Inverse problems and

uncertainty quantification††thanks: Partly supported by the Deutsche

Forschungsgemeinschaft (DFG) through SFB 880.

Alexander Litvinenko

Institute of Scientific Computing,

Technische Universität Braunschweig

Hermann G. Matthies

Corresponding author: D-38092 Braunschweig,

Germany, e-mail: wire@tu-bs.deInstitute of Scientific Computing,

Technische Universität Braunschweig

Abstract

In a Bayesian setting, inverse problems and uncertainty quantification (UQ)—the

propagation of uncertainty through a computational (forward)

model—are strongly connected.

In the form of conditional expectation the Bayesian update becomes computationally

attractive. This is especially the case as together with a functional or

spectral approach for the forward UQ there is no need for time-consuming and slowly

convergent Monte Carlo sampling. The developed sampling-free non-linear

Bayesian update is derived from the variational problem associated with conditional

expectation. This formulation in general calls for further discretisation to

make the computation possible, and we choose a polynomial approximation.

After giving details on the actual computation in the framework of functional

or spectral approximations, we demonstrate the workings of the algorithm on a

number of examples of increasing complexity. At last, we compare the linear

and quadratic Bayesian update on the small but taxing example of

the chaotic Lorenz 84 model, where we experiment with the influence of

different observation or measurement operators on the update.

In trying to predict the behaviour of physical systems, one is often

confronted with the fact that although one has a mathematical model

of the system which carries some confidence as to its fidelity, some

quantities which characterise the system may only be incompletely

known, or in other words they are uncertain.

See [23] for a synopsis on our approach to

such parametric problems.

We want to identify these parameters through

observations or measurement of the response of the system,

which can be approached in different ways.

In the mathematical description, the measurement / observation / output is

determined by the uncertain parameters, i.e. we have a mapping

from parameters to observations. The problems is that usually

this mapping is not invertible, hence these inverse identification

problems are generally ill-posed.

One way to deal with this difficulty is to measure the difference

between observed and predicted system output and try to find parameters such

that this difference is minimised. Frequently it may happen that

the parameters which realise the minimum are not unique. In case

one wants a unique parameter, a choice has to be made, usually by

demanding additionally that some norm or similar functional of the parameters

is small as well, i.e. some regularity is enforced. This optimisation

approach hence leads to regularisation procedures [3].

Here we take the view that our lack of knowledge or uncertainty

of the actual value of

the parameters can be described in a Bayesian way through a

probabilistic model [14, 37, 36].

The unknown parameter is then modelled as a random variable (RV)—also

called the prior model—and additional information on the

system through measurement or observation

changes the probabilistic description to the so-called posterior model.

The second approach is thus a method to update the probabilistic description

in such a way as to take account of the additional information, and the

updated probabilistic description is the parameter estimate,

including a probabilistic description of the remaining uncertainty.

It is well-known that such a Bayesian update is in fact closely related

to conditional expectation

[2, 9], and this will be the basis

of the method presented. For these and other probabilistic notions

see for example [27] and the references therein.

As the Bayesian update may be numerically

very demanding, we show computational procedures

to accelerate this update through methods based on

functional approximation or spectral representation

of stochastic problems [21]. These approximations

are in the simplest case known as Wiener’s so-called homogeneous

or polynomial chaos expansion

[38], which are polynomials in independent Gaussian RVs

—the ‘chaos’—and which

can also be used numerically in a Galerkin procedure

[8, 22, 21]. This approach

has been generalised to other types of RVs [39].

It is a computational variant of white noise analysis, which means

analysis in terms of independent RVs, hence the term ‘white noise’

[12, 13, 11], see also

[22, 28], and

[6] for here relevant results on stochastic

regularity. Here we describe computational extensions of this

approach to the inverse problem of Bayesian updating, see also

[25, 32, 26, 29].

To be more specific, let us consider the following situation:

we are investigating some physical system which

is modelled by an evolution equation for its state:

(1)

where describes the state of the system

at time lying in a Hilbert space (for the sake of

simplicity), is a—possibly non-linear—operator modelling

the physics of the system, and is some external

influence (action / excitation / loading). The model depends on some parameters

which are uncertain and which we would thus like to identify.

To have a concrete example of Eq. (1), consider the diffusion equation

(2)

with appropriate boundary and initial conditions, where

is a suitable domain. The diffusing quantity is (heat, concentration)

and the term models sinks and sources.

Similar examples will be used for the numerical

experiments in Section 4 and Section 5.

Here , the subspace

of the Sobolev space satisfying the essential boundary

conditions, and we assume that the diffusion coefficient is uncertain.

The parameters could be the positive diffusion coefficient

field , but for reasons to be explained fully later we prefer

to take , and assume .

Our main application focus are models described by partial differential

equations (PDEs) like Eq. (2), and discretised for

example by finite element procedures.

The updating methods have to be well defined and stable in a continuous

setting, as otherwise one can not guarantee numerical stability with

respect to the PDE discretisation refinement, see [36]

for a discussion of related questions. Due to this we describe the update

before any possible discretisation in the simplest Hilbert space setting.

On the other hand

no harm will result for the basic understanding if the reader wants to

view the occurring spaces as finite dimensional Euclidean spaces.

Now assume that we observe a function of

the state , and from this observation we would like to identify

the corresponding . In the concrete example Eq. (2) this could

be the value of at some points .

This is called the inverse problem, and

as the mapping is usually not invertible, the inverse

problem is ill-posed. Embedding this problem of finding the best

in a larger class by modelling our knowledge

about it with the help of probability theory, then in a Bayesian manner the

task becomes to estimate conditional expectations, e.g. see

[14, 37, 36]

and the references therein. The problem now is

well-posed, but at the price of ‘only’ obtaining probability

distributions on the possible values of , which now is modelled

as a -valued random variable (RV). On the other hand one

naturally also obtains information about the remaining uncertainty.

Predicting what the measurement

should be from some assumed is computing the forward

problem. The inverse problem is then approached by comparing the

forecast from the forward problem with the actual information.

Since the parameters of the model to be estimated are uncertain, all relevant

information may be obtained via their stochastic description.

In order to extract information from the posterior, most estimates take

the form of expectations w.r.t. the posterior.

These expectations—mathematically integrals, numerically to be evaluated

by some quadrature rule—may be computed via asymptotic,

deterministic, or sampling methods.

In our review of current work we

follow our recent publications [25, 32, 26, 29].

One often used technique is a

Markov chain Monte Carlo (MCMC) method [18, 7],

constructed such

that the asymptotic distribution of the Markov chain is the Bayesian

posterior distribution; for further information see [29]

and the references therein.

These approaches require a large number of samples in order

to obtain satisfactory results. Here

the main idea here is to perform the Bayesian update directly on the

polynomial chaos expansion (PCE) without any sampling

[25, 32, 23, 26, 29].

This idea has appeared independently in [1]

in a simpler context, whereas

in [34] it appears as a variant of the Kalman filter

(e.g. [15]).

A PCE for a push-forward of the posterior

measure is constructed in [24].

From this short overview it becomes apparent that

the update may be seen abstractly

in two different ways.

Regarding the uncertain parameters

(3)

where the set of elementary events is , a -algebra of

events, and a probability measure, one set of methods performs

the update by changing the probability measure and leaving the

mapping as it is, whereas the other set of methods leaves the

probability measure unchanged and updates the function .

In any case, the push forward measure on

defined by for a measurable

subset is changed from prior to posterior. For the

sake of simplicity we assume here that —the set containing possible

realisations of —is a Hilbert space. If the parameter is a RV,

then so is the state of the system Eq. (1). In order to avoid a

profusion of notation, unless there is a possibility of confusion,

we will denote the random variables which now take values

in the respective spaces and with the same symbol as

the previously deterministic quantities in Eq. (1).

In our overview on [29] spectral methods in

identification problems we show that Bayesian identification

methods [14, 37, 9, 36] are

a good way to tackle the identification problem, especially

when these latest developments in functional approximation methods

are used. In the series of papers [25, 32, 23, 26, 29], Bayesian updating has been

used in a linearised form, strongly related to the Gauss-Markov

theorem [17], in ways very similar to the well-known

Kalman filter [15]. This turns out to be a linearised version

of conditional expectation. Here we want to extend this

to a non-linear form, and show some examples of linear (LBU) and

non-linear (NLBU) Bayesian updates.

