1.2in1.2in.8in.8in

Homogeneity in Regression

Abstract

This paper explores the homogeneity of coefficients in high-dimensional regression, which extends the sparsity concept and is more general and suitable for many applications. Homogeneity arises when one expects regression coefficients corresponding to neighboring geographical regions or a similar cluster of covariates to be approximately the same. Sparsity corresponds to a special case of homogeneity with a known atom zero. In this article, we propose a new method called clustering algorithm in regression via data-driven segmentation (CARDS) to explore homogeneity. New mathematics are provided on the gain that can be achieved by exploring homogeneity. Statistical properties of two versions of CARDS are analyzed. In particular, the asymptotic normality of our proposed CARDS estimator is established, which reveals better estimation accuracy for homogeneous parameters than that without homogeneity exploration. When our methods are combined with sparsity exploration, further efficiency can be achieved beyond the exploration of sparsity alone. This provides additional insights into the power of exploring low-dimensional strucuture in high-dimensional regression: homogeneity and sparsity. The newly developed method is further illustrated by simulation studies and applications to real data.

Keywords: clustering, homogeneity, sparsity.

1 Introduction

Driven by applications in genetics, image processing, etc., high dimensionality has become one of the major themes in statistics. To overcome the difficulty of fitting high dimensional models, one usually assumes that the true parameters lie in a low dimensional subspace. For example, many papers focus on sparsity, i.e., only a small fraction of coefficients are nonzero. In this article, we consider a more general type of low dimensional structure: homogeneity, i.e., the coefficients share only a few common clusters of values. A motivating example is the gene network analysis, where it is assumed that genes cluster into groups which play similar functions in molecular processes. It can be modeled as a linear regression problem with groups of homogeneous coefficients. Similarly, in diagnostic lab tests, one often counts the number of positive results in a battery of medical tests, which implicitly assumes that their regression coefficients (impact) in the joint models are approximately the same. In spatial-temporal studies, it is not unreasonable to assume the dynamics of neighboring geographical regions are similar, namely, their regression coefficients are clustered. In the same vein, financial returns of similar sectors of industry share similar loadings on risk factors.

Homogeneity is a more general assumption than sparsity, where the latter can be viewed as a special case of the former with a large group of -value coefficients. In addition, the atom 0 is known to data analysts. One advantage of assuming homogeneity rather than sparsity is that it enables us to select more than variables ( is the sample size). Moreover, identifying the homogeneous groups naturally provides a structure in the covariates, which can be helpful in scientific discoveries.

Regression under the homogeneity setting has been studied in a few literature. First of all, the fused lasso (Tibshirani et al., 2005; Friedman et al., 2007) can be regarded as an effort of exploring homogeneity, with the assistance of neighborhoods defined according to either time or location. The difference of our studies is that we do not assume such a neighborhood to be known a priori. The clustering of homogeneous coefficients is completely data-driven. For example, in the fused Lasso, where given a complete ordering of the covariates, Tibshirani et al. (2005) add penalties to the pair of adjacent coordinates; in the case without a complete ordering, they suggest penalizing the pair of ‘neighboring’ nodes in the sense of a general distance measure. Bondell and Reich (2008) propose the method OSCAR where a special octagonal shrinkage penalty is applied to each pair of coordinates to promote equal-value solutions. Shen and Huang (2010) develop an algorithm called Gouping Pursuit, where they add truncated penalties to the pairwise differences for all pairs of coordinates. However, these methods depend either on a known ordering of the covariates, which is usually not available, or exhaustive pairwise penalties, which may increase the computation complexity when the dimension is large.

In this article, we propose a new method called Clustering Algorithm in Regression via Data-driven Segmentation (CARDS) to explore homogeneity. The main idea of CARDS is to take advantage of available estimates without homogeneity structure and shrink those coefficients, that are estimated “close”, further towards homogeneity. In the basic version of CARDS, it first builds an ordering of covariates from a preliminary estimate, then runs a penalized least squares with fused penalties in the new ordering. The number of penalty terms is only , compared to in the exhaustive pairwise penalties. In an advanced version of CARDS, it builds an “ordered segmentation” on the covariates, which can be viewed as a generalized ordering, and imposes so-called “hybrid pairwise penalties”, which can be viewed as a generalization of fused penalties. This version of CARDS is more tolerant on possible misorderings in the preliminary estimate. Compared with other methods for homogeneity, CARDS can successfully deal with the case of unordered covariates. At the same time, it avoids using exhaustive pairwise penalties and can be computationally more efficient than the Grouping Pursuit and OSCAR.

We also provide theoretical analysis on CARDS. It reveals that the sum of squared errors of estimated coefficients is , where is the number of true homogeneous groups. Therefore, the smaller the number of true groups is, the better precision it can achieve. In particular, when , there is no homogeneity to explore and the result reduces to the case without grouping. Moreover, in order to exactly recover the true groups with high probability, the minimum signal strength (the gaps between different groups) is of the order where ’s are sizes of true groups. In addition, the asymptotic normality of our proposed CARDS estimator is established, which reveals better estimation accuracy than that without homogeneity exploration. Furthermore, our results can be further combined with the sparsity results to provide additional insights on the power of the low-dimensional structure in high-dimensional regression: homogeneity and sparsity. Our analysis on the basic version of CARDS also establishes a framework for analyzing the fused type of penalties, which is to our knowledge new to the literature.

Throughout this paper, we consider the following linear regression setting

| (1) |

where is an design matrix, is an vector of response, denotes the true parameters of interest, and with ’s being independent and identically distributed noises with and . We assume further that there is a partition of denoted as such that

| (2) |

where is the common value shared by all indices in . By default, , so is the group of -value coefficients. This allows us to explore homogeneity and sparsity simultaneously. Write . Without loss of generality, we assume .

Our theory and methods are stated for the standard least-squares problem although they can be adapted to other more sophisticated models. For example, when forecasting housing appreciation in the United States (Fan et al., 2011), one builds the spatial-temporal model

| (3) |

in which indicates a spatial location and indicates time. It is expected that are approximately the same for neighboring zip codes and this type of homogeneity can be explored in a similar fashion. Similarly, when represents the returns of a stock and stands for risk factors, one can assume certain degree of homogeneity within a sector of industry; namely, the factor loading vector is approximately the same.

Throughout this paper, denotes the set of real numbers, and for a positive integer , denotes the -dimensional real Euclidean space. For any positive sequences and , we write if tends to infinity as increases to infinity. Given , for any vector , denotes the -norm of . In particular, . For any matrix , denotes the matrix -norm of . In particular, is the maximum absolute row sum of . We omit the subscript when . denotes the maxtrix max norm. When is symmetric, and denote the maximum and minimum eigenvalues of , respectively.

The rest of the paper is organized as follows. Section 2 describes CARDS, including the basic and advanced versions. Section 3 states theoretical properties of the basic version of CARDS, and Section 4 analyzes the advanced version. Sections 5 and 6 present the results of simulation studies and real data analysis. Section 7 contains concluding remarks. Proofs can be found in Section 8.

2 CARDS: a data-driven pairwise shrinkage procedure

2.1 Basic version of CARDS

Without considering the homogeneity assumption (2), there are many methods available for fitting model (1). Let be such a preliminary estimator. A very simple idea to generate homogeneity is as follows: first, rearrange the coefficients in in the ascending order; second, group together those adjacent indices whose coefficients in are close; finally, force indices in each estimated group to share a common coefficient and refit model (1). A main problem of this naive procedure is how to group the indices. Alternatively, we can run a penalized least squares to simultaneously extract the grouping structure and estimate coefficients. To shrink coefficients of adjacent indices (after reordering) towards homogeneity, we can add fused penalties, i.e., are penalized. This leads to the following two-stage procedure:

-

•

Preordering: Construct the rank statistics such that is the -th smallest value in , i.e.,

(4) -

•

Estimation: Given a folded concave penalty function (Fan and Li, 2001) with a regularization parameter , let

(5)

We call this two-stage procedure the basic version of CARDS (bCARDS). In the first stage, it establishes a data-driven rank mapping from the preliminary estimator . In the second stage, only “adjacent” coefficient pairs under the order are penalized, resulting in only penalty terms in total. In addition, note that (5) does not require that . This allows coordinates in to have a different order of increasing values from that in .

