Abstract:

In survey sampling, calibration is a very popular tool used to make total estimators consistent with known totals of auxiliary variables and to reduce variance.

When the number of auxiliary variables is large, calibration on all the variables may lead to estimators of totals whose mean squared error (MSE) is larger than the MSE of the Horvitz-Thompson estimator even if this simple estimator does not take account of the available auxiliary information. We study in this paper a new technique based on dimension reduction through principal components that can be useful in this large dimension context. Calibration is performed on the first principal components, which can be viewed as the synthetic variables containing the most important part of the variability of the auxiliary variables. When some auxiliary variables play a more important role than the others, the method can be adapted to provide an exact calibration on these important variables. Some asymptotic properties are given in which the number of variables is allowed to tend to infinity with the population size.

A data driven selection criterion of the number of principal components ensuring that all the sampling weights remain positive is discussed. The methodology of the paper is illustrated, in a multipurpose context, by an application to the estimation of electricity consumption for each day of a week with the help of 336 auxiliary variables consisting of the past consumption measured every half an hour over the previous week.

Key words and phrases:

calibration on estimated auxiliary variables; dimension reduction; model-assisted estimation; multipurpose surveys; partial calibration; partial least squares; penalized calibration; ridge regression; survey sampling; variance approximation.

1. Introduction

Since the seminal work by Deville and Särndal (1992), calibration is one of the most popular and useful tools to improve Horvitz-Thompson estimators of totals in a

design-based survey sampling framework.

Roughly speaking, it consists in looking for a modification of the sampling weights so that the totals, in the population, of the auxiliary variables are perfectly estimated. Performing calibration often leads to total estimators with smaller variances and this technique is routinely used by several national statistical agencies (see Särndal, 2007 for a review).

With the spread of automatic process for data collection as well as increasing storage capacities, it is not unusual anymore to have to analyze data coming from very large surveys with many auxiliary variables. In this finite population context, calibration on all the auxiliary variables may lead to estimators whose performances are worse than the simple Horvitz-Thompson estimator even if this latter estimator does not account for any auxiliary information (see e.g. Silva and Skinner, 1997).

Calibration over a very large number of auxiliary variables has been called over-calibration by Guggemos and Tillé (2010).

Several difficulties arise in this context such as instability of the calibration weights or variance inflation.

There are different ways of dealing with these issues. One possibility is to choose only a subset of the auxiliary variables and to consider only the auxiliary variables that are expected to be the more pertinent, avoiding the problem of multicollinearity (see e.g. Silva and Skinner, 1997; Chambers, Skinner and Wang, 1999 and Clark and Chambers, 2008). Another way is to relax the calibration constraints, meaning that the too restrictive requirement of being exactly calibrated is dropped off and replaced by the requirement of being only approximately calibrated. A class of penalized estimators has been suggested by Bardsley and Chambers (1984) in a model-based setting and extended later by Chambers (1996), Rao and Singh (1997, 2009) and Théberge (2000) in a design-based (or model-assisted) setting. Usually, some auxiliary variables play a role that is more important than the others and it is required that their totals be estimated exactly. To fulfill this requirement, Bardsley and Chambers (1984) and Guggemos and Tillé (2010) suggested two different penalized optimization problems which lead in fact to the same system of weights, and by consequence to the same partially penalized estimator (see Goga and Shehzad, 2014).

We present in this paper another way of dealing with this issue. Our estimator is based on dimension reduction of the auxiliary variables via principal components calibration. In multivariate statistics, principal component analysis (PCA) is a very popular tool for reducing the dimension of a set of quantitative variables (see e.g. Jolliffe, 2002) by transforming the initial data set into a new set of a few uncorrelated synthetic variables, called principal components (PC), which are linear combinations of the initial variables with the largest variance. The method we suggest consists in reducing the number of auxiliary variables by considering a small number of PC’s and by performing calibration on these new synthetic variables. As far as we know, its application in a survey sampling setting is new.

Adopting a model-assisted point of view (see Särndal et. al 1992), the PCA Calibration approach can also be viewed as a GREG estimator based on Principal Components Regression (PCR).

PCR can be very useful to reduce the number of covariates in a linear regression model especially when the regressors are highly correlated (see e.g Frank and Friedman,1993). As explained in Jolliffe (2002), even if PCR is a biased estimation method for estimating a regression coefficient, it is useful to overcome the problem of multicollinearity among the regressors. The method is easy to put into practice with classical softwares used for performing calibration, such as CALMAR used at the French National Statistical Institut (Insee) since, with centered data, these new calibration variables are also centered and their totals are known and equal to zero.

Note that a natural alternative to principal components regression is partial least squares (PLS) which is also a popular dimension reduction regression technique that can be useful when there is a large number of auxiliary variables that are highly correlated (see for example Swold et al. 2001 for a pedagogical presentation of PLS).

As noted in Frank and Friedman (1993), it often has similar prediction errors to principal components regression. Other model selection techniques such as the Lasso (Tibshirani, 1996) or the elastic net (Zou and Hastie, 2005) can be employed to deal with survey data with large number of auxiliary variables. The main drawback of all these model selection techniques is that they would give survey weights that would depend explicitly on the outcome variable.

Having weights that depend on the outcome variable is generally not desired in surveys, particularly in multipurpose surveys, in which there can be many outcome variables under study.

Consequently, all these alternative regression techniques that would have given weights depending explicitly on the outcome variable have not been considered in this work.

The paper is structured as follows: we briefly recall in Section 2 the calibration method as it was suggested by Deville and Särndal (1992) and the problems which may arise when the number of auxiliary variables is large. We introduce in Section 3 the suggested method and we give a model-assisted interpretation. As expected, with the chi-squared distance, the calibration estimator on PC’s may be written as a GREG-type estimator with respect to the initial auxiliary variables but with a modified regression coefficient estimator.

When the auxiliary information is not complete, i.e. the values of the auxiliary variables are only known in the sample, we first estimate the PC’s and then we perform calibration on the first estimated principal components (Section 4). In Section 5, under mild assumptions on the sampling design and on the study and auxiliary variables, we prove that the calibration estimator on true PC’s as well as on estimated PC’s are asymptotical unbiased and consistent. We show also that these estimators are asymptotically equivalent to the generalized difference estimator computed with a PCR estimator. Variance estimators are also presented. We present, in Section 6, how the method can be adapted to provide an exact calibration on variables considered by the survey statistician more important than the other variables.

