Approximate Dynamic Programming

using Fluid and Diffusion Approximations

with Applications to Power Management

Abstract

Neuro-dynamic programming is a class of powerful techniques for approximating the solution to dynamic programming equations. In their most computationally attractive formulations, these techniques provide the approximate solution only within a prescribed finite-dimensional function class. Thus, the question that always arises is how should the function class be chosen? The goal of this paper is to propose an approach using the solutions to associated fluid and diffusion approximations. In order to illustrate this approach, the paper focuses on an application to dynamic speed scaling for power management in computer processors.

1 Introduction

Stochastic dynamic programming based on controlled Markov chain models have become key tools for evaluating and designing communication, computer, and network applications. These tools have grown in popularity as computing power has increased. However, even with increasing computing power, it is often impossible to obtain exact solutions to dynamic programming problems. This is primarily due to the so-called “curse of dimensionality”, which refers to the fact that the complexity of dynamic programming equations often grows exponentially with the size of the underlying state space.

Recently though, the “curse of dimensionality” is slowly dissolving in the face of approximation techniques such as temporal difference learning (TD-learning) and Q-learning [8], which fall under the category of neuro-dynamic programming. These techniques are designed to approximate a solution to a dynamic programming equation within a prescribed finite-dimensional function class. A key determinant of the success of these techniques is the selection of this function class. Although this question has been considered in specific contexts in prior work, these solutions are often either “generic” or highly specific to the application at hand. For instance, in [29], a vector space of polynomial functions has been used for TD-learning, and a function class generated by a set of Gaussian densities is used in [18]. However, determining the appropriate function class for these techniques continues to be more of an art than a science.

1.1 Main contributions

The goal of this paper is to illustrate that a useful function class can be designed using solutions to highly idealized approximate models. Specifically, the value functions of the dynamic program obtained under fluid or diffusion approximations of the model can be used as basis functions that define the function class. This can be accomplished by first constructing a fluid or diffusion approximation of the model, and then solving (or approximating) the corresponding dynamic programming equation for the simpler system. The value functions of these simpler systems can then be used as some of the basis functions used to generate the function class used in the TD-learning and Q-learning algorithms.

A significant contribution of this paper is to establish bounds on approximation error by exploiting the similarity between the dynamic programming equation for the MDP model and the corresponding dynamic programming equation for the fluid or diffusion model. The bounds are obtained through Taylor series approximations. A first-order Taylor series approximation is used in a comparison with the fluid model, and a second-order Taylor series is used when we come to the diffusion model approximation.

1.2 Dynamic speed scaling

An important tradeoff in modern computer system design is between reducing energy usage and maintaining good performance, in the sense of low delay. Dynamic speed scaling addresses this tradeoff by adjusting the processing speed in response to workload. Initially proposed for processor design [26], dynamic speed scaling is now commonly used in many chip designs, e.g. [1]. It has recently been applied in other areas such as wireless communication [34]. These techniques have been the focus of a growing body of analytic research [2, 4, 14, 33, 3].

For the purposes of this paper, dynamic speed scaling is simply a stochastic control problem – a single server queue with a controllable service rate – and the goal is to understand how to control the service rate in order to minimize a weighted sum of the energy cost and the delay cost.

Analysis of the fluid model provides a good fit to the solution to the average-cost dynamic programming equations, and subsequent analysis of the diffusion model provides further insight, leading to a two-dimensional basis for application in TD-learning. This educated choice for basis functions in TD-learning leads to fast convergence and almost insignificant Bellman error. A polynomial basis results in much poorer results – one example is illustrated in Fig. 6.

Although the paper focuses in large part on the application of TD-learning to the dynamic speed scaling problem, the approach presented in the paper is general: The use of fluid and diffusion approximations to provide an appropriate basis for Neuro-dynamic programming is broadly applicable to a wide variety of stochastic control problems.

1.3 Related work

Fluid-model approximations for value functions in network optimization is over fifteen years old [20, 19, 15, 22], and these ideas have been applied in approximate dynamic programming [30, 25]. The same approach is used in [15] to obtain a TD-learning algorithm for variance reduction in simulation for network models.

The preliminary version of this work [13] and the related conference article [24] use these techniques for TD-learning, and motivate the approach through Taylor series approximations. In the present work, these arguments are refined to obtain explicit bounds on the Bellman error.

There is a large body of analytic work in the literature studying the dynamic speed scaling problem, beginning with Yao et al. [35]. Many focus on models with either a fixed power consumption budget [28, 11, 36] or job completion deadline [27, 2]. In the case where the performance metric is the weighted sum of power consumption and delay (as in the current paper), a majority of prior research considers a deterministic, worst-case setting [2, 4]. Most closely related to the current paper are [14, 33, 3], which consider the MDP described in (25). However, these papers do not consider the fluid or diffusion approximations of the speed scaling model; nor do they discuss the application of TD-learning.

1.4 Paper organization

The remainder of the paper is organized as follows. Some basics of optimal control theory is reviewed

2 s.mdp

: Markov Decision Process (MDP) models and the associated average-cost optimality equations are reviewed, as well as approaches to neuro-dynamic programming for approximating the solution to these equations. This section also contains formulations of fluid and diffusion models, defined with respect to a general class of MDP models, along with results explaining why we can expect the solution to one dynamic programming equation might approximate the solution to another.

3 s.speedscaling

contains application to the power management model, including explicit tight bounds on the Bellman error. These results are illustrated through simulation experiments in

4 s:DSSnum

. Conclusions are contained in

5 s.conclusion

. The proofs of all the main results are relegated to the appendix.

6 Optimal Control

We begin with a review of Markov Decision Processes (MDPs). The appendix contains a summary of symbols and notation used in the paper.

6.1 Markov Decision Processes

Dynamic programming equations

Throughout, we consider the following MDP model. The state space is taken to be , or a subset. Let denote the action space, and denote the set of feasible inputs for when . In addition there is an i.i.d. process evolving on that represents a disturbance process. For a given initial condition , and a sequence evolving on , the state process evolves according to the recursion,

| (1) |

This defines a Markov Decision Process (MDP) with controlled transition law

The controlled transition law can be interpreted as a mapping from functions on to functions on the joint state-action space : For any function we denote,

| (2) |

It is convenient to introduce a generator for the model,

| (3) |

This is the most convenient bridge between the MDP model and any of its approximations.

A cost function is given. For a given control sequence and initial condition , the average cost is given by,

| (4) |

where . Our goal is to find an optimal control policy with respect to the average cost. The infimum over all is denoted , which is assumed to be independent of for this model111For sufficient conditions see [6, 20, 19, 9, 22]..

