Randomized Methods for Design of Uncertain Systems: Sample Complexity and Sequential Algorithms

Abstract

In this paper, we study randomized methods for feedback design of uncertain systems. The first contribution is to derive the sample complexity of various constrained control problems. In particular, we show the key role played by the binomial distribution and related tail inequalities, and compute the sample complexity. This contribution significantly improves the existing results by reducing the number of required samples in the randomized algorithm. These results are then applied to the analysis of worst-case performance and design with robust optimization. The second contribution of the paper is to introduce a general class of sequential algorithms, denoted as Sequential Probabilistic Validation (SPV). In these sequential algorithms, at each iteration, a candidate solution is probabilistically validated, and corrected if necessary, to meet the required specifications. The results we derive provide the sample complexity which guarantees that the solutions obtained with SPV algorithms meet some pre-specified probabilistic accuracy and confidence. The performance of these algorithms is illustrated and compared with other existing methods using a numerical example dealing with robust system identification.

keywords:

randomized and probabilistic algorithms, uncertain systems, sample complexity, , ,

1 Introduction

The use of randomized algorithms for systems and control has matured thanks to the considerable research efforts made in recent years. Key areas where we have seen convincing developments include uncertain and hybrid systems [37, 41]. A salient feature of this approach is the use of the theory of rare events and large deviation inequalities, which suitably bound the tail of the probability distribution. These inequalities are crucial in the area of statistical learning theory [39], which has been utilized for feedback design of uncertain systems [42].

Design in the presence of uncertainty is of major relevance in different areas, including mathematical optimization and robustness [7, 31]. The goal is to find a feasible solution which is optimal in some sense for all possible uncertainty instances. Unfortunately, the related semi-infinite optimization problems are often NP-hard (examples of NP-hard problems in systems and control can be found in [8, 9]), and this may seriously limit their applicability from the computational point of view. There are two approaches to resolve this NP-hard issue. The first approach is based on the computation of deterministic relaxations of the original problem, which are usually polynomial time solvable. However, this might lead to overly conservative solutions [35]. An alternative is to assume that a probabilistic description of the uncertainty is available. Then, a randomized algorithm may be developed to compute, in polynomial time, a solution with probabilistic guarantees [37, 41]. Stochastic programming methods [34] are similar in spirit to the methods studied in this paper and take advantage that, for random uncertainty, the underlying probability distributions are known or can be estimated. The goal is to find a solution that is feasible for almost all possible uncertainty realizations and maximizes the expectation of some function of the decisions variables.

The field of probabilistic methods [38, 14, 37] has received a growing attention in the systems and control community. Two complementary approaches, non-sequential and sequential, have been proposed. A classical approach for non-sequential methods is based upon statistical learning theory [39], [41]. Subsequent work along this direction includes [27], [42], [43], [2], [18]. Furthermore, in [4], [3] and [29] the case in which the design parameter set has finite cardinality is analyzed. The advantage of these methods is that the problem under attention may be non-convex. For convex optimization problems, a non-sequential paradigm, denoted as the scenario approach, has been introduced in [11] and [12], see also [16], [17], [10], [4] for more advanced results, and [33], [40] for recent developements in the areas of stochastic hybrid systems and multi-stage optimization, respectively. Finally, we refer to [23] for a randomized approach to solve approximate dynamic programming.

In non-sequential methods, the original robustness problem is reformulated as a single optimization problem with sampled constraints, which are randomly generated. A relevant feature of these methods is that they do not require any validation step and the sample complexity is defined a priori. The main result of this line of research is to derive explicit lower bounds to the required sample size. However, the obtained explicit sample bounds can be overly conservative because they rely on a worst-case analysis and grow (at least linearly) with the number of decision variables.

For sequential methods, the resulting iterative algorithms are based on stochastic gradient [15], [32], ellipsoid iterations [26], [30]; or analytic center cutting plane methods [13], [44], see also [5, 19] for other classes of sequential algorithms. Convergence properties in finite-time are one of the focal points of these papers. Various control problems have been solved using these sequential randomized algorithms, including robust LQ regulators [32], switched systems [28] and uncertain linear matrix inequalities (LMIs) [15]. Sequential methods are often used for uncertain convex feasibility problems because the computational effort at each iteration is affordable. However, they have been studied also for non-convex problems, see [2], [25].

The common feature of most of these sequential algorithms is the use of the validation strategy presented in [30] and [22]. The candidate solutions provided at each iteration of these algorithms are tested using a validation set which is drawn according to the probability measure associated to the uncertainty. If the candidate solution satisfies the design specifications for every sampled element of this validation set, then it is classified as probabilistic solution and the algorithm terminates. The main point in this validation scheme is that the cardinality of the validation set increases very mildly at each iteration of the algorithm. The strategy guarantees that, if a probabilistic solution is obtained, then it meets some probabilistic specifications.

In this paper, we derive the sample complexity for various analysis and design problems related to uncertain systems. In particular we provide new results which guarantee that the tail of the binomial distribution is bounded by a pre-specified value. These results are then applied to the analysis of worst-case performance and constraint violation. With regard to design problems, we consider the special cases of finite families and robust convex optimization problems. This contribution improves the existing results by reducing the number of samples required to solve the design problem. We remark that the results we have obtained are fairly general and the assumptions on convexity and on finite families appear only in Section 4 which deals with probabilistic analysis and design.