Our method is illustrated in Section 7, in a multipurpose and large dimension context, on the estimation of the total electricity consumption for each day of a week with the help of the past consumption measured every half an hour over the previous week. Borrowing ideas from Bardsley and Chambers (1984), a data-driven choice of the tuning parameter is suggested which consists in selecting the largest dimension such that all the estimated principal component weights remain positive.

Finally, a brief Section 8 gives some concluding remarks as well as some directions that would deserve further investigation. The proofs are gathered in an Appendix.

2. Calibration over a large number of auxiliary variables

We consider the finite population and we wish to estimate the total

where is the value of the variable of interest for the th unit. Let be a random sample, with fixed size , drawn from according to a sampling design that assigns to unit a known inclusion probability satisfying . The corresponding sampling design weight is denoted by We suppose that is known for all (complete response).

Without auxiliary information, the total is estimated unbiasedly by the Horvitz-Thompson (HT) estimator

Consider now auxiliary variables, , and let be the transposed vector whose elements are the values of the auxiliary variables for the th unit. The calibration method has been developed by Deville and Särndal (1992) to use as effectively as possible the known population totals of at the estimation stage. The calibration estimator of is a weighted estimator

(2.1)

whose (calibration) weights are chosen so that they are as close as possible to the initial sampling weights , according to some distance and subject to some constraints. More exactly,

(2.2)

(2.3)

where is the vector of weights assigned to each unit in the sample and is the vector whose elements are the known totals of for . Several distance functions have been studied in Deville and Särndal (1992). Under weak regularity assumptions these authors have shown that all resulting estimators are asymptotically equivalent to the one obtained by minimizing the chi-square distance function

where the ’s are known positive constants that can be used to take account of the variability of the observations and are unrelated to . A common use in the applications is to consider uniform weights for all units and we will suppose, without loss of generality, that in the following. We will only consider calibration estimators derived using the chi-square distance. The calibration weights , , are

(2.4)

and the corresponding calibration estimator is obtained by plugging-in in (2.1).

With a different point of view, it can be shown that the calibration estimator obtained with the chi-squared distance is equal to the generalized regression estimator (GREG) which is derived by assuming a linear regression model between the study variable and the auxiliary variables ,

(2.5)

where is a centered random vector with a diagonal variance matrix, whose diagonal elements are equal to . Cassel et al. (1976) suggested the generalized difference estimator

(2.6)

where is the ordinary least squares estimator of and is the HT estimator of . Remark that can not be computed because can not be computed unless we have observed the whole population. We estimate by and obtain the GREG estimator of

Under mild regularity assumptions, Deville and Särndal (1992) have proven that the calibration estimator and have the same asymptotic distribution. We have and as a result, the asymptotic variance of is

where is the probability that both and are included in the sample , and .

Calibration will improve the HT estimator, namely if the predicted values are close enough to the ’s, that is to say if the model stated in (2.5) explains sufficiently well the variable of interest. Nevertheless, when a very large number of auxiliary variables are used, this result is no longer true as it was remarked by Silva and Skinner (1997) in a simulation study.

One way to circumvent the problems due to over-calibration such as extremely large weights and variance inflation, is to relax the calibration constraints, meaning that the too restrictive requirement of being exactly calibrated as in (2.3) is dropped off and replaced by the requirement of being only approximately calibrated. Then, the deviation between and is controlled by means of a penalty. Bardsley and Chambers (1984), in a model-based setting, and Chambers (1996), Rao and Singh (1997) in a design-based setting, suggested finding weights satisfying (2.2), subject to a quadratic constraint, as

where , and is a user-specified cost associated with the th calibration constraint. The tuning parameter controls the trade off between exact calibration () and no calibration (). With the chi-square distance, the solution is, for ,

and the penalized calibration estimator is a GREG type estimator, whose regression coefficient is estimated by a ridge-type estimator (Hoerl and Kennard, 1970):

For an infinite cost , the th calibration constraint is satisfied exactly (see Beaumont and Bocci, 2008). As noted in Bardsley and Chambers (1984), the risk of having negative weights (in the case of the chi-square distance) is greatly reduced by using penalized calibration. In the context of empirical likelihood approach, Chen et al. (2002) suggested replacing the true totals with where is a diagonal matrix depending on the costs and a tuning parameter controling the deviation between and .

Different algorithms have been studied in the literature to select good values, with data driven procedures, of the ridge parameter (see Bardsley and Chambers, 1984; Chen et al. (2002); Beaumont and Bocci, 2008; Guggemos and Tillé, 2010).

3. Calibration on Principal Components

We consider in this work another class of approximately calibrated estimators which are based on dimension reduction through principal components analysis (PCA). In multivariate statistics PCA is one of most popular techniques for reducing the dimension of a set of quantitative variables (see e.g. Jolliffe, 2002) by extracting most of the variability of the data by projection on a low dimension space. Principal components analysis consists in transforming the initial data set into a new set of a few uncorrelated synthetic variables, called principal components (PC), which are linear combinations of the initial variables with the largest variance. The principal components are “naturally” ordered, with respect to their contribution to the total variance of the data, and the reduction of the dimension is then realized by taking only the first few of PCs. PCA is particularly useful when the correlation among the variables in the dataset is strong.

These new variables can be also used as auxiliary information for calibration as noted in Goga et al. (2011) and Shehzad (2012).

Complete Auxiliary Information

We suppose without loss of generality that the auxiliary variables are centered, namely and to avoid heavy notations we do not include an intercept term in the model. Note that in applications this intercept term should be included. We suppose now that the auxiliary information is complete, that is to say the -dimensional vector is known for all the units .

Let be the data matrix having as rows. The variance-covariance matrix of the original variables is given by Let be the eigenvalues of associated to the corresponding orthonormal eigenvectors ,

(3.1)

For , the th principal component, denoted by , is defined as follows

(3.2)

Each variable has a (population) variance equal to .

We only consider the first (with ) principal components, which correspond to the largest eigenvalues.

