Nonparametric regression with homogeneous group testing data

Abstract

We introduce new nonparametric predictors for homogeneous pooled data in the context of group testing for rare abnormalities and show that they achieve optimal rates of convergence. In particular, when the level of pooling is moderate, then despite the cost savings, the method enjoys the same convergence rate as in the case of no pooling. In the setting of “over-pooling” the convergence rate differs from that of an optimal estimator by no more than a logarithmic factor. Our approach improves on the random-pooling nonparametric predictor, which is currently the only nonparametric method available, unless there is no pooling, in which case the two approaches are identical.

doi:

10.1214/11-AOS952keywords:

[class=AMS] .keywords:

.T2Supported by grants and fellowships from the Australian Research Council.

and

1 Introduction

In large screening studies where infection is detected by testing a fluid (e.g., blood, urine, water, etc.), data are often pooled in groups before the test is carried out, which permits savings in time and money. This technique, known as group testing, dates back at least to the Second World War, where Dorfman (1943) suggested using it to detect syphilis in US soldiers. It has been used in a variety of large screening studies, for example, to detect human immunodeficiency virus, or HIV [Gastwirth and Hammick (1989)], but pooling is also employed to detect pollution, for example, in water or milk; see Nagi and Raggi (1972), Wahed et al. (2006), Lennon (2007), Fahey, Ourisson and Degnan (2006). Often in these studies, one or several explanatory variables are available, in which case it is generally of interest to estimate the conditional probability of infection. This problem has received considerable attention in the group testing literature, where most suggested techniques are parametric; see, for example, Vansteelandt, Goetghebeur and Verstraeten (2000), Bilder and Tebbs (2009) and Chen, Tebbs and Bilder (2009). Related work includes that of Chen and Swallow (1990), Gastwirth and Johnson (1994), Hardwick, Page and Stout (1998) and Xie (2001).

Thus, although the original purpose of group testing was merely to identify infected individuals more economically, the idea has since been expanded extensively to include more general statistical methodology when the data have to be gathered through grouping. Our paper contributes in this context, developing and describing a particularly effective approach to nonparametric regression. Obtaining information in this way can be useful on its own, or for planning a subsequent study.

Recently, Delaigle and Meister (2011) suggested a nonparametric estimator of the conditional probability of infection. Their method enjoys optimal convergence rates when pooling is random, but it is not consistent in the case of nonrandom, homogeneous pooling, which can be defined as a setting where the covariates of individuals in a group take similar values. In the parametric context it is well known that homogeneous grouping improves the quality of estimators, but the potential gains of homogeneous grouping are even greater in the nonparametric context, where random grouping in moderate to large groups can seriously degrade the quality of estimators.

We demonstrate that, when the data are grouped homogeneously, one can construct more accurate nonparametric estimators of the conditional probability of infection. We show that these improved estimators enjoy faster, and optimal, convergence rates in a variety of contexts. Having reliable estimators of the conditional probability of infection enables more accurate identification of vulnerable categories of people, and can lead to subsequent studies that can assist individuals who are particularly vulnerable to infection. We illustrate the practical performance of our procedure via simulated examples and an application to the National Health and Nutrition Examination Survey (NHANES) study, a large health and nutrition survey collected in the US; see www.cdc.gov/nchs/nhanes.htm for more about the NHANES research program.

2 Model and methodology

2.1 Main group testing model

We observe independent and identically distributed (i.i.d.) data , where is a covariate observed on each of respective objects (e.g., items or individuals), each of which is subject to a potential, relatively rare “abnormality.” For example, could be the age or weight of an individual, and the abnormality could be contamination by HIV. Let denote the result of a test on the th object, such as blood or urine test. That is, takes the value 1 or 0 according to whether the abnormality is detected or not, respectively. In large screening studies, where is very large, testing each individual for contamination can be too expensive or take too much time, and to overcome this difficulty, it is common to pool data on several individuals before performing the detection test.

Pooling is performed by partitioning the original dataset , comprised of the values , into subsets, or groups, , say, where is of size and . We denote the elements of by . Each corresponds to an , and each has a concomitant . If the th element of is , then the concomitant of is . Instead of trying to determine the value of directly, each group is tested to discover whether the abnormality is present in the group, that is, to determine the value of

Of course, is obtained without observing the ’s directly; for example, when the abnormality is detected by a blood test, the bloods of all individuals in a group are mixed together, and this mixed blood is tested for contamination. From the data pairs we wish to estimate the probability function .

Since is a regression curve, then if the sample , were observed, we could use standard nonparametric regression techniques such as, for example, local polynomial estimators. Let be an integer, a bandwidth, a kernel function and . The standard th degree local polynomial estimator of is defined by

| (1) |

where , , with , and where and . See, for example, Fan and Gijbels (1996). Of course, when the data are pooled, the ’s are not available, and we cannot calculate such estimators. Therefore we need to develop specific ways to estimate from pooled data.