The organisation of the remainder of the paper is as follows:

in Section 2 we review the Bayesian update—classically defined via

conditional probabilities—and recall the link between conditional

probability measures and conditional expectation. We show how to

approximate this up to any desried polynomial degree, not only the

linearised version [17, 15] which was used in

[25, 32, 23, 26, 29].

The numerical realisation in terms of a functional or spectral

approximation—here we use the well known Wiener-Hermite chaos—is

shortly sketched in Section 3.

In Section 4 we then show some computational

examples with the linear version (LBU), whereas in Section 5

we show how to compute with the non-linear version. Some concluding

remarks are offered in Section 6.

2 Bayesian Updating

In the setting of Eq. (1) let us pose the following problem:

the parameters are uncertain or unknown.

By making observations at times

one would like to infer what they are. But we can not observe

the entity directly—like in Plato’s cave allegory we can only see

a ‘shadow’ of it, formally given by a ‘measurement operator’

(4)

at least this is our model of what we are measuring.

We assume that the space of possible measurements is a vector space,

which frequently may be regarded as finite dimensional,

as one can only observe a finite number of quantities.

Usually the observation of the ‘truth’

will deviate from what we expect to observe even if we knew the right

as Eq. (1) is only a model—so there is some model error

, and the measurement will be polluted by some measurement error

.

Hence we observe .

From this one would like to know what and are. For the

sake of simplicity we will only consider one error term

which subsumes all the errors.

The mapping in Eq. (4) is usually not invertible and hence the problem

is called ill-posed. One way to address this is via regularisation

(see e.g. [3]),

but here we follow a different track. Modelling our lack-of-knowledge

about and in a Bayesian way [37] by replacing them

with a - resp. -valued random variable (RV), the problem

becomes well-posed [36]. But of course one is looking now at the

problem of finding a probability distribution that best fits the data;

and one also obtains a probability distribution, not just one pair

and . Here we focus on the use of a linear Bayesian approach

[9] in the framework of ‘white noise’ analysis.

We also assume that the error is a -valued RV.

Please observe that although may be a deterministic

quantity—the unknown ‘truth’—the model for the observed

quantity therefore

becomes a RV as well.

The mathematical setup then is as follows: we assume that

is a measure space with -algebra and

with a probability measure , and that

and are random variables (RVs).

The corresponding expectation will be denoted by ,

giving the mean of the random variable, also denoted by

. The quantity is the

zero-mean or fluctuating part of the RV . The covariance between

two RVs and is denoted by , the

expected value of the tensor product of the fluctuating parts.

For simplicity, we shall also require to be a Hilbert space

where each vector is a possible realisation. This is in order to allow

to measure the distance between different ’s as the norm of their

difference, and to allow the operations of linear algebra to be

performed.

Bayes’s theorem is commonly accepted as a consistent way to incorporate

new knowledge into a probabilistic description [14, 37].

The elementary textbook statement of the theorem is about

conditional probabilities

(5)

where is some subset of possible ’s, and is the information

provided by the measurement. This becomes problematic when

the set has vanishing probability measure, but if all measures

involved have probability density functions (pdf), it may be formulated

as ([37] Ch. 1.5)

(6)

where is the pdf of , is the likelihood of

given , as a function of sometimes denoted by , and

(from German Zustandssumme)

is a normalising factor such that the conditional density

integrates to unity. These terms are in direct correspondence with

those in Eq. (5). Most computational approaches determine

the pdfs [20, 36, 16]. Please observe that

the model for the RV representing the error determines

the likelihood functions resp. .

However, to avoid the critical cases alluded to above, Kolmogorov already

defined conditional probabilities via conditional expectation, e.g. see

[2]. Given the conditional expectation

, the conditional

probability is easily recovered as ,

where is the characteristic function of the subset .

It may be shown that this extends the simpler formulation described by

Eq. (5) or Eq. (6) and is the more fundamental notion, which

we examine next.

2.1 Conditional expectation

The easiest point of departure for conditional expectation in our setting

is to define it not just for one piece of measurement —which may

not even possible unambigously—but for

sub--algebras . A sub--algebra

is a mathematical description of a reduced possibility of randomness,

as it contains fewer events than the full algebra .

The connection with a measurement is to take ,

the -algebra generated by the measurement .

These are all events which are consistent with possible observations of

some value for .

For RVs with finite variance—elements of —the space with the sub--algebra

is a closed subspace of the full space [2].

It represents the

RVs which are possible candidates to represent the posterior, as they

are consistent with any possible observation or measurement.

For RVs in

the conditional expectation is defined as

the orthogonal projection onto the closed subspace

, e.g. see [2].

This allows a simple geometrical interpretation: the difference

between the original RV and its projection has to be perpendicular

to the subspace (see Eq. (8)),

and the projection minimises the distance to the

original RV over the whole subspace (see Eq. (7)).

The square of this distance may

be interpreted as a difference in variance, tying conditional

expectation with variance minimisation; see for example

[27] and the references therein for basic descriptions

of conditional expectation.

As we have to deal with -valued RVs, a bit more formalism is needed:

define the space of -valued RVs

of finite variance, and set

for the -valued RVs with finite

variance on the sub--algebra , representing the new information.

The Bayesian update as conditional expectation is now simply formulated:

(7)

where is the orthogonal projector onto . The norm

on the Hilbert tensor product in Eq. (7) is as usually derived

from the inner product for ,

so that .

Already in [15] it was noted that the conditional expectation

is the best estimate not only for the loss function ‘distance squared’,

as in Eq. (7),

but for a much larger class of loss functions under certain distributional

constraints. However for the above loss function this is valid without

any restrictions.

Requiring the derivative of the quadratic loss function in Eq. (7) to

vanish—equivalently recalling the simple geometrical characterisation

mentioned just before about the orthogonality—one arrives at the well-known

orthogonality conditions. For later reference, we collect this result in

Proposition 1.

There is a unique minimiser to the problem in Eq. (7), denoted

by , and it is

characterised by the orthogonality condition

(8)

Proof.

Either by requiring the derivative of the loss function on the closed subspace to vanish, or by

remembering that the difference between and its best approximation

from is orthogonal to that subspace [17], one

arrives immediately at Eq. (8).

The existence and uniqueness of the best approximation follows from the fact that

is a closed subspace (as is

a closed subspace), hence a closed convex set, and the loss function is

continuous and strictly convex. Equivalently, this says that the projection

is continuous and orthogonal, i.e. its norm is equal to unity.

Alternatively, we may invoke the Lax-Milgram lemma for Eq. (8),

coerciveness and continuity are trivially satisfied on the subspace

, which is closed and hence a Hilbert space.

∎

Let us remark that Pythagoras’s theorem implies that

To continue, note that the Doob-Dynkin lemma

[2] assures us that if a RV like is

in the subspace , then

for some , the space of measurable functions

from to .

We state this key fact and the resulting new

characterisation of the conditional expectation in

Proposition 2.

The subspace is given by

(9)

Finding

the conditional expectation may be seen as rephrasing

Eq. (7) as:

(10)

Proof.

Follows directly from the Doob-Dynkin lemma.

∎

Then is called the updated, analysis,

assimilated, or posterior value,

incorporating the new information. This is the Bayesian update

expressed in terms of RVs instead of measures. It is the estimate of

the unknown parameters after the measurement has been performed.

2.2 Approximation of the conditional expectation

Computationally we will not be able to deal with the whole space ,

so we look at the effect of approximations. Assume that in

Eq. (10) is approximated by subspaces , where

is a parameter describing the level of approximation and

if , such that the subspaces

(11)

are closed and their union is dense ,

a consistency condition.

From Céa’s lemma we immediately get:

Proposition 3.

Define

(12)

Then the sequence converges to

:

(13)

Proof.

Well-posedness is a direct consequence of Proposition 1,

and the are orthogonal projections

onto the subspaces , hence their norms are all equal to

unity—a stability condition.

Application of Céa’s lemma then directly yields Eq. (13).

∎

Here we choose the subspaces of polynomials up to degree for the purpose

of approximation, i.e.

and we remark that in case is finite-dimensional—the usual case—then

the space of degree polynomials is a closed space.

