Joint Hitting-Time Densities for Finite State Markov Processes

Abstract

For a finite state Markov process and a finite collection of subsets of its state space, let be the first time the process visits the set . We derive explicit/recursive formulas for the joint density and tail probabilities of the stopping times . The formulas are natural generalizations of those associated with the jump times of a simple Poisson process. We give a numerical example and indicate the relevance of our results to credit risk modeling.

1 Introduction

One of the basic random variables associated with a Markov process is its first hitting time to a given subset of its state space. In the present work we will confine ourselves to finite state Markov processes. If has an absorbing state and all of the states can communicate with it, the distribution of the first hitting time to the absorbing state is said to be a phase-type distribution. Phase-type distributions can model a wide range of phenomena in reliability theory, communications systems, in insurance and finance and go back to Erlang [6]. The literature on these distributions is immense, see, e.g., [4, 8, 10, 12, 1, 2]. To the best of our knowledge, [3] introduced higher dimensional versions of phasetype distributions. Their setup, for the two dimensional case is as follows: take two proper subsets and of the state space, and assume that with probability the process enters their intersection; let be the first time the process enters . The joint distribution of is a two dimensional phase type distribution. Higher dimensional versions are defined similarly for a finite collection of subsets of the state space.

Denote the number of elements in by . Multidimensional phase type distributions can put nonzero mass on lower dimensional subsets of and the density of the distribution when restricted to these subsets is called the “singular part of the distribution.” To the best of our knowledge, the only result available in the current literature giving a complete characterization of any multidimensional phase type density is the case of two dimensions treated in [3]. The same work derives a density formula for the nonsingular part of a phasetype distribution of arbitrary finite dimension, which is proved to be correct in [7]. The main contribution of the present paper is Theorem 3.2, which gives an explicit formula for the joint density (over appropriate subsets of ) of the random vector covering all possible singular and nonsingular parts. It turns out that it is simpler to work with no assumptions on whether are absorbing or not. Thus, Theorem 3.2 gives the joint density of a collection of first hitting times for any finite state Markov process . The density of phasetype densities follows as a special case (see Proposition 4.1 for the one dimensional case and Proposition 4.2 for the general case).

The primary difficulty in the prior literature in identifying the singular part of the density seems to have stemmed from the method of derivation, which is: find expressions for tail probabilites and differentiate them. As will be seen in subsection 3.4 tail probabilities turn out to be more complicated objects than densities. Thus, we follow the opposite route and compute first the density directly using the following idea: for each , is the limit of a specific and simple set of trajectories of the Markov process whose (vanishing) probability can be written in terms of the exponentials of submatrices of the intensity matrix. Subsection 3.1 explains the idea in its simplest form in the derivation of the density of a single , given as Theorem 3.1. The same idea extends to multiple hitting time in Subsection 3.2 and the multidimensional density is given as Theorem 3.2. Subsection 3.4 derives the tail probabilities of using the same idea; the result is given as Theorem 3.3. The formulas for tail probabilities are more complex and are best expressed recursively. We provide a second formula (3.5) which explicitly states some of the integration that is hidden in the completely recursive (26).

Let be the filtration generated by . The Markov property of implies that the conditional density of given directly follows from the density formula (14), which we note as Proposition 3.2. In Section 4 we derive alternative expressions for the density and the tail probability formulas for absorbing and indicate the connections between our results and the prior literature. Section 5 gives a numerical example. We discuss potential applications of our results to credit risk modeling and point out several directions of future research in the conclusion.

2 Definitions

Let be a finite set and a -valued continuous time process defined over a measurable pair equipped with a family of measures , , such that . Under each , is assumed Markov with intensity matrix . Denote by the collection of measures written as a column. If is a probability measure on (written as a row), we will denote by the measure on . It follows from these definitions that under the initial distribution of is , i.e., The total jump rate of the process when in state is . For a finite collection of subsets of define The index set can be any finite set, but we will always take it to be a finite subset of the integers. In the next section we derive formulas for the (conditional) joint density and tail probabilities of the stopping times To ease notation, unless otherwise noted, we will assume throughout that is not empty and that the initial distribution puts its full mass on this set, see Remark 3.2 and subsection 3.3 for comments on how one removes this assumption.

For a set , will mean its complement and if it is finite will mean the number of elements in it. For two subsets define as

| (1) |

For , we will write for We note .

Throughout we will need to refer to zero matrices and vectors of various dimensions, we will write all as ; the dimension will always be clear from the context.