Under typical assumptions [19, 21], an optimal policy achieving this minimal average cost can be obtained by solving the Average Cost Optimality Equation (ACOE):

| (5) |

where the generator is defined in (3). The ACOE is a fixed point equation in the relative value function , and the optimal cost for the MDP [22].

For any function , the -myopic policy is defined as,

| (6) |

The optimal policy is a -myopic policy, which is any minimizer,

| (7) |

A related fixed point equation is Poisson’s equation. It is a degenerate version of the ACOE, in which the control policy is fixed. Assume a stationary policy is given. Let denote the resulting generator of the MDP, and a cost function. Poisson’s equation is defined as,

| (8) |

where is the average cost defined in (4) with policy .

Approximate dynamic programming

Since solving the dynamic programming equation is complex due to the curse of dimensionality, we use approaches to approximate a solution to the dynamic programming equation. We review standard error criteria next.

The most natural error criterion is the direct error. Let be an approximation of . Define the direct error as,

| (9) |

However, the direct error is not easy to calculate since is not known.

Another common error criterion is the Bellman error. For given , it is defined as,

| (10) |

This is motivated by the associated perturbed cost function,

| (11) |

where is an arbitrary constant. The following proposition can be verified by substituting (11) into (10).

Proposition 1.

The triplet satisfies the ACOE,

The solution of the ACOE may be viewed as defining a mapping from one function space to another. Specifically, it maps a cost function to a pair . Exact computation of the pair () is notoriously difficult, even in simple models when the state space is large. However, a simpler problem is the inverse mapping problem: Given a function and a constant , find a cost function such that the triple satisfies the ACOE (5). The solution of this problem is known as inverse dynamic programming. If the function approximates then, subject to some technical conditions, the resulting -myopic policy will provide approximately optimal performance. Proposition 1 indicates that defined in (11) is a solution to the inverse dynamic programming problem.

To evaluate how well approximates , we define the normalized error,

| (12) |

If is small for all , then is a good approximation of .

A bound on the Bellman error will imply a bound on the direct error under suitable assumptions. In most cases the relative value function may be expressed using the Stochastic Shortest Path (SSP) representation:

| (13) |

where is the first return time to a state . Conditions under which the SSP representation holds are given in [21, 19, 7, 6, 22].

The following result establishes bounds on the direct error.

Proposition 2.

Suppose that and each admit SSP representations. For the latter, this means that

where and are defined in (11), and the corresponding policy is the -myopic policy. Then, the following upper and lower bounds hold for the direct error,

where denotes the expectation taken over the controlled Markov chain under policy .

The bounds for the direct error in Proposition 2 are derived by using the Bellman error and the SSP representation. The details of the proof are given in

7 s:Error bounds

of the appendix.

7.1 Neuro-dynamic programming

Neuro-dynamic programming concerns approximation of dynamic programming equations through either simulation or through observations of input-output behavior in a physical system. The latter is called reinforcement learning, of which TD-learning is one example. The focus of this paper is on TD-learning, although similar ideas are also applicable for other approaches such as Q-learning.

Approximation of the relative value function will be obtained with respect to a parameterized function class: . In TD-learning a fixed stationary policy is considered (possibly randomized), and the goal is to find the parameter so that best approximates the solution to Poisson’s equation (8). In standard versions of the algorithm, the direct error is considered.

TD-learning algorithms are based on the assumption that the given policy is stabilizing, in the sense that the Markov chain has unique invariant probability distribution . The mean-square direct error is minimized,

In the original TD-learning algorithm, The optimal parameter is obtained through a stochastic approximation algorithm based on steepest descent. The LSTD (least-squares TD) algorithm is a Newton-Raphson stochastic approximation algorithm.

TD-learning was first introduced in [10]. The LSTD-learning for the average cost problem is described in [17, 22].

In this paper we restrict to a linear function class. It is assumed that there are basis functions, so that . We also write . In this special case, the optimal parameter is the solution to a least-squares problem, and the LSTD algorithm is frequently much more reliable than other approaches, in the sense that variance is significantly reduced.

The TD-learning algorithm is used to compute an approximation of the relative value function for a specific policy. To estimate the relative value function with the optimal policy, the TD-learning algorithm is combined with policy improvement.

The policy iteration algorithm (PIA) is a method to construct an optimal policy through the following steps. The algorithm is initialized with a policy and then the following operations are performed in the th stage of the algorithm:

-

1.

Given the policy , find the solution to Poisson’s equation , where , and is the average cost.

-

2.

Update the policy via

In order to combine TD-learning with PIA, the TDPIA algorithm considered replaces the first step with an application of the LSTD algorithm, resulting in an approximation to the function . The policy in (ii) is then taken to be .

7.2 Approximation architectures

We now introduce approximate models and the corresponding approximations to the ACOE.

Fluid model

The fluid model associated with the MDP model given in (1) is defined by the ordinary differential equation,

| (14) |

where . The fluid model has state that evolves on , and input that evolves on . The existence of solutions to (14) will be assumed throughout the paper.

The fluid value function considered in prior work on network models surveyed in the introduction is defined to be the infimum over all policies of the total cost,

| (15) |

However, in the general setting considered here, there is no reason to expect that is finite-valued.

In this paper we consider instead the associated perturbed HJB equation: For given , we assume we have a solution to the differential equation,

| (16) |

where is the generator for the fluid model defined as:

| (17) |

Given a solution to (16), we denote the corresponding policy for the fluid model,

| (18) |

In the special case that the total cost (15) is finite-valued, and some regularity conditions hold, this value function will solve (16) with , and will be an optimal policy with respect to total-cost [5].

The HJB equation (16) can be interpreted as an optimality equation for an optimal stopping problem for the fluid model. Denote the first stopping time , and let denote the minimal total relative cost,

| (19) |

where the infimum is over all policies for the fluid model. Under reasonable conditions this function will satisfy the dynamic programming equation,

A typical necessary condition for finiteness of the value function is that the initial condition satisfy .

Let us now investigate the relationship between the MDP model and its fluid model approximation. It is assumed that is a smooth solution to (16), so that the following first-order Taylor series expansion is justified: Given , ,

A more quantitative approximation is obtained when is twice continuously differentiable ().

If is of class then lower and upper bounds on the Bellman error in the following proposition, which measure the quality of the approximation of to . The proof of Proposition 3 is contained in the appendix.

Diffusion model

The diffusion model is a refinement of the fluid model to take into account volatility. It is motivated similarly, using a second-order Taylor series expansion.