In a survey sampling framework, the goal is not to give interpretations of these new variables as it is the custom in PCA. These variables serve as a tool to obtain calibration weights which are more stable than the calibration weights that would have been obtained with the whole set of auxiliary variables.

More exactly, we want to find the principal component (PC) calibration estimator

where the vector of PC calibration weights , which depends on the number of principal components used for calibration, is the solution of the optimization problem (2.2) and

subject to

,

where is the vector containing the values of the first PCs computed for the -th individual. The PC calibration weights ’s are given by

where is the HT estimator of the total

since we have supposed that the original variables have mean zero.

The total is again estimated by a GREG-type estimator which uses as auxiliary variables

(3.3)

where

(3.4)

The PC calibration estimator depends on the number of PC variables and it can be noted that

if , that is to say if we do not take auxiliary information into account, then is simply the HT estimator (or the Hájek estimator if the intercept term is included in the model) whereas if , we get the calibration estimator which takes account of all the auxiliary variables.

A Model-Assisted Point of View

Consider again the superpopulation model presented in (2.5) and denote by the matrix whose th column is the th eigenvector . Model may be written in the equivalent form

where and where is the value of for the th unit. Principal components regression consists in considering a reduced linear regression model, denoted by , which uses as predictors the first principal components, as follows

(3.5)

where is a vector of elements composed of the first elements of and is the appropriate error term of mean zero. The least squares estimation, at the population level, of , is

(3.6)

which in turn can be estimated, on a sample , by the design-based estimator given by (3.4). We can see now that the PC calibration estimator given in (3.3) is in fact equal to a GREG-type estimator assisted by the reduced model described in (3.5). Note also that since the principal components are centered and uncorrelated, the matrix is diagonal, with diagonal elements .

When there is a strong multicollinearity among the auxiliary variables, it is well known that the ordinary least squares estimator of ,

is very sensitive to small changes in and and it has a very large variance (see e.g Hoerl and Kennard, 1970). To see better how small eigenvalues may affect , Gunst and Mason (1977) write the least squares estimator as follows:

Approximating the covariance matrix by the rank matrix leads to consider the following approximation to the regression estimator that is based on the first principal components,

(3.7)

where This means that is obtained by subtracting from the part of the data that belongs to the dimensional space with the smallest variance and by performing the regression in the dimensional space that contains most of the variability of the data. Note that ridge-regression (Hoerl and Kennard, 1970), which is an alternative way of dealing with the multicollinearity issue, consists in adding a positive term to all eigenvalues . More exactly, the ridge estimator of may be written as where is the -dimensional identity matrix. Both the ridge regression estimator and the principal components estimator are biased for under the model (Gunst and Mason, 1977).

The PC regression estimator can be estimated under the sampling design by

(3.8)

where is given in (3.4). Using relation (3.8) and the fact that we obtain that Consequently can also be written as follows,

and may be seen as a GREG-type estimator assisted by the model when is estimated by .

Calibration on the second moment of the PC variables

With complete auxiliary information, Särndal (2007) stated that “we are invited to consider and other functions of for inclusion in ” especially when “the relationship to the study variable is curved”. Calibration on higher-order moments of the auxiliary variables has also been studied by Ren (2000). In our case, the PC variables satisfy

This means that in presence of complete auxiliary information, the totals of squares of the PCs are known. As a consequence, if we keep the first variables corresponding to the largest eigenvalues, we can consider additional calibration constraints on the second moment of these PCs. We look for the calibration weights solution to (2.2) and subject to

where .

The estimator derived in this way is expected to perform better than the estimator calibrated only on the first moment of the principal components. Nevertheless, calibration on the second moment of the PCs requires additional calibration constraints.

4. Calibration on Estimated Principal Components

The approach presented in the above Sections supposes that the values of the auxiliary variables for are known for all units in the population . In practice, it often happens that the variables are only known for the sampled individuals, but their population totals are known. Then, it is not possible anymore to compute the eigenvalues and the eigenvectors of the population variance-covariance matrix. We present in this section a way to perform principal components calibration when the auxiliary variables are only observed for the units belonging to the sample.

Let be the variance-covariance matrix estimated by

(4.1)

where and . Let be the sorted eigenvalues of and the corresponding orthonormal eigenvectors,

(4.2)

We have that and are the design-based estimators of and respectively, for . It is shown in Cardot et al. (2010) that with large samples and under classical assumptions on the first and second order inclusion probabilities as well as on the variables (see the assumptions (A1)-(A6) in Section 5), that the estimators and are asymptotically design unbiased and consistent for and respectively, for .

The unknown population principal components defined in (3.2) can be approximated as follows,

reminding that is only known for the units in the sample. Nevertheless, its population total is known and is equal to zero since

Note also that are not exactly the principal components associated with the variance-covariance matrix because the original variables are centered in the population but not necessarily in the sample.

Consider now the first estimated principal components

,

corresponding to the largest eigenvalues and suppose that .

The estimated principal component (EPC) calibration estimator of is

,

where the EPC calibration weights are the solution of the optimization problem (2.2) subject to the constraints

where is the vector of values of recorded for the th unit.

With the chi-square distance function , the EPC calibration weights are given by

(4.3)

where is the HT estimator of the total The EPC calibration estimator for is given by

where

The EPC calibration estimator may also be written with respect to the population totals of the original variables, as follows

,

where

5. Some Asymptotic Properties of the Principal Components Calibration Estimators

We adopt in this section the asymptotic framework of Isaki and Fuller (1982). We consider a sequence of growing and nested populations with size tending to infinity and a sequence of samples of size drawn from according to the fixed-size sampling designs . The sequence of subpopulations is an increasing nested one, whereas the sample sequence is not. For simplicity of notation, we drop the subscript in the following when there is no ambiguity. The number of auxiliary variables as well as the number of principal components are allowed to tend to infinity. We suppose that the following assumptions hold.

(A1)

(A2)

for all

(A3)

There is a constant such that for all , .

(A4)

The largest eigenvalue of is bounded, .

(A5)

There is a contant and a non decreasing sequence of integers such that for all we have .

(A6)

There is a constant such that, satisfying , we have .

Conditions (A1), (A2) and (A3) are classical hypotheses for asymptotics in survey sampling (see e.g. Breidt and Opsomer, 2000).

Condition (A4) is closely related to a moment condition on for . If (A4) is fulfilled, .

