Fast Estimation of Multinomial Logit Models:

\proglangR Package \pkgmnlogit

Asad Hasan, Zhiyu Wang, Alireza S. Mahani \PlaintitleFast Estimation of Multinomial Logit Models: R Package mnlogit \ShorttitleFast Estimation of Multinomial Logit Models: \proglangR package \pkgmnlogit \Abstract

We present \proglangR package \pkgmnlogit for training multinomial logistic regression models, particularly those involving a large number of classes and features.

Compared to existing software, \pkgmnlogit offers speedups of 10x-50x for modestly sized problems and more than 100x for larger problems.

Running in parallel mode on a multicore machine gives upto 4x additional speedup on 8 processor cores.

\pkgmnlogit achieves its computational efficiency by drastically speeding up computation of the log-likelihood function’s Hessian matrix through exploiting structure in matrices that arise in intermediate calculations.

\Keywordslogistic regression, multinomial logit, discrete choice, large scale, parallel, econometrics

\Plainkeywordslogistic regression, multinomial logit, discrete choice, large scale, parallel, econometrics \Address

Asad Hasan

Scientific Computing Group

Sentrana Inc.

1725 I St NW

Washington, DC 20006

E-mail:

Zhiyu Wang

Department of Mathematical Sciences

Carnegie Mellon University

5000 Forbes Ave

Pittsburgh, PA 15213

Alireza S. Mahani

Scientific Computing Group

Sentrana Inc.

1725 I St NW

Washington, DC 20006

E-mail:

1 Introduction

Multinomial logit regression models, the multiclass extension of binary logistic regression, have long been used in econometrics in the context of modeling discrete choice (MCFAD:74; Bhat, 1995; TRAIN:03) and in machine learning as a linear classification technique (HastieTibBook) for tasks such as text classification (Nigam1999). Training these models presents the computational challenge of having to compute a large number of coefficients which increases linearly with the number of classes and the number of features. Despite the potential for multinomial logit models to become computationally expensive to estimate, they have an intrinsic structure which can be exploited to dramatically speedup estimation. Our objective in this paper is twofold: first we describe how to exploit this structure to optimize computational efficiency, and second, to present an implementation of our ideas in our \proglangR (Rlang) package \pkgmnlogit which is available from CRAN at: http://cran.r-project.org/web/packages/mnlogit/index.html.

An older method of dealing with the computational issues involved in estimating large scale multinomial logistic regressions has been to approximate it as a series of binary logistic regressions (BeggandGray, 1984). In fact the \proglangR package \pkgmlogitBMA (mlogitBMA) implements this idea as the first step in applying Bayesian model averaging to multinomial logit data. Large scale logistic regressions can, in turn, be tackled by a number of advanced optimization algorithms (KomarekMoore; LinLogistic2009). A number of recent \proglangR packages have focussed on slightly different aspects of estimating regularized multinomial logistic regressions. For example: package \pkgglmnet (glmnet) is optimized for obtaining the entire -regularized paths and uses the coordinate descent algorithm with ‘warm starts’, package \pkgmaxent (JurkaMaxent) is intended for large text classification problems which typically have very sparse data and the package \pkgpmlr (pmlr) which penalizes the likelihood function with the Jeffreys prior to reduce first order bias and works well for small to medium sized datasets. There are also \proglangR packages which estimate plain (unregularized) multinomial regression models. Some examples are: the \pkgVGAM package (VGAM), the \codemultinom function in package \pkgnnet (nnet) and package the \pkgmlogit (mlogit).

Of all the \proglangR packages previously described, \pkgmlogit is the most versatile in the sense that it handles many data types and extensions of multinomial logit models (such as nested logit, heteroskedastic logit, etc.). These are especially important in econometric applications, which are motivated by the utility maximization principle (MCFAD:74), where one encounters data which depends upon both the observation instance and the choice class. Our package \pkgmnlogit provides the ability of handling these general data types while adding the advantage of very quick computations. This work is motivated by our own practical experience of the impossibility of being able to train large scale multinomial logit models using existing software.

In \pkgmnlogit we perform maximumum likelihood estimation (MLE) using the Newton-Raphson (NR) method. We speed up the NR method by exploiting structure and sparsity in intermediate data matrices to achieve very fast computations of the Hessian of the log-likelihood function. This overcomes the NR method’s well known weakness of incurring very high per-iteration cost, compared to algorithms from the quasi-Newton family (Nocedal1992; Nocedal1990). Indeed classical NR estimations of multinomial logit models (usually of the Iteratively Reweighted Least Square family) have been slow for this very reason. On a single processor our methods have allowed us to achieve speedups of 10x-50x compared to \pkgmlogit on modest-sized problems while performing identical computations. In parallel mode111Requires \pkgmnlogit to be compiled with OpenMP support (usually present by default with most \proglangR installations, except on Mac OS X)., \pkgmnlogit affords the user an additional speedup of 2x-4x while using up to 8 processor cores.