For , take the identity matrix and replace its rows whose indices appear in with the vector and call the resulting matrix , e.g., is itself and is the zero matrix. The matrix has the following action on matrices and vectors:

Lemma 2.1.

Let be a positive integer. For any , is the same as except that its rows whose indices are in are replaced by (a zero row vector of dimension ), i.e., if is the row of then the row of is if and otherwise.

The proof follows from the definitions and is omitted. Right multiplication by acts on the columns, i.e., is the same as except now that the columns with indices in are set to zero. As an operator on dimensional vectors, replaces with the coordinates of the vector whose indices are in .

It follows from the definition (1) of and Lemma 2.1 that

| (2) |

The operation of setting some of the columns of the identity matrix to zero commutes with set operations, i.e., one has

| (3) |

Using this and Lemma 2.1 one can write any formula involving in a number of ways. For example, can be written as or as

2.1 Restriction and extension of vectors and as a random function

For any nonempty finite set let be the set of functions from to . is the same as , except for the way we index the components of their elements. For two sets and denote ’s restriction to by :

| (4) |

The same notation continues to make sense for of the form , and therefore can be used to write submatrices of a matrix. Thus, for and nonempty

| (5) |

will mean the submatrix of consisting of its components with For we will write

For denote by the following extension of to :

| (6) |

The random vector can also be thought of as a random function on , and we will often do so. Thus for , we may write to denote . The advantage of the notation is that we are able to index its components with elements of rather than with the integers ; this proves useful when stating the recursive formulas and proofs below.

2.2 Subpartitions of

The key aspect of the distribution of , already referred to in the introduction, is that it may put nonzero mass on lower dimensional subsets of This happens, for example, when can hit before with positive probability for some with . As this example suggests, one can divide into a number of regions and associate with each an intersection of events of the form “ hits before ” for appropriate subsets of . To write down the various regions and the corresponding events we will use subpartitions of , which we introduce now.

Recall that is the set of indices of the stopping times or equivalently the sets . We call an ordered sequence of disjoint nonempty subsets of a subpartition of . If the union of all elements of a subpartition is then we call it a partition. For example, [] is a [sub]partition of . Denote by the number of components in the subpartition and by its component, In which order the sets appear in the partition matters. For example, is different from the previous partition. In the combinatorics literature this is often called an “ordered partition,” see ,e.g., [11]. Only ordered partitions appear in the present work and therefore to be brief we always assume every subpartition to have a definite order and drop the adjective “ordered.” With a slight abuse of notation we will write to denote the element of the set in the partition.

Two subpartitions and are said to be disjoint if and are disjoint subsets of . For a given disjoint pair of subpartitions , let be their concatenation, for example

For a subpartition let be its left shift, i.e., Let denote left shift times. Similarly for , let be its left shift. For and let denote

Given a subpartition and an index , let be the subpartition which is the same as but without , e.g., Given a subpartition and a nonempty let denote the subpartition that has all the sets is and , e.g.,

Define

For a partition define

For example, for

Let be the set of all partitions of . The sets , are disjoint and their union is . It turns out that for each , the distribution of restricted to is absolutely continuous with respect to the dimensional Lebesgue measure on . Our main result, given as Theorem 3.2 below, is a formula for this density.

3 The density of first hitting times

We start by deriving the density of a single hitting time over sets of sample paths that avoid a given subset of the state space until the hitting occurs.

3.1 Density of one hitting time

For any set and define and In addition set . The distribution is a row vector and and are matrices. Conditioning on the initial state implies It follows from the definition of , and that

| (7) |

for

Lemma 3.1.

Let be an initial distribution on with . Then

| (8) |

Proof.

We only need to modify slightly the proof of [1, Theorem 3.4, page 48]. The steps are: 1) write down a linear ordinary differential equation (ODE) that the matrix valued function , , satisfies, 2) the basic theory of ODEs will tell us that the unique solution is .

Let be the first jump time of ; for , is exponentially distributed with rate . Conditioning on gives

| (9) |

for . In comparison with the aforementioned proof we have only changed the index set of the last sum to ensure that only paths that keep away from are included. The unique solution of (9) equals The equality (8) follows from this and ∎

Remark 3.1.

The next result (written in a slightly different form) is well known, see, e.g., [9, 3]. We record it as a corollary here and will use it in subsection 4.1 where we indicate the connections of our results to prior literature. Let be the dimensional column vector with all components equal to .

