretical properties of with a fixed . However, the theoretical choice of may not be optimal in finite sample performance, as we can see in the following example. Let and be -dimensional matrices such that and . Here is the indicator function, are i.i.d. random variables that are uniformly distributed on . In this setting, both and are sparse, but their difference is even more sparse. We set and generate independent samples from and independent samples from . For various values of , we implement the proposed method with hard thresholding and repeat the experiments for 100 times. The average loss in spectral, and Frobenious norms are shown in Figure 1.

Figure 1: Average (Spectral, , Frobenious) norm losses for . , .

Obviously in this example, is not the best choice.

Empirically, we find that the numerical performance of the estimator can often be improved by using a data-driven choice of based on cross-validation. We thus begin by introducing the following -fold cross-validation method for the empirical selection of .

4.1 Empirical Choice of

For an integer , we first divide both samples and randomly into two groups for times as , , and . Here represents the -th division. For and , the size of the first group is approximately and the size of the second group is approximately . We then calculate the corresponding sample correlation matrices as , and for all four sub-samples. Partition the interval into an equi-spaced grid . For each value of , we obtain the thresholding estimator defined in (2) and (10) with the thresholding constant based on the subsamples and . Denote the average loss for each for the second sub-samples and as

We select

as our empirical choice of the thresholding constant , and calculate the final estimator with the thresholding constant based on the whole samples and .

4.2 Estimation of Differential Correlation Matrix

The adaptive thresholding estimator is easy to implement. We consider the following two models under which the differential correlation matrix is sparse.

1.

Model 1 (Random Sparse Difference) and are -dimensional symmetric positive definite matrices such that is a fixed matrix, where with if and 02 if , is the identity matrix, and is randomly generated as , where with

and is a constant that ensures the positive definiteness of .

2.

Model 2 (Banded Difference) In this setting, -dimensional matrices and satisfy 0208 and 02. Here is the indicator function.

In each of the two settings, we set for both , where are two i.i.d. samples from . These operations make the covariance matrices and have different values along the diagonals.

We generate i.i.d. samples from and for various values of , and and then apply the proposed algorithm with 5-fold cross-validation for the selection of the thresholding constant . For each setting, both the hard thresholding and adaptive-Lasso thresholding (Rothman et al. (2009)),

(20)

are used.

For comparison, we also implement three natural estimators of .

1.

The covariance matrices and are estimated individually by the adaptive thresholding method proposed in Cai and Liu (2011) with 5-fold cross-validation and then and are normalized to yield estimators of and ,

and finally is estimated by the difference .

2.

The correlation matrices and are estimated separately using the method proposed in Section 6.2 and then take the difference.

3.

is estimated directly the difference of the sample correlation matrices .

The numerical results are summarized in Tables 1 and 2 for the two models respectively. In each case, we compare the performance of the three estimators , and under the spectral norm, matrix norm, and Frobenius norm losses.

For both models, it is easy to see that the direct thresholding estimator significantly outperforms and .

Under Model 1, the individual correlation matrices and are “dense” in the sense that half of the rows and columns contain many non zeros entries, but their difference is sparse. In this case, and cannot be estimated consistently and the two difference estimators and based on the individual estimators of and perform very poorly, while the direct estimator performs very well.

Moreover, the numerical performance of the thresholding estimators does not depend on the specific thresholding rules in a significant way. Different thresholding rules including hard thresholding and adaptive Lasso behave similarly.

Hard

Adaptive Lasso

Sample

Spectral Norm

100

50

50

050(041)

175(137)

694(107)

033(031)

151(175)

617(098)

728(093)

100

100

100

034(021)

379(317)

474(055)

028(023)

353(271)

449(071)

502(065)

100

200

200

029(019)

422(214)

323(047)

024(013)

452(186)

314(054)

355(047)

100

500

500

024(010)

172(035)

207(032)

022(008)

182(035)

187(026)

223(025)

500

50

50

056(077)

302(276)

3188(404)

040(065)

347(463)

2915(426)

3466(384)

500

100

100

041(048)

809(1102)

2338(452)

034(039)

1299(1326)

2182(323)

2419(277)

500

200

200

032(040)

2222(1306)

1567(330)

026(034)

2131(929)

