On the asymptotic behavior of a Boltzmann-type price formation model

Martin Burger11Institute for Computational and Applied Mathematics, University of Münster, Einsteinstrasse 62, 48149 Münster, Germany

, Luis Caffarelli22University of Texas at Austin, 1 University Station, C120, Austin, Texas 78712-1082, USA

, Peter A. Markowich33 4700 King Abdullah University of Science and Technology, Thuwal 23955-6900, Kingdom of Saudi Arabia

and Marie-Therese Wolfram3

Abstract.

In this paper we study the asymptotic behavior of a Boltzmann type price formation

model, which describes the trading dynamics in a financial market. In many of these markets

trading happens at high frequencies and low transactions costs. This observation motivates the study

of the limit as the number of transactions tends to infinity, the transaction cost to zero and

. Furthermore we illustrate the

price dynamics with numerical simulations.

1. Introduction

According to O’Hara [9] financial markets are characterized by two functions: first by providing

liquidity and second by facilitating the price. The evolution of the price emerges from the microscopic

trading strategies of the players and the trading system considered. High frequency trading (HFT) is an

automated trading strategy, which is carried out by computers that place and withdraw orders within

milli- or even microseconds. In 2012 HFT accounted for approximately of the overall US equity trading volume.

This note focuses on the asymptotic behavior of markets, where the price dynamics of a traded good

are determined by the following situation: Consider a large number of vendors and a large number of buyers trading a specific good. If a buyer and a vendor agree on a price a transaction takes place.

The price of this transaction is given by a positive constant .

After the transaction, the buyer and vendor immediately switch places. Since the actual cost for the buyer is ,

he/she will sell the good for at least that price. The profit for the vendor is , hence he/she will

try to buy the good for a price lower than .

Based on the situation described above Lasry & Lions [7] proposed the following parabolic free boundary price formation model:

(1.1a)

(1.1b)

The functions and denote the density of buyers and vendors and the transaction costs.

The agreed price enters as a free boundary and . Trading events take only place at

the price , since the density of buyers and vendors is zero for prices smaller or larger than . The Lasry & Lions model

was analyzed in a series of papers, see [8, 2, 3, 4, 5].

Lasry & Lions motivated their model using mean field game theory, but did not discuss its microscopic origin.

The lack of understanding system (1.1) on the microscopic level motivated further research in this direction. In

[1] we considered a simple agent based model with standard stochastic price fluctuations and discrete trading events.

This Boltzmann-type price formation (BPF) model reads as

(1.2a)

(1.2b)

with initial data

(1.2c)

independent of . In system (1.2) the parameter denotes the transaction rate and the diffusivity.

The total number of transactions at a price is given by

(1.3)

One of the fundamental differences between (1.1) and (1.2)

is the fact that trading events in the first take only place at the price . In BPF (1.2) a good

can be traded at any price, with a rate given by (1.3). Then the mean, median and

maximum of gives an estimate for the price.

There is however a strong connection between the BPF model (1.2) and (1.1). We showed

that solutions of (1.2) converge

to solutions of (1.1) as the transaction rate tends to infinity, see [1].

This finding motivated further research on different asymptotic limits, for example by considering high trading

frequencies and little transaction costs. This market behavior corresponds to the case ,

with . For studying this limit rewrite system (1.2) as

In this note we analyze the behavior of (1.5) as and illustrate the results with

numerical simulations. The note is organized as follows: in Section 2 we discuss the general

structure of the BPF model. We identify the limiting solutions of the Boltzmann price formation model (1.5)

in Section 3. Finally we illustrate

the asymptotic behavior of solutions with numerical simulations in Section 4.

2. Structure of the Model

We start by highlighting some structural aspects of (1.2), which also clarify certain steps in the previous analysis in [1, 2, 3]. The general understanding of the structure will serve as a basis for future generalizations and modifications and shall be used in the analysis of the asymptotic case later on. W.l.o.g. we set throughout this paper.

Let denote the differential operator , and and the shift-operators

In the setting of kinetic equations and are to be interpreted as the gain terms in the collision operators.

A key property, which allows to derive heat equations for transformed variables, is that commutes with the collision operators. Hence by defining the formal Neumann series

(2.2)

we find that

(2.3a)

(2.3b)

Then solves the heat equation. Note that this transformation was already used for the L&L model (1.1) in [2, 3]

and serve as a key feature of the performed analysis. There the authors motivated the transformation by the structure of the Dirac- terms rather than by inverting the collision operator. Note also that the computations above are purely formal. Since and have norm equal to one, the convergence of the Neumann series is not automatically guaranteed and needs to be verified, see [1].