The second main contribution of this paper is to propose a sequential validation scheme, denoted as Sequentially Probabilistic Validation (SPV), which allows the candidate solution to violate the design specifications for one (or more) of the members of the validation set. The idea of allowing some violations of the constraints is not new and can be found, for example, in the context of system identification [6], chance-constrained optimization [17] and statistical learning theory [2]. This scheme makes sense in the presence of soft constraints or when a solution satisfying the specifications for all the admissible uncertainty realizations can not be found. In this way, we improve the existing results with this relaxed validation scheme that reduces the chance of not detecting the solution even when it exists. Furthermore, we also show that a strict validation scheme may not be well-suited for some robust design problems.

This paper is based on the previous works of the authors [4] and [1]. However, some results are completely new (Property 4) and others (Theorem 2, Property 1 and Property 3 and their proofs) are significant improvements of the preliminary results presented in the conference papers. Furthermore, the unifying approach studied here, which combines sample complexity results with SPV algorithms, was not present in previous papers. Finally, the numerical example in Section 8, which compares various approaches available in the literature, is also new. The rest of the paper is organized as follows. In the next section, we first introduce the problem formulation. In Section 3, we provide bounds for the binomial distribution which are used in Section 4 to analyze the probabilistic properties of different schemes involving randomization. In Section 5, we introduce the proposed family of probabilistically validated algorithms. The sample complexity of the validating sets is analyzed in Section 6. A detailed comparison with the validation scheme presented in [30] is provided in Section 7. A numerical example where different schemes are used to address a robust identification problem is presented in Section 8. The paper ends with a section of conclusions and an appendix which contains some auxiliary properties and proofs that are used in the previous sections.

2 Problem Statement

We assume that a probability measure over the sample space is given. Given , a collection of independent identically distributed (i.i.d.) samples drawn from belongs to the Cartesian product ( times). Moreover, if the collection of i.i.d. samples is generated from according to the probability measure , then the multisample is drawn according to the probability measure . The scalars and denote probabilistic parameters called accuracy and confidence, respectively. Furthermore, is the natural logarithm and is the Euler number. For , , denotes the largest integer smaller than or equal to ; denotes the smallest integer greater or equal than . For ,

denotes the Riemann zeta function.

In a robustness problem, the controller parameters and auxiliary variables are parameterized by means of a decision variable vector , which is denoted as design parameter and is restricted to a set . Furthermore, the uncertainty is bounded in the set and represents one of the admissible uncertainty realizations. We also consider a binary measurable function and a real measurable function which helps to formulate the specific design problem under attention. More precisely, the binary function , is defined as

where design specifications are, for example, norm bounds on the sensitivity function, see specific examples in [37], or the numerical example in Section 8.

Given , the constraint is satisfied for a subset of . This concept is rigorously formalized by means of the notion of probability of violation, which is now introduced.

Definition 1.

[probability of violation] Consider a probability measure over and let be given. The probability of violation of for the function is defined as

Using this notion we study the robust optimization problem

| (1) |

where is a measurable function which represents the controller performance and is a probabilistic accuracy. Given accuracy and confidence , the main point of the probabilistic approach is to design an algorithm such that any probabilistic solution obtained by running the algorithm, satisfies with probability no smaller than .

Even in analysis problems when is given, it is often very hard to compute the exact value of the probability of violation because this requires to solve a multiple integral with a usually non-convex domain of integration. However, we can approximate its value using the concept of empirical mean. For given , and multisample drawn according to the probability measure , the empirical mean of with respect to is defined as

Clearly, the empirical mean is a random variable. Since is a binary function, is always within the closed interval .

The power of randomized algorithms stems from the fact that they can approximately solve non-convex design problems (with no-violation) of the type

| (2) |

In this setting, we draw i.i.d. samples from according to probability and solve the sampled optimization problem

| (3) |

Since obtaining a global solution to this problem is still a difficult task in general, in this paper we analyze the probabilistic properties of any suboptimal solution. Furthermore, if at most violations of the constraints are allowed, the following sampled problem can be used to obtain a probabilistic relaxation to the original problem (2)

| (4) |

Randomized strategies to solve problems (3) and (4) have been studied in [2], see also [37]. In order to analyze the probabilistic properties of any feasible solution to problem (4), we introduce the definitions of non-conforming feasible set and probability of failure.

Definition 2.

[non-conforming feasible set] Given , the integer where , , and multisample , drawn according to the probability measure , the non-conforming feasible set is defined as

Definition 3.

[probability of failure] Given , the integer where , and , the probability of failure, denoted by is defined as

The probability defined here is slightly different than the probability of one-sided constrained failure introduced in [2]. We notice that the non-conforming feasibility set is empty with probability . This means that every feasible solution to problem (4) satisfies with probability . Given the confidence parameter , the objective is to obtain explicit expressions yielding a minimum number of samples such that .

3 Sample complexity for the binomial distribution

In this section, we provide bounds for the binomial distribution which are used in Section 4. Given a positive integer and a nonnegative integer , , and , the binomial distribution function is given by

| (7) |

The problem we address in this section is the explicit computation of the sample complexity, i.e. a function such that the inequality holds for any , where . As it will be illustrated in the following section, the inequality plays a fundamental role in probabilistic methods. Although some explicit expressions are available, e.g. the multiplicative and additive forms of Chernoff bound [20], the results obtained in this paper are tuned on the specific inequalities stemming from the problems described in Section 4.

The following technical lemma provides an upper bound for the binomial distribution .

Lemma 1.

