Online Convex Optimization Against Adversaries with Memory and Application to Statistical Arbitrage

Abstract

The framework of online learning with memory naturally captures learning problems with temporal constraints, and was previously studied for the experts setting. In this work we extend the notion of learning with memory to the general Online Convex Optimization (OCO) framework, and present two algorithms that attain low regret. The first algorithm applies to Lipschitz continuous loss functions, obtaining optimal regret bounds for both convex and strongly convex losses. The second algorithm attains the optimal regret bounds and applies more broadly to convex losses without requiring Lipschitz continuity, yet is more complicated to implement. We complement our theoretic results with an application to statistical arbitrage in finance: we devise algorithms for constructing mean-reverting portfolios.

1 Introduction

One of the most well-studied frameworks of online learning is Online Convex Optimization (OCO). In this framework, an online player iteratively chooses a decision in a convex set, then a convex loss function is revealed, and the player suffers loss that is the convex function applied to the decision she chose. It is usually assumed that the set of loss functions is chosen arbitrarily, possibly by an all-powerful adversary. The performance of the online player is measured using the regret criterion, which compares the accumulated loss of the player with the accumulated loss of the best fixed decision in hindsight.

This notion of regret captures only memoryless adversaries who determine the loss based on the player’s current decision, and fails to cope with bounded-memory adversaries who determine the loss based on the player’s current and previous decisions. However, in many scenarios such as coding, compression, portfolio selection and more, the adversary is not completely memoryless and the previous decisions of the player affect her current loss. We are particularly concerned with scenarios in which the memory is relatively short-term and simple, in contrast to state-action models for which reinforcement learning models are more suitable [Put09].

An important aspect of our work is that the memory is not used to relax the adaptiveness of the adversary (cf. [ADT12, CBDS13]), but rather to model the feedback received by the player. In particular, throughout this work we assume a counterfactual feedback model: the player is aware of the loss she would suffer had she played any sequence of decisions in the previous time points. In addition, we assume that the adversary is oblivious, that is, the adversary must determine the whole set of loss functions in advance. This model is quite common in the online learning literature [MOSW02, MOSW06, GN11], yet was studied only for the experts problem.

Our goal in this work is to extend the notion of learning with memory to one of the most general online learning frameworks - the OCO. To this end, we adapt the policy regret111The policy regret compares the performance of the online player with the best fixed sequence of actions in hindsight, and thus captures the notion of adversaries with memory. A formal definition appears in Section 2. criterion of [ADT12], and propose two different approaches for the extended framework, both attain the optimal bounds with respect to this criterion.

We demonstrate the effectiveness of the proposed framework in the extensively studied problem of constructing mean-reverting portfolios. Specifically, we cast this problem as an OCO problem with memory in which the loss functions are proxies for mean reversion, and the decisions of the player are wealth distributions over assets. The main novelty we present is the ability to maintain the wealth distributions online, in contrast to traditional approaches that determine the wealth distribution only at the end of the training period. The experimental results support the superiority of our algorithm with respect to the state-of-the-art.

1.1 Summary of Results

| Framework | Previous bound | Our first approach | Our second approach |

|---|---|---|---|

| Experts | Not applicable | ||

| with Memory | |||

| OCO with memory | |||

| (convex losses) | |||

| OCO with Memory | |||

| (strongly convex losses) |

We present and analyze two algorithms for the framework of OCO with memory, both attain policy regret bounds that are optimal in the number of iterations. Our first algorithm utilizes the Lipschitz property of the loss functions, and — to the best of our knowledge — is the first algorithm for this framework that is not based on any blocking technique (this technique is detailed in the related work section below). This algorithm attains -policy regret for generally convex loss functions and -policy regret for strongly convex loss functions.

For the case of convex and non-Lipschitz loss functions, our second algorithm attains the nearly optimal -policy regret; its downside is that it is randomized and more difficult to implement. A novel result that follows immediately from our analysis is that our second algorithm attains an expected -regret222The notation is a variant of the notation that ignores logarithmic factors., along with decision switches in the standard OCO framework. Similar result currently exists only for the special case of the experts problem [GVW10].

2 Preliminaries and Model

We continue to formally define the notations for both the standard OCO framework and the framework of OCO with memory. For sake of readability, we shall use the notations for memoryless loss functions (that correspond to memoryless adversaries), and for loss functions with memory (that correspond to bounded-memory adversaries).