Assumption (A5) ensures that there is no identifiability issue for the sequence of regression coefficients defined at the population level. It only deals with and does not prevent from being equal to zero or from being very small. The finite population moment assumptions (A4) and (A6) indicate that the vectors cannot be too concentrated in one direction (see Vershynin (2012) for examples in a classical statistical inference context). The proofs of Proposition 1 and Proposition 2 are given in a Supplementary file.

We first show that the estimator based on the true principal components is consistent and we give its asymptotic variance. Note that the assumption on the eigenvalues ensures that there is no identifiability problem of the eigenspace generated by the eigenvectors associated to the largest eigenvalues.

The condition prevents the number of principal components from being too large and ensures that the remainder term, whose order is , tends to zero and is negligible compared to the main term whose order is .

Proposition 1.

Assume that (A1)-(A6) hold and that .

If when goes to infinity, then

and satisfies

.

The condition could certainly be relaxed for particular sampling designs with high entropy under additional moment assumptions.

Note also that the asymptotic variance of is given by

Before stating a consistency result for calibration on estimated principal components, let us introduce an additional condition on the spacing between adjacent eigenvalues.

(A7)

There is a constant such that .

This assumption ensures that the largest eigenvalues are nearly equidistributed in .

Proposition 2.

Assume that (A1)-(A7) hold. If when goes to infinity, then

A more restrictive condition on how may go to infinity is imposed when the principal components are estimated. The condition ensures that the remainder term of order is negligible compared to .

If is bounded, one gets back to classical -rates of convergence whether the population principal components are known or not.

If all the second-order inclusion probabilities are strictly positive, the asymptotic variance of can be estimated by the Horvitz-Thompson variance estimator for the residuals ,

while the asymptotic variance of can be estimated by the Horvitz-Thompson variance estimator for the residuals

6. Partial Calibration on Principal Components

The calibration estimators derived before are not designed to give the exact finite population totals of the original variables . In practice, it is often desired to have this property satisfied for a few but important socio-demographical variables such as sex, age or socio-professional category.

We can adapt the method presented in the previous section in order to fulfill this requirement. We split the auxiliary matrix into two blocks: a first block containing the most important variables with small compared to , and a second block containing the remaining variables. We have

. Note that the constant term will generally belong to the first block of variables.

The goal is to get calibration weights such that the totals of the auxiliary variables in are estimated exactly while the totals of the remaining variables are estimated only approximately. The idea is to calibrate directly on the auxiliary variables from and on the first principal components of , after having taken into account the fact that the variables in and all their linear combinations are perfectly estimated.

For that, we introduce the matrix which is the -dimensional identity matrix and the orthogonal projection onto the vector space spanned by the column vectors of matrix . We also define the matrix ,

which is the projection of onto the orthogonal space spanned by the column vectors of . Matrix represents the residual part of that is not “calibrated” when considering an estimator of the total of calibrated on the variables in .

We define the residual covariance matrix

and denote by its eigenvalues and by the

corresponding orthonormal eigenvectors.

Consider now,

, for ,

the principal components of . The calibration variables are of zero totals and the partial principal component (PPC) calibration estimator of is

,

where the PPC calibration weights , for , are the solution of the optimization problem (2.2) subject to

where is the vector of the values of the variables in and is the vector whose elements are the partial principal components for unit .

Note that with a different point of view, Breidt and Chauvet (2012) use, at the sampling stage, similar ideas in order to perform penalized balanced sampling.

Suppose now that we only have a sample at hand and we know the totals of all the calibration variables. We denote by (resp. ) the (resp. ) matrix containing the observed values of the auxiliary variables. We can estimate the matrix by

where , is the estimation of the projection onto the space generated by the columns of and is the diagonal matrix, with diagonal elements . Then, we can perform the principal components analysis of the projected sampled data corresponding to the variables belonging to the second group and compute the estimated principal components associated to the largest eigenvalues as in Section 4. At last, the total estimator is calibrated on the totals of the variables in and the first estimated principal components.

7. Application to the estimation of the total electricity consumption

Description of the data

The interest of using principal components calibration is illustrated on data from the Irish Commission for Energy Regulation (CER) Smart Metering Project that was conducted in 2009-2010 (CER, 2011)††The data are available on request at the address: http://www.ucd.ie/issda/data/commissionforenergyregulation/.

In this project, which focuses on energy consumption and energy regulation, about 6000 smart meters have been installed in order to collect every half an hour, over a period of about two years, the electricity consumption of Irish residential and business customers.

We evaluate the interest of employing reduction dimension techniques based on PCA by considering a period of 14 consecutive days and a population of smart meters (households and companies). Thus, we have for each unit in the population measurement instants and we denote by the data corresponding to unit where is the electricity consumption (in kW) associated to smart meter at instant . We consider here a multipurpose setting and our aim is to estimate the mean electricity consumption of each day of the second week. For each day of the week, with , the outcome variable is

and our target is the corresponding population total, .

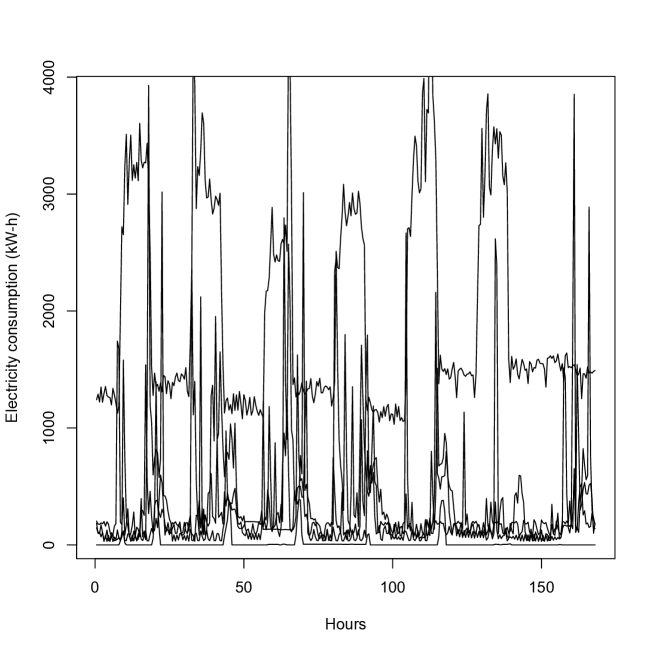

The auxiliary information is the load electricity curve of the first week. This means that we have auxiliary variables, which are the consumption electricity levels at each of the half hours of the first week. A sample of 5 auxiliary information curves is drawn in Figure 7.1.

