Loss of regularity for Kolmogorov equations

Abstract

The celebrated Hörmander condition is a sufficient (and nearly necessary) condition for a second-order linear Kolmogorov partial differential equation (PDE) with smooth coefficients to be hypoelliptic. As a consequence, the solutions of Kolmogorov PDEs are smooth at all positive times if the coefficients of the PDE are smooth and satisfy Hörmander’s condition even if the initial function is only continuous but not differentiable. First-order linear Kolmogorov PDEs with smooth coefficients do not have this smoothing effect but at least preserve regularity in the sense that solutions are smooth if their initial functions are smooth. In this article, we consider the intermediate regime of nonhypoelliptic second-order Kolmogorov PDEs with smooth coefficients. The main observation of this article is that there exist counterexamples to regularity preservation in that case. More precisely, we give an example of a second-order linear Kolmogorov PDE with globally bounded and smooth coefficients and a smooth initial function with compact support such that the unique globally bounded viscosity solution of the PDE is not even locally Hölder continuous. From the perspective of probability theory, the existence of this example PDE has the consequence that there exists a stochastic differential equation (SDE) with globally bounded and smooth coefficients and a smooth function with compact support which is mapped by the corresponding transition semigroup to a function which is not locally Hölder continuous. In other words, degenerate noise can have a roughening effect. A further implication of this loss of regularity phenomenon is that numerical approximations may converge without any arbitrarily small polynomial rate of convergence to the true solution of the SDE. More precisely, we prove for an example SDE with globally bounded and smooth coefficients that the standard Euler approximations converge to the exact solution of the SDE in the strong and numerically weak sense, but at a rate that is slower then any power law.

doi:

10.1214/13-AOP838keywords:

[class=AMS]keywords:

, and T1Supported by EPSRC, the Royal Society and by the Leverhulme Trust. T2Supported by the research project “Numerical approximation of stochastic differential equations with non-globally Lipschitz continuous coeffcients”. T3Supported by the research project “Numerical solutions of stochastic differential equations with non-globally Lipschitz continuous coeffcients”.

35B65, Kolmogorov equation, loss of regularity, roughening effect, smoothing effect, hypoellipticity, Hormander condition, viscosity solution, degenerate noise, nonglobally Lipschitz continuous

1 Introduction and main results

The key observation of this article is to reveal the phenomenon of loss of regularity in Kolmogorov partial differential equations (PDEs). This observation has a direct consequence on the literature on regularity analysis of linear PDEs, on the literature on regularity analysis of stochastic differential equations (SDEs) and on the literature on numerical approximations of SDEs. We will illustrate the implications for each field separately.

Regularity analysis of linear partial differential equations. For some , let and be smooth functions such that there exists a real number such that and for all . (Here and below, we write and for the Euclidean scalar product and norm on .) Let furthermore be a globally bounded and continuous function and consider the second-order PDE

for . The PDE (1) is referred to as Kolmogorov equation in the literature (see, e.g., Cerrai Cerrai2001 , Da Prato DaPrato2004 , Röckner Roeckner1999 and Röckner and Sobol RoecknerSobol2006 ; it is also referred to as Kolmogorov backward equation or Kolmogorov PDE, see, e.g., Da Prato and Zabczyk dz02b , Øksendal Oeksendal2000 ). It has a strong link to probability theory and appeared first (in a slightly different form; see display (125) in Kolmogorov1931 ) in Kolmogorov’s celebrated paper Kolmogorov1931 . Corollary 4.17 in Section 4 below implies that the PDE (1) admits a unique globally bounded viscosity solution. More precisely, Corollary 4.17 proves that there exists a unique globally bounded continuous function such that is a viscosity solution of (1) and such that for all . In this article, we are interested to know whether solutions of the PDE (1) preserve regularity in the sense that is smooth if the initial function is smooth. In particular, we will answer the question whether smoothness and global boundedness of the initial function implies the existence of a classical solution of the PDE (1).

In the case of first-order Kolmogorov PDEs with smooth coefficients, that is, in (1), regularity preservation of solutions of (1) is well known. More precisely, if for all and if the initial function in (1) is smooth, then it is well known that there exists a unique smooth classical solution of (1). In this sense, the PDE (1) is regularity preserving in the purely first-order case . In the second-order case , the situation may be even better in the sense that the PDE (1) often has a smoothing effect. More precisely, if the PDE (1) is hypoelliptic, then by definition solutions of the PDE (1) are smooth in the sense that is infinitely often differentiable even if the initial function is only continuous but not differentiable. In the seminal paper Hoermander1967 , Hörmander gave a sufficient (and also nearly necessary; see the discussion before Theorem 1.1 in Hoermander1967 and Section 2 in Hairer Hairer2011 ) condition for (1) to be hypoelliptic; see Theorem 1.1 in Hoermander1967 . To formulate Hörmander’s condition, set for all . Then the Hörmander condition is fulfilled if

| (2) | |||

for all where denotes the Lie bracket of two smooth vector fields . Consequently, if Hörmander’s condition (1) is satisfied, then the PDE (1) admits a unique globally bounded smooth classical solution even if the initial function is assumed to be continuous and globally bounded only. Clearly, there are many cases where the Hörmander condition (1) fails to be fulfilled and where (1) is not hypoelliptic, for example, if . Next, we point out that if all derivatives of the drift coefficient , of the diffusion coefficient and of the initial function are globally bounded ( and are then, in particular, globally Lipschitz continuous), then smoothness of the solution of the PDE (1) is known even in the nonhypoelliptic case (see, e.g., Theorem 4.32 in Krylov Krylov1999 for twice differentiability of the solution; infinitely often differentiability of the solution follows analogously as in the proof of Theorem 4.32 in Krylov Krylov1999 ). Obviously, there are many cases where and are not both globally Lipschitz continuous, for example, when is a polynomial with a degree greater or equal (see, e.g., Section 4 in HutzenthalerJentzen2014Memoires for a list of examples). To the best of our knowledge, regularity of solutions of the PDE (1) is in general unknown in the nonhypoelliptic case if and if and are not both globally Lipschitz continuous.

In this article, we address the question whether second-order linear PDEs with smooth coefficients of the form (1) at least preserve regularity in the nonhypoelliptic case. The following Theorem 1.1 answers this question to the negative. More precisely, the key observation of this article is to reveal the phenomenon of loss of regularity in the sense that the solution of the PDE (1) starting with a smooth compactly supported function may turn into a nondifferentiable function for every positive time . In analogy to the well-known “smoothing effect” in the hypoelliptic case, we will say in the case of loss of regularity that the PDE (1) has a roughening effect. Here is a simple two-dimensional example with polynomial and linear which has this roughening effect. In the special case and and for all , the PDE (1) reads as

| (3) |

for . Theorem 2.1 and Corollary 4.17 below imply that there exists an infinitely often differentiable function with compact support such that the unique globally bounded viscosity solution to (3) with has the property that is not differentiable and not locally Lipschitz continuous. In particular, we thereby disprove the existence of a globally bounded classical solution of the PDE (3) with . Note that the drift coefficient of the PDE (3) grows superlinearly. One could wonder whether the roughening effect of example (3) is due to this superlinear growth of . To exclude this possibility, we prove for an example PDE with globally bounded and smooth coefficients that there exists a smooth initial function with compact support such that the solution is not even locally Hölder continuous; see Theorem 1.1 below. In particular, Theorem 1.1 implies that, in general, the PDE (1) does not have a classical solution even if the coefficients and the initial function are globally bounded and infinitely often differentiable.

Theorem 1.1 ((Disprove of the existence of classical solutions of the Kolmogorov PDE with smooth and globally bounded coefficients and initial function)).

There exists a natural number , a globally bounded and infinitely often differentiable function , a symmetric nonnegative matrix and an infinitely often differentiable function with compact support such that there exists no globally bounded classical solution of the PDE

for . In addition, there exists a unique globally bounded viscosity solution of (1.1) and this function fails to be locally Hölder continuous.