We provide a simple formula-based interface for specifiying a varied menu of models to \pkgmnlogit. Section 2 illustrates aspects of the formula interface, the expected data format and the precise interpretations of variables in \pkgmnlogit. To make the fullest use of \pkgmnlogit we suggest that the user understand the simple \proglangR example worked out over the course of this section. Section 3 and Appendix A contain the details of our estimation procedure, emphasizing the ideas that underlie the computational efficiency we achieve in \pkgmnlogit. In Section 4 we present the results of our numerical experiments in benchmarking and comparing \pkgmnlogit’s performance with other packages while Appendix C has a synopsis of our timing methods. Finally Section 5 concludes with a short discussion and a promising idea for future work.

2 On using \pkgmnlogit

The data for multinomial logit models may vary with both the choice makers (‘individuals’) and the choices themselves. Besides, the modeler may prefer model coefficients that may (or may not) depend on choices. In \pkgmnlogit we try to keep the user interface as minimal as possible without sacrificing flexibility. We follow the interface of the \codemlogit function in package \pkgmlogit. This section describes the \pkgmnlogit user interface, emphasizing data preparation requirements and model specification via an enhanced formula interface. To start, we load the package \pkgmnlogit in an \proglangR session: {Schunk} {Sinput} R> library("mnlogit")

2.1 Data preparation

mnlogit accepts data in the ‘long’ format which requires that if there are choices, then there be rows of data for each individual (see also Section 1.1 of the \pkgmlogit vignette). Here is a snapshot from data in the ‘long’ format on choice of recreational fishing mode made by 1182 individuals: {Schunk} {Sinput} R> data("Fish", package = ’mnlogit’) R> head(Fish, 8) {Soutput} mode income alt price catch chid 1.beach FALSE 7083.332 beach 157.930 0.0678 1 1.boat FALSE 7083.332 boat 157.930 0.2601 1 1.charter TRUE 7083.332 charter 182.930 0.5391 1 1.pier FALSE 7083.332 pier 157.930 0.0503 1 2.beach FALSE 1250.000 beach 15.114 0.1049 2 2.boat FALSE 1250.000 boat 10.534 0.1574 2 2.charter TRUE 1250.000 charter 34.534 0.4671 2 2.pier FALSE 1250.000 pier 15.114 0.0451 2 In the ‘Fish’ data, there are 4 choices (‘beach’, ‘boat’, ‘charter’, ‘pier’) available to each individual: labeled by the ‘chid’ (chooser ID). The ‘price’ and ‘catch’ column show, respectively, the cost of a fishing mode and (in unspecified units) the expected amount of fish caught. An important point here is that this data varies both with individuals and the fishing mode. The ‘income’ column reflects the income level of an individual and does not vary between choices. Notice that the snapshot shows this data for two individuals.

The actual choice made by an individual, the ‘response’ variable, is shown in the column ‘mode’. \pkgmnlogit requires that the data contain a column with exactly two categories whose levels can be coerced to integers by \codeas.numeric(). The greater of these integers is automatically taken to mean \codeTRUE.

The only other column strictly mandated by \pkgmnlogit is one listing the names of choices (like column ‘alt’ in Fish data). However if the data frame is an \codemlogit.data class object, then this column maybe omitted. In such cases \pkgmnlogit can query the \codeindex attribute of an \codemlogit.data object to figure out the information contained in the ‘alt’ column.

2.2 Model parametrization

Multinomial logit models have a solid basis in the theory of discrete choice models. The central idea in these discrete models lies in the ‘utility maximization principle’ which states that individuals choose the alternative, from a finite, discrete set, which maximizes a scalar value called ‘utility’. Discrete choice models presume that the utility is completely deterministic for the individual, however modelers can only model a part of the utility (the ‘observed’ part). Stochasticity entirely arises from the unobserved part of the utility. Different assumptions about the probability distribution of the unobserved utility give rise to various choice models like multinomial logit, nested logit, multinomial probit, GEV (Generalized Extreme Value), mixed logit etc. Multinomial logit models, in particular, assume that unobserved utility is i.i.d. and follows a Gumbel distribution.222See the book TRAIN:03, particularly Chapters 3 and 5, for a full discussion.

We consider that the observed part of the utility for the individual choosing the alternative is given by:

| (1) |

Here Latin letters (, , ) stand for data while Greek letters (, , , ) stand for parameters. The parameter is called the intercept. For many practical applications data in multinomial logit models can be naturally grouped into two types:

-

•

Individual specific variables which does not vary between choices (e.g., income of individuals in the ‘Fish’ data of Section 2).

-

•

Alternative specific variables and which vary with alternative and may also differ, for the same alternative, between individuals (e.g., the amount of fish caught in the ‘Fish’ data: column ‘catch’).

In \pkgmnlogit we model these two data types with three types of coefficients:

-

1.

Individual specific data with alternative specific coefficients

-

2.

Alternative specific data with generic coefficients .

-

3.

Alternative specific data with alternative specific coefficients .