2.2 Method for homogeneous pools

Depending on the study, it is not always possible to observe the ’s before pooling the data, so that the individuals are pooled randomly. This is the context of the work of Delaigle and Meister (2011), who constructed a nonparametric estimator for the case where data are assigned randomly to the groups . See Appendix A.1 of the supplemental article [Delaigle and Hall (2011)] for a summary of properties of their estimator. In other studies, the ’s are observed beforehand; see, for example, the study of hepatitis C infection among 10,654 health care workers in Scotland, carried out by Thorburn et al. (2001). In such cases, it has already been demonstrated in the parametric context that it can be greatly advantageous to pool the data nonrandomly; see Vansteelandt, Goetghebeur and Verstraeten (2000).

Unfortunately, the only nonparametric estimator available for group testing data [see Delaigle and Meister (2011)] crucially relies on random grouping and is not valid when homogeneous groups are created. Below we suggest a new nonparametric approach which is valid with homogeneous pooling. We introduce our procedure in the case of a single covariate and equally sized groups. Generalizations of our method to unequal group sizes and multiple covariates will be treated in Section 5. These generalizations are similar in most respects.

To create homogeneous pools we divide the data into groups of equal number, taking the th group to be , where , in this case not depending on , is the number of data in each group, and denotes an ordering of the data in . We assume that divides ; the case where it does not is a particular case of our generalization in Section 5. Note that, with ,

| (2) |

The right-hand side here is generally close to , where denotes the average value of the ’s in the th group, and that closeness motivates the definition of at (4), below. Let

| (3) |

Reflecting (2) and the above discussion, we suggest estimating by

| (4) |

where is a nonparametric estimator of .

It remains to estimate . We begin by giving motivation for our methodology. Since, by construction, the groups are homogeneous, the observations in a given group are similar. In particular, are well approximated by . Together, this and identity (2) suggest that can be approximated by , so that is approximately equal to the average of the ’s over the ’s close to , which can be estimated by standard nonparametric regression estimators calculated from the data , . Motivated by these considerations, we define an th order local polynomial estimator of , constructed from the data , by

| (5) |

where and , with , , and .

3 Theoretical properties

To study properties of our estimator it is convenient to express the probability , at a particular , as

| (6) |

where denotes a sequence of positive numbers that potentially depend on , and is a fixed, nonnegative function. To be as general as possible, we permit the group size to increase, and to decrease, as diverges.

In large screening studies the abnormalities under investigation are invariably rare, that is, is small. To understand the limitations of our estimator, we shall study properties in the extreme situation where (and hence ) as . More precisely, we shall consider the “low prevalence” situation where as , which is an asymptotic representation of the case where the group size is relatively small and infection is rare. In practice, groups larger than to are rarely taken. One reason for this is that, depending on the proportion of positive individuals in the population, some tests (e.g., HIV tests) become too unreliable if the pool size is too large (larger than to 10 in the HIV example). To reflect this fact, we shall also consider the standard “moderate pooling” situation where as . However, there are tests for which groups could be taken as large as to . From the viewpoint of economics, large groups would be beneficial, and might even be the only possible way to screen individuals in poor countries. Hence we need to understand their effects on the quality of estimators. We shall do this by investigating asymptotic properties of our estimator in the extreme “over-pooling” situation where as .

3.1 Conditions

We shall derive theoretical properties of the estimator defined at (4), where for we shall generalize the local polynomial estimators introduced at (5), by considering a whole class of linear smoothers, defined by

| (7) |

where the weights depend on but not on the variables . The local polynomial estimator defined at (5) can be rewritten easily in this form, and other popular nonparametric estimators (e.g., smoothing splines) can be expressed in this form too; see, for example, Ruppert, Wand and Carroll (2003).

Recall that and let denote a sequence of constants decreasing to zero as . We can interpret as the bandwidth in a kernel-based construction of the weight functions in (7). Typically, the weights would depend on , and we assume that, for each , where is a given compact, nondegenerate interval:

Condition S.

(S1) ;

(S2) ;

(S3) ;

(S4) for each integer , , where the functions and are continuous on and are related to the type of estimator.

We also assume that:

Condition T.

(T1) the distribution of has a continuous density, , that is bounded away from zero on an open interval containing ;

(T2) is bounded away from 1 uniformly in and in ;

(T3) the function in (6) has two Hölder-continuous derivatives on ;

(T4) for some , as ;

(T5) the weights vanish for , where is a constant.

The assumption in (T1) that is bounded away from zero on a compact interval allows us to avoid pathological issues that arise when too few values of are available in neighbourhoods of zeros of . Finally, when describing the size of simultaneously in many values we shall ask that for some ,

| (8) |

For example, if the weights correspond to the local polynomial estimator in (5) with (i.e., the local linear estimator), with bandwidth and a compactly supported, symmetric, Hölder continuous, nonnegative kernel satisfying , and if for some , and (T1) holds, then (T5), Condition S and (8) hold with, in (S2) and (S3), (not depending on ) and . Furthermore, Condition S holds uniformly in . More generally it is easy to see that when , the th order local polynomial estimator in (5) satisfies for , and hence conditions (S1) and (S2) are trivially satisfied. Conditions (S3) and (S4) too are satisfied in this case, under mild conditions on the kernel. Note that condition (S1) is not satisfied in the local constant case [ in (5)]. Although this instance can be easily accommodated by modifying our conditions slightly, we simply omit it from our theory because in practice the local linear estimator is almost invariably preferred to the local constant one.