1461(224)

1650(197)

500

500

500

020(019)

780(137)

780(129)

018(014)

821(169)

870(139)

1046(131)

Matrix Norm

100

50

50

089(068)

363(297)

1891(155)

078(080)

314(320)

1688(142)

2133(161)

100

100

100

064(025)

734(485)

1342(108)

070(087)

703(414)

1272(118)

1497(114)

100

200

200

064(034)

963(185)

922(075)

061(037)

937(177)

867(087)

1060(081)

100

500

500

058(022)

454(056)

592(054)

056(021)

485(061)

533(045)

669(044)

500

50

50

169(309)

785(814)

9728(664)

137(287)

949(1193)

8702(731)

11240(897)

500

100

100

106(128)

2012(1950)

6498(593)

117(147)

2795(2275)

6560(507)

7966(537)

500

200

200

097(148)

5164(1013)

4674(501)

095(124)

4787(850)

4554(370)

5577(370)

500

500

500

068(054)

2319(286)

2347(256)

069(052)

2467(292)

2721(209)

3532(204)

Frobenious Norm

100

50

50

140(132)

434(251)

1901(037)

106(104)

326(261)

1660(042)

1987(038)

100

100

100

096(059)

714(367)

1338(023)

094(081)

623(331)

1210(027)

1405(025)

100

200

200

089(057)

909(103)

930(020)

084(050)

815(107)

842(025)

994(018)

100

500

500

085(032)

437(027)

592(011)

082(030)

443(025)

526(011)

639(010)

500

50

50

333(563)

1118(771)

9505(091)

227(392)

957(931)

8340(124)

9997(093)

500

100

100

218(298)

2017(1455)

6137(209)

210(247)

2254(1669)

6058(085)

7040(067)

500

200

200

177(239)

4506(589)

4211(167)

163(196)

3952(514)

4188(073)

4953(049)

500

500

500

127(109)

2017(099)

2174(065)

122(084)

2048(091)

2547(041)

3134(033)

Table 1: Comparison of with and under Model 1.

Hard

Adaptive Lasso

Sample

Spectral Norm

100

50

50

098(100)

461(149)

725(087)

071(070)

447(144)

605(074)

829(098)

100

100

100

070(051)

288(081)

501(057)

062(047)

293(087)

425(052)

583(059)

100

200

200

060(035)

193(055)

353(042)

048(024)

198(057)

298(037)

407(047)

100

500

500

047(014)

123(027)

232(023)

046(017)

130(036)

198(021)

266(027)

500

50

50

097(099)

503(100)

2061(107)

080(075)

455(096)

1691(090)

2496(116)

500

100

100

079(062)

317(049)

1364(059)

059(041)

314(063)

1113(053)

1639(071)

500

200

200

060(036)

213(030)

912(042)

051(031)

211(035)

744(037)

1094(050)

500

500

500

051(020)

134(016)

563(023)

049(020)

135(022)

465(021)

678(029)

Matrix Norm

100

50

50

184(266)

1061(348)

1911(155)

126(186)

988(314)

1618(155)

2192(161)

100

100

100

118(144)

673(224)

1362(108)

110(126)

673(212)

1173(120)

1587(111)

100

200

200

098(098)

453(147)

979(085)

071(071)

468(146)

839(089)

1137(097)

100

500

500

067(048)

295(089)

644(056)

065(059)

308(103)

558(047)

747(053)

500

50

50

179(265)

1103(280)

7971(264)

164(226)

1038(302)

6446(273)

9788(255)

500

100

100

145(175)

766(179)

5652(216)

102(135)

773(240)

4565(186)

6942(176)

500

200

200

102(118)

497(109)

3986(139)

083(114)

503(127)

3190(115)

4911(133)

500

500

500

081(070)

315(072)

2534(077)

082(077)

327(100)

2039(077)

3136(079)

Frobenious Norm

100

50

50

336(253)

1382(183)

1846(081)

266(147)

1213(200)

1587(079)

1992(094)

100

100

100

267(119)

946(128)

1326(055)

254(110)

877(118)

1151(054)

1432(058)

100

200

200

243(069)

694(072)

975(039)

226(051)

668(076)

859(037)

1049(043)

100

500

500

224(034)

529(036)

696(019)

225(046)

528(044)

633(017)

739(019)

500

50

50

677(486)

3424(333)

9109(085)

618(386)

2739(339)

7597(083)

10071(092)

500

100

500

619(298)

2276(192)

6437(056)

530(179)

2012(221)

5372(056)

7123(058)

500

200

200

532(149)

1634(118)

4579(044)

510(136)

1501(115)

3836(042)

5061(043)

500

500

500

500(062)

1214(059)

2977(027)

499(069)

1176(070)

2527(024)

3280(025)

Table 2: Comparison of with and under Model 2.