We may write this as

(14)

where is symmetric

and -linear; and is the symmetric tensor product of

the ’s taken times with itself. Let us remark here that the form of

Eq. (14), given in monomials, is numerically not a good form—except

for very low —and straightforward use in computations is not recommended.

The relation Eq. (14) could be re-written in some orthogonal

polynomials—or in fact any other system of multi-variate functions; this

generalisation will be published elsewhere.

For the sake of conceptual simplicity, we stay wtih Eq. (14) and

then have that

(15)

is a function of the maps . The stationarity or orthogonality

condition Eq. (8) can then be written in terms of the .

We need the following abbreviations for any :

and

We may then characterise the in the following way:

Theorem 4.

With given by Eq. (15), the stationarity condition

Eq. (8) becomes for any ( the

Gâteaux derivative w.r.t. ):

(16)

which determine the and may be concisely written as

(17)

The Hankel operator matrix in the

linear equations Eq. (17) is symmetric and positive definite, hence

the system Eq. (17) has a unique solution.

Proof.

The relation Eq. (17) is the result of straightforward differentiation

in Eq. (16) (and division by ), and may be written in more detail as:

Symmetry of the operator matrix is obvious—the are the

coefficients—and positive definiteness follows

easily from the fact that it is the gradient of the functional in Eq. (16),

which is strictly convex.

∎

A la Penrose in ‘symbolic index’ notation—or the reader may just think of

indices in a finite dimensional space with orthonormal basis—the

system Eq. (16) can be given yet another form:

denote in symbolic index notation , and , then Eq. (17)

becomes, with the use of the Einstein convention of summation (a tensor contraction)

over repeated indices, and with the symmetry explicitly indicated:

(18)

We see in this representation that the matrix does not depend on —it is

identically block diagonal after appropriate reordering, which makes the solution

of Eq. (17) or Eq. (18) much easier.

Some special cases are:

for —constant functions, we do not use any information from the

measurement—we have from Eq. (17) or Eq. (18)

. One could argue

that this is the best approximation to in absence of any further information.

The case in Eq. (17) or Eq. (18) is more interesting,

allowing up to linear terms:

Remembering that and

analogous for , one obtains by tensor multiplication

in Eq. (19) with and

symbolic Gaussian elimination the Eq. (20).

(19)

(20)

This gives

(21)

(22)

where in Eq. (21) is the well-known Kalman gain operator

[15], so that finally

(23)

This is called the linear Bayesian update (LBU).

It is important to see Eq. (23) as a symbolic expression, especially

the inverse indicated there should not really be computed,

especially when is ill-conditioned or close to singular. The

inverse can in that case be replaced by the pseudo-inverse, or rather

the computation of , which is in linear algebra terms a least-squares

approximation, should be done with orthogonal transformations and not by

elimination. We will not dwell on these well-known matters here.

The case can still be solved symbolically, the system to be solved is

from Eq. (17) or Eq. (18):

After some symbolic elimination steps one obtains

with the Kalman gain operator from Eq. (21),

the third order tensors given in Eq. (24),

and given in Eq. (25),

and the fourth order tensor given

in Eq. (26):

(24)

(25)

(26)

where the single central dot ‘’ denotes as usual a contraction over

the appropriate indices, and a colon ‘:’ a double contraction. From this one easily obtains the solution

(27)

(28)

(29)

2.3 Prior information and mappings

In case one has prior information and a prior

estimate (forecast), and a new measurement comes in

generating via a subspace ,

one now needs a projection onto ,

with reformulation as an orthogonal direct sum

in order not to update twice with the nonzero part of .

The update / conditional expectation /

assimilated value is

where is the innovation, the orthogonal projection onto

. This is reminiscent of

Eq. (23), where the term may be regarded as the

prior information (before any measurement is performed) and replaced

here by , and the innovation there is , which is

here represented by .

The version of Theorem 4 is well-known,

and in conjunction with what was just stated about prior information is

of considerable practical importance; it is an extention of the

Kalman filter [15, 17, 27].

We rephrase this generalisation of the well-known Gauss-Markov

theorem from [17] Chapter 4.6, Theorem 3:

Theorem 5.

The update , minimising over all elements generated

by affine mappings (the up to case of Theorem 4) of

the measurement in the case with prior information and predicted

measurement is given from the observation by

(30)

where the notation is according to Eq. (15),

and the operator is the Kalman gain from Eq. (23).

This update is in some ways very similar to the

‘Bayes linear’ approach [9]. We point out that

and are RVs, i.e. this is an equation in , whereas the traditional Kalman filter—which

looks superficially just like Eq. (30) is an equation in .

Observe that

and that the error term is a RV. Hence the quantity is an RV, and

Eq. (30) is an equation between RVs. If the mean is taken in

Eq. (30), one obtains the familiar Kalman filter formula [15]

for the update of the mean, and one may show [25]

that Eq. (30) also contains the Kalman update for the covariance,

i.e. the Kalman filter is a low-order part of Eq. (30).

The computational strategy is now to replace and approximte the—only abstractly

given—computation of by the practically possible calculation

of as in Eq. (15). This means that we

approximate by by using ,

and rely on Proposition 3. This corresponds to some loss of

information from the measurement, but yields a managable computation.

If the assumptions of Proposition 3 are satisfied, then one

can expect for large enough that the terms in Eq. (15)

converge to zero, thus providing an error indicator on when a sufficient

accuracy has been reached.

In case the space generated by the measurements is not dense in

a residual error will thus remain, as the measurements do not contain enough

information to resolve our lack of knowledge about . Anyway,

finding is limited by the presence of the error ,

as obviously the error influences the update in Eq. (30).

If the measurement operator is approximated in some way—as it will be

in the computational examples to follow—this will introduce a new error,

further limiting the resolution.

It is maybe worthwhile to pursue the following idea: The mapping we try

to approximate is an orthogonal projection,

hence linear. This carries with it several suggestions on how to

change the update process.

Given a couple and measurement operator , one may change

the arrangement by mappings of or . On one hand one may consider

a—preferrably—injective map and choose

as parameter,

the measurement operator is then . This may

be useful as we want to perform essentially linear operations on like

the above mentioned projection and linear approximations to it, and

if the set where ‘lives’ is not a linear set, this is problematic.

We will come across this example in Section 4, where is positive—or

a symmetric positive definite tensor—and hence ‘lives’ on an open cone

in a vector space. There we will choose , and in

[29] we give some arguments why this may be meaningful,

as this transformation puts us in the tangent space of the positive cone,

which is a linear space.

On the other hand looking again at a given pair and , the linear map

is approximated by

from Eq. (14)—neglecting measurement error for the moment.

This means that when is nonlinear in

, the update map from Eq. (14) has to somehow

‘straighten’ the nonlinearity out. This opens the possibility to make

the update ‘easier’: we update not from , but from ,

where is chosen so that the composition

is ‘less nonlinear’. This means that in the computation of ,

we try to minimise the error of .

Finding a suitable —in some way an ‘inverse’

of —is not easy. Anyway, some preliminary examples where has been

chosen heuristically were very promising and will be reported elsewhere.

If the mapping is not injective, then

of course this can not be ‘ironed out’ by any mapping , as we would need

to undo the loss of information from being not injective—another sign

of ill-posedness. The mapping could be speculatively made into a set-valued

mapping to achieve this, but we would have, for a certain , to find all

to construct such that it distinguishes them, not an easy task.

We close this section by pointing out a little example connected to these

considerations—suggested to us by [35]—which is a bit

disturbing and shows the possible problems involved and that

one has to be a bit careful: Assume that is a single centred

Gaussian variable with variance , and

that the measurement operator is ,

i.e. all information about the sign is lost. Assume that

is independent of and also centred. Taking first the linear Bayesian update

(LBU) from Theorem 5 defined in Eq. (21), we have that—as

and

and hence and the LBU Eq. (30)

will not change anything; . Looking for the reason for this,

we observe that in the system Eq. (17) in Theorem 4—or in

Eq. (18)—the right-hand-side (rhs) is in the

-th equation. In our case this evaluates to

as for any . Obviously the are the

binomial coefficients. This means that in Eq. (17) or Eq. (18)

the rhs vanishes identically for any , and hence

all will vanish too; i.e. no matter what polynomial update we

take, always , and hence for all .