With an appropriately large tuning parameter , is a piecewise constant vector in the order of and consequently its elements have homogeneous groups. In Section 3, we shall show that, if is from a rank consistent estimate of , namely

| (6) |

then under some regularity conditions, can consistently estimate the true coefficient groups of with high probability.

When is a folded-concave penalty function (e.g. SCAD, MCP), (5) is a non-convex optimization problem. It is generally difficult to compute the global minimum. The local linear approximation (LLA) algorithm can be applied to produce a certain local minimum for any fixed initial solution; see Zou and Li (2008); Fan et al. (2012) and references therein for details.

2.2 Advanced version of CARDS

To guarantee the success of CARDS, (6) is an essential condition. To be more specific, (6) requires that within each true group , the order of the coordinates can be arbitrarily shuffled, but for belonging to different true groups, if , must hold. This imposes fairly strong conditions on the preliminary estimator . For example, (6) can be easily violated if is larger than the minimum gap between groups. To relax such a restrictive requirement, we now introduce an advanced version of CARDS, where the main idea is to use less information from and to add more penalty terms in (5).

We first introduce the ordered segmentation, which can be viewed as a generalized ordering. It is similar to letter grades assigned to a class.

Definition 2.1.

For a positive integer , the mapping is called an ordered segmentation if the sets , , form a partition of .

Each set is called a segment. When , is a one-to-one mapping and it defines a complete ordering. When , only the segments are ordered, but the order of coordinates within each segment is not defined.

In the basic version of CARDS, the preliminary estimator produces a complete rank mapping . Now in the advanced version of CARDS, instead of extracting a complete ordering, we only extract an ordered segmentation from . The analogue is similar to grading an exam: overall score rank (percentile rank) versus letter grade. Let be a predetermined parameter. First, obtain the rank mapping as in (4) and find all indices such that the gaps

Then, construct the segments

| (7) |

where and . This process is indeed similar to the letter grade that we assign. The intuition behind this construction is that when , i.e., the estimated coefficients of two “adjacent coordinates” differ by only a small amount, we do not trust the ordering between them and group them into a same segment. Compared to the complete ordering , the ordered segments utilize less information from .

Given an ordered segmentation , how can we design the penalties so that we can take advantage of the ordering of segments and at the same time allow flexibility of order shuffling within each segment? Towards this goal, we introduce the hybrid pairwise penalty.

Definition 2.2.

Given a penalty function and tuning parameters and , the hybrid pairwise penalty corresponding to an ordered segmentation is

| (8) |

In (8), we call the first part between-segment penalty and the second part within-segment penalty. The within-segment penalty penalizes all pairs of indices in each segment, hence, it does not rely on any ordering within the segment. The between-segment penalty penalizes pairs of indices from two adjacent segments, and it can be viewed as a “generalized” fused penalty on segments.

When , each is a singleton and (8) reduces to the fused penalty in (5). On the other hand, when , there is only one segment , and (8) reduces to the exhaustive pairwise penalty

| (9) |

It is also called the total variation penalty, and the case with being a truncated penalty is studied in Shen and Huang (2010). Thus, the penalty (8) is a generalization of both the fused penalty and the total variation penalty, which explains the name “hybrid”.

Now, we discuss how the condition (6) can be relaxed. Parallel to the definition that preserves the order of , we make the following definition.

Definition 2.3.

An ordered segmentation preserves the order of if , for .

By the construction (7), even if does not preserve the order of , it is still possible that the resulting does. Consider a toy example where , and so that and are two true homogeneous groups in . By definition of , ranks wrongly ahead of based on the preliminary estimate . It is obvious that does not preserve the order of . However, as long as , and are grouped into the same segment in (7), say, and . Then still preserves the order of according to the above definition.

Now we formally introduce the advanced version of Clustering Algorithm in Regression via Data-driven Segmentation (aCARDS). It consists of three steps, where the first two steps are very similar to the way that we assign letter grades based on an exam (preliminary estimate).

-

•

Preliminary Ranking: Given a preliminary estimate , generate the rank statistics such that .

-

•

Segmentation: For a tuning parameter , construct an ordered segmentation as described in (7).

-

•

Estimation: For tuning parameters and , compute the solution that minimizes

(10)

In Section 4, we shall show that if preserves the order of , under certain conditions, recovers the true homogeneous groups of with high probability. Therefore, to guarantee the success of this advanced version of CARDS, we need the existence of a for the initial estimate such that the associated preserves the order of . We see from the toy example that even when (6) fails, this condition can still hold. So the advanced version of CARDS requires weaker conditions on . The main reason is that the hybrid penalty contains penalty terms corresponding to more pairs of indices. Hence, it is more robust to possible mis-ordering in . In fact, the basic version of CARDS is a special case with .

2.3 CARDS under sparsity

In applications, we may need to explore homogeneity and sparsity simultaneously. Often the preliminary estimator takes into account the sparsity, namely it is obtained with a penalized least-squares method (Fan and Li, 2001; Tibshirani et al., 2005) or sure independence screening (Fan and Lv, 2008). Suppose has the sure screening property, i.e., with high probability, where and denote the support of and , respectively. We modify CARDS as follows: In the first two steps, using the non-zero elements of , we can similarly construct data-driven hybrid penalties only on coefficients of variables in . In the third step, we fix and obtain by minimizing the following penalized least squares

| (11) |

where is the submatrix of restricted to columns in . In (11), the second term is the hybrid penalty to encourage homogeneity among coefficients of variables already selected in , and the third term is the element-wise penalty to help further filter out falsely selected variables. We call this modified version the shrinkage-CARDS (sCARDS).

3 Analysis of the basic CARDS

In this section, we analyze theoretical properties of the basic CARDS. For simplicity, we assume that there is no group of , i.e., the usual sparsity is not explicitly explored. We first provide heuristics to two essential questions: (1) How does it help reduce the convergence rate of by taking advantage of homogeneity? (2) What is the order of minimum signal strength required for recovering the true groups with high probability? We then formally state our main results. After that, we will give conditions under which the ordinary least squares can provide a good preliminary estimator, as well as the effect of mis-ranking on CARDS.

3.1 Heuristics

Consider an ideal case of orthogonal design (necessarily ). The ordinary least-square estimator has the decomposition

It is clear by the square-root law that . Now, if there are homogeneous groups in and we know the true groups, the original model (1) can be rewritten as

where contains distinct values in , and with . The corresponding ordinary least-squares estimator has the decomposition

| (12) |

Here is the noise averaged over group . The oracle estimator is defined such that for all . Then, by the square-root law,

which implies immediately that .

The surprises of the results are two fold: First, the rate is for instead of . The former can be viewed as duplicate counts of the terms in the latter, hence it can be much larger than the latter. However, since there are parameters in , common heuristics in regression analysis give , and so the convergence rate of should be much larger than . The above results seem to be counter-intuitive. The point is that in (12) the noises are averaged, and so the rate of is much smaller than . In fact, by taking advantage of homogeneity, we not only estimate much fewer parameters, but also reduce the noise level.

The second surprise is that the rate has nothing to do with the sizes of true homogeneous groups. No matter whether we have groups of equal size, or one dominating group and very small groups, the rate is always the same in the oracle situation. This is also a consequence of noise averaging.

Next, we discuss when the CARDS estimator equals the oracle estimator that is based on the knowledge of the true grouping structure. For simplicity, we still consider the case of orthogonal design , and assume the preliminary ordering preserves the order of so that the basic version of CARDS works. Write without loss of generality. CARDS finds a local solution of

where is the vector of marginal correlations (when is also normalized). As a result, if the estimator produced by CARDS is the oracle estimator , necessarily has to satisfy the KKT condition

| (13) |

where for ; and with for , for , and any value on for . Write the true groups as , , for some . It is not hard to show that the sufficient and necessary conditions for (13) to hold are

| (14) |

Here is the estimated coefficient gap between groups and in the oracle estimator, and it is equal to , where is the true coefficient gap between groups and . Also, for , which is purely determined by the noises. Therefore, to guarantee (14), the penalty function must have flat tails, i.e., when ( is a constant); furthermore, the true coefficient gaps , the tuning parameter and the noises need to satisfy, say,

| (15) |

Note that for most sparsity penalty functions; and is much smaller than with high probability. So (15) requires that the minimum true coefficient gap between groups satisfies

| (16) |

Using results in Darling and Erdos (1956), the right hand side of (16) is upper bounded by with high probability, for a sufficiently large constant . Therefore, for CARDS to produce the oracle estimator, the minimum coefficient gap between true groups should be at least in that order. Up to a logarithmic factor, we write this order as .