5 Analysis of A Breast Cancer Dataset

Identifying gene expression networks can be helpful for conducting more effective treatment based to the condition of patients. de la Fuente (2010) demonstrated that the gene expression networks can vary in different disease states and the differential correlations in gene expression (i.e. co-expression) are useful in disease studies.

In this section, we consider the dataset “70pathwaygenes-by-grade” from the study by van de Vijver et al. (2002) and investigate the differential co-expressions among genes in different tumor stages of breast cancer. In this dataset, there are 295 records of patients with 1624 gene expressions, which are categorized into three groups based on the histological grades of tumor (“Good”, “Intermediate” and “Poor”) with 74, 101 and 119 records, respectively. We denote these three groups of samples as and . In order to analyze the difference in the correlation alternation in different grades of tumor, we apply our adaptive thresholding method with cross-validation to estimate the differential correlation matrices among those gene expressions from different stages.

The number of gene pairs with significant difference in correlation are listed in Table 3. The results show that the correlation structures between the “Good” and “Intermediate” groups are similar and there is some significant changes between the “Good” and “Poor” group.

Good v.s. Intermediate

Intermediate v.s. Poor

Good v.s. Poor

# of selected pairs

0

2

152

Table 3: The number of gene pairs that have significant differential correlation betweens two groups of different tumor grades

More interestingly, by combining the “Good” and “Intermediate” sub-samples and comparing with the “Poor” group, we find significant differences between their correlation structure. There are 4526 pairs of genes that have significantly different correlations between the “Good + Intermediate” and “Poor” groups. For each given gene, we count the number of the genes whose correlation with this gene is significantly different between these two groups, and rank all the genes by the counts. That is, we rank the genes by the size of the support of in each row.

The top ten genes are listed in Table 4.

Table 4: The top ten genes that appear for most times in the selected pairs in “Good + Intermediate” v.s. “Poor”

Among these ten genes, six of them, GDF5, TCF7L1, PAPSS1, SFRP1, GABRP, TGFB1, have been previously studied and verified in the literature that are associated with the breast cancer (See Margheri et al. (2012), Shy et al. (2013), Xu et al. (2012), Klopocki et al. (2004), Zafrakas et al. (2006), and Ghellal et al. (2000), respectively). Take for example GDF5 and TCF7L1, the overproduction of Transforming growth factor beta-1 (TGF), a multifunctional cytokine, is an important characteristic of late tumor progression. Based on the study by Margheri et al. (2012), TGF produced by breast cancer cells brings about in endothelial cells expression of GDF5. The findings in (Shy et al. (2013)) suggested the important role played by TCF7L1 in breast cancer. Although these biological studies mainly focus on the the behavior of the single gene expression, our study provides evidence in the gene co-expression level that these gene expressions are related with the breast cancer.

We should point out that the two well-known genes related to the breast cancer, BRCA1 and BRCA2, were not detected by our method. This is mainly due to the fact that our method focus on the differential gene co-expressions, not the changes in the gene expression levels.

6 Other Related Problems

We have so far focused on optimal estimation of the differential correlation matrix. In addition to optimal estimation, hypothesis testing of the differential correlation matrix is also an important problem. In this section we consider testing the hypotheses versus and propose a test which is particularly well suited for testing again sparse alternatives.

Similar ideas and techniques can also be used to treat several other related problems, including estimation of a single sparse correlation matrix from one random sample, estimation of the differential covariance matrices, and estimation of the differential cross-correlation matrices. We also briefly discuss these problems in this section.