The loss of information about the sign is so intertwined with the measurement

that no update of the form Eq. (14) can undo it!

If we now come

back to the first idea of choosing a map as sketched above, we might chose

, then ;

which means we do not care about the sign,

as information about the sign is lost anyway. The rhs now is—again

neglecting measurement error for the sake of simplicity

as these are simply the moments of the half-normal or -distribution,

and hence one could now compute a polynomial update map for any .

One might think that in the formula for the Bayesian update of densities

Eq. (6) this kind of problem does not appear, but the difficulty comes

when one has

to compute the likelihood in Eq. (6). Given a measurement

we have to find all which might have produced it,

and this means that one has to compute the set ; so this is where the

difficulty appears then!

We now turn to some examples where we identify parameters in models of varying

complexity.

In Section 4 we will show several examples for the case of for

the update map , and in Section 5 an example for the case

.

3 Numerical realisation

In the instances where we want to employ the theory detailed in the

previous Section 2, the spaces and are usually infinite

dimensional, as is the space .

For an actual computation they have to be discretised or approximated

by finite dimensional spaces. In our examples we will chose finite

element discretisations and corresponding subspaces. Hence let

be an

-dimensional subspace with basis . An element

of will be represented by the vector such that . To avoid a profusion of notations, the corresponding

random vector in will also be denoted by .

The norm to take on

results from the inner product with ,

the Gram matrix of the basis. We will later choose an orthonormal basis, so that

is the identity matrix. Similarly, on

the inner product is

.

The space of possible measurements

can usually be taken to be finite dimensional (here ), whose elements are

similarly represented by a vector of coefficients .

On , representing , the Kalman gain operator in Theorem 5

in Eq. (30) becomes a matrix .

Then the update corresponding to Eq. (30) is

(31)

Here the covariances are ,

and similarly for . Often the measurement error is

independent of — actually uncorrelated would be sufficient—hence

and . We once more

recall our comments in Subsection 2.2 following Eq. (23)

regarding the inverse which also appears in Eq. (31). Recall that usually

the error model involves a regular covariance ,

so that is at

least theoretically regular.

It is important to emphasise that the theory presented in the forgoing Section 2

is independent of any discretisation. But one usually can still

not numerically compute with objects like , as is normally an

infinite dimensional space and has to be discretised. One well-known possibility

are samples, i.e. the RV is represented by its value at certain points

, and the points usually come from some quadrature rule. The well-known

Monte Carlo (MC) method uses random samples, the quasi-Monte Carlo (QMC) method uses

low discrepancy samples, and other rules like sparse grids (Smolyak rule) are possible.

Using MC samples in the context of the linear update Eq. (30)

is known as the Ensemble Kalman Filter (EnKF), see [29]

for a general overview in this context, and [4, 5] for

a thorough description and analysis. This method is concepyually fairly simple

and is currently

a favourite for problems where the computation of the predicted measurement

is difficult or expensive. It needs far fewer samples

for meaningful results than MCMC, but on the other hand it uses the linear

approximation inherent in Eq. (31).

Here we want to use so-called functional or spectral approximations, so

similarly as for , we pick a finite set of linearly independent

vectors in . As , these abstract vectors

are in fact RVs with finite variance. Here we will use the best known

example, namely Wiener’s polynomial chaos expansion (PCE) as basis

[38, 8, 12, 13, 19, 21],

this allows us to use Eq. (31) without sampling, see

[29, 25, 32, 23, 26], and also

[34, 1].

The PCE is an expansion in multivariate Hermite polynomials

[8, 12, 13, 19, 21]; we denote

by the multivariate polynomial in standard independent Gaussian RVs

,

where is the usual univariate Hermite polynomial, and

is a multi-index of generally infinite lenght but with only finitely many

entries non-zero. As ,

the infinite product is effectively finite and always well-defined.

The Cameron-Martin theorem assures us [12, 19, 13]

that the set of these polynomials is dense in ,

and in fact is a complete orthonormal system (CONS),

where is the product

of the individual factorials, also well-defined as except for finitely many

one has . So we may write with ,

and similarly for and all other RVs.

In this way the RVs are expressed as functions of other,

known RVs —hence the name functional

approximation—and not through samples.

The space may now be discretised by taking a finite subset of size , and setting . The

orthogonal projection onto is then simply

Projecting both sides of Eq. (34) is very

simple and results in

(35)

Obviously the projection commutes with the Kalman operator and

hence with its finite dimensional analogue . One may actually

concisely write Eq. (35) as

(36)

Elements of the discretised space thus may be written as

. The tensor representation is

, where the

are the unit vectors in , may be used

to express Eq. (35) or Eq. (36) succinctly as

(37)

again an equation between the tensor representations of some RVs,

where with from Eq. (31).

Hence the update equation is naturally in a tensorised form. This is

how the update can finally be computed in the PCE representation without

any sampling [29, 25, 30, 23].

Analogous statements hold for the forms of the update Eq. (14)

with higher order terms , and do not have to be repeated here. Let us

remark that these updates go very seamlessly with very efficient methods for

sparse or low-rank approximation of tensors, c.f. the monograph

[10] and the literature therein. These methods are PCE-forms

of the Bayesian update, and in particular the Eq. (37), because of

its formal affinity to the Kalman filter (KF), may be called the polynomial

chaos expansion based Kalman filter (PCEKF).

It remains to say how to compute the terms in the update equation

Eq. (14)—or rather the terms in the defining Eq. (17)

in Theorem 4—in this approach. Given the PCEs of the RVs, this is actually

quite simple as any moment can be computed directly from the PCE

[21, 25, 32].

A typical term

in the operator matrix Eq. (17), where , may be computed through

(38)

As here the are polynomials,

the last expectation in Eq. (38)

is finally over products of powers of pairwise independent normalised Gaussian variables,

which actually may be done analytically [12, 19, 13].

But some simplifications come from

remembering that , ,

the orthogonality relation , and that the Hermite polynomials

are an algebra. Hence , where the structure

coefficients are known analytically

[19, 21, 25, 32].

Similarly, for a typical right-hand-side term in Eq. (17) with one has

(39)

As these relations may seem a bit involved—they are actually just a bit intricate

combination of known terms—we show here how simple they become for

the case of the covariance needed in the linear update formula Eq. (30)

or rather Eq. (31):

(40)

(41)

Looking for example at Eq. (31) and our setup as explained in Section 1,

we see that the coefficients of or rather those of have to be computed from those of

. This propagation

of uncertainty through the system is known as uncertainty quantification (UQ),

e.g. [21] and the references therein. For the sake of brevity,

we will not touch further on this subject, which nevertheless is the bedrock

on which we built the whole computational procedure.

We next concentrate in Section 4 on examples of updating with

for the case in Eq. (14), whereas in Section 5

an example for the case in Eq. (14) will be shown.

4 The linear Bayesian update

All the examples in this section have been computed with the case

of up to linear terms in Eq. (14), i.e. this is the LBU with

PCEKF.