To bring in randomness to the fluid model, it is useful to first introduce a fluid model in discrete-time. For any , the random variable denoted has zero mean. The evolution of can be expressed as a discrete time nonlinear system, plus “white noise”,

| (20) |

The fluid model in discrete time is obtained by ignoring the noise,

| (21) |

This is the discrete time counterpart of (14). Observe that it can be justified exactly as in the continuous time analysis: If is a smooth function of , then we may approximate the generator using a first order-Taylor series approximation as follows:

The right hand side is the generator applied to , for the discrete-time fluid model (21).

Consideration of the model (21) may give better approximation for value functions in some cases, but we lose the simplicity of differential equations that characterize value functions in the continuous time model (14).

The representation (20) also motivates the diffusion model. Denote the conditional covariance matrix by

and let denote an “square-root”, for each . The diffusion model is of the form,

| (22) |

where the process is a standard Brownian motion on .

To justify its form we consider a second order Taylor series approximation. If is a function, and at time we have , , then the standard second order Taylor series about gives,

Suppose we can justify a further approximation, obtained by replacing with in this equation. Then, on taking expectations of each side, conditioned on , , we approximate the generator for by the second-order ordinary differential operator,

| (23) |

This is precisely the differential generator for (22).

The minimal average cost is defined as in the MDP model (4), but as a continuous-time average. The ACOE has the precise form as in the MDP, only the definition of the generator is changed:

| (24) |

and is again called the relative value function.

The solution to the ACOE for the diffusion model is often a good approximation for the MDP model. Moreover, as in the case of fluid models, the continuous time model is more tractable because tools from calculus can be used for computation or approximation. This is illustrated in the power management model in the next section.

8 Power management model

The dynamic speed scaling problem surveyed in the introduction is now addressed through the techniques described in the previous section. To begin, we construct an MDP that is described as a single server queue with a controllable service rate that determines power consumption.

8.1 The MDP model

For each , let denote the job arrivals in this time slot, the number of jobs in the queue awaiting service, and the rate of service. The MDP model is a controlled random walk:

| (25) |

The following assumptions on the arrival process are imposed throughout the paper.

-

A1

The arrival process is i.i.d., its marginal distribution is supported on with finite mean . Moreover, zero is in the support of its distribution:

and there exists a constant such that .

The boundedness assumption is not critical – a th moment for would be sufficient. The assumption that may be zero is imposed to facilitate a proof that the controlled Markov model is “-irreducible”, with (see [22]).

The cost function is chosen to balance cost of delay with power consumption:

where denotes the power consumption as a function of the service rate , and . This form of cost function is common in the literature, e.g., [14, 33, 3].

The remaining piece of the model is to define the form of . Two forms of are considered, based on two different applications: processor design and wireless communication.

For processor design applications, is typically assumed to be a polynomial. In earlier work in the literature, has been taken to be a cubic. The reasoning is that the dynamic power of CMOS is proportional to , where is the supply voltage and is the clock frequency [16]. Operating at a higher frequency requires dynamic voltage scaling (DVS) to a higher voltage, nominally with , yielding a cubic relationship. However, recent work, e.g. [33], has found that the dynamic power usage of real chips is well modeled by a polynomial closer to quadratic. When considering polynomial cost, in this paper we take a single term,

| (26) |

where , and we focus primarily on the particular case of .

For wireless communication applications, the form of differs significantly for different scenarios. An additive white Gaussian noise model [34] gives,

| (27) |

for some .

Considered next are fluid and diffusion models to approximate the solution to the ACOE in this application.

8.2 Convex and continuous approximations

Here we apply the fluid and diffusion approximations introduced in

9 s.approach

to the power management model, and derive explicit error bounds for the approximations to the ACOE.

The fluid model

Specializing the fluid model given in (14) to the case of dynamic speed scaling (25) gives the following continuous-time deterministic model:

where is the expectation of , and the processing speed and queue length are both non-negative.

The total cost defined in (15) is not finite for the cost function (8.1) when is defined in (26) or (27). Consider the alternate value function defined in (19), with and with the modified stopping time,

This value function is denoted, for , by

| (28) |

where the infimum is over all input processes for the fluid model. The function solves the HJB equation (16) with , and is finite-valued.

Fluid model with general polynomial cost are discussed in detail in

10 s:fluidandprop

. Here we review results in the simple case of quadratic cost with ,

| (29) |

In this case we obtain by elementary calculus,

| (30) |

Rather than modify the optimization criterion, we can approximate the solution to (16) by modifying the cost function so that it vanishes at the equilibrium . A simple modification of (29) is the following,

where . The fluid value function defined in (15) is similar to given in (30),

| (31) |

and in this case the optimal fluid policy takes the simple form ,

To measure the quality of these approximation to the relative value function , we estimate bounds for the Bellman error and direct error. In Proposition 4, we first compute the bounds for the Bellman error. They are derived based on Proposition 3. The bounds for the direct error are derived based on Proposition 2, which assumes the SSP representation holds for . This will be assumed throughout our analysis:

A2 The relative value function admits the SSP representation (13), with . Moreover, under the optimal policy, any bounded set is small: For each there exists and such that whenever and ,

| (32) |

Analytic techniques to verify this assumption are contained in [31] (see also [12] for verification of the “small set” condition (32) for countable state-space models).

Under these assumptions we can obtain bounds on the Bellman error. We present explicit bounds only for the case of quadratic cost.

Proposition 4.

Consider the speed scaling model with cost function (29), and with the fluid value function given in (30). The following hold for the Bellman error defined in (10) and the direct error defined in (9):

-

1.

Under Assumption A1, the Bellman error is non-negative, and grows at rate , with

-

2.

If in addition Assumption A2 holds, then the direct error satisfies,

where the upper bound grows at most linearly, , and the lower bound is independent of ; that is, .

In particular, under Assumptions A1 and A2,

The bounds on the Bellman error in (i) imply a bound on the normalized error defined in (12):

| (33) | ||||

This implies that the inverse dynamic programming solution gives a good approximation of the original cost for large . The bounds on the direct error in (ii) imply that the fluid value function is a good approximation for large ,

The diffusion model

Following (23), the generator for the diffusion model is expressed, for any smooth function by,

| (34) |

where .

Provided is monotone, so that for all , the minimizer in (24) can be expressed

| (35) |

Substituting (35) into (24) gives the nonlinear equation,

| (36) |

We do not have a closed form expression, but we will show that an approximation is obtained as a perturbation of defined in (19), with . The constant is not known, but the structure revealed here will allow us to obtain the desired basis for TD-learning.

For any function , denote the Bellman error for the diffusion model by,

| (37) |

The value function defined in (30) is an approximation of in the sense that the Bellman error is bounded:

Proposition 5.

The function defined in (30) is convex and increasing. Moreover, with , the Bellman error for the diffusion has the explicit form, .