The vector notation serves to remind that more than one variable of each type maybe used to build a model. For example in the fish data we may choose both the ‘price’ and ‘catch’ with either generic coefficients (the ) or with alternative specific coefficients (the ).

Due to the principle of utility maximization, only differences between utility are meaningful. This implies that the multinomial logit model can not determine absolute utility. We must specify the utility for any individual with respect to an arbitrary base value333In choice model theory this is called ‘normalizing’ the model. which we choose to be . For convenience in notation, we fix the choice indexed by as the base, thus normalized utility is given by:

Notice that the above expression implies that . To simplify notation we re-write the normalized utility as:

| (2) |

This equation retains the same meaning as the previous, notice the restriction: , since we need . The most significant difference is that in Equation 2 stands for: (in terms of the original data).

The utility maximization principle, together with the assumtion on the error distribution, implies that for multinomial logit models (TRAIN:03) the probability of individual choosing alternative , , is given by:

| (3) |

Here is the normalized utility given in Equation 2 and is the base alternative with respect to which we normalize utilities. The number of available alternatives is taken as which is a positive integer greater than one. From the condition that every individual makes a choice, we have that: ,. This gives us the probability of individual picking the base alternative:

| (4) |

Note that is the familiar binary logistic regression model.

Equation 2 has implications about which model parameters maybe identified. In particular for alternative-specific coefficients of individual-specific data we may only estimate the difference . Similarly for the intercept only the difference , and not and separately maybe estimated. For a model with alternative we estimate sets of parameters and intercepts .

2.3 Formula interface

To specify multinomial logit models in \proglangR we need an enhanced version of the standard formula interface - one which is able to handle multi-part formulas. In \pkgmnlogit we built the formula interface using tools from the \proglangR package \pkgFormula (ZEIL:CROIS:10). Our formula interface closely confirms to that of the \pkgmlogit package. We illustrate it with examples motivated by the ‘Fish’ dataset (introduced in Section 2). Consider a multinomial logit model where ‘price’ has a generic coefficient, ‘income’ data being individual-specific has an alternative-specific coefficient and the ‘catch’ also has an alternative-specific coefficient. That is, we want to fit a model that has the 3 types of coefficients described in Section 2.2. Such a model can be specified in \pkgmnlogit with a 3-part formula: {Schunk} {Sinput} R> fm <- formula(mode price | income | catch) By default, the intercept is included, it can be omitted by inserting a ‘-1’ or ‘0’ anywhere in the formula. The following formulas specify the same model with omitted intercept: {Schunk} {Sinput} R> fm <- formula(mode price | income - 1 | catch) R> fm <- formula(mode price | income | catch - 1) R> fm <- formula(mode 0 + price | income | catch)

We can omit any group of variables from the model by placing a as a placeholder: {Schunk} {Sinput} R> fm <- formula(mode 1 | income | catch) R> fm <- formula(mode price | 1 | catch) R> fm <- formula(mode price | income | 1) R> fm <- formula(mode price | 1 | 1) R> fm <- formula(mode 1 | 1 | price + catch) When the meaning is unambiguous, an omitted group of variables need not have a placeholder. The following formulas represent the same model where ‘price’ and ‘catch’ are modeled with generic coefficients and the intercept is included: {Schunk} {Sinput} R> fm <- formula(mode price + catch | 1 | 1) R> fm <- formula(mode price + catch | 1) R> fm <- formula(mode price + catch)

2.4 Using package \pkgmnlogit

In an \proglangR session with \pkgmnlogit loaded, the man page can be accessed in the standard way: {Schunk} {Sinput} R> ?mnlogit The complete \codemnlogit function call looks like: {Schunk} {Sinput} R> mnlogit(formula, data, choiceVar = NULL, maxiter = 50, ftol = 1e-6, gtol + = 1e-6, weights = NULL, ncores = 1, na.rm = TRUE, print.level = 0, + linDepTol = 1e-6, start = NULL, alt.subset = NULL, …) We have described the ‘formula’ and ‘data’ arguments in previous sections while others are explained in the man page, only the ‘linDepTol’ argument needs further elaboration. Data used to train the model must satisfy certain necessary conditions so that the Hessian matrix, computed during Newton-Raphson estimation, is full rank (more about this in Appendix B). In \pkgmnlogit we use the \proglangR built-in function \codeqr, with its argument ‘tol’ set to ‘linDepTol’, to check for linear dependencies . If collinear columns are detected in the data then some are removed so that the remaining columns are linearly independent.

We now illustrate the practical usage of \codemnlogit and some of its methods by a simple example. Consider the model specified by the formula: {Schunk} {Sinput} R> fm <- formula(mode price | income | catch) This model has:

-

•

One variable of type : ‘price’.

-

•

Two variable of type : ‘income’ and the intercept.

-

•

One variable of type : ‘catch’.

In the ‘Fish’ data the number of alternatives , so the number of coefficients in the above model is:

-

•

coefficient for data that may vary with individuals and alternatives, corresponding to .