Moreover, also

(2.4a)

(2.4b)

solve the heat equation. This transformation was used, again without the above interpretation in [1].

In the special case of the operators above, we have and in the scalar product even , i.e. and are unitary operators. Then

i.e. we simply have . Note that this structure was exploited in case of the Lasry & Lions model (1.1) in [2, 3] to derive a-priori estimates.

3. Asymptotic behavior when trading with high frequencies

In this Section we study the limiting behavior of system (1.5) as . The limiting

analysis is done in two steps: first by considering the special equilibrated state of system (1.5) and then

the full system.

Throughout this paper we make the following assumptions. Let the initial datum and satisfy:

(A)

on and ,

Let , then system (1.5) reads (omitting the tilde)

(3.1a)

(3.1b)

Next we reformulate (3.1) for the new variables and , i.e.

(3.2a)

(3.2b)

System (3.2) can be considered either on the whole line or a bounded domain . Note

that the bounded interval corresponds to the shifted and scaled interval , where denotes the

maximum price. In the later case system (3.2) is supplemented with no flux boundary conditions of the form

(3.2c)

which are equivalent to no-flux boundary conditions for (3.1). Throughout this note we consider system (3.1) on the bounded domain with no-flux boundary conditions (3.2c)

only.

Proposition 3.1.

Let and and satisfy (A) and .

Then system (3.2) has a unique smooth solution . Furthermore for all .

Note that the functions and solve transport diffusion equations, which preserve non-negativity. Trivially

and therefore the inequality holds.

3.1. Special case

We consider the special case as a first step towards understanding the asymptotic

behavior of (3.1). Hence it corresponds to the equilibrated solution of the heat equation

(3.2a) on the bounded domain with no flux boundary conditions and appropriately

chosen initial datum. Then system (3.2) reduces to the viscous Burgers’ equation

(3.3a)

(3.3b)

The analytic behavior of the classical viscous Burgers’ equation (with viscosity ) for small viscosity in the long-time limit

was studied in [10, 6]. The authors showed that a reversal of the limiting passages and

gives different limiting profiles. Note however that the time scaling of (3.3) is different. Equation (3.3a) is a viscous Burgers’ equation on a short time scale, a case not considered in the literature so far.

Monotonicity behavior and a-priori estimates of the solution :

Next we discuss monotonicity properties and a-priori estimates for the solution , which shall be used in the identification of the limiting case .

Lemma 3.2.

Let , and let the initial datum . Then the solution of (3.3) satisfies .

Proof.

We introduce the function , which solves

(3.4)

with at . Then the standard maximum principle implies that does not attain a positive

maximum inside the parabolic domain. Furthermore the solution depends continuously on the data, which yields the

desired estimate.

∎

Let us consider (3.3) on the bounded domain with no-flux boundary conditions. Then the following a-priori

estimate for the first order moment holds:

Therefore we conclude

using that .

In the limit we obtain that

Since , this implies that

for . From these estimates we deduce

(3.5)

for .

Identification of the limiting function for :

Finally estimate (3.5) allows us to identify the limiting functions.

Theorem 3.3.

Let assumption (A) be satisfied. Let and the mass of buyers and vendors. Then there exists a unique limit of the solutions of equation (3.3) as . The limit is given by

(3.6)

Proof.

First we observe that the total mass of and is conserved in time. Since the initial functions and satisfy

assumption (A), there exists a constant , such that . Hence

for all and the limiting function cannot jump up from to .

Using estimate (3.5) we conclude that the limiting function can only take the values and has a single

jump down from to at . The location of the jump (which corresponds to the stationary

price of the traded good) is determined by the conservation of mass, i.e.

Next we identify the limiting solutions for the full system (3.2),

using the same arguments as in the previous subsection.

Lemma 3.4.

Let , and let the initial datum satisfy assumption (A).

Then

The proof follows the arguments of the previous subsection. From Lemma 3.4 we conclude that

(3.7)

Next we show that the function can not have a jump up from to . To do so we consider the function , which satisfies

(3.8)

Then the standard maximum principle implies that and

Therefore cannot have a jump upward and we deduce that the limiting function can be written as

(3.9)

where denotes the position of the jump, i.e. the price of the traded good. It is uniquely determined

for all by

(3.10)

The previous calculations lead to the following theorem:

Theorem 3.5.

Let assumption (A) be satisfied. Then there exist unique limiting functions of system (3.2)

as , which are given by

where is determined by (3.10) and is the solution of the heat equation (3.2a) with

homogeneous Neumann boundary conditions.