Theorem 1.1 follows immediately from Corollary 4.17 in Section 4 and from Theorem 3.1 in Section 3. More precisely, Corollary 4.17 and Theorem 3.1 imply that there exists an infinitely differentiable function with compact support such that the unique globally bounded viscosity solution of the PDE

| (5) |

with initial condition for is not locally Hölder continuous. In particular, the PDE (5) with has no globally bounded classical solution. The PDE (5) has a globally bounded and highly oscillating drift coefficient and a constant diffusion coefficient and serves as a counterexample to regularity preservation for Kolmogorov PDEs. An SDE with a globally bounded and highly oscillating diffusion coefficient and a vanishing drift coefficient has been presented in Li and Scheutzow LiScheutzow2011 as a counterexample for strong completeness of SDEs. Another interesting observation is that the PDE (5) without the second-order term on the right-hand side of (5) preserves regularity and has a smooth classical solution and that the PDE (5) without the first-order term on the right-hand side of (5) also preserves regularity and has a smooth classical solution. Thus, the roughening effect of the PDE (5) is a consequence of the interplay between the first-order and the second-order term in (5). We add that Theorem 3.4 in Section 3 is a stronger version of Theorem 1.1 in which the roughening effect appears on every arbitrarily small open subset of the state space; see Section 3 and also Theorem 1.2 below for more details. Note that in both counterexamples to regularity preservation [PDE (5) and PDE (3)] it does not hold that all derivatives of and are globally bounded. Indeed, in both counterexamples the drift coefficient is not globally Lipschitz continuous. As observed above, regularity preservation is known if all derivatives of and are globally bounded. Moreover, note that the coefficients in our counterexample PDE (5) are analytic functions and that the initial function may be chosen to be analytic (see Theorem 3.1 for details). We emphasize that this does not contradict the classical Cauchy–Kovalevskaya theorem (e.g., Theorem 4.6.2 in Evans Evans2010 ) proving existence, uniqueness and analyticity of solutions of PDEs with analytic coefficients as the Cauchy–Kovalevskaya theorem applies to (1.1) in the case only. Moreover, we would like to point out that Theorem 1.1 does not contradict to Theorems 7.1.3, 7.1.4 and 7.1.7 in Evans Evans2010 , which show the existence of a unique classical solution of (1.1) if is strictly positive [note that in (5) is nonnegative but not strictly positive].

Theorem 1.1 shows that a general existence theorem for globally bounded classical solutions of the PDE (1) cannot be established. However, it is possible to ensure the existence of a viscosity solution of the PDE (1) under rather general assumptions on the coefficients. More precisely, one of our main results, Theorem 4.16 below, establishes the existence of a within a certain class unique viscosity solution for every second-order linear Kolmogorov PDE whose coefficients are locally Lipschitz continuous and satisfy the Lyapunov-type inequality (111). To the best of our knowledge, this is the first result in the literature proving existence and uniqueness of solutions of the Kolmogorov PDE (1) in the above generality; see also the discussion after Theorem 4.16 for a short review of existence and uniqueness results for Kolmogorov PDEs. A crucial result on the route to Theorem 4.16 is the uniqueness result of Corollary 4.14 for viscosity solutions of degenerate parabolic second-order linear PDEs.

The roughening effect of the PDE (1) revealed in this first paragraph of this Introduction has a direct consequence on the literature on regularity analysis of SDEs. This is the subject of the next paragraph.

Regularity analysis of stochastic differential equations. For the rest of this Introduction, we use the following notation. Let be an arbitrary probability space with a normal filtration which supports a standard -Brownian motion with continuous sample paths. It is a classical result that the above assumptions on and ensure the existence of a family , , of up to indistinguishability unique solution processes (see, e.g., Theorem 3.1.1 in PrevotRoeckner2007 ) with continuous sample paths of the SDE

| (6) |

for and and with for all (see, e.g., Theorem 1 in Krylov Krylov1990 ). Here, the function is the infinitesimal mean and the function is the infinitesimal covariance matrix of the SDE (6). It is also well known that the coercivity assumption on and the linear growth bound on additionally imply moment bounds for all for the solution processes of the SDE (6). The transition semigroup , of the SDE (6) is defined by for all , and all where is as usual the space of globally bounded and continuous functions from to . Note for every that the function is continuous (see, e.g., Theorem 1.7 in Krylov Krylov1999 ) and hence, the semigroup is well defined. Observe also that the function is continuous for every although the SDE (6) is, in general, not strongly complete; see Li and Scheutzow LiScheutzow2011 and see, for example, also Elworthy Elworthy1978 , Kunita Kunita1990 and Fang, Imkeller and Zhang FangImkellerZhang2007 for further results on strong completeness of SDEs.

Theorem 1.1 in Hörmander Hoermander1967 and Proposition 4.18 below imply that if the Hörmander condition (1) is fulfilled, then the semigroup is smoothing in the sense that for all . To the best of our knowledge, it remained an open question in the nonhypoelliptic case whether SDEs with infinitely often differentiable coefficients such as (6) in general preserve regularity in the sense that for all . This article answers this question to the negative. More precisely, the following theorem reveals that smooth functions with compact support may be mapped to nonsmooth functions by the transition semigroup of the SDE (6). In analogy to the well-known “smoothing effect” of many SDEs, we will say that the semigroup has a roughening effect in that case. Here is a simple two-dimensional example SDE with polynomial drift coefficient and linear diffusion coefficient which has this roughening effect. In the special case , and and for all , the SDE (6) reads as

for and . Observe that (3) is the Kolmogorov PDE of (1); see Corollary 4.17 for details. Moreover, note that for all in this example. Thus, the solution process of the associated ordinary differential equation stays on the circle centered at going through the starting point. Theorem 2.1 in Section 2 shows for the SDE (1) that there exists an infinitely often differentiable function with compact support such for every the functions and are continuous but not differentiable and not locally Lipschitz continuous. For every , we hence have the roughening effect in the case of the SDE (1). The drift coefficient of the SDE (1) grows superlinearly. As above, the superlinear growth of is not necessary for the transition semigroup of the SDE to be roughening. This is subject of the next main result of this article.

Theorem 1.2 ((A counterexample to regularity preservation with degenerate additive noise)).

There exists a natural number , a globally bounded and infinitely often differentiable function and a constant function , that is for all , with the following properties. For every the function is continuous but nowhere locally Hölder continuous and for every nonempty open set there exists an infinitely often differentiable function with compact support such that the function is continuous but not locally Hölder continuous. In particular, for every we have .

Theorem 1.2 follows immediately from Theorem 3.4 in Section 3. The roughening effect of some SDEs with smooth coefficients revealed through example (1) and Theorem 1.2 above, has a direct consequence on the literature on numerical approximations of SDEs. This is the subject of the next paragraph.

Numerical approximations of stochastic differential equations. Starting with Maruyama’s adaptation of Euler’s method to SDEs in 1955 (see m55 ), an extensive literature on the numerical approximation of solutions of SDEs has been published in the last six decades; see, for example, the books and overview articles kp92 , kps94 , m95 , g02 , BurrageEtAl2004 , mt04 , mr08 , jk09d , KloedenNeuenkirch2013 for extensive lists of references. A key objective in this field of research is to prove convergence of suitable numerical approximation processes to the solution process of the SDE and to establish a rate of convergence for the considered approximation scheme in the strong, in the almost sure or in the numerically weak sense.

Almost sure convergence rates of many numerical schemes such as the standard Euler method or the higher-order Milstein method are well known for the SDE (6) and even for a much larger class of nonlinear SDEs; see Gyöngy g98b and Jentzen, Kloeden and Neuenkirch jkn09a . Many applications, however, require the numerical approximation of moments or other functionals of the solution process, for instance, the expected pay-off of an option in computational finance; see, for example, Glasserman g04 for details. For this reason, applications are particularly interested in strong and numerically weak convergence rates. The vast majority of research results establishing strong and numerically weak convergence rates assume that the coefficients of the SDE are globally Lipschitz continuous or at least that they satisfy the global monotonicity condition that there exists a real number such that for all (see, e.g., Theorem 2.4 in Hu h96 , Theorem 5.3 in Higham, Mao and Stuart hms02 , Schurz Schurz2006 , Theorems 2 and 3 in Higham and Kloeden hk07 , Theorem 6.3 in Mao and Szpruch MaoSzpruch2013Rate , Theorem 1.1 in Hutzenthaler, Jentzen and Kloeden HutzenthalerJentzenKloeden2012 , Theorem 3.2 in Wang and Gan WangGan2013 ). Strong and numerically weak convergence rates without assuming global monotonicity are established in Gyöngy and Rásonyi GyoengyRasonyi2011 in the case of a class of scalar SDEs with globally Hölder continuous coefficients, in Dörsek Doersek2012 in the case of the two-dimensional stochastic Navier–Stokes equations and in Dereich, Neuenkirch and Szpruch DereichNeuenkirchSzpruch2012 , Alfonsi Alfonsi2012 , Neuenkirch and Szpruch NeuenkirchSzpruch2012 in the case of a class of scalar SDEs (including, e.g., the Cox–Ingersoll–Ross process) that can be transformed in a suitable sense to SDEs that satisfy the global monotonicity assumption. The global monotonicity assumption is a serious restriction on the coefficients of the SDE and excludes many interesting SDEs in the literature (e.g., stochastic Lorenz equations, stochastic Duffing–van der Pol oscillators and the stochastic SIR model; see Section 4 in HutzenthalerJentzen2014Memoires for details and further examples). It remains an open problem to establish strong and numerically weak convergence rates in the general setting of the SDE (6).