-

•

, alternative specific coefficients for individual specific data (note: that we have subtract from the number of alternative because after normalization the base choice coefficient can’t be identified), corresponding to .

-

•

alternative specific coefficients for data which may vary with individuals and alternatives, corresponding to .

Thus the total number of coefficients in this model is .

We call the function \codemnlogit to fit the model using the ‘Fish’ dataset on processor cores. {Schunk} {Sinput} R> fit <- mnlogit(fm, Fish, ncores=2) R> class(fit) {Schunk} {Soutput} [1] "mnlogit" For \codemnlogit class objects we have the usual methods associated with \proglangR objects: \codecoef, \codeprint, \codesummary and \codepredict methods. In addition, the returned ‘fit’ object can be queried for details of the estimation process by: {Schunk} {Sinput} R> print(fit444One dimensional minimization along the Newton direction.

3 Estimation algorithm

In \pkgmnlogit we employ maximum likelihood estimation (MLE) to compute model coefficients and use the Newton-Raphson method to solve the optimization problem. The Newton-Raphson method is well established for maximizing the logistic family loglikelihoods (HastieTibBook; TRAIN:03). However direct approaches of computing the Hessian of multinomial logit model’s log-likelihood function have extremely deleterious effects on the computer time and memory required. We present an alternate approach which exploits structure of the the intermediate data matrices that arise in Hessian calculation to achieve the same computation much faster while using drastically less memory. Our approach also allows us to optimally parallelize Hessian computation and maximize the use of BLAS (Basic Linear Algebra Subprograms) Level 3 functions, providing an additional factor of speedup.

3.1 Maximizing the likelihood

Before going into details we specify our notation. Throughout we assume that there are alternatives. The letter labels individuals (the ‘choice-makers’) while the letter labels alternatives (the ‘choices’). We also assume that we have data for individuals available to fit the model ( is assumed to be much greater than the number of model parameters). We use symbols in bold face to denote matrices, for example stands for the Hessian matrix.

To simplify housekeeping in our calculations we organize model coefficients into a vector . If the intercept is to be estimated then it simply considered another individual specific variable with an alternative specific coefficient but with the special provision that the ‘data’ corresponding to this variable is unity for all alternatives. The likelihood function is defined by , where each labels the alternative observed to chosen by individual . Now we have:

Here is the indicator function which unity if its argument is true and zero otherwise. The likelihood function is given by: . It is more convenient to work with the log-likelihood function which is given by . A little manipulation gives:

| (5) |

In the above we make use of the identity and the definition of in Equation 4. MCFAD:74 has shown that the log-likelihood function given above is globally concave. A quick argument to demostrate global concavity of is that it’s the sum of affine functions and the negation of the composition of the log-sum-exp function with a set of affine functions. 555The log-sum-exp function’s convexity and its closedness under affine composition are well known, see for example Chapter 3 of BoydBook.

We solve the optimization problem by the Newton-Raphson (NR) method which requires finding a stationary point of the gradient of the log-likelihood. Note that MLE by the Newton-Raphson method is the same as the Fisher scoring algorithm (HastieTibBook; jialimlogit). For our log-likelihood function 5, this point (which we name ) is unique (because of global concavity) and is given by the solution of the equations: . The NR method is iterative and starting at an initial guess obtains an improved estimate of by the equation:

| (6) |

Here the Hessian matrix, and the gradient , are both evaluated at . The vector is called the full Newton step. In each iteration we attempt to update by this amount. However if the log-likelihood value at the resulting is smaller, then we instead try an update of . This linesearch procedure is repeated with half the previous step until the new log-likelihood value is not lower than the value at . Using such a linesearch procedure guarantees convergence of the Newton-Raphson iterations (NocedalBook).

3.2 Gradient and Hessian calculation

Each Newton-Raphson iteration requires computation of the Hessian and gradient of the log-likelihood function. The expressions for the gradient and Hessian are quite well known666See for example (mlogit, Section 2.5) and (TRAIN:03, Chatper 3). and in there usual form are given by:

| (7) |

For a model where where only individual specific variables are used (that is only the matrix contributes to the utility in Equation 2), the matrices and are given by (jialimlogit; Bohning:92):

here is a matrix of order ( is the number of variables or features) and,

Here the sub-matrices are diagonal matrices of order , where and is the Kronecker delta which equals if and otherwise. Using this notation the gradient can be written as (jialimlogit):

Where we take vectors and as vectors of length , formed by vertically concatenating the probabilities and responses , for each . The Newton-Raphson iterations of Equation 6 take the form: = . Although in this section we have shown expressions for models with only individual specific variables, a general formulation of and including the two other types of variables appearing in Equation 2 exists777And is implemented in the \proglangR packages \pkgmlogit (mlogit) and \pkgVGAM (VGAM).. This is presented in Appendix B but their specific form is tangential to the larger point we make (our ideas extend to the general case in a simple way).

