Testing the fractional integration parameter revisited: a

Fractional Dickey-Fuller Test

Ahmed BENSALMA111High national school of statistic and applied economic

(ENSSEA), Algiers, Algeria, Email: bensalma.ahmed@gmail.com and

Mohamed BENTARZI222 Faculty of Mathematics, University of Science and

Technology Houari Boumediene, Algiers, Algeria. , Email:

bentarzimohamed@yahoo.fr

- Abstract

-

In this paper, in the first step, we show that the fractional Dickey-Fuller test proposed by Dolado et al is useless in practice. In the second step, we propose a new testing procedure for the degree of fractional integration of a time series inspired on the unit root test of Dickey-Fuller . The composite null hypothesis is that of against . The test statistics is the same as in Dickey-Fuller test using as output instead of and as input and eventually some lag of instead some lag of , exploiting the fact that if is then is under the null . If , using the generalization of Sowell’s result , we propose a test based on the least favorable case, , to control type error, and when we show that the tests statistics diverges to , providing consistency. Through a simulation study, we show the good performance of the test in terms of size and power. Finally, in order to show how to use the new testing procedure, the test is applied to the well-known Nelson and Plosser data.

Keywords: Fractional integration, Fractional unit root; Dickey-Fuller unit root test; Fractional Dickey-Fuller test.

1 Introduction

As the most popular long memory model and a useful extension of the classical models, the fractionally integrated autoregressive moving average () process, introduced by Granger and Jojeux and Hosking , has seen a considerable interest in the past three decades and has been widely applied in many fields like hydrology, economics and finance. The process generalizes the standard linear model by permitting to the degree of integration to be non-integer. Compared with the standard and specifications, the generalization provides a more flexible framework in modelling the long range dependence, where a special role is played by the fractional differencing parameter whose precise determination is very important in applied work.

The stationary and invertible Fractional processes, is defined as the following

where is the backshift operator and are independently and identically distributed () random variables with zero mean and finite variance; and are polynomial functions of with order and , and both of them have only roots outside the unit circle. The fractional difference operator is defined by its Maclaurin series (by its binomial expansion, if is an integer):

where

If , is defined by the recursion formula .

In recent years, an increasing effort has been made to establish reliable testing procedures to determine whether or not an observed time series is fractionally integrated. In particular, there has been a considerable interest in generalizing the familiar Dickey-Fuller test by taking into account the fractional integration order. It is well documented that the power of Dickey-Fuller [] type tests against alternatives of fractional integration is low (see Sowell ; Diebold and Rudebusch ; Hassler and Wolters Krämer ). This motivated the development of powerful tests against fractional alternatives. Robinson pioneered an integration test constructed from the Lagrange Multiplier [] principle, which was proven by Robinson to be locally the most powerful under Gaussianity. The test has been further studied and modified by Agiakloglou and Newbold , Tanaka . Tanaka showed, through simulation experiments, that the tests have serious size distortion. Another serious criticism addressed to the tests is that, by working under the null hypothesis, it does not yield any direct information about the correct long-memory parameter , when the null is rejected (Candelon, Gil Alana ).

More recently, Dolado et al introduced a fractional integration test (henceforth test) based on an auxiliary regression for the null of unit root against the alternative of fractional integration (, ). Their proposed test reduces to the standard Dickey-Fuller test when while under the null and when known, the statistic in the corresponding regression model depends on a fractional Brownian motion if . Further, the test was refined by Lobato and Velasco using the same null and alternative hypotheses.

While the test represents a useful generalization of the Dickey-Fuller test in the presence of a fractionally integrated alternative, it might give arbitrary conclusions when the true is not present neither in the null nor in the alternative, because the auxiliary regression model, they used, depends on the null and alternative (i.e. and ). Indeed, through some simulation experiments we conduct, it may be seen (see Table below) that the test performs somewhat badly in the case where the parameter is wrongly specified under the null and alternative. In such situation three cases can arise: the case where the null is true, the case where the alternative is true and the case where neither the null nor the alternative is true.

In this paper, we propose an alternative test for the fractional parameter inspired by the unit root test of Dickey-Fuller . The composite null hypothesis is that of against . The test statistics is the same as in Dickey-Fuller test using as input instead of , exploiting the fact that if is then is under the null . If , using the generalization of Sowell’s result , we propose a test based on the least favorable case, , to control type error, and when we show that the tests statistics diverges to , providing consistency. Clearly such testing procedure is conceptually attractive since, first, the hypotheses we consider are rather composite-versus-composite against ) resulting in a dichotomic choice which excludes the third case. Second, by the choice of a suitable regression model, , the usual statistics or have the same asymptotic distribution as the Dickey-Fuller test. This is because the maximum probability of rejecting the null hypothesis i.e. , level of the test, is reached when . So, the standard Dickey-Fuller table may be used for our test without an extra-effort i.e. without using the tabulated values of a fractional Brownian motion.