3.2 Notations and regularity conditions

Let be the subspace of defined by

For each , we can always write , where is an matrix with with denoting the -element of , and is a vector with its th component being the common coefficient in group . Define the matrix . We introduce the following conditions on the design matrix :

Condition 3.1.

, for . The eigenvalues of the matrix are bounded below by and bounded above by .

In the case of orthogonal design, i.e., , the matrix simplifies to , and .

Let and . We assume that the penalty function satisfies the following condition.

Condition 3.2.

is a symmetric function and it is non-descreasing and concave on . exists and is continuous except for a finite number of with . There exists a constant such that is a constant for all .

We also assume that the noise vector has sub-Gaussian tails.

Condition 3.3.

For any vector and , , where is a positive constant.

Given the design matrix , let be its submatrix formed by including columns in , for . For any vector , let be the “deviation from centrality”. Define

| (17) |

where denotes the largest eigenvalue operator. In the case of orthogonal design, and . Let denote the minimal gap between two groups in , and the tuning parameter in the penalty function.

3.3 Main results

When the true groups are known, the oracle estimator is

Theorem 3.1.

Suppose Conditions 3.1-3.3 hold, , and the preliminary estimate generates an order that preserves the order of with probability at least . If and

| (18) |

then with probability at least , is a strictly local minimum of (5). Moreover, .

Theorem 3.1 shows that there exists a local minimum of (5) which is equal to the oracle estimator with overwhelming probability. This strong oracle property is a stronger result than the oracle property in (Fan and Li, 2001).

The bCARDS formulation (5) is a non-convex problem and it may have multiple local minima. In practice, we apply the Local Linear Approximation algorithm (LLA) (Zou and Li, 2008) to solve it: start from an initial solution ; at step , update solution by

Given , this algorithm produces a unique sequence of estimators which converge to a certain local minimum. Theorem 3.2 shows that under certain conditions, the sequence of estimators produced by the LLA algorithm converge to the oracle estimator.

Theorem 3.2.

The penalty is widely used in high-dimensional penalization methods partially due to its convexity. For example, it can be used here to get the initial solution for the LLA algorithm. However, this penalty function is excluded in Condition 3.2, and consequently Theorem 3.1 does not apply. Now, we discuss the penalty in more details.

We first relax the requirement that preserves the order of . Instead, we consider the case that is “consistent” with coefficient groups in , that is, for any two variables in the same true group, variables ranked between them are also in this group (if preserves the order of , belongs to this class). Note that we do not require for all . In this case, recovering the true groups is equivalent to locating jumps (which can have positive or negative magnitudes) in .

Below we introduce an “irrepresentability” condition. For , write . Define the -dimensional vector by , and

Here is the adjacent difference of the sign vector of jumps in . For example, suppose and the common coefficients in 4 groups satisfy , and . Then . Also, define the -dimensional vector

In the case of orthogonal design , and it has the form for . For each , let

Namely, contain indices in group that have ranks in the mapping , and contain those have ranks . Write as the proportion of indices in group which is mapped in front of (and including) . Denote the average of elements in over the indices in , and the average of elements in over the indices in . The following inequality is called the “irrepresentability” condition on and : for any and , ,

| (19) | |||

| (23) |

Here is a positive sequence, which can go to . In the case of orthogonal design, and holds for all and . The “irrepresentability” condition reduces to

This is possible only when

| (24) |

Noting that , the associated can be chosen as when (24) holds.

Theorem 3.3.

Suppose Conditions 3.1 and 3.3 hold, the “irrepresentability” condition (19) is satisfied, , and the preliminary estimate generates an order that is consistent with with probability at least . If and satisfy

| (25) |

then with probability at least , (5) has a unique global minimum such that and it satisfies the sign restrictions , . Moreover, , where .

Compared to Theorem 3.1, there is an extra bias term in the estimation error. We consider an ideal case where the sizes of all groups have the same order , the sequence for some positive constant , and . From (25), the magnitude of the bias term is , which is much larger than . So in the penalty case, it is generally hard to guarantee both exact recovery of the true grouping structure and the -convergence rate of . Moreover, the “irrepresentability” condition is very restrictive, even in the orthogonal design case. From (24), in order to exactly locate all jumps, necessarily all consecutive jumps (in the ordering ) have opposite signs. However, this is sometimes hard to guarantee. Especially when preserves the order of , all the jumps have positive signs.

3.4 Preliminary estimator, effects of mis-ranking

We now give sufficient conditions under which the least-squares estimator induces an order-preserving rank. When sparsity is explored, after the model selection consistency (Fan and Lv, 2011; Fan et al., 2012), the problem becomes a dense problem. Hence, the fundamental insights can be gained when the coefficients are not sparse and it will be the case that we focus upon next.

The ordinary least squares estimator

can be used as the preliminary estimator. The following theorem shows that it induces a rank preserving mapping that satisfies Theorem 3.1.

Theorem 3.4.

Under Condition 3.3, suppose and for some constant . If , then with probability at least , the order generated from preserves the order of .

When the order extracted from does not preserve the order of , the penalty in (5) is no longer a “correct” penalty for promoting the true grouping structure. There is no hope that local minima of (5) exactly recover the true groups. However, if there are not too many misordering in , it is still possible to control .

Given an order , define , which is the number of jumps in in the ordering . These jumps define subgroups , each being a subset of one true group. Although different subgroups may share the same true coefficients, consecutive subgroups, and , have a gap in coefficient values. As a result, the above results apply to this subgrouping structure. The following theorem is a direct application of the proof of Theorem 3.1 and its details are omitted.

4 Analysis of the advanced CARDS

In this section, we analyze the advanced version of CARDS described, as well as its variate the shrinkage-CARDS.

4.1 Main results

To guarantee the success of the advanced CARDS, a key condition is that the ordered segmentation preserves the order of . This implies restrictions on how much the ordering (in terms of increasing values) of coordinates in deviates from that of . This is reflected on how the segments intersect with the true groups . Write . We have the following proposition:

Proposition 4.1.

When preserves the order of , for each , there exist and such that , and for . For each , there exist and such that , and for .

Proposition 4.1 indicates that there are two cases for each : either is contained in a single or it is contained in some consecutive ’s where except the first and last one, all the other ’s are fully occupied by . Similarly, there are two cases for each : either it is contained in a single or it is contained in some consecutive ’s where except the first and last one, all the other ’s are fully occupied by .

Theorem 4.1.

Suppose Conditions 3.1-3.3 hold, , and the preliminary estimate and the tuning parameter together generate an ordered segmentation that preserves the order of with probability at least . If ,

| (26) |

and

| (27) |

then with probability at least , is a strictly local minimum of (10). Moreover, .

Compared to Theorem 3.1, the advanced version of CARDS not only imposes less restrictive conditions on , but also requires a smaller minimum gap between true coefficients.

Next, we establish the asymptotic normality of the CARDS estimator. By Theorem 4.1, with probability tending to , the advanced CARDS performs as if the oracle. In the oracle situation, for example, if and , , the accuracy of estimating is the same as if we know the model:

Theorem 4.2.

Let be any local minimum of (10) such that for a large constant with probability at least . Under conditions of Theorem 4.1, if , then for a fixed positive integer , and any sequence such that , and , where is a fixed positive definite matrix, we have

where is the -dimensional vector of distinct values in .

In the case of orthogonal design , the matrix has orthonormal columns, so it is reasonable to assume . In addition, when all the entries of have the same order, , as long as .

To compare the asymptotic variance of and , we introduce the following corollary.

Corollary 4.1.

Suppose conditions of Theorem 4.2 hold and let and be the ordinary least squares estimator and CARDS estimator respectively. Let be the matrix with . For any sequence of -dimensional vectors ,

where and . In addition, .

