Hypothesis Testing in High-Dimensional Regression under the Gaussian Random Design Model: Asymptotic Theory

Abstract

We consider linear regression in the high-dimensional regime where the number of observations is smaller than the number of parameters . A very successful approach in this setting uses -penalized least squares (a.k.a. the Lasso) to search for a subset of parameters that best explain the data, while setting the other parameters to zero. Considerable amount of work has been devoted to characterizing the estimation and model selection problems within this approach.

In this paper we consider instead the fundamental, but far less understood, question of statistical significance. More precisely, we address the problem of computing p-values for single regression coefficients.

On one hand, we develop a general upper bound on the minimax power of tests with a given significance level. We show that rigorous guarantees for earlier methods do not allow to achieve this bound, except in special cases. On the other, we prove that this upper bound is (nearly) achievable through a practical procedure in the case of random design matrices with independent entries. Our approach is based on a debiasing of the Lasso estimator. The analysis builds on a rigorous characterization of the asymptotic distribution of the Lasso estimator and its debiased version. Our result holds for optimal sample size, i.e., when is at least on the order of .

We generalize our approach to random design matrices with i.i.d. Gaussian rows . In this case we prove that a similar distributional characterization (termed ‘standard distributional limit’) holds for much larger than . Our analysis assumes is known. To cope with unknown , we suggest a plug-in estimator for sparse covariances and validate the method through numerical simulations.

Finally, we show that for optimal sample size, being at least of order , the standard distributional limit for general Gaussian designs can be derived from the replica heuristics in statistical physics. This derivation suggests a stronger conjecture than the result we prove, and near-optimality of the statistical power for a large class of Gaussian designs.

1 Introduction

The Gaussian random design model for linear regression is defined as follows. We are given i.i.d. pairs , , , with and , for some covariance matrix . Further, is a linear function of , plus noise

| (1) |

Here is a vector of parameters to be estimated and is the standard scalar product. The special case is usually referred to as ‘standard’ Gaussian design model.

In matrix form, letting and denoting by the matrix with rows ,, we have

| (2) |

We are interested in high-dimensional settings where the number of parameters exceeds the sample size, i.e., , but the number of non-zero entries of (to be denoted by ) is smaller than . In this situation, a recurring problem is to select the non-zero entries of that hence can provide a succinct explanation of the data. The vast literature on this topic is briefly overviewed in Section 1.1.

The Gaussian design assumption arises naturally in some important applications. Consider for instance the problem of learning a high-dimensional Gaussian graphical model from data. In this case we are given i.i.d. samples , with a sparse positive definite matrix whose non-zero entries encode the underlying graph structure. As first shown by Meinshausen and Bühlmann [1], the -th row of can be estimated by performing linear regression of the -th entry of the samples onto the other entries [2]. This reduces the problem to a high-dimensional regression model under Gaussian designs. Standard Gaussian designs were also shown to provide useful insights for compressed sensing applications [3, 4, 5, 6].

In statistics and signal processing applications, it is unrealistic to assume that the set of nonzero entries of can be determined with absolute certainty. The present paper focuses on the problem of quantifying the uncertainty associated to the entries of . More specifically, we are interested in testing null-hypotheses of the form:

| (3) |

for and assigning p-values for these tests. Rejecting is equivalent to stating that .

Any hypothesis testing procedure faces two types of errors: false positives or type I errors (incorrectly rejecting , while ), and false negatives or type II errors (failing to reject , while ). The probabilities of these two types of errors will be denoted, respectively, by and (see Section 2.1 for a more precise definition). The quantity is also referred to as the power of the test, and as its significance level. It is trivial to achieve arbitrarily small if we allow for (never reject ) or arbitrarily small if we allow for (always reject ). This paper aims at optimizing the trade-off between power and significance .

Without further assumptions on the problem structure, the trade-off is trivial and no non-trivial lower bound on can be established. Indeed we can take arbitrarily close to , thus making in practice indistinguishable from its complement. We will therefore assume that, whenever , we have as well. The smallest value of such that the power and significance reach some fixed non-trivial value (e.g., and ) has a particularly compelling interpretation, and provides an answer to the following question: What is the minimum magnitude of to be able to distinguish it from the noise level, with a given degree of confidence?

More precisely, we are interested in establishing necessary and sufficient conditions on , , , and such that a given significance level , and power can be achieved in testing for all coefficient vectors that are -sparse and . Some intuition can be gained by considering special cases (for the sake of comparison, we assume that the columns of are normalized to have norm of order ):

-

•

In the case of orthogonal designs we have and . By an orthogonal transformation, we can limit ourselves to , i.e., . Hence testing hypothesis reduces to testing for the mean of a univariate Gaussian.

It is easy to see that we can distinguish the -th entry from noise only if its size is at least of order . More precisely, for any , , we can achieve significance and power if and only if for some constant [7, Section 3.9].

-

•

To move away from the orthogonal case, consider standard Gaussian designs. Several papers studied the estimation problem in this setting [8, 9, 10, 11]. The conclusion is that there exist computationally efficient estimators that are consistent (in high-dimensional sense) for , with a numerical constant. By far the most popular such estimator is the Lasso or Basis Pursuit Denoiser [12, 13].

These simple remarks motivate the following seemingly simple question:

-

Q:

Assume standard Gaussian design , and fix . Are there constants , and a hypothesis testing procedure achieving the desired significance and power for all , ?

Despite the seemingly idealized setting, the answer to this question is highly non-trivial. To document this point, we consider in Appendix C two hypothesis testing methods that were recently proposed by Zhang and Zhang [16], and by Bühlmann [17]. These approaches apply to a broader class of design matrices that satisfy the restricted eigenvalue property [18]. We show that, when specialized to the case of standard Gaussian designs , these methods require to reject hypothesis with a given degree of confidence (with being a constant independent of the problem dimensions). In other words, these methods are guaranteed to succeed only if the coefficient to be tested is larger than the ideal scale , by a diverging factor of order . In particular, the results of [16, 17] do not allow to answer the above question.

In this paper, we answer positively to this question. As in [16, 17], our approach is based on the Lasso estimator [12, 13]

| (4) |

We use the solution to this problem to construct a debiased estimator of the form

| (5) |

with a properly constructed matrix. We then use its -th component as a test statistics for hypothesis . (We refer to Sections 3 and 4 for a detailed description of our procedure.)

A similar approach was developed independently in [16] and (after a a preprint version of the present paper became available online) in [19]. Apart from differences in the construction of , the three papers differ crucially in the assumptions and the regime analyzed, and establish results that are not directly comparable. In the present paper we assume a specific (random) model for the design matrix . In contrast [16] and [19] assume deterministic designs, or random designs with general unknown covariance.

On the other hand, we are able to analyze a regime that is significantly beyond reach of the mathematical techniques of [16, 19], even for the very special case of standard Gaussian designs. Namely, for standard designs, we consider of order , and of order .

This regime is both challenging and interesting because (when non-vanishing) is of the same order as the noise level. Indeed our analysis requires an exact asymptotic distributional characterization of the problem (4).

The contributions of this paper are organized as follows:

- Section 2: Upper bound on the minimax power.

-

We state the problem formally, by taking a minimax point of view. Based on this formulation, we prove a general upper bound on the minimax power of tests with a given significance level . We then specialize this bound to the case of standard Gaussian design matrices, showing formally that no test can achieve non-trivial significance , and power , unless , with a dimension-independent constant.

- Section 3: Hypothesis testing for standard Gaussian designs.

-

We define a hypothesis testing procedure that is well-suited for the case of standard Gaussian designs, . We prove that this test achieves a ‘nearly-optimal’ power-significance trade-off in a properly defined asymptotic sense. Here ‘nearly optimal’ means that the trade-off has the same form as the previous upper bound, except that is replaced by with a universal constant. In particular, we provide a positive answer to the open question discussed above.

Our analysis builds on an exact asymptotic characterization of the Lasso estimator, first developed in [10].

- Section 4: Hypothesis testing for nonstandard Gaussian designs.

-

We introduce a generalization of the previous hypothesis testing method to Gaussian designs with general covariance matrix . In this case we cannot establish validity in the regime , since a rigorous generalization of the distributional result of [10] is not available.

However: We prove that such a generalized distributional limit holds under the stronger assumption that is much larger than (see Theorem 4.5). We show that this distributional limit can be derived from the powerful replica heuristics in statistical physics for the regime . (See Section 4 for further discussion of the validity of this heuristics.)

Conditional on this standard distributional limit holding, we prove that the proposed procedure is nearly optimal in this case as well.

- Numerical validation.

