Input design for Bayesian identification of non-linear state-space models

Abstract

We propose an algorithm for designing optimal inputs for on-line Bayesian identification of stochastic non-linear state-space models. The proposed method relies on minimization of the posterior Cramér Rao lower bound derived for the model parameters, with respect to the input sequence. To render the optimization problem computationally tractable, the inputs are parametrized as a multi-dimensional Markov chain in the input space. The proposed approach is illustrated through a simulation example.

AND , , , , ††thanks: This article has been published in: Tulsyan, A, S.R. Khare, B. Huang, R.B. Gopaluni and J.F. Forbes (2013). Bayesian identification of non-linear state-space models: Part I- Input design. In: Proceedings of the 10th IFAC International Symposium on Dynamics and Control of Process Systems. Mumbai, India. ††thanks: This work was supported by the Natural Sciences and Engineering Research Council (NSERC), Canada.

1 Introduction

Over the last decade, great progress has been made within the statistics community in overcoming the computational issues, and making Bayesian identification tractable for a wide range of complicated models arising in demographic and population studies, image processing, and drug response modelling (Gilks et al. (1995)). A detailed exposition of Bayesian identification methods can be found in Kantas et al. (2009). This paper is directed towards the class of on-line methods for Bayesian identification of stochastic non-linear SSMs, the procedure for which is briefly introduced here first. Let and be and valued stochastic processes, and let be the sequence of inputs in , such that the state is an unobserved or unmeasured process, with initial density and transition density :

| (1) |

is an unobserved process, but is observed through , such that is conditionally independent given , with marginal density :

| (2) |

in (1) and (2) is a vector of unknown model parameters, such that is an open subset of . All the densities are with respect to suitable dominating measures, such as Lebesgue measure. Although (1) and (2) represent a wide class of non-linear time-series models, the model form and the assumptions considered in this paper are given below

| (3) |

where is a vector of static parameters.

Assumption 1.

and are mutually independent sequences of independent random variables known a priori in their distribution classes (e.g., Gaussian) and parametrized by a known and finite number of moments.

Assumption 2.

are such that in the open sets and , is and , respectively, and in , is , and in and , is , and is , where .

Assumption 3.

For any random sample and satisfying (3), and have rank and , respectively, such that using implicit function theorem, and do not involve any Dirac delta functions.

For a generic sequence , let . Let be the true, but unknown parameter vector generating a measurement sequence given , such that and . In Bayesian identification of (3), the problem of estimating the parameter vector in real-time, given a sequence of input-output data is formulated as a joint state and parameter estimation problem. This is done by ascribing a prior density , such that , and computing , where: is a valued extended Markov process with and . The inference on then relies on the marginal posterior . Note that by a judicious choice of the input sequence , can be ‘steered’ in order to yield , which gives more accurate inference on . This is called the input design problem for Bayesian identification or simply, the Bayesian input design problem. A detailed review on this subject can be found in Chaloner and Verdinelli (1995).

Bayesian input design for linear and non-linear regression models is an active area of research (see Huan and Marzouk (2012), Kück et al. (2006), Müller and Parmigiani (1995) and references cited therein); however, its extension to SSMs has been limited. Recently, Bayesian input design procedure for non-linear SSMs, where is completely observed was developed by Tulsyan et al. (2012). Despite the success with regression models, to the best of authors’ knowledge, no known Bayesian input design methods are available for identification of stochastic non-linear SSMs. This is due to the unobserved state process , which makes the design problem difficult to solve.

This paper deals with the Bayesian input design for identification of stochastic SSMs given in (3). The proposed method is based on minimization of the posterior Cramér-Rao lower bound (PCRLB), derived by Tichavský et al. (1998). First, we use Monte-Carlo (MC) methods to obtain an approximation of the PCRLB, and then parametrize the inputs as a multi-dimensional Markov chain in , to render the optimization problem computationally tractable. Markov-chain parametrization not only allows to include amplitude constraints on the input, it can be easily implemented using a standard PID controller or any other regulator. The notation used here is given next.

Notation: ; ; is the set of real-valued matrices of cardinality ; is the space of symmetric matrices; is the cone of symmetric positive semi-definite matrices in ; and is its interior. The partial order on induced by and are denoted by and , respectively. is the set of stochastic matrix, where and the sum of each row adds up to . For , denotes its trace. For vectors , , and , denotes element-wise inequality, and is a diagonal matrix with elements of as its diagonal entries. Finally, is a Laplacian and is a gradient.