An immediate advantage of using the above formulation, is that Newton-Raphson iterations can be carried out using the framework of IRLS (Iteratively Re-weighted Least Squares) (HastieTibBook, Section 4.4.1). IRLS is essentially a sequence of weighted least squares regresions which offers superior numerical stability compared to explicitly forming and directly solving Equation 6 (TrefethenBook, Lecture 19). However this method, besides being easy to implement, is computationally very inefficient. The matrices and are huge, of orders and respectively, but are otherwise quite sparse and possess a neat structure. We now describe our approach of exploiting this structured sparsity.

3.3 Exploiting structure - fast Hessian calculation

We focus our attention on computation of the Hessian since it’s the most expensive step, as we later show from empirical measurements in Table 1 of Section 4. We start by ordering the vector , which is a concatenation of all model coefficients as specified in Equation 2, in the following manner:

| (8) |

Here, the subscripts index alternatives and the vector notation reminds us there maybe multiple features modeled by coefficients of type , , . In we group together coefficients corresponding to an alternative. This choice is deliberate and leads to a particular structure of the Hessian matrix of the log-likelihood function with a number of desirable properties.

Differentiating the log-likelihood function with respect to the coefficient vector , we get:

| (11) |

Here we have partitioned the gradient vector into chunks according to which is a group of coefficients of a particular type (defined in Section 2.2), either alternative specific or generic. Subscript (and subscript ) indicates a particular alternative, for example:

-

•

if then

-

•

if then

-

•

if then .

The vector is a vector of length whose entry is given by , it tells us whether the observed choice of individual is alternative , or not. Similarly is vector of length whose entry is given by , which is the probability individual choosing alternative . The matrices and contain data for choice and , respectively. Each of these matrices has rows, one for each individual. Specifically:

Similarly, the matrices are analogues of the and have rows each (note that due to normalization ).

To compute the Hessian we continue to take derivatives with respect to chunks of coefficients . On doing this we can write the Hessian in a very simple and compact block format as shown below.

| (15) |

Here is a block of the Hessian and the matrices are diagonal matrix of dimension , whose diagonal entry is given by: .888Here is the Kronecker delta, which is 1 if and 0 otherwise. The details of taking derivatives in this block-wise fashion are given in Appendix A.

The first thing to observe about Equation 15 is that effectively utilizes spartsity in the matrices and to obtain very compact expressions for . The block format of the Hessian matrix is particularly suited for extremely efficient numerical computations. Notice that each block can be computed independently of other blocks with two matrix multiplications. The first of these involves multiplying a diagonal matrix to a dense matrix, while the second requires multiplication of two dense matrices. We handle the first multiplication with a handwritten loop which exploits the sparsity of the diagonal matrix, while the second multiplication is handed off to a BLAS (Basic Linear Algebra Subprograms) call for optimal efficiency (GolubBook)999Hessian computation is implemented in a set of optimized \proglangC++ routines. Computing the Hessian block-by-block is very efficient since we can use level 3 BLAS calls (specifically \codeDGEMM) to handle the most intensive calculations. Another useful property of the Hessian blocks is that because matrices are diagonal (hence symmetric), we have the symmetry property , implying that we only need to compute roughly half of the blocks.

Independence of Hessian blocks leads to a very fruitul strategy for parallelizing Hessian calculations: we simply divide the work of computing blocks in the upper triangular part of the Hessian among available threads. This strategy has the great advantage that threads don’t require any synchronization or communication overhead. However the cost of computing all Hessian blocks is not the same: the blocks involving generic coefficients (the ) take much longer to compute longer. In \pkgmnlogit implementation, computation of the blocks involving generic coefficients is handled separately from other blocks and is optimized for serial computation.

Hessian calculation is, by far, the most time consuming step in solving the multinomial logit MLE problem via the Newton-Raphson method. The choice we make in representing the Hessian in the block format of Equation 15 has dramatic effects on the time (and memory) it takes for model estimation. In the next section we demonstrate the impact on computation times of this choice when contrasted with earlier approaches.

4 Benchmarking performance

For the purpose of performance profiling \pkgmnlogit code, we use simulated data generated using a custom R function \codemakeModel sourced from \codesimChoiceModel.R which is available in the folder \codemnlogit/vignettes/. Using simulated data we can easily vary problem size to study performance of the code - which is our main intention here - and make comparisons to other packages. Our tests have been performed on a dual-socket, 64-bit Intel machine with 8 cores per socket which are clocked at GHz101010The machine has 128 GB of RAM and 20 MB of shared L3 cache.. \proglangR has been natively compiled on this machine using \codegcc with BLAS/LAPACK support from single-threaded Intel MKL v11.0.

The 3 types of model coefficients mentioned in Section 2.2 entail very different computational requirements. In particular it can be seen from Equations 11 and 15, that Hessian and gradient calculation is computationally very demanding for generic coefficients. For clear-cut comparisons we speed test the code with 4 types of problems described below. In our results we shall use to denote the number of alternatives and to denote the total number of coefficients in the model.

-

1.