A tighter approximation can be obtained with the ‘relative value function’ for the fluid model, . This satisfies a nonlinear equation similar to (36),

Elementary calculations show that for any constant we have the approximation,

where is given in (30). We then take the right hand side for granted in the approximation , and on integrating this gives

| (38) |

The constant is chosen so that .

We note that this is a reflected diffusion, so that the generator is subject to the boundary condition [22, Theorem 8.7.1]. The boundary condition is satisfied for (38) on taking .

The resulting approximation works well for the diffusion model. The proof of Proposition 6 follows from calculus computations contained in the Appendix.

Proposition 6.

Assume that . For any , , the function defined in (38) is convex and increasing. Moreover, the Bellman error is bounded over , and the following bound holds for large :

The function (38) also serves as an approximation for the MDP model. The proof is omitted since it is similar to the proof of Proposition 3.

Proposition 7.

The function defined in (38) is an approximate solution to the ACOE for the MDP model, in the sense that the Bellman error has growth of order ,

The bounds obtained in this section quantify the accuracy of the fluid and diffusion model approximations. We next apply this insight to design the function classes required in TD-learning algorithms.

11 Experimental results

The results of the previous section are now illustrated with results from numerical experiments. We restrict to the quadratic cost function given in (29) due to limited space.

In application to TD-learning, based on a linear function class as discussed in

12 s:pappro

, the following two dimensional basis follows from the analysis of the fluid and diffusion models,

| (39) |

where the value function is given in (30). The basis function is motivated by the error bound in Proposition 4, and is motivated by Proposition 7. The parameter is fixed, and then we take

The details of the simulation model are as follows: The arrival process is i.i.d. on , satisfying the assumptions imposed in

13 s.speedscalingMDP

, although the boundedness assumption in A1 was relaxed for simplicity of modeling: In the first set of experiments, the marginal distribution is a scaled geometric random variable, of the form

| (40) |

where is geometrically distributed on with parameter , and is chosen so that the mean is equal to unity:

| (41) |

The variance of is given by,

In

14 s:Arho

experiments are described in which the variance of the arrival process was taken as a parameter, to investigate the impact of variability.

14.1 Value iteration

We begin by computing the actual solution to the average cost optimality equation using value iteration. This provides a reference for evaluating the proposed approach for TD-learning.

The value iteration (VIA) solves the fixed point equation (5) based on the successive approximation method – see [32] for the origins, and [12, 22] for more recent relevant results.

The algorithm is initialized with a function , and the iteration is given by,

| (42) |

For each , the function can be expressed as

| (43) |

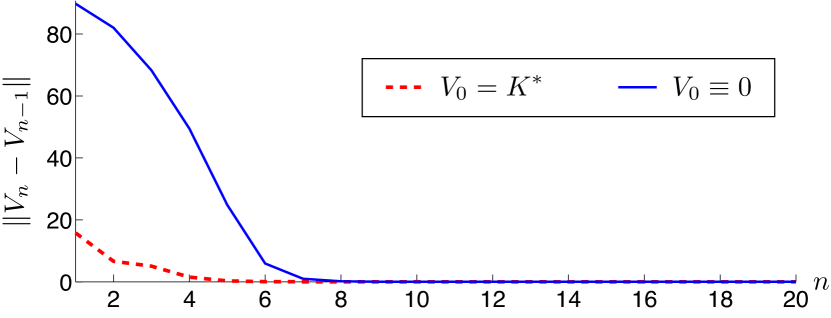

The approximate solution to the ACOE at stage is taken to be the normalized value function , , where is the th value function defined in (43). The convergence of to is illustrated in Fig. 1. The error converges to zero much faster when the algorithm is initialized using the fluid value function of (30).

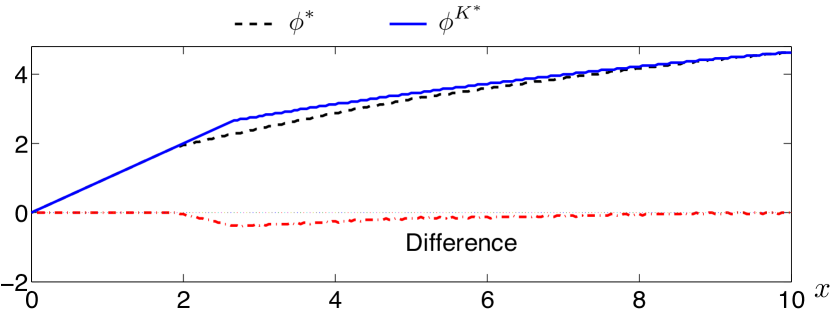

Shown in Fig. 2 is a comparison of the optimal policy , computed numerically using value iteration, and the -myopic policy, .

14.2 TD-learning with policy improvement

The first set of experiments illustrates convergence of the TD-learning algorithm with policy improvement introduced in

15 s:pappro

.

Recall from Proposition 7 that a linear combination of the basis functions in (39) provides a tight approximation to the ACOE for the MDP model. In the numerical results surveyed here it was found that the average cost is approximated by , and recall that we take in all experiments. Hence and were chosen in the basis function given in (39).

The initial policy was taken to be , , and the initial condition for TD learning was taken to be .

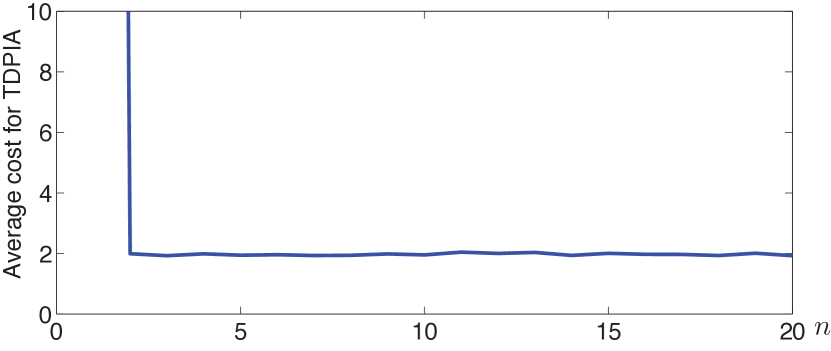

Fig. 3 shows the estimated average cost in each of the twenty iterations of the algorithm. The algorithm results in a policy that is nearly optimal after a small number of iterations.