2 Problem formulation

Bayesian input design for regression models is a well studied problem in statistics (Chaloner and Verdinelli (1995)); wherein, the problem is often formulated as follows

| (4) |

where is an -step ahead optimal input sequence, and is a utility function. When inference on is of interest, Lindley (1956) suggested using the mean-square error (MSE) as a utility function, such that

| (5) |

where is the MSE associated with the parameter estimate given by , and is a test function.

Remark 4.

Remark 5.

To address the issues in Remarks 4 and 5, we propose to define a lower bound on the MSE first, and minimize the lower bound instead. The PCRLB, derived by Tichavský et al. (1998) provides a lower bound on the MSE associated with the estimation of from , and is given in the next lemma.

Lemma 6.

Let be an output sequence generated from (3) using , then the MSE associated with the estimation of from is bounded from below by the following matrix inequality

| (6) |

where: is an estimate of ; , , are the MSE, posterior information matrix (PIM), and PCRLB, respectively.

See Tichavský et al. (1998) for proof. ∎

Lemma 7.

See Tichavský et al. (1998) for proof. ∎

Corollary 8.

The proof is based on the fact that the PCRLB inequality in (6) guarantees that . ∎

Theorem 9.

The proof is based on matrix inversion lemma.∎ Finally, the input design problem for Bayesian identification of in (3) can be formulated as follows

| (11a) | ||||

| (11b) | ||||

where ; and and are the maximum and minimum magnitude of the input.

Remark 10.

The optimization problem in (11) allows to impose magnitude constraints on the inputs. Although constraints on and are not included, but if required, they can also be appended. ∎

Remark 11.

Integral in (8), with respect to , makes (11) independent of the random realizations from , , and . The optimization in (11) in fact only depends on: the process dynamics represented in (3); noise densities and ; and the choice of and . This makes (11) independent of or the Bayesian estimator used for estimating . ∎

Remark 12.

There are two challenges that need to be addressed in order to make the optimization problem in (11) tractable: (a) computing the lower bound ; and (b) solving the high-dimensional optimization problem in . Our approach to address the above challenges is discussed next.

3 Computing the lower bound

The first challenge is to compute the lower bound in (11). It is well known that computing in closed form is non-trivial for the model form considered in (3) (see Tichavský et al. (1998), Bergman (2001)). This is because of the complex, high-dimensional integrals in (8a) through (8f), which do not admit any analytical solution.

MC sampling is a popular numerical method to solve integrals of the form , where . Using i.i.d. trajectories , the probability distribution , can be approximated as

| (12) |

where is a MC estimate of and is the Dirac delta mass at . Finally, substituting (12) into , we get , where is an -sample MC estimate of .

Remark 13.

Example 14.

Consider the following stochastic SSM with additive Gaussian state and measurement noise

| (13a) | ||||

| (13b) | ||||

where and are mutually independent sequences of independent zero mean Gaussian random variables, such that and , where and for all .

Note that for the model form considered in Example 14, using the Markov property of the states and conditional independence of the measurements, the dimension of the integrals in (8a) through (8f) can be reduced, as given next.

Theorem 15.

(14a): First note that (see Tichavský et al. (1998)). On simplifying, we have .

This is due to . For Example 14, . Substituting it into , and using , we have (14a). Note that the expression in (14b) through (14f) can be similarly derived. ∎

Theorem 15 reduces the dimension of the integral in (8) for Example 14 from to . Using MC sampling, (14a), for instance, can be computed as

. Here and is an -sample MC estimate of . Note that the MC estimates of (14b) through (14f) can be similarly computed.

In general, substituting the MC estimates of (8a) through (8f) first into Lemma 7, and then into Theorem 9, yields

| (15) |

where is an estimate of , and , and are the estimates of the PIMs in Lemma 7. Finally, substituting (15) into (11) gives the following optimization problem

| (16a) | ||||

| (16b) | ||||

Theorem 16.

Since (15) is based on perfect MC sampling, using the strong law of large numbers, we have as . Equation (17) follows from this result, which completes the proof. ∎ A natural approach to solve (16) is to treat as a vector of continuous variables in ; however, this will render (16) computationally inefficient for large . A relaxation method to make (16) tractable is given next.