4.2 CARDS under sparsity

In Section 2.3, we introduced the shrinkage-CARDS (sCARDS) to explore both homogeneity and sparsity. In sCARDS, given a preliminary estimator and a parameter , we extract segments such that , where is the support of . Denote . In this case, we say preserves the order of if , and , for . This implies that has the sure screening property; and on those preliminarily selected variables, the data-driven segments preserve the order of true coefficients. In particular, from Proposition 4.1, those falsely selected variables, i.e., , should be contained in either a single segment or some consecutive segments.

Suppose there is a group of zero coefficients in , namely, . Let be the subspace of defined by

Denote the support of as and . The following theorem is proved in Section 8.

Theorem 4.3.

Suppose Conditions 3.1-3.3 hold, , , and the preliminary estimate and the tuning parameter together generate an ordered segmentation that preserves the order of with probability at least . If , , and satisfy (26)-(27) and , then with probability at least , is a strictly local minimum of (11). Moreover, .

The preliminary estimator can be chosen, for example, as the SCAD estimator

| (28) |

where is the SCAD penalty function Fan and Li (2001). The following theorem is a direct result of Theorem 2 in Fan and Lv (2011), and the proof is omitted.

Theorem 4.4.

Under Condition 3.1 and 3.3, if , and , then with probability at least , there exists a strictly local minimum and which together generate a segmentation preserving the order of .

5 Simulation studies

We conduct numerical experiments to implement two versions of CARDS and their variate sCARDS. The goal is to investigate the performance of CARDS under different situations: Experiment 1 and 2 are based on the linear regression setting , where in Experiment 1 only the homogeneity is explored, and in Experiment 2 the homogeneity and sparsity are explored simultaneously. Experiment 3 is based on the spatial-temporal model .

In all experiments, or are generated independently and identically from the multivariate standard Gaussian distributions, and or are IID samples of . All results are based on repetitions.

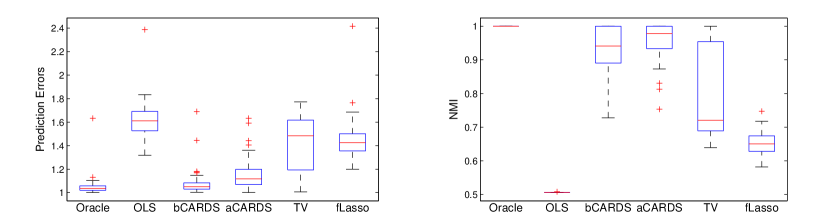

Example 1: Consider the linear regression setting with and . Predictors are divided into four groups with each group having a size of 15. The four different values of the true regression coefficients are , , and , respectively. Here different values of lead to various signal-to-noise ratios.

We compare the performance of six different methods: Oracle, ordinary least squares (OLS), bCARDS, aCARDS, total variations (TV), fused Lasso (fLasso). Oracle is the least squares estimator knowing the true groups. aCARDS and bCARDS are described in Section 2; here we let the penalty function be the SCAD penalty with , and take the OLS estimator as the preliminary estimator. TV uses the exhaustive pairwise penalty (9) with being the same as that in aCARDS and bCARDS. The fused Lasso is based on an order generated from ranking the OLS coefficients. Tuning parameters of all these methods are selected via Bayesian information criteria (BIC).

Performance is evaluated in terms of the average prediction error over an independent test set of size . In addition, to measure how close the estimated grouping structure approaches the true one, we introduce the normalized mutual information (NMI), which is a common measure for similarity between clusterings Fred and Jain (2003). Suppose and are two sets of disjoint clusters of , define

where is the mutual information between and , and is the entropy of . takes values on , and large NMI implies that the two grouping structures are close.

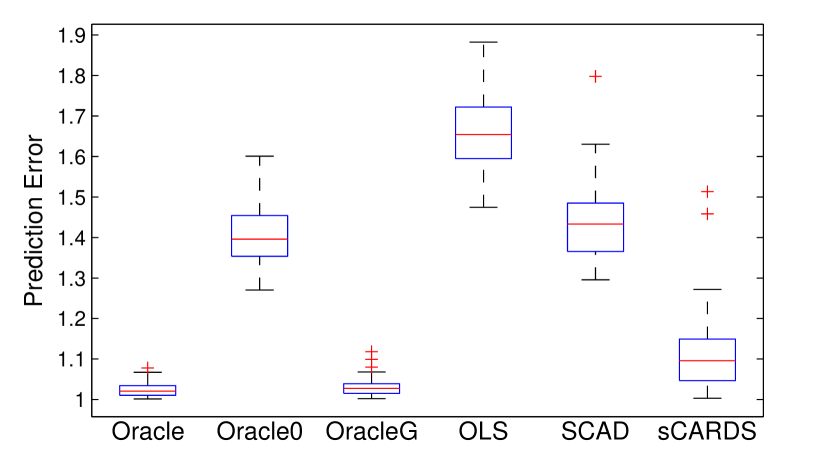

Table 1 shows medians of the average prediction error for six different methods under various values of . Table 2 shows medians of NMI. The boxplots are displayed in Figure 1. We see that except for the case of weak signals (), two versions of CARDS outperform other methods in terms of smaller prediction error and larger NMI. bCARDS is especially good in achieving low prediction errors, even in the case . aCARDS has a better performance in NMI, which shows that it is good in recovering the true grouping structure.

| Oracle | OLS | bCARDS | aCARDS | TV | fLasso | |

|---|---|---|---|---|---|---|

| r=1 | 1.0355 | 1.6112 | 1.0504 | 1.1182 | 1.4847 | 1.4253 |

| r=0.9 | 1.0273 | 1.5885 | 1.0479 | 1.1048 | 1.4608 | 1.4186 |

| r=0.8 | 1.0359 | 1.5947 | 1.0826 | 1.1786 | 1.4777 | 1.4427 |

| r=0.7 | 1.0311 | 1.6038 | 1.1250 | 1.2830 | 1.5591 | 1.4625 |

| r=0.6 | 1.0370 | 1.6054 | 1.3172 | 1.4586 | 1.5795 | 1.4824 |

| r=0.5 | 1.0347 | 1.5826 | 1.3645 | 1.5734 | 1.5734 | 1.4668 |

| Oracle | OLS | bCARDS | aCARDS | TV | fLasso | |

|---|---|---|---|---|---|---|

| r=1 | 1.0000 | 0.5059 | 0.9414 | 0.9784 | 0.7203 | 0.6503 |

| r=0.9 | 1.0000 | 0.5059 | 0.9414 | 0.9784 | 0.7167 | 0.6521 |

| r=0.8 | 1.0000 | 0.5059 | 0.8609 | 0.9355 | 0.7245 | 0.6549 |

| r=0.7 | 1.0000 | 0.5059 | 0.7912 | 0.8989 | 0.6991 | 0.6458 |

| r=0.6 | 1.0000 | 0.5059 | 0.7008 | 0.8763 | 0.6808 | 0.6373 |

| r=0.5 | 1.0000 | 0.5059 | 0.6722 | 0.6741 | 0.6654 | 0.6251 |

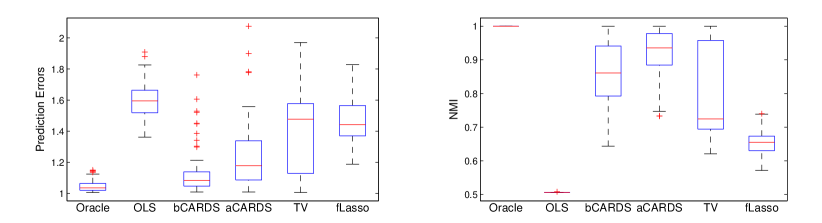

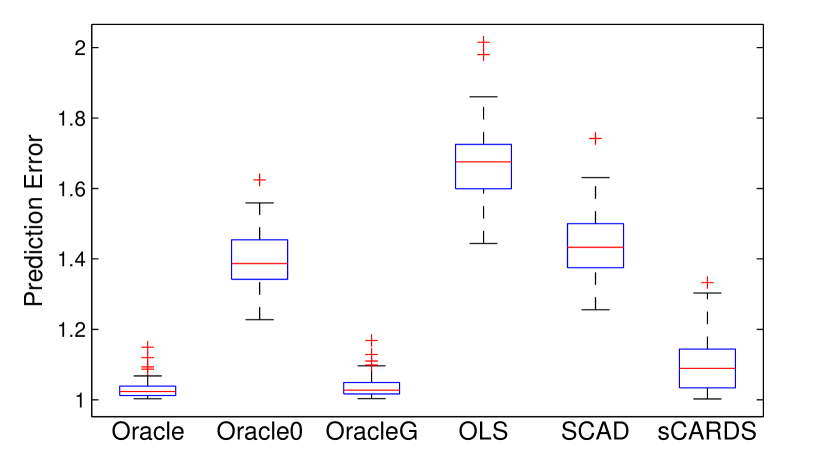

Experiment 2: Consider the linear regression setting with and . Among the 100 predictors, 60 are important ones and their coefficients are the same as those in Experiment 1. Besides, there are 40 unimportant predictors whose coefficients are all equal to .