-

We validate our approach on both synthetic and real data in Sections 3.4, 4.6 and Section 6, comparing it with the methods of [16, 17]. Simulations suggest that the latter are indeed overly conservative in the present setting, resulting in suboptimal statistical power. (As emphasized above, the methods of [16, 17] apply to a broader class of design matrices .)

Proofs are deferred to Section 7.

Let us stress that the present treatment has two important limitations. First, it is asymptotic: it would be important to develop non-asymptotic bounds. Second, for the case of general designs, it requires to know or estimate the design covariance . In Section 4.5 we discuss a simple approach to this problem for sparse . A full study of this issue is however beyond the scope of the present paper.

After a a preprint version of the present paper became available online, several papers appeared that partially address these limitations. In particular [19, 20] make use of debiased estimators of the form (5), and have much weaker assumptions on the design . Note however that these papers require a significantly larger sample size, namely . Hence, even limiting ourselves to standard designs, the results presented here are not comparable to the ones of [19, 20], and instead complement them. We refer to Section 5 for further discussion of the relation.

1.1 Further related work

High-dimensional regression and -regularized least squares estimation, a.k.a. the Lasso (4), were the object of much theoretical investigation over the last few years. The focus has been so far on establishing order optimal guarantees on: The prediction error , see e.g. [21]; The estimation error, typically quantified through , with , see e.g. [22, 18, 23]; The model selection (or support recovery) properties typically by bounding , see e.g. [1, 24, 25]. For estimation and support recovery guarantees, it is necessary to make specific assumptions on the design matrix , such as the restricted eigenvalue property of [18] or the compatibility condition of [26]. Both [16] and [17] assume conditions of this type for developing hypothesis testing procedures.

In contrast we work within the Gaussian random design model, and focus on the asymptotics with and . The study of this type of high-dimensional asymptotics was pioneered by Donoho and Tanner [3, 4, 5, 6] , who assumed standard Gaussian designs and focused on exact recovery in absence of noise. The estimation error in presence of noise was characterized in [11, 10]. Further work in the same or related setting includes [27, 8, 9].

Wainwright [25] also considered the Gaussian design model and established upper and lower thresholds , for correct recovery of in noise , under an additional condition on . The thresholds , are of order for many covariance structures , provided for some constant . Correct support recovery depends, in a crucial way, on the irrepresentability condition of [24].

Let us stress that the results on support recovery offer limited insight into optimal hypothesis testing procedures. Under the conditions that guarantee exact support recovery, both type I and type II error rates tend to rapidly as , thus making it difficult to study the trade-off between statistical significance and power. Here we are interested in triples for which and stay bounded. As discussed in the previous section, the regime of interest (for standard Gaussian designs) is . At the lower end the number of observations is so small that essentially nothing can be inferred about using optimally tuned Lasso estimator, and therefore a nontrivial power cannot be achieved. At the upper end, the number of samples is sufficient enough to recover with high probability, leading to arbitrary small errors

Let us finally mention that resampling methods provide an alternative path to assess statistical significance. A general framework to implement this idea is provided by the stability selection method of [28]. However, specializing the approach and analysis of [28] to the present context does not provide guarantees superior to [16, 17], that are more directly comparable to the present work.

1.2 Notations

We provide a brief summary of the notations used throughout the paper. We denote by the set of first integers. For a subset , we let denote its cardinality. Bold upper (resp. lower) case letters denote matrices (resp. vectors), and the same letter in normal typeface represents its coefficients, e.g. denotes the th entry of . For an matrix and set of indices , we let denote the submatrix containing just the columns in and use to denote the submatrix formed by rows in and columns in . Likewise, for a vector , is the restriction of to indices in . We denote the rows of the design matrix by . We also denote its columns by . The support of a vector is denoted by , i.e., . We use to denote the identity matrix in any dimension, and whenever is useful to specify the dimension .

Throughout, is the Gaussian density and is the Gaussian distribution. For two functions and , with , the notation means that is bounded below by asymptotically, namely, there exists constant and integer , such that for . Further, means that is bounded above by asymptotically, namely, for some constants and integer , for all . Finally if both and .

2 Minimax formulation

In this section we define the hypothesis testing problem, and introduce a minimax criterion for evaluating hypothesis testing procedures. In subsection 2.2 we state our upper bound on the minimax power and, in subsection 2.3, we outline the prof argument, that is based on a reduction to binary hypothesis testing.

2.1 Tests with guaranteed power

We consider the minimax criterion to measure the quality of a testing procedure. In order to define it formally, we first need to establish some notations.

A testing procedure for the family of hypotheses , cf. Eq. (3), is given by a family of measurable functions

| (6) |

Here has the interpretation that hypothesis is rejected when the observation is and the design matrix is . We will hereafter drop the subscript whenever clear from the context.

As mentioned above, we will measure the quality of a test in terms of its significance level (probability of type I errors) and power ( is the probability of type II errors). A type I error (false rejection of the null) leads one to conclude that a relationship between the response vector and a column of the design matrix exists when in reality it does not. On the other hand, a type II error (the failure to reject a false null hypothesis) leads one to miss an existing relationship.

Adopting a minimax point of view, we require that these metrics are achieved uniformly over -sparse vectors. Formally, for , we let

| (7) | |||||

| (8) |

In words, for any -sparse vector with , the probability of false alarm is upper bounded by . On the other hand, if is -sparse with , the probability of misdetection is upper bounded by . Note that is the induced probability distribution on for random design and noise realization , given the fixed parameter vector . Throughout we will accept randomized testing procedures as well333Formally, this corresponds to assuming with uniform in and independent of the other random variables..

Definition 2.1.

The minimax power for testing hypothesis against the alternative is given by the function where, for

| (9) |

Note that for standard Gaussian designs (and more generally for designs with exchangeable columns), , do not depend on the index . We shall therefore omit the subscript in this case.

The following are straightforward yet useful properties.

Remark 2.2.

The optimal power is non-decreasing. Further, by using a test such that with probability independently of , , we conclude that .

Proof.

To prove the first property, notice that, for any we have . Indeed is obtained by taking the supremum in Eq. (9) over a family of tests that includes those over which the supremum is taken for .

Next, a completely randomized test outputs with probability independently of . We then have for any , whence . Since this test offers –by definition– the prescribed control on type I errors, we have, by Eq. (9), . ∎

2.2 Upper bound on the minimax power

Our upper bound on the minimax power is stated in terms of the function , , defined as follows.

| (10) |

It is easy to check that, for any , is continuous and monotone increasing. For fixed is continuous and monotone increasing. Finally and .

We then have the following upper bound on the optimal power of random Gaussian designs. (We refer to Section 7.3 for the proof.)

Theorem 2.3.

For , let be the minimax power of a Gaussian random design with covariance matrix , as per Definition 2.1. For , define . Then, for any and ,

| (11) | ||||

| (12) |

where , and is a chi-squared random variable with degrees of freedom.

In other words, the statistical power is upper bounded by the one of testing the mean of a scalar Gaussian random variable, with effective noise variance . (Note indeed that by concentration of a chi-squared random variable around their mean, can be taken small as compared to .)

The next corollary specializes the above result to the case of standard Gaussian designs. (The proof is immediate and hence we omit it.)

Corollary 2.4.

For , let be the minimax power of a standard Gaussian design with covariance matrix , cf. Definition 2.1. Then, for any we have

| (13) |

It is instructive to look at the last result from a slightly different point of view. Given and , how big does the entry need to be so that ? It follows from Corollary 2.4 that to achieve a pair as above we require for some .

Previous work [16, 17] requires to achieve the same goal although for deterministic designs (see Appendix C). This motivates the central question of the present paper (already stated in the introduction): Can hypothesis testing be performed in the ideal regime ?

As further clarified in the next section and in Section 7.1, Theorem 2.3 by an oracle-based argument. Namely, we upper bound the power of any hypothesis testing method, by the power of an oracle that knows, for each coordinates , whether or not. In other words the procedure has access to . At first sight, this oracle appears exceedingly powerful, and hence the bound might be loose. Surprisingly, the bound turns out to be tight, at least in an asymptotic sense, as demonstrated in Section 3.

Let us finally mention that a bound similar to the present one was announced independently –and from a different viewpoint– in [29].

2.3 Proof outline

The proof of Theorem 2.3 is based on a simple reduction to the binary hypothesis testing problem. We first introduce the binary testing problem, in which the vector of coefficients is chosen randomly according to one of two distributions.

Definition 2.5.

Let be a probability distribution on supported on , and a probability distribution supported on . For fixed design matrix , and , let denote the law of as per model (2) when is chosen randomly with .

We denote by the optimal power for the binary hypothesis testing problem versus , namely:

| (14) |

The reduction is stated in the next lemma.

Lemma 2.6.