In this article, we establish in the setting (6) the existence of an SDE with globally bounded and infinitely often differentiable coefficients for which the Euler approximations converge in the strong and in the numerically weak sense without any arbitrarily small polynomial rate of convergence. More precisely, our main result for the literature on the numerical approximation of SDEs is the following theorem.

Theorem 1.3 ((A counterexample to the rate of convergence in the numerical approximation of nonlinear SDEs with additive noise)).

Let and be arbitrary. Then there exists a globally bounded and infinitely often differentiable function and a symmetric nonnegative matrix such that the stochastic process with continuous sample paths satisfying for all and its Euler–Maruyama approximations , , satisfying and for all , , fulfill that

| (8) | |||

for all . In particular, for every there exists no real number such that for all .

Theorem 1.3 follows immediately from Theorem 5.1 in Section 5. In the deterministic case , it is well known that the Euler approximations converge to the solution process of (6) with the rate . In the stochastic case , this rate of convergence can often not be achieved. In particular, Clark and Cameron ClarkCameron1980 proved for an SDE in the setting of (6) that a class of Euler-type schemes cannot, in general, converge strongly with a higher-order than . Since then, there have been many results on lower bounds of strong and numerically weak approximation errors for numerical approximation schemes of SDEs; see, for example, Ruemelin1982 , CambanisHu1996 , hmr00a , hmr00b , dg01 , m02 , mr07a , mr08 , hjk11 , Kruse2011 and the references therein. Now the observation of Theorem 1.3 is that there exist SDEs with smooth and globally bounded coefficients for which the standard Euler approximations converge in the strong and numerically weak sense without any arbitrarily small polynomial rate of convergence. To the best of our knowledge, Theorem 1.3 is the first result in the literature in which it has been established that Euler’s method converges to the solution of an SDE with smooth coefficients in the strong and numerical weak sense without any arbitrarily small polynomial rate of convergence. Clearly, this lack of a rate of convergence is not a special property of the Euler scheme and holds for other schemes such as the Milstein scheme, too. It is based on the fact that our counterexample SDE for Theorem 1.3 [see (5)] suffers under the roughening effect revealed in Theorems 1.1 and 1.2 (see Corollary 5.2 and Theorem 5.1 in Section 5 for details).

Comparing Theorem 5.1 with Theorem 2.4 in Gyöngy g98b reveals the remarkable difference that the Euler approximations for some SDEs have almost sure convergence rate but no strong and no numerically weak rate of convergence. More formally, Theorem 2.4 in g98b shows in the setting of Theorem 1.3 that there exist finite random variables , , such that , -a.s. for all and all . Taking expectation then results in for all and all and from Theorem 1.3 we hence get that the error constants have infinite expectations, that is, for all . In addition, we refer to Theorem 2.3 in Milstein and Tretyakov mt05 for a weak convergence result restricted to certain subevents of the probability space. Finally, we emphasize that Monte Carlo simulations confirm the slow strong and numerically weak convergence phenomenon of Euler’s method revealed in Theorem 1.3. For details, the reader is referred to Figure 1 in Section 5 below.

2 Counterexamples to regularity preservation with linear multiplicative noise

In this section, we establish the phenomenon of loss of regularity of the simple example SDE (1) with polynomial drift coefficient and linear diffusion coefficient. For this, we consider the following setting. Let be a probability space with a normal filtration , let be a one-dimensional standard -Brownian motion with continuous sample paths and let , , be the up to indistinguishability unique solution processes with continuous sample paths of the SDE

for and satisfying for all . Corollary 2.6 in Gyöngy and Krylov GyoengyKrylov1996 ensures that the processes , , do indeed exist. The following Theorem 2.1 shows that the semigroup associated with the SDE (2) loses regularity in the sense that there exists an infinitely often differentiable function with compact support, which is mapped to a nonsmooth function by the semigroup.

Theorem 2.1 ((A counterexample to regularity preservation with linear multiplicative noise)).

Let , , be solution processes of the SDE (2) with continuous sample paths and with for all . Then for all and there exists an infinitely often differentiable function with compact support such that for every the mappings , and are continuous but not locally Lipschitz continuous and not differentiable.

The proof of Theorem 2.1 is deferred to the end of this section. The proof of Theorem 2.1 uses the following simple lemma.

Lemma 2.2 ((Restricted exponential integrals of a geometric Brownian motion)).

Let be a probability space and let be a one-dimensional standard Brownian motion with continuous sample paths. Then

| (10) |

for all with .

Independence of from for all implies

| (11) | |||

for all with where we used Jensen’s inequality and convexity of the exponential function in the last step. The time integrated Brownian bridge on the right-hand side of (2) is normally distributed with mean and variance

| (12) | |||

for every . As the double exponential normal distribution has infinite mean, we conclude that the right-hand side of (2) is infinite for all . This finishes the proof Lemma 2.2.

The proof of the following Lemma 2.3 makes use of Lemma 2.2. Using Lemma 2.3, the proof of Theorem 2.1 is then completed at the end of this section.

Lemma 2.3.

Let , , be solution processes of the SDE (2) with continuous sample paths and with for all . Then for all and

| (13) | |||

for all and there exists an infinitely often differentiable function with compact support such that for all .

The global Lipschitz continuity of , the local Lipschitz continuity of and for all imply that

for all . Next, we disprove local Lipschitz continuity of the mapping for every . More precisely, aiming at a contradiction, we assume that the second equality in (2.3) is false. Then there exist positive real numbers and a sequence of real numbers , , such that and such that . Theorem 1.7 in KrylovKrylov1999 (see also Proposition 3.2.1 in Prévôt and Röckner PrevotRoeckner2007 ) yields that in probability as . Hence, there exists a strictly increasing sequence , , of natural numbers such that , -a.s.; see, for example, Corollary 6.13 in Klenke Klenke2008 . Applying this, Fatou’s lemma and Lemma 2.2 implies

This contradiction implies that the second equality in (2.3) is true. The first equality in (2.3) follows from the second equality in (2.3) as for all and all . In the next step, let be an arbitrary fixed real number and let and be two infinitely often differentiable functions with for all , with for all and with and for all . Due to partition of unity, such functions indeed exist. Next, let be given by for all . Note that is an infinitely often differentiable function with compact support. We now show that for all . Aiming at a contradiction, assume that there exist positive real numbers and a sequence , , such that and such that

| (15) |

Theorem 1.7 in Krylov Krylov1999 yields that in probability as . Hence, there exists a strictly increasing sequence , , of natural numbers such that , -a.s.; see, for example, Corollary 6.13 in Klenke Klenke2008 . Applying this, the fact for all and all , Fatou’s lemma and Lemma 2.2 then results in

This contradiction implies that for all . The proof of Lemma 2.3 is thus completed.

Proof of Theorem 2.1 Theorem 1.7 in Krylov Krylov1999 (see also Proposition 3.2.1 in Prévôt and Röckner PrevotRoeckner2007 ), in particular, shows for every that the mapping

| (17) |

is continuous. This implies for every and every that the mapping is continuous. Moreover, Lemma 2.3 proves that for all . Combining this, (17), Corollary 6.21 in Klenke Klenke2008 and Theorem 6.25 in Klenke Klenke2008 shows for every that the mappings and are continuous. Furthermore, Lemma 2.3 implies that there exists an infinitely often differentiable function with compact support such that for every the mappings , and are not locally Lipschitz continuous and not differentiable. The proof of Theorem 2.1 is thus completed.

In the remainder of this section, we briefly consider slightly modified versions of the SDE (2). The generator of the SDE (2) is nowhere elliptic. We remark that the phenomenon of loss of regularity may also appear for an SDE whose generator is in many points of the state space elliptic. For example, let be a probability space with a normal filtration , let be a two-dimensional standard -Brownian motion and let , , be the up to indistinguishability unique solution processes with continuous sample paths of the SDE

for and satisfying for all . The generator of the SDE (2) is in every point with elliptic but there exists a function such that for every the functions and are not locally Lipschitz continuous. The proof of this statement is completely analogous as in the case of the SDE (2). Furthermore, the same statement holds if the two independent standard Brownian motion in (2) are replaced by one and the same standard Brownian motion. More precisely, if is a probability space with a normal filtration and if is a one-dimensional standard -Brownian motion, then the up to indistinguishability unique solution processes , , of the SDE

| (19) |

for and with continuous sample paths and with for all fulfill that there exists a function such that for every the functions and are not locally Lipschitz continuous.

3 Counterexamples to regularity preservation with degenerate additive noise

In this section, we show the roughening effect for an example SDE with globally bounded and infinitely often differentiable coefficients. For this, it suffices to consider the following counterexample to regularity preservation. Let be a probability space, let be a one-dimensional standard Brownian motion and let , , be the up to indistinguishability unique solution processes with continuous sample paths of the SDE

| (20) | |||||

for and satisfying for all . Observe that

| (21) |

-a.s. for all and all .