6.1 Testing Differential Correlation Matrices

Suppose we are given two sets of independent and identical distributed samples with the mean , covariance matrix and correlation matrix , where and , and wish to test the hypotheses

(21)

This testing problem is similar to, but also different from, testing the equality of two high-dimensional covariance matrices, which has been considered in several recent papers. See, for example, Schott (2007), Srivastava and

Yanagihara (2010), Li et al. (2012), and Cai et al. (2013).

Here we are particularly interested in testing against sparse alternatives and follow similar ideas as those in Cai et al. (2013).

To construct the test statistic, we need more precise understanding of the sample correlation coefficients . It follows from (5) that

Since , , , we introduce

Then asymptotically as ,

The true value of is unknown but can be estimated by

We define the test statistic by

where

Under regularity conditions (similar to (C1)-(C3) in Cai et al. (2013)), the asymptotic distribution of can be shown to be the type I extreme value distribution. More precisely,

(22)

for any given .

The asymptotic null distribution (22) can then be used to construct a test for testing the hypothesis . For a given significance level , define the test by

(23)

where

is the quantile of the type I extreme value distribution with the cumulative distribution function . The hypothesis is rejected whenever .

As the test proposed in Cai et al. (2013) for testing the equality of two covariance matrices, the test defined in (23) can also be shown to be particularly well suited for testing against sparse alternatives.

6.2 Optimal Estimation of a Sparse Correlation Matrix

The ideas and technical tools can also be used for estimation of a single correlation matrix from one random sample, which is a simpler problem.

Suppose we observe an independent and identical distributed sample from a -dimensional distribution with mean , covariance matrix , and correlation matrix .

When is approximately sparse, it can be naturally estimated by a thresholding estimator as follows.

Let . Define the sample covariance matrix and the sample correlation matrix respectively by

where is the thresholding constant that can be chosen empirically through cross-validation. The correlation matrix is then estimated by with

We consider the following class of approximately sparse correlation matrices

The following theoretical results for can be established using a similar analysis.

Proposition 6.1

Suppose and satisfies (12), (13). For , there exists some constant does not depend on or such that

(27)

(28)

(29)

Moreover, when , for some constant , the rate in (27) is optimal as we also have the lower bound

(30)

(31)

(32)

Remark 6.1

Cai and Liu (2011) proposed an adaptive thresholding estimator of a sparse covariance matrix . This estimator leads naturally to an estimator of a sparse correlation matrix by normalizing via . The correlation matrix estimator has similar properties as the estimator introduced above. For example, and achieve the same rate of convergence.

6.3 Optimal Estimation of Sparse Differential Covariance Matrices

Our analysis can also be used for estimation of sparse differential covariance matrices, . Define as in (3) and its estimate as in (8).

Similar to the estimation of the differential correlation matrix , we estimate by adaptive entrywise thresholding. Specifically, we define the thresholding estimator by

(33)

where is the thresholding level given by

(34)

Same as in the last section, here belongs to the class of thresholding functions satisfying Conditions (C1)-(C3) and the thresholding constant can be taken chosen empirically by cross-validation.

We consider the following class of paired covariance matrices with approximately sparse differences, for ,

(35)

Under the same conditions as those in Theorems 3.1 and 3.2, a similar analysis can be used to derive the minimax upper and lower bounds. It can be shown that the estimator given in (33) with satisfies

(36)

for some constant . Furthermore, the following minimax lower bound holds,

(37)

for some constant . Equations (36) and (37) together show that the thresholding estimator defined in (33) and (34) is rate-optimal.

In many applications such as phenome-wide association studies (PheWAS) which aims to study the relationship between a set of genomic markers and a range of phenotypes , the main focus is on the cross-correlations between the components of and those of . That is, the object of interest is a submatrix of the correlation matrix of the random vector

.

More specifically, let be a -dimensional random vector and be a -dimensional random vector. In the PheWAS setting, may be all phenotypic disease conditions of interest and is a vector of genomic markers.

Suppose we have two independent and identical distributed samples of the pairs, one for the case group and one for the control group,

Here for , , are independent and identical distributed samples generated from some distribution with mean , covariance matrix and correlation matrix given by

In applications such as PheWAS, it is of special interest to estimate the differential cross-correlation matrix of and , i.e. . Again, we introduce the following set of paired correlation matrices with sparse cross-correlations,

The thresholding procedure proposed in Section 2 can be applied to estimate ,

(38)

where is sample cross-correlation matrix of and ; is given by (10). Similar to Theorem 3.1, the following theoretical results hold for the estimator .