We implemented sCARDS in this setting and compared its performance to different oracle estimators, Oralce, Oracle0 and OracleG, as well as ordinary least squares (OLS) and the SCAD estimator. The three oracles are defined with different prior information: The Oracle knows both the important predictors and the true groups among them; the Oracle0 only knows which are important predictors; and the OracleG only knows the true groups (it treats all unimportant predictors as one group with unknown coefficients). sCARDS is as described in Section 2; when implementing it, we take the SCAD estimator as the preliminary estimator.

Table 3 shows medians of the average prediction error, number of false positives and normalized mutual information on grouping important predictors. Figure 2 displays the boxplots of average prediction errors under different values of . First, by comparing prediction errors of the three oracles, we see a significant advantage of taking into account both homogeneity and sparsity over pure sparsity. Moreover, the results of Oracle0 and OracleG show that exploring group structure is more important than sparsity. Second, sCARDS achieves a much smaller prediction error than that of OLS and SCAD. Third, compared to the preliminary estimator SCAD, sCARDS can further filter out falsely selected unimportant variables. Fourth, sCARDS successfully recovers the grouping structure on important variables in most cases ( means the estimated groups exactly overlap with the true ones).

| Oracle | Oracle0 | OracleG | OLS | SCAD | sCARDS | ||

| PE | r=1 | 1.0234 | 1.3869 | 1.0273 | 1.6758 | 1.4333 | 1.0895 |

| r=0.7 | 1.0204 | 1.3961 | 1.0274 | 1.6544 | 1.4330 | 1.0960 | |

| FP | r=1 | 0 | 0 | 40 | 40 | 5 | 1 |

| r=0.7 | 0 | 0 | 40 | 40 | 4 | 2.5 | |

| NMI | r=1 | 1.0000 | 0.5059 | 1.0000 | 0.5059 | 0.5059 | 1.0000 |

| r=0.7 | 1.0000 | 0.5059 | 1.0000 | 0.5059 | 0.5059 | 1.0000 | |

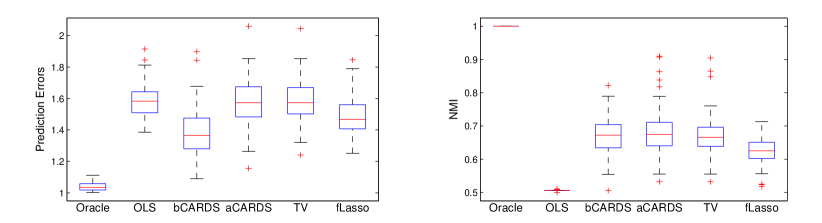

Experiment 3: We consider a special case of the spacial-temporal model, where for , i.e., the predictors are common for all spacial locations. is the total number of locations. Each is a -dimensional vector. In each coordinate , the coefficients are divided into four groups of equal size , with coefficients in the same group sharing a same value. In coordinate , the four true coefficients are ; in coordinate , they are .

We extend aCARDS (bCARDS) to this model: given a preliminary estimator, for each coordinate , extract the data-driven segments (ordering) and build the cross-sectional hybrid (fused) penalty , then sum them up to build the penalty term, and finally solve a penalized maximum likelihood:

We still call the method aCARDS (bCARDS). The Oracle is the maximum likelihood estimator knowing the true groups in each coordinate. We aim to compare the performance of Oracle, OLS and aCARDS.

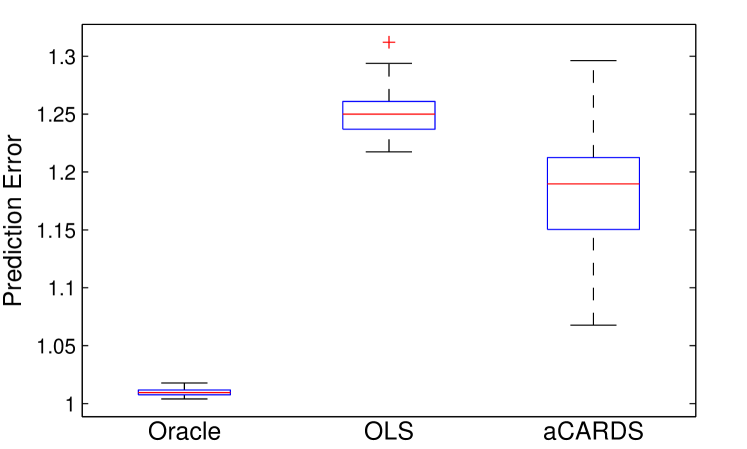

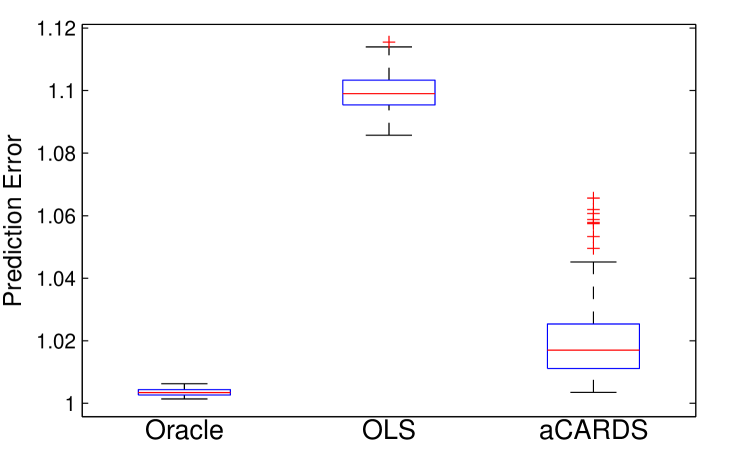

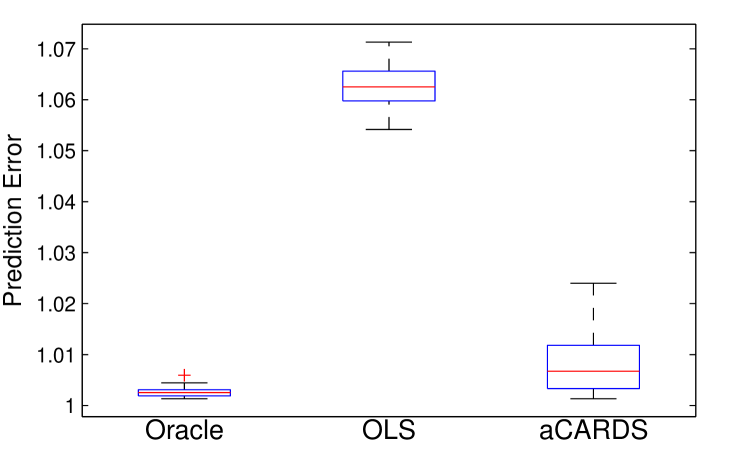

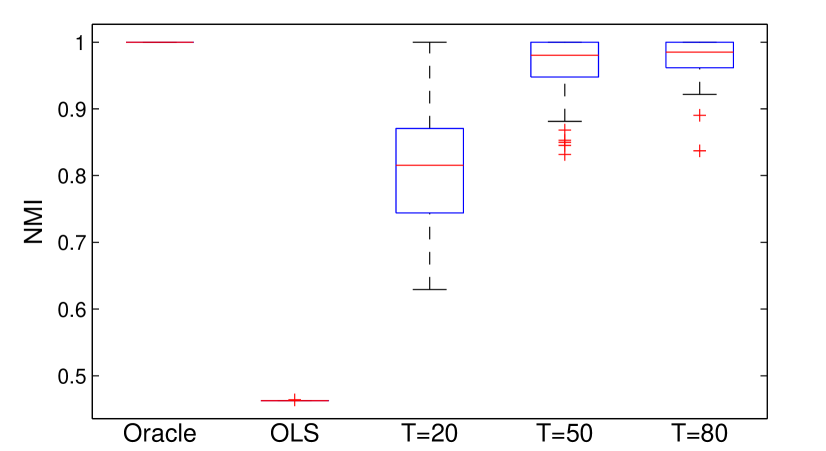

Table 4 shows medians of the average prediction error and normalized mutual information(averaged over coordinates). Instead of varying the signal-to-noise ratio directly, we equivalently change , the total number of time points. Figure 3 contains the boxplots. We see that aCARDS achieves significantly lower prediction errors in all cases. Moreover, aCARDS estimates well the true grouping structure; in particular, when , in most repetitions.