Suppose that and that the nonnegative integer and the positive integer satisfy . Then,

Proof: The proof of the lemma follows from the following sequence of inequalities:

∎

We notice that each particular choice of provides an upper bound for . When using Lemma 1 to obtain a specific sample complexity, the selected value for plays a significant role.

Lemma 2.

Given and the nonnegative integer , suppose that the integer and the scalars and satisfy the inequality

| (11) |

Then, and .

Proof: We first prove that if inequality (11) is satisfied then . Since and , (11) implies

Next, we notice that

Since for every , it follows that

Using this fact, we conclude that is a strictly increasing function for . This means that

We now prove that (11) guarantees that . The inequality (11) can be rewritten as

| (12) |

Since for every , and , from inequality (12), we obtain a sequence of inequalities

We have therefore proved that inequality (11) implies and . The claim of the property follows directly from Lemma 1. ∎

Obviously, the best sample size bound is obtained taking the infimum with respect to . However, this requires to solve numerically a one-dimensional optimization problem for given , and . We observe that a suboptimal value can be immediately obtained setting equal to the Euler constant, which yields the sample complexity

| (13) |

Since , we obtain , which is (numerically) a significant improvement of the bound given in [10] and other bounds available in the literature [14]. We also notice that, if then the choice

provides a less conservative bound at the price of a more involved expression [4]. Based on extensive numerical computations for several values of , and we conclude that this bound is very close to the “optimal” one. Note, however, that the optimal value can be obtained numerically using the Lambert function [21]. In the next corollary, we present another more involved sample complexity bound which improves (13) for some values of the parameters.

Corollary 1.

Given and the nonnegative integer , suppose that the integer and the scalar satisfy the inequality

| (14) |

Then, and .

The proof of this corollary is shown in the appendix.

4 Sample complexity for probabilistic analysis and design

We now study some problems in the context of randomized algorithms where one encounters inequalities of the form In particular, we show how the results of the previous section can be used to derive explicit sample size bounds which guarantee that the probabilistic solutions obtained from different randomized approaches meet some pre-specified probabilistic properties.

In Subsection 4.2 we derive bounds on when consists of a finite number of elements. On the other hand, if consists of an infinite number of elements, a deeper analysis involving statistical learning theory is needed [37], [41]. In Subsection 4.3 we study the probabilistic properties of the optimal solution of problem (3) under the assumption that is equivalent to , where is a convex function with respect to in . In this case, the result is not expressed in terms of probability of failure because it applies only to the optimal solution of problem (3), and not to every feasible solution.

4.1 Worst-case performance analysis

We recall a result shown in [36] for the probabilistic worst-case performance analysis.

Theorem 1.

Given the function and , consider the multisample drawn from according to probability and define If

then with probability no smaller than .

The proof of this statement can be found in [36] and is based on the fact that with probability no smaller than . Therefore, it suffices to take such that .

4.2 Finite families for design

We consider the non-convex sampled problem (4) for the special case when consists of a set of finite cardinality . As a motivation, we study the case when, after an appropriate normalization procedure, the design parameter set is rewritten as Suppose also that a gridding approach is adopted. That is, for each component , of the design parameters , only equally spaced values are considered. That is, is constrained into the set With this gridding procedure, the following finite cardinality set is obtained. We notice that the cardinality of the set is . Another situation in which the finite cardinality assumption holds is when a finite number of random samples in the space of design parameter are drawn according to a given probability, see e.g. [24, 42].

The following theorem states the relation between the binomial distribution and the probability of failure under this finite cardinality assumption.

Theorem 2.

Suppose that the cardinality of is no larger than , , and . Then,

Proof: If there is no element in with probability of violation larger than , then the non-conforming feasible set is empty for every multisample and .

Suppose now that the subset of of elements with probability of violation larger than is not empty. Denote such a set. In this case, given a multisample , the non-conforming feasible set is not empty if and only if the empirical mean is smaller or equal than for at least one of the elements of this set. Therefore

Notice that the last inequality is due to the fact that , and that the binomial distribution is a strictly decreasing function of if (see Property 4 in the Appendix). To conclude the proof it suffices to notice that . ∎

Consider now the optimization problem (4). It follows from Lemma 2 that to guarantee that every feasible solution satisfies with probability no smaller than , it suffices to take such that , where is an upper bound on the cardinality of . As it will be shown next, the required sample complexity in this case grows with the logarithm of . This means that we can consider finite families with high cardinality and still obtain very reasonable sample complexity bounds.

Theorem 3.

Suppose that the cardinality of is no larger than . Given the nonnegative integer , and , if

| (15) |

then . Moreover, if

then .

Proof: From Lemma 2 we have that provided that and . The two claims of the property now follow directly from Lemma 2 and Corollary 1 respectively.

∎

From the definition of and Theorem 3 we conclude that if one draws i.i.d. samples from according to probability , then with probability no smaller than , all the feasible solutions to problem (4) have a probability of violation no larger than , provided that the cardinality of is upper bounded by and the sample complexity is given by

We remark that taking equal to the Euler constant in (15), the following sample size bound

is immediately obtained from Theorem 3. If then a suboptimal value for is given by

4.3 Optimal robust optimization for design

In this subsection, we study the so-called scenario approach for robust control introduced in [12]. To address the semi-infinite optimization problem (2), we solve the randomized optimization problem (3). That is, we generate i.i.d. samples from according to the probability and then solve the following sampled optimization problem:

| (16) |

We consider here the particular case in which , the constraint is convex in for all and the solution of (16) is unique. These assumptions are now stated precisely.

Assumption 1.

[convexity] Let be a convex and closed set. We assume that

where is convex in for every fixed value of .