2.1 The Standard OCO Framework

In the standard OCO framework, an online player iteratively chooses a decision , and suffers loss that equals to . The decision set is assumed to be a bounded convex subset of , and the loss functions are assumed to be convex functions from to . In addition, the set is assumed to be chosen in advance, possibly by an all-powerful adversary that has full knowledge of our learning algorithm (see for instance [CBL06]). The performance of the player is measured using the regret criterion, defined as follows:

where is a predefined integer denoting the total number of iterations played. The goal in this framework is to design efficient algorithms, whose regret grows sublinearly in , corresponding to an average per-round regret going to zero as increases.

2.2 The Framework of OCO with Memory

In this work we consider the framework of OCO with memory, detailed as follows: at each time point , the online player chooses a decision . Then, a loss function is revealed, and the player suffers loss that equals to . For simplicity of analysis we assume that , and that for any . Notice that the loss at time point depends on the previous decisions of the player, as well as on his current one. We assume that after is revealed, the player is aware of the loss she would suffer had she played any sequence of decisions (this correspond to the counterfactual feedback model mentioned earlier).

Our goal in this framework is to minimize the policy regret, as defined in [ADT12]333The iterations in which are ignored since we assume that the loss per iteration is bounded by a constant; this adds at most a constant to the final regret bound.:

We define the notion of convexity for the loss functions as follows: we say that is a convex loss function with memory if is convex in . Throughout this work we assume that are convex loss functions with memory. This assumption can be shown to be necessary in some cases, if efficient algorithms are considered; otherwise, the optimization problem might be unsolvable efficiently.

3 Policy Regret for Lipschitz Continuous Loss Functions

In this section we assume that the loss functions are Lipschitz continuous for some Lipschitz constant , that is

and adapt the well-known Regularized Follow The Leader (RFTL) algorithm to cope with bounded-memory adversaries. We present here only the algorithm and the main theorem, and defer the complete analysis to Appendix A.

Intuitively, Algorithm 1 relies on the fact that the corresponding functions are memoryless and convex. Thus, standard regret minimization techniques are applicable, yielding a regret bound of for . This however, is not the policy regret bound we are interested in, but is in fact quite close if we use the Lipschitz property of and set the learning parameter properly.

For Algorithm 1 we can prove the following:

4 Policy Regret with Low Switches

In this section we present a different approach to the framework of OCO with memory — low switches. This approach was considered before in [GN11], who adapted the Shrinking Dartboard (SD) algorithm of [GVW10] to cope with limited-delay coding. However, in [GVW10, GN11] consider only the experts setting, in which the decision set is the simplex and the loss functions are linear. Here we adapt this approach to general decision sets and generally convex loss functions, and obtain optimal policy regret against bounded-memory adversaries. We present here only the algorithm and main theorem, and defer the complete analysis to Appendix B.

Intuitively, Algorithm 2 defines a probability distribution over at each time point . By sampling from this probability distribution one can generate an online sequence that has an expected low regret guarantee. This however is not sufficient in order to cope with bounded-memory adversaries, and thus an additional element of choosing with high probability is necessary (line 6). Our analysis shows that if this probability equals to the regret guarantee remains, and we get an additional low switches guarantee.

For Algorithm 2 we can prove the following:

Theorem 4.1.

Let be convex functions from to , such that and , and define for some . Then, Algorithm 2 generates an online sequence , for which it holds that

and in addition

where denotes the number of decision switches in the sequence .

Setting yields , and .

5 Application to Statistical Arbitrage

Our application is motivated by financial models that are aimed at creating statistical arbitrage opportunities. In the literature, “statistical arbitrage” refers to statistical mispricing of one or more assets based on their expected value. One of the most common trading strategies, known as “pairs trading”, seeks to create a mean reverting portfolio using two assets with same sectoral belonging (typically using both long and short sales). Then, by buying this portfolio below its mean and selling it above, one can have an expected positive profit with low risk.

Here we extend the traditional pairs trading strategy, and present an approach that aims at constructing a mean reverting portfolio from an arbitrary (yet known in advance) number of assets. Roughly speaking, our goal is to synthetically create a mean reverting portfolio by maintaining weights upon different assets. The main problem arises in this context is how do we quantify the amount of mean reversion of a given portfolio? Indeed, mean reversion is somewhat an ill-defined concept, and thus different proxies are usually defined to capture its notion. We refer the reader to [Sch11, D’A11], in which few of these proxies (such as predictability and zero-crossing) are presented.