The condition number of the matrix , which is defined as the ratio , is equal to 67055.78. This large value means that this matrix is ill-conditioned and there may exist strong correlations between some of the variables used for calibration.

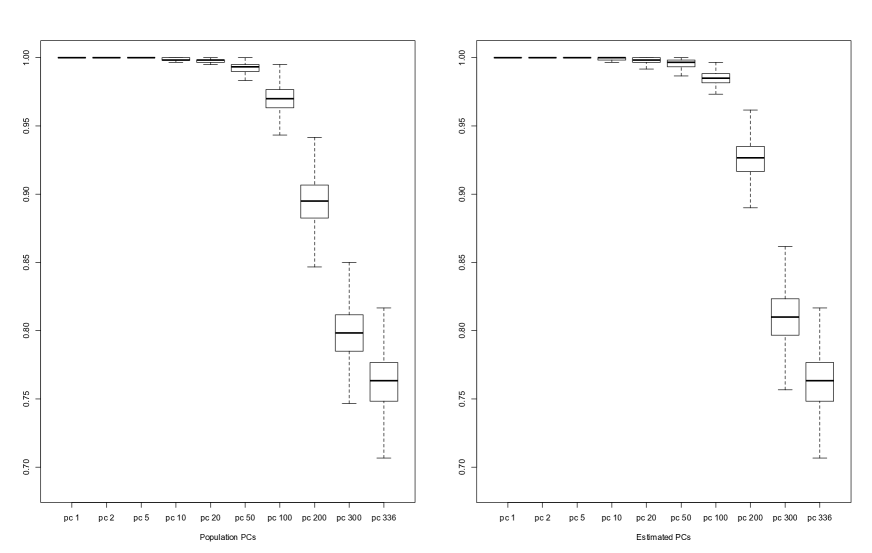

Indeed, the first principal component explains about 63% of the variance of the 336 original variables and about 83% of the total variability of the data is preserved by projection onto the subspace span by the first ten principal components.

Comparison of the estimators

To make comparisons, we draw samples of size (the sampling fraction is about )

according to a simple random sampling design without replacement and we estimate the total consumption over each day of the second week with the following estimators:

•

Horvitz-Thompson estimators,

•

Calibration estimators, denoted by ,

that take account of all the auxiliary variables plus the intercept term.

•

Estimators calibrated on the principal components in the population or in the sample plus the constant term, denoted by ,

for different values of the dimension .

When performing principal components calibration, the dimension plays the role of a tuning parameter. We also study the performances of an automatic and simple rule for selecting the dimension and consider estimators based on principal components calibration with a data-driven choice of the tuning parameter which consists in selecting the largest dimension such that all the estimated principal component weights remain positive. Note that this selection strategy is the analogue of the strategy suggested in Bardsley and Chambers (1984) for choosing the tuning parameter in a ridge regression context.