Assumption 2.

[feasibility and uniqueness] For all possible multisample extractions , , , the optimization problem (16) is always feasible and attains a unique optimal solution. Moreover, its feasibility domain has a nonempty interior.

Uniqueness may be assumed essentially without loss of generality, since in case of multiple optimal solutions one may always introduce a suitable tie-breaking rule [12]. We now state a result that relates the binomial distribution to the probabilistic properties of the optimal solution obtained from (16). See [16, 10, 17].

Lemma 3.

Let Assumptions 1 and 2 hold. Suppose that , and satisfy the inequality

| (17) |

Then, with probability no smaller than , the optimal solution to the optimization problem (16) satisfies the inequality .

We now state an explicit sample size bound, which improves upon previous bounds, to guarantee that the probability of violation is smaller than with probability at least .

Theorem 4.

Let Assumptions 1 and 2 hold. Given and , if

| (18) |

or

| (19) |

then, with probability no smaller than , the optimal solution to the optimization problem (16) satisfies the inequality .

Proof: From Lemma 3 it follows that it suffices to take such that . Both inequalities (18) and (19) guarantee that (see Lemma 2 and Corollary 1 respectively). This completes the proof.

∎

Taking equal to the Euler constant in (18), we obtain

which improves the bound given in [10] and other bounds available in the literature [14]. More precisely, the constant 2 appearing in [10] is reduced to , which is (numerically) a substantial improvement for small values of . If a suboptimal value for is given by

5 Sequential algorithms with probabilistic validation

In this section, we present a general family of randomized algorithms, which we denote as Sequential Probabilistic Validation (SPV) algorithms. The main feature of this class of algorithms is that they are based on a probabilistic validation step. This family includes most of the sequential randomized algorithms that have been presented in the literature and are discussed in the introduction of this paper.

Each iteration of an SPV algorithm includes the computation of a candidate solution for the problem and a subsequent validation step. The results provided in this paper are basically independent of the particular strategy chosen to obtain candidate solutions. Therefore, in the following discussion we restrict ourselves to a generic candidate solution. The accuracy and confidence required for the probabilistic solution play a relevant role when determining the sample size of each validation step. The main purpose of this part of the paper is to provide a validation scheme which guarantees that, for given accuracy and confidence , all the probabilistic solutions obtained running the SPV algorithm have a probability of violation no larger than with probability no smaller than .

We enumerate each iteration of the algorithm by means of an integer . We denote by the number of violations that are allowed at the validation step of iteration . We assume that is a function of , that is, where the function is given. We also denote by the sample size of the validation step of iteration . We assume that is a function of , and . That is, where has to be appropriately designed in order to guarantee the probabilistic properties of the algorithm. In fact, one of the main contributions of [30, 22] is to provide this function for the particular case for every . The functions and are denoted as level function and cardinality function respectively.

We now introduce the structure of an SPV algorithm

-

(i)

Set accuracy and confidence equal to the desired levels. Set equal to 1.

-

(ii)

Obtain a candidate solution to the robust optimization problem (1).

-

(iii)

Set and .

-

(iv)

Obtain validation set drawing i.i.d. validation samples from according to probability .

-

(v)

If , then is a probabilistic solution.

-

(vi)

Exit if the exit condition is satisfied.

-

(vii)

. Goto (ii).

Although the exit condition can be quite general, a reasonable choice is to exit after a given number of candidate solutions have been classified as probabilistic solutions or when a given computational time has elapsed since the starting of the algorithm. After exiting one could choose the probabilistic solution which maximizes a given performance index. We notice that in step (iv) we need to satisfy the i.i.d. assumption, and therefore sample reuse techniques are not applicable. In the next section, we propose a strategy to choose the cardinality of the validation set at iteration in such a way that, with probability no smaller than , all candidate solutions classified as probabilistic solutions by the algorithm meet the accuracy .

6 Adjusting the validation sample size

The cardinality adjusting strategy provided in this section constitutes a generalization of that presented in [30] and [22]. To obtain the results of this section we rely on some contributions on the sample complexity presented in the previous sections.

We now formally introduce the failure function.

Definition 4 (failure function).

The function is said to be a failure function if it satisfies the following conditions:

-

(i)

for every positive integer .

-

(ii)

We notice that the function

where is the Riemann zeta function, is a failure function for every . This is due to the fact that converges for every scalar greater than 1 to . This family has been used in the context of validation schemes in [22] and in [30] for the particular value .

Property 1.

Consider an SPV algorithm with given accuracy parameter , confidence , level function and cardinality function . If , for all , and there exists a failure function such that

then, with probability greater than , all the probabilistic solutions obtained running the SPV algorithm have a probability of violation no greater than .

The proof of this property follows the same lines as the proof of Theorem 9 in [30].

Proof: We denote by the probability of classifying at iteration the candidate solution as a probabilistic solution under the assumption that the probability of violation is larger than . Furthermore, let , then

Property 4 in the Appendix, , and have been used to derive the last inequality. Then, we obtain

Therefore, the probability of misclassification of a candidate solution at iteration is smaller than . We conclude that the probability of erroneously classifying one or more candidate solutions as probabilistic solutions is bounded by

∎

We now present the main contribution of this part of the paper, which is a general expression for the cardinality of the validation set at each iteration of the algorithm.

Theorem 5.

Consider an SPV algorithm with given accuracy , confidence and level function . Suppose also that is a failure function. Then, the cardinality function

guarantees that, with probability greater than , all the probabilistic solutions obtained running the SPV algorithm have a probability of violation no greater than .