Theorem 3.1 ((A counterexample to regularity preservation with degenerate additive noise)).

Let and let , , be solution processes of the SDE (3) satisfying for all . Then there exists an infinitely often differentiable function with compact support such that for every the functions and are continuous but not locally Hölder continuous.

In the following, regularity properties of the solution processes , , of the SDE (3) are investigated in order to prove Theorem 3.1. To do so, we first establish a few auxiliary results. We begin with a simple lemma on trigonometric integrals.

Lemma 3.2.

Let be real numbers with , let be a continuously differentiable function and let be a twice continuously differentiable function with and with , and for all . Then .

First, assume w.l.o.g. that (otherwise we have for all , and hence ). Moreover, assume w.l.o.g. that for all (otherwise consider where and observe that ). In particular, is strictly increasing and there exists a unique strictly increasing continuous function with for all and with and for all . Integration by substitution and integration by parts therefore imply

| (22) | |||

This completes the proof of Lemma 3.2.

The next lemma analyzes suitable regularity properties of the solution processes , , of the SDE (3). Its proof is based on Lemma 3.2.

Lemma 3.3 ((A lower bound)).

Let be a probability space and let be a one-dimensional standard Brownian motion. Then

| (23) |

for all , and all and

| (24) | |||

for all , , and all bounded and Borel measurable sets .

First of all, define a family ,, of functions by

| (25) |

for all , , and all . Observe that

| (26) |

and

| (27) |

for all , , and all . In addition, note that for all , and all . We can thus apply Lemma 3.2 to obtain that

| (28) |

for all , and all . This implies

| (29) | |||

for all , and all . Moreover, Lemma 22.2 in Klenke Klenke2008 yields

| (30) |

for all . Combining this and inequality (3) then shows

for all , and all and the estimate for all therefore results in the first inequality in (23). Next, the first inequality in (23) implies

| (32) | |||

for all , , with and all bounded and Borel measurable sets . Hence, we get

| (33) | |||

for all , , and all bounded and Borel measurable sets . This completes the proof of Lemma 3.3.

We are now ready to prove Theorem 3.1 stated at the beginning of this section. Its proof uses the lower bound established in Lemma 3.3 above.

Proof of Theorem 3.1 First of all, note that (21) and Lemma 3.3 imply that

| (34) | |||

for all . We hence get for every that the function is not locally Hölder continuous. Moreover, let be an infinitely often differentiable function with compact support and with for all and let be a function given by for all . Again (21) and Lemma 3.3 then show

| (35) | |||

for all . The proof of Theorem 3.1 is thus completed.

In the remainder of this section, we briefly consider a slightly modified version of the SDE (3). More formally, let be a family of sets defined by and by for all . Then let and be given by

for all . Note that is infinitely often differentiable and globally bounded by . Moreover, let be a probability space, let be a one-dimensional standard Brownian motion and let , , be the up to indistinguishability unique solution processes with continuous sample paths of the SDE

| (37) |

for and satisfying for all . The following Theorem 3.4 establishes that the function is nowhere locally Hölder continuous. Its proof is a straightforward consequence of Lemma 3.3 and, therefore, omitted.

Theorem 3.4 ((A further counterexample to regularity preservation with degenerate additive noise)).

Let and let , , be solution processes of the SDE (37) with continuous sample paths and with for all . Then for every and every nonempty open set , the function is continuous but not locally Hölder continuous. Moreover, there exists an infinitely often differentiable function with compact support such that for every and every nonempty open set the function is continuous but not locally Hölder continuous.

4 Solutions of Kolmogorov equations

If the transition semigroup associated with an SDE is smooth, then it satisfies the Kolmogorov equation (which is a second-order linear PDE) corresponding to the SDE in the classical sense. The transition semigroups in our counterexamples are, however, not locally Lipschitz continuous and are therefore no classical solutions of the Kolmogorov equations of the corresponding SDEs. The purpose of this section is to verify that the nonsmooth transition semigroup associated with such an SDE still satisfies the Kolmogorov equation but in a certain weak sense. More precisely, in Section 4.4, we show that the transition semigroups in our counterexamples are viscosity solutions of the associated Kolmogorov equations. Moreover, in Section 4.5, we show that the transition semigroups in our counterexamples are solutions of the associated Kolmogorov equations in the distributional sense. Throughout this section, the notation and is used.

4.1 Definition and basic properties of viscosity solutions

Viscosity solutions were first introduced in Crandall and Lions CrandallLions1983 (see also Evans1978 , Evans1980 , CrandallLions1981 ). The name viscosity solution is due to the method of vanishing viscosity; see the discussion in Section 10.1 in Evans Evans2010 . For a review of the theory and for more references, we refer the reader to the well-known users’s guide Crandall, Ishii and Lions CrandallIshiiLions1992 .

For , we denote by the set of all symmetric -matrices. Moreover, for and we write in the following if for all . Furthermore, for and an open set we call a function degenerate elliptic (see, e.g., (0.3) in Crandall, Ishii and Lions CrandallIshiiLions1992 ) if for all , , and all with . For convenience of the reader, we recall the definition of a viscosity solution (see, e.g., Section 2 in Crandall, Ishii and Lions CrandallIshiiLions1992 and also Definition 1.2 in Appendix C in Peng Peng2010 ).

Definition 4.1 ((Viscosity solution)).

Let , let be an open set and let be a degenerate elliptic function. A function is said to be a viscosity subsolution of (or, equivalently, a viscosity solution of ) if is upper semicontinuous and if it holds for all and all with and that

| (38) |

Similarly, a function is said to be a viscosity supersolution of (or, equivalently, a viscosity solution of ) if is lower semicontinuous and if it holds for all and all with and that

| (39) |

Finally, a function is said to be a viscosity solution of if is both a viscosity subsolution and a viscosity supersolution of .

In the proof of Corollary 4.11 below, the following elementary lemma (Lemma 4.2) is used. The proof of Lemma 4.2 is clear and, therefore, omitted.

Lemma 4.2 ((Sign changes of viscosity solutions)).

Let , let be an open set, let be a degenerate elliptic function and let be a viscosity solution of . Then the function defined by for all is degenerate elliptic and the function is a viscosity solution of . The corresponding statement holds for viscosity solutions of and , respectively.

Above in Definition 4.1, the concept of viscosity solutions is presented via suitable test functions. An alternative instrument to characterize viscosity solutions are so-called semijets (see, e.g., Definition 2.2 in Crandall, Ishii and Lions CrandallIshiiLions1992 ). They are recalled in the next definition.

Definition 4.3 ((Second-order semijets)).

Let , let be an open set and let be a function. Then we define functions , , and by

and

for all .

The next lemma (Lemma 4.4), which is essentially one of the statements in Remark 2.3 in Crandall, Ishii and Lions CrandallIshiiLions1992 , illustrates the relationship between semijets in the sense of Definition 4.3 and suitable test functions in the sense of Definition 4.1.

Lemma 4.4 ((Properties of semijets)).

Let , let be an open set and let be a function. Then

and

for all .

The next corollary, which is essentially one of the statements in Remark 2.3 in Crandall, Ishii and Lions CrandallIshiiLions1992 , is an immediate consequence of Lemma 4.4 above.

Corollary 4.5 ((Characterizations of viscosity solutions)).

Let , let be an open set, let be a degenerate elliptic function and let be an upper semicontinuous function. Then the following three assertions are equivalent:

-

•

is a viscosity subsolution of ( is a viscosity solution of ),

-

•

for every and every it holds that ,

-

•

for every and every it holds that .

The corresponding statement holds for viscosity supersolutions and viscosity solutions.

The next corollary, which is Remark 2.4 in Crandall, Ishii and Lions CrandallIshiiLions1992 , illustrates a further characterization of viscosity solutions under the assumption that is continuous. It follows immediately from Corollary 4.5 and from the semicontinuity of .

Corollary 4.6 ((Characterizations of viscosity solutions for semicontinuous left-hand sides)).

Let , let be an open set, let be a degenerate elliptic and lower semicontinuous function and let be an upper semicontinuous function. Then is a viscosity solution of if and only if it holds for every and every that . The corresponding statement holds for viscosity solutions of and , respectively.

The next well-known remark (see, e.g., Section 2 in Crandall, Ishii and Lions CrandallIshiiLions1992 ) illustrates that classical solutions are viscosity solutions. We will use it in the proof of Lemma 4.15 below.

Remark 4.1 ((Classical solutions are viscosity solutions)).

Let , let be an open set, let be a degenerate elliptic function and let be a classical subsolution of , that is, suppose that

| (42) |

for all . Then is also a viscosity subsolution of . Indeed, for every and every it holds that and and, therefore,

due to (42) and due to the degenerate ellipticity assumption on . The corresponding statement holds for classical supersolutions and classical solutions of .