Let , be any two probability measures supported, respectively, on and as per Definition 2.5. Then, the minimax power for testing hypothesis under the random design model, cf. Definition 2.1, is bounded as

| (15) |

Here expectation is taken with respect to the law of and the is over all measurable functions .

For the proof we refer to Section 7.1.

The binary hypothesis testing problem is characterized in the next lemma by reducing it to a simple regression problem. For , we denote by the orthogonal projector on the linear space spanned by the columns . We also let be the projector on the orthogonal subspace.

Lemma 2.7.

Let and . For , , define

| (16) |

If then for any there exists distributions , as per Definition 2.5, depending on , , but not on , such that .

The proof of this Lemma is presented in Section 7.2.

3 Hypothesis testing for standard Gaussian designs

In this section we describe our hypothesis testing procedure (that we refer to as SDL-test) in the case of standard Gaussian designs, see subsection 3.1. In subsection 3.2, we develop asymptotic bounds on the probability of type I and type II errors. The test is shown to nearly achieve the ideal tradeoff between significance level and power , using the upper bound stated in the previous section.

Our results are based on a characterization of the high-dimensional behavior of the Lasso estimator, developed in [10]. For the reader’s convenience, and to provide further context, we recall this result in subsection 3.3. Finally, subsection 3.4 discusses some numerical experiments.

3.1 Hypothesis testing procedure

Our SDL-test procedure for standard Gaussian designs is described in Table 1.

SDL-test : Testing hypothesis under standard Gaussian design model.

Input: regularization parameter , significance level

Output: p-values , test statistics

1: Let

2: Let

| (17) |

where for , is the -th largest entry in the vector .

3: Let

4: Assign the p-values for the test as follows.

5: The decision rule is then based on the p-values:

The key is the construction of the unbiased estimator in step 3. The asymptotic analysis developed in [10] and in the next section establishes that is an asymptotically unbiased estimator of , and the empirical distribution of is asymptotically normal with variance . Further, the variance can be consistently estimated using the residual vector . These results establish that (in a sense that will be made precise next) the regression model (2) is asymptotically equivalent to a simpler sequence model

| (18) |

with noise having zero mean. In particular, under the null hypothesis , is asymptotically gaussian with mean and variance . This motivates rejecting the null if .

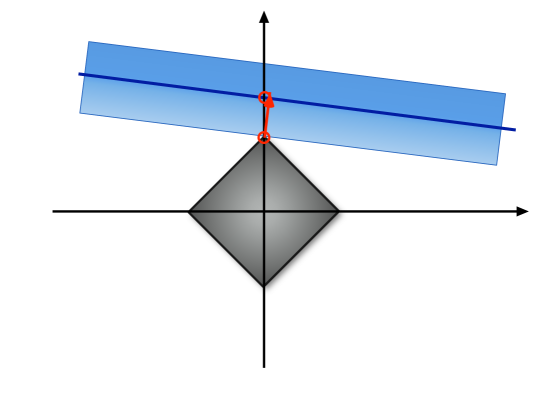

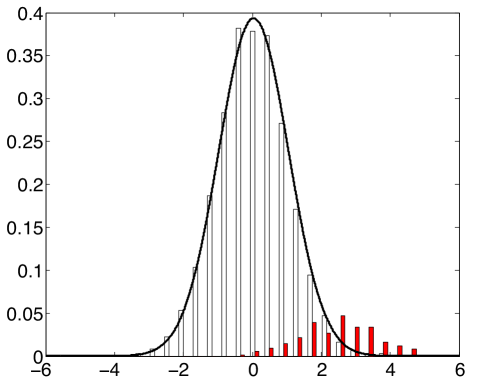

The construction of has an appealing geometric interpretation. Notice that is necessarily biased towards small norm. The minimizer in Eq. (4) must satisfy , with a subgradient of norm at . Hence, we can rewrite . The bias is eliminated by modifying the estimator in the direction of increasing norm. See Fig. 1 for an illustration.

3.2 Asymptotic analysis

For given dimension , an instance of the standard Gaussian design model is defined by the tuple , where , , . We consider sequences of instances indexed by the problem dimension .

Definition 3.1.

The sequence of instances indexed by is said to be a converging sequence if , , and the empirical distribution of the entries converges weakly to a probability measure on with bounded second moment. Further .

Note that this definition assumes the coefficients are of order one, while the noise is scaled as . Equivalently, we could have assumed and : the two settings only differ by a scaling of . We favor the first scaling as it simplifies somewhat the notation in the following.

As before, we will measure the quality of the proposed test in terms of its significance level (size) and power . Recall that and respectively indicate the type I error (false positive) and type II error (false negative) rates. The following theorem establishes that the ’s are indeed valid p-values, i.e., allow to control type I errors. Throughout is the support of .

Theorem 3.2.

Let be a converging sequence of instances of the standard Gaussian design model. Assume . Then, for , we have

| (19) |

A more general form of Theorem 3.2 (cf. Theorem 4.3) is proved in Section 7. We indeed prove the stronger claim that the following holds true almost surely

| (20) |

The result of Theorem 3.2 follows then by taking the expectation of both sides of Eq. (20) and using bounded convergence theorem and exchangeability of the columns of .

Our next theorem proves a lower bound for the power of the proposed test. In order to obtain a non-trivial result, we need to make suitable assumption on the parameter vectors . In particular, we need to assume that the non-zero entries of are lower bounded in magnitude. If this were not the case, it would be impossible to distinguish arbitrarily small parameters from . (In Appendix B, we also provide an explicit formula for the regularization parameter that achieves this power.)

Theorem 3.3.

There exists a (deterministic) choice of such that the following happens.

Let be a converging sequence of instances under the standard Gaussian design model. Assume that , and for all , with . for , we have

| (21) |

where is defined as follows

| (22) |

Here, is given by the following parametric expression in terms of the parameter :

| (23) |

Theorem 3.3 is proved in Section 7. We indeed prove the stronger claim that the following holds true almost surely:

| (24) |

The result of Theorem 3.3 follows then by taking the expectation of both sides of Eq. (24) and using exchangeability of the columns of .

Again, it is convenient to rephrase Theorem 3.3 in terms of the minimum value of for which we can achieve statistical power at significance level . It is known that [11]. Hence, for , we have . Since , any pre-assigned statistical power can be achieved by taking which matches the fundamental limit established in the previous section.

Let us finally comment on the choice of the regularization parameter . Theorem 3.2 holds irrespective of , as long as it is kept fixed in the asymptotic limit. In other words, control of type I errors is fairly insensitive to the regularization parameters. On the other hand, to achieve optimal minimax power, it is necessary to tune to the correct value. The tuned value of for the standard Gaussian sequence model is provided in Appendix A. Further, the factor (and hence the need to estimate the noise level) can be omitted if –instead of the Lasso– we use the scaled Lasso [30]. In subsection 3.4, we discuss another way of choosing that also avoid estimating the noise level.

3.3 Gaussian limit

Theorems 3.2 and 3.3 are based on an asymptotic distributional characterization of the Lasso estimator developed in [10]. We restate it here for the reader’s convenience.

Theorem 3.4 ([10]).

Let be a converging sequence of instances of the standard Gaussian design model. Denote by the Lasso estimator given as per Eq. (4) and define , by letting

| (25) |

with .

Then, with probability one, the empirical distribution of converges weakly to the probability distribution of , for some , where , and is independent of . Furthermore, with probability one, the empirical distribution of converges weakly to .

In particular, this result implies that the empirical distribution of is asymptotically normal with variance . This naturally motivates the use of as a test statistics for hypothesis .

The definitions of and in step 2 are also motivated by Theorem 3.4. In particular, is asymptotically normal with variance . This is used in step 2, where is just the robust median absolute deviation (MAD) estimator (we choose this estimator since it is more resilient to outliers than the sample variance [31]).

3.4 Numerical experiments

As an illustration, we generated synthetic data from the linear model (1) with and the following configurations.

Design matrix: For pairs of values , the design matrix is generated from a realization of i.i.d. rows .

Regression parameters: We consider active sets with , chosen uniformly at random from the index set . We also consider two different strengths of active parameters , for , with .