As the traditional Kalman filter is highly geared towards Gaussian

distributions [15], and also its Monte Carlo variant EnKF

which was mentioned in Section 3 tilts towards Gaussianity,

we start with a case—already described in [25]—where

the the quantity to be identified has a strongly

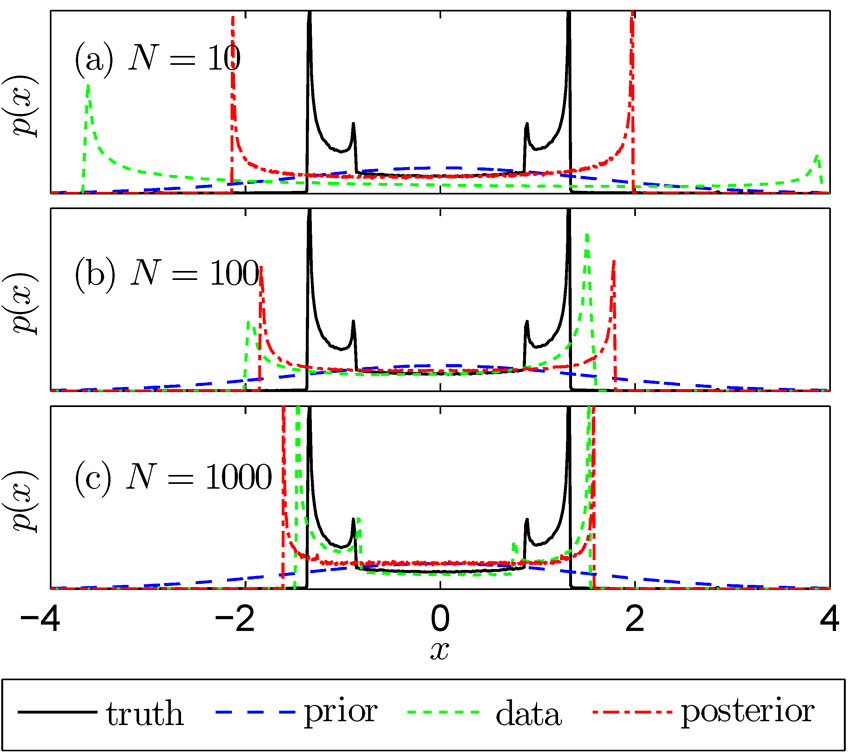

non-Gaussian distribution, shown in black—the ‘truth’—in Fig. 1.

The operator describing the system is the identity—we compute the quantity

directly, but there is a Gaussian measurement error. The ‘truth’ was

represented as a degree PCE.

We use the methods as described in Section 3, and here in particular

the Eq. (31) and Eq. (37), the PCEKF.

The update is repeated several times (here ten times)

with new measurements—see Fig. 1. The task is here

to identify the distribution labelled as ‘truth’ with ten updates of

samples (where was used), and we start with

a very broad Gaussian prior (in blue). Here we see the ability of

the polynomial based LBU, the PCEKF, to identify highly non-Gaussian distributions,

the posterior is shown in red and the pdf estimated from the samples in green;

for further details see [25].

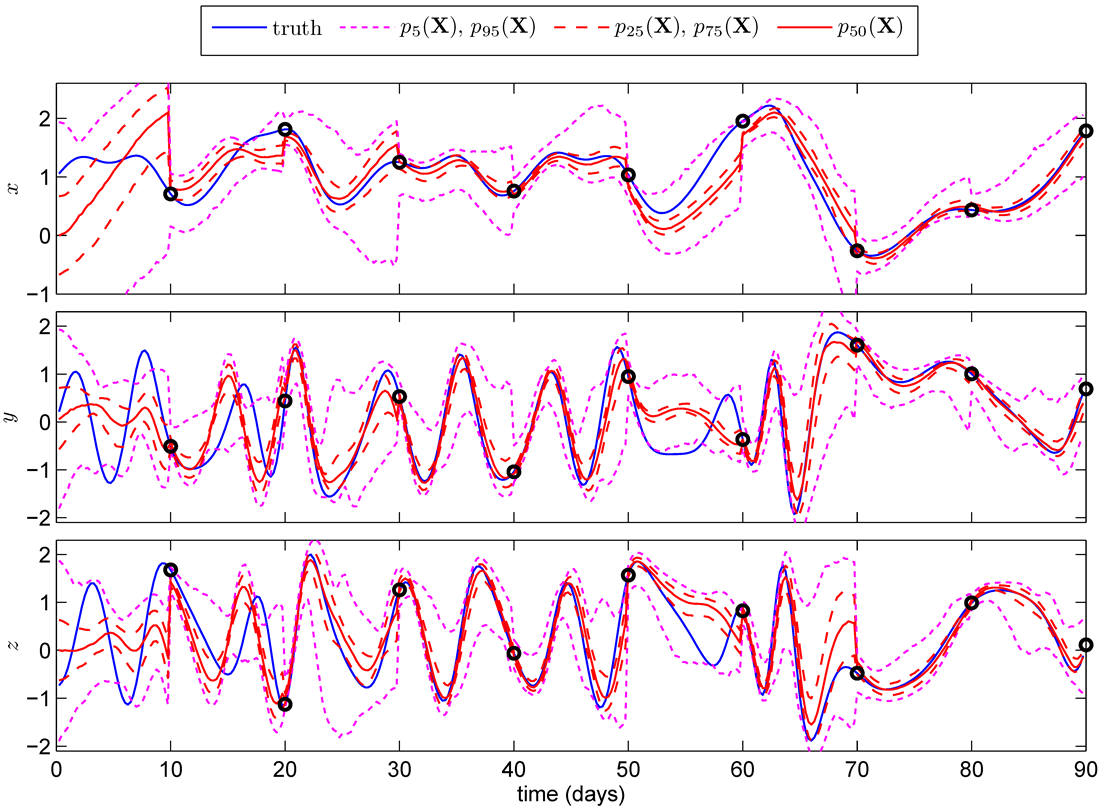

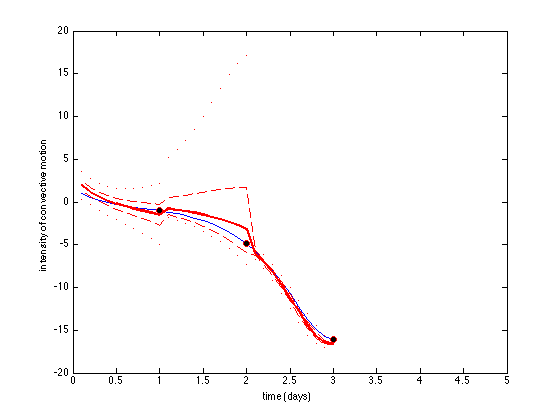

Figure 2: Time evolution of Lorenz-84 state and uncertainty with LBU [25]

The next example is also from [25], where the system is the well-known

Lorenz-84 chaotic model, a system of three nonlinear ordinary differential equations

operating in the chaotic regime. Remember that this was originally a model to

describe the evolution of some amplitudes of a spherical harmonic expansion of

variables describing world climate. As the original scaling of the variables has

been kept, the time axis in Fig. 2 is in days. Every ten days a

noisy measurement is performed and the state description is updated. In between

the state description evolves according to the chaotic dynamic of the system.

One may observe from Fig. 2 how the uncertainty—the width of the distribution

as given by the quantile lines—shrinks every time a measurement is performed, and

then increases again due to the chaotic and hence noisy dynamics.

Of course, we did not really measure world climate, but rather simulated the ‘truth’

as well, i.e. a virtual experiment, like the others to follow.

More details may be found in [25] and the references therein.