For the convenience of the reader, we also state a special case of Theorem 3.2 in Crandall, Ishii and Lions CrandallIshiiLions1992 in the next lemma. It will be used in the proof of Lemma 4.10 below.

Lemma 4.7 ((Construction of suitable semijets)).

Let , , let be an open set, let , let , , be upper semicontinuous functions and let be a local maximum point of the function . Then there exist matrices such that for all it holds that and such that

4.2 An approximation result for viscosity solutions

The following approximation result for viscosity solutions is essentially well known (see Proposition 1.2 in Ishii Ishii1989 which refers to the first-order case in Theorem A.2 in Barles and Perthame BarlesPerthame1987 ; see also Lemma 6.1 in Crandall, Ishii and Lions CrandallIshiiLions1992 and the remarks thereafter). For completeness, we give the proof here following the line of arguments for the first-order case in Theorem A.2 in Barles and Perthame BarlesPerthame1987 . In the remainder of this article, we use the notation for all , all and all .

Lemma 4.8.

Let , let be an open set, let , , be functions and let , , be degenerate elliptic functions such that is continuous. Moreover, assume that

| (45) | |||

for all nonempty compact sets and all nonempty compact sets and assume for every that is a viscosity solution of . Then is a viscosity solution of .

The proof is divided into two steps.

Step 1: Let and let be a function such that is a strict maximum of , that is,

| (46) |

for all . Then we define . Since is an open set, we obtain that . Furthermore, continuity of the function and of the functions , , together with compactness of the set proves that there exists a sequence , , of vectors such that

| (47) |

for all and all . We now prove that the sequence converges to . Aiming at a contraction, we assume that the sequence does not converge to . Due to compactness of , there exists a vector and an increasing sequence , , such that . In particular, we obtain that the set is compact. Assumption (4.8), inequality (47) and inequality (46) hence imply that

From this contradiction, we infer that . Assumption (4.8) and continuity of and of hence imply that

| (48) | |||

In addition, and (47) show that there exists a natural number such that we have for all that and that is a local maximum of the function . Hence, Corollary 4.5 and the assumption that is a viscosity solution of show that

| (49) |

for all . Continuity of , equation (4.2), assumption (4.8), inequality (49) and compactness of the set therefore yield that

| (50) | |||

We thus have proved that for all is a strict maximum of and all .

Step 2: Let and let be a function such that and . Next define functions , , by for all and all . Note for every that is a strict maximum of the function . Step 1 can thus be applied to obtain

| (51) |

for all . Moreover, observe that and that for all where is the -unit matrix. Consequently, we see that and that . Continuity of and inequality (51) hence yield

| (52) | |||

We thus have proved that for all with and and all . This shows that is a viscosity subsolution of . In the same way, it can be shown that is a viscosity supersolution of and we thereby obtain that is a viscosity solution of . The proof of Lemma 4.8 is thus completed.

4.3 Uniqueness of viscosity solutions of Kolmogorov equations

A key result of this subsection (Corollary 4.14) establishes uniqueness of viscosity solutions of a second-order linear PDE within a certain class of functions and is apparently new. This uniqueness result is based on the well-known concept of superharmonic functions or—in the PDE language—on the idea of dominating supersolutions. More precisely, let and let be a probability space with a normal filtration . For solution processes , , of many SDEs, there exists a function [often ] and a real number such that the stochastic processes , , are nonnegative supermartingales (so that for all ); see, for example, the examples in Section 4 in HutzenthalerJentzen2014Memoires . For these stochastic processes to be supermartingales, it suffices that the Lyapunov function satisfies

| (53) |

for all , where is the generator of the SDE under consideration. In other words, it suffices that the map is a classical supersolution of the Kolmogorov equation. For , and an open set , a function is here called degenerate elliptic if for all , , , and all with (see, e.g., inequality (1.2) in Appendix C in Peng Peng2010 and compare also with Section 4.1 above). To establish Corollary 4.14, we first state a few auxiliary results. For the convenience of the reader, we first state Proposition 3.7 from Crandall, Ishii and Lions CrandallIshiiLions1992 in the next lemma.

Lemma 4.9.

Let , let be a set, let be an upper semicontinuous function, let be a lower semicontinuous function satisfying and let be a function satisfying

| (54) |

Then and for all , , with and it holds that and.

The next lemma essentially generalizes Theorem 2.2 in Appendix C in Peng Peng2010 (which assumes the functions to be uniformly continuous in the second argument uniformly in the last argument) and is a generalized analog of Theorem 8.2 in Crandall, Ishii and Lions CrandallIshiiLions1992 for unbounded domains. Given an open set , we define a sequence , , of compact sets by

| (55) |

for all . We also write for the complement of in .

Lemma 4.10 ((A domination result for viscosity subsolutions)).

Let , , let be an open set, let be degenerate elliptic and upper semicontinuous functions and let be upper semicontinuous functions such that for every it holds that is a viscosity subsolution of

| (56) |

for . Moreover, assume that

| (57) | |||

for all , , , satisfying that , that , that , that and that . Furthermore, assume that for all and that

| (58) |

Then for all .

If , then the assertion is trivial. So for the rest of the proof, we assume that . We will show that for all and all . Letting will then yield that for all . In the following, we thus fix . In a first step of this proof, we modify the problem. More precisely, define functions by and functions by

Then it holds for every that is a viscosity subsolution of

| (60) |

for . It remains to prove that for all . Aiming at a contradiction, we assume that the extended real number satisfies that . Assumption (58) then implies that there exists a natural number such that is nonempty and such that for all . This, together with and for all implies that

| (61) |

Moreover, the function is upper semicontinuous and is hence bounded from above on the compact set . Combining this with (61) proves that and we thus get . In the next step, we define a function by for all . For several , we will apply Lemma 4.7 with , and with below. For this, we now check the assumptions of Lemma 4.7. Define a function by for all . Note for every that the function is upper semicontinuous with a compact domain of definition and therefore, attains its maximum in a point . Next observe that

| (62) |

for all . This together with monotonicity of the function implies that the limit exists in , that is, it holds that . The set is relatively compact and, therefore, there exists a limit point of this set. Let , , be a strictly increasing sequence such that . Clearly, for all and all implies that for all . In addition, observe that if , then (62) implies that

and this contradiction shows that . Next observe that

| (64) | |||

Hence, Lemma 4.9 applied to and to yields that

| (65) |

and that . The definition of therefore ensures that for all . Furthermore, observe that if , then (62) and the upper semicontinuity of show that

and this contradiction implies that . Consequently, there exists a natural number such that for every it holds that . Next, for every , we apply Lemma 4.7 with , with , with the functions and and with the local maximum point to obtain the existence of matrices , , such that for every and every it holds that

| (67) |

and

Combining this with the identity for all then implies that

for all . To simplify the notation we define matrices , , , by for all and all . Corollary 4.6 together with (67) and the fact that it holds for every that is a viscosity subsolution (60) then proves that

| (69) | |||

for all and all . Summing over hence results in

| (70) | |||

for all . Next note that the definition of ensures in the case that

for all and all and, therefore, we obtain that in the case it holds that

| (72) | |||

for all . Combining this with (4.3) results in

| (73) |

for all . Therefore, we obtain from (4.3) and from and for all that

| (74) | |||

for all . In the next step, we define , , , by

| (75) | |||

for all and all . Moreover, observe that in the case it holds that

for all and all . Then (4.3) ensures that

| (77) | |||

Next, we observe that the Taylor expansion for all implies that for all . This together with (4.3), (4.3) and the estimate for all results in

for all . Inequality (4.3) implies that. Consequently, (4.3), (4.3) and for all yield that

for all and all . Inequality (4.3), in particular, implies , for all and all . Combining this, the identities

[see (65)] and the estimate with assumption (4.10) and with (4.3) shows that

This contradiction implies that . As was arbitrary, we conclude that for all . This finishes the proof of Lemma 4.10.

The next result, Corollary 4.11, establishes a comparison result for certain viscosity subsolutions and certain viscosity supersolutions of a PDE. It is a direct consequence of Lemma 4.10 above in the case . Corollary 4.11 essentially generalizes Theorem 2.4 in Appendix C in Peng Peng2010 (which assumes the function to be globally Lipschitz continuous in the third and last argument uniformly in the remaining arguments) and essentially generalizes Theorem 8.2 in Crandall, Ishii and Lions CrandallIshiiLions1992 (which assumes a bounded domain and a globally uniform estimate on the function ). Corollary 4.11 is an immediate consequence of Lemma 4.2 and Lemma 4.10 with . Its proof is therefore omitted.

Corollary 4.11 ((A comparison result for viscosity subsolutions and viscosity supersolutions)).

Let , , let be an open set, let , let be a degenerate elliptic and continuous function and assume that is a viscosity subsolution of

| (81) |

for and that is a viscosity supersolution of (81). Moreover, assume that

| (82) | |||

for all , , satisfying that , that , that and that . Furthermore, assume that for all and that

| (83) |

Then , that is, it holds that for all .