4 Input parametrization

To overcome the complications due to continuous valued input , we discretize the input space from to , such that , where , and is the number of discrete values for each input in . If we denote , then , for all , such that (16) can be written as follows

| (18) |

Note that although the input in (18) is defined on a discrete input space of , (18) is still intractable for large . To address this issue, a multi-dimensional Markov chain input parametrization, first proposed by Brighenti et al. (2009), is used here.

Definition 17.

For and , let be a valued first-order finite Markov chain, where , such that the sample values of , depend on the past only through the sample values of , such that for all and , we have the following

| (19) |

where is a probability measure and is a probability transition matrix. ∎

In Definition 17, , where represents the probability that the Markov chain transits from to the input state . Consider the following example.

Example 18.

For , , and , we have and , such that is a Markov chain on the input space of , then the probability matrix can be represented as

where .

Example 19.

For , , and , we have and , such that is a Markov chain on of then can be represented as

where .

Assumption 20.

The Markov chain considered in Definition 17 is time-homogeneous.

Assumption 21.

The Markov chain in Definition 17 has a prior probability distribution , where is a vector.

Theorem 22.

Using probability chain rule, the joint probability distribution of can be written as

| (21a) | |||

| (21b) | |||

where in (21b), we have used the first-order Markov property of . Noting the time-homogeneous property of and repeatedly appealing to the probability chain rule in (21b), we get (20). This completes the proof. ∎

Remark 23.

Using Definition 17 and Theorem 22, (18) can be reformulated to the following stochastic programming problem

| (22a) | |||

| (22b) | |||

| (22c) | |||

| (22d) | |||

| (22e) | |||

The expectations in (22a), with respect to and can again be approximated using MC sampling, such that

| (23) |

where is the -sample MC estimate. Note that marginalizing (23) with respect to yields , where is a MC estimate of . Substituting and into (22a) yields

| (24a) | |||

| (24b) | |||

| (24c) | |||

| (24d) | |||

| (24e) | |||

Note that solving (24), yields , which is the optimal distribution of the input sequence.

Corollary 24.

Proof is similar to Theorem 16. ∎

Remark 25.

There are several advantages of using the formulation given in (24): (a) the optimization is independent of , as the number of parameters to be estimated are ; (b) easy to include magnitude and other transition constraints on the inputs; and (c) samples from the optimal distribution can be easily sampled, and implemented using a PID or any classical regulator. ∎

In this paper, the optimization problem in (24) is implemented through an iterative approach, that involves standard numerical solvers (Nocedal and Wright (2006)). The proposed method for input design, including the iterations in the optimization, is summarized in Algorithm 1.

5 Simulation example

Consider a process described by the following univariate, and non-stationary stochastic SSM (Tulsyan et al. (2013b))

| (26a) | ||||

| (26b) | ||||

where is a vector of model parameters to be estimated, with being the true parameter vector. The noise covariances are selected as and , for all . For Bayesian identification, in (24) is a random process, with , such that , where , . Here we assume that , where and . Starting at , we are interested in choosing an input sequence that would eventually lead to minimization of the MSE of the parameter estimates, computed using an SMC based Bayesian estimator given in Tulsyan et al. (2013a). Algorithm 1 was implemented with , , and . For input, we consider Example 18, with , such that . Here have the following initial and transition probability

where , where in Cases through are the probabilities. For comparison purposes, we also consider a pseudo-random binary signal, which can be represented as

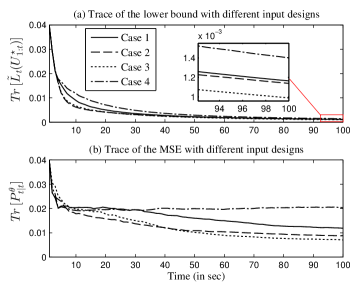

For all of the above cases, in (24a) was selected as the trace. Table 1 gives and for Cases 1 through 3 as computed by Algorithm 1, and Figure 1(a) gives the corresponding trace of the lower bound. It is clear from Table 1 and Figure 1(a) that Case 3 yields the lowest objective function value. Although the objective function value for Case 2 is comparable to Case 3, note that Case 3 provides the most general form of the Markov chain in .