We examine the performance of SDL-test (cf. Table 1) at significance levels . The experiments are done using glmnet-package in R that fits the entire Lasso path for linear regression models. Let and . We do not assume is known, but rather estimate it as . The value of is half the maximum sparsity level for the given such that the Lasso estimator can correctly recover the parameter vector if the measurements were noiseless [32, 10]. Provided it makes sense to use Lasso at all, is thus a reasonable ballpark estimate.

| Method | Type I err | Type I err | Avg. power | Avg. power |

|---|---|---|---|---|

| (mean) | (std.) | (mean) | (std) | |

| SDL-test | 0.05422 | 0.01069 | 0.44900 | 0.06951 |

| Ridge-based regression | 0.01089 | 0.00358 | 0.13600 | 0.02951 |

| LDPE | 0.02012 | 0.00417 | 0.29503 | 0.03248 |

| Asymptotic Bound | 0.05 | NA | 0.37692 | NA |

| SDL-test | 0.04832 | 0.00681 | 0.52000 | 0.06928 |

| Ridge-based regression | 0.01989 | 0.00533 | 0.17400 | 0.06670 |

| LDPE | 0.02211 | 0.01031 | 0.20300 | 0.08630 |

| Asymptotic Bound | 0.05 | NA | 0.51177 | NA |

| SDL-test | 0.05662 | 0.01502 | 0.56400 | 0.11384 |

| Ridge-based regression | 0.02431 | 0.00536 | 0.25600 | 0.06586 |

| LDPE | 0.02305 | 0.00862 | 0.27900 | 0.07230 |

| Asymptotic Bound | 0.05 | NA | 0.58822 | NA |

The regularization parameter is chosen as to satisfy

| (26) |

where and are determined in step 2 of the procedure. Here is the minimax threshold value for estimation using soft thresholding in the Gaussian sequence model, see [11] and Remark B.1. Note that and in the equation above depend implicitly upon . Since glmnet returns the entire Lasso path, the value of solving the above equation can be computed by the bisection method.

As mentioned above, the control of type I error is fairly robust for a wide range of values of . However, the above is an educated guess based on the analysis of [32, 10]. We also tried the values of proposed for instance in [26, 17] on the basis of oracle inequalities.

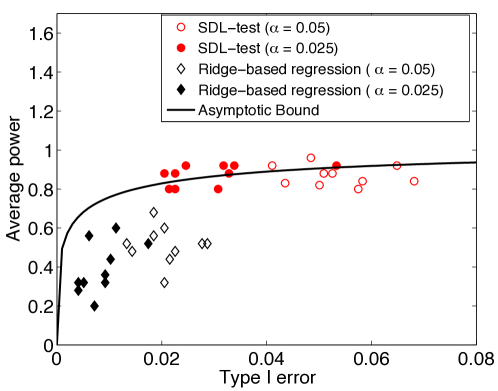

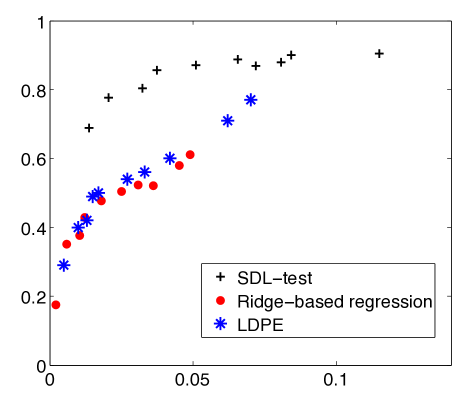

Figure 2 shows the results of SDL-test and the method of [17] for parameter values , and significance levels . Each point in the plot corresponds to one realization of this configuration (there are a total of realizations). We also depict the theoretical curve , predicted by Theorem 3.3. The empirical results are in good agreement with the asymptotic prediction.

We compare SDL-test with the ridge-based regression method [17] and the low dimensional projection estimator (LDPE ) [16]. Table 2 summarizes the results for a few configurations , and . Simulation results for a larger number of configurations and are reported in Tables 8 and 9 in Appendix E.

As demonstrated by these results, LDPE [16] and the ridge-based regression [17] are both overly conservative. Namely, they achieve smaller type I error than the prescribed level and this comes at the cost of a smaller statistical power than our testing procedure. This is to be expected since the approach of [17] and [16] cover a broader class of design matrices , and are not tailored to random designs.

Note that being overly conservative is a drawback, when this comes at the expense of statistical power. The data analysts should be able to decide the level of statistical significance , and obtain optimal statistical power at that level.

The reader might wonder whether the loss in statistical power of methods in [17] and [16] is entirely due to the fact that these methods achieve a smaller number of false positives than requested. In Fig. 3, we run SDL-test , ridge-based regression [17], and LDPE for and for realizations of the problem per each value of . We plot the average type I error and the average power of each method versus . As we see even for the same empirical fraction of type I errors, SDL-test results in a higher statistical power.

4 Hypothesis testing for nonstandard Gaussian designs

In this section, we generalize our testing procedure to nonstandard Gaussian design models where the rows of the design matrix are drawn independently from distribution .

We first describe the generalized SDL-test procedure in subsection 4.1 under the assumption that is known. In subsection 4.2, we show that this generalization can be justified from a certain generalization of the Gaussian limit theorem 3.4 to nonstandard Gaussian designs.

Establishing such a generalization of Theorem 3.4 appears extremely challenging. We nevertheless show that such a limit theorem follows from the replica method of statistical physics in section 4.4. We also show that a version of this limit theorem is relatively straightforward in the regime .

Finally, in Section 4.5 we discuss a procedure for estimating the covariance (cf. Subroutine in Table 4). Appendix F proposes an alternative implementation that does not estimate but instead bounds the effect of unknown .

4.1 Hypothesis testing procedure

SDL-test: Testing hypothesis under nonstandard Gaussian design model.

Input: regularization parameter , significance level , covariance matrix

Output: p-values , test statistics

1: Let

2: Let

| (27) |

where for , is the -th largest entry in the vector .

3: Let

4: Assign the p-values for the test as follows.

5: The decision rule is then based on the p-values:

The hypothesis testing procedure SDL-testfor general Gaussian designs is defined in Table 3.

The basic intuition of this generalization is that is expected to be asymptotically , whence the definition of (two-sided) p-values follows as in step 4. Parameters and in step 2 are defined in the same manner to the standard Gaussian designs.

4.2 Asymptotic analysis

For given dimension , an instance of the nonstandard Gaussian design model is defined by the tuple , where , , , , . We are interested in the asymptotic properties of sequences of instances indexed by the problem dimension . Motivated by Proposition 3.4, we define a property of a sequence of instances that we refer to as standard distributional limit.

Definition 4.1.

A sequence of instances indexed by is said to have an (almost sure) standard distributional limit if there exist (with potentially random, and both , potentially depending on ), such that the following holds. Denote by the Lasso estimator given as per Eq. (4) and define , by letting

| (28) |

Let , for , and be the empirical distribution of defined as

| (29) |

where denotes the Dirac delta function centered at . Then, with probability one, the empirical distribution converges weakly to a probability measure on as . Here, is the probability distribution of , where , and and are random variables independent of . Furthermore, with probability one, the empirical distribution of converges weakly to .

Remark 4.2.

Proving the standard distributional limit for general sequences is an outstanding mathematical challenge. In sections 4.4 and 5 we discuss both rigorous and non-rigorous evidence towards its validity. The numerical simulations in Sections 4.6 and 5 further support the usefulness of this notion.

We will next show that the SDL-test procedure is appropriate for any random design model for which the standard distributional limit holds. Our first theorem is a generalization of Theorem 3.2 to this setting.

Theorem 4.3.

Let be a sequence of instances for which a standard distributional limit holds. Further assume . Then,

| (30) |

The proof of Theorem 4.3 is deferred to Section 7. In the proof, we show the stronger result that the following holds true almost surely

| (31) |

The result of Theorem 4.3 follows then by taking the expectation of both sides of Eq. (31) and using bounded convergence theorem.

The following theorem characterizes the power of SDL-test for general , and under the assumption that a standard distributional limit holds .

Theorem 4.4.

Let be a sequence of instances with standard distributional limit. Assume (without loss of generality) , and further for all , and . Then,

| (32) |

Theorem 4.4 is proved in Section 7. We indeed prove the stronger result that the following holds true almost surely

| (33) |

We also notice that in contrast to Theorem 3.3, where has an explicit formula that leads to an analytical lower bound for the power (for a suitable choice of ), in Theorem 4.4, depends upon implicitly and can be estimated from the data as in step 3 of SDL-test procedure. The result of Theorem 4.4 holds for any value of .

4.3 Gaussian limit for

In the following theorem we show that if sample size asymptotically dominates , then the standard distributional limit can be established rigorously.

Theorem 4.5.

Assume the sequence of instances such that, as (letting ):

-

, and ;

-

;

-

There exist constants such that the eigenvalues of lie in the interval : ;

-

The empirical distribution of converges weakly to the probability distribution of the random variable ;

-

The regularization parameter is for a sufficiently large constant.

Then the sequence has a standard distributional limit with and . Alternatively, can be taken to be a solution of Eq. (37) below.

Notice that this result does allow to control type I errors using Theorem 4.3, but does not allow to lower bound the power, using Theorem 4.4, since . A lower bound on the power under the same assumptions presented in this section can be found in [33]. In the present paper we focus instead on the case bounded away from .