Assumption (83) in Corollary 4.11 is in several cases difficult to verify. Lemma 4.13 below gives an extension of Corollary 4.11 which postulates a less restrictive condition than (83) by using a suitable Lyapunov type function [cf. (90) in Lemma 4.13 and (83) in Corollary 4.11]. In the proof of Lemma 4.13, the following elementary lemma is used.

Lemma 4.12 ((Scaling of viscosity subsolutions and viscosity supersolutions)).

Let , , let be an open set, let , let be a degenerate elliptic function, let be a viscosity subsolution (supersolution) of (81) and let be a function defined by

| (84) | |||

for all . Then is degenerate elliptic and the function defined by for all is a viscosity subsolution (supersolution) of

| (85) |

for .

We proof Lemma 4.12 in the case where is a viscosity subsolution of (81). The case where is a viscosity supersolution of (81) follows analogously. We thus assume in the following that is a viscosity subsolution of (81). First, observe that is upper semicontinuous and that is degenerate elliptic. In the next step assume that there exist a vector and a function satisfying and . Then the function is in and satisfies and . As is a viscosity subsolution of (81), we get

| (86) | |||

Rearranging this inequality results in

This proves inequality (4.3) for all and all . Therefore, is a viscosity subsolution of (85) and the proof of Lemma 4.12 is completed.

Lemma 4.13 ((A further comparison result for viscosity subsolutions and viscosity supersolutions)).

Let , , let be an open set, let , , let be a degenerate elliptic and continuous function and assume that is a viscosity subsolution of

| (88) |

for , that is a viscosity supersolution of (88) and that for every it holds that is a classical supersolution of (88). Moreover, assume that

| (89) | |||

for all , , satisfying that , that, that , that , that , that and that . Furthermore, assume that for all and that

| (90) |

Then , that is, it holds that for all .

Define functions and by and for all and by

| (91) | |||

for all . Lemma 4.12 then ensures that is degenerate elliptic, that is a viscosity subsolution of

| (92) |

for and that is viscosity supersolution of (92). Below we will finish this proof by an application of Corollary 4.11 with , and . For this, we now check the assumptions of Corollary 4.11. First, observe that assumption (90) ensures that (83) is fulfilled. In addition, observe that the assumption for all ensures that for all . In the next step, we verify (4.11). For this, let , , be sequences satisfying that , that , that and that . To verify (4.11), we will apply assumption (4.13). For this, we define and , , by for all and by , , , ,

| (93) | |||||

| (94) | |||||

for all . Continuity of and then imply that

Moreover, note that the local Lipschitz continuity of and and the continuity of together with the assumptions , and imply that

and . Combining this and (4.3) with assumption (4.13) shows that

| (100) | |||

The definition of hence implies that

| (101) | |||

as is by assumption a classical supersolution of (88). We can thus apply Corollary 4.11 to obtain that for all . This finishes the proof of Lemma 4.13.

The next result, Corollary 4.14, asserts uniqueness of the solution of a linear second-order PDE. We assume that the Lyapunov-type function in Lemma 4.13 is of the form for all where is a real number and where is a twice continuously differentiable function.

Corollary 4.14 ((Uniqueness of viscosity solutions of Kolmogorov type equations)).

Let , , , let be an open set, let , , let and be locally Lipschitz continuous functions and let satisfy

| (102) | |||

for all . Then there exists at most one continuous function which fulfills for all , which fulfills and which fulfills that is a viscosity solution of

| (103) | |||

for .

Let be two continuous functions such that for all , such that

and such that and are viscosity solutions of (4.14). Then define a function by . We show Corollary 4.14 by applying Lemma 4.13. To this end we now verify (4.13). For this, let , , satisfy that , that , that , that , that , that and that . Then it holds that

| (104) | |||

Hence, the local Lipschitz continuity of the functions and together with the properties of , , , implies that

| (105) | |||

This shows assumption (4.13). Moreover, by assumption, is a viscosity subsolution of (4.14) and is a viscosity supersolution of (4.14). Furthermore, (4.14) shows for every that the function is a classical supersolution of (4.14). In addition, observe that (90) follows from . Consequently, Lemma 4.13 implies that . Repeating these arguments with and interchanged finally shows that so that . This proves uniqueness and finishes the proof of Corollary 4.14.

4.4 Viscosity solutions of Kolmogorov equations

The main result of this subsection, Theorem 4.16 below, establishes that the transition semigroup associated with a suitable SDE with locally Lipschitz continuous coefficients is within a certain class of functions the unique viscosity solution of the Kolmogorov equation of the SDE. To establish this result, we first prove an auxiliary result.

Lemma 4.15 ((Existence of viscosity solutions of Kolmogorov equations with globally Lipschitz continuous coefficients with compact support)).

Let , let be a probability space with a normal filtration, let be a standard -Brownian motion, let be an open set, let be a continuous function and let and be locally Lipschitz continuous functions with compact support. Then there exists a family , , of up to indistinguishability unique adapted stochastic processes with continuous sample paths satisfying

| (106) |

for all , -a.s. and all and the function given by is a viscosity solution of

| (107) | |||

for .

First of all, observe that since and have compact supports, they are globally Lipschitz continuous, so that (106) has unique solutions. It thus remains to show that the function introduced above is a viscosity solution of (4.15). Let be a relatively compact open set in with the property that . By assumption and are compact sets, and hence such a set does indeed exist. Next, let , , and , , be sequences of smooth functions satisfying and for all and denote by , , , the solutions to the corresponding SDEs. Moreover, let , , be a sequence of smooth functions satisfying for each . Now we define functions , , and , by and . For any fixed and , the function , is smooth and globally Lipschitz continuous (see, e.g., Corollary 2.8.1 and Theorem 2.8.1 in GihmanSkorohod1972 ). Theorem 4.3 in PardouxPeng1992 then shows that

| (108) | |||

for all , . Remark 4.1 hence shows that the functions , , are also viscosity solutions to these equations. Furthermore, observe that the smoothness of the functions , , and the global Lipschitz continuity of the functions , , and imply that

| (109) | |||

for all and all . Combining this with Lemma 4.8 shows that for every it holds that is a viscosity solution of (4.15) with initial condition . In addition, note that

| (110) | |||

for all compact sets . Combining this with Lemma 4.8 eventually shows that is indeed a viscosity solution of (4.15) as claimed.

The next result is a generalization and a consequence of Lemma 4.15 above and constitutes the main result of this section.

Theorem 4.16 ((Existence and uniqueness of viscosity solutions of Kolmogorov equations)).

Let , , let be an open set, let be a continuous function, let and be locally Lipschitz continuous functions and let be such that , such that

| (111) |

for all and such that . Then there exists a unique continuous function which fulfills for all , which fulfills for all and which is a viscosity solution of

| (112) | |||

for . Moreover, if is a probability space with a normal filtration and if is a standard -Brownian motion, then there exist up to indistinguishability unique global solutions , , to

| (113) |

-a.s. for all and all . In that case, has the probabilistic representation for all .

W.l.o.g. we assume throughout this proof that is a probability space with a normal filtration and that is a standard -Brownian motion. Then, since is a Lyapunov function, (113) does have global solutions which furthermore (assuming without loss of generality that ) have the property that

| (114) |

for any stopping time . As a consequence, for every it holds that is finite so that we can define by for all . Note that as a consequence of our assumption on , for every there exists a constant such that

| (115) |

holds for all . The bound (114) immediately implies a similar bound on , so that has the required behaviour at infinity. It therefore remains to show that is indeed a viscosity solution of (4.16), as uniqueness of such a solution follows from Corollary 4.14. The proof for this goes again by approximation. Let and for be any sequence of Lipschitz continuous functions such that for all it holds that

| (116) |

and

| (117) |

Denoting by , , , the solutions to the corresponding SDEs, we set for all , . It then follows from Lemma 4.15 that is a viscosity solution to the equation analogous to (4.16). As a consequence of Lemma 4.8, it remains to show that , uniformly on compact subsets of . For this, we introduce the stopping times , , . As a consequence of (115), the fact that and coincide until time , and the fact that , -a.s. provided that , we have for all and all with that

| (118) | |||

Using (114), we obtain from Chebychev’s inequality that for all it holds that

| (119) |

Inserting this into (4.4), the required locally uniform convergence follows at once.