Figure 1(b) validates the quality of the designed inputs based on the performance of the Bayesian estimator. From Figure 1(b), it is clear that with Case 3, the estimator yields the lowest trace of MSE at all sampling time. The same is also evident from Table 1; wherein, the sum of the trace of MSE is smallest with Case 3 as the input. The Results are based on MC simulations, starting with i.i.d. input path trajectories generated from for Cases 1 through 4. If required, a more rigorous validation of the designed input can be performed using the approach proposed in Tulsyan et al. (2013b).

The results appear promising; however, we faced problems in solving the optimization. As discussed earlier, (24) is a stochastic programming problem, as a result (24a) tends to be non-smooth, and have many local minima. In future, we will consider use of stochastic gradient-based methods.

| Case 1 | Case 2 | Case 3 | Case 4 | |

|---|---|---|---|---|

| N.A. | N.A. | N.A. | ||

| N.A. | ||||

| N.A. | N.A. | |||

| 0.42 | 0.37 | 0.36 | 0.51 | |

| 1.66 | 1.27 | 1.25 | 2.02 |

6 conclusions

An algorithm for input design for Bayesian identification of stochastic non-linear SSM is proposed. The developed algorithm is based on minimization of the PCRLB with respect to inputs. One of the distinct advantages of the proposed method is that the designed input is independent of the Bayesian estimator used for identification. Simulation results suggest that the proposed method can be used to deliver accurate inference on the parameter estimates.

References

- Bergman [2001] N. Bergman. Sequential Monte Carlo Methods in Practice, chapter Posterior Craḿer-Rao Bounds for Sequential Estimation. Springer–Verlag, New York, 2001.

- Brighenti et al. [2009] C. Brighenti, B. Wahlberg, and C.R. Rojas. Input design using Markov chains for system identification. In Proceedings of the 48th IEEE Conference on Decision and Control and the 28th Chinese Control Conference, pages 1557–1562, Shanghai, China, 2009.

- Chaloner and Verdinelli [1995] K. Chaloner and I. Verdinelli. Bayesian experimental design: A review. Statistical Science, 10(3):273–304, 1995.

- Gilks et al. [1995] W.R. Gilks, S. Richardson, and D. Spiegelhalter. Markov Chain Monte Carlo in Practice. Chapman & Hall, 1995.

- Huan and Marzouk [2012] X. Huan and Y.M. Marzouk. Simulation-based optimal Bayesian experimental design for non-linear systems. Journal of Computational Physics, 232(1):288–317, 2012.

- Kantas et al. [2009] N. Kantas, A. Doucet, S.S. Singh, and J. Maciejowski. An overview of sequential Monte Carlo methods for parameter estimation in general state-space models. In Proceedings of the 15th IFAC Symposium on System Identification, pages 774–785, Saint-Malo, France, 2009.

- Kück et al. [2006] H. Kück, N. de Freitas, and A. Doucet. SMC samplers for Bayesian optimal non-linear design. In Proceedings of the Non-linear Statistical Signal Processing Workshop, pages 99–102, Cambridge, U.K., 2006.

- Lindley [1956] D.V. Lindley. On a measure of the information provided by an experiment. The Annals of Mathematical Statistics, 27(4):986–1005, 1956.

- Müller and Parmigiani [1995] P. Müller and G. Parmigiani. Optimal design via curve fitting of Monte Carlo experiments. Journal of the American Statistical Association, 90(432):1322–1330, 1995.

- Nocedal and Wright [2006] J. Nocedal and S.J. Wright. Numerical Optimization: Springer Series in Operations Research. Springer, New York, 2006.

- Tichavský et al. [1998] P. Tichavský, C. Muravchik, and A. Nehorai. Posterior Cramér-Rao bounds for discrete-time non-linear filtering. IEEE Transactions on Signal Processing, 46(5):1386–1396, 1998.

- Tulsyan et al. [2012] A. Tulsyan, J.F. Forbes, and B. Huang. Designing priors for robust Bayesian optimal experimental design. Journal of Process Control, 22(2):450–462, 2012.

- Tulsyan et al. [2013a] A. Tulsyan, B. Huang, R.B. Gopaluni, and J.F. Forbes. On simultaneous on-line state and parameter estimation in non-linear state-space models. Journal of Process Control, 23(4):516–526, 2013a.

- Tulsyan et al. [2013b] A. Tulsyan, B. Huang, R.B. Gopaluni, and J.F. Forbes. Bayesian identification of non-linear state-space models: Part II-Error Analysis. In Proceedings of the 10th International Symposium on Dynamics and Control of Process Systems, Mumbai, India, 2013b.