Problem ‘X’: A model with only individual specific data with alternative specific coefficients.

-

2.

Problem ‘Y’: A model with data varying both with individuals and alternatives and alternative specific model coefficients.

-

3.

Problem ‘Z’: Same type of data as problem ‘Y’ but with generic coefficients which are independent of alternatives.

-

4.

Problem ‘YZ’: Same type of data as problem ‘Y’ but with a mixture of alternative specific and generic coefficients.

Although problem ‘X’ maybe considered a special case of problem ‘Y’ but we have considered it separately, because it’s typically used in machine learning domains as the simplest linear multiclass classifier (HastieTibBook). We shall also demonstrate that \pkgmnlogit runs much faster for this class of problems.111111And use it to compare with the \proglangR packages \pkgVGAM and \pkgnnet which run only this class of problems (see Appendix C). The ‘YZ’ class of problems serves to illustrate a common use case of multinomial logit models in econometrics where the data may vary with both individuals and alternatives while the coefficients are a mixture of alternative specific and generic types (usually only a small fraction of variables are modeled with generic coefficients).

The workings of \pkgmnlogit can be logically broken up into 3 steps:

-

1.

Pre-processing: Where the model formula is parsed and matrices are assembled from a user supplied \codedata.frame. We also check the data for collinear columns (and remove them) to satisfy certain necessary conditions, specified in Appendix B, for the Hessian to be non-singular.

-

2.

Newton-Raphson Optimization: Where we maximize the log-likelihood function to estimate model coefficients. This involves solving a linear system of equations and one needs to compute the log-likelihood function’s gradient vector and Hessian matrix.

-

3.

Post-processing: All work needed to take the estimated coefficients and returning an object of class \codemnlogit.

Table 1 has profile of \pkgmnlogit performance for the four representative problems discussed earlier. Profiling the code clearly shows the highest proportion of time is spent in Hessian calculation (except for problem ‘Z’, for which the overall time is relatively lower). This is not an unexpected observation, it underpins our focus on optimizing Hessian calculation.

| Problem | Pre-processing time(s) | NR time(s) | Hessian time(s) | Total time(s) | |

| X | 93.64 | 1125.5 | 1074.1 | 1226.7 | 4950 |

| Y | 137.0 | 1361.5 | 1122.4 | 1511.8 | 5000 |

| Z | 169.9 | 92.59 | 60.05 | 272.83 | 50 |

| YZ | 170.1 | 1247.4 | 1053.1 | 1417.5 | 4505 |

Notice the very high pre-processing time for problem ‘Z’ whereof a large portion is spent in ensuring that the data satisfies necessary conditions, mentioned in Appendix B, for the Hessian to be non-singular.

4.1 Comparing \pkgmnlogit performance

We now compare the performance of \pkgmnlogit in single-threaded mode with some other \proglangR packages. This section focuses on the comparison with the \proglangR package \pkgmlogit since it’s the only one which covers the entire range of variable and data types as \pkgmnlogit. Appendix C contains a synopsis of our data generation and timing methods including a comparison of \pkgmnlogit with the \proglangR packages \pkgVGAM and \pkgnnet.

Table 2 shows the ratio between \pkgmlogit and \pkgmnlogit running times for the 4 classes of problems considered in Table 1. We see that for most problems, except those of type ‘Z’, \pkgmnlogit outperforms \pkgmlogit by a large factor.

| Optimizer | Newton-Raphson | BFGS | ||||

|---|---|---|---|---|---|---|

| K | 10 | 20 | 30 | 10 | 20 | 30 |

| Problem X | 18.9 | 37.3 | 48.4 | 14.7 | 29.2 | 35.4 |

| Problem Y | 13.8 | 20.6 | 33.3 | 14.9 | 18.0 | 23.9 |

| Problem YZ | 10.5 | 22.8 | 29.4 | 10.5 | 17.0 | 20.4 |

| Problem Z | 1.16 | 1.31 | 1.41 | 1.01 | 0.98 | 1.06 |

We have not run larger problems for this comparison because \pkgmlogit running times become too long, except problem ‘Z’121212In this case with and keeping other parameters the same as Table 2, \pkgmnlogit outperforms \pkgmlogit by factors of and while running the NR and BFGS, respectively..

Besides Newton-Raphson, which is the default, we have also run \pkgmlogit with the BFGS optimizer. Typically the BFGS method, part of the quasi-Newton class of methods, takes more iterations than the Newton method but with significantly lower cost per iteration since it never directly computes the Hessian matrix. Typically for large problems the cost of computing the Hessian becomes too high and the BFGS method becomes overall faster than the Newton method (NocedalBook). Our approach in \pkgmnlogit attacks this weakness of the Newton method by exploiting the structure and sparsity in matrices involved in the Hessian calculation to enable it to outperform BFGS.