| Prediction Error | NMI | |||||

|---|---|---|---|---|---|---|

| Oracle | OLS | aCARDS | Oracle | OLS | aCARDS | |

| T=20 | 1.0095 | 1.2501 | 1.1898 | 1.0000 | 0.4628 | 0.8154 |

| T=50 | 1.0034 | 1.0990 | 1.0170 | 1.0000 | 0.4628 | 0.9803 |

| T=80 | 1.0025 | 1.0625 | 1.0067 | 1.0000 | 0.4628 | 0.9851 |

6 Real data analysis

6.1 S&P500 returns

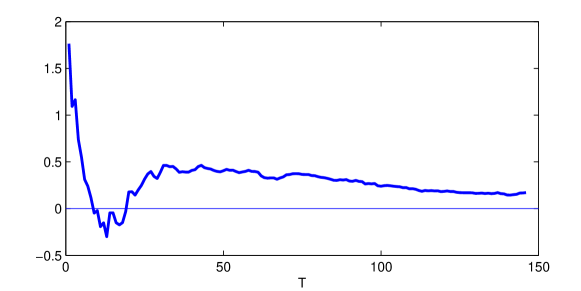

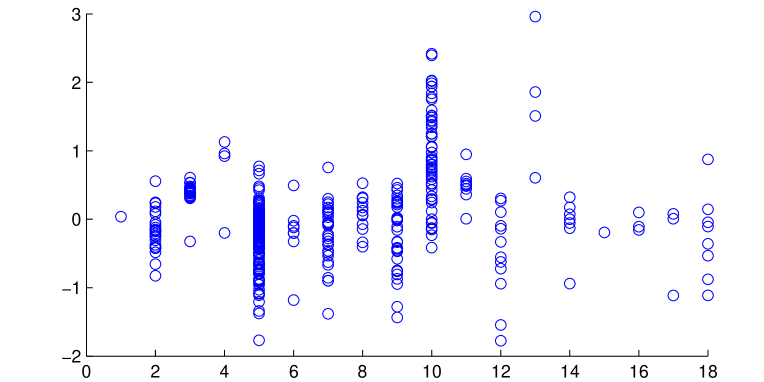

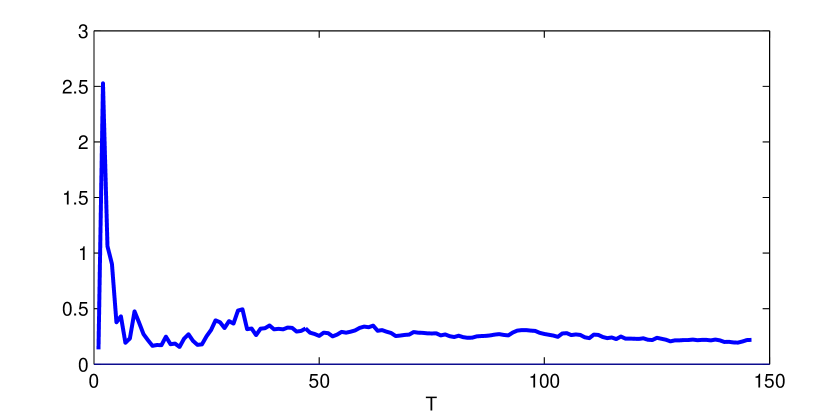

In this study, we fit a homogeneous Fama-French model for stock returns: , where contains three Fama-French factors at time and is the excess return of stocks. We collected daily returns of stocks, which were in the components of the S&P500 index in the period December 1, 2010 to December 1, 2011 (). We applied bCARDS as in Experiment 3, except that the intercepts ’s were also penalized. The tuning parameters were chosen via generalized cross validation (GCV). Table 5 shows the number of fitted coefficient groups on three factors and the number of non-zero intercepts. We then used the daily returns of those stocks in the period December 1, 2011 to July 2, 2012 () to evaluate the estimation error. Let and be the fitted and observed excess returns of stock at time , respectively. Define the cumulative sum of squared estimation errors at time as , where is a chosen constant between and . Here we take . Figure 4 shows the percentage improvement in of the CARDS estimator over the OLS estimator. We see that CARDS achieves a smaller cumulative sum of squared estimation errors compared to OLS at most time points, especially in the “very-close” and “far-away” future. The North American Industry Classification System (NAICS) classifies these 410 companies into different industry sectors. Figure 5(a) shows the OLS coefficients on the “book-to-market ratio” factor. We can see that stocks belonging to Sector 2 “Utilities” (29 stocks in total) have very close OLS coefficients, and 17 stocks in this sector were clustered into one group in CARDS estimator. Figure 5 (b) shows the percentage improvement in only for stocks in this sector, where the improvement is more significant.

| Fama-French factors | No. of coef. groups |

|---|---|

| “market return” | 41 |

| “market capitalization” | 32 |

| “book-to-market ratio” | 56 |

| intercept | 60 |

6.2 Polyadenylation signals

The proposed method can be easily extended to more general settings such as generalized linear models although we have focused on the linear regression setting so far. In this subsection, we will apply the proposed method to a logistic regression example. This study tried to predict polyadenylation signals (PASes) in human DNA and mRNA sequences by analyzing features around them. The data set was first used in Legendre and Gautheret (2003) and later analyzed by Liu et al. (2003), and it is available at http://datam.i2r.a-star.edu.sg/datasets/krbd/SequenceData/Polya.html. There is one training data set and five testing data sets. To avoid any platform bias, we use the training data set only. It has 4418 observations each with 170 predictors and a binary response. The binary response indicates whether a terminal sequence is classified as a “strong” or “weak” polyA site, and the predictors are features from the upstream (USE) and downstream (DSE) sequence elements. We randomly select 2000 observations to perform model estimation and use the rest to evaluate performance. Our numerical analysis consists the following steps. Step 1 is to apply the lasso penalized logistic regression to these 2000 observations with all 170 predictors and to use AIC to select an appropriate regularization parameter. In step 2, we use the logistic regression coefficients obtained in step 1 as our preliminary estimate and apply CARDS accordingly. Average prediction error (and standard error in parentheses) over 40 random splitting are reported in Table 6. We also report the average number of non-zero coefficient groups and the average number of selected features. It shows that two versions of CARDS lead to a smaller prediction error when compared with the total variation penalty. In addition, the aCARDS has fewer groups of non-zero coefficients but more selected features.

| aCARDS | bCARDS | TV | |

|---|---|---|---|

| Prediction Error | 0.2449 (.0015) | 0.2485 (.0014) | 0.2757 (.0026) |

| No. of non-zero coef. groups | 5.5000 | 21.6250 | 5.7500 |

| No. of selected features | 73.2750 | 21.6250 | 40.3500 |

7 Conclusion

In this paper, we explored homogeneity of coefficients in high-dimensional regression. We proposed a new method called clustering algorithm in regression via data-driven segmentation (CARDS) to estimate regression coefficients and to detect homogeneous groups. The implementation of CARDS does not need any geographical information (neighborhoods, distance, graphs, etc.) as a priori, which differs it from other methods in similar settings and makes it more general to applications. A modification of CARDS, sCARDS, can be used to explore homogeneity and sparsity simultaneously. Our theoretical results show that by exploring homogeneity better estimation accuracy can be achieved. In particular, when the number of homogeneous groups is small, the power of exploring homogeneity and sparsity simuntaneously is much larger than that of exploring sparsity only, which is justified in our simulation studies.