Before going through the topic, it is important to precise certain essential points, which may facilitate the reading of this paper. The main theme of our article is how to extend the familiar Dickey-Fuller type tests for unit root ( against ) by embedding the case and in continuum of memory properties (i.e. ). Such extension has already been discussed by Dolado et Al . In our paper, we show, in the first step, that the approach is not the best and adequate way to extend the Dickey-Fuller test by taking into account the fractional case. In the second step, we provide how to extend adequately the standard Dickey-Fuller test by taking into account the fractional case.

In order to expose clearly the alternative approach and permit the careful comparison with the approach, we choose to use a simple framework like () process. The case, where the errors are autocorrelated, deserves that one devotes another paper, by taking into account the seminal work of Said and Dickey and Phillips . Our approach is based on the following forth points:

- 1

-

Using the composite hypothesis

- 2

-

If then

- 3

-

Testing the composite null hypothesis is based upon testing the statistical significance of the coefficient (or ) in the regression model

- 4

-

The level of the test

In order to highlight these four important points and not to overlook them into a mid-general framework, the case where the errors are correlated, will not be pursued in this paper. However, I provide (see Appendix ) some discussions when the process is generated by

with being a vector of deterministic functions like a constant or time trend.

Another reason that led us to choose a simple theoretical framework is to highlight the importance of considering correctly, some basic rules of the testing statistical hypothesis theory. In this paper, we focus on the importance to consider the statistic of the test, exclusively, deduced under the null hypothesis (see section , for more details).

The rest of this paper is organized as follows. In section , to highlight the contribution of our approach, we first give some comments on the approach. Then in section , we define in a simple framework our test and in particular the auxiliary regression model used to test the null. Moreover, the main results on the asymptotic distribution under the null and alternative composite hypothesis are given. Section explores a theoretical study about the size and power of our proposed - test. Furthermore, Monte-Carlo simulation experiments are undertaken in order to support the analytical results and in particular to confirm that the proposed test is robust to any misspecification of the order of integration parameter . In Section , we present empirical applications by revisiting Nelson-Plosser data. It is important to note that the empirical application is made only to explain how to use the new testing procedure (The reader should not understand this application as to provide a new evidence for the order of integration of the Nelson and Plosser data). Because, as it has been mentioned previously, the data generating process adopted in this paper is restrictive). Finally, the proofs of the main results presented in Section are left to the appendix and some discussions when the process is generated by some deterministic trend plus process are left to the Appendix .

2 Fractional Dickey-Fuller testing: the approach

2.1 Hypotheses and the auxiliary regression model

Dolado, Gonzalo, and Mayoral [] introduced a test based on an auxiliary regression for the null of unit root against the alternative of fractional integration. The fractional Dickey-Fuller (-) test considered by , in the basic framework, is described as follows.

Let a series generated from the fractionally integrated process ( in short) given by

| () |

where is the true order of integration and, is an innovation with mean zero and variance . For the data generating process () , propose to test the following hypotheses,

| () |

by means of the statistic of the coefficient of in the ordinary least squares () regression

| () |

where . explains the choice of the auxiliary regression model by arguing that, in the simple Dickey-Fuller test, to test the hypotheses

| () |

the maintained regression model is:

| () |

where . If is , then the regression is unbalanced in the sense that the orders of integration of the regressand and the regressor are different, being and respectively. After this, claim that in the simple Dickey-Fuller test the null hypothesis correspond to the regressor and the alternative correspond to . This leads them to consider that the null hypothesis correspond to and the alternative correspond to . In the following we show that the interpretation, made by , in the use of the model , in the simple Dickey-Fuller test is incorrect. In fact, the standard Dickey and Fuller test is not based directly on the regression model . The hypotheses are based on the following regression model

| () |

which is equivalent to the regression model , with . The regression model is balanced in the sense that the regressand and the regressor have the same order of integration which is equal under the null. The scheme and summarize, respectively, the incorrect and correct interpretation in the use of the model , in the simple Dickey-Fuller test.

| Scheme : Incorrect interpretation, in the use of model , | |

|---|---|

| in the simple Dickey-Fuller test | |

| interpretation, in the use of the model | The use of the incorrect |

| , in the simple Dickey-Fuller test | interpretation in fractional case |

| Scheme : Correct interpretation, in the use of the models and , | |

|---|---|

| in the simple Dickey-Fuller test | |

| Correct interpretation, in use | Correct interpretation, in the use |

| of the model | of the model |

The scheme , indicates that the choice of the model or equivalently is based only on the null hypothesis. The scheme , indicates that the incorrect interpretation leads to consider a regression model based on the null and alternative in the fractional case. In fact, for the regression model we have, under the null ()

and under the alternative (),

As a result, the authors are locked into the trap set by this semblance of analogy. There are other inconsistencies in the use of statistical concepts. Someone, can easily feel, throughout the reading of the article , the efforts granted by the authors to justify inconsistencies. It would be long to enumerate all the inconsistencies in the test procedure.