4.4 Gaussian limit via the replica heuristics for smaller sample size

As mentioned above, the standard distributional limit follows from Theorem 3.4 for . Even in this simple case, the proof is rather challenging [10]. Partial generalization to non-gaussian designs and other convex problems appeared recently in [34] and [35], each requiring over 50 pages of proofs.

On the other hand, these and similar asymptotic results can be derived heuristically using the ‘replica method’ from statistical physics. In Appendix D, we use this approach to derive the following claim444In Appendix D we derive indeed a more general result, where the regularization is replaced by an arbitrary separable penalty..

Replica Method Claim 4.6.

Assume the sequence of instances to be such that, as : ; ; The sequence of functions

| (34) |

with and admits a differentiable limit on , with . Then the sequence has a standard distributional limit. Further let

| (35) | ||||

| (36) |

where the the limit exists by the above assumptions on the convergence of . Then, the parameters and of the standard distributional limit are obtained by setting and solving the following with respect to :

| (37) |

In other words, the replica method indicates that the standard distributional limit holds for a large class of non-diagonal covariance structures . It is worth stressing that convergence assumption for the sequence is quite mild, and is satisfied by a large family of covariance matrices. For instance, it can be proved that it holds for block-diagonal matrices as long as the blocks have bounded length and the blocks empirical distribution converges.

The replica method is a non-rigorous but highly sophisticated calculation procedure that has proved successful in a number of very difficult problems in probability theory and probabilistic combinatorics. Attempts to make the replica method rigorous have been pursued over the last 30 years by some world-leading mathematicians [36, 37, 38, 39]. This effort achieved spectacular successes, but so far does not provide tools to prove the above replica claim. In particular, the rigorous work mainly focuses on ‘i.i.d. randomness’, corresponding to the case covered by Theorem 3.4.

Over the last ten years, the replica method has been used to derive a number of fascinating results in information theory and communications theory, see e.g. [40, 41, 42, 43, 44]. More recently, several groups used it successfully in the analysis of high-dimensional sparse regression under standard Gaussian designs [45, 46, 47, 44, 48, 49, 50]. The rigorous analysis of ours and other groups [51, 10, 34, 35] subsequently confirmed these heuristic calculations in several cases.

There is a fundamental reason that makes establishing the standard distributional limit a challenging task. This requires in fact to characterize the distribution of the estimator (4) in a regime where the standard deviation of is of the same order as its mean. Further, does not converge to the true value , hence making perturbative arguments ineffective.

4.5 Covariance estimation

So far we assumed that the design covariance is known. This setting is relevant for semi-supervised learning applications, where the data analyst has access to a large number of ‘unlabeled examples’. These are i.i.d. feature vectors , ,… with distributed as , for which the response variable is not available. In this case can be estimated accurately by . We refer to [52] for further background on such applications.

In other applications, is unknown and no additional data is available. In this case we proceed as follows:

-

1.

We estimate from the design matrix (equivalently, from the feature vectors , , …). We let denote the resulting estimate.

-

2.

We use instead of in step 3 of our hypothesis testing procedure.

The problem of estimating covariance matrices in high-dimensional setting has attracted considerable attention in the past. Several estimation methods provide a consistent estimate , under suitable structural assumptions on . For instance if is sparse, one can apply the graphical model method of [1], the regression approach of [53], or CLIME estimator [54], to name a few.

Since the covariance estimation problem is not the focus of our paper, we will test the above approach using a very simple covariance estimation method. Namely, we assume that is sparse and estimate it by thresholding the empirical covariance. A detailed description of this estimator is given in Table 4. We refer to [55] for a theoretical analysis of this type of methods. Note that the Lasso is unlikely to perform well if the columns of are highly correlated and hence the assumption of sparse is very natural. On the other hand, we would like to emphasize that this covariance thresholding estimation is only one among many possible approaches.

As an additional contribution, in Appendix F we describe an alternative covariance-free procedure that only uses bounds on where the bounds are estimated from the data.

In our numerical experiments, we use the estimated covariance returned by Subroutine. As shown in the next section, computed p-values appear to be fairly robust with respect to errors in the estimation of . It would be interesting to develop a rigorous analysis of SDL-test that accounts for the covariance estimation error.

Subroutine: Estimating covariance matrix

Input: Design matrix

Output: Estimate

1: Let .

2: Let be the empirical variance of the entries in and let .

3: Let be the variance of entries in .

4: Construct as follows:

| (38) |

5: Denote by and the smallest and the smallest

positive eigenvalues of respectively.

6: Set

| (39) |

4.6 Numerical experiments

In carrying out our numerical experiments for correlated Gaussian designs, we consider the same setup as the one in Section 3.4. The only difference is that the rows of the design matrix are independently . We choose to be a the symmetric matrix with entries are defined as follows for

| (40) |

Elements below the diagonal are given by the symmetry condition . (Notice that this is a circulant matrix.)

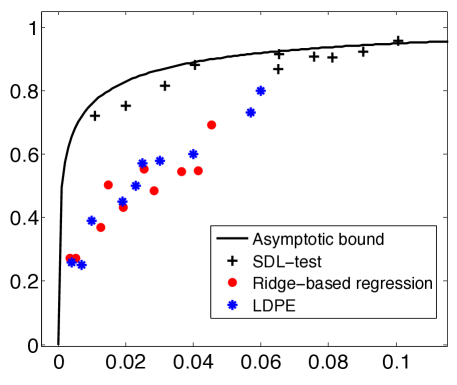

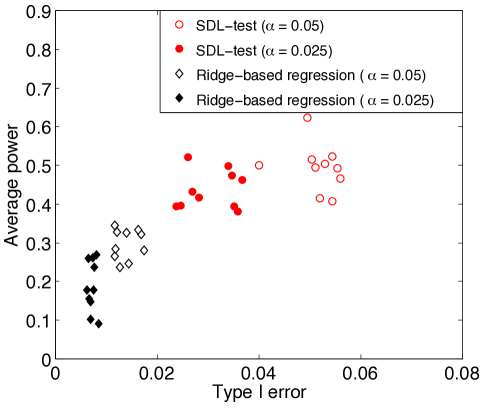

In Fig. 4(a), we compare SDL-test with the ridge-based regression method proposed in [17]. While the type I errors of SDL-test are in good match with the chosen significance level , the method of [17] is conservative. As in the case of standard Gaussian designs, this results in significantly smaller type I errors than and smaller average power in return. Also, in Fig. 5, we run SDL-test , ridge-based regression [17], and LDPE [16] for and for realizations of the problem per each value of . We plot the average type I error and the average power of each method versus . As we see, similar to the case of standard Gaussian designs, even for the same empirical fraction of type I errors, SDL-test results in a higher statistical power.

Table 5 summarizes the performances of the these methods for a few configurations , and . Simulation results for a larger number of configurations and are reported in Tables 10 and 11 in Appendix E.

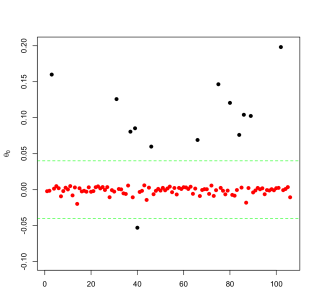

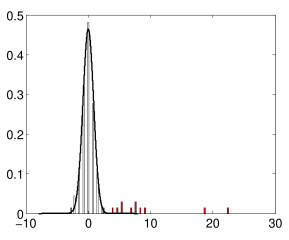

Let denote the vector with entries . In Fig. 4(b) we plot the normalized histograms of (in red) and (in white), where and respectively denote the restrictions of to the active set and the inactive set . The plot clearly exhibits the fact that has (asymptotically) standard normal distribution and the histogram of appears as a distinguishable bump. This is the core intuition in defining SDL-test.

| Method | Type I err | Type I err | Avg. power | Avg. power |

|---|---|---|---|---|

| (mean) | (std.) | (mean) | (std) | |

| SDL-test | 0.06733 | 0.01720 | 0.48300 | 0.03433 |

| Ridge-based regression | 0.00856 | 0.00416 | 0.17000 | 0.03828 |

| LDPE | 0.01011 | 0.00219 | 0.29503 | 0.03248 |

| Lower bound | 0.05 | NA | 0.45685 | 0.04540 |

| SDL-test | 0.04968 | 0.00997 | 0.50800 | 0.05827 |

| Ridge-based regression | 0.01642 | 0.00439 | 0.21000 | 0.04738 |

| LDPE | 0.02037 | 0.00751 | 0.32117 | 0.06481 |

| Lower bound | 0.05 | NA | 0.50793 | 0.03545 |

| SDL-test | 0.05979 | 0.01435 | 0.55200 | 0.08390 |

| Ridge-based regression | 0.02421 | 0.00804 | 0.22400 | 0.10013 |

| LDPE | 0.02604 | 0.00540 | 0.31008 | 0.06903 |

| Lower bound | 0.05 | NA | 0.54936 | 0.06176 |

5 Discussion

In this section we compare our contribution with related work in order to put it in proper perspective. We first compare it with other recent debiasing methods [16, 19, 20] in subsection 5.1. In subsection 5.2 we then discuss the role of of the factor in our definition of : this is an important difference with respect to the methods of [16, 19, 20]. We finally contrast the Gaussian limit in Theorem 3.4 and Le Cam’s local asymptotic normality theory, that plays a pivotal role in classical statistics.