To promote homogeneity, the CARDS uses a preliminary estimate to construct data-driven penalties. This so-called “hybrid pairwise penalty” is built through a preliminary ranking and a parameter for segmentation. Such idea of taking advantage of a preliminary estimate can be generalized. For example, we may apply clustering methods to these preliminary coefficients, such as -mean algorithm or hierarchical clustering algorithm, to help construct penalties and further promote homogeneity.

This paper only considers the case where predictors in one homogeneous group have equal coefficients. In a more general situation, coefficients of predictors in the same group are close but not exactly equal. The idea of data-driven pairwise penalties still applies, but instead of using the class of folded concave penalty functions, we may need to use penalty functions which are smooth at the origin, e.g., the penalty function. Another possible approach is to use posterior-type estimators combined with, say, a Gaussian prior on the coefficients. These are beyond the scope of this paper and we leave them as future work.

8 Proofs

8.1 Proof of Theorem 3.1

Introduce the mapping , where is the -dimensional vector whose -th coordinate equals to the common value of for . Note that is a bijection and is well-defined for any . Also, introduce the mapping , where . We see that on , and is the orthogonal projection from to . Denote and .

Denote and , so that we can write . For any , let

and define . Note that when preserves the order of , there exist such that for . Then and for any and .

In the first part of the proof, we show . By definition and direct calculations,

Therefore, we can write

From Condition 3.1, and . By the Markov inequality, for any ,

Combining the above, we have shown that with probability at least , . This proves .

Furthermore, we can write , where and is the unit vector with on the -th coordinate and elsewhere. Note that . It follows from Condition 3.3 and the union bound that

| (29) |

Since , we have

| (30) |

In the second part of the proof, we show that is a strictly local minimum of with probability at least . By assumption, there is an event such that and over the event , preserves the order of . Consider the neighborhood of :

By (30), there is an event such that and over the event , . Hence, over the event . For any , write as its orthogonal projection to . We aim to show

-

(a)

Over the event ,

(31) and the inequality is strict whenever .

-

(b)

There is an event such that . Over the event , there exists , a neighborhood of , such that

(32) and the inequality is strict whenever .

Combining (a) and (b), for any , a neighborhood of , and the inequality is strict whenever . This proves that is a strictly local minimum of over the event , and the claim follows immediately. Below we show (a) and (b).

Consider (a) first. We claim

| (33) |

To see this, for a given , write . It suffices to check for . Note that . Since , it is easy to see that .

Using (33), we see that , for all . By definition and the fact that is positive definite, is the unique global minimum of . As a result, , and the inequality is strict for any . Note that and is the orthogonal projection from to . Combining the above, for any ,

and the inequality is strict whenever , i.e., . This proves (31).

Second, consider (b). For a positive sequence to be determined, let

Since is the orthogonal projection of to , for any . In particular, . As a result, to show (32), it suffices to show

| (34) |

and the inequality is strict whenever .

To show (34), write so that . By Taylor expansion,

where is in the line between and . Consider first. Direct calculations yield

where and . Plugging it into and rearranging the sum, we obtain

| (35) |

Note that when and belong to the same group, , and hence the sign of is the same as the sign of if neither of them is . In addition, recall that for all , for some indices . Combining the above, we can rewrite

First, since and is the orthogonal projection of to , . Hence, implies . By repeating the proof of (33), we can show for . So the second term in disappears. Second, in the first term of , since , it follows by concavity that . Together, we have

| (36) |

Next, we simplify . Denote and write . For any fixed and such that and , let and . Regarding that for , we can reexpress as

| (37) | |||||

where for any vector ,

We aim to bound . Denote , and write . First, is a linear function of . Second, since lies between and , we have . It follows that . Moreover, for all . Combining the above yields

| (38) | |||||

First, we bound the term . Let be the event that

| (39) |

where we recall is the maximum eigenvalue of restricted to the -block. Given , we can express as

Write and , so that . It is observed that . Using the fact that for any real values , we have . Applying Condition 3.3 and the probability union bound,

| (40) | |||||

Second, we bound the term . Observing that for any vector , , where is the mean of , we have

Since and , we have . As a result,

| (41) |

8.2 Proof of Theorem 3.2

First, we show that the LLA algorithm yields after one iteration. Let be the event that preserves the order of , the event that and the event that (39) holds. We have shown that . It suffices to show that over the event , the LLA algorithm gives after the first iteration.

Let . At the first iteration, the algorithm minimizes

This is a convex function, hence it suffices to show that is a strictly local minimum of . Using the same notations as in the proof of Theorem 3.1, for any , write as its orthogonal projection to . Let , and for a sequence to be determined, consider the neighborhood of defined by . It suffices to show

| (43) |

and the first inequality is strict whenever , and the second inequality is also strict whenever .

We first show the second inequality in (43). For and in different groups, ; also, . Hence, , and it follows that . On the other hand, for and in the same group, whenever . Consequently,

We have seen in the proof of Theorem 3.1 that is the unique global minimum of constrained on . So the second inequality in (43) holds.

Next, consider the first inequality in (43). By applying Talylor expansion and rearranging terms, for some that lies in the line between and ,

We first simplify . Note that when and are in different groups. When and are in the same , first, , and has the same sign as ; second, , and hence . Combining the above yields

| (44) |

Next, we simplify . Denote . Similarly to (37)-(42), we find that

where over the event , for any ,

By the choice of , the sum of the first two terms is upper bounded by for large ; in addition, we choose . It follows that

| (45) |

Combining (44) and (45), over the event ,

This proves the first inequality in (43).

Second, we show that over the event , at the second iteration, the LLA algorithm still yields and therefore it converges to . We have shown that after the first iteration, the algorithm outputs . It then treats as the initial solution for the second iteration. So it suffices to check

This is true because over the event , . ∎

8.3 Proof of Theorem 3.3

Since is consistent with , there exists such that for all . We shall write without loss of generality.

In the first part of the proof, we show that , and it satisfies the sign restrictions , .

When , is strictly convex. So is the unique global minimum if and only if it satisfies the first-order conditions:

where when , when , and any value in when . Therefore, it suffices to show there exists that satisfy the sign restrictions and the first-order conditions simultaneously.

For , we write and , where the mapping is the same as that in the proof of Theorem 3.1. The sign restrictions now become for all . Note that when predictors and belong to the same group in . The first-order conditions can be re-expressed as

| (46) |

where ’s take any values on and we set by default. Denote by when and when ; similarly, for . In (46), we first remove ’s by summing up the equations corresponding to indices in each . Using the fact that , we obtain

Under the sign restrictions , , it becomes a pure linear equation of :

where is the -dimensional vector with , as defined in Section 3.2. It follows immediately that

| (47) |

Second, given , (46) can be viewed as equations of ’s and we can solve them directly. Denote . For each , define and . The solutions of (46) are

Here the two expressions of are equivalent because from (46). It follows that any convex combination of the two expressions is also an equivalent expression of . Taking the combination coefficients as and , and plugging in the sign restrictions , , we obtain

where the function is defined as in (37). Here ’s still depend on through . Combining (47) to the definition of gives

where and is defined as in Section 3.2. By plugging in the expression of , we can remove the dependence on of the solutions of ’s:

| (48) |

Now, to show the the existence of that satisfies both the sign restrictions and first-order conditions, it suffices to show with probability at least ,

Consider (a) first. In (48), under the “irrepresentability” condition, the sum of the last two terms is bounded by in magnitude. To deal with the first term, recall that in deriving (39), we write . It follows immediately that . Since , similarly to (39), we obtain

except for a probability at most . Therefore, by the choice of , the absolute value of the first term is much smaller than . So except for a probability at most , i.e., (a) holds.

Next, consider (b). Since , it suffices to show that . Note that (47) can be rewritten as

It follows from Condition 3.1 that . First, note that . Second, from (30), , except a probability of at most . Moreover, . These together imply

From the conditions on , the right hand side is much smaller than . It follows that . This proves (b).