4.2 Parallel performance

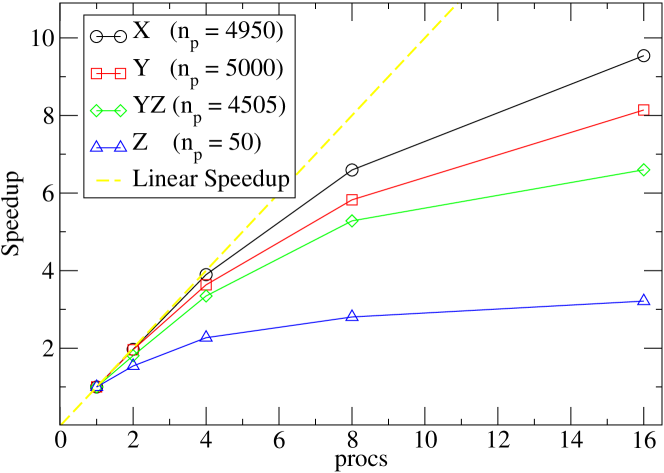

We now now turn to benchmarking \pkgmnlogit’s parallel performance. Figure 1 shows the speedups we obtain in Hessian calculation for the same problems considered in Table 1.

The value of , the number of model parameters, is significant because it’s the dimension of the Hessian matrix (the time taken to compute the Hessian scales like ). We run the parallel code separately on 2, 4, 8, 16 processor cores, comparing in each case with the single core time. Figure 1 shows that it’s quite profitable to parallelize problems ‘X’ and ‘Y’, but the gains for problem ’Z’ are not too high. This is because of a design choice we make: Hessian calculation for type ‘Z’ variables is optimized for serial processing. In practical modeling, number of model coefficients associated with ‘Z’ types variable is not high, especially when compared to those of types ‘X’ and ‘Y’ (because the number of the coefficients of these types is also proportional to the number of choices in the model, see Section 2.4). For problems of type ‘YZ’ (or other combinations which involve ‘Z’), parallelization can bring significant gains if the number of model coefficients of type ‘Z’ is low, relative to other types.

It can also be seen from figure 1 that, somewhat mysteriously, parallel performance degrades quickly as the number of processor cores is increased beyond . This is a consequence of the fact that our OpenMP progam runs on a machine with shared cache and main memory, so increasing the number of threads degrades performance by increasing the chance of cache misses and hence slowing memory lookups. This is an intrinsic limitation of our hardware for which there is a theoretically simple solution: run the program on a machine with a larger cache!

An important factor to consider in parallel speedups of the whole program is Amdahl’s Law131313See Chapter 6 of openmpBook. which limits the maximum speedup that maybe be achieved by any parallel program. Assuming parallelization between threads, Amdahl’s law states that the ultimate speedup is given by: , where is the fraction of non-parallelized, serial code. Table 3 lists the observed speedups on , and processor coress together with for problems of Table 1.

| Problem | Serial fraction () | |||

|---|---|---|---|---|

| X | 0.124 | 1.76(1.78) | 2.87(2.92) | 4.04(4.28) |

| Y | 0.258 | 1.59(1.62) | 2.26(2.27) | 2.59(2.85) |

| Z | 0.780 | 1.08(1.12) | 1.14(1.20) | 1.17(1.24) |

| YZ | 0.257 | 1.44(1.59) | 2.08(2.26) | 2.36(2.86) |

We take the time not spent in computing the Hessian as the ‘serial time’ to compute and neglect the serial time spent in setting up the parallel computation in Hessian calculation, which mainly involves spawning threads in OpenMP and allocating separate blocks of working memory for each thread141414For type ‘Z’ problems, this is an underestimate because some Hessian calculation is also serial.. Our tests have shown that compared to the Hessian calculation, the (serial) work required in setting up parallel computation is negligible, except for very small problems.

5 Discussion

Through \pkgmnlogit we seek to provide the community a package which combines quick calculation and the ability to handle data collinearity with a software interface which encompasses a wide range of multinomial logit models and data types used in econometrics and machine learning. Our main idea, exploiting matrix structure in large scale linear algebra calculations is not novel; however this work is the first, as far as we are aware, to apply it to the estimation of multinomial logit models problems in a working software package. The parallelization capability of \pkgmnlogit, which can easily add a 2x-4x factor of speedup on now ubiquitous mulitcore computers, is another angle which is underutilized in statistical software. Although \pkgmnlogit code is not parallelized to the maximum possible extent, parallelizing the most expensive parts of the calculation was an important design goal. We hope that practical users of the package benefit from this feature.

This work was initially motivated by the need to train large-scale multinomial logistic regression models. For very large-scale problems, Newton’s method is usually outperformed by gradient based, quasi-Newton methods like the l-BFGS algorithm (l-BFGS1989). Hessian based methods based still hold promise for such problems. The class of inexact Newton (also called truncated Newton) methods are specifically designed for problems where the Hessian is expensive to compute but taking a Hessian-vector product (for any given vector) is much cheaper (NashSurvey2000). Multinomial logit models have a Hessian with a structure which permits taking cheap, implicit products with vectors. Where applicable, inexact Newton methods have the promise of being better than l-BFGS methods (NasNocedal1991) besides having low memory requirements (since they never store the Hessian) and are thus very scalable. In the future we shall apply inexact Newton methods to estimating multinomial logit models to study their convergence properties and performance.