5.1 Comparison with other debiasing methods

As explained several times in the previous sections, the key step in our procedure is to correct the Lasso estimator through a debiasing procedure. For the reader’s convenience, we copy here the definition of the latter:

| (41) |

The approach of [16] is similar in that it is based on debiased estimator of the form

| (42) |

where is computed from the design matrix . The authors of [16] propose to compute by doing sparse regression of each column of onto the others.

After a first version of the present paper became available as an online preprint, de Geer, Bühlmann and Ritov [19] studied an approach similar to [16] (and to ours) in a random design setting. They provide guarantees under the assumptions that is sparse and that the sample size asymptotically dominates . The authors also establish asymptotic optimality of their method in terms of semiparametric efficiency. The semiparametric setting is also at the center of [16, 29].

A further development over the approaches of [16, 19] was proposed by the present authors in [20]. This paper constructs the matrix by solving an optimization problem that controls the bias of and minimize its variance meanwhile. This method does not require any sparsity assumption on or , but still requires sample size to asymptotically dominate .

It is interesting to compare and contrast the results of [16, 19, 20], with the contribution of the present paper. (Let us emphasize that [19] appeared after submission of the present work.)

- Assumptions on the design matrix.

-

The approach of [16, 19, 20] guarantees control of type I error, and optimality for non-Gaussian designs. (Both of [16, 19] require however sparsity of .)

In contrast, our results are fully rigorous only in the special case .

- Covariance estimation.

-

Neither of the papers [16, 19, 20] requires knowledge of covariance . The method in [19] estimates assuming that it is sparse, however the method [20] does not require such estimation.

In contrast, our generalization to arbitrary Gaussian designs postulates knowledge of . (Further this generalization relies on the standard distributional limit assumption.)

- Sample size assumption.

-

The work of [19, 20] focuses on random designs, but requires much larger than . This is roughly the square of the number of samples needed for consistent estimation.

In contrast, we achieve similar power, and confidence intervals with optimal sample size .

In summary, the present work is complementary to the one in [16, 19, 20] in that it provides a sharper characterization, within a more restrictive setting. Together, these papers provide support for the use of debiasing methods of the form (42).

5.2 Role of the factor

It is worth stressing one subtle, yet interesting, difference between the methods of of [16, 19] and the one of the present paper. In both cases, a debiased estimator is constructed using Eq. (42). However:

- •

-

•

In contrast, our prescription (41) amounts to setting , with . In other words, we choose as a scaled version of the inverse covariance.

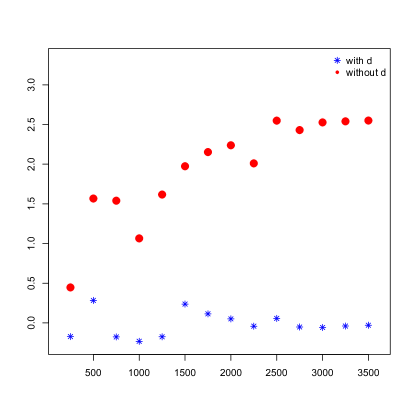

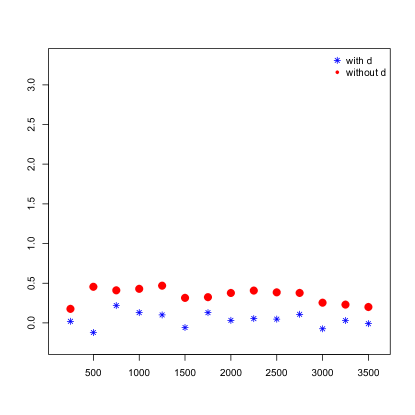

The mathematical reason for the specific scaling factor is elucidated by the proof of Theorem 3.4 in [10]. Here we limit ourselves to illustrating through numerical simulations that this factor is indeed crucial to ensure the normality of in the regime .

We consider the same setup as in Section 4.6 where the rows of the design matrix are generated independently from with given by (40) for . We fix undersampling ratio and sparsity level and consider values . We also take active sets with chosen uniformly at random from the index set and set for .

The goal is to illustrate the effect of the scaling factor on the empirical distribution of , for large . As we will see, the effect becomes more pronounced as the ratio (i.e. the number of samples per non-zero coefficient) becomes smaller. As above, we use for the unbiased estimator developed in this paper (which amounts to Eq. (42) with ). We will use for the ‘ideal’ unbiased estimator corresponding to the proposal of [16, 19] (which amounts to Eq. (42) with ).

-

(). Let with . In Fig 6(a), the empirical kurtosis555Recall that the empirical of sample kurtosis is defined as with and . of is plotted for the two cases , and . When using , the kurtosis is very small and data are consistent with the kurtosis vanishing as . This is suggestive of the fact that is asymptotically Gaussian, and hence satisfies a standard distributional limit. However, if we use , the empirical kurtosis of does not converge to zero.

In Fig. 7, we plot the histogram of for and using both and . Again, the plots clearly demonstrate importance of in obtaining a Gaussian behavior.

(a)

(b) Figure 6: Empirical kurtosis of vector with and without normalization factor . In left panel (with , ) and in the right panel (with , ).

(a) with factor

(b) without factor Figure 7: Histogram of for (, ) and . In left panel, factor is computed by Eq. (27) and in the right panel, .

(a) with factor

(b) without factor Figure 8: Histogram of for (, ) and . In left panel, factor is computed by Eq. (27) and in the right panel, .

5.3 Comparison with Local Asymptotic Normality

Our approach is based on an asymptotic distributional characterization of the Lasso estimator, cf. Theorem 3.4. Simplifying, the Lasso estimator is in correspondence with a debiased estimator that is asymptotically normal in the sense of finite-dimensional distributions. This is analogous to what happens in classical statistics, where local asymptotic normality (LAN) can be used to characterize an estimator distribution, and hence derive test statistics [56, 57].

This analogy is only superficial, and the mathematical phenomenon underlying Theorem 3.4 is altogether different from the one in local asymptotic normality. We refer to [10] for a more complete understanding, and only mention a few points:

-

1.

LAN theory holds in the low-dimensional limit, where the number of parameters is much smaller than the number of samples . Even more, the focus is on fixed, and .

In contrast, the Gaussian limit in Theorem 3.4 holds with proportional to .

-

2.

The starting point of LAN theory is low-dimensional consistency, namely as . As a consequence, the distribution of can be characterized by a local approximation around .

-

3.

Indeed, in the present case, the Lasso estimator (which is of course a special case of M-estimator) is not normal. Only the debiased estimator is asymptotically normal. Further, while LAN theory holds quite generally in the classical asymptotics, the present theory is more sensitive to the properties of the design matrix .

6 Real data application

We tested our method on the UCI communities and crimes dataset [58]. This concerns the prediction of the rate of violent crime in different communities within US, based on other demographic attributes of the communities. The dataset consists of a response variable along with 122 predictive attributes for 1994 communities. Covariates are quantitative, including e.g., the fraction of urban population or the median family income. We consider a linear model as in (2) and hypotheses . Rejection of indicates that the -th attribute is significant in predicting the response variable.

We perform the following preprocessing steps: Each missing value is replaced by the mean of the non missing values of that attribute for other communities. We eliminate attributes to make the ensemble of the attribute vectors linearly independent. Thus we obtain a design matrix with and ; We normalize each column of the resulting design matrix to have mean zero and norm equal to .

In order to evaluate various hypothesis testing procedures, we need to know the true significant variables. To this end, we let be the least-square estimator, using the whole data set. Figure 9 shows the the entries of . Clearly, only a few entries have non negligible values which correspond to the significant attributes. In computing type I errors and powers, we take the elements in with magnitude larger than as active and the others as inactive.

In order to validate our approach in the high-dimensional regime, we take random subsamples of the communities (hence subsamples of the rows of ) of size . We compare SDL-test with the method of [17], over realizations and significance levels . The fraction of type I errors and statistical power is computed by comparing to . Table 6 summarizes the results. As the reader can see, Buhlmann’s method is very conservative yielding to no type-I errors and but much smaller power than SDL-test.