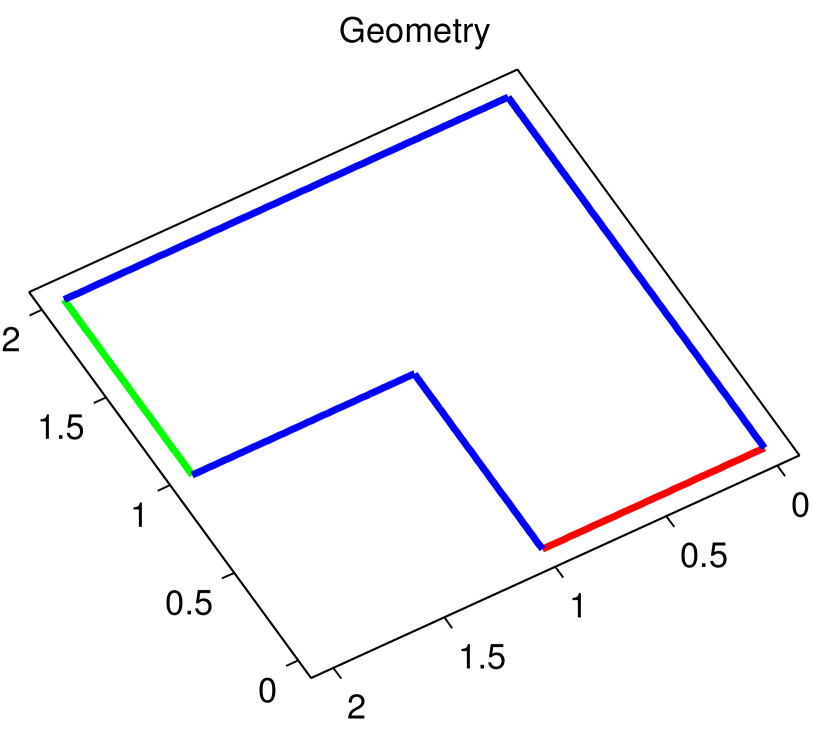

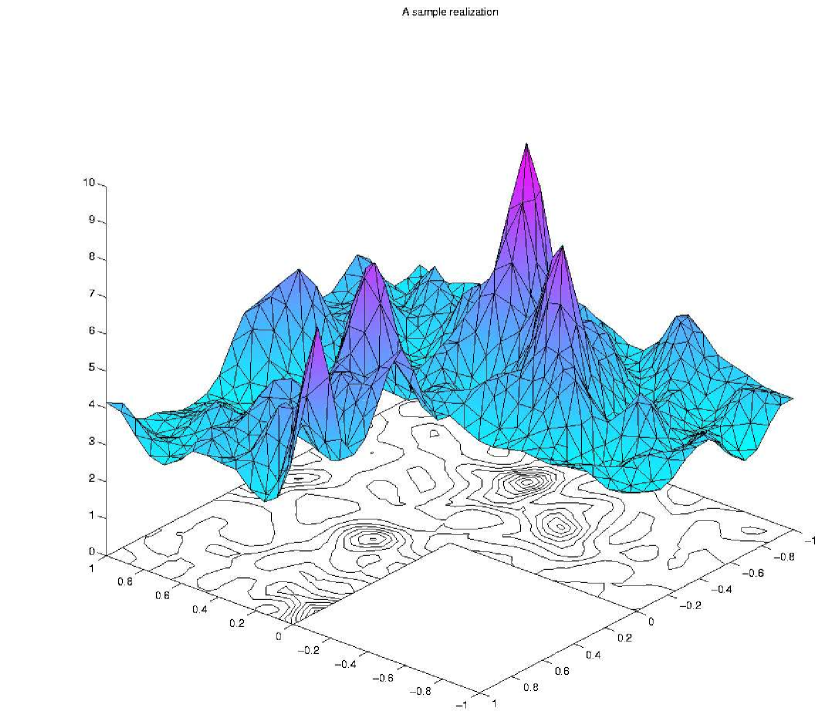

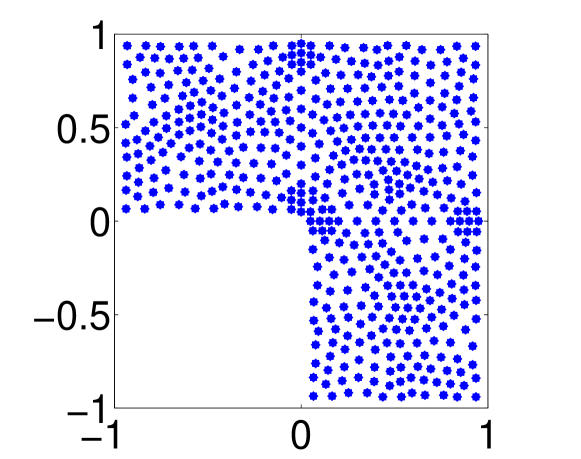

Figure 3: Diffusion domain Figure 4: Conductivity field

From [30, 32] we take the example shown in

Fig. 3, a linear stationary diffusion equation on an L-shaped

plane domain as alluded to in Section 1. The diffusion coefficient

in Eq. (2) is to be identified. As argued in [29],

it is better to work with as the diffusion coefficient has

to be positive, but the results are shown

in terms of .

One possible realisation of the diffusion coefficient

is shown in Fig. 4. More realistically, one should assume that

is a symmetric positive definite tensor field, unless one knows that

the diffusion is isotropic. Also in this case one should do the updating

on the logarithm. For the sake of simplicity we stay with the scalar case,

as there is no principal novelty in the non-isotropic case.

The virtual experiments use different right-hand-sides in Eq. (2),

and the measurement is the observation of the solution averaged over little patches,

two of these arrangements are shown in Fig. 5 and Fig. 6.

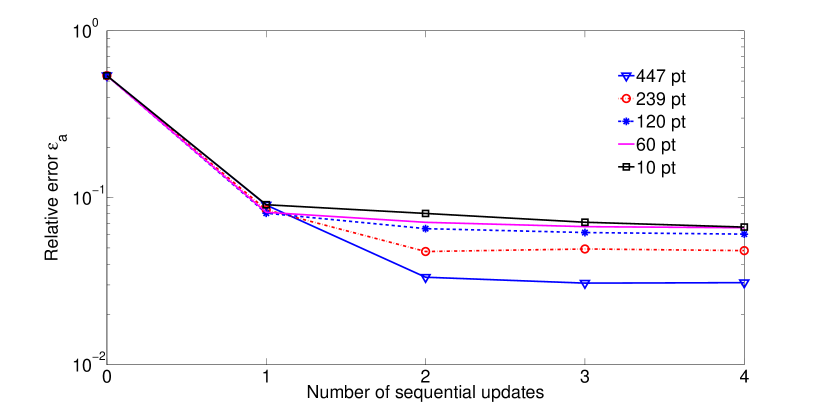

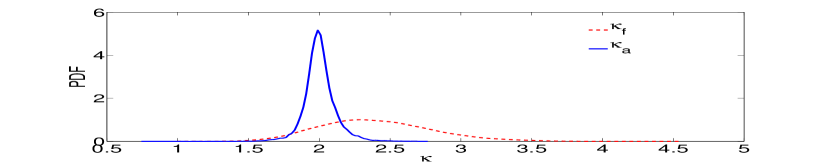

Figure 7: Convergence of identification [32] Figure 8: Prior and posterior [32]

In Fig. 7 one may observe the decrease of the error with successive

updates, but due to measurement error and insufficient information from just

a few patches, the curves level off, leaving some residual uncertainty.

The pdfs of the diffusion coefficient at some point in the domain before

and after the updating is shown in Fig. 8, the ‘true’ value at

that point was .

Further details can be found in [30, 32].

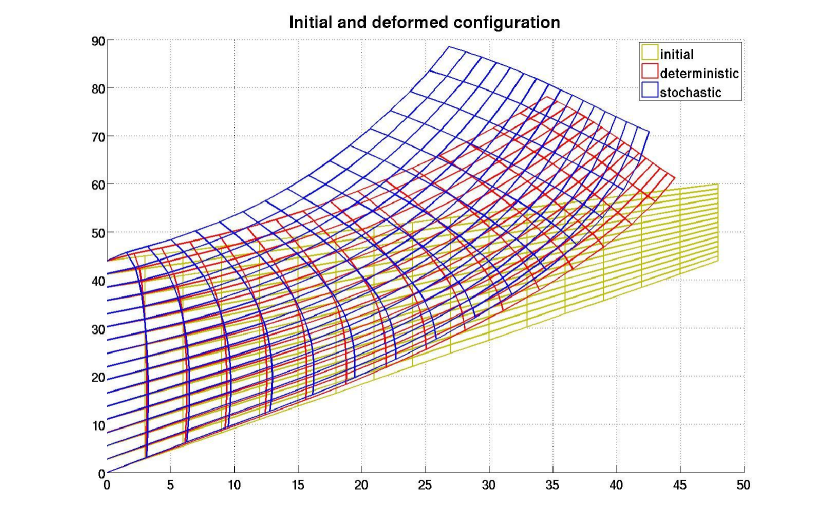

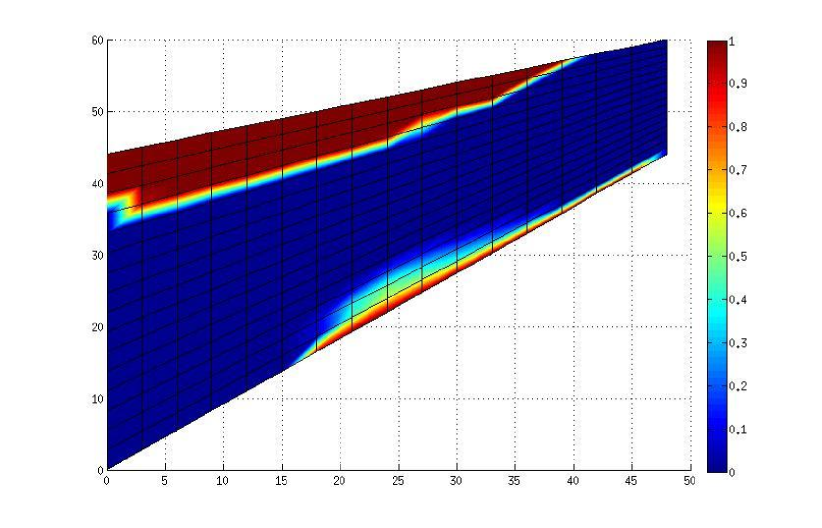

Figure 9: Deformations [31] Figure 10: Exceedance probability [31]