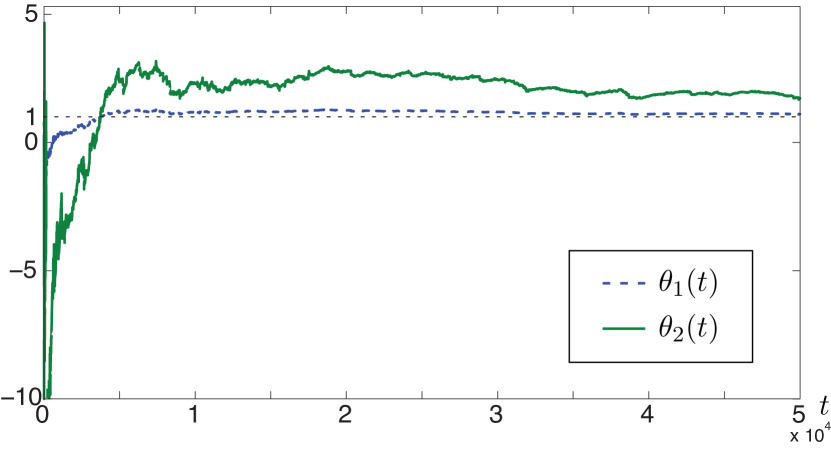

Fig. 4 shows the estimates of the coefficients obtained after iterations of the LSTD algorithm, after four steps of policy iterations. The value of the optimal coefficient corresponding to was found to be close to unity, which is consistent with (38).

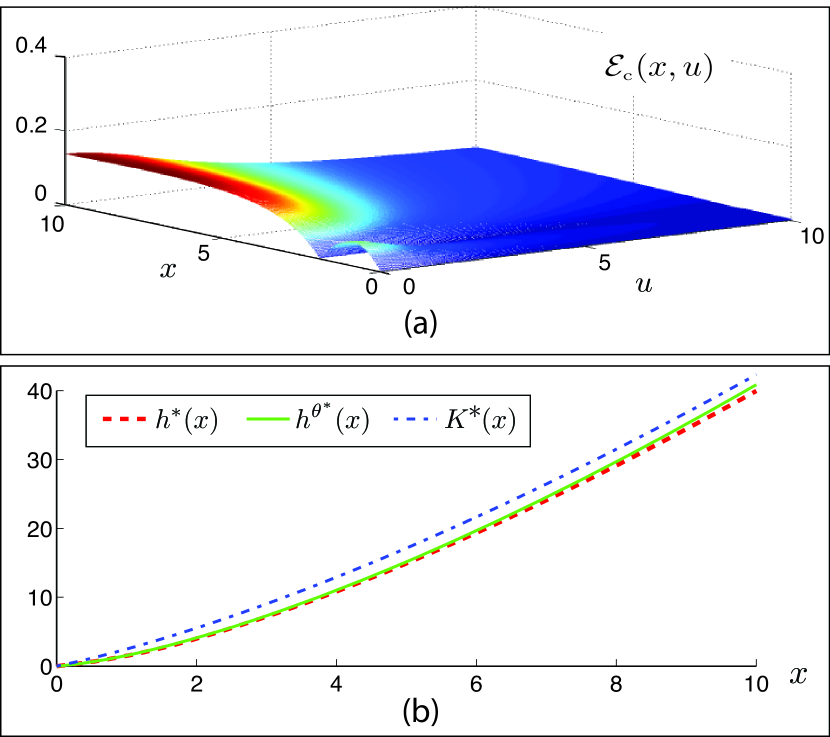

Shown in Fig. 5 are error plots for the final approximation of from TDPIA. Fig. 5 (a) is the Bellman error – note that it is less than unity for all . Fig. 5 (b) provides a comparison of two approximations to the solution to the relative value function . It is clear that the approximation obtained from the TDPIA algorithm closely approximates the relative value function.

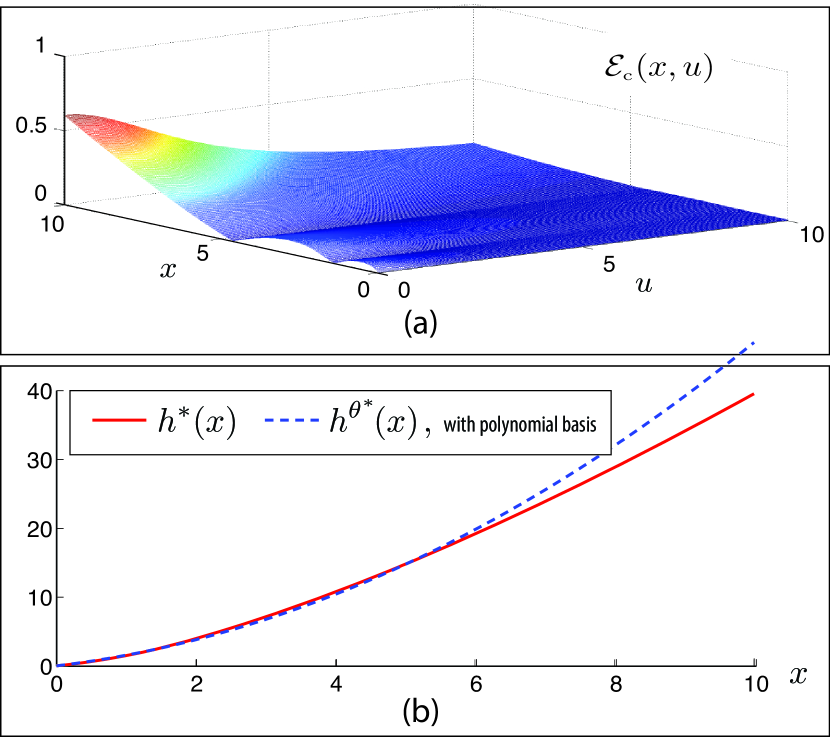

To illustrate the results obtained using a generic polynomial basis, identical experiments were run using

| (44) |

The experiments were coupled, in the sense that the sample path of the arrival process was held fixed in experiments comparing the results from the two different basis sets.

Fig. 6 shows error plots for the final approximation of using this quadratic basis for TD-learning. In (a) we see that the Bellman error is significantly larger for , when compared with the previous experiments using the basis (39). Similarly, the plots shown in Fig. 5 (b) show that the quadratic basis does not give a good fit for .

15.1 The impact of variability

The influence of variability was explored by running the TDPIA with arrival distributions of increasing variance, and with mean fixed to unity.

The variance is denoted , which is taken as a variable. The specification of the marginal distribution is described informally as follows: A weighted coin is flipped. If a head is obtained, then is a scaled Bernoulli random variable. If a tail, then is a realization of the scaled geometric random variable defined in (40). Thus, this random variable can be expressed,

| (45) |

where , , and are mutually independent, is a Bernoulli random variable with parameter , is a Bernoulli random variable with parameter , and . Hence the mean of is unity:

The variance of is a function of the parameters and :

The parameter was chosen to be , so that for a given we obtain,

Eight values of were considered. To reduce the relative variance, the simulations were coupled as follows: At each time , the eight Bernoulli random variables were generated as follows:

where are mutually independent Bernoulli random variables with parameters . The arrival processes were then generated by using and according to (45). The parameters were chosen such that the eight variances were , , , , , , and .