Corollary 3.1.

For , and an initial distribution with

| (10) |

Proof.

where the last equality is implied by (8). ∎

Remark 3.2.

Theorem 3.1.

Let , be given. Define and set Then

| (11) |

where is the initial distribution of with .

The idea behind (11) and its proof is this: for with staying out of until time , has to stay in the set until time and jump exactly at that time into .

Proof of Theorem 3.1.

The ideas in the previous proof also give

Proposition 3.1.

Let , , nonempty be given. Define and Let is an initial distribution on with Set and . Then

where is the indicator function of the event

is the event that does not visit the set before time .

Proof.

3.2 The multidimensional density

One can extend (11) to a representation of the distribution of using the subpartition notation of subsection 2.2. For a partition of , and define

| (13) |

where stands for “waiting” and for “target.” The key idea of the density formula and its proof is the step version of the one in Theorem 3.1: in order for , has to stay in the set until time and jump exactly at that time into ; then stay in the set until time and jump exactly then into and so on until all of the pairs , , are exhausted.

Although not explicitly stated, all of the definitions so far depend on the collection . We will express this dependence explicitly in the following theorem by including the index set as a variable of the density function . This will be useful in its recursive proof, in the next subsection where we comment on the case when is an arbitrary initial distribution and in Proposition 3.2 where we give the conditional density of given , . For a sequence of square matrices of the same size will mean .

Theorem 3.2.

For any partition of , the distribution of on the set has density

| (14) |

, with respect to the dimensional Lebesgue measure on

In the proof we will use

Lemma 3.2.

Let and be two measurable spaces and a bounded measurable function. Let be an valued random variable on a probability space . Let be a sub -algebra of and suppose 1) is measurable and 2) under , has a regular conditional distribution given For define Then

The value in the previous lemma is defined via a conditional expectation and therefore it depends on . The proof of Lemma 3.2 follows from the definition of regular conditional distributions, see, for example, [5, Section 5.1.3, page 197]. To invoke Lemma 3.2 we need the existence of the regular conditional distribution of ; in the proof below will take values in a finite dimensional Euclidean space (a complete separable metric space) and therefore will have a regular conditional distribution, for further details we refer the reader to, e.g., [5, Theorem 2.1.15] and [5, Theorem 5.1.9].

Proof.

The proof will use induction on For (14) (with ) and (11) are the same. Suppose that (14) holds for all with ; we will now argue that then it must also hold for Fix a partition of . We would like to show that restricted to has the density (14).

For any continuous with compact support, we would like to show

| (15) |

where denotes the dimensional Lebesgue measure on . Define ; is the first time enters In the rest of the proof we will proceed as if ; the treatment of the possibility needs no new ideas and the following argument can be extended to handle it by adding several case by case comments.

If holds then 1) and 2) for ; 1) and 2) also imply Therefore,

| (16) |

Theorem 3.1 implies that is non zero if and only if has nonzero probability. Thus if is zero then and indeed is the density of over From here on we will treat the case when is nonzero.

Define and for

one obtains from by shifting time for the latter left by , i.e., once time hits reset it to and call the future path of the process . The Markov property of implies that is a Markov process with intensity matrix and initial point . The relation (16) implies

| (17) |

on the set Finally, the last display, the definition of and that of imply

| (18) |

In words this display says: for to be partitioned according to , among all , must visit first and after this visit the rest of the hitting times must be partitioned according to .

Denote by the function that maps all elements of to . Define as

where we use the function restriction/ extension notation of (4) and (6). Displays (17) and (18) imply

| Condition the last expectation on : | ||||

| is measurable and gets out of the inner expectation | ||||

| (19) | ||||

For define

| (20) |

the last equality is by the strong Markov property of . Once again, is a conditional expectation and thus it depends on . Lemma 3.2 implies that the conditional expectation in (19) equals ( is substituted for the of the lemma). The random variable takes values in a finite set and therefore one can compute the last conditional expectation by conditioning on each of these values separately. This, that is a Markov process with intensity matrix and the induction assumption imply that on

| (21) |

Once we substitute (21) for the conditional expectation in (19) we get an expectation involving only three random variables: , and Theorem 3.1 implies that the density of on the set is and Proposition 3.1 implies that the distribution of conditioned on and is

These, the induction hypothesis, (20) and (21) imply that the outer expectation (19) equals (15). This last assertion finishes the proof of the induction step and hence the theorem. ∎

In what follows, to ease exposition, we will sometimes refer to as the “density” of without explicitly mentioning the reference measures , .