Proposition 6.2

Suppose , and (12) and (13) hold. Suppose the thresholding function satisfies Conditions (C1)-(C3). Then defined in (38) with the thresholding constant satisfies

(39)

(40)

(41)

for some constant that does not depend on or .

The proof of Proposition 6.2 is similar to that of Theorem 3.1 by analyzing the block instead of the whole matrix . We omit the detailed proof here.

References

Bandyopadhyay

et al. (2010)

Bandyopadhyay, S., Mehta, M., Kuo, D., Sung, M.-K., Chuang, R., Jaehnig, E. J.,

Bodenmiller, B., Licon, K., Copeland, W., Shales, M., Fiedler, D., Dutkowski,

J., Guénolé, A., van Attikum, H., Shokat, K. M., Kolodner, R. D.,

Huh, W.-K., Aebersold, R., Keogh, M.-C., Krogan, N. J., and Ideker, T.

(2010).

Rewiring of genetic networks in response to DNA damage.

Sci. Signal., 330(6009):1385–1389.

Barabási et al. (2011)

Barabási, A.-L., Gulbahce, N., and Loscalzo, J. (2011).

Network medicine: a network-based approach to human disease.

Nat. Rev. Genet., 12(1):56–68.

Barabási and

Oltvai (2004)

Barabási, A.-L. and Oltvai, Z. N. (2004).

Network biology: understanding the cell’s functional organization.

Nat. Rev. Genet., 5(2):101–113.

Bickel and Levina (2008)

Bickel, P. and Levina, E. (2008).

Covariance regularization by thresholding.

The Annals of Statistics, 26:879–921.

Cai and Liu (2011)

Cai, T. T. and Liu, W. (2011).

Adaptive thresholding for sparse covariance matrix estimation.

Journal of American Statistical Association, 106:672–684.

Cai et al. (2013)

Cai, T. T., Liu, W., and Xia, Y. (2013).

Two-sample covariance matrix testing and support recovery in

high-dimensional and sparse settings.

Journal of American Statistical Association, 108:265–277.

Cai and Yuan (2012)

Cai, T. T. and Yuan, M. (2012).

Adaptive covariance matrix estimation through block thresholding.

The Annals of Statistics, 40:2014–2042.

Cai et al. (2010)

Cai, T. T., Zhang, C.-H., and Zhou, H. H. (2010).

Optimal rates of convergence for covariance matrix estimation.

The Annals of Statistics, 38:2118–2144.

Cai and Zhou (2012)

Cai, T. T. and Zhou, H. H. (2012).

Optimal rates of convergence for sparse covariance matrix estimation.

The Annals of Statistics, 40:2389–2420.

Carter et al. (2004)

Carter, S. L., Brechbühler, C. M., Griffin, M., and Bond, A. T. (2004).

Gene co-expression network topology provides a framework for

molecular characterization of cellular state.

Bioinformatics, 20(14):2242–2250.

de la Fuente (2010)

de la Fuente, A. (2010).

From “differential expression” to “differential networking” –

identification of dysfunctional regulatory networks in diseases.

Trends in Genetics, 26:326––333.

Dubois et al. (2010)

Dubois, P. C., Trynka, G., Franke, L., Hunt, K. A., Romanos, J., Curtotti, A.,

Zhernakova, A., Heap, G. A., Ádány, R., Aromaa, A., et al. (2010).

Multiple common variants for celiac disease influencing immune gene

expression.

Nature genetics, 42(4):295–302.

Fukushima (2013)

Fukushima, A. (2013).

Diffcorr: an r package to analyze and visualize differential

correlations in biological networks.

Gene, 518(1):209–214.

Fuller et al. (2007)

Fuller, T. F., Ghazalpour, A., Aten, J. E., Drake, T. A., Lusis, A. J., and

Horvath, S. (2007).

Weighted gene coexpression network analysis strategies applied to

mouse weight.

Mammalian Genome, 18(6-7):463–472.