The TDPIA was run 1000 times in parallel for these eight systems. Four steps of policy improvement were performed: In each step of policy iteration, the value function was estimated with iterations of the LSTD algorithm. The final estimation of the coefficients from TDPIA were projected onto the interval .

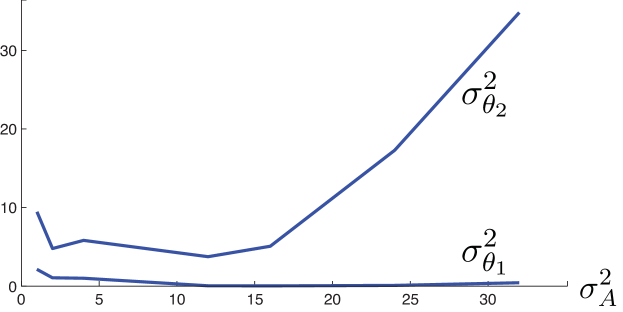

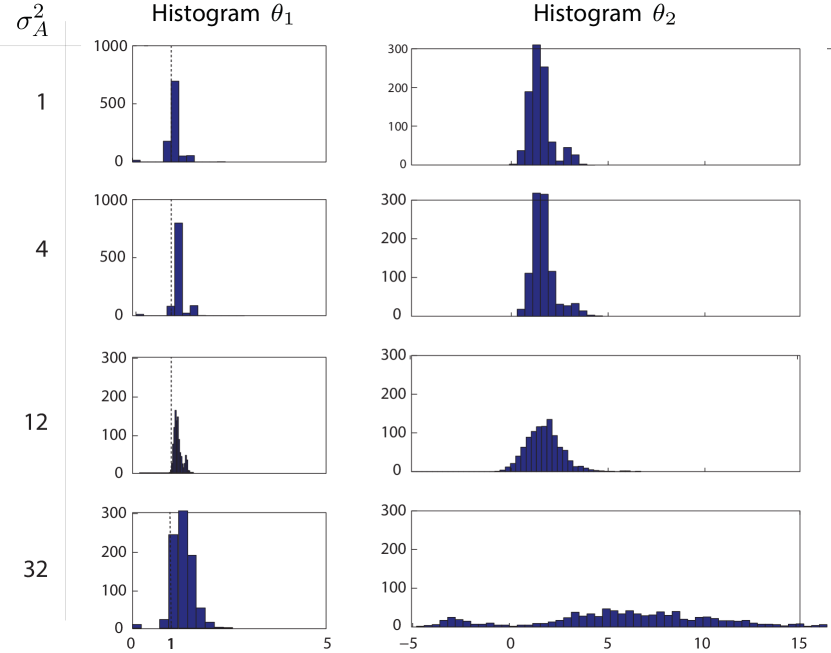

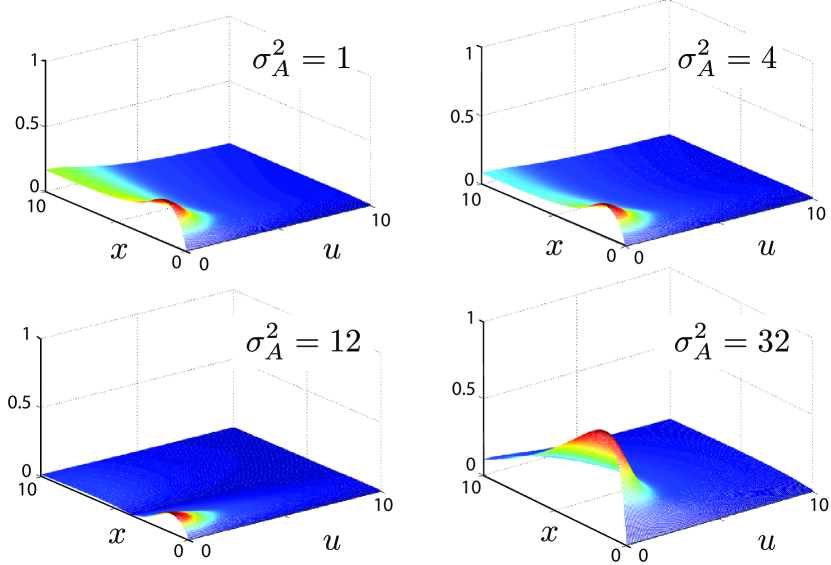

Fig. 7 shows that the empirical variance of the final estimates of the coefficients. The variance for is much larger than and increases with the variance of the arrival process when the variance is larger than . This is also indicated by the histograms of the final estimations of the coefficients given in Fig. 8.

Let denote the mean of the final estimations of coefficients. A comparison of normalized Bellman errors for is given in Fig. 9. The normalized error of is largest when the variance of the arrival process is .

16 Concluding remarks

The main message of this paper is that idealized models are useful for designing the function class for TD-learning. This approach is applicable for control synthesis and performance approximation of Markov models in a wide range of applications. Strong motivation for this approach is provided by a Taylor series arguments that can be used to bound the difference between the relative value function and approximations based on fluid or diffusion models.

We have focused on the problem of power management in processors via dynamic speed scaling in order to illustrate the application of this approach for TD-learning. This application reveals that this approach to approximation yields remarkably accurate results. Bounds for the Bellman error and the direct error w.r.t. the fluid and diffusion approximations indicate that the value functions of these idealized models are good approximations of the solution to the ACOE. In particular, numerical experiments revealed that value iteration initialized using the fluid approximation results in much faster convergence, and policy iteration coupled with TD-learning quickly converges to an approximately optimal policy when the fluid and diffusion models are considered in the construction of a basis. Besides, by using the fluid and diffusion value functions as basis functions, the Bellman error for the value function from TDPIA is much smaller than that obtained using quadratic basis functions.

Acknowledgment

Financial support from the National Science Foundation (ECS-0523620 and CCF-0830511), AFOSR FA9550-09-1-0190, ITMANET DARPA RK 2006-07284, European Research Council (ERC-247006) and Microsoft Research is gratefully acknowledged.222Any opinions, findings, and conclusions or recommendations expressed in this material are those of the authors and do not necessarily reflect the views of NSF, AFOSR, DARPA, or Microsoft.