Proof: Corollary 1 guarantees that the proposed choice for the cardinality function satisfies , for all , and

The result then follows from a direct application of Property 1. ∎

We notice that the proposed cardinality function in Theorem 5 depends on the previous selection of the level function and the failure function . A reasonable choice for these functions is , where is a non-negative scalar and where is greater than one. We recall that this choice guarantees that is a failure function. As shown in the following section, the proposed level and failure functions allow us to recover, for the particular choice the validation strategies proposed in [22] and [30]. In the next corollary, we specify the generic structure of the SPV algorithm with the level function , and state a probabilistic result.

Corollary 2.

Consider an SPV algorithm of the form given in Section 5 in which steps (i) and (iii) are substituted by

-

(i)

Set accuracy , confidence and scalars , equal to the desired levels. Set equal to 1.

-

(iii)

Set and

Then, with probability greater than , all the probabilistic solutions obtained running the SPV algorithm have a probability of violation no greater than .

Proof: The result is obtained directly from Theorem 5 using as level function and failure function . ∎

Since the probabilistic properties of the algorithm presented in Corollary 2 are independent of the particular value of , a reasonable choice for is to select this parameter to minimize the cardinality of the validation sample set.

7 Comparison with other validation schemes

In this section, we provide comparisons with the validation schemes presented in [30, 22]. We notice that setting and in Corollary 2 we obtain for every iteration and

This is the same cardinality function presented in [30] if one takes into account that for small values of , can be approximated by . In the same way, and lead to the cardinality function presented in [22].

We notice that not allowing any failure in each validation test makes perfect sense for convex problems if the feasibility set is not empty. Under this assumption, the algorithm takes advantage of the validation samples that have not satisfied the specifications to obtain a new candidate solution. If is not empty, a common feature of the methods which use this strict validation scheme is that a probabilistic solution (not necessarily belonging to the feasibility set ) is obtained in a finite number of iterations of the algorithm, see e.g., [5], [13], [30].

A very different situation is encountered when is empty. We now state a property showing that a strict validation scheme () should not be used to address the case of empty robust feasible set because the algorithm might fail to obtain a probabilistic solution even if the set is not empty.

Property 2.

Consider the SPV algorithm presented in Corollary 2 with and . Suppose that for all . Then the SPV algorithm does not find any probabilistic solution in the first iterations of the algorithm with probability greater than

where the function is given by

where is a strictly positive scalar and is a non-negative integer.

Proof: We notice that implies that, at iteration , the algorithm classifies a candidate solution as a probabilistic solution only if it satisfies the constraint , where is the randomly obtained validation set . Since for all and , the probability of classifying a candidate solution as a probabilistic solution at iteration is no greater than

Therefore, the probability of providing a probabilistic solution at any of the first iterations of the algorithm is smaller than

Taking and using Property 5 in the Appendix we have

We conclude that the probability of not finding any probabilistic solution in the first iterations of the algorithm is smaller than

∎

We now present an example demonstrating that a strict validation scheme may not be well-suited for a robust design problem.

Example 1.

Suppose that , , , and

Suppose also that is the uniform distribution. It is clear that minimizes the probability of violation and satisfies . Therefore, we obtain Consider now the choice and a maximum number of iterations equal to . We conclude from Property 2 that, regardless of the strategy used to obtain candidate solutions, the choice and in Corollary 2, no probabilistic solution with probability greater than is found. The choice leads to a probability greater than . This illustrates that a strict validation scheme is not well suited for this robust design problem.

∎

The next result states that the probabilistic validation scheme presented in this paper achieves, under minor technical assumptions, a solution with probability one in a finite number of iterations.

Property 3.

Consider an SPV algorithm with given accuracy parameter , confidence and level function . Suppose that

-

(i)

is a failure function.

-

(ii)

The cardinality function is given by

-

(iii)

There exist an integer , scalars and such that at every iteration a candidate solution satisfying is obtained with probability greater than .

-

(iv)

Then, the SPV algorithm achieves with probability one a solution in a finite number of iterations.

Proof: Using the assumption

we conclude that

Since and converges to , then there exists such that

That is, at each iteration , the SPV algorithm provides candidates solutions satisfying

for every with probability greater than . We notice that is the empirical mean associated to . We recall that the Chernoff inequality (see [37]) guarantees that the probability of obtaining an empirical mean larger than from the value is no larger than . Notice that

Therefore we have that if then with probability no smaller than the candidate solution is classified as a probabilistic solution. Taking into account that tends to infinity with , there exists such that for every . This means that the probability of classifying a candidate solution as a probabilistic one is no smaller than for every iteration . Since , we conclude that the algorithm obtains a probabilistic solution with probability one. ∎

8 Numerical example

The objective of this numerical example is to obtain probabilistic upper and lower bounds of a given time function with unknown parameters and of the form

where . The uncertainty set is

For a given order , we define the regressor as

The objective of this example is to find a parameter vector , and such that, with probability no smaller than ,

The vector is obtained from the absolute values of . The binary function , is defined as

where “design specifications” means satisfying the following constraint:

for uniformly randomly generated samples .

A similar problem is addressed in [16] using the scenario approach. For the numerical computations, we take and . We address the problem studying the finite families, scenario and SPV approach, and use the explicit sample complexity derived in the previous sections.

8.1 Finite families approach

We apply the results of Section 4.2 to determine both the degree and the parameter vectors that meet the design specification and optimize a given performance index.