In the literature, there are many results proving an assertion similar to Theorem 4.16 and Corollary 4.14, respectively, under various assumptions on the functions and . Theorem 4.3 in Pardoux and Peng PardouxPeng1992 implies that the transition semigroup associated with the SDE (113) is a viscosity solution of (4.16) if and are globally Lipschitz continuous; see also Peng Peng1993 . Theorem C.2.4 in Peng Peng2010 can be applied if is locally Hölder continuous and if is constant and then proves uniqueness of an at most polynomially growing viscosity solution of (4.16). Uniqueness of the viscosity solution of (4.16) with given initial function follows from Theorem 8.2 in the User’s guide Crandall, Ishii and Lions CrandallIshiiLions1992 if is globally one-sided Lipschitz continuous, that is, if there exists a constant such that for all , and if is globally Lipschitz continuous. Moreover, Theorem 5.13 in Krylov Krylov1999 implies that the transition semigroup solves the Kolmogorov equation (4.16) in the sense of distributions if and are globally Lipschitz continuous. In addition, Theorems 7.1.3 and 7.1.4 in Evans Evans2010 show that there exists a unique weak solution of the PDE (4.16) if the coefficients and are bounded and if the PDE (4.16) is uniformly parabolic.

In many situations, the open set and the Lyapunov-type function in Theorem 4.16 satisfy and for all where is an arbitrary real number. This is subject of the following Corollary 4.17. It is a direct consequence of Theorem 4.16 and its proof is therefore omitted.

Corollary 4.17 ((Existence and uniqueness of at most polynomially growing viscosity solutions of Kolmogorov equations)).

Let , let be a continuous and at most polynomially growing function,let and be locally Lipschitz continuous functions with and . Then there existsa unique continuous function which fulfills for all , which fulfills for all , and which is a viscosity solution of

for . Moreover, if is a probability space with a normal filtration and if is a standard -Brownian motion, then has the probabilistic representation for all , where the stochastic processes , , are as before.

Note that all examples in this article fulfill the assumptions of Corollary 4.17. In particular, observe that and from the SDE (2) in Section 2, and from the SDE (2) in Section 2, and from the SDE (19) in Section 2, and from the SDE (3) in Section 3, and from the SDE (37) in Section 3 as well as and from the SDE (5) in Section 5 all fulfill the assumptions of Corollary 4.17.

4.5 Distributional solutions of Kolmogorov equations

In this section, we formulate a slight extension to Theorem 5.13 in Krylov Krylov1999 , which states that the semigroup associated to an SDE with smooth coefficients solves the corresponding Kolmogorov equation in the distributional sense, even if the coefficients are badly behaved near the boundary of the domain of definition .

Proposition 4.18.

Let , let be an open set, let , , let , let be a probability space with a normal filitration , let be a standard -Brownian motion and let , , be solutions to

| (121) |

-a.s. for all . Then the function given by for all solves the Kolmogorov equation

| (122) |

in the distributional sense.

Let be as above, consider for every smooth and globally Lipschitz continuous functions and which agree with and on , and denote by , , solutions of the corresponding SDE. Fix some final time , denote by the law of on and for every by the law of on . It then follows from the smoothness of the coefficients and that is weakly continuous; see Theorem 1.7 in Krylov Krylov1999 . In particular, this implies that is continuous and that, for every compact , the set is tight. Let now for all , , where , , are smooth approximations of such that and for all and such that . Note now that and that, locally uniformly in , the -measure of the set converges to as . In particular, there exists a real number such that for all it holds that

| (123) |

As a consequence, one has , locally uniformly in and . The claim now follows at once from the fact that, by Theorem 5.13 in Krylov Krylov1999 , each of the solves the Kolmogorov equation with and .

5 A counterexample to the rate of convergence of the Euler–Maruyama method

In this section, we use the results of Section 3 to establish the existence of an SDE with smooth and globally bounded coefficients for which the Euler–Maruyama method convergences without any arbitrarily small polynomial rate of convergence, thereby proving Theorem 1.3 of the Introduction. Denote by the constant

| (124) |

and set

for all . The function that appears in has been used as a mollifier function in Lemma 1.2.3 in Hörmander Hoermander1990 . Note that is infinitely often differentiable and globally bounded. Moreover, let be any probability space supporting a four-dimensional standard Brownian motion with continuous sample paths. Then there exists a unique stochastic process with continuous sample paths which fulfills for all . The stochastic process is thus a solution process of the SDE

| (126) | |||||

for satisfying . In the next step, we define the Euler–Maruyama approximations for the SDE (5) using the following notation. Let , , be a family of mappings defined by

| (127) |

for all and all . Then let , , be Euler–Maruyama approximation processes defined recursively by

for all , and all . Observe that this definition ensures that

for all and all . The following Theorem 5.1 proves that the Euler–Maruyama method (5) for the SDE (5) convergences without any arbitrarily small polynomial rate of convergence. Theorem 5.1 together with an elementary transformation argument [dealing with general and general ] then implies Theorem 1.3.

Theorem 5.1 ((A counterexample to the rate of convergence of the Euler–Maruyama method)).

Let be a solution process of the SDE (5) with continuous sample paths and with . Then

| (130) |

for all and all and, therefore, we obtain

for all and all . In particular, for every and every there exists a real number such that .

The proof of Theorem 5.1 is deferred to the end of this section. To the best of our knowledge, the SDE (5) is the first SDE with smooth coefficients in the literature for which it has been established that the Euler–Maruyama scheme converges in the strong and numerical weak sense without any arbitrarily small rate of convergence. Using the results of Section 3, one can show that the SDE (5) is not locally Hölder continuous with respect to the initial value. This is summarized in the next corollary of Lemma 3.3 in Section 3.

Corollary 5.2.

Let , , be solution processes of the SDE (5) with continuous sample paths and with for all . Then for every the function is not locally Hölder continuous.

Note that

| (132) | |||

for all . Combining this with Lemma 3.3 in Section 3 completes the proof of Corollary 5.2.

In the following, the size of the quantity is analyzed for sufficiently small and thereby Theorem 5.1 is established. To do so, we first establish a few auxiliary results. We begin with an elementary estimate for the numerical integration of concave functions.

Lemma 5.3 ((Numerical integration of concave functions)).

Let , , be given by (127), let be a real number and let be a continuously differentiable function with a nonincreasing derivative. Then

for all .

The fundamental theorem of calculus and monotonicity of imply

| (134) | |||

for all . This finishes the proof of Lemma 5.3.

Using Lemma 5.3, we establish in the next lemma a simple lower bound for the numerical integration of the function , , in the third component of .

Lemma 5.4 ([Numerical integration of the function , ]).

First of all, observe that

for all . We hence obtain that the function has a nonincreasing derivative. Applying Lemma 5.3 and using that the function is nonincreasing therefore results in

| (137) | |||

for all where we used the estimate for all in the penultimate inequality in (5). Moreover, note that (5) implies that

| (138) | |||

for all . Combining (5) and (5) completes the proof of Lemma 5.4.

We are now ready to prove Theorem 5.1. Its proof uses Lemma 5.4 as well as Lemma 3.3 in Section 3 above.

Proof of Theorem 5.1 First of all, note that , -a.s. for all . Combining this with (5) then shows that

for all and all . The estimate for all , and Lemmas 5.4 and 3.3 therefore show that

for all , and all . Hence, we finally obtain that

| (139) | |||

for all and all . This completes the proof of Theorem 5.1.

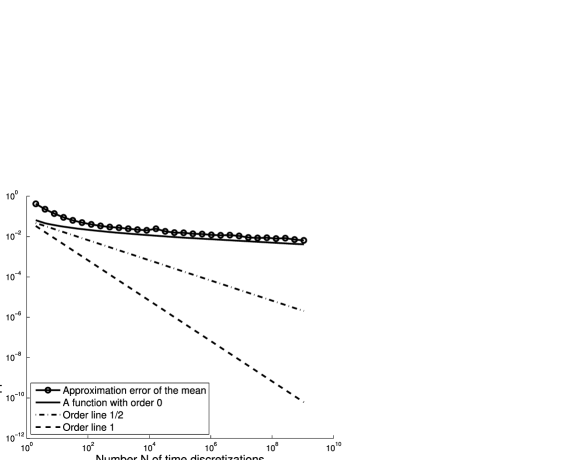

In the next step, we illustrate the lower bound on the weak approximation error in Theorem 5.1 by a numerical simulation. More precisely, we ran Monte Carlo simulations and approximatively calculated the quantity for and . We approximated these differences of expectations with an average over independent Monte Carlo realizations. Moreover, we discretized the integrals and in the exact solution with a uniform grid and mesh size . Figure 1 depicts the resulting graph.

In addition to the weak approximation error for and , we also plotted the function

(a function with order ), the function (order line ) and the function (order line ) in Figure 1. In the standard literature in computational stochastics (see, e.g., Kloeden and Platen kp92 ) the Euler–Maruyama scheme is shown to converge in the numerically weak sense with order if the coefficients of the SDE are smooth and globally Lipschitz continuous (see Chapter 8 in Kloeden and Platen kp92 for the precise assumptions) and, therefore, the order line is plotted in Figure 1. Moreover, the function with order is included in Figure 1 so that one can compare the graph visually with a function which has convergence order . According to our simulations, the approximation error for the mean does not drop far below even for time discretizations. This indicates that calculating the mean with the Euler–Maruyama method up to a high precision requires a huge computational effort. In particular, this suggests for applications that an approximation cannot, in general, be assumed to be very close to the exact value even after a very high computational effort.