Ghellal et al. (2000)

Ghellal, A., Li, C., Hayes, M., Byrne, G., Bundred, and N., Kumar, S. (2000).

Prognostic significance of tgf beta 1 and tgf beta 3 in human breast

carcinoma.

Anticancer Rec., 20:4413–4418.

Hudson et al. (2009)

Hudson, N. J., Reverter, A., and Dalrymple, B. P. (2009).

A differential wiring analysis of expression data correctly

identifies the gene containing the causal mutation.

PLoS Comput. Biol., 5(5):e1000382.

Ideker and Krogan (2012)

Ideker, T. and Krogan, N. J. (2012).

Differential network biology.

Molecular systems biology, 8(1):565.

Klopocki et al. (2004)

Klopocki, E., Kristiansen, G., Wild, P. J., Klaman, I., Castanos-Velez, E.,

Singer, G., Stöhr, R., Simon, R., Sauter, G., Leibiger, H., Essers, L.,

Weber, B., Hermann, K., Rosenthal, A., Hartmann, A., and Dahl, E. (2004).

Loss of sfrp1 is associated with breast cancer progression and poor

prognosis in early stage tumors.

Int. J. Oncol., 25:641–649.

Kostka and Spang (2004)

Kostka, D. and Spang, R. (2004).

Finding disease specific alterations in the co-expression of genes.

Bioinformatics, 20(suppl 1):i194–i199.

Lai et al. (2004)

Lai, Y., Wu, B., Chen, L., and Zhao, H. (2004).

A statistical method for identifying differential gene-gene

co-expression patterns.

Bioinformatics, 20:3146–3155.

Lee et al. (2004)

Lee, H. K., Hsu, A. K., Sajdak, J., Qin, J., and Pavlidis, P. (2004).

Coexpression analysis of human genes across many microarray data

sets.

Genome research, 14(6):1085–1094.

Li et al. (2012)

Li, J., Chen, S. X., et al. (2012).

Two sample tests for high-dimensional covariance matrices.

The Annals of Statistics, 40(2):908–940.

Margheri et al. (2012)

Margheri, F., Schiavone, N., Papucci, L., Magnelli, L., Serratì, S., Chillà,

A., Laurenzana, A., Bianchini, F., Calorini, L., Torre, E., Dotor, J.,

Feijoo, E., Fibbi, G., and Del Rosso, M. (2012).

Gdf5 regulates tgfß-dependent angiogenesis in breast carcinoma mcf-7

cells: In vitro and in vivo control by anti-tgfß peptides.

PloS ONE, 7:e50342.

Rothman et al. (2009)

Rothman, A., Levina, E., and Zhu, J. (2009).

Generalized threshholding of large covariance matrices.

Journal of the American Statistical Association, 104:177–186.

Schott (2007)

Schott, J. R. (2007).

A test for the equality of covariance matrices when the dimension is

large relative to the sample sizes.

Computational Statistics & Data Analysis, 51(12):6535–6542.

Shaw et al. (2006)

Shaw, P., Greenstein, D., Lerch, J., Clasen, L., Lenroot, R., Gogtay, N.,

Evans, A., Rapoport, J., and Giedd, J. (2006).

Intellectual ability and cortical development in children and

adolescents.

Nature, 440(7084):676–679.

Shedden and

Taylor (2005)

Shedden, K. and Taylor, J. (2005).

Differential correlation detects complex associations between gene

expression and clinical outcomes in lung adenocarcinomas.

In Methods of Microarray Data Analysis, pages 121–131.

Springer.

Shy et al. (2013)

Shy, B., Wu, C., Khramtsova, G., Zhang, J., Olopade, O., Goss, K., and Merrill,

B. (2013).

Regulation of tcf7l1 dna binding and protein stability as principal

mechanisms of wnt/b-catenin signaling.

Cell Reports, 4:1–9.

Srivastava and

Yanagihara (2010)

Srivastava, M. S. and Yanagihara, H. (2010).

Testing the equality of several covariance matrices with fewer

observations than the dimension.