Remark 1.

Instead of linear smoothers, such as local polynomial estimators, we could use alternative procedures which are sometimes preferred in the context of binary dependent variables. For example, Fan, Heckman and Wand (1995) suggest modeling the regression curve by , where is a known link function, and is an unknown curve. These methods have theoretical properties similar to those of local polynomial estimators; the two methods differ mostly through their bias, and, depending on the shapes of and , one method has a smaller bias than the other. We prefer local polynomial estimators because they are easier to implement in practice.

3.2 Low prevalence and moderate pooling

Our first result establishes convergence rates and asymptotic normality for the estimator defined at (4), with at (7). Note that we do not insist that and vary with ; the regularity conditions for Theorem 3.1 hold in many cases where and are both fixed. Below we use the notation to denote the value taken by a function at a point , and the notation when referring to the function itself. However, in some places, for example, in result (9) where it is necessary to refer explicitly to the point mentioned in the statement “for all ,” and in definitions (10) and (11), where we are defining functions, the two notations may appear a little ambiguous.

Theorem 3.1

Assume that Conditions S and T hold, and that . Then, for each ,

| (9) |

where the distribution of converges to the standard normal law as , and the functions and are given by

| (10) | |||||

| (11) |

where and are as in (S2) and (S3). If, in addition, Condition S holds uniformly in , if (8) holds, and if the functions and are bounded and continuous, then

| (12) |

Note that and represent, to first order, the standard deviation of the error about the mean, and the main effect of bias, which arise from the asymptotic distribution. For simplicity we shall call and the asymptotic variance and bias of the estimator. From the theorem we see that, when (e.g., for the local polynomial estimator with ), if as , then the rate of the estimator is optimized when is of size , in which case the estimator satisfies

| (13) |

Note that when (no grouping), and our estimator of reduces to a standard local linear smoother of . For example, the estimator at (5) coincides with in (1). Taking in the theorem, we deduce that the convergence rate of our estimator for , given at (13), coincides with the rate for conventional linear smoothers employed with nongrouped data. By standard arguments it is straightforward to show that this rate is optimal when has two derivatives, and hence our estimator is rate optimal. Although, in (T3), we assume that has two continuous derivatives, continuity is imposed only so that the dominant term in an expansion of bias can be identified relatively simply, and the convergence rate at (13) can be derived without the assumption of continuity. In addition, note that when our estimator has the same asymptotic bias and variance expressions, and , as the estimator when , which in that case reduce to and . In other words, in that case the statistical cost of pooling is virtually zero.

The results discussed above also apply if performance is measured in terms of integrated squared error (ISE), as at (12). In particular, if is of size , provided that is bounded, the estimator achieves the minimax optimal convergence rate,

| (14) |

Remark 2.

Similar conclusions can be drawn in the case of estimators for which , but this requires us to assume that the function has enough derivatives so that an explicit, asymptotic, dominating, nonzero bias term can be derived. For example, for our local polynomial estimator of order , we have and the term is only an upper bound to the bias of the estimator. A nonvanishing asymptotic expression for the bias can easily be obtained for if we assume that has continuous derivatives. This can be done in a straightforward manner, but to keep presentation simple, and since in practice local linear estimators are almost invariably preferred to other local polynomial estimators, we omit such expansions.

Remark 3.

In the case where , it could be argued that the rates are meaningless since we are trying to estimate a function that tends to zero, and that it is more appropriate to consider the nonzero part of in the model at (6), and see how fast converges to . The convergence rate of is easily deducible from (13):

| (15) |

Provided that as , is consistent for , and the convergence rate evinced by (15) is optimal.

3.3 Over-pooling

The situation is quite different when as , which can be interpreted as an asymptotic representation of the situation where the data are pooled in groups of relatively large size . In practical terms the results in this section serve as a salutary warning not to skimp on the testing budget. The work in Section 3.2 shows that the performance of estimators is robust, up to a point, against increasing group size, but in the present section we demonstrate that, after the dividing line between moderate pooling and overpooling has been crossed, performance decreases sharply.

When , properties of the estimator of depend on , because there the order of magnitude of , at (3), depends critically on the rate at which converges to zero. The following condition captures this aspect:

| (16) |

and the following theorem replaces Theorem 3.1.

Theorem 3.2

Note that the orders of magnitude given by the second identities in each of (10) and (11) are not valid in this case, and neither does result (12) necessarily hold under the conditions of Theorem 3.2. Note too that the theorem can be extended to cases where , along the lines discussed in Remark 2. To elucidate the implications of Theorem 3.2, assume that is nonzero, and define , which, when , diverges exponentially fast as a function of . Given a sequence of constants and a sequence of random variables , write to indicate that both and as . Theorem 3.2 implies that, if and is a constant multiple of , then

| (17) |

and in particular diverges at a rate that is exponentially slower, as a function of , than in the case where , treated in Section 3.2. Result (17) follows from the fact that and , where means that is bounded away from zero and infinity. Note that (17) includes the case where (and hence ) is held fixed, and as .