Acknowledgements

We gratefully acknowledge Verena Bögelein, Sonja Cox, Weinan E, Alessandra Lunardi, Étienne Pardoux, Michael Röckner and Tobias Weth for helpful remarks and for pointing out useful references to us. Special thanks are due to Shige Peng for fruitful discussions about questions on uniqueness of viscosity solutions, in particular, for pointing out his quite instructive book Peng2010 to us.

References

- (1) {bmisc}[auto:STB—2014/01/06—10:16:28] \bauthor\bsnmAlfonsi, \bfnmA.\binitsA. (\byear2012). \bhowpublishedStrong convergence of some drift implicit Euler scheme. Application to the CIR process. Available at \arxivurlarXiv:1206.3855. \bptokimsref\endbibitem

- (2) {barticle}[mr] \bauthor\bsnmBarles, \bfnmG.\binitsG. and \bauthor\bsnmPerthame, \bfnmB.\binitsB. (\byear1987). \btitleDiscontinuous solutions of deterministic optimal stopping time problems. \bjournalRAIRO Modél. Math. Anal. Numér. \bvolume21 \bpages557–579. \bidissn=0764-583X, mr=0921827 \bptokimsref\endbibitem

- (3) {barticle}[mr] \bauthor\bsnmBurrage, \bfnmK.\binitsK., \bauthor\bsnmBurrage, \bfnmP. M.\binitsP. M. and \bauthor\bsnmTian, \bfnmT.\binitsT. (\byear2004). \btitleNumerical methods for strong solutions of stochastic differential equations: An overview. \bjournalProc. R. Soc. Lond. Ser. A Math. Phys. Eng. Sci. \bvolume460 \bpages373–402. \biddoi=10.1098/rspa.2003.1247, issn=1364-5021, mr=2052268 \bptokimsref\endbibitem

- (4) {barticle}[mr] \bauthor\bsnmCambanis, \bfnmStamatis\binitsS. and \bauthor\bsnmHu, \bfnmYaozhong\binitsY. (\byear1996). \btitleExact convergence rate of the Euler–Maruyama scheme, with application to sampling design. \bjournalStochastics Stochastics Rep. \bvolume59 \bpages211–240. \bidissn=1045-1129, mr=1427739 \bptokimsref\endbibitem

- (5) {bbook}[mr] \bauthor\bsnmCerrai, \bfnmSandra\binitsS. (\byear2001). \btitleSecond Order PDE’s in Finite and Infinite Dimension: A Probabilistic Approach. \bseriesLecture Notes in Math. \bvolume1762. \bpublisherSpringer, \blocationBerlin. \biddoi=10.1007/b80743, mr=1840644 \bptokimsref\endbibitem

- (6) {bincollection}[mr] \bauthor\bsnmClark, \bfnmJ. M. C.\binitsJ. M. C. and \bauthor\bsnmCameron, \bfnmR. J.\binitsR. J. (\byear1980). \btitleThe maximum rate of convergence of discrete approximations for stochastic differential equations. In \bbooktitleStochastic Differential Systems (Proc. IFIP-WG 7/1 Working Conf., Vilnius, 1978). \bseriesLecture Notes in Control and Information Sci. \bvolume25 \bpages162–171. \bpublisherSpringer, \blocationBerlin. \bidmr=0609181 \bptokimsref\endbibitem

- (7) {barticle}[mr] \bauthor\bsnmCrandall, \bfnmMichael G.\binitsM. G., \bauthor\bsnmIshii, \bfnmHitoshi\binitsH. and \bauthor\bsnmLions, \bfnmPierre-Louis\binitsP.-L. (\byear1992). \btitleUser’s guide to viscosity solutions of second order partial differential equations. \bjournalBull. Amer. Math. Soc. (N.S.) \bvolume27 \bpages1–67. \biddoi=10.1090/S0273-0979-1992-00266-5, issn=0273-0979, mr=1118699 \bptokimsref\endbibitem

- (8) {barticle}[mr] \bauthor\bsnmCrandall, \bfnmMichael G.\binitsM. G. and \bauthor\bsnmLions, \bfnmPierre-Louis\binitsP.-L. (\byear1981). \btitleCondition d’unicité pour les solutions généralisées des équations de Hamilton–Jacobi du premier ordre. \bjournalC. R. Acad. Sci. Paris Sér. I Math. \bvolume292 \bpages183–186. \bidissn=0151-0509, mr=0610314 \bptokimsref\endbibitem

- (9) {barticle}[mr] \bauthor\bsnmCrandall, \bfnmMichael G.\binitsM. G. and \bauthor\bsnmLions, \bfnmPierre-Louis\binitsP.-L. (\byear1983). \btitleViscosity solutions of Hamilton–Jacobi equations. \bjournalTrans. Amer. Math. Soc. \bvolume277 \bpages1–42. \biddoi=10.2307/1999343, issn=0002-9947, mr=0690039 \bptokimsref\endbibitem

- (10) {barticle}[mr] \bauthor\bsnmDavie, \bfnmA. M.\binitsA. M. and \bauthor\bsnmGaines, \bfnmJ. G.\binitsJ. G. (\byear2001). \btitleConvergence of numerical schemes for the solution of parabolic stochastic partial differential equations. \bjournalMath. Comp. \bvolume70 \bpages121–134. \biddoi=10.1090/S0025-5718-00-01224-2, issn=0025-5718, mr=1803132 \bptokimsref\endbibitem

- (11) {bbook}[mr] \bauthor\bparticleDa \bsnmPrato, \bfnmGiuseppe\binitsG. (\byear2004). \btitleKolmogorov Equations for Stochastic PDEs. \bpublisherBirkhäuser, \blocationBasel. \biddoi=10.1007/978-3-0348-7909-5, mr=2111320 \bptokimsref\endbibitem

- (12) {bbook}[mr] \bauthor\bparticleDa \bsnmPrato, \bfnmGiuseppe\binitsG. and \bauthor\bsnmZabczyk, \bfnmJerzy\binitsJ. (\byear2002). \btitleSecond Order Partial Differential Equations in Hilbert Spaces. \bseriesLondon Mathematical Society Lecture Note Series \bvolume293. \bpublisherCambridge Univ. Press, \blocationCambridge. \biddoi=10.1017/CBO9780511543210, mr=1985790 \bptokimsref\endbibitem

- (13) {barticle}[mr] \bauthor\bsnmDereich, \bfnmSteffen\binitsS., \bauthor\bsnmNeuenkirch, \bfnmAndreas\binitsA. and \bauthor\bsnmSzpruch, \bfnmLukasz\binitsL. (\byear2012). \btitleAn Euler-type method for the strong approximation of the Cox–Ingersoll–Ross process. \bjournalProc. R. Soc. Lond. Ser. A Math. Phys. Eng. Sci. \bvolume468 \bpages1105–1115. \biddoi=10.1098/rspa.2011.0505, issn=1364-5021, mr=2898556 \bptokimsref\endbibitem

- (14) {barticle}[mr] \bauthor\bsnmDörsek, \bfnmPhilipp\binitsP. (\byear2012). \btitleSemigroup splitting and cubature approximations for the stochastic Navier–Stokes equations. \bjournalSIAM J. Numer. Anal. \bvolume50 \bpages729–746. \biddoi=10.1137/110833841, issn=0036-1429, mr=2914284 \bptokimsref\endbibitem

- (15) {bincollection}[mr] \bauthor\bsnmElworthy, \bfnmK. D.\binitsK. D. (\byear1978). \btitleStochastic dynamical systems and their flows. In \bbooktitleStochastic Analysis (Proc. Internat. Conf., Northwestern Univ., Evanston, Ill., 1978) \bpages79–95. \bpublisherAcademic Press, \blocationNew York. \bidmr=0517235 \bptokimsref\endbibitem

- (16) {barticle}[mr] \bauthor\bsnmEvans, \bfnmLawrence C.\binitsL. C. (\byear1978). \btitleA convergence theorem for solutions of nonlinear second-order elliptic equations. \bjournalIndiana Univ. Math. J. \bvolume27 \bpages875–887. \biddoi=10.1512/iumj.1978.27.27059, issn=0022-2518, mr=0503721 \bptokimsref\endbibitem

- (17) {barticle}[mr] \bauthor\bsnmEvans, \bfnmLawrence C.\binitsL. C. (\byear1980). \btitleOn solving certain nonlinear partial differential equations by accretive operator methods. \bjournalIsrael J. Math. \bvolume36 \bpages225–247. \biddoi=10.1007/BF02762047, issn=0021-2172, mr=0597451 \bptokimsref\endbibitem