In this work, we consider a proxy that is aimed at preserving the mean price of the constructed portfolio (over the last trading periods) close to zero, while maximizing its variance. We note that due to the very nature of the problem: weights of one trading period affect future performance, the memory comes unavoidably into the picture.

We proceed to formally define the new mean reversion proxy and the use of our new memory-learning algorithm in this model. Denote by the prices of assets at time , and by a distribution of weights over these assets. Since short selling is allowed, the norm of can sum up to an arbitrary number, determined by the loan flexibility. Without loss of generality we assume that , and define:

| (1) |

for some . Notice that minimizing iteratively yields a process such that its mean is close to zero (due to the expression on the left), and its variance is maximized (due to the expression on the right). We use the regret criterion to measure our performance against the best distribution of weights in hindsight, and wish to generate a series of weights such that the regret is sublinear. Thus, define the memoryless loss function and denote

Notice we can write . Since is not convex in general, our techniques are not straightforwardly applicable here. However, the hidden convexity of the problem allows us to bypass this issue by a simple and tight Positive Semi-Definite (PSD) relaxation. Define

| (2) |

where is a PSD matrix with , and is defined as . Now, notice that the problem of minimizing is a PSD relaxation to the minimization problem , and for the optimal solution it holds that:

where . Also, we can recover a vector from the PSD matrix using an eigenvector decomposition as follows: represent , where each is a unit vector and are non-negative coefficients such that . Then, by sampling the eigenvector with probability , we get that . Technically, this decomposition is possible due to the fact that is a PSD matrix with . Notice that is linear in , and thus we can apply regret minimization techniques on the loss functions . This procedure is formally given in Algorithm 3 below.

For Algorithm 3 we can prove the following:

Corollary 5.1.

The main novelty of our approach to the task of constructing mean reverting portfolios is the ability to maintain the weight distributions online. This is in contrast to the traditional offline approaches that require a training period (to learn a weight distribution), and a trading period (to apply a corresponding trading strategy).

6 Experimental Results

In this section we present some preliminary results that demonstrate the effectiveness of the proposed algorithm to the task of creating statistical arbitrage opportunities under the pairs trading setting. In this setting, we are given two assets with the same sectoral belonging and our goal is to construct a mean reverting portfolio by maintaining weights upon these assets. To simplify the setting we ignore transaction costs (both for our algorithm and the benchmarks).

In order to isolate the problem of constructing a mean reverting portfolio (which is of our interest) from the problem of designing a trading strategy, the experiments are executed in two stages: first, a mean reverting portfolio is constructed by each of the considered approaches (which are described below in Section 6.1). Then, the same trading strategy is applied to all resulted portfolios, so that the different approaches are comparable in terms of return.

Our dataset contains time series of daily closing rates of 10 pairs of assets based on their common sectoral belonging (e.g., Coca Cola and Pepsi, AT&T and Verizon, etc.). We use data between 01/01/2008 and 01/02/2013, which is divided into training set (75% of the data, from 01/01/2008 to 01/10/2011) and test set (25% of the data, from 02/10/2011 to 01/02/2013).

6.1 Baselines

In order to capture the essence of our Online Statistical Arbitrage (OSA) algorithm with respect to its offline counterparts, we choose some of the fundamental offline approaches444We refer the reader to [MK98, Joh91] for more comprehensive information about OLS and Johansen. to serve as benchmarks:

-

Orthogonal Least Squares (OLS) this baseline proposes to choose the eigenvector that corresponds to smallest eigenvalue of the empirical covariance matrix of . This matrix is denoted by , and formally defined as follows:

where denotes the number of days in the training set.

-

Johansen Vector Error Correction Model this baseline relies on co-integration techniques. Basically, co-integration is a statistical relationship where two time series (e.g., stock prices) that are both integrated of same order can be linearly combined to produce a single time series which is integrated of order , where . In its application to pairs trading, the co-integration technique seeks to find a linear combination such that , which roughly results in a mean reverting combined asset.

-

The offline optimum (Offline) this baselines refers to the best distribution of weights in hindsight with respect to our proxy, that is

Here, denotes the number of days in the test set. Clearly, the performance of this baselines cannot be obtained in practice, as it relies on the future prices of the considered assets when constructing the portfolio. Nevertheless, this baseline has a crucial role in understanding the effectiveness of the proposed mean reversion proxy.