In this example a finite family of cardinality is considered. In order to compare the finite family approach with the scenario one, we consider no allowed failures (i.e ). For this choice of parameters (, , and ), the number of samples required to obtain a solution with the specified probabilistic probabilities is (see Theorem 3). A set of samples is drawn (i.i.d.) from . We use these samples to select the optimal parameters corresponding to each of the different regressors . Each pair is obtained minimizing the empirical mean of the absolute value of the approximation error. That is, each pair is the solution to the optimization problem

We notice that the obtained parameters do not necessarily satisfy the probabilistic design specifications. In order to resolve this problem, we consider a new set of candidate solutions of the form

This family has cardinality . We take a large factor to increase the probability to meet the design specifications. Therefore, choosing a large enough value for leads to a non-empty intersection of with the set of parameters that meet the design specifications. In this example, we take and , which yields .

Using the finite family approach, we choose from the design parameter that optimizes a given performance index. We draw from a set of (i.i.d.) samples and select the pair that minimizes the empirical mean of the absolute value of the approximation error in the validation set . That is, we consider the performance index

subject to the constraints

We remark that the feasibility of this problem can be guaranteed in two ways. The first one is to choose large enough. The second one is to allow failures. As previously discussed, in this example we take and .

As the cardinality of has been chosen using Theorem 3, the probability of violation and the probability of failure of the best solution from are bounded by and respectively.

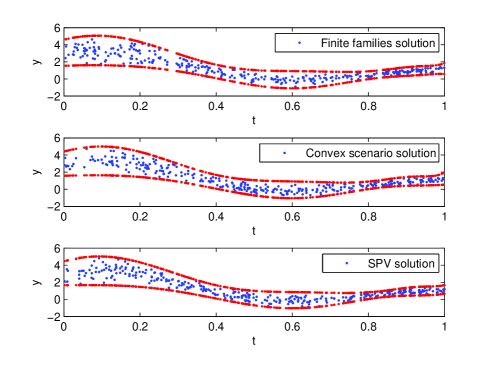

The obtained solution corresponds to and and the value for the performance index is . Figure 1 shows the approximation for the set and the obtained probabilistic upper and lower bounds for the random function.

Finally, for illustrative purposes, we used a validation set of sample size , obtaining a number of violations. The empirical violation probability turned out to be , while the specification was .

8.2 Convex scenario approach

In this case we take advantage of the result of Subsection 8.1 and choose as the order of the approximation polynomial. Following the scenario approach we draw a set of samples (i.i.d) from and solve the convex optimization problem

In order to guarantee the design specifications we use Theorem 4 to determine the value of . Since the number of decision variables is , and , the resulting value for is . We notice that the convex scenario approach does not apply directly to the minimization of the empirical mean. This is why one has to resort to the exact computation of the mean of the approximation error , see [16]. Figure (1) shows the initial data set generated using the procedure described above, plus the envelope that contains all the polynomials.

For illustrative purposes, we check with a validation set of size . The experimental value is obtained, while the specification was . Using this strategy, samples are required, considerably bigger than in the finite families approach. We obtained a performance index of , slightly better than that obtained by the finite families strategy. The advantage of the finite families approach is that, using a smaller number of samples, a similar performance is obtained. This allows us to determine the best order of the polynomial with the further advantage that the exact computation of the mean of the error is not required. Furthermore, the finite family approach does not rely on a convexity assumption.

8.3 SPV algorithm

We again take advantage of the result of Subsection 8.1 and choose as the order of the approximation polynomial. Following the SPV algorithm approach, we begin setting , confidence , scalars , and iteration index . The initial is a set of samples drawn from according to probability .

-

(i)

A candidate solution to the problem

is obtained.

-

(ii)

Set and

-

(iii)

Obtain validation set drawing i.i.d. validation samples from according to the probability .

-

(iv)

If , then is a probabilistic solution.

-

(v)

Exit if the exit condition is satisfied.

-

(vi)

. Goto (i).

Figure (1) shows the initial data set generated using the procedure described above, and the envelope that contains all the solution polynomials. Using this strategy, samples are required. We obtained a performance index of 0.9406, slightly better than the ones obtained by the other approaches.

The level function in the last step of the algorithm is , being the empirical probability of failure

Remark 1.

| 0.1 | 398 | 488 | 988 |

|---|---|---|---|

| 0.05 | 794 | 849 | 1972 |

| 0.01 | 3962 | 7090 | 4163 |

| 0.005 | 7924 | 16078 | 13652 |

| 0.001 | 39614 | 74062 | 41617 |

In Table 1 the results of the three approaches are compared for different values of . Note that , and denote the total number of samples required in each of the three proposed strategies. We notice that, for small values of the probability of violation , the sample complexity corresponding to the convex scenario is the largest one. On the other hand, as can be observed in Table 2, the performance index obtained with the SPV algorithms is slightly better than the ones corresponding to the other two approaches. We recall that the SPV algorithms do not rely on a convexity or finite cardinality assumptions.

| 0.1 | 1.0411 | 0.8803 | 0.8589 |

| 0.05 | 1.0085 | 0.9217 | 0.9597 |

| 0.01 | 0.9841 | 0.9613 | 0.9406 |

| 0.005 | 1.0111 | 1.0447 | 0.9741 |

| 0.001 | 0.9904 | 1.0183 | 0.9828 |

9 Conclusions

In this paper, we have derived sample complexity for various analysis and design problems related to uncertain systems. In particular, we provided new results which guarantee that a binomial distribution is smaller than a given probabilistic confidence. These results are subsequently exploited for analysis problems to derive the sample complexity of worst-case performance and robust optimization. With regard to design problems, these results can be used for finite families and for the special case when the design problem can be recast as a robust convex optimization problem.