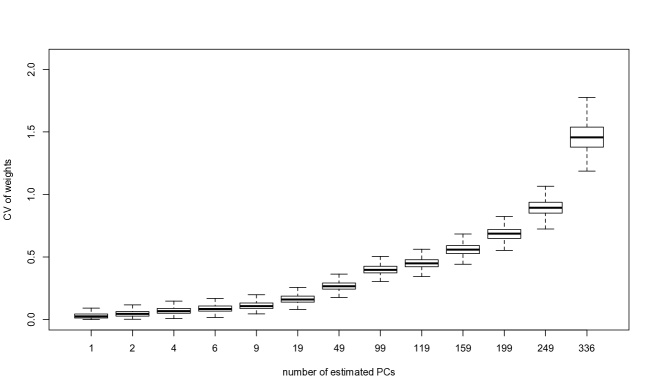

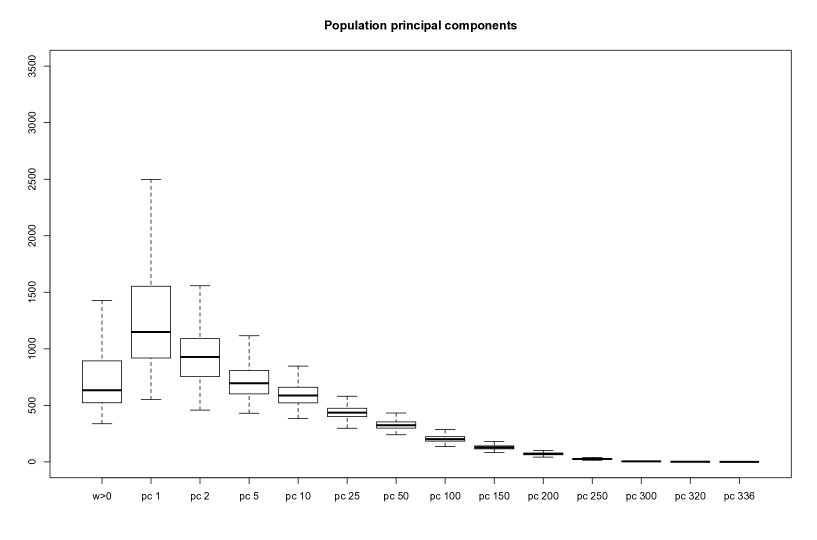

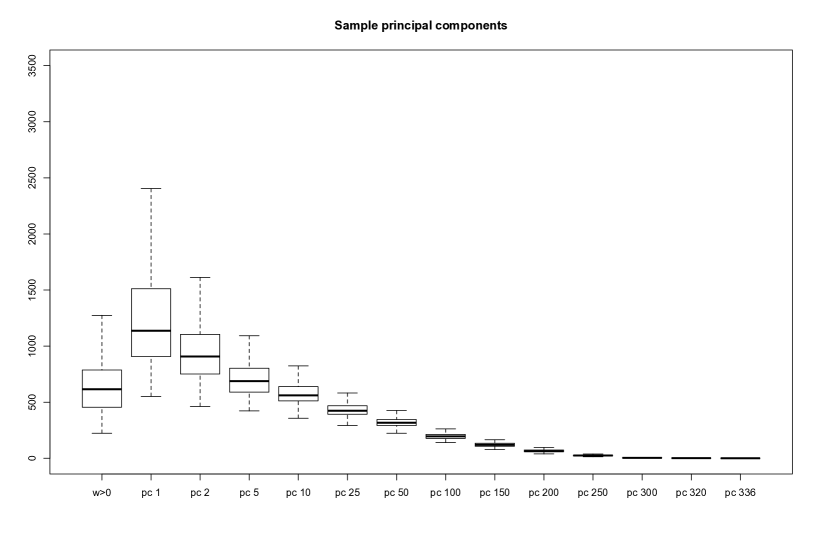

Figure 7.1: A sample of 5 electricity load curves observed every half an hour during the first week.Figure 7.2: Distribution of the coefficient of variation (CV) of the sampling weights for different values of the dimension . The sample size is .

The distribution of the coefficient of variation (CV) of the calibration weights for the =1000 Monte Carlo experiments is presented in Figure 7.2 for different values of the dimension . Recall that these weights do not depend on the variable of interest. It is clearly seen that those calibration weights have larger dispersion and are more and more heterogeneous as the number of principal components used for calibration increases. Calibrating with a large number of correlated auxiliary variables may lead to instable estimations and to a lack of robustness with respect to measurement errors or misspecification in the data bases, with for example the presence of strata jumpers. Note also that when all the auxiliary variables are used for calibration, around 25 % of the sampling weights take negatives values which is generally not desirable. The distribution of the proportion of positive sampling weights are given in Figure 7.3. It can be seen the proportion of negative weights increases as the number of dimension increases. Note also that it is slightly smaller for the estimated principal components.

Figure 7.3: Proportion of positive calibrated weights for different values of the dimension . On the right for calibration on the population principal components and on left for the sample principal components.

Our benchmarks are the estimators which are calibrated on all the auxiliary variables. For each day , the performances of an estimator of the total are measured by considering the relative mean squared error,

(7.1)

Days

Estimators

monday

tuesday

wednesday

thursday

friday

saturday

sunday

Horvitz-Thompson

14.4

13.9

11.8

10.8

12.5

6.4

5.4

0.65

0.62

0.50

0.47

0.64

1.17

1.57

0.64

0.62

0.50

0.47

0.57

0.80

0.63

0.52

0.47

0.40

0.50

0.51

0.53

0.52

0.50

0.50

0.43

0.44

0.54

0.48

0.48

0.57

0.60

0.59

0.51

0.58

0.60

0.64

0.60

0.64

0.58

0.66

0.69

0.68

0.63

0.82

0.85

0.83

0.86

0.84

0.85

0.87

0.75

0.73

0.61

0.56

0.73

1.23

1.59

0.66

0.64

0.53

0.50

0.61

0.85

0.74

0.53

0.47

0.40

0.41

0.53

0.59

0.53

0.45

0.46

0.40

0.41

0.48

0.46

0.47

0.46

0.47

0.42

0.45

0.52

0.49

0.50

0.57

0.55

0.51

0.58

0.62

0.60

0.57

0.78

0.80

0.77

0.84

0.80

0.81

0.83

,

0.51

0.49

0.41

0.41

0.52

0.55

0.50

,

0.49

0.48

0.41

0.40

0.50

0.53

0.49

Ridge Calibration

0.44

0.46

0.40

0.41

0.48

0.48

0.43

Table 7.1: Comparison of the mean relative mean squared errors of the different estimators, according to criterion (7.1).

Better estimators will correspond to small values of criterion .

The values of this relative error for several values of , as well as for the estimators obtained with the data driven dimension selection are given in Table 7.1. This relative error has also been computed for the ridge-type estimators derived with the sampling weights given in Section 2 and a penalty chosen to be the smallest value of such that all the resulting weights remain positive.

We can first note that the naive Horvitz-Thompson estimator can be greatly improved, for all the days of the week, by considering an over-calibration estimator which takes account of all the (redundant) auxiliary information. Indeed, the mean square error of the HT estimator is between five times and fourteen times larger than the MSE of this reference estimator.

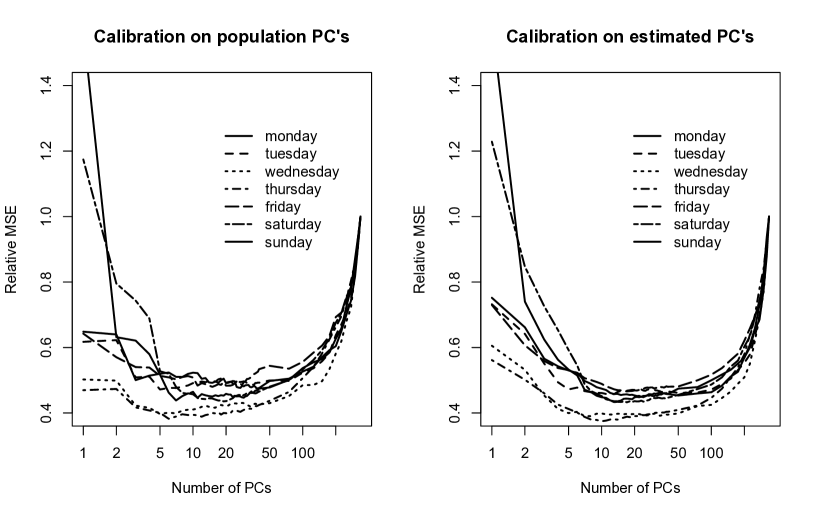

We can also remark that reducing the number of effective auxiliary variables through principal components, estimated on the sample or deduced from the population, can still improve estimation compared to calibration on all the variables and permits to divide by two the MSE. In Figure 7.4 the MSE is drawn for all the seven considered days and various dimensions starting from to . Note that the largest dimension corresponds to the estimators calibrated on all the original variables.

A remarkable feature is the stability of the principal components calibration techniques with respect to the choice of the dimension . Indeed, in this application, choosing between 5 and 100 principal components permits to divide by two, for all the outcome variables, the MSE compared to the calibration estimator based on the whole auxiliary information.

We noted that the mean number of selected principal components with the data driven selection rule is equal to 17.3 for the population principal components and 21.3 for the sample principal components, explaining in each case about 85% of the variance of the original variables.

As expected, the variability of the number of selected components is slightly larger when considering calibration on the estimated principal components (interquartile range of 26 versus 17 for the population principal components).

As seen in Table 7.1, the performances of the resulting estimators are good and comparable to the estimators based on ridge calibration with a selection rule for based on the same principle. The advantage of the principal components is that it permits to divide by more than 15 the final number of effective variables used for calibration and it can directly be used in classical survey sampling softwares.

Figure 7.4: Relative MSE, defined in (7.1), for different values of the dimension and the different days of the week and a sample size of for calibration estimators based on the population (left) and the sample (right) principal components. The horizontal axis is at a log scale.

Finally, we have also evaluated the calibration error. It is the difference between the total of the original auxiliary variables and their "estimation" on the samples obtained with the weights defined in (3.3) and the weights defined in (4.3). The distribution the estimation squared calibration error is drawn in Figure 7.5 (resp. Figure 7.6) for calibration on principal components at the population level (resp. for the estimated principal components). We have also plotted the distribution (first boxplot) of the squared error for the weight obtained with the data driven choice of the dimension . For both approaches, the distributions of the errors are very similar. The errors are high and highly variable when the number of principal components is small (a mean value of about 1300 for ) and then they decrease rapidly (a mean value of 720 for and 600 for ). For larger values of , the decrease is slower. When the dimension is not chosen in advance, the mean value is about at the level of the error when is equal to but with a variability that is much larger.

Figure 7.5: Calibration error for the original variables, in terms of MSE, for different number of principal components estimated at the population level. The first boxplot () corresponds to the data-driven choice of the number of components.Figure 7.6: Calibration error for the original variables, in terms of MSE, for different number of principal components estimated in the sample. The first boxplot () corresponds to the data-driven choice of the number of components.

8. Discussion and concluding remarks

A simple dimension reduction technique based on principal components calibration has been studied in this article. It provides an effective technique for approximate calibration, when the number of auxiliary variables is large, that can improve significantly the estimation compared to calibration on the whole set of initial auxiliary variables. Furthermore this simple technique can also be modified so that calibration can be exact for a set of a few important auxiliary variables.

A very simple rule which consists in choosing the largest number of principal components such that all the resulting sampling weights remain positive allows to construct estimators with very good performances in terms of MSE. Furthermore, in our case study, this automatic selection technique allows, in average, to divide by 15 the number of effective calibration variables and to reduce by a half the mean squared error of estimation compared to calibration over all the auxiliary variables.

Some asymptotic justifications of this dimension reduction technique are given with a number of auxiliary variables as well as a number of principal components used for calibration that are allowed to grow to infinity as the population size increases. Nevertheless, our conditions on the asymptotic behavior of appear to be rather restrictive and could probably be relaxed (see for example the results presented in Vershynin, 2012 on the estimation of covariance matrices for independent observations in a infinite population). However, this would require to have at hand exponential inequalities for Horvitz-Thompson estimators in order to control in very accurately their deviations around their target. This difficult issue, in a finite population context, is clearly beyond the scope of this paper but certainly deserves further investigation.

Note finally that borrowing ideas from Marx and Smith (1990) and Wu and Sitter (2001), it would be not too difficult to extend the principal component calibration approach in order to deal with non linear model-calibration.

Acknowledgements. The authors thank an associate editor and the anonymous referees for comments and suggestions, and more particularly for suggesting the data-driven rule for selecting the number of components.

References

Bardsley, P. and Chambers, R. (1984). Multipurpose estimation from unbalanced samples. Applied Statistics, 33, 290-299.

Beaumont, J.-F. and Bocci, C. (2008). Another look at ridge calibration.

Metron-International Journal of Statistics, LXVI: 5-20.

Bosq, D. (2000). Linear processes in function spaces. Lecture Notes in Statistics, Vol. 149. Springer-Verlag.

Breidt, J.F. and Opsomer, J. D.(2000). Local polynomial regression estimators in survey sampling. Ann. Statist., 28, 1023-1053.

Breidt, J.F. and Chauvet, G. (2012). Penalized balanced sampling. Biometrika, 99, 945-958.

Cardot, H., Chaouch, M., Goga, C. and Labruère, C. (2010). Properties of design-based functional principal components analysis. Journal of Statistical and Planning Inference, 140, 75-91.

Cassel, C., Särndal, C.-E. and Wretman, J. (1976). Some results on generalized difference estimation and generalized regression estimation for finite populations. Biometrika, 63, 615-620.

Chambers, R.L. (1996). Robust case-weighting for multipurpose establishment surveys. Journal of Official Statistics,12, 3-32.

Chambers, R., Skinner, C. and Wang, S. (1999). Intelligent calibration. Bulletin of the International Statistical Institute, 58(2), 321-324.

Chen, J., Sitter, R.R. and Wu, C. (2002). Using empirical likelihood methods to obtain range restricted weights in regression estimators for surveys. Biometrika, 89, 230-237.

Clark, R. G. and Chambers, R.L. (2008). Adaptive calibration for prediction of finite population totals. Survey Methodology, 34, 163-172.

Deville, J.C. and Särndal, C.E. (1992). Calibration estimators in survey sampling. J. Amer. Statist. Assoc., 87, 376-382.

Frank, I.E. and Friedman, J.H. (1993). A statistical view of some chemometrics regression tools. Technometrics, 35, 109-148.

Goga, C., Shehzad, M.A., and Vanheuverzwyn, A. (2011). Principal component regression with survey data. application on

the french media audience. Proceedings of the 58th World Statistics Congress of the International Statistical Institute, Dublin, Ireland, 3847-3852.

Goga, C. and Shehzad, M.A. (2014). A note on partially penalized calibration. Pakistan Journal of Statistics, 30(4), 429-438.

Guggemos, F. and Tillé, Y. (2010). Penalized calibration in survey sampling: Design-based estimation assisted by mixed models.

Journal of Statistical Planning and Inference, 140, 3199-3212.

Gunst, R.F. and Mason, R.L. (1977). Biased estimation in regression: an evaluation using mean squared error.

J. Amer. Statist. Assoc., 72, 616-628.

Hoerl, E. and Kennard, R. W. (1970). Ridge Regression: Biased Estimation for Nonorthogonal Problems. Technometrics, 12, 55-67.

Isaki, C. and Fuller, W. (1982). Survey design under the regression superpopulation model.

J. Amer. Statist. Assoc., 77, 49-61.

Jolliffe, I.T. (2002). Principal Components Analysis. Second Edition, Springer- Verlag. New York.

Rao, J.N.K. and Singh, A.C. (1997). A ridge-shrinkage method for range-restricted weight calibration in survey sampling.

Proceedings of the Section on Survey Research Methods, American Statistical Association, 57-65.

Ren, R. (2000). Utilisation de l’information auxiliaire par calage sur fonction de répartition. PhD, Université Paris Dauphine, France.

Särndal, C.E., Swensson, B., and Wretman J. (1992). Model Assisted Survey Sampling. Springer-Verlag, New York Inc.

Särndal, C.E. (2007). The calibration approach in survey theory and practice. Survey Methodology, 33, 99-119.

Shehzad, M.-A. (2012). Penalization and auxiliary information reduction methods in surveys. Doctoral dissertation, Université de Bourgogne, France.

Available at http://tel.archives-ouvertes.fr/tel-00812880/.

Silva, P.L.N. and Skinner, C. (1997). Variable selection for regression estimation in finite populations. Survey Methodology, 23, 23-32.

Singh, A. C. and Mohl, C. (1996). Understanding calibration in survey sampling. Survey Methodology, 22, 107-115.

Swold, S., Sjöström, M. and Eriksson, L. (2001). PLS-regression : a basic tool of chemometrics. Chemometrics and Intelligent Laboratory,

58, 109-130.

Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. J. Roy. Statist. Soc. Ser. B, 58, 267-288.

Théberge, A. (2000). Calibration and restricted weights. Survey Methodology, 26, 99-107.

Vershynin, R. (2012). How close is the sample covariance matrix to the actual covariance matrix?

J. Theoret. Probab.25, 655-686.

Wu, C. and Sitter, R. R. (2001). A Model-Calibration Approach to Using Complete Auxiliary Information from Survey Data. J. Amer. Statist. Assoc., 96, 185-193.

Zou, H. and Hastie, T. (2005). Regularization and variable selection via the Elastic Net. J. Roy. Statist. Soc. Ser. B, 67, 301-320.

Cardot, H.

IMB, UMR CNRS 5584, Université de Bourgogne, 9 avenue Alain Savary, Dijon, France

herve.cardot@u-bourgogne.fr

Goga, C.

IMB, UMR CNRS 5584, Université de Bourgogne, 9 avenue Alain Savary, Dijon, France

camelia.goga@u-bourgogne.fr

Shehzad, M.-A.

Bahauddin Zakariya University, Bosan Road Multan, Pakistan.

mdjan708@gmail.com

Appendix : Proofs

Throughout the proofs, we use the letter C to denote a generic constant whose value may vary from place to place. This constant does not depend on N. For sake of clarity, subscript N has been suppressed when there were no ambiguity.

For a vector , we denote by its Euclidean norm. The spectral norm of a matrix is denoted by . We often use the following well known inequality, as well as the equality .

Proof of Proposition 1

We may write

(8.1)

where

(8.2)

We get by linearity of the Horvitz-Thompson estimators, that

(8.3)

By construction, the new real variable is a projection and we have that

Consequently, we get with (8.3) and with classical properties of Horvitz-Thompson estimators (and because assumptions (A1) and (A2) hold) that

(8.4)

Recall that , and

By definition of the principal components and assumption (A5) we have that .

Following the same lines as in Breidt and Opsomer (2000), we obtain with assumptions (A1)-(A5) that

(8.5)

It remains to bound . For that, we first bound the estimation error of . Considering the spectral norm for square matrices, we have for some constant , with classical algebra (see e.g. Cardot et al. 2010, Proposition 1),

(8.6)

Expanding now each in the eigenbasis , we have

and thus

(8.7)

thanks to assumption (A6). We deduce from (8.6) and (8.7) that

(8.8)

Note that as in Cardot et al. (2010), we can deduce from previous upper bounds that

(8.9)

and

(8.10)

An application of Cauchy-Schwarz inequality as well as the bound obtained in (8.7), gives with assumptions (A1)-(A6) that there is some constant such that

(8.11)

Note finally, that we have for some constant

(8.12)

because the largest eigenvalue of the non negative matrix is equal to and is supposed to be bounded.

Finally, using again decomposition (8.1), we get with previous bounds

(8.15)

Proof of Proposition 2

The proof follows the same lines as the proof of Proposition 1. We first write

(8.16)

and note that, as in Proposition 1, we have that .

We now look for an upper bound on the second term at the right-hand side of equality (8.16). It can be shown easily that .

We can also write

(8.17)

and bound each term at the right-hand side of the equality.

We denote by the matrix whose columns are the orthonormal eigenvectors of

associated to the largest eigenvalues, . Note that these eigenvectors are unique up to sign change and, for , we choose such that .

Since are orthonormal vectors, the spectral norm . This is also true for , and we have .

Now, using the fact that and , it can be shown that

(8.18)

We deduce with Lemma 4.3 in Bosq (2000) and equation (8.18) that

(8.19)

and

(8.20)

with and for .

Consequently,

with (8.18), (8.20) and the fact that which comes from the fact that we have supposed that with .

Employing a similar technique as before (see the bound obtained in (8.10)), we also get that

(8.22)

and

Using the inequality for any symmetric non negative matrices and , we also have

because and the largest eigenvalue of the non negative matrix is equal to . Note also that , for some constant , because is supposed to be bounded and (see Assumption A2).

We can now bound . Combining previous inequalities, we have

(8.23)

Let us study now . Writing , we have

because the largest eigenvalue of the non negative matrix is equal to . Since is supposed to be bounded, we obtain

(8.24)

On the other hand, noting that denoting by , we have that

(8.25)

Combining (8.24) and (8.25), we finally obtain that

(8.26)

Hence, using now a decomposition similar to (8.13), we obtain

(8.27)

Combining previous bounds we get

and using again decomposition (8.16), we finally get