For the OLS and Johansen baselines we use the training period to generate a weight distribution , and then construct the portfolio . For OSA we run Algorithm 3 on the training set to get the sequence . Then, we use as a warm start for a new run of Algorithm 3 on the test data to generate the portfolio (which will be used for the benchmark task).

6.2 Trading Strategy

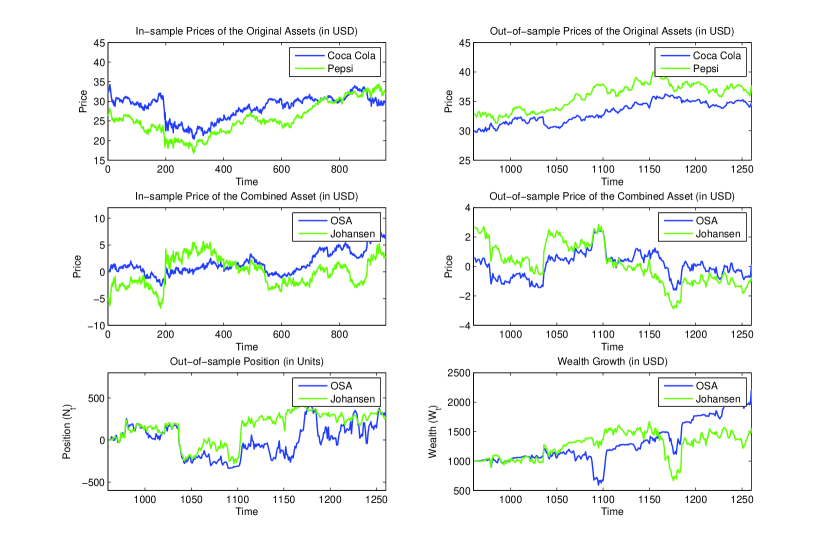

In order to compare the different approaches, we apply the trading strategy of [JY07] to each of the resulting portfolios. Basically, [JY07] propose to take a position in the asset proportionally to , where denotes the wealth at time and is assumed to be an auto regressive process of order 1 with mean that complies with (and ). Essentially, this strategy takes a long position whenever the asset is below its mean and short position whenever it is above, while taking into account the autoregressive model parameters and . In practice, these parameters are estimated on the training set and then used to generate . A sample experiment for the pair Coca Cola and Pepsi (using the entire training and test sets) that compares the performance of our algorithm and Johansen’s is illustrated in Figure 1.

6.3 Results

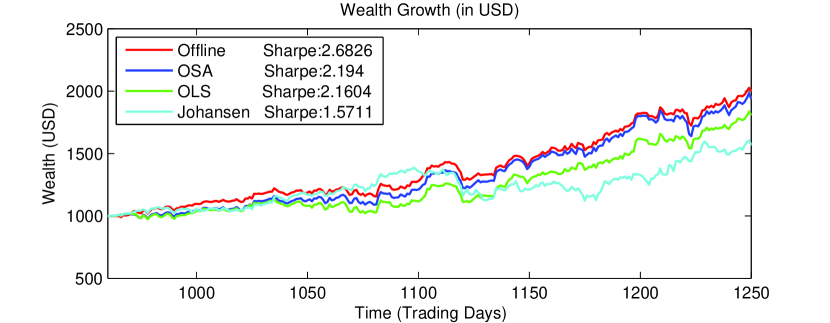

In Figure 2 we plot the cumulative wealth of our online algorithm and the three offline baselines, and also provide the Sharpe ratios. To execute this experiments we use the 10 pairs of assets in our dataset. In all runs of our online algorithm and its offline counterpart we set and , arbitrarily. The task of determining the best values of and is outside the scope of this paper, yet is a very challenging problem. The empirical observations clearly verify the effectiveness of the proposed mean reversion proxy and the online algorithm, as both OSA and Offline outperform the other baselines. It can can also be seen that the performance of OSA approaches the performance of Offline as time advances, corresponding to our theoretic regret guarantee. It remains for future work to compare the performance of the online approach and the offline state-of-the-art approaches in the presence of transaction costs.

| Return (in %) | ||

|---|---|---|

| 8-month | 16-month | |

| Offline | 39.45 | 102.67 |

| OSA | 33.59 | 98.33 |

| OLS | 23.64 | 83.68 |

| Johansen | 33.87 | 60.47 |

References

- [ADT12] Raman Arora, Ofer Dekel, and Ambuj Tewari. Online bandit learning against an adaptive adversary: from regret to policy regret. 2012.