As a last example with LBU, we take a strongly nonlinear and also non-smooth

situation, namely elasto-plasticity with linear hardening and large deformations

and a Kirchhoff-St. Venant elastic material law

[31, 29, 33]. This example is known as Cook’s membrane,

and is shown in Fig. 9 with the undeformed mesh (initial), the deformed one

obtained by computing with average values of the elasticity and plasticity material

constants (deterministic), and finally the average result from a stochastic forward

calculation of the probabilistic model (stochastic), which is described by a

variational inequality [31, 33]. In Fig. 10 one may get another

impression of results of the forward model, the probability of the von Mises

stress being beyond a certain value.

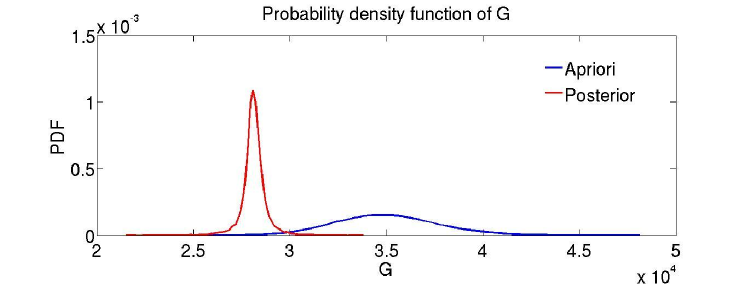

Figure 11: Prior and posterior of shear modulus [33]

The shear modulus has to be identified, which is made more difficult by the

non-smooth nonlinearity. In Fig. 11 one may see the prior and posterior

distributions of the shear modulus at one point in the domain. The ‘truth’ is

, and one may observe that the update is successful although

the prior density almost vanishes at .

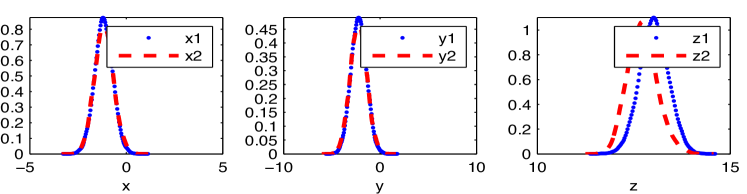

5 The nonlinear Bayesian update

Figure 12: Linear measurement: prior and posterior after one update

In this Section we want to show a computation with the case

of up to quadratic terms in Eq. (14). We go back to

the example of the chaotic Lorentz-84 [25] model already shown in

Section 4. For this kind of experiment it has several advantages:

it has only a three-dimensional state space, these are the uncertain ‘parameters’,

i.e. , the corresponding operator in the

abstract Eq. (1) is sufficiently nonlinear to make the problem difficult,

and adding to this we operate the equation in its chaotic regime, so that

new uncertainty is added between measurements.

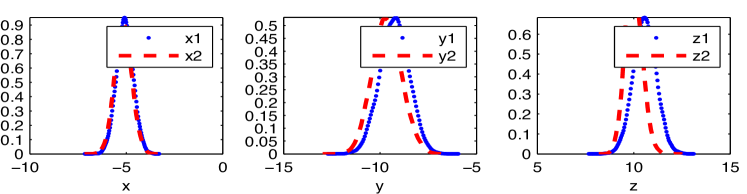

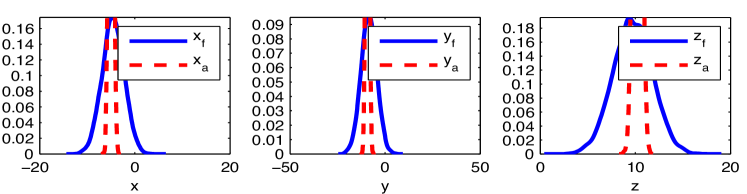

Figure 13: Linear measurement: Comparison posterior for LBU () and

NLBU () after one update

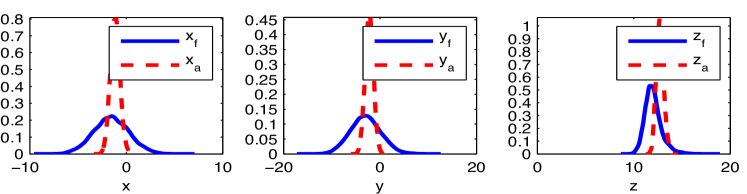

As a first set of experiments we take the measurement operator to be

linear in ; , i.e. we can observe the whole

state directly. At the moment we consider updates after each day—whereas

in Fig. 2 the updates were performed every 10 days.

The results for the pdfs of the state variables are shown in Fig. 12,

where the prior and the posterior pdf for a LBU after one update

are given. Then we do the same experiment, but with a quadratic nonlinear

BU (NLBU) with . The results for the posterior pdfs

are given in Fig. 13, where the

linear update is dotted in blue, and the full red line is the quadratic NLBU; there is

hardly any difference between the two. This might have been expected after

our discussion at the end of Subsection 2.3. If we go on to the second update—after

two days—some differences appear, the results for the posterior pdfs

are in Fig. 14.

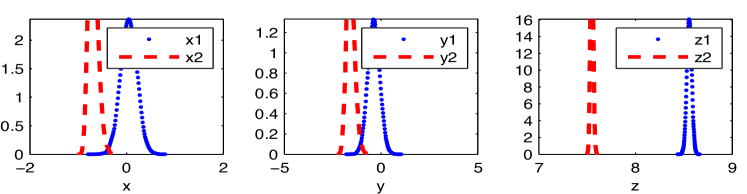

Figure 14: Linear measurement: Comparison posterior for LBU () and

NLBU () after second update

As the differences between LBU and NLBU with were small—we take this as an

indication that the LBU is not too inaccurate an approximation to the conditional

expectation—we change the experiment and

take a nonlinear measurement function, which is now cubic: .

As discussed at the end of Subsection 2.3, we now expect larger differences

between LBU and NLBU.

Figure 15: Cubic measurement: Comparison posterior for LBU () and

NLBU () after one update

These differences in posterior pdfs after one update may be gleaned

from Fig. 15, and they are indeed larger

than in the linear case Fig. 13, due to the strongly nonlinear

measurement operator.

Figure 16: Partial state trajectory with uncertainty and three updates

As the cubic is quite a strong nonlinearity, we performed a set of experiments

where the measurement function is ;

only a quadratic nonlinearity, but no loss of information about the sign like

in the small example at the end of Subsection 2.3. The updates are performed every

day, the Fig. 16, which shows the trajectory of one state variable,

corresponds in that way to Fig. 2.

Figure 17: Quadratic measurement: Comparison posterior for LBU () and

NLBU () after one update

The results for the -nd update are displayed for the posterior pdfs

in Fig. 17. This has to be compared Fig. 14, and the

differences are indeed much larger.

6 Conclusion

Here we have tried to show the connection between inverse problems and

uncertainty quantification. An abstract model of a system was introduced, together

with a measurement operator, which provides a possibility to predict—in a

probabilistic sense—a measurement. The framework chosen is that of Bayesian

analysis, where uncertain quantities are modelled as random variables.

New information leads to an update of the probabilistic description via

Bayes’s rule.

After elaborating on the—often not well-known—connection between conditional

probabilities as in Bayes’s rule and conditional expectation, we set out to

compute and—necessarily—approximate the conditional expectation. As a

polynomial approximation as chosen, there is the choice up to which degree

one should go. The case with up to linear terms—the linear Bayesian update—is

best known and intimately connected with the well-known Kalman filter. In addition,

we show how to compute approximations of higher order.

There are several possibilities on how one may choose a numerical realisation of

these theoretical concepts, and we decided on functional or spectral approximations.