Journal of Multivariate Analysis, 101(6):1319–1329.

van de Vijver et al. (2002)

van de Vijver, M., He, Y., van’t Veer, L., Dai, H., Hart, A. A., Voskuil,

D. W., Schreiber, G. J., Peterse, J. L., Roberts, C., Marton, M. J., Parrish,

M., Atsma, D., Witteveen, A., Glas, A., Delahaye, L., vander Velde, T.,

Bartelink, H., Rodenhuis, S., Rutgers, E. T., Friend, S. H., and Bernards, R.

(2002).

A gene-expression signature as a predictor of survival in breast

cancer.

New England Journal of Medicine, 347:1999––2009.

Xu et al. (2012)

Xu, Y., Liu, X., Guo, F., Ning, Y., Zhi, X., Wang, X., Chen, S., Yin, L., and

Li, X. (2012).

Effect of estrogen sulfation by sult1e1 and papss on the development

of estrogen-dependent cancers.

Cancer science, 103:1000–1009.

Zafrakas et al. (2006)

Zafrakas, M., Chorovicer, M., Klaman, I., Kristiansen, G., Wild, P.-J.,

Heindrichs, U., Knüchel, R., and Dahl, E. (2006).

Systematic characterisation of gabrp expression in sporadic breast

cancer and normal breast tissue.

International Iournal of Cancer, 118(6):1453–1459.

Zhang et al. (2008)

Zhang, J., Li, J., and Deng, H. (2008).

Class-specific correlations of gene expressions: identification and

their effects on clustering analyses.

The American Journal of Human Genetics, 83(2):269–277.

Appendix: Proofs

We prove the main theorems in the Appendix. Throughout the Appendix, we denote by a constant which does not depend on and , and may vary from place to place.

Proof of Theorem 3.1 To prove this theorem, we consider the following three events separately,

(42)

(43)

(44)

Here is the fixed constant which satisfies where is introduce in (13); and are constants which do not depends on and shall be specified later in Lemma 6.1.

1.

First we would like to show that under the event ,

(45)

(46)

(47)

In fact,

for all , so

(48)

So by the definition of , we have

(49)

(50)

Hence,

(51)

(52)

Suppose , . By (51) and , we have when is large enough. Thus for large , we obtain

(53)

It then follows from the assumption that for large ,

(54)

and

We shall note the difference between and above. Next, we rearrange the inequality above and write it into an inequality for ,

Besides, since are the population and sample correlations, , . By (C1) of thresholding , we have for all . Thus,

which yields

(74)

Similarly, ,

.

Therefore,

(75)

(76)

(77)

Finally, we combine the situations of and . When and , we have

(78)

which has proved (14). (15) and (16) can be proved similarly by (46), (62), (76) and (47), (63), (77).

Proof of Lemma 6.1. (64) is directly from (25) in Cai and Liu (2011). For (66), the proof is essentially the same as the proof of (26) in Cai and Liu (2011) as long as we use in stead of in their proof. Now we mainly focus on the proof of (65). Without loss of generality, we can translate and assume that . Note that we have the following formulation,

(79)

Since

where is a constant which does not depend on . Thus, we set ; based on lemma 1 in Cai and Liu (2011), we have

(80)

for all , where . Next for , we similarly apply Lemma 1 in Cai and Liu (2011) and get

Proof of Theorem 3.2. Without loss of generality, we assume . For , set and we have already known this information. The estimation of sparse difference immediately becomes the estimation of the sparse correlation matrix . Then the lower bound result for estimating single sparse covariance matrix can be used to prove this theorem.

We follow the idea of Cai and Zhou (2012) and define the set of diagonal-1 covariance matrices as

We have . Besides, the proof of Theorem 2 in Cai and Zhou (2012) shows that

(83)

Since the correlation matrix equals to covariance matrix (i.e. ) when , then

(84)

which implies (17). By for symmetric matrices, (18) also follow immediately.

Similarly, (19) follows from Theorem 4 of Cai and Zhou (2012).

Proof of Proposition 6.1. The proof of Proposition 6.1 is similar to Theorem 3.1. For the upper bound, again, we split the whole events into three,

(85)

(86)

(87)

Here is the fixed constant which satisfies where was introduced in (13); are constants specified in Lemma 6.1. Similarly to the proof of Theorem 3.1, we can prove the following statements.

1.

Under ,

2.

For ,

3.

For ,

The rest of proof, including the lower bound results, are omitted here as they are essentially the same as Theorem 3.1.