Remark 3.6.

The behavior of the price is determined by the conservation of mass. This implies that

Differentiation of the later with respect to time yields .

Hence we deduce that the evolution of the price in time is given by

(3.11)

The function solves the heat equation and converges exponentially fast to its steady state, given by

This implies exponential convergence of the price , since .

4. Numerical simulations

In this last section we illustrate the behavior of the limiting system with numerical experiments.

All simulations are performed on the interval with no-flux boundary conditions

(3.2c). We split the interval into equidistant intervals for size .

System (3.2) is discretized using a finite difference discretization, i.e.

(4.1a)

(4.1b)

The resulting system of ODEs is solved using an explicit 4th-order Runge-Kutta method (implemented

within the GSL library).

We illustrate the behavior of system (3.2) for a not well prepared initial data and

, i.e. the function is split into two groups with in between. We choose the following

set of parameters

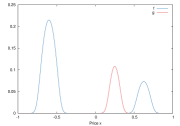

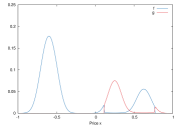

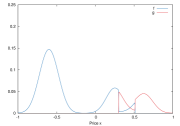

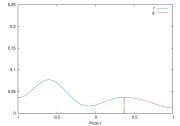

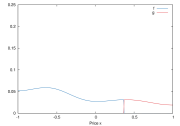

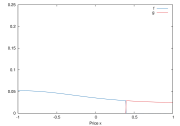

The evolution of both function is illustrated in Figure 1.

(a)

(b)

(c)

(d)

(e)

(f)

Figure 1. Evolution of the buyer and vendor density in the case of not-well prepared initial data

We observe the fast segregation of and and the formation of a unique interface, which corresponds

to the price in time. This behavior is not unexpected since system (3.1) has

a similar structure as classical segregation or reaction-diffusion models. Furthermore we observe

a fast equilibration of the price in time, as discussed in Remark 3.6.

5. Conclusion

In this paper we study the asymptotic behavior of a Boltzmann type price formation model, which

describes the trading dynamics in a financial market with high trading frequencies and low transaction

costs. We identify the limiting solutions as the number of transactions tends to infinity and observe

an exponentially fast equilibration of the price in time. Numerical simulations illustrate that

uneconomic situations, like trading at different prices, are ’corrected’ quickly. Hence we conclude

that small fluctuations in the trading frequency or the transaction costs influence the price on

a very short time scale only.

References

[1]M. Burger, L. Caffarelli, P. A. Markowich, and M.-T. Wolfram, On a

boltzmann-type price formation model, Proceedings of the Royal Society A:

Mathematical, Physical and Engineering Science, 469 (2013).

[2]L. A. Caffarelli, P. A. Markowich, and J.-F. Pietschmann, On a price

formation free boundary model by Lasry and Lions, C. R. Math. Acad. Sci.

Paris, 349 (2011), pp. 621–624.

[3]L. A. Caffarelli, P. A. Markowich, and M.-T. Wolfram, On a price

formation free boundary model by Lasry and Lions: the Neumann problem,

C. R. Math. Acad. Sci. Paris, 349 (2011), pp. 841–844.

[4]L. Chayes, M. d. M. González, M. P. Gualdani, and I. Kim, Global

existence and uniqueness of solutions to a model of price formation, SIAM J.

Math. Anal., 41 (2009), pp. 2107–2135.

[5]M. d. M. González and M. P. Gualdani, Asymptotics for a free

boundary model in price formation, Nonlinear Anal., 74 (2011),

pp. 3269–3294.

[6]Y. J. Kim and A. E. Tzavaras, Diffusive -waves and

metastability in the Burgers equation, SIAM J. Math. Anal., 33 (2001),

pp. 607–633 (electronic).

[7]J.-M. Lasry and P.-L. Lions, Mean field games, Jpn. J. Math., 2

(2007), pp. 229–260.

[8]P. A. Markowich, N. Matevosyan, J.-F. Pietschmann, and M.-T. Wolfram,

On a parabolic free boundary equation modeling price formation, Math.

Models Methods Appl. Sci., 19 (2009), pp. 1929–1957.

[9]M. O’Hara, Market Microstructure Theory, Wiley, Mar. 1998.

[10]J. Smoller, Shock waves and reaction-diffusion equations, vol. 258

of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of

Mathematical Sciences], Springer-Verlag, New York, second ed., 1994.

Acknowledgement.

MTW acknowledges support from the Austrian Science Foundation FWF via the Hertha-Firnberg project T456-N23.