It turns out that this approach goes very well with recent very efficient approximation

methods building on separated or so-called low-rank tensor approximations.

Starting with the linear Bayesian update, we show a series of examples of increasing

complexity. The method works well in all cases. One of the examples is then chosen

to show the nonlinear Bayesian update, where we go up to quadratic terms. A series

of experiments is chosen with different measurement operators, which have quite

a marked influence on whether the linear and quadratic update are close to

each other.

References

[1]

E. D. Blanchard, A. Sandu, and C. Sandu, A polynomial chaos-based

Kalman filter approach for parameter estimation of mechanical systems,

Journal of Dynamic Systems, Measurement, and Control 132 (2010),

no. 6, 061404, doi:10.1115/1.4002481.

[2]

A. Bobrowski, Functional analysis for probability and stochastic

processes, Cambridge University Press, Cambridge, 2005.

[3]

H. W. Engl, M. Hanke, and A. Neubauer, Regularization of inverse

problems, Kluwer, Dordrecht, 2000.

[4]

G. Evensen, Data assimilation — the ensemble Kalman filter,

Springer, Berlin, 2009.

[5]

, The ensemble Kalman filter for combined state and parameter

estimation, IEEE Control Systems Magazine 29 (2009), 82–104, doi:10.1109/MCS.2009.932223.

[6]

J. Galvis and M. Sarkis, Regularity results for the ordinary product

stochastic pressure equation, SIAM Journal on Mathematical Analysis

44 (2012), 2637–2665, doi:10.1137/110826904.

[7]

D. Gamerman and H. F. Lopes, Markov Chain Monte Carlo: Stochastic

simulation for bayesian inference, Chapman & Hall, Boca Raton, FL, 2006.

[8]

R. Ghanem and P. D. Spanos, Stochastic finite elements—a spectral

approach, Springer, Berlin, 1991.

[9]

M. Goldstein and D. Wooff, Bayes linear statistics—theory and methods,

Wiley Series in Probability and Statistics, John Wiley & Sons, Chichester,

2007.

[10]

W. Hackbusch, Tensor spaces and numerical tensor calculus, Springer,

Berlin, 2012.

[11]

T. Hida, H. H. Kuo, J. Potthoff, and L. Streit, White noise—an infinite

dimensional calculus, Kluwer, Dordrecht, 1999.

[12]

H. Holden, B. Øksendal, J. Ubøe, and T.-S. Zhang, Stochastic

partial differential equations, Birkhäuser, Basel, 1996.

[13]

S. Janson, Gaussian Hilbert spaces, Cambridge Tracts in Mathematics,

129, Cambridge University Press, Cambridge, 1997.

[14]

E. T. Jaynes, Probability theory, the logic of science, Cambridge

University Press, Cambridge, 2003.

[15]

R. E. Kálmán, A new approach to linear filtering and prediction

problems, Transactions of the ASME—J. of Basic Engineering (Series D)

82 (1960), 35–45.

[16]

A. Kučerová and H. G. Matthies, Uncertainty updating in the

description of heterogeneous materials, Technische Mechanik 30

(2010), no. 1–3, 211–226.

[17]

D. G. Luenberger, Optimization by vector space methods, John Wiley &

Sons, Chichester, 1969.

[18]

N. Madras, Lectures on Monte Carlo methods, American Mathematical

Society, Providence, RI, 2002.

[19]

P. Malliavin, Stochastic analysis, Springer, Berlin, 1997.

[20]

Y. M. Marzouk, H. N. Najm, and L. A. Rahn, Stochastic spectral methods

for efficient Bayesian solution of inverse problems, Journal of

Computational Physics 224 (2007), no. 2, 560–586, doi:10.1016/j.jcp.2006.10.010.

[21]

H. G. Matthies, Uncertainty quantification with stochastic finite

elements, Encyclopaedia of Computational Mechanics (E. Stein, R. de Borst,

and T. J. R. Hughes, eds.), John Wiley & Sons, Chichester, 2007, doi:10.1002/0470091355.ecm071.

[22]

H. G. Matthies and A. Keese, Galerkin methods for linear and nonlinear

elliptic stochastic partial differential equations, Computer Methods in

Applied Mechanics and Engineering 194 (2005), no. 12-16, 1295–1331.

MR MR2121216 (2005j:65146)

[23]

H. G. Matthies, A. Litvinenko, O. Pajonk, B. V. Rosić, and E. Zander,

Parametric and uncertainty computations with tensor product

representations, Uncertainty Quantification in Scientific Computing (Berlin)

(A. Dienstfrey and R. Boisvert, eds.), IFIP Advances in Information and

Communication Technology, vol. 377, Springer, 2012, pp. 139–150, doi:10.1007/978-3-642-32677-6.

[24]

T. A. E. Moselhy and Y. M. Marzouk, Bayesian inference with optimal

maps, Journal of Computational Physics 231 (2012), 7815–7850,

doi:10.1016/j.jcp.2012.07.022.

[25]

O. Pajonk, B. V. Rosić, A. Litvinenko, and H. G. Matthies, A

deterministic filter for non-Gaussian Bayesian estimation —

applications to dynamical system estimation with noisy measurements, Physica

D 241 (2012), 775–788, doi:10.1016/j.physd.2012.01.001.

[26]

O. Pajonk, B. V. Rosić, and H. G. Matthies, Sampling-free linear

Bayesian updating of model state and parameters using a square root

approach, Computers and Geosciences 55 (2013), 70–83, doi:10.1016/j.cageo.2012.05.017.

[27]

A. Papoulis, Probability, random variables, and stochastic processes,

third ed., McGraw-Hill Series in Electrical Engineering, McGraw-Hill, New

York, 1991.

[28]

L. Roman and M. Sarkis, Stochastic Galerkin method for elliptic

SPDEs: A white noise approach, Discrete Cont. Dyn. Syst. Ser. B 6

(2006), 941–955.

[29]

B. V. Rosić, A. Kučerová, J. Sýkora, O. Pajonk, A. Litvinenko, and

H. G. Matthies, Parameter identification in a probabilistic setting,

Engineering Structures 50 (2013), 179–196, doi:10.1016/j.engstruct.2012.12.029.

[30]

B. V. Rosić, A. Litvinenko, O. Pajonk, and H. G. Matthies, Direct

Bayesian update of polynomial chaos representations, Informatikbericht

2011-02, Technische Universität Braunschweig, Brunswick, 2011, Available

from: http://www.digibib.tu-bs.de/?docid=00039000.

[31]

B. V. Rosić, Variational Formulations and Functional Approximation Algorithms in Stochastic Plasticity of Materials, PhD Thesis,

Technische Universität Braunschweig, Brunswick, 2013, Available

from: http://www.digibib.tu-bs.de/?docid=00052794.

[32]

, Sampling-free linear Bayesian update of polynomial chaos

representations, Journal of Computational Physics 231 (2012),

5761–5787, doi:10.1016/j.jcp.2012.04.044.

[33]

B. V. Rosić and H. G. Matthies, Identification of properties of

stochastic elastoplastic systems, Computational Methods in Stochastic

Dynamics (Berlin) (M. Papadrakakis, G. Stefanou, and V. Papadopoulos, eds.),

Computational Methods in Applied Sciences, vol. 26, Springer, 2013,

pp. 237–253, doi:10.1007/978-94-007-5134-7\_14.

[34]

G. Saad and R. Ghanem, Characterization of reservoir simulation models

using a polynomial chaos-based ensemble Kalman filter, Water Resources

Research 45 (2009), W04417, doi:10.1029/2008WR007148.

[35]

B. Sprungk, personal communication, November 2013.

[36]

A. M. Stuart, Inverse problems: A Bayesian perspective, Acta Numerica

19 (2010), 451–559, doi:10.1017/S0962492910000061.

[37]

A. Tarantola, Inverse problem theory and methods for model parameter

estimation, SIAM, Philadelphia, PA, 2004.

[38]

N. Wiener, The homogeneous chaos, American Journal of Mathematics

60 (1938), no. 4, 897–936.

[39]

D. Xiu and G. E. Karniadakis, The Wiener-Askey polynomial chaos for

stochastic differential equations, SIAM Journal of Scientific Computing

24 (2002), 619–644.