List of symbols and definitions

| State at time ; values in . | |

| Action at time ; values in . | |

| Transition kernel of the MDP, (2). | |

| Cost function. | |

| Minimum average cost. | |

| The first return time to state . | |

| Direct error, (9). | |

| Bellman error for the MDP model, (10). | |

| Bellman error for the diffusion model, (37). | |

| Normalized error, (12). | |

| Relative value function. | |

| Fluid value function. | |

| The -myopic policy, (6). | |

| The -myopic policy, (7). | |

| Fluid optimal policy, (18). |

Appendix A Fluid value function and its properties

For computation it is simplest to work with modified cost functions, defined as follows

| Polynomial cost | (46) | |||

| Exponential cost |

where . The corresponding fluid value functions are given in the following.

Part (i) of Proposition 8 exposes a connection between the fluid control policy and prior results on worst-case algorithms for speed scaling [26].

Proposition 8.

The fluid value functions for the speed scaling can be computed or approximated for general :

-

1.

For polynomial cost, the value function and optimal policy for the fluid model are given by,

(47) (48) -

2.

For exponential cost, the fluid value function satisfies the following upper and lower bounds: On setting and , there are constants such that the following holds whenever ,

Proof.

(i) From (16), the value function for the fluid model solves the following equation:

| (49) |

Equivalently,

where is the minimizer of the function . For each , this function is decreasing on ; thus . Using the first-order optimality condition gives

| (50) |

By substituting (50) into (49), we have , which gives the desired value function and optimal policy.

We now prove (ii). The fluid value function satisfies the dynamic programming equation

Arguing as in case (i), we see that the minimizer of the right-hand-side satisfies . The first-order optimality condition gives:

| (51) |

By substituting (51) for into the dynamic programming equation, and after some manipulation, we arrive at

where . Letting , we can write the above as,

| (52) |

alternatively

| (53) |

where is the Lambert W function.

To show the bounds on , write . Now

where the inequality holds for . Using the substitution , taking and letting we obtain

Again using that , we can derive an upper bound on as follows,

This completes the proof.

The next section applies elementary calculus to obtain bounds on value functions.

Appendix B Error bounds

We now establish the bounds on direct and Bellman error surveyed in the paper. The first proof establishes bounds on the direct error in terms of the Bellman error:

Proof of Proposition 2

We first obtain an upper bound on the direct error . Based on the assumptions, and have the SSP representations. Consequently, the direct error can be written as,

where the last equality follows from the definition of the perturbed cost in (11).

The proof of the lower bound is identical.

Bounds on the Bellman error are obtained using elementary calculus in the following.

Proof of Proposition 3

By the Mean Value Theorem, there exists a random variable between and such that,

From the definition of the Bellman error (10), we have

The first term in brackets is made smaller if is replaced by , and then vanishes by (16). This gives the desired lower bound on the Bellman error.

The proof of the upper bound is similar: From the definition of the Bellman error (10), we have

| (54) | ||||

By the Mean Value Theorem, there exists a random variable between and such that

The following properties of the fluid value function with quadratic will be used repeatedly in the analysis that follows. We note that part (i) of the lemma holds whenever is convex and increasing.

Lemma 9.

Proof.

The first derivative of in (30) is

| (56) |

It is an increasing, concave and positive function. Consequently, the function is convex and increasing.

The second derivative of is

| (57) |

It is positive, decreasing, and vanishes as as .

The proof for the properties of is identical.

Proof of Proposition 5

The convexity and monotonicity of is established in Lemma 9.

Proof of Proposition 6

It is easy to verify that the derivative of defined in (38) is increasing, so that is convex. Moreover, it is non-decreasing since .

Using the first-order optimality condition in the definition of the Bellman error gives the minimizer in (37),

| (59) |

Substituting (34) and (59) into (37) gives,

| (60) | ||||

The first term in can be approximating using Taylor series,

| (61) | ||||

To compute the bounds on in (66), we first give some properties of the -myopic policy in the following lemma.

Lemma 10.

The policy satisfies

Proof.

On denoting , we can express the -myopic policy by using the first-order optimality condition in the definition (6),

Since is a concave function of , a result given in Lemma 9, by Jensen’s inequality we obtain

| (62) | ||||

The first equality is justified because has bounded support and is , so we can justify the exchange of expectation and derivative. The first inequality follows from convexity of .

Proof of Proposition 4 Part (i)

The lower bound of follows directly from Proposition 3 Part (i),

| (66) | ||||

where the second and third inequalities follow from Lemma 9 that the second derivative of is positive and decreasing.

Combining Lemma 10 and Assumption A1 we obtain

| (67) |

Similarly, the upper bound of the Bellman error follows from Proposition 3 Part (ii),

where the second inequality follows from the fact that is decreasing.

The fluid optimal policy based on is , and (57) provides an expression for the second derivative of . Substituting these expressions in the previous limit gives,

| (68) |

To bound the direct error, we begin with a lemma useful to obtain finer bounds on value functions. A drift condition for this purpose is a relaxation of (8) called Poisson’s inequality [12, 22]: For some policy , a constant , and a function ,

| (69) |

where , and , as in (8).

It is simplest to state the following result for a general Markov chain on :

Proposition 11.

Suppose that Poisson’s inequality (69) holds, and that the continuous functions and satisfy for some , and ,

Then there exists a bounded set such that for any scalar satisfying and , there exists a solution to (V3) of [23],

where is a bounded set, is a constant, and the functions satisfy, for perhaps a different ,

Proof.

The function is given by . First note that Poisson’s inequality implies a version of (V3),

where , is a constant, and is a bounded interval. This holds because of the assumptions on .

The bound is then a simple application of concavity:

| (70) | ||||

Taking conditional expectations given gives,

which implies the result.

The following lemma is based on the Comparison Theorem in [23].

Lemma 12.

The following inequality holds,

where and are two constants.

Proof.

By Proposition 1, the fluid value function also satisfies the ACOE,

| (71) |

where is the inverse dynamic programming solution given in (11), and is an arbitrary constant.

It shows that the following Poisson’s equation holds,

where , , and is a Lyapunov function. Applying (30) and (33), there exist and such that

Consequently, Proposition 11 implies that there exists a solution of (V3):

where , is a bounded set, is a constant, and the functions satisfy, for ,

Proof of Proposition 4 Part (ii)

We first obtain an upper bound on . Combining Proposition 2 and Lemma 12 gives the desired upper bound on the direct error:

The proof of the lower bound is similar. Proposition 4 implies that there exist a constant and a bounded set such that,

| (72) |

By Lemma 11.3.10 in [23] and the bound (32) assumed in Assumption A2, we have , where is a constant. Consequently, Proposition 2 together with (72) gives the lower bound on the direct error,

References

- [1] ”Intel Xscale.” [Online]. Available:www.intel.com/design/intelxscale.