- [CBDS13] Nicolò Cesa-Bianchi, Ofer Dekel, and Ohad Shamir. Online learning with switching costs and other adaptive adversaries. CoRR, abs/1302.4387, 2013.

- [CBL06] N. Cesa-Bianchi and G. Lugosi. Prediction, learning, and games. Cambridge University Press, 2006.

- [D’A11] Alexandre D’Aspremont. Identifying small mean-reverting portfolios. Quant. Finance, 11(3):351–364, 2011.

- [GN11] András György and Gergely Neu. Near-optimal rates for limited-delay universal lossy source coding. In ISIT, pages 2218–2222, 2011.

- [GVW10] Sascha Geulen, Berthold Vöcking, and Melanie Winkler. Regret minimization for online buffering problems using the weighted majority algorithm. In COLT, pages 132–143, 2010.

- [HAK07] Elad Hazan, Amit Agarwal, and Satyen Kale. Logarithmic regret algorithms for online convex optimization. Machine Learning, 69(2-3):169–192, 2007.

- [Haz11] Elad Hazan. The convex optimization approach to regret minimization. Optimization for machine learning, page 287, 2011.

- [Joh91] Soren Johansen. Estimation and Hypothesis Testing of Cointegration Vectors in Gaussian Vector Autoregressive Models. Econometrica, 59(6):1551–80, November 1991.

- [JY07] Jakub W Jurek and Halla Yang. Dynamic portfolio selection in arbitrage. In EFA 2006 Meetings Paper, 2007.

- [LV03] László Lovász and Santosh Vempala. Logconcave functions: Geometry and efficient sampling algorithms. In FOCS, pages 640–649. IEEE Computer Society, 2003.

- [MK98] G.S. Maddala and I.M. Kim. Unit Roots, Cointegration, and Structural Change. Themes in Modern Econometrics. Cambridge University Press, 1998.

- [MOSW02] Neri Merhav, Erik Ordentlich, Gadiel Seroussi, and Marcelo J. Weinberger. On sequential strategies for loss functions with memory. IEEE Transactions on Information Theory, 48(7):1947–1958, 2002.

- [MOSW06] N. Merhav, E. Ordentlich, G. Seroussi, and M. J. Weinberger. On sequential strategies for loss functions with memory. IEEE Trans. Inf. Theor., 48(7):1947–1958, September 2006.

- [NR10] Hariharan Narayanan and Alexander Rakhlin. Random walk approach to regret minimization. In John D. Lafferty, Christopher K. I. Williams, John Shawe-Taylor, Richard S. Zemel, and Aron Culotta, editors, NIPS, pages 1777–1785. Curran Associates, Inc., 2010.

- [Put09] Martin L Puterman. Markov decision processes: discrete stochastic dynamic programming, volume 414. Wiley. com, 2009.

- [Sch11] Anatoly B. Schmidt. Financial Markets and Trading: An Introduction to Market Microstructure and Trading Strategies (Wiley Finance). Wiley, 1 edition, August 2011.

- [SS12] Shai Shalev-Shwartz. Online learning and online convex optimization. Foundations and Trends in Machine Learning, 4(2):107–194, 2012.

- [Zin03] M. Zinkevich. Online convex programming and generalized infinitesimal gradient ascent. In ICML, pages 928–936, 2003.

Appendix A Complete Analysis for Section 3

We start by providing some necessary background, and then turn to state and prove our main theorem. We complement our analysis with the special case in which the loss functions are strongly convex (Appendix A.3).

A.1 Background

Recall the RFTL algorithm, which is one of the most popular algorithms for the standard OCO framework. Basically, RFTL generates the decision at time point according to the following rule:

where is a predefined learning parameter, and is called a regularization function. Note that is chosen by the online player, and assumed to be -strongly convex555 The function is called -strongly convex if for all . and smooth, such that its second derivative is continuous.

Usually, general matrix norms are used to analyze and bound the regret of the RFTL algorithm: a PSD matrix gives rise to the norm ; its dual norm is . In particular, the interesting case is when , the Hessian of the regularization function. In this case, the notation is shorthanded to be and .