2.1.1 Unit root test against fractional alternatives and its asymptotic Properties

To study the performances of their procedure in terms of power and size, consider only the particular case,

| () |

by means of the -statistic of the coefficient , in the ordinary least squares () regression

| () |

The -ratio, , is given by

Theorem 1

(DGM [10]. Under the null hypothesis that is a random walk, the asymptotic distribution of is given by

and

where is fractional Brownian motion.

Proof. See DGM [10]

Theorem , shows that under the null the asymptotic distribution of -statistic depends on fractional Brownian motion if and if . These asymptotic distributions are different from those derived by Dickey and Fuller which depend only on standard Brownian motion. The implementation of test would require tabulation of the percentiles of the functional of Brownian motion, which imply that inference on the presence of unit root would be conditional on . But given the well-known difficulties in estimating the order of fractional integration in finites samples, thus the test might suffer from misspecification (i.e. the parameter is wrongly specified)

Under , we have and under the alternative we have . Thus build the decision rule as follows,

| () |

The hypotheses based on the regression model and the decision rule is called by their authors ”Fractional Dickey and Fuller Test”.

Remark 2

Why does DGM consider only the case ? To respond this question, let us consider the case . Since , the set of alternatives values of is

In this example, we have two cases. The first case, is given by and and the decision rule is based on ”( or ). The second case is given by and . In this case it is easy to show that the decision rule is based on ”( or )”, because we have

Remark 3

We can suggest another D.G.M. type test. Indeed, since DGM would only use the decision rule , they would have been better advised if they had thought about testing hypothesis

| () |

This choice can be justified by the integration order of the majority of economic series. By using the scheme 1, we can deduce that to test we must use the regression model

| () |

With the test hypotheses (2.10) and the regression model (2.11) we can use the decision rule ”( ou ), since the case is excluded.

2.1.2 Power and size of DGM’s FDF test.

The problem with the test based on the hypotheses and regression model and the test suggested above, based on and are useless in practice. The problem with the type tests is that they are based on a choice of two possible orders of integration and , of which the true order can be different either in the null or in the alternative. In fact, in the fractional integration case, there is a continuum of possible orders of integration. This would make the simple-versus-simple hypothesis invalid, particularly if the auxiliary regression model, used for the test, is based on the null and alternative. For instance, in the test one of the following three cases holds:

-

•

,

-

•

,

-

•

and .

The third case causes serious troubles in practice, particularly, if the statistic of the test depends on null and alternative hypothesis. When , in the first two cases, Dolado et al showed by means of a simulation study that their test procedure has a good performance in terms of power and level. For the third case, Dolado et al studied the effect of hypotheses misspecification by considering the deviations from the true value with size , and . In the following; however, we replicate the simulation results of Dolado et al and present them more clearly by using a single table. We generate series from the data generating process with sample size . The first column of Table gives the true values of the parameter while the second line shows the values of specified under the alternative. The first line gives the tabulated values by (see Dolado et al , table page ). The last line of Table represents the performance of the test in terms of level, i.e. the percentage of rejection of the null, when it is true (), while the main diagonal represents the performance of the test in terms of power i.e. the percentage of acceptance of the alternative hypothesis when it is true, (). and are respectively the type and the type errors, defined by

The other values in the table are the percentage of acceptance of the alternative hypothesis when both the null and alternative are false i.e. when the value of is wrongly specified. In fact, these values represents another type of errors, namely

When performing a test one may arrive at the correct decision, or one may commit one of two errors: rejecting the null hypothesis when it is true (type error, or error of the first kind) or accepting it when it is false (type error or error of the second kind). In statistical testing theory, there is no place for type error (or error of the third kind). This anomaly is the consequence of the choice of inappropriate auxiliary regression model, which depends on the null and alternative. From Table , it may be easily observed that when the true is well specified, the test has a good performance in terms of power and level. However, in the case where the true value of , the conclusions of the test are somewhat arbitrary. For example, when , the percentage of acceptance of the alternative is equal regardless of the alternative hypothesis. In other word, if the process , is fractionally integrated of order (i.e. stationary stationary process), the table , show that for against , we have

This example shows clearly that the risk to specify the stationary process as a nonstationary process is high.