Acknowledgements

We would like to thank Florian Oswald of the Economics Department at University College London for contributing code for the \codepredict.mnlogit method. We are also grateful to numerous users of \pkgmnlogit who gave us suggestions for improving the software and reported bugs.

Appendix A Log-likelihood differentiation

In this Appendix we give the details of our computation of gradient and Hessian of the log-likelihood function in Equation 5. We make use of the notation of Section 3.3. Taking the derivative of the log-likelihood with respect to a chunk of coefficient one gets:

The second term in this equation is a constant term, since the utility , defined in Equation 2, is a linear function of the coefficients. Indeed we have:

| (18) |

The vectors and the matrices and are specified in Section 3.3. We take the derivative of the base case probability, which is specified in Equation 4, as follows:

| (21) |

Here the probability vector is of length with entries . In the last line we have used the fact that, after normalization, is . Using Equations 18 and 21 we get the gradient in the form shown in Equation 11.

Upon differentiating the probability vector () in Equation 3 with respect to we get:

| (24) |

where is an diagonal matrix whose diagonal entry is and, matrix is also an an diagonal matrix whose diagonal entry is . In matrix form this is: where is the Kronecker delta.

We write the Hessian of the log-likelihood in block form as:

However it can be derived in a simpler way by differentiating the gradient with respect to . Doing this and making use of Equation 24 gives us Equation 15. The first two cases of equation are fairly straightforward with the matrices being the same as shown in Equation 24. The third case, when ( are both , is a bit messy and we describe it here.

Here the last line follows from the definition of matrix as used in Equation 24.

Appendix B Data requirements for Hessian non-singularity

We derive necessary conditions on the data for the Hessian to be non-singular. Using notation from Section 3.2, we start by building a ‘design matrix’ by concatenating data matrices , and in the following format:

| (25) |

In the above stands for a matrix of zeros of appropriate dimension. Similarly we build two more matrices and as shown below:

Using the 2 matrices above we define a ‘weight’ matrix :

| (26) |

The full Hessian matrix, containing all the blocks of Equation 15, is given by: . For the matrix to be non-singular, we must have the matrix be full-rank. This leads us to the following necessary conditions on the data for the Hessian to be non-singular:

-

1.

All matrices in the set: , , must be of full rank.

-

2.

Atleast one matrix from the set: … must be of full rank.

In \pkgmnlogit we directly test condition 1, while the second condition is tested by checking for collinearity among the columns of the matrix151515Since number of rows is less than the number of columns:

Columns are arbitrarily dropped one-by-one from a collinear set until the remainder becomes linearly independent.

Another necessary condition: It can be shown with some linear algebra manipulations (omitted because they aren’t illuminating) that if we have a model with has only: data for generic variables independent of alternatives and the intercept, then the resulting Hessian will always be singular. \pkgmnlogit does not attempt to check the data for this condition which is independent of the 2 necessary conditions given above.

Appendix C Timing tests

We give the details of our simulated data generation process and how we setup runs of the \proglangR packages \pkgmlogit, \pkgVGAM and \pkgnnet to compare running times against \pkgmnlogit. We start by loading \pkgmlogit into an \proglangR session: {Schunk} {Sinput} R> library("mlogit") Next we generate data in the ‘long format’ (described in Section 2) using the \codemakeModel function sourced from the file \codesimChoiceModel.R which is in the \codemnlogit/vignettes/ folder. The data we use for the timing tests shown here is individual specific (problem ‘X’ of Section 4) because this is the only one that packages \pkgVGAM and \pkgnnet can run. We generate data for a model with choices as shown below. {Schunk} {Sinput} R> source("simChoiceModel.R") R> data <- makeModel(’X’, K=10) Default arguments of \codemakeModel set the number of variables and the number of observations, which are: {Schunk} {Soutput} Number of choices in simulated data = K = 10. Number of observations in simulated data = N = 10000. Number of variables = p = 50. Number of model parameters = (K - 1) * p = 450.

The next steps setup a \codeformula object which specifies that individual specific data must be modeled with alternative specific coefficients and the intercept is excluded from the model. {Schunk} {Sinput} R> vars <- paste("X", 1:50, sep="", collapse=" + ") R> fm <- formula(paste("response 1|", vars, " - 1 | 1")) Using this formula and our previously generated \codedata.frame we run \pkgmnlogit to measure its running time (in single threaded mode). {Schunk} {Sinput} R> system.time(fit.mnlogit <- mnlogit(fm, data, "choices")) {Soutput} user system elapsed 2.200 0.096 2.305 Likewise we measure running times for \pkgmlogit running the same problem with the Newton-Raphson (the default) and the BFGS optimizers. {Schunk} {Sinput} R> mdat <- mlogit.data(data[order(data