The result at (17) shows that when as , suffers from a clear degradation of rates compared to the case where . Next we show that this degradation is intrinsic to the problem, not to our estimator ; any estimator based on the pooled data in Section 2.2 will experience an exponentially rapid decline in performance as . More precisely we show in Theorem 3.3 that, when as , is near rate-optimal among all such estimators. Recall that, under our model (6), , where potentially converges to zero. If , then, by (17), we have

| (18) |

Although this result was derived under the assumption that is a fixed function with two continuous derivatives, since (18) is only an upper bound, then it is readily established under the following more general assumption:

|

(19) |

Take the explanatory variables to be uniformly distributed on the interval , and let where 0 is an interior point of . Let , where satisfies (19), let denote the version of when , and consider the condition

| (20) |

This assumption permits to diverge with , but not too quickly. Indeed, using arguments similar to those in Section 6.3, it can be shown that if (20) fails, then no estimator of is consistent. Let be the class of measurable functions of the pooled data pairs introduced in Section 2.2.

Theorem 3.3

Except for the fact that , rather than , appears in (3.3), the latter result represents a converse to (18). The difference in powers here is of minor importance since the main issue is the factor , which (in the context of over-pooling), diverges faster than any power of , and this feature is represented in both (18) and (19).

3.4 Comparison with the approach of Delaigle and Meister

Arguments similar to those of Delaigle and Meister (2011) can be used to show that, under conditions similar to those used in our Theorem 3.1, their estimator [see (A.1) in the supplemental article, Delaigle and Hall (2011)] satisfies where the random variable has an asymptotic standard normal distribution and

| (22) | |||||

| (23) |

with . Likewise, the analog of (12) can be derived in the following way: To simplify the comparison, assume that we use estimators for which and do not vanish, and that . We see when comparing (22)–(23) with (10)–(11) that the asymptotic variance term of our estimator is an order of magnitude times smaller than . Note too the asymptotic bias terms of and are of the same size (the two biases are asymptotically equivalent if , and have the same magnitude in other cases). Hence, with our procedure, the gain in accuracy can be quite substantial, especially if is large.

4 Numerical study

We applied the local linear version of our local polynomial estimation procedure [i.e., the one based on (5) with ] on simulated and real examples. This method, which we denote below by DH, is the one we prefer because it works well, it is very easy to implement and we can easily derive and compute a good data-driven bandwidth for it. The practical advantages of local linear estimators over other local polynomial estimators have been discussed at length in the standard nonparametric regression literature. Of course, other versions of our general local linear smoother procedure can be used, such as a spline approach or more complicated iterative kernel procedures (see Remark 1). Each of the methods gives essentially the same estimator.

In our simulations we compared the DH procedure, calculated by definition from homogeneous groups, with the local linear estimator at (1) that we would use if we had access to the original nongrouped data. We also compared DH with the local linear version of the method of Delaigle and Meister (2011), which, by definition, is calculated from randomly created groups. We denote these two methods by LL and DM, respectively. We took the kernel, , equal to the standard normal density. For , in the DM case we used the plug-in bandwidth of Delaigle and Meister (2011) with their weight ; we used a similar plug-in bandwidth in the LL and DH cases; see Section A.2 of the supplemental article [Delaigle and Hall (2011)] for details.

4.1 Simulation results

To facilitate the comparison with the DM method, we simulated data according to the four models used by Delaigle and Meister (2011):

and or ;

and or ;

and or ;

and or .

We generated 200 samples from each model, with normal or uniform, and with , and . Then for the DH method we split each sample homogeneously into groups of equal sizes , or ; for the DM method, we created the groups randomly (remember that this estimator is valid only for random groups).

= Model LL DH DM DH DM DH DM (i) 122 (110) 29.2 (25.2) 16.8 (13.9) (ii) 166 (169) 35.8 (30.0) 19.1 (17.2) (iii) 19.9 (19.5) 4.48 (3.97) 2.28 (1.79) (iv) 39.7 (34.1) 9.62 (9.11) 5.47 (4.80)

To assess the performance of our DH estimator we calculated, in each case and for each of the 200 generated samples, the integrated squared error , with and denoting the 0.05 and 0.95 quantiles of the distribution of . We did the same for the DM and LL estimators and . For brevity, figures illustrating the results are provided in Section A.4 of the supplemental article [Delaigle and Hall (2011)], and here we show only summary statistics. In the graphs of Section A.4, we show the target curve (thin uninterrupted curve) as well as three interrupted curves; these were calculated from the samples that gave the first, second and third quartiles of the 200 ISE values.