![[Uncaptioned image]](/html/1209.1031/assets/x1.png)

argue that is not the best class of regression one can choose and propose another auxiliary regression model for the test . In the case they propose to test by using the following auxiliary model

where

The same criticisms can be formulated concerning test concerning test. The and tests present an analogy with the original Dickey-Fuller test, but can not be considered as a generalization of the familiar Dickey-Fuller test in the sense that the conventional vs framework is recovered (for the test the conventional framework is recovered only if and ). The implementation of test would require tabulations of the percentiles of the functional of fractional Brownian motion, which imply that the inference on the presence of unit root would be conditional on , and thus might suffer from misspecification resulting from errors in specifying the fractional parameter . When is not taken to be known a priory, a pre-estimation of it is needed to implement the test. In this case, we can perform the test only if the estimator of () is sufficiently close to unity (see for more details). Indeed, the table , show that the test have ”a realistic” behavior (i.e. likely results) in terms of size and power only when the true value of is close to (see for instance in table :, and ). This is why, recommend to use an estimator of that originates from the trimming rule

where is any -consistent estimator of , for example select in their simulation experiments. This rule makes this test more vague in how to use it in practice.

To extend adequately the standard Dickey-Fuller test , we propose a new test based on mutually exclusive and complementary null, alternative hypotheses and a suitable auxiliary regression model.

3 Fractional Dickey-Fuller testing: an alternative approach

3.1 Hypotheses, the auxiliary regression model and asymptotic under the null and the alternative

In this section, we deal with a series generated from the fractionally integrated model, , given by , where the order is any real number. Under this setting, we propose to test the following hypotheses333The special case of hypothesis testing against was presented at ICMSAO’13 Conference, Hammamet, Tunisia, 28–30 April 2013, in the paper entitled ”A consistent test for unit root against fractional alternative”. Expanded version of this paper forthcoming in Inderscience journal ”International Journal of operational research ”444This paper is an expanded version of the paper entitled ”New fractional Dickey-Fuller test” presented at ICMSAO’15 conference, Istanbul, May 27-29,2015 :

| () |

Our proposal is based upon testing the statistical significance of the coefficient (or ) in the following regression model,

| () |

or equivalently

| () |

where and are the residuals. The most important idea behind the choice of the framework above is that

More generally,

with

Before stating the main results of this paper, we give some technical tools that we need in the sequel. Let , with and defined as above. Let , where . When , we have (see Sowell

| () |

where denotes the Gamma or generalized factorial function. For the case , (see Liu,

| () |

Furthermore, under the following additional assumption for some , the following useful results apply:

| () |

and

| () |

where is the standard Brownian motion on associated with the sequence and the symbols and denotes respectively weak convergence and convergence in probability.

Since can always be decomposed as , where and , the following result provides the asymptotic distribution of the Dickey-Fuller normalized bias statistic and the Dickey-Fuller t-statistic, , in the least square esimate of the model .

Theorem 4

Let be generated from the DGP . If the regression model is fitted to a sample of size then, as ,

-

1.

satisfies

() () () () () -

2.

is such that

() () () () () () where is the fold integral of recursively defined as , with and denotes the standard Brownian motion.

Proof. See Appendix.

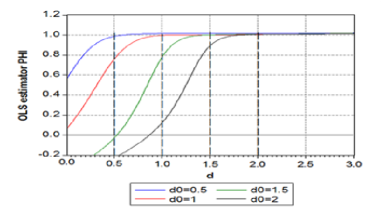

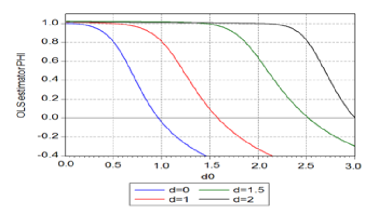

The later properties represent generalizations of those established by Sowell for the cases , and . From , and , the rate at which converges to zero (i.e. converge to ) is slow for non-positive values of , and is particularly very slow for . Moreover for , the limiting distribution of has non-positive support and then . From and , converges to zero at rate , when . The rate of convergence is faster than the usual standard rate , when we deal with stationary variables. Then, for , the least squares estimate is superconsistent. In other words, if a first order autoregression is fitted to a series generated from an , where is the order of integration of , then when , asymptotically, the estimator will not exceed in probability. Figure and Figure below illustrate this fact in an obvious way.

Figure shows that as long as , and as long as , where is the estimator in the autoregression model .

Example 5

For example, for , we have,

and for , we have,

Figure shows that as long as , we have , and whenever where is the estimator in the autoregression model .