Remark 3.3.

If any of the matrices in the product (14) equals the zero matrix then will be . Therefore, if for some then By definition if Thus as a special case we have if for some .

Remark 3.4.

The first jump times of a standard Poisson process with rate have the joint density

. The density (14) is a generalization of this simple formula.

3.3 When puts positive mass on

If puts positive mass on one best describes the distribution of piecewise as follows. Define and if ; is a real number and , when defined, is a distribution. First consider the case when . The foregoing definitions imply

| (22) |

for any measurable . By its definition puts no mass on and therefore Theorem 3.2 is applicable and is the density of the distribution . For the second summand of (22), it is enough to compute each separately. Define , , Now remember that ; thus if then under , and therefore For , the stopping times are all deterministically . Thus to compute it suffices to compute But by definition and once again Theorem 3.2 is applicable and gives the density of under as If then

and the computation of goes as above.

3.4 Tail probabilities of

By tail probabilities we mean probabilities of sets of the form

| (23) |

where is a partition of and such that , Thus this definition of tail events require that every equality and inequality condition be explicitly specified. One can write standard tail events in terms of these, e.g., is the same as the disjoint union

Both of these sets are of the form (23). Thus, it is enough to be able to compute probabilities of the form (23). From here on, to keep the notation short, we will assume that, over tail events, unless explicitly stated with an equality condition, all stopping times appearing in them are strictly unequal to each other (therefore, when writing formulas, we will omit the last intersection in (23)).

A tail event of the form (23) consists of a sequence of constraints of the form

There are two types of subconstraints involved here: that entrance to all , , happen at the same time and that this event occurs after time . Keeping track of all of these constraints as they evolve in time requires more notation, which we now introduce.

Take two disjoint subpartitions and of and an element such that ; if by convention set Generalize the class of tail events to

| (24) |

Setting and reduces (3.4) to (23). The indices in appear both in equality constraints and time constraints while indices in appear only in equality constraints.

Remark 3.5.

The definition (3.4) implies that if a component of has only a single element, that component has no influence on . For example, is the same as

To express we will define a collection of functions , , of , and . Let be the collection written as a column matrix. For , and define as

The definitions of and and Remark 3.5 imply

| (25) |

if is empty or it consists of components with single elements. For a given disjoint pair of subpartitions , define

If define

| (26) | ||||

where If and (26) reduces to

| (27) |

We have the following representation of tail probabilities:

Theorem 3.3.

Suppose is not empty and that is an initial distribution on that puts all of its mass on this set. Then

The proof is parallel to the proof of Theorem 3.2 and involves the same ideas and is omitted.

One can write (14) recursively, similar to (26). The reverse is not true: equality constraints, when present, preclude a simple explicit formula for similar to (14), but see subsection 3.5 for a slightly more explicit representation of .

When has no equality constraints and , one can invoke (27) times along with Remark 3.5 and (25) and get

Corollary 3.2.

If we have no time constraints and reduces to the probability that certain equality and inequality constraints hold among the stopping times. This can be written as the solution of a sequence of linear equations whose defining matrices are submatrices of the intensity matrix. The details require further notation and are left to future work (or to the reader) except for the special case of which we would like use in what follows to relate our results to earlier works in the literature.

Define , and for The sequence is the jump times of the process . Define is a discrete time Markov chain with state space ; it is called the embedded Markov chain of the process . It follows from (7) that the one step transition matrix of is

Define as the diagonal matrix

Left multiplying a matrix by divides its row by Therefore,

Define The event means that hits the set and at the same time; because this event makes no reference to how time is measured, it can also be expressed in terms of as .

Define the column vector , Conditioning on the initial position of implies From here on we derive a formula for . Parallel to the arguments so far, we know that this event happens if and only if hits before . Set . satisfies the boundary conditions

| (29) |

and is to be determined only for the states in . If a state cannot communicate with , is trivially ; let denote the set of states in that can communicate with The Markov property of implies that for

or in matrix notation (see (5)):

| For , and in particular the same holds for and therefore | ||||

There is no harm in taking the diagonal out of the projection operation on both sides of the last display:

That all states in can communicate with implies that the matrix on the left is invertible and therefore

| (30) |

3.5 A second representation of tail probabilities

For a nonnegative integer , denote by the set of all subpermutations of , e.g., The tail probability formula (26) conditions on the first time that one of the equality constraints is attained in the time interval and writes what happens after that as a recursion. What can happen between and ? A number of other equalities can be attained and rather than pushing these into the recursion, one can treat them inside the integral using a density similar to (14):

| (31) | ||||

where and

is the dimensional Lebesgue measure on for ; and is the trivial measure on for . The proof involves no additional ideas and is omitted.