We also presented a general class of randomized algorithms based on probabilistic validation, denoted as Sequential Probabilistic Validation (SPV). We provided a strategy to adjust the cardinality of the validation sets to guarantee that the obtained solutions meet the probabilistic specifications. The proposed strategy is compared with other existing schemes in the literature. In particular, it has been shown that a strict validation strategy where the design parameters need to satisfy the constraints for all the elements of the validation set might not be appropriate in some situations. We have shown that the proposed approach does not suffer from this limitation because it allows the use of a non-strict validation test. As it has been shown in this paper, this relaxed scheme allows us to reduce, in some cases dramatically, the number of iterations required by the sequential algorithm. Another advantage of the proposed approach is that it does not rely on the existence of a robust feasible solution. Finally, we remark that this strategy is quite general and it is not based on finite families or convexity assumptions.

This work was supported by the MCYT-Spain and the European Commission which funded this work under projects DPI2010-21589-C05-01, DPI2013-48243-C2-2-R and FP7-257462. The work of Roberto Tempo was supported by the European Union Seventh Framework Programme [FP7/2007-2013] under grant agreement n. 257462 HYCON2 Network of Excellence.

References

- [1] T. Alamo, A. Luque, D.R. Ramirez, and R. Tempo. Randomized control design through probabilistic validation. In Proceedings of the American Control Conference, Montreal, Canada, 2012.

- [2] T. Alamo, R. Tempo, and E.F. Camacho. Randomized strategies for probabilistic solutions of uncertain feasibility and optimization problems. IEEE Transactions on Automatic Control, 54(11):2545–2559, 2009.

- [3] T. Alamo, R. Tempo, and A. Luque. On the sample complexity of probabilistic analysis and design methods. In S. Hara, Y. Ohta, and J. C. Willems, editors, Perspectives in Mathematical System Theory, Control, and Signal Processing, pages 39–50. Springer-Verlag, Berlin, 2010.

- [4] T. Alamo, R. Tempo, and A. Luque. On the sample complexity of randomized approaches to the analysis and design under uncertainty. In Proceedings of the American Control Conference, Baltimore, USA, 2010.

- [5] T. Alamo, R. Tempo, D.R. Ramirez, and E.F. Camacho. A sequentially optimal randomized algorithm for robust LMI feasibility problems. In Proceedings of the European Control Conference, Kos, Greece, 2007.

- [6] E.W. Bai, H. Cho, R. Tempo, and Y. Ye. Optimization with few violated constraints for linear bounded error parameter estimation. IEEE Transactions on Automatic Control, 47(4):1067–1077, 2002.

- [7] A. Ben-Tal and A. Nemirovski. Robust convex optimization. Mathematics of Operations Research, 23:769–805, 1998.

- [8] V. Blondel and J.N. Tsitsiklis. NP-hardness of some linear control design problems. SIAM Journal on Control and Optimization, 35:2118–2127, 1997.

- [9] V. Blondel and J.N. Tsitsiklis. A survey of computational complexity results in system and control. Automatica, 36:1249–1274, 2000.

- [10] G. Calafiore. Random convex programs. SIAM Journal of Optimization, 20:3427–3464, 2010.

- [11] G. Calafiore and M.C. Campi. Uncertain convex programs: Randomized solutions and confidence levels. Mathematical Programming, 102:25–46, 2005.

- [12] G. Calafiore and M.C. Campi. The scenario approach to robust control design. IEEE Transactions on Automatic Control, 51(5):742–753, 2006.

- [13] G. Calafiore and F. Dabbene. A probabilistic analytic center cutting plane method for feasibility of uncertain LMIs. Automatica, 43:2022–2033, 2007.

- [14] G. Calafiore, F. Dabbene, and R. Tempo. Research on probabilistic methods for control system design. Automatica, 47:1279–1293, 2011.

- [15] G. Calafiore and B.T. Polyak. Stochastic algorithms for exact and approximate feasibility of robust lmis. IEEE Transactions on Automatic Control, 11(46):1755––1759, 2001.

- [16] M.C. Campi and S. Garatti. The exact feasibility of randomized solutions of robust convex programs. SIAM Journal of Optimization, 19:1211––1230, 2008.

- [17] M.C. Campi and S. Garatti. A sampling-and-discarding approach to chance-constrained optimization: feasibility and optimality. Journal of Optimization Theory and Applications, 148:257–280, 2011.

- [18] M. Chamanbaz, F. Dabbene, R. Tempo, V. Venkatakrishnan, and Q.-G. Wang. A statistical learning theory approach for uncertain linear and bilinear matrix inequalities. Automatica, 2014 (accepted for publication).

- [19] M. Chamanbaz, F. Dabbene, R. Tempo, V. Venkataramanan, and Q.-G. Wang. Sequential randomized algorithms for convex optimization in the presence of uncertainty. arXiv: arxiv.org/abs/1304.2222, 2013.

- [20] H. Chernoff. A measure of asymptotic efficiency for tests of a hypothesis based on the sum of observations. Annals of Mathematical Statistics, 23:493–507, 1952.

- [21] R.M. Corless, G.H. Gonnet, D.E.G. Hare, D.J. Jeffrey, and D.E. Knuth. On the Lambert W function. Advances in Computational Mathematics, 5:329–359, 1996.