Example 6

For example, when ,

and when

Figure is made as follows: For a fixed sample generated from a Gaussian process, samples of processes were generated for varying between and with step-size and fixed. Similarly, Figure is made as follows. For a series generated from a Gaussian process, samples from processes were generated for varying between and with step-size for fixed . For each series , a first order autoregression is fitted and an estimate of is calculated. By plotting the estimate against the fractional parameter , one obtains Figure and by plotting the parameter against the fractional parameter one obtains Figure . A general procedure for generating a fractionally integrated series with length is to apply the formula for .

Remark 7

By fixing the parameter and varying the parameter , we increase the order of integration of , and by varying the parameter and fixing the parameter we decrease the order of integration of .

The relationships between and and between and , highlighted by the results - and illustrated by Figures and , suggest that when we deal with testing the degree of fractional integration, we have

Like , we call the test which is based on the hypotheses and the auxiliary regression model , or equivalently as ”Fractional Dickey-Fuller test (- test in short).

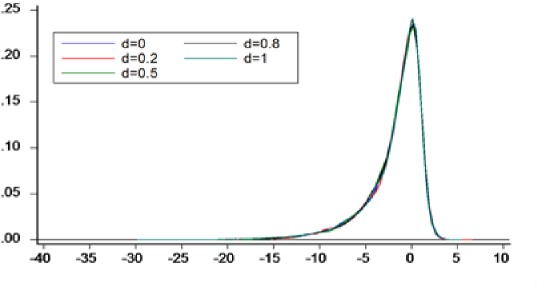

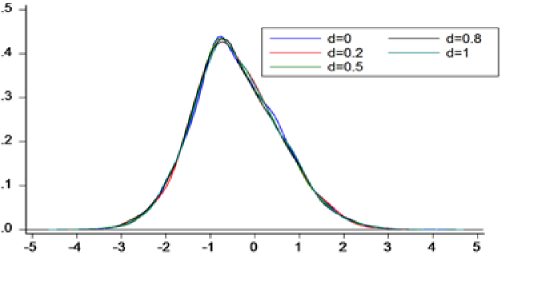

Another important property highlighted by Theorem is that the tests are invariant to the original value of , so the asymptotic properties only depend on . For example, we have used several series with sample size to estimate the densities (following Sowell ) of and under . The estimated densities are presented in Figures and above.

In figures and , for each one of the statistics and under with , the estimated densities for different values of are represented on the same graph. Figures and show that by fitting the regression model to the sample generated from , one obtains the same distribution as those used by Dickey-Fuller . In other words, as shown below, the proposed test, which is based on the regression model (or equivalently ) and the composite hypotheses , can be understood and implemented exactly as the simple Dickey-Fuller test for unit root by using the usual statistical tables of the conventional statistics and .

4 Power and size of the - test

4.1 Some theoretical aspects

Let and For a composite hypothesis, the parameter space is divided into disjoint regions, and . The test is written

| () |

For a series generated from with sample size we introduce two nonrandomized test defined by a function , on the sample space of the observations , with critical regions , . The test for a given rejection region is

| () |

The power of the test is defined by the function

measures the probability of rejecting the null hypothesis for a given and rejection region . The ideal test function has

and the test function yields the correct decision with probability nearly . The type and type errors can be summarized in the power function . For

and for ,

For the alternative hypothesis , we consider the one sided critical regions of the form

| () |

where is the level of the test and the critical points. The level of the test is given by

It measures the maximum probability of rejecting the null hypothesis when it is true. For the statistic , the figures and , where , show clearly that the supremum occurs at ,

For the statistic , the figure shows also clearly that

because the asymptotic distribution of is well defined, in all the real line for and diverge to for . The figures , and show that the level of the test is

| () |

Another technical argument that supports , is that the asymptotic distributions of and , , have positive support for and well defined in all the real line for . Consequently, the critical points are those used in the simple Dickey-Fuller test (i.e. without trend and intercept). Note that all the critical values are less than zero for , and . As indicated by , a test has level if its size is less than

![[Uncaptioned image]](/html/1209.1031/assets/x6.png)

![[Uncaptioned image]](/html/1209.1031/assets/x7.png)

![[Uncaptioned image]](/html/1209.1031/assets/x8.png)

Theorem 8

For a given level , a sequence of test , , defined by (4.1), with critical region (4.2) is consistent i.e.