In table 7, we report the relevant features obtained from the whole dataset as described above, corresponding to the nonzero entries in . We also report the features identified as relevant by SDL-test and those identified as relevant by Ridge-based regression method, from one random subsample of communities of size . Features description is available in [58].

Finally, in Fig. 10 we plot the normalized histograms of (in red) and (in white). Recall that denotes the vector with . Further, and respectively denote the restrictions of to the active set and the inactive set . This plot demonstrates that has roughly standard normal distribution as predicted by the theory.

| Method | Type I err | Avg. power |

|---|---|---|

| (mean) | (mean) | |

| SDL-test | 0.0172043 | 0.4807692 |

| Ridge-based regression | 0 | 0.1423077 |

| SDL-test | 0.01129032 | 0.4230769 |

| Ridge-based regression | 0 | 0.1269231 |

| SDL-test | 0.008602151 | 0.3576923 |

| Ridge-based regression | 0 | 0.1076923 |

| Relevant features | racePctHisp, PctTeen2Par, PctImmigRecent, PctImmigRec8, PctImmigRec10, PctNotSpeakEnglWell, OwnOccHiQuart, NumStreet, PctSameState85, LemasSwFTFieldPerPop, LemasTotReqPerPop, RacialMatchCommPol, PolicOperBudg | |

|---|---|---|

| Relevant features (SDL-test ) | racePctHisp, PctTeen2Par, PctImmigRecent, PctImmigRec8, PctImmigRec10, PctNotSpeakEnglWell, OwnOccHiQuart, NumStreet, PctSameState85, LemasSwFTFieldPerPop, LemasTotReqPerPop, RacialMatchCommPol, PolicOperBudg | |

| Relevant features (ridge-based regression) | racePctHisp, PctSameState85 | |

| Relevant features (SDL-test ) | racePctHisp, PctTeen2Par, PctImmigRecent, PctImmigRec8, PctImmigRec10, PctNotSpeakEnglWell, PctHousOccup, OwnOccHiQuart, NumStreet, PctSameState85, LemasSwFTFieldPerPop, LemasTotReqPerPop, RacialMatchCommPol, PolicOperBudg | |

| Relevant features (ridge-based regression) | racePctHisp, PctSameState85 | |

| Relevant features (SDL-test ) | racePctHisp, PctUnemployed, PctTeen2Par, PctImmigRecent, PctImmigRec8, PctImmigRec10, PctNotSpeakEnglWell, PctHousOccup, OwnOccHiQuart, NumStreet, PctSameState85, LemasSwornFT, LemasSwFTFieldPerPop, LemasTotReqPerPop, RacialMatchCommPol, PctPolicWhite | |

| Relevant features (ridge-based regression) | racePctHisp, PctSameState85 | |

7 Proofs

7.1 Proof of Lemma 2.6

Fix , , and assume that the minimum error rate for type II errors in testing hypothesis at significance level is . Further fix arbitrarily small. By definition there exists a statistical test such that for any and for any (with defined as in Definition 2.5). Equivalently:

| (43) | ||||

We now take expectation of these inequalities with respect to (in the first case) and (in the second case) and we get, with the notation introduced in the Definition 2.5,

Call . By assumption, for any test , we have and therefore the last inequalities imply

| (44) | ||||

The thesis follows since is arbitrary.

7.2 Proof of Lemma 2.7

Fix , , , as in the statement and assume, without loss of generality, , and . We take where is the diagonal matrix with if and otherwise. Here and will be chosen later. For the same covariance matrix , we let where is the -th element of the standard basis. Recalling that , and , the support of is in and the support of is in .

Under we have , and under we have . Hence the binary hypothesis testing problem under study reduces to the problem of testing a null hypothesis on the mean of a Gaussian random vector with known covariance against a simple alternative. It is well known that the most powerful test [7, Chapter 8] is obtained by comparing the ratio with a threshold. Equivalently, the most powerful test is of the form

| (45) |

for some that is to be chosen to achieve the desired significance level . Letting

| (46) |

it is a straightforward calculation to drive the power of this test as

where the function is defined as per Eq. (10). Next we show that the power of this test converges to as . Hence the claim is proved by taking for some large enough.

Write

| (47) |

where the second step follows from matrix inversion lemma. Clearly, as , the right hand side of the above equation converges to . Therefore, the power converges to .

7.3 Proof of Theorem 2.3

Let . By Lemma 2.6 and 2.7, we have,

| (48) |

with the taken over measurable functions , and defined as per Eq. (10).

It is easy to check that is concave for any and is non-decreasing for any (see Fig. LABEL:fig:AlphaBeta1d). Further takes values in . Hence

| (49) | ||||

Since and are jointly Gaussian, we have

| (50) |

with independent of . It follows that

| (51) |

with a chi-squared random variable with degrees of freedom. The desired claim follows by taking .

7.4 Proof of Theorem 3.3

Since has a standard distributional limit, the empirical distribution of converges weakly to (with probability one). By the portmanteau theorem, and the fact that , we have

| (52) |

In addition, since is a continuity point of the distribution of , we have

| (53) |

Now, by Eq. (52), . Further, for , as . Therefore, Eq. (53) yields

| (54) |

Hence,

| (55) |

Note that depends on the distribution . Since , using Eq. (54), we have , i.e, is -sparse. Let denote the maximum corresponding to densities in the family of -sparse densities. As shown in [32], , where is defined by Eqs. (22) and (23). Consequently,

| (56) |

Now, we take the expectation of both sides of Eq. (56) with respect to the law of random design and random noise . Changing the order of limit and expectation by applying dominated convergence theorem and using linearity of expectation, we obtain

| (57) |

Since takes values in , we have . The result follows by noting that the columns of are exchangeable and therefore does not depend on .

7.5 Proof of Theorem 4.3

Since the sequence has a standard distributional limit, with probability one the empirical distribution of converges weakly to the distribution of . Therefore, with probability one, the empirical distribution of

converges weakly to . Hence,

| (58) |

Applying the same argument as in the proof of Theorem 3.3, we obtain the following by taking the expectation of both sides of the above equation

| (59) |

In particular, for the standard Gaussian design (cf. Theorem 3.2), since the columns of are exchangeable we get for all .

7.6 Proof of Theorem 4.4

The proof of Theorem 4.4 proceeds along the same lines as the proof of Theorem 3.3. Since has a standard distributional limit, with probability one the empirical distribution of converges weakly to the distribution of . Similar to Eq. (54), we have

| (60) |

Also

| (61) |

Similar to the proof of Theorem 3.3, by taking the expectation of both sides of the above inequality we get

| (62) |

7.7 Proof of Theorem 4.5

In order to prove the claim, we will establish the following (corresponding to the the case of Definition 4.1):

- Claim 1.

-

If solves Eq. (37), then as .

- Claim 2.

-

The empirical distribution of converges weakly to the random vector , with independent of . Namely fixing , bounded Lipschitz, we need to prove

(63) - Claim 3.

-

Recalling , the empirical distribution of converges weakly to .

We will prove these three claims after some preliminary remarks. First notice that, by [59, Theorem 6] (and using assumptions and ) satisfies the restricted eigenvalue property RE of [18] with a -independent constant , almost surely for all large enough. (Indeed Theorem 6 of [59] ensures that this holds with probability at least , and hence almost surely for all large enough by Borel-Cantelli lemma.)

We can therefore apply [18, Theorem 7.2] to conclude that there exists a constant such that, almost surely for all large enough, we have

| (64) | ||||

| (65) | ||||

| (66) | ||||

| (67) |

(Here we used for all large enough.) In particular, from Eq. (67) and assumption , it follows that and hence, almost surely,

| (68) |

7.7.1 Claim 1

By Eq. (68), we can assume for all large enough. By Eq. (37) it is sufficient to show that uniformly for , , for some . Since , and by dominated convergence, we have

| (69) |

It is easy to see that for some constant depending on , . Hence, letting , we conclude that is bounded uniformly in . By Cauchy-Schwarz

| (70) |

It is therefore sufficient to prove that . By definition of , cf. Eq. (35), we have if and only if

| (71) |

Therefore, substituting , we have

| (72) |

The random variables are . Therefore by union bound, since , for , we have

| (73) |

Therefore since , provided , by Eq. (70).

7.7.2 Claim 2

Let . Conditional on , we have

| (74) |

Using the assumption and employing [33, Lemma 7.2], we have, almost surely,

| (75) |

Consequently, we have, for almost every sequence of matrices , letting independent of

| (76) | ||||

| (77) | ||||

| (78) |

(Here, the first identity follows from Eq. (74), the second from Eq. (75) and the Lipschitz continuity of , and the last from assumption , together with the fact that is bounded Lipschitz.)