A.2 Adapting RFTL to the Framework of OCO with Memory

We start by defining the function as follows: . Recall that is convex in for all , as assumed in Section 2. Following the notations of Section A.1, we define a regularization function and upper-bound

| (4) |

Notice that might depend implicitly on . It follows that the loss functions are Lipschitz continuous for the Lipschitz constant with respect to the -norm. I.e., it holds that

Without loss of generality, we can assume that the loss functions are Lipschitz continuous for the same constant, i.e.,

Otherwise, we can simply set to satisfy this condition.

The following is our main theorem, stated and proven:

Theorem 3.1. Let be Lipschitz continuous loss functions with memory (from to ), and let and be as defined in Equation (4). Then, Algorithm 1 generates an online sequence , for which the following holds:

Setting yields .

Proof.

First, note that applying Algorithm 1 to the loss functions is equivalent to applying the original RFTL algorithm to the loss functions . I.e., given initial points , both algorithms generate the same sequence of decisions , for which it holds that:

or equivalently:

| (5) |

due to the regret guarantee in Equation (3). On the other hand, is Lipschitz continuous for the Lipschitz constant , and thus we can bound

where . The inequality follows from the standard analysis of the RFTL algorithm [Haz11]. It follows that and by summing over we get that

| (6) |

Next, by integrating Equations (5) and (6) and using the fact that in our setting, we have that

Finally, setting yields

as stated in the theorem. ∎

A.3 Extending Algorithm 3.1 to Strongly Convex Loss Functions

In the standard OCO framework, it is well known that plugging in the RFTL algorithm yields the familiar Online Gradient Descent (OGD) algorithm of [Zin03]. In this case, it is easy to show that and , where and . Substituting these values in Equation (3) results in the following regret bound for the memoryless loss functions :

By setting we get the familiar bound of , which is known to be tight in , and against memoryless adversaries. In addition, if the memoryless loss functions are assumed to be -strongly convex, it is well known that the OGD algorithm attains logarithmic regret bound if is set properly. More specifically, [HAK07] showed that the OGD algorithm generates an online sequence , for which it holds that:

Setting yields .

In the framework of OCO with memory, when we allow the loss functions to rely on memory of length , Algorithm 1 with the regularization function yields the OGD variant for bounded-memory adversaries — denoted as Algorithm 4. Here, refers to the Euclidian projection onto .

We then extend the property of strong convexity to loss functions with memory as follows: we say that is -strongly convex loss function with memory if is -strongly convex in . Thus, for that are -strongly convex loss functions with memory, we can apply Algorithm 4 to get the following result:

Corollary A.1.

Let be Lipschitz continuous and -strongly convex loss functions with memory (from to ), and denote . Then, Algorithm 4 generates an online sequence , for which the following holds:

Setting yields .

The proof simply requires plugging time-dependent learning parameter in the proof of Theorem 3.1, and thus omitted here.

Appendix B Complete Analysis for Section 4

The outline of this section is as follows: we begin by adapting the EWOO algorithm of [HAK07] to memoryless convex loss functions (Appendix B.1). Then, we present an algorithm for the standard OCO framework that attains low regret and small number of decision switches in expectation (Appendix B.2). Finally, we show that these properties together can be reduced to the framework of OCO with memory, yielding a nearly optimal policy regret bound (Appendix B.3).

B.1 Adapting EWOO to Convex Loss Functions

Recall the Exponentially Weighted Online Optimization (EWOO) algorithm, presented in [HAK07] and designed originally for -exp-concave (memoryless) loss functions .

[HAK07] prove the following regret bound for Algorithm 5:

Next, we consider the following modification of the EWOO algorithm — denoted as Algorithm 6.

Basically, is sampled from the density function , instead of being computed deterministically.

The following two lemmas state that applying Algorithm 6 to the loss functions yields regret bound of .

We first bound the regret of Algorithm 6 when applied to general -exp-concave loss functions (Lemma B.1), and then plug in the loss functions (Lemma B.2).

Lemma B.1.

Let be -exp-concave loss functions. Then, Algorithm 6 generates an online sequence , for which the following holds:

Proof.