= Model LL DH DM DH DM DH DM (i) 85.6 (72.8) 17.3 (18.8) 13.6 (11.0) (ii) 167 (202) 28.3 (36.9) 15.0 (17.7) (iii) 23.7 (27.3) 4.26 (4.93) 2.42 (2.58) (iv) 82.3 (75.2) 16.6 (18.1) 10.1 (9.96)

In Table 1 we show, for each model with uniform, the median (MED) and interquartile range (IQR) of the 200 ISE values obtained using the LL estimator based on nongrouped data, and, for several values of , the DH and the DM approaches based on data pooled in groups of size ; Table 2 shows the same but for normal. Note that LL cannot be calculated from grouped data, but we include it to assess the potential loss incurred by pooling the data. The tables show that for , pooling the data homogeneously hardly affects the quality of the estimator. Sometimes, the results are even slightly better with the DH method than with the LL one. Indeed a careful analysis of the bias and variance of the various estimators shows that for some curves , grouping homogeneously can sometimes be slightly beneficial when is small. (Roughly this is because by grouping a little we lose very little information, but we increase the number of positive, which makes the estimation a little easier for this particular estimator. Theoretical arguments support this conclusion.) The situation is much less favorable for the DM random grouping method, whose quality degrades quickly as increases. Unsurprisingly, DH beat DM systematically, except when was small ( and ), where the grouped observations did not suffice to estimate very well the curves from models (i) and (ii).

4.2 Real data application

We also applied our DH method on real data. To make the comparison with the LL estimator possible, we used data for which we had access to the entire, nongrouped set of observations . Then we grouped the data and compared the DH and LL procedures. We used data from the NHANES study, which are available at www.cdc.gov/ nchs/nhanes/nhanes1999-2000/nhanes99_00.htm. These data were collected in the US between 1999 and 2000.

As in Delaigle and Meister (2011), our goal was to estimate two conditional probabilities: and , where was the age of a patient, or indicating the absence or presence of antibody to hepatitis B virus core antigen in the patient’s serum or plasma and or indicating the absence or presence of genital Chlamydia trachomatis infection in the urine of the patient. The sample size was for and for . The percentage of ’s equal to one was in the HBc case and in the CL case. See Delaigle and Meister (2011) for more details on these data and the methods employed to collect them.

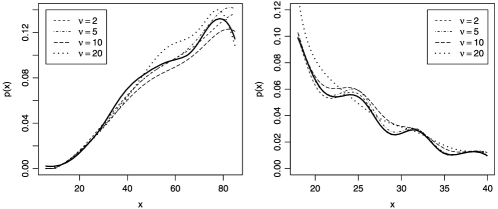

For brevity here we only present the results obtained using our method by pooling the data homogeneously in groups of equal size , , and . As in the simulations, our DH estimator improved considerably on the DM method. An illustration of our procedure with a second covariate is given in Section A.3 of the supplemental article [Delaigle and Hall (2011)]. In Figure 1 we compare DH with LL. All curves were calculated using our bandwidth procedure described in Section A.2 of the supplemental article [Delaigle and Hall (2011)]. We see that, in these examples, grouping data in pools of size as large as does not dramatically degrade performance.

5 Generalizations to unequal groups and the multivariate case

Our procedure for estimating can be extended to the multivariate setting, where the covariates are random -vectors, and to unequal group sizes. These extensions can be performed in many different ways, for example, by binning on each variable, using bins of potentially different sizes to accommodate different levels of homogeneity. If we group using bins of equal dimension, then, to a large extent, the theoretical properties discussed earlier, in the setting of equal-size groups, continue to hold. To briefly indicate this we give, below, details of methodology and results in the case of multivariate histogram binning where, for definiteness, the bin sizes and shapes, but not the group sizes, are equal. Cases where the bin sizes and shapes also vary can be treated in a similar manner, provided the variation is not too great, but since there are so many possibilities we do not treat those cases here. An approach of this type is discussed in Section A.3 of the supplemental article [Delaigle and Hall (2011)].

In the analysis below we take to be a -vector, and the function to be -variate, where . We group the data in bins of equal width, specifically width along each of the coordinate axes, rather than in groups of equal number. In the theory described below, for notational simplicity, we assume that the support of the distribution of contains the cube , and we estimate there. We choose so that is an integer (on this occasion is not necessarily an integer itself), and take the bins to be the cubes defined by

where for . In this setting it is convenient to write the paired data as simply , where is a -vector and each or 1, and refer to in terms of the bin in which it lies, rather than give it a double subscript (as in the notation , where is the bin index).

Put , representing the center of the bin , define

and compute by applying a -variate local polynomial smoother to the values of , interpreted as (explanatory variable, response variable) pairs in a conventional -variate nonparametric regression problem. To derive an estimator of from we take

| (24) |

where denotes the number of data in the bin containing .

In developing theoretical properties of this estimator we choose our regularity conditions to simplify exposition. In particular, we replace assumptions (S1)–(S4) and (T5) by the following restriction:

Condition U.

The nonparametric smoother defined by the estimator at (7) is a standard -variate local linear smoother [see, e.g., Fan (1993)], where the kernel , a function of variables, is a spherically symmetric, compactly supported, Hölder continuous probability density, and, for some , the bandwidth satisfies as .

Conditions (T1)–(T4) are replaced by (V1)–(V4) below, and (V5) is additional:

Condition V.

(V1) the distribution of has a continuous density, , that is bounded away from zero on an open set that contains the cube ;

(V2) the function is bounded below 1 uniformly on and in ;

(V3) the fixed, nonnegative function has two Hölder-continuous derivatives on ;

(V4) for some , as ;

(V5) for constants .

The “” term on the right-hand side of (25) has exactly the same size as the dominant remainder term, , on the right-hand side of (9) in Theorem 3.1, provided of course that we take in Theorem 5.1. Refinements given in Theorem 3.1 and in the results in Section 3.3 can also be derived in the present setting.