8.4 Proof of Theorem 3.4

The order generated by preserves the order of , if and only if, implies for any pair . Note that when , necessarily . Moreover, . So it suffices to show that with probability at least .

From direct calculations, . Let , . Then . Note that . By Condition 3.3 and applying the union bound,

So, with probability at least , . This completes the proof. ∎

8.5 Proof of Proposition 4.1

Consider the first claim. Given , let and . Then . Moreover, for any ,

where the first and last inequalities are because and , and the inequalities between come from Definition 2.3. It follows that for all . This means , and hence .

Consider the second claim. Given , let and , and so . For any and ,

where the first inequality comes from Definition 2.3, the second inequality is because and the last inequality is from the labelling of groups and the fact that . It follows that . Similarly, for any , . As a result, and . ∎

8.6 Proof of Theorem 4.1

Recall the mappings , and defined in the proof of Theorem 3.1. Write , where and . For any , let

and define .

We only need to show that is a strictly local minimum of with probability at least . Let be the event that preserves the order of , and define the event and the set the same as in the proof of Theorem 3.1. For an event to be defined such that , we shall show that (31) and (32) hold on the event . The claim then follows immediately. Similar to the proof of Theorem 3.1, it suffices to show (33) and (34).

Consider (33) first. Recall that . Define and , for . Write for short and . It follows that

Therefore, it suffices to check . Note that the left hand side is lower bounded by , which proves (33).

Next, consider (34). For , write , . By Taylor expansion,

where is in the line between and . Let , . By rearranging terms in , we can write

For those not belonging the same true group, . Similarly as before, we obtain . On the other hand, for those belonging to the same true group, and hence . Together, we find that

| (49) | |||||

where means and are in the same true group, and the last inequality comes from the concavity of and the fact that .

Now, we simplify . Let and write . Note that for each , , where , and are as in Proposition 4.1.

Using notations in Proposition 4.1, . Therefore,

| (50) | |||||

where for . To simplify , note that given any such that and , for some and , we have

Plugging this into the expression , we obtain

where for such that , and ,

and is the average of . By rearranging terms, . Therefore,

| (51) | |||||

where

Let and . Then for any such that , and , we have the following expression

| (52) | |||||

Combining (49), (50) and (51) gives

Therefore, to show (34), we only need to show for sufficiently small ,

| (53) |

Note that , where and . It is seen that . So , where the remainder term is uniformly bounded by with . Similar situations are observed for . As a result, to show (53), it suffices to show

| (54) |

and

| (55) |

First, consider (54). Let be the event

Note that , where . Moreover, the number of such pairs is bounded by . Applying Condition 3.3 and the union bound, we see that . Moreover, , where is the average of . Note that and because is the orthogonal projection of onto . Noticing that , we obtain

Combing the above results to the choice of yields , and (54) follows.

Next, consider (55). In (52), the first term can be written as , where has a similar form to that of in (37). Let be the event that

| (56) |

It is easy to see that we can follow the steps of proving (39) and (41) to show . Write the second term in (52) as . First, let be the event that

| (57) |

We observe that , where

So , where and . Similar to (40), we can show . Second, note that , where . As a result,

| (58) |

Let , where . Combining (56)-(58) gives

over the event . By choice of , the right hand side is much smaller than . This proves (55). ∎

8.7 Proof of Theorem 4.2

Write and . Let be as in the proof of Theorem 4.1. Denote

be a neighbourhood of . We have seen: (i) with probability tending to ; (ii) for ; (iii) is a strictly local minimum of in . Combining the above, we find that

It follows from that

Therefore, to show the claim, it suffices to show , i.e., for any ,

| (59) |

Let , and write the left hand side of (59) as . The ’s are independently distributed with and . Let . By Lindeberg’s central limit theorem, if for any ,

| (60) |

then . Since , (59) follows immediately from the Slutsky’s lemma.

It remains to show (60). Using the formula for , we have

From Condition 3.3, and . Note that for any and positive integer . It follows that

where in the last inequality we have used the facts that and . Note that . ∎

8.8 Proof of Corollary 4.1

It is easy to see that the asymptotic variance of is . To compute the asymptotic variance of , note that

where . Applying Theorem 4.2, the asymptotic variance is

Since , the above quantity is equal to .

Next, we show . There exists an orthogonal matrix such that is equal to the first columns of . Write and . Direct calculations yield and , where is the subvector of formed by its first elements and is the upper left block of . From basic algebra, . ∎

8.9 Proof of Theorem 4.3

It suffices to show that is a strictly local minimum of with probability at least . First, there exists an event such that and preserves the order of over the event . Second, for a sufficiently large constant , define as the set of all such that . By recalling the proof of Theorem 3.1, we see that there exists an event such that and over the event . Third, for any , let be the vector such that , where is the support of ; and let be the orthogonal projection of onto . We aim to show there exists an event such that and over the event :

| (61) |

and the inequality is strict whenever ; for a positive sequence ,

| (62) |

and the inequality is strict whenever ; for a positive sequence ,

| (63) |

and the inequality is strict whenever .

Suppose (61)-(63) hold. Consider the neighborhood of defined as . It is easy to see that and for any . As a result, for , and the inequality is strict except that . It follows that is a strictly local minimum of .

Now, we show (61)-(63). The proofs of (61) and (62) are exactly the same as those of (31) and (32), by noting that for any whose support is contained in . To show (63), write

where lies in the line between and . First, note that for . Second, . Hence, for , . By the concavity of , . Third, write , where and . Combining the above,

where satisfying . First, from Condition 3.1, , except for a probability of . Since , when is sufficiently large, . Second, since , we can always choose sufficiently small so that for any . Combining the above gives

Then (63) follows immediately. The proof is now complete. ∎

References

- Bondell and Reich (2008) H. D. Bondell and B. J. Reich. Simultaneous regression shrinkage, variable selection, and supervised clustering of predictors with oscar. Biometrics, 64:115–123, 2008.

- Darling and Erdos (1956) D.A. Darling and P. Erdos. A limit theorem for the maximum of normalized sums of independence random variables. Duke Math. J., 23:143–155, 1956.

- Fan and Li (2001) J. Fan and R. Li. Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of American Statistical Association, 96:1348–1360, 2001.

- Fan and Lv (2008) J. Fan and J. Lv. Sure independence screening for ultra-high dimensional feature space. Journal of Royal Statistical Society B, 70:849–911, 2008.

- Fan and Lv (2011) J. Fan and J. Lv. Non-concave penalized likelihood with np-dimensionality. IEEE – Information Theory, 57:5467–5484, 2011.

- Fan et al. (2011) J. Fan, J. Lv, and L. Qi. Sparse high-dimensional models in economics. Annual Review of Economics, 3:291–317, 2011.

- Fan et al. (2012) J. Fan, L. Xue, and H. Zou. Strong oracle optimality of folded concave penalized estimation. Manuscript, 2012.

- Fred and Jain (2003) A. Fred and A. K. Jain. Robust data clustering. Proceedings of IEEE Computer Society Conference on Computer Vision and Pattern Recognition, 3:128–136, 2003.

- Friedman et al. (2007) J. Friedman, T. Hastie, H. H fling, and R. Tibshirani. Pathways coordinate optimization. Ann. Appl. Stat., 1:302–332, 2007.

- Legendre and Gautheret (2003) M. Legendre and D. Gautheret. Sequence determinants in human polyadenylation site selection. BMC genomics, 4, 2003.

- Liu et al. (2003) H. Liu, H. Han, J. Li, and L. Wong. An in-silico method for prediction of polyadenylation signals in human sequences. Genome Inform Ser Workshop Genome Inform, 14:84–93, 2003.

- Shen and Huang (2010) X. Shen and H.-C. Huang. Grouping pursuit through a regularization solution surface. J. Amer. Statist. Assoc., 105(490):727–739, 2010.

- Tibshirani et al. (2005) S. Tibshirani, M. Saunders, S. Rosset, J. Zhu, and K. Knight. Sparsity and smoothness via the fused lasso. J. Roy. Statist. Soc. B, 67:91–108, 2005.

- Zou and Li (2008) H. Zou and R. Li. One-step sparse estimates in nonconcave penalized likelihood models (with discussion). Ann. Statist., 36:1509–1566, 2008.