Proof. First, we consider the statistic . For (i.e. ), since from result, , the asymptotic distribution of has non-positive support and , then we have

We have, also, , because has a positive support for , and Now consider the statistic . For For (i.e. ), using the same arguments as above we have,

For , with , when and when , we have

4.2 Simulation study

In this subsection, through a Monte Carlo study, we show that the proposed - test performs very well in terms of power and size when we use the statistic. To investigate the size and power of the - test, samples of Gaussian processes are generated and the regression model is used to estimate . The sample-sizes considered are and . Three values of are used ; . For each value, we specify the various values for . Letting be the set of values of for a given value of , the sets which will be used for the three values of are respectively

Table and Table give simulation results on the size of the test, (i.e. when ), where it may be easily seen that the - test, based on the auxiliary regression model , has good performances in terms of size since

Table and Table provide, also, the simulation results on the power of the test (i.e. when )

In this case, there are some conclusions to be drawn from it. First, the power of the - test increases with the increase of sample size and . For example, for , and , the power is for and for . When , and , the power is for and for . Second, as shown in table , for the power of the - test is below for () and for (, ). Third, for given , and , the power for , and are approximately similar because the asymptotic under the alternative does not depend on but only on . Finally, another important property showed by the table and is that the power function satisfies

A test for which the power function satisfies the conditions above is said to be unbiased.

![[Uncaptioned image]](/html/1209.1031/assets/x9.png)

![[Uncaptioned image]](/html/1209.1031/assets/x10.png)

Similar results are obtained for the statistic. Since has the non degenerate limit distribution, we choose to give the simulation results in the form of estimation density (by kernel methods, like Sowell . The figures and above summarize these results and support clearly those of Theorem .

5 Application to the Nelson-Plosser data

For the sake of illustration, this section applies our - test to the well-known Nelson-Plosser data. The starting date is for the consumer price index and industrial production, for velocity, for stock prices, for GNP deflator and money stock, for employment and unemployment rate, for bond yield, real wages and wages, and for the nominal and real GNP and GNP per capita. The variables are expressed in natural logarithms. All variables exhibit an upward trend with the exception of velocity, which shows a strong downward trend and the unemployment rate which tends to fluctuate around a constant level. The seminal empirical work by Nelson and Plosser suggests that there is a strong evidence for the unit root hypothesis for most macroeconomic time series data. Two possible specifications for the data generating processes are then

| (5.1) |

and

| (5.2) |

The theoretical framework provided in this paper does not allow us to use the (see Appendix ). At this level, we only use the . For the , we test the null for several values of , namely: ; ; ; and by using respectively the following regression models,

| (Model (I)) |

| (Model (II)) |

| (Model (III)) |

| (Model (IV)) |

| (Model (V)) |

Note that, the sample sizes for all the U.S. macroeconomic Nelson-Plosser series, used here, are between and . Consequently, the decision rules adopted for the testing problem are

where and are respectively the usual statistic and , and where are the corresponding critical values at level , obtained from the usual statistical tables of Dickey-Fuller . The results of the decision rules shown in Table suggest that:

-

•

for model , all series are found to be integrated with order ,

-

•

for model , all series are found to be integrated with order ,

-

•

for model , all series are found to be integrated with order ,

-

•

for model , all series are found to be integrated with order , except the Industrial production and Money stock series.

-

•

for model , all series are found to be integrated with order .

In summary, it may be concluded from Table that, following our test, all the macroeconomic variables are -integrated with , except for the Industrial production and Money stock whose order of integration is between and , i.e. .

![[Uncaptioned image]](/html/1209.1031/assets/x11.png)

Note that the - test was done assuming that the empirical variables are derived from data generating process . A more general study is needed to achieve adequate conclusions about the integration order for the Nelson-Plosser Data, by considering more general data generating process and also by incorporating non zero drift and time trend in data generating process while using a suitable auxiliary regression model.

6 Concluding remarks and discussion.

In the Dickey-Fuller paper, the parameter , without restrict the generality, can have only two values or . To test

| (Standard test) |

in the simple case, Dickey and Fuller use the regression model

| (Standard regression model) |

Since Anderson , White developed the statistical theory on the first order autoregressive process with the autoregressive parameter equal to (i.e. ) and greater than one (explosive process), Box and Jenkins formalized the analysis of time series, and Nelson and Plosser argue that the most macroeconomic series have unit roots. The unit root test has been an important topic on the econometric literatures.

Phillips show that under the null hypothesis (i.e. ) that the asymptotic distributions of and are respectively,

|

||||||

where is the standard Brownien motion. These later asymptotic distributions has been tabulated, the tabulated values are used to perform the standard test.

In fractional case the parameter can have an infinite values, for example can have an infinite number of values ; ; ; ; ; ; ; ; ; ;. For the fractional case, the standard regression model can be used only for testing the hypothesis . In our paper, the question is

| How to extend the standard framework above to take into account |

| the fractional case? |

Such extension has already been discussed by Dolado et Al . Dolado et al propose to test

by using the auxiliary regression model

| (DGM regression model) |

In this paper, we show in the first step, that the approach is not the best and adequate way to extend the Dickey-Fuller test by taking into account the fractional case, because the regression model is based on the null and the alternative (i.e. and ).