Theorem 5.1 is proved similarly to Theorem 3.1, and so is not derived in detail here. The main difference in the argument comes from incorporating a slightly different definition of , given by (24). For example, suppose is as defined at (24), and note that , where and denotes the density of . Since, in addition, , then where , and, much as in the argument leading to (33),

Now, is minimized by taking , and for this choice of we have

This quantity is not of smaller order than if and only if both and , where . This is in turn equivalent to

for constants , which is also equivalent to (V5). Therefore if (V5) holds, then we can deduce (25) from (5).

6 Technical arguments

6.1 Proof of Theorem 3.1

Let equal the maximum of over . The ratio equals the order of magnitude of the expected value of the width of the group that contains , and it can be proved that

|

(27) |

Note that, by (T4), for sufficiently small .

For let be the th derivative of , and put . Let denote the exponent of Hölder continuity of on ; see (T3); that is, uniformly in . Then, using (27) it can be proved that for each ,

uniformly in the sense of (27) and for each . [Assumption (T4) implies that for some .] Observe too that, uniformly in the same sense,

| (29) | |||

again uniformly in the sense of (27). [Note that, by (T4), .] Combining (7), (T4), (S1), (S2), (S4), (6.1) and (6.1) we deduce that, for each and each ,

whence, for all ,

uniformly in . Hence, defining

| (31) |

noting that is bounded away from zero [see (T2)], and taking the argument of the functions below to equal the specific point referred to in (9), we deduce that

| (33) | |||||

where (33) holds without the assumption [it holds under either that condition or (16)], but (33) requires . Note that, by (T4), for some , and so . Additionally, it will follow from (6.1) below that, when , , and by (T4), , so . The identity leading from (33) to (33) follows from this property.

Observe that, by (6.1) and (6.1), and

uniformly in such that , where is as in (T5), and moreover,

[Here and in (6.1)–(6.1) the argument of the functions is the point in (9).] Therefore, by (S3),

Properties (T4) and (6.1), and Lyapounov’s central limit theorem (see the next paragraph for details), imply that when and [the latter is assumed here and below; the proof when is simpler], we can write

where the second identity follows from the fact that for some [see (T4)], and denotes a random variable that is asymptotically distributed as normal N. This result and (33) imply that

When applying a generalized from of Lyapounov’s theorem to establish a central limit theorem for , conditional on , we should, in view of (S4), prove that for some integer , When this is equivalent to , and hence to ; call this result (R). Now, (T4) ensures that for some , . Therefore (R) holds for all sufficiently large .

Next we outline the derivation of (12). It can be proved from (8) that if is given, if is chosen sufficiently large, if is a regular grid of points in and if, for each , we define to be the point in nearest to , then

| (37) |

Note that, by (T4), applying (S3), (S4), Rosenthal’s and Markov’s inequalities, we can prove that, for each , It follows that, for all ,

| (38) |

Together (37) and (38) imply that, for each ,

| (39) |

Results (6.1) (which holds uniformly in ) and (39) imply that (33) holds uniformly in . Hence,

Conditional on the random variable , at (31), equals a sum of independent random variables with zero means, and using that property, Condition S (which, for this part of the theorem, holds uniformly in ) and (9), it can be proved that

| (41) | |||||

| (42) | |||||

| (43) |

Result (41) follows from (6.1). To derive (42), note that by (6.1) we have, uniformly in ,

where

again uniformly in . [The last and second-last identities here follow from (T4) and (S4), resp.] Noting these bounds, defining and integrating (6.1) over , we deduce that

which implies (42).

To derive (43), define and , write for the left-hand side of (43), and note that

In view of (T5), if , and so the series in the numerator inside the integrand can be confined to indices for which both and . Therefore the integrand equals zero unless . Hence, defining if , and otherwise, using the Cauchy–Schwarz inequality to derive both the inequalities below and writing for the length of the interval , we have

Using (6.1) show that , uniformly in , noting that uniformly in [the bound at (12) holds uniformly in the argument of ] and observing that uniformly in , whence it follows from the bound for that uniformly in , we deduce from (6.1) that

6.2 Proof of Theorem 3.2

The proof is similar to that of the first part of Theorem 3.1, the main difference occurring at the point at which the remainder term, where , in (33), is shown to be negligible relative to the term there. It suffices to prove that in probability, or equivalently, in view of (6.1), that . However, the latter result is ensured by (16).

6.3 Proof of Theorem 3.3

Without loss of generality, the point in (3.3) is . Recall that , and take , where is bounded and has two bounded derivatives on the real line, is supported on and satisfies . The respective functions and satisfy (19). [The quantity here is not a bandwidth, but converges to 0 as .] Therefore, except when . We assume that as , and consider the problem of discriminating between and using the data pairs .

Without loss of generality, we confine attention to those pairs for which is wholly contained in . Pairs for which has no intersection with convey no information for discriminating between and , and it is readily proved that including pairs for which overlaps the boundary does not affect the results we derive below. In a slight abuse of notation we shall take the integers for which to be , where and is assumed to be an integer.