3.6 Conditional formulas

The proof of Theorem 3.2 shows how one can use the density formula (14) to write down the regular conditional distribution of given . One can do the same for , where is a given deterministic time. To that end, introduce the set valued process

is finite, then so is its power set , thus takes values in a finite set. is the collection of that has visited up to time . For ease of notation we will denote the complement of by . The times are known by time and hence they are constant given . Thus, we only need to write down the regular conditional density of , i.e., the hitting times to the that have not been visited by time . From here on the idea is the same as in the proof of Theorem 3.2. Define and for

The definitions of and imply

| (32) |

is a constant given . Thus the process has exactly the same distribution as with initial point and Theorem 3.2 applies and gives the density of , which is, by (32), the regular conditional distribution of . Therefore, for any bounded measurable and a partition of

We record this as

Proposition 3.2.

The regular conditional density of given is .

4 Absorbing and connections to earlier results

A nonempty subset is said to be absorbing if for all and , i.e., if . We next derive an alternative expression for the density formula (14) under the assumption that all are absorbing. The first step is

Proposition 4.1.

| (33) |

if is absorbing and

Proof.

We already know from Lemma 3.1 that the first equality holds. Therefore, it only remains to show [1, Theorem 3.4, page 48] implies that the distribution of at time is , i.e., for all . That is absorbing implies that if then for all , Therefore for

i.e.,

| (34) |

The definition of and imply ; The definition of implies . This and (34) imply (33). ∎

Proposition 4.1 says the following: if is absorbing then is the same as and both describe the probability of each state in at time over all paths that avoid in the time interval . The first expression ensures that all paths under consideration avoid the set by setting the jump rates into to . The second expression does this by striking out those paths that end up in one of the states in (the term does this); this is enough because is absorbing: once a path gets into it will stay there and one can look at the path’s position at time to figure out whether its weight should contribute to . In the general case this is not possible, hence the in the exponent.

The previous proposition implies that one can replace the in the density formula (14) with :

Proposition 4.2.

Proof.

Set ,

and for

The right side of (35) is and its left side is We will prove

| (36) |

by induction; setting in the last display will give (35). For (36) is true by definition; assume that it holds for ; we will argue that this implies that it must also for . Union of absorbing sets is also absorbing, therefore is absorbing. This, , the induction hypothesis and (33) (set ) imply

| The identities (2) and (3) imply and therefore | ||||

This completes the induction step and therefore the whole proof. ∎

Using the same ideas and calculations as in the previous proof one can write the tail probability formula (26) as

and (27) as

| (37) |

when are absorbing.

Let us briefly point out another possible modification of the density formula for absorbing Define

where and . If are absorbing one can replace the target and waiting sets and of (13) with and defined above. One can prove that the density formula continues to hold after this modification with an argument parallel to the proof of Proposition 4.2 using in addition that the intersection of absorbing sets is again absorbing.

4.1 Connections to earlier results

This subsection gives several examples of how to express density/distribution formulas from the prior phase-type distributions literature as special cases of the ones derived in the present work.

We begin by three formulas from [3]. The first two concern a single hitting time and the last a pair. [3] denotes the state space of by assumes that it has an absorbing element , denotes by and by . [3] also uses the letter to denote the initial distribution of , but over the set (and implicitly assuming ). We will use the symbol to denote the ‘ of [3].’ The relation between and is .

The first line of [3, equation (2), page 690] says where is the dimensional vector with all component equal to . The corresponding formula in the present work is (10) where one takes . The following facts imply the equality of these formulas 1) and 2) the row of corresponding to is . The second line of the same equation gives as the density of . The corresponding formula here is (11) with , and for which it reduces to . This time, 1), 2) and the following fact imply the equality of the formulas: the row sums of are zero, therefore The matrix is the column of corresponding to ; one way to write it is as the negative of the sums of the rest of the columns, this is what the last equality says.