In the second step, we provide how to extend adequately the standard Dickey-Fuller test by taking into account the fractional case. In fact, in our approach, the question is

| How to extend the standard framework below to take into account |

| the fractional case by using the usual asymptotic distribution |

A correct answer to this question can be very useful in practice. The answer we give to this question is based on four points:

-

1.

Using the composite hypothesis

-

2.

If than

-

3.

Testing the composite null hypothesis is based upon testing the statistical significance of the coefficient (or ) in the regression model

-

4.

The level of the test

Our test is based on a composite null hypothesis, , this choice was not done arbitrarily. This choice was made based on the results of the asymptotic theory given in the theorem . To use our test, we recommend to follow the following steps:

-

1.

Estimate the parameter in the regression model This regression provides a more flexible and unified framework to test the null for different values of while using the same critical value.

-

2.

The null hypothesis is rejected if , where and . The level of the test can be approximated by its asymptotic value: ().

-

3.

The critical values () can be chosen so as to achieve a predetermined size by using the usual Dickey-Fuller statistical tables.

Finally, some remarks are in order:

- To implement our test we do not need to estimate the parameter .

- We have referred to our test as the Fractional Dickey-Fuller (-) test. A similar designation, -, has been adopted by Dolado et al for their test.

- Regarding the Dickey-Pantula test, both the upward and downward procedures are still valid in our fractional case (see Dickey and Pantula ). Moreover, by sequentially repeating the test in upward or in the downward senses, we can cover the value of at the desired accuracy.

- The empirical study on the Nelson-Plosser Data is only made to illustrate the - test.

- In this article we have not discussed the situation when there is an additional short memory component in the series, like the or . Also, the situation when there is a non-zero drift or a time trend in data generating process may be investigated. In fact, the proposed - test may be easily generalized to such situations. Here, we give just an indication when

where , is the backward shift operator, , the roots of are outside the unit circle and is defined as above. Then the fractional augmented Dickey-Fuller test, for the null hypothesis , would be based on the regression model

Further research is currently being undertaken toward generalizing the - testing approach, along similar directions as the test has been extended in the unit root literature accounting for time series which may exhibit a trending behavior and for general case.

References

- [1] Agiakloglou, C. and Newbold, P. Lagrange multplier tests for fractional difference, Journal of Time Series Analysis, (15), 253-262, .

- [2] Anderson, T.W. On the asymptotic distribution of estimates of parameters of stochastic difference equations, Ann.Math.Statist.,30, 676-687, .

- [3] Bensalma, A. A consistent against for unit root against fractional alternative, Fothcoming in International Journal of operational research, Inderscience Editor .

- [4] Bensalma, A. Unified theoretical framework for the unit root and fractional unit root, , arXiv:1209.1031v2.

- [5] Box, G.E.P., and G.M. Jenkins, Time series analysis: Forecasting and Control, Second Edition, Holden-Day, San Francisco, .

- [6] Candelon, B. and Gil-Alana. On finite Sample properties of the tests of Robinson (1994) for fractional integration, Journal of Statistical Computation and Simulation 73 (2), 445-464, .

- [7] Dickey, D.A. and Fuller, W.A. Distribution of the estimators for autoregressive time series with a unit root, Journal of the American Statistical Association 74 (366a), 427-431, .

- [8] Dickey, D.A. and Pantula, S.G. Determining the order of differencing in autoregressive processes, Journal of Business and Economic Statistics 15 (4), 455-461, .

- [9] Diebold, F.X., and Rudebush, G.D. On the power of the Dickey-Fuller test against fractional alternatives, Economic Letters 35 (2), 155-160, .

- [10] Dolado, J.J., Gonzalo, J. and Mayoral, M. A fractional Dickey-Fuller test for unit root, Econometrica 70 (5), 1963-2006, .

- [11] Granger, C.W.J. and Joyeux, R. An introduction to long memory time series models and fractional differencing, Journal of Time Series Analysis 1 (1), 15-29,

- [12] Hassler, U., Wolters, J. On the power of unit roots against fractionallyintegrated alternatives, Economic Letters 45 (1), 1-5, .

- [13] Hosking, J.R.M. Fractional differencing, Biométrika, 68 (1) 165-176, .

- [14] Krämer, W. Fractional integration and the augmented Dickey-Fuller test, Economics Letters 61, 269-272, .

- [15] Liu, M. Asymptotics of nonstationary fractional integrated series, Econometric Theory 14 (5), 641-662, .

- [16] Lobato, I.N. and Velasco, C. Optimal fractional Dickey-Fuller tests, Econometrics Journal 9 (3), 492-510, .

- [17] Lobato, I.N. and Velasco, C. Efficient Wald tests for fractional unit roots, Econometrica 75 (2), 575-589, .