Next, applying Gaussian isoperimetry [60] to the conditional measure of given (noting that almost surely for all large enough and some constant ), and to the Lipschitz function , we have

| (79) |

almost surely for all large enough. Using Borel-Cantelli lemma, we conclude that, almost surely

| (80) |

Substituting in definition of , we get

| (81) | ||||

| (82) |

where we recall that and we defined

| (83) |

The proof is therefore concluded if we can show that, almost surely,

| (84) |

In order to simplify the notation, and since the last argument plays no role, we let . Without loss of generality we will assume that , and that the Lipschitz modulus of is at most one.

The first term in Eq. (86) vanishes since by assumption , , and therefore

| (87) |

Consider next the third term in Eq. (86):

| (88) |

where the second inequality follows from (65), that holds almost surely for all large enough. Next, using Eq. (68),

| (89) |

Consider next the last term in Eq. (86), and fix arbitrarily small. Since by Eq. (68), almost surely for all large enough, we have

| (90) |

where the last equality follows from Eq. (80), applied to . Finally, letting , we get, by dominated convergence, , and hence

| (91) |

Finally, consider the second term. Fix a partition , where , and . Then

| (92) |

Let . By Eq. (67) we have almost surely for all large enough. Hence, using for all large enough, we get

| (93) |

The operator norm can be upper bounded using the following lemma, whose proof can be found in Appendix G. (See also the conference paper [33] for a similar estimate: we provide a full proof in appendix for the reader’s convenience.)

Lemma 7.1.

Under the assumption of Theorem 4.5, for any constant , there exists

| (94) |

with probability at least for all large enough.

7.7.3 Claim 3

Note that, by definition

| (97) |

Defining , , and , the proof consists in two steps. First, for any Lipschitz bounded function , we have

| (98) |

This is immediate by the law of large numbers, since has i.i.d. entries and by assumption .

Acknowledgements

This work was partially supported by the NSF CAREER award CCF-0743978, and the grants AFOSR FA9550-10-1-0360 and AFOSR/DARPA FA9550-12-1-0411.

Appendix A Effective noise variance

As stated in Theorem 3.4 the unbiased estimator can be regarded –asymptotically– as a noisy version of with noise variance . An explicit formula for is given in [10]. For the reader’s convenience, we explain it here using our notations.

Denote by the soft thresholding function

| (100) |

Further define function as

| (101) |

where and are defined as in Theorem 3.4. Let be the unique non-negative solution of the equation

| (102) |

The effective noise variance is obtained by solving the following two equations for and , restricted to the interval :

| (103) | |||||

| (104) |

Existence and uniqueness of is proved in [10, Proposition 1.3].

Appendix B Tunned regularization parameter

In previous appendix, we provided the value of for a given regularization parameter . In this appendix, we discuss the tuned value for to achieve the power stated in Theorem 3.3.

Let be the family of -sparse distributions. Also denote by the minimax risk of soft thresholding denoiser (at threshold value ) over , i.e.,

| (105) |

The function can be computed explicitly by evaluating the mean square error on the worst case -sparse distribution. A simple calculation gives

| (106) |

Further, let

| (107) |

In words, is the minimax optimal value of threshold over . The value of for Theorem 3.3 is then obtained by solving Eq. (103) for with , and then substituting and in Eq. (104) to get .

Appendix C Statistical power of earlier approaches

In this appendix, we briefly compare our results with those of Zhang and Zhang [16], and Bühlmann [17]. Both of these papers consider deterministic designs under restricted eigenvalue conditions. As a consequence, controlling both type I and type II errors requires a significantly larger value of .

In [16], authors propose low dimensional projection estimator (LDPE ) to assess confidence intervals for the parameters . Following the treatment of [16], a necessary condition for rejecting with non-negligible probability is

| (109) |

which follows immediately from [16, Eq. (23)]. Further and are lower bounded in [16] as follows

| (110) | ||||

| (111) |

where for a standard Gaussian design . Using further which again holds with high probability for standard Gaussian designs, we get the necessary condition

| (112) |

for some constant .

In [17], p-values are defined, in the notation of the present paper, as

| (113) |

with a ‘corrected’ estimate of , cf. [17, Eq. (2.14)]. The corrected estimate is defined by the following motivation. The ridge estimator bias, in general, can be decomposed into two terms. The first term is the estimation bias governed by the regularization, and the second term is the additional projection bias , where denotes the orthogonal projector on the row space of . The corrected estimate is defined in such a way to remove the second bias term under the null hypothesis . Therefore, neglecting the first bias term, we have .

Assuming the corrected estimate to be consistent (which it is in sense under the assumption of the paper), rejecting with non-negligible probability requires

| (114) |

Following [17, Eq. (2.13)] and keeping the dependence on instead of assuming , we have

| (115) |

Further, plugging for we have

| (116) |

For a standard Gaussian design is approximately distributed as , where is a uniformly random vector with . In particular is approximately . A standard calculation yields with high probability. Furthermore, concentrates around . Finally, by definition of (cf. [17, Eq. (2.3)]) and using classical large deviation results about the singular values of a Gaussian matrix, we have with high probability. Hence, a necessary condition for rejecting with non-negligible probability is

| (117) |

as stated in Section 1.

Appendix D Replica method calculation

In this section we outline the replica calculation leading to the Claim 4.6. Indeed we consider an even more general setting, whereby the regularization is replaced by an arbitrary separable penalty. Namely, instead of the Lasso, we consider regularized least squares estimators of the form

| (118) |

with being a convex separable penalty function; namely for a vector , we have , where is a convex function. Important instances from this ensemble of estimators are Ridge-regression (), and the Lasso (). The Replica Claim 4.6 is generalized to the present setting replacing by . The only required modification concerns the definition of the factor . We let be the unique positive solution of the following equation

| (119) |

where denotes the Hessian, which is diagonal since is separable. If is non differentiable, then we formally set for all the coordinates such that is non-differentiable at . It can be checked that this definition is well posed and that yields the previous choice for .

We pass next to establishing the claim. We limit ourselves to the main steps, since analogous calculations can be found in several earlier works [40, 41, 48]. For a general introduction to the method and its motivation we refer to [61, 62]. Also, for the sake of simplicity, we shall focus on characterizing the asymptotic distribution of , cf. Eq. (28). The distribution of is derived by the same approach.

Fix a sequence of instances . For the sake of simplicity, we assume and (the slightly more general case and does not require any change to the derivation given here, but is more cumbersome notationally). Fix a continuous function convex in its first argument, and let be its Lagrange dual. The replica calculation aims at estimating the following moment generating function (partition function)

| (120) |

Here are i.i.d. pairs distributed as per model (1) and with to be defined below. Further, is a continuous function strictly convex in its first argument. Finally, and is a ‘temperature’ parameter not to be confused with the type II error rate as used in the main text. We will eventually show that the appropriate choice of is given by Eq. (119).

Within the replica method, it is assumed that the limits , exist almost surely for the quantity , and that the order of the limits can be exchanged. We therefore define

| (121) | |||||

| (122) |

In other words is the exponential growth rate of . It is also assumed that concentrates tightly around its expectation so that can in fact be evaluated by computing

| (123) |

where expectation is being taken with respect to the distribution of . Notice that, by Eq. (122) and using Laplace method in the integral (120), we have

| (124) |

Finally we assume that the derivative of as can be obtained by differentiating inside the limit. This condition holds, for instance, if the cost function is strongly convex at . We get

| (125) |

where and is the minimizer of the regularized least squares as per Eq. (4). Since, by duality , we get

| (126) |

Hence, by computing using Eq. (123) for a complete set of functions , we get access to the corresponding limit quantities (126) and hence, via standard weak convergence arguments, to the joint empirical distribution of the triple , cf. Eq. (29).

In order to carry out the calculation of , we begin by rewriting the partition function (120) in a more convenient form. Using the definition of and after a simple manipulation

| (127) |

Define the measure over as follows

| (128) |

Using this definition and with the change of variable , we can rewrite Eq. (127) as

| (129) |

where denotes the standard Gaussian measure on : .

The replica method aims at computing the expected log-partition function, cf. Eq. (123) using the identity

| (130) |

This formula would require computing fractional moments of as . The replica method consists in a prescription that allows to compute a formal expression for the integer, and then extrapolate it as . Crucially, the limit is inverted with the one :

| (131) |

In order to represent , we use the identity

| (132) |

In order to apply this formula to Eq. (129), we let, with a slight abuse of notation, be a measure over , with . Analogously , with . With these notations, we have

| (133) |

In the above expression denotes expectation with respect to the noise vector , and the design matrix . Further, we used to denote matrix scalar product as well: .

At this point we can take the expectation with respect to , . We use the fact that, for any ,

| (134) |