- [22] F. Dabbene, P.S. Shcherbakov, and B.T. Polyak. A randomized cutting plane method with probabilistic geometric convergence. SIAM Journal of Optimization, 20:3185–3207, 2010.

- [23] D.P. de Farias and B. Van Roy. The linear programming approach to approximate dynamic programming. Operations Research, 51:850–865, 2003.

- [24] Y. Fujisaki and Y. Kozawa. Probabilistic robust controller design: probable near minimax value and randomized algorithms. In G. Calafiore and F. Dabbene, editors, Probabilistic and Randomized Methods for Design under Uncertainty, Springer, London, 2006.

- [25] H. Ishii, T. Basar, and R. Tempo. Randomized algorithms for synthesis of switching rules for multimodal systems. IEEE Transactions on Automatic Control, 50:754–767, 2005.

- [26] S. Kanev, B. De Schutter, and M. Verhaegen. An ellipsoid algorithm for probabilistic robust controller design. Systems and Control Letters, 49:365–375, 2003.

- [27] V. Koltchinskii, C.T. Abdallah, M. Ariola, P. Dorato, and D. Panchenko. Improved sample complexity estimates for statistical learning control of uncertain systems. IEEE Transactions on Automatic Control, 12(45):2383–2388, 2000.

- [28] D. Liberzon and R. Tempo. Common Lyapunov functions and gradient algorithms. IEEE Transactions on Automatic Control, 49:990–994, 2004.

- [29] J. Luedtke and S. Ahmed. A sample approximation approach for optimization with probabilistic constraints. SIAM Journal of Optimization, 2(19):674–699, 2008.

- [30] Y. Oishi. Polynomial-time algorithms for probabilistic solutions of parameter-dependent linear matrix inequalities. Automatica, 43:538–545, 2007.

- [31] I.R. Petersen and R. Tempo. Robust control of uncertain systems: Classical results and recent developments. Automatica, 50:1315–1335, 2014.

- [32] B.T. Polyak and R. Tempo. Probabilistic robust design with linear quadratic regulators. Systems and Control Letters, 43:343–353, 2001.

- [33] M. Prandini, S. Garatti, and R. Vignali. Performance assessment and design of abstracted models for stochastic hybrid systems through a randomized approach. Automatica, 50, 2013, provisionally accepted.

- [34] A. Prékopa. Stochastic Programming. Kluwer, Dordrecht, 1995.

- [35] C. Scherer. LMI relaxations in robust control. European Journal of Control, 12:3–29, 2006.

- [36] R. Tempo, E.W. Bai, and F. Dabbene. Probabilistic robustness analysis: explicit bounds for the minimum number of samples. Systems & Control Letters, 30:237–242, 1997.

- [37] R. Tempo, G. Calafiore, and F. Dabbene. Randomized Algorithms for Analysis and Control of Uncertain Systems, with Applications. Springer-Verlag, London, second edition, 2013.

- [38] R. Tempo and H. Ishii. Monte Carlo and Las Vegas Randomized algorithms for systems and control: An introduction. European Journal of Control, 13:189–203, 2007.

- [39] V.N. Vapnik. Statistical Learning Theory. John Wiley and Sons, New York, 1998.

- [40] P. Vayanos, D. Kuhn, and B. Rustem. A constraint sampling approach for multi-stage robust optimization. Automatica, 48:459–471, 2012.

- [41] M. Vidyasagar. A Theory of Learning and Generalization: with Applications to Neural Networks and Control Systems. Springer, London, 1997.

- [42] M. Vidyasagar. Randomized algorithms for robust controller synthesis using statistical learning theory. Automatica, 37:1515–1528, 2001.

- [43] M. Vidyasagar and V.D. Blondel. Probabilistic solutions to some NP-hard matrix problems. Automatica, 37:1397–1405, 2001.

- [44] T. Wada and Y. Fujisaki. Probabilistic cutting plane technique based on maximum volume ellipsoid center. In Proceedings of the IEEE Conference Decision and Control and the Chinese Control Conference, pages 1169–1174, Shanghai, China, 2009.

Appendix A Appendix: Auxiliary proofs and properties

Proof of Corollary 1: We first notice that if , then . Therefore, it follows from that . This proves the result for .

Consider now the case . We first prove that for all Since , the inequality holds if the derivative of is strictly positive for every .

This proves the inequality , for all . Denote now , with . Clearly . Therefore, from a direct application of Lemma 2, we conclude that it suffices to choose such that

Since we conclude that

From this inequality, we finally conclude that inequality holds if

∎

Property 4.

For fixed values of and , , the binomial distribution function is a strictly decreasing function of .

Proof: To prove the property, we show that the derivative of with respect to is negative. Let us define the scalars , as follows

| (22) | |||||

With this definition we have

| (25) | |||||

| (28) |

We consider here two cases, and . In the first case we have from equation (22) that , for . This fact, along with equation (28) implies that the derivative with respect to is negative and therefore the claim of the property is proved for this case.

Consider now the case . In this case we have that , for . Since we obtain

We notice that in the last step of the proof the identity

has been used. ∎

Property 5.

Suppose that is a positive integer and that is a strictly positive scalar. Then, where, given and the integer ,

Proof: Given and , define and . Then we have Next we show that for every integer greater than 0. Since and , the inequality is clearly satisfied for . We now prove the inequality for greater than 1

We have therefore proved the inequality for every integer greater than 0. Using this inequality in a recursive way with we obtain This proves the result. ∎