The likelihood of the data pairs for , conditional on , is where Let and denote the versions of when and , respectively. Also, let and . In this notation the log-likelihood ratio statistic is given by

and therefore, , Writing and to denote expectation and variance when , we deduce that

| (48) | |||||

| (49) |

Assume for the time being that

| (50) |

as , and observe that, since , then

where , and uniformly in . [We used (50) to derive the last identity in (6.3). To obtain uniformity in the bound for , and in later bounds, we used the fact that is bounded.] Hence,

Similarly, since

then

uniformly in . It follows that

| (52) | |||

| (53) | |||

uniformly in . Using (48), (49), (6.3) and (6.3) we deduce that

Choose so that

| (54) |

In particular, take and hence

| (55) |

or equivalently, using the fact that ,

| (56) |

where are positive constants; can be chosen arbitrarily. It follows that

| (57) |

where . If is given by (57), then and therefore (50) follows from (20).

It can be shown that, conditional on the explanatory variables, the log-likelihood ratio , centred at the conditional mean and variance, is asymptotically normally distributed with zero mean and unit variance. (We shall give a proof below.) Therefore by taking , and hence , sufficiently small, we can ensure that: (i) The probability of discriminating between and , when , is bounded below 1 as . [This follows from (54).] Similarly it can be proved that: (ii) The probability of discriminating between and , when , is bounded below 1. Consider the assertion: (iii) converges in probability to 0, along a subsequence, at a strictly faster rate than . If (iii) is true, then the error rate of the classifier which asserts that if is closer to than to , and otherwise, and converges to 0 as . However, properties (i) and (ii) show that even the optimal classifier, based on the likelihood ratio rule, does not enjoy this degree of accuracy, and so (iii) must be false. This proves (3.3).

Finally we derive the asymptotic normality of claimed in the previous paragraph. We do this using Lindeberg’s central limit theorem, as follows. In view of the definition of at (6.3) it is enough to prove that for each ,

in probability, where we define

| (59) | |||||

| (60) |

with and (59) holding uniformly in . [We used (6.3) to obtain the second identities in each of (59) and (60).] Since , then, by (56) and (60), in probability, where . Hence, by (6.3), with probability converging to 1 as ,

where are constants, and depends on .

Acknowledgments

We thank three referees and an Associate Editor for their helpful comments which led to an improved version of the manuscript.

[id=suppA] \stitleAdditional material \slink[doi]10.1214/11-AOS952SUPP \sdatatype.pdf \sfilenameaos952_supp.pdf \sdescriptionThe supplementary article contains a description of Delaigle and Meister’s method, details for bandwidth choice, an alternative procedure for multivariate setting and unequal groups, and additional numerical results.

References

- Bilder and Tebbs (2009) {barticle}[mr] \bauthor\bsnmBilder, \bfnmChristopher R.\binitsC. R. and \bauthor\bsnmTebbs, \bfnmJoshua M.\binitsJ. M. (\byear2009). \btitleBias, efficiency, and agreement for group-testing regression models. \bjournalJ. Stat. Comput. Simul. \bvolume79 \bpages67–80. \biddoi=10.1080/00949650701608990, issn=0094-9655, mr=2655675 \bptokimsref \endbibitem

- Chen and Swallow (1990) {barticle}[pbm] \bauthor\bsnmChen, \bfnmC. L.\binitsC. L. and \bauthor\bsnmSwallow, \bfnmW. H.\binitsW. H. (\byear1990). \btitleUsing group testing to estimate a proportion, and to test the binomial model. \bjournalBiometrics \bvolume46 \bpages1035–1046. \bidissn=0006-341X, pmid=2085624 \bptokimsref \endbibitem

- Chen, Tebbs and Bilder (2009) {barticle}[mr] \bauthor\bsnmChen, \bfnmPeng\binitsP., \bauthor\bsnmTebbs, \bfnmJoshua M.\binitsJ. M. and \bauthor\bsnmBilder, \bfnmChristopher R.\binitsC. R. (\byear2009). \btitleGroup testing regression models with fixed and random effects. \bjournalBiometrics \bvolume65 \bpages1270–1278. \biddoi=10.1111/j.1541-0420.2008.01183.x, issn=0006-341X, mr=2756515 \bptokimsref \endbibitem

- Delaigle and Hall (2011) {bmisc}[auto:STB—2012/01/18—07:48:53] \bauthor\bsnmDelaigle, \bfnmA.\binitsA. and \bauthor\bsnmHall, \bfnmP.\binitsP. (\byear2011). \bhowpublishedSupplement to “Nonparametric regression with homogeneous group testing data.” DOI:10.1214/11-AOS952SUPP. \bptokimsref \endbibitem

- Delaigle and Meister (2011) {barticle}[auto:STB—2012/01/18—07:48:53] \bauthor\bsnmDelaigle, \bfnmA.\binitsA. and \bauthor\bsnmMeister, \bfnmA.\binitsA. (\byear2011). \btitleNonparametric regression analysis for group testing data. \bjournalJ. Amer. Statist. Assoc. \bvolume106 \bpages640–650. \bptokimsref \endbibitem