[3, Equation (5), page 692] concerns the following setup (using the notation of that paper): we are given two set with , is the first hitting time to The formula just cited says

| (38) |

where and for two matrices and , . The absorbing property of and implies that the matrix inside the parenthesis in the last display equals , where i.e., the same matrix as except that the rows whose indices appear in are replaced with . Thus is another way to take the column of and replace its components whose indices appear in with . Denote this vector by . Then the right side of (38) is

| (39) |

The same probability is expressed by a special case of (37); for the present case one sets , ; for these values, (27) and conditioning on the initial state gives

| (40) |

where . Remember that we have denoted the last probability as and derived for it the formulas (29) and (30). The article [3] assumes that all states can communicate with , which implies that of (30) equals . This and imply in (30) equals i.e., the column of projected to its indices in , i.e., . The only difference between and is that the former has zeros in its extra dimensions. This and the absorbing property of imply

Note that we are commuting the projection operation and the inverse operation; this is where the absorbing property is needed. The last display, (29) and (30) give . This and imply that one can rewrite the right side of (40) as

Once again implies that the last expression equals (39).

The density formula [7, (3.1.11)] will provide our last example. The process of [7] is a random walk (with absorbing boundary) on with increments where is the unit vector with coordinate equal to ([7] uses different but equivalent notation, in particular the name of the process is and its state space is represented by subsets of ; the notation of this paragraph is chosen to ease discussion here and in the ensuing sections). [7] takes (, see the display after [7, (2.3)]). and assumes them to be absorbing. The jump rate for the increment is assumed to be for fixed and (given in [7, (2.1)]). A key property of this setup is this: take any collection with ; because the only increments of are the , the process cannot enter the sets in the collection at the same time. Thus, in this formulation, must hit the at separate times and the distribution of has no singular part, i.e., for and one needs only the density of with respect to the full Lebesgue measure in (the “absolutely continuous part”). As noted in [7], this is already available in [3] (see the display following (7) on page 694) and is given in [7, display (3.1.1)] as follows:

| (41) |

for with ; here and is the index for which ([7] uses the letter for the rate matrix ). We briefly indicate why (35) is equivalent to the last formula with the assumptions of this paragraph, i.e., when the dynamics of precludes it to enter more than one of the at the same time and in particular when equals the dimension of (denoted by in the current paragraph). Lemma 2.1 and the absorbing property of imply

On the other hand again Lemma 2.1 and the absorbing property of imply . The row sums of equal . The last two facts imply These imply that one can write (41) as

As we noted above, for the dynamics of imply that it cannot enter and at the same time. Furthermore, by definition for . Finally, the initial distribution is assumed to be such that it puts zero mass on These imply that one can replace of (35) with (a full argument requires an induction similar to the proof of Proposition 4.2), and therefore under the current assumptions the last display and (35) are equal.