- [18] Nelson, C.R. and Plosser, C.I. Trends and random walks in macroeconomic time series: some evidence and implications, Journal of Monetary Economics, 10 (2), 139-162, .

- [19] Philips, P.C.B., Time series regression with a unit root, Econometrica 55, 277-301, .

- [20] Robinson, P. M. Testing for strong serial correlation and dynamic conditional heteroskedasticity in multiple regression, Journal of Econometrics 47 67-84,

- [21] Robinson, P.M. Efficient tests of nonstationary hypotheses, Journal of the American Statistical Association 89 (428), 1420-1437, .

- [22] Said, S.E., and Dickey, D.A., Testing for unit roots in autoregressive moving average models of unknown order, Biometrika, 71, 3,pp. 599-607, .

- [23] Sowell, F.B. The fractional unit root distribution, Econometrica, 58 (2), 494-505, .

- [24] Tanaka, K. The nonstationary fractional unit root. Econometric Theory, 15 (4), 549-582, .

- [25] White, J.S., The limiting distribution of the serial correlation coefficient in the explosive case, Ann. Math. Statist, 29,1188-1197, .

- [26] White, J.S., The limiting distribution of the serial correlation coefficient in the explosive case II, Ann. Math. Statist, 30,831-384, .

Appendix 1: Proof of Theorem 1

By denoting , the estimator of and its -ratio for the auxiliary regression model , are given by the usual squares expressions

where the variance of the residuals, is given by . Note that, and . Since is stationary fractionally integrated process for and nonstationary fractional integrated process for , we divide our proof into two parts

-

1.

Part

When , given that is stationary fractionally integrated, of order and ergodic process, then

Therefore, given that

| () |

(see, Hosking ) and the recursive identity , it follows that

which, in turn, given that , entails that . Consequently, . With respect to the -test (i.e. ), it is straightforward to prove that

and then, by using and the recursive identity , it follows that

and

Consequently, and then

-

2

Part .

For the term, it follows from , , , and the continuous mapping theorem. When

| (A1) |

When

| (A2) |

When

| (A3) |

When

| (A4) |

When

| (A5) |

When ,

| (A6) |

For the term, we have

For the first term, it follows from (3.4), (3.5), (3.6), (3.7) and the continuous mapping theorem. When

| (A7) |

When

| (A8) |

When

| (A9) |

When

| (A10) |

When

| (A11) |

when

| (A12) |

For the second term, we have:

When , by using Lemma

of Ming Liu result

| (A13) |

When , by using and the ergodic theorem (note that here )

| (A14) |

When , by using and the ergodic theorem

| (A15) |

When , by using and the ergodic theorem (note that here )

| (A16) |

When , , by using , and the continuous mapping theorem

| (A17) |

When , , by using , and the continuous mapping theorem

| (A18) |

Therefore, when , we have, using and ,

| (A19) |

When , by using and , we have

| (A20) |

When , by using and , we have

| (A21) |

When , by using and , we have

| (A22) |

When , , by using and , we have

| (A23) |

When ,

| (A24) |

Hence, using respectively (A1,A19), (A2,A20), (A3,A21), (A4,A22), (A5,A23), (A6,A24) and the continuous mapping theorem, we obtain When

| (A25) |

When

| (A26) |

When

| (A27) |

When

| (A28) |

When

and then

when ,

| (A30) |

Now consider the -statistic. First notice that

. Hence, when , by using ,

and , it follows

| (A31) |

When , by using , , and , it follows

| (A32) |

When , by using , , and , it follows

| (A33) |

When , by using , , and , it follows

| (A34) |

When , , by using , , and , it follows

| (A35) |

When , by using , , and , it follows

| (A36) |

Finally, by using respectively (A1,A19,A31), (A2,A20,A32), (A3,A21,A33),

(A4,A22,A34) (A5,A23,A35), (A6,A24,A36) we obtain for the -statistic:

When and .

When

and

When and

When and

When

and

When ,

and

Appendix 2: test in the Presence of deterministic components

We assume that the univariate process can be generated by the following two mechanisms

| (A) |

and

| (B) |

where is as in . For and we can use the test without having to use their specific asymptotic theory. This can be done by differencing the process one time in and twice in . To be more clear, we consider testing hypotheses

| (C) |

even though, the framework provided in this paper does not allow us to use the and , we can , nevertheless use it as the following.

For the , the constant, , can be removed by first differencing,

and then, by transforming the in this way, instead , we consider testing hypotheses

by using the auxiliary regression model

For the , the constant, , and the parameter time trend, , can be removed by differencing twice the process ,

and then, for this transformed model, instead , we consider testing hypotheses

by using the auxiliary regression model