- Dorfman (1943) {barticle}[auto:STB—2012/01/18—07:48:53] \bauthor\bsnmDorfman, \bfnmR.\binitsR. (\byear1943). \btitleThe detection of defective members of large populations. \bjournalAnn. Math. Statist. \bvolume14 \bpages436–440. \bptokimsref \endbibitem

- Fahey, Ourisson and Degnan (2006) {barticle}[auto:STB—2012/01/18—07:48:53] \bauthor\bsnmFahey, \bfnmJ. W.\binitsJ. W., \bauthor\bsnmOurisson, \bfnmP. J.\binitsP. J. and \bauthor\bsnmDegnan, \bfnmF. H.\binitsF. H. (\byear2006). \btitlePathogen detection, testing, and control in fresh broccoli sprouts. \bjournalNutrition J. \bvolume5 \bpages13. \bptokimsref \endbibitem

- Fan (1993) {barticle}[mr] \bauthor\bsnmFan, \bfnmJianqing\binitsJ. (\byear1993). \btitleLocal linear regression smoothers and their minimax efficiencies. \bjournalAnn. Statist. \bvolume21 \bpages196–216. \biddoi=10.1214/aos/1176349022, issn=0090-5364, mr=1212173 \bptokimsref \endbibitem

- Fan and Gijbels (1996) {bbook}[mr] \bauthor\bsnmFan, \bfnmJ.\binitsJ. and \bauthor\bsnmGijbels, \bfnmI.\binitsI. (\byear1996). \btitleLocal Polynomial Modelling and Its Applications. \bseriesMonographs on Statistics and Applied Probability \bvolume66. \bpublisherChapman and Hall, \baddressLondon. \bidmr=1383587 \bptokimsref \endbibitem

- Fan, Heckman and Wand (1995) {barticle}[mr] \bauthor\bsnmFan, \bfnmJianqing\binitsJ., \bauthor\bsnmHeckman, \bfnmNancy E.\binitsN. E. and \bauthor\bsnmWand, \bfnmM. P.\binitsM. P. (\byear1995). \btitleLocal polynomial kernel regression for generalized linear models and quasi-likelihood functions. \bjournalJ. Amer. Statist. Assoc. \bvolume90 \bpages141–150. \bidissn=0162-1459, mr=1325121 \bptokimsref \endbibitem

- Gastwirth and Hammick (1989) {barticle}[mr] \bauthor\bsnmGastwirth, \bfnmJoseph L.\binitsJ. L. and \bauthor\bsnmHammick, \bfnmPatricia A.\binitsP. A. (\byear1989). \btitleEstimation of the prevalence of a rare disease, preserving the anonymity of the subjects by group testing: Applications to estimating the prevalence of AIDS antibodies in blood donors. \bjournalJ. Statist. Plann. Inference \bvolume22 \bpages15–27. \biddoi=10.1016/0378-3758(89)90061-X, issn=0378-3758, mr=0996796 \bptokimsref \endbibitem

- Gastwirth and Johnson (1994) {barticle}[auto:STB—2012/01/18—07:48:53] \bauthor\bsnmGastwirth, \bfnmJ. L.\binitsJ. L. and \bauthor\bsnmJohnson, \bfnmW. O.\binitsW. O. (\byear1994). \btitleScreening with cost-effective quality control: Potential applications to HIV and drug testing. \bjournalJ. Amer. Statist. Assoc. \bvolume89 \bpages972–981. \bptokimsref \endbibitem

- Hardwick, Page and Stout (1998) {barticle}[mr] \bauthor\bsnmHardwick, \bfnmJanis\binitsJ., \bauthor\bsnmPage, \bfnmConnie\binitsC. and \bauthor\bsnmStout, \bfnmQuentin F.\binitsQ. F. (\byear1998). \btitleSequentially deciding between two experiments for estimating a common success probability. \bjournalJ. Amer. Statist. Assoc. \bvolume93 \bpages1502–1511. \bidissn=0162-1459, mr=1666644 \bptokimsref \endbibitem

- Lennon (2007) {barticle}[pbm] \bauthor\bsnmLennon, \bfnmJay T.\binitsJ. T. (\byear2007). \btitleDiversity and metabolism of marine bacteria cultivated on dissolved DNA. \bjournalApplied and Environmental Microbiology \bvolume73 \bpages2799–2805. \biddoi=10.1128/AEM.02674-06, issn=0099-2240, pii=AEM.02674-06, pmcid=1892854, pmid=17337557 \bptokimsref \endbibitem

- Nagi and Raggi (1972) {barticle}[pbm] \bauthor\bsnmNagi, \bfnmM. S.\binitsM. S. and \bauthor\bsnmRaggi, \bfnmL. G.\binitsL. G. (\byear1972). \btitleImportance to “airsac” disease of water supplies contaminated with pathogenic Escherichia coli. \bjournalAvian Diseases \bvolume16 \bpages718–723. \bidissn=0005-2086, pmid=4562575 \bptokimsref \endbibitem

- Ruppert, Wand and Carroll (2003) {bbook}[mr] \bauthor\bsnmRuppert, \bfnmDavid\binitsD., \bauthor\bsnmWand, \bfnmM. P.\binitsM. P. and \bauthor\bsnmCarroll, \bfