On the Log Quantile Difference of the Temporal Aggregation of a Stable Moving Average Process

A. W. Barker

Department of Statistics, Macquarie University, Sydney, NSW 2109 Australia

Abstract

A formula is derived for the log quantile difference of the temporal

aggregation of some types of stable moving average processes, MA(q). The

shape of the log quantile difference as a function of the aggregation level

is examined and shown to be dependent on the parameters of the moving

average process but not the quantile levels. The classes of invertible,

stable MA(1) and MA(2) processes are examined in more detail.

keywords:

Quantile , Stable Distribution , Temporal Aggregation

††journal: Statistics and Probability Letters

1 Introduction

We recall some basic facts and definitions about stable moving average

processes, temporal aggregation and log quantile differences.

1.1 Stable Moving Average Processes

Let be the moving average process of order

(1)

where and is an independently and

identically distributed (iid) sequence of stable random variables such that

(2)

using the parameterisation of stable distributions in Nolan (1998).

Let denote the dimensional vector of moving average

parameters

(3)

In and the remainder of this paper, with the

addition of various subscripts or superscripts, we use and to denote respectively the stability, skewness,

scale and location parameters of a stable distribution. The

parameterisation has the following useful properties.

(P1)

If

then for any

(4)

(P2)

If are pairwise independent and

for then where

(5)

and

(6)

Properties (P1) and (P2) for were given in Nolan (1998). The

extension of Property (P2) to general is a straightforward induction.

1.2 Temporal Aggregation

The temporal aggregation of the stochastic process

is generally defined as the weighted sum of past and current process values.In this paper, we consider only a special case of temporal aggregation,

sometimes referred to as flow aggregation, where all the weights equal

The flow aggregation of is given by

(7)

Henceforth, we refer to as the

temporal aggregation of or the aggregated process,

to as the aggregation level and to as the base

process.

We note that a moving average process is the temporal aggregation of an iid

process and that the temporal aggregation of a moving average process is

also a moving average process. A recent survey on temporal aggregation

can be found in Silvestrini and Veredas (2008).

1.3 Log Quantile Difference

Let denote the pth quantile of some distribution function. At

quantile levels such that , we define the

log quantile difference to be

(8)

We assume for the remainder of this paper, that any random variable on which

a log quantile difference is calculated has a positive density at and This assumption implies uniqueness of the

quantiles and and that the log quantile

difference is finite. Let us recall that the stable distributions satisfy

this condition.

2 Log Quantile Difference of the Temporal Aggregation of a Stable

Moving Average Process

Let be the moving average process of order

defined in with stable innovations let denote the

temporal aggregation of at aggregation level

and let and denote respectively the log quantile

difference of and at quantile levels In this section, we show

under certain conditions on that

(9)

where

(10)

We start with a general result which applies to all stable moving average

processes.

Theorem 1

The distribution of the aggregated process is given by

(11)

where

(12)

if

if

and

(15)

Proof. From the definition of the aggregated process we have for that

(16)

where is given by An application of

properties (P1) and (P2) proves the theorem.

Whilst Theorem 1 provides formulae for the stable distribution

parameters of the aggregated process, in general it is not possible to

derive from these a formula for the log quantile difference of the

aggregated process. However, we can derive such a formula for those

processes where To

achieve this, we make use of the following lemma, which shows how the log

quantile difference of a random variable is affected by linear

transformations.

Lemma 2

Suppose is a random variable and for some

and Let and denote respectively the pth quantile of

and then

(17)

Let and denote

respectively the log quantile difference of and at quantile levels then

(18)

Proof. By assumption we have

(19)

which proves and follows immediately.

We can now prove the formula for

in under certain conditions on the base

process, .

Theorem 3

If the base process satisfies

either

(A1)

(20)

or

(A2)

(21)

then for the log quantile difference is given by the formula in .

Proof. From Theorem 1, we have for that the aggregated

process, has a stable

distribution given by

(22)

where and are as shown in and

or . If

(A2) is satisfied, then all the terms in are non-negative and so

(23)

Note that implies that Thus, if either (A1) or (A2) is satisfied,

then

(24)

and is a scale and location

transformation of the innovations Thus

Although for our purposes the formula for in is only valid for integer

values of nonetheless it is a function of which is

well-defined for all real positive values of Formally, we can take

partial derivatives of with

respect to to get for

(27)

and

(28)

and draw conclusions on the shape of .

Corollary 4

Let be a MA(q) process satisfying

the conditions of Theorem 3. Then

(29)

For ,

(30)

and therefore

(31)

Remark 5

If and any of the

terms in are negative, then In that case, and consequently do not

hold. In general, equality relations for the quantiles of the sums of random

variables in terms of the quantiles of the summands are difficult to

achieve. (Watson and Gordon (1986), Liu and David (1989))

Remark 6

In the special case where is iid,

we have

(34)

and the expression for in reduces to

(35)

Note that the expressions for in are different from those derived in Section 2.2 of

Chan et al. (2008) which the author believes to be in error.

Remark 7

The derivatives in and and therefore the results of Corollary 4 do not depend on for all and all

In the next section we examine Corollary 4 in more detail for

the special cases of invertible MA(1) and MA(2) processes.

3 Invertible Stable MA(1) and MA(2) Processes

An invertible MA(q) process is one where all roots of the polynomial

(36)

lie outside the complex unit circle, . The

region of

in which invertible parameters reside is referred to as the

invertibility region. The invertibility region of MA(1) processes is the

set

(37)

The invertibility region of MA(2) processes is the set

(38)

Expressions for the invertibility region of higher order MA

processes can be found in Wise (1956). In this section we identify regions

of the invertibility region of MA(1) and MA(2) processes where is either positive, zero or negative for various

values of To conduct this analysis we require the following lemma.

Lemma 8

(39)

Proof. If a function is strictly convex on , then from

Jensen’s inequality for

(40)

The relations in are proved by applying to the function for and to the function for .

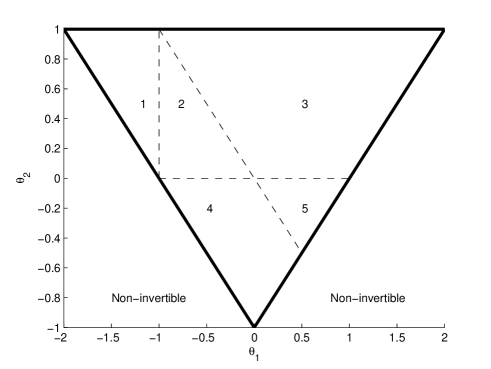

To assist this analysis we divide the invertibility region for an MA(2)

process into 5 sub-regions as shown in Figure 1. These

sub-regions are defined as open sets, so that the entire invertibility

region consists of the union of the 5 sub-regions, the borders between them

and the origin. The inequalities defining these sub-regions are listed in

Sub-region 1 =

Sub-region 2 =

Sub-region 3 =

Sub-region 4 =

Sub-region 5 =

(41)

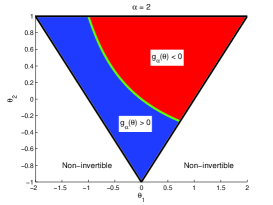

Figure 1: The 5 sub-regions of the invertibility region of an MA(2) process.

Remark 9

For an invertible MA(2) process, the set of values of which satisfy condition (A2) in

Theorem 3 consists of sub-region 3 and its borders with

sub-regions 2 and 5.

The following theorem provides some properties of for in sub-region 3.

Theorem 10

If is an element of sub-region 3, then the

function satisfies the following

relations

(42)

Proof. By definition for we have,

(43)

All in sub-region 3 satisfy so using

Lemma 8 we get for

(44)

All in sub-regions 3, satisfy and

so using Lemma 8 we get for

(45)

Therefore, for all in sub-region 3 and for we have

that is the sum of two strictly positive

terms and so is strictly positive.

Similarly, for all in sub-region 3 and for we have

that is the sum of two zero terms and so

is zero. Finally, for all in sub-region 3 and for

we have that is the sum of two strictly

negative terms and so is strictly negative.

Theorems similar to Theorem 10 for the other sub-regions and the

borders between the sub-regions can be proven using the same approach. To

cover all the sub-regions and borders of the invertibility region of an

MA(2) process requires several such theorems. These are straightforward and

are omitted from this paper.

A sub-region is said to be positive, zero or negative for a given

if is respectively positive, zero or

negative for all points in the sub-region. A sub-region is said to be mixed

for a given if there exist some points in the sub-region for which

is positive and other points for which is negative. Similar descriptions are

used to describe the borders between the sub-regions. In Tables 1 and 2 we present a categorisation of all the

sub-regions and the borders between the sub-regions using these

descriptions.

Positive Sub-regions

All

1,2,4,5

1,4

Zero Sub-regions

None

3

None

Negative Sub-regions

None

None

3

Mixed Sub-regions

None

None

2,5

Table 1: Categorisation of the sub-regions of the invertibility region of an MA(2) process into positive, zero,

negative and mixed sub-regions with respect of g.

Positive Borders

All

Zero Borders

None

None

Negative Borders

None

None

Table 2: Categorisation of the borders between the sub-regions of the invertibility region of an MA(2) process into

positive, zero and negative borders with respect of g.

We use (a,b) to denote the border between sub-regions a and b.

The set of invertible MA(1) processes is equivalent to the borders

sub-regions 2 and 4 and between sub-regions 3 and 5.

For iid processes for all

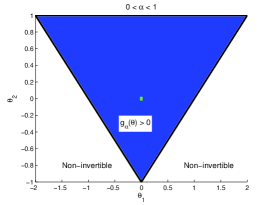

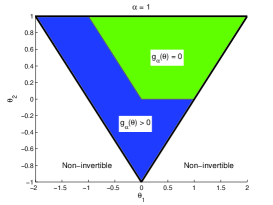

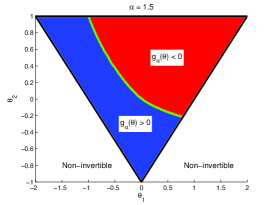

. It is perhaps helpful to see the results of Tables 1 and 2 in graphical form as provided in Figure 2.

(a)

(b)

(c)

(d)

Figure 2: A graphical display of the categorisation of the invertibility region of MA(2) processes into

positive (blue), zero (green) and negative (red) sub-regions for (a) , (b) = 1.0,

(c) = 1.5 and (d) = 2.0.

Figure 2(a) is applicable to for

any Whilst Figures 2(c) and 2(d) appear similar, the locations of the respective green

lines, i.e. the sets

(46)

are not the same.

Remark 11

For an MA(2) process, it is straightforward to show that

(47)

For closed form expressions for have

not been obtained except to note that contains the

points and Strictly

is on the border of, but not in the invertibility region.

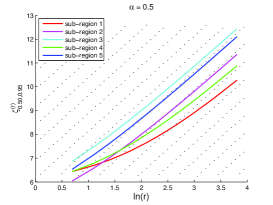

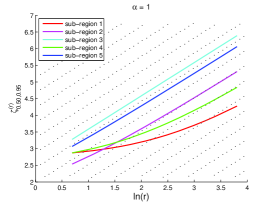

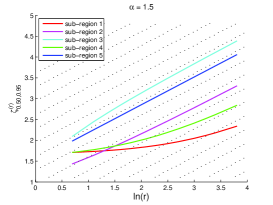

To illustrate the behaviour of

where lie in different sub-regions of the invertibility region, we

present plots of for various

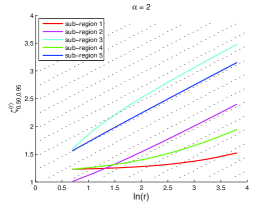

combinations of and in Figure 3.

(a)

(b)

(c)

(d)

Figure 3: Plots of against the logarithm of the aggregation level for various

symmetric stable MA(2) processes satisfying the conditions on Theorem 1.

For each sub-figure in Figure 3, we choose for sub-region 1:

(,) = (-1.4,0.6),

sub-region 2: (,) = (-0.5,0.2),

sub-region 3: (,) = (0.2,0.9),

sub-region 4: (,) = (-0.2,-0.4) and

sub-region 5: (,) = (0.7,-0.2).

The dotted parallel lines in Figure 3 have a slope .

As shown in Corollary 4, for each choice of

in Figure 3, it can be seen that the plot of

against is concave, linear

or convex wherever is negative, zero or

positive and that the sign of agrees

with the results in Table 1. In all cases the derivative approaches with increasing The convergence of the derivative to can

be much slower in the positive sub-regions than in the negative sub-regions.

The example shown in Figure 3(d) for and

sub-region 1, still has a derivative much less than at an aggregation

level of .

Acknowledgement

The author would like to thank Dr N. Kordzakhia and A/Prof A. Kozek for

their comments on this paper.

References

Chan et al. (2008)

Chan, W., Cheung, S.,

Zhang, L., Wu, K., 2008.

Temporal aggregation of equity return time series

models.

Mathematics and Computers in Simulation

78, 172–180.

Liu and David (1989)

Liu, J., David, H., 1989.

Quantiles of sums and expected values of ordered

sums.

Australian Journal of Statistics

31, 469–474.

Nolan (1998)

Nolan, J., 1998.

Parameterizations and modes of stable distributions.

Statistics and Probability Letters

38, 187–195.

Silvestrini and Veredas (2008)

Silvestrini, A., Veredas, D.,

2008.

Temporal aggregation of univariate and multivariate

time series models: A survey.

Journal of Economic Surveys 22,

458–497.

Watson and Gordon (1986)

Watson, R., Gordon, I.,

1986.

On quantiles of sums.

Australian Journal of Statistics

28, 192–199.

Wise (1956)

Wise, J., 1956.

Stationarity conditions for stochastic processes of

the autoregressive and moving-average type.

Biometrika 43,

215–219.