- [2] Susanne Albers and Hiroshi Fujiwara. Energy-efficient algorithms for flow time minimization. In Lecture Notes in Computer Science (STACS), volume 3884, pages 621–633, 2006.

- [3] Lachlan LH Andrew, Minghong Lin, and Adam Wierman. Optimality, fairness, and robustness in speed scaling designs. In ACM SIGMETRICS Performance Evaluation Review, volume 38, pages 37–48. ACM, 2010.

- [4] Nikhil Bansal, Kirk Pruhs, and Cliff Stein. Speed scaling for weighted flow times. In Proc. ACM-SIAM SODA, pages 805–813, 2007.

- [5] D. P. Bertsekas. Dynamic programming and optimal control. Vol. I, volume 1. Athena Scientific, Belmont, MA, third edition, 2005.

- [6] D. P. Bertsekas. Dynamic Programming and Optimal Control, volume 2. Athena Scientific, 4th edition, 2012.

- [7] Dimitri P Bertsekas and John N Tsitsiklis. An analysis of stochastic shortest path problems. Mathematics of Operations Research, 16(3):580–595, 1991.

- [8] D.P. Bertsekas and J. N. Tsitsiklis. Neuro-Dynamic Programming. Atena Scientific, Cambridge, Mass, 1996.

- [9] V. S. Borkar. Convex analytic methods in Markov decision processes. In Handbook of Markov decision processes, volume 40 of Internat. Ser. Oper. Res. Management Sci., pages 347–375. Kluwer Acad. Publ., Boston, MA, 2002.

- [10] S. J. Bradtke and A. G. Barto. Linear least-squares algorithms for temporal difference learning. Mach. Learn., 22(1-3):33–57, 1996.

- [11] David P. Bunde. Power-aware scheduling for makespand and flow. In Proc. ACM Symp. Parallel Alg. and Arch., 2006.

- [12] R-R. Chen and S. P. Meyn. Value iteration and optimization of multiclass queueing networks. Queueing Syst. Theory Appl., 32(1-3):65–97, 1999.

- [13] Wei Chen, Dayu Huang, Ankur A. Kulkarni, Jayakrishnan Unnikrishnan, Quanyan Zhu, Prashant Mehta, Sean Meyn, and Adam Wierman. Approximate dynamic programming using fluid and diffusion approximations with applications to power management. In Proc. of the 48th IEEE Conf. on Dec. and Control; held jointly with the 2009 28th Chinese Control Conference, pages 3575–3580, 2009.

- [14] Jennifer M. George and J. Michael Harrison. Dynamic control of a queue with adjustable service rate. Operations Research, 49(5):720–731, September 2001.

- [15] S. G. Henderson, S. P. Meyn, and V. B. Tadić. Performance evaluation and policy selection in multiclass networks. Discrete Event Dynamic Systems: Theory and Applications, 13(1-2):149–189, 2003. Special issue on learning, optimization and decision making (invited).

- [16] Stefanos Kaxiras and Margaret Martonosi. Computer Architecture Techniques for Power-Efficiency. Morgan and Claypool, 2008.

- [17] V. R. Konda and J. N. Tsitsiklis. On actor-critic algorithms. SIAM J. Control Optim., 42(4):1143–1166 (electronic), 2003.

- [18] S. Mannor, I. Menache, and N. Shimkin. Basis function adaptation in temporal difference reinforcement learning. Annals of Oper. Res., 134(2):215–238, 2005.

- [19] S. P. Meyn. The policy iteration algorithm for average reward Markov decision processes with general state space. IEEE Trans. Automat. Control, 42(12):1663–1680, 1997.

- [20] S. P. Meyn. Stability and optimization of queueing networks and their fluid models. In Mathematics of stochastic manufacturing systems (Williamsburg, VA, 1996), pages 175–199. Amer. Math. Soc., Providence, RI, 1997.

- [21] S. P. Meyn. Algorithms for optimization and stabilization of controlled Markov chains. Sādhanā, 24(4-5):339–367, 1999. Special invited issue: Chance as necessity.

- [22] S. P. Meyn. Control Techniques for Complex Networks. Cambridge University Press, Cambridge, 2007. Pre-publication edition available online.

- [23] S. P. Meyn and R. L. Tweedie. Markov chains and stochastic stability. Cambridge University Press, Cambridge, second edition, 2009. Published in the Cambridge Mathematical Library. 1993 edition online.

- [24] Sean Meyn, Wei Chen, and Daniel O’Neill. Optimal cross-layer wireless control policies using td learning. In Proc. of the 49th IEEE Conf. on Dec. and Control, pages 1951 –1956, 2010.

- [25] C.C. Moallemi, S. Kumar, and B. Van Roy. Approximate and data-driven dynamic programming for queueing networks. Submitted for publication., 2006.

- [26] T. Kimbrel N. Bansal and K. Pruhs. Speed scaling to manage energy and temperature. J. ACM, 54(1):1–39, March 2007.

- [27] Kirk Pruhs, Patchrawat Uthaisombut, and Gerhard Woeginger. Getting the best response for your erg. In Scandinavian Worksh. Alg. Theory, 2004.

- [28] Kirk Pruhs, Rob van Stee, and Patchrawat Uthaisombut. Speed scaling of tasks with precedence constraints. In Proc. Workshop on Approximation and Online Algorithms, 2005.

- [29] J. N. Tsitsiklis and B. Van Roy. An analysis of temporal-difference learning with function approximation. IEEE Trans. Automat. Control, 42(5):674–690, 1997.

- [30] M. H. Veatch. Approximate dynamic programming for networks: Fluid models and constraint reduction, 2004. Submitted for publication.

- [31] C. Wei. Value function approximation architectures for neuro-dynamic programming. PhD thesis, Harvard University Cambridge, Massachusetts, 2013.

- [32] D. J. White. Dynamic programming, Markov chains, and the method of successive approximations. J. Math. Anal. Appl., 6:373–376, 1963.

- [33] A. Wierman, L. Andrew, and A. Tang. Power-aware speed scaling in processor sharing systems. In Proc. of INFOCOM, pages 2007–15, 2009.

- [34] L. Xie and P. R. Kumar. A network information theory for wireless communication: scaling laws and optimal operation. IEEE Trans. on Info. Theory, 50(5):748–767, 2004.

- [35] Francis Yao, Alan Demers, and Scott Shenker. A scheduling model for reduced CPU energy. In Proc. IEEE Symp. Foundations of Computer Science (FOCS), pages 374–382, 1995.

- [36] Sushu Zhang and K. S. Catha. Approximation algorithm for the temperature-aware scheduling problem. In Proc. IEEE Int. Conf. Comp. Aided Design, pages 281–288, November 2007.