5 Numerical Example

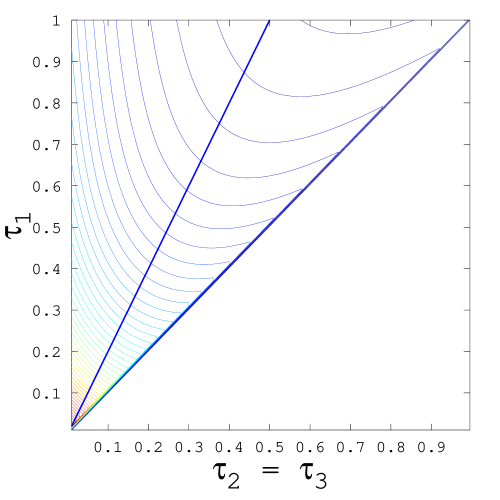

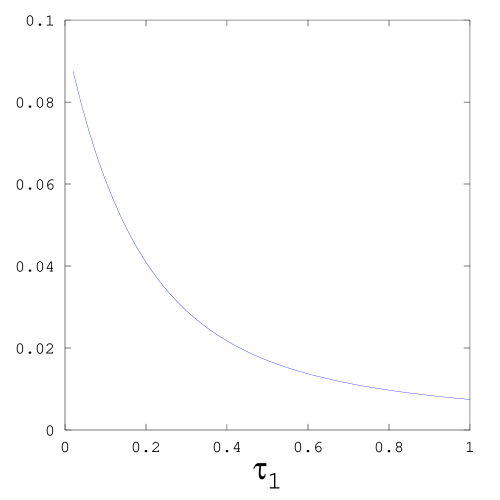

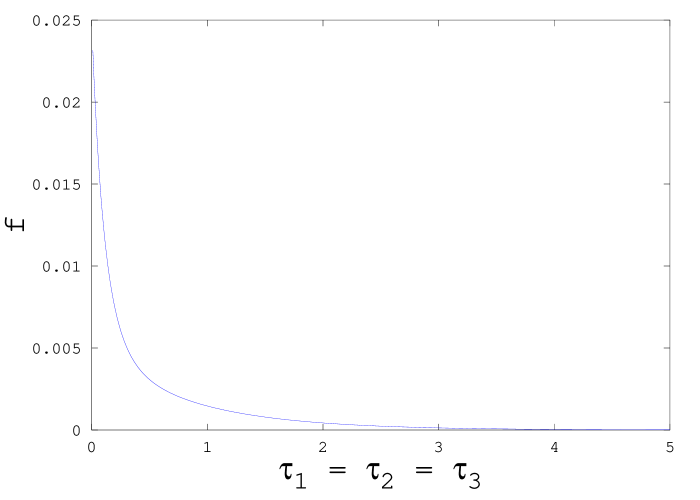

The state space of our numerical example is . For and let denote the component of . For the collection take

, as before, is the first time the process hits the set . The initial distribution will be the uniform distribution over the set

We will compute the density of over the sets , defined by the partitions and ; the first corresponds to the event and the second to .

The dynamics of on for our numerical example will be that of a constrained random walk with the following increments:

| (42) |

where , and ; the are assumed to be absorbing, i.e., if any increment involving can no longer be an increment of for . The sets are “reflecting” in the sense that if for some , increments involving cannot be the first increment of in the time interval . We assume the following jump rates for the increments listed in (42):

These rates and the aforementioned dynamics give a matrix. The level sets are depicted in Figure 1 and the graph of is depicted in Figure 2.

For the parameter values of this numerical example, and thus the singular parts account for around of the distribution of .

6 Conclusion

Our primary motivation in deriving the formulas in the present paper has been their potential applications to credit risk modeling. Let us comment on this potentiality starting from the credit risk model of [7]. With the results in the present work one can extend the modeling approach of [7] in two directions. Remember that the underlying process in [7] can only move by increments of i.e., the model assumes that the obligors can default only one at a time. However, for highly correlated obligors it may make sense to allow simultaneous defaults, i.e., allow increments of the form . Once multiple defaults are allowed the default times will have nonzero singular parts and the formulas in the present work can be used to compute them, as is done in the numerical example of Section 5. Secondly, the default sets no longer have to be assumed to be absorbing. Thus, with our formulas, one can treat models that allow recovery from default.

As increases (14) and other formulas derived in the present paper can take too long a time to compute (the same holds for earlier density formulas in the prior literature). Thus it is of interest to derive asymptotic approximations for these densities.

References

- [1] Søren Asmussen, Applied probability and queues, Springer, 2003.

- [2] Søren Asmussen and Hansjörg Albrecher, Ruin probabilities, vol. 14, World Scientific, 2010.

- [3] David Assaf, Naftali A Langberg, Thomas H Savits, and Moshe Shaked, Multivariate phase-type distributions, Operations Research 32 (1984), no. 3, 688–702.

- [4] Aldous David and Shepp Larry, The least variable phase type distribution is erlang, Stochastic Models 3 (1987), no. 3, 467–473.

- [5] Rick Durrett, Probability: theory and examples, vol. 3, Cambridge university press, 2010.

- [6] Agner Krarup Erlang, Solution of some problems in the theory of probabilities of significance in automatic telephone exchanges, Elektrotkeknikeren 13 (1917), 5–13.

- [7] Alexander Herbertsson, Modelling default contagion using multivariate phase-type distributions, Review of Derivatives Research 14 (2011), no. 1, 1–36.

- [8] Mary A Johnson and Michael R Taaffe, Matching moments to phase distributions: Mixtures of erlang distributions of common order, Stochastic Models 5 (1989), no. 4, 711–743.

- [9] Marcel F Neuts, Probability distributions of phase type, Liber Amicorum Prof. Emeritus H. Florin 173 (1975), 206.

- [10] , Matrix-geometric solutions in stochastic models: an algorithmic approach, Courier Dover Publications, 1981.

- [11] Richard P Stanley, Enumerative combinatorics, vol. 49, Cambridge university press, 2011.

- [12] Ryszard Syski, Passage times for markov chains, vol. 1, Ios Press, 1992.