The proof goes along the lines of [HAK07]; for completeness, we present here the full proof. Define and notice that

Then, by telescopic product we have

| (7) |

where we used the fact that for all . Denote , then it exists that . Define nearby points by

By concavity and non-negativity of it holds that for every , and thus

By substituting the above in Equation (7) and using the fact that is a rescaling of by factor of in dimensions, we have that

Now, by taking logarithm on both sides we get that

or equivalently

| (8) |

Next, we use the facts that for and for , to derive the following inequality:

By substituting the above in Equation (8) and rearanging we get that

as stated in the lemma. ∎

Plugging in the loss functions into the previous lemma yields the following result:

Lemma B.2.

Let be convex functions from to , such that and and define for some . Then, Applying Algorithm 6 to the loss functions generates an online sequence , for which the following holds:

Setting yields .

B.2 Algorithm and Analysis

We turn now to restate and prove our main theorem:

Theorem 4.1. Let be convex functions from to , such that and , and define for some . Then, Algorithm 2 generates an online sequence , for which it holds that

and in addition

Setting yields , and .

Proof.

The proof follows immediately by observing that: (1) Algorithm 2 generates the decisions from the same distribution with respect Algorithm 6 (stated formally in Lemma B.3 below), and thus attains the same expected regret bound; and (2) Algorithm 2 has an expected low switches guarantee (also stated below in Lemma B.4). ∎

We shall continue to prove the lemmas.

Lemma B.3.

Proof.

Let and be the density functions of and , respectively, and . The proof is by induction: for we have from the definition that for all . Now, let us assume that for all , and prove for . Notice that the weights update for both algorithms is the same and is independent of the decisions actually played by the player. Thus, by applying the law of total probability we have that

The above holds for all , and thus the lemma is obtained. ∎

Lemma B.4.

Let be convex functions from to , such that and . Then, applying Algorithm 2 to the loss functions generates an online sequence , for which the it holds that

where denotes the number of decision switches in the sequence .

Setting yields .

Proof.

From Algorithm 2 it follows that

Using the inequality for all , and substituting from the definition yields

Next, by summing the above for all we have that

Finally, since for all and for all and , setting gives the stated result. ∎

B.3 Reduction to the Framework of OCO with Memory

Up to this point, we presented an algorithm that attains -regret along with expected decision switches for generally convex loss functions . The next lemma states that these two properties imply learning against bounded-memory adversaries.

Lemma B.5.

Let be loss functions with memory from to , define , and denote and . Then, applying Algorithm 2 to the loss functions yields an online sequence , for which it holds that:

Setting yields .

Proof.

From Theorem 4.1, we know that applying Algorithm 2 to the loss functions yields:

or equivalently:

| (9) |

Now, notice that if a decision switch did not occur between time points and , it trivially holds that Otherwise, if a decision switch did occur between these time points, we can bound Thus, it follows that

where again, denotes the number of decision switches in the sequence . From Lemma B.4 we have that , and it follows that

Plugging the above in Equation (B.3) yields the result stated in the lemma. ∎

Appendix C Efficient Implementation of Algorithm 2

The original EWOO algorithm (Algorithm 5) of [HAK07] is not efficient, since it generates as the expectation with respect to the distribution in every iteration. Hazan et al. solve this issue by referring to the works of [LV03], that offer a sampling method from logconcave distributions. These techniques enable the sampling of points from the distribution in time of . Since an accuracy of to the expectation is necessary for maintaining logarithmic regret, must be on the order of . Thus, generating a single decision via a slightly modified EWOO algorithm requires running time of , which results in a total running time of .

The implementation of the proposed algorithm (Algorithm 2) can rely on the same techniques as algorithm EWOO, yet can be carried out more efficiently in various ways. First, our algorithm requires only samples (in compare to samples that EWOO requires), due to its low switches guarantee. Second, each of these samples requires time of using the techniques of [LV03], because need not be generated as the expectation of , but rather only be sampled from this distribution. Therefore, an efficient implementation of our algorithm can be carried out in a total running time of .

Another efficient implementation of Algorithm 2 relies on the work of [NR10], in which techniques of random walks are utilized for regret minimization. Basically, these techniques are applicable in our setting for two reasons: (1) two successive distributions over the decision set, and , are relatively close; and (2) each distribution can be approximated quite well using a Gaussian distribution. This allows sampling via a random walk technique that requires only one step, due to the fact that can be used as its warm start. This results in a same running time guarantee for our algorithm, as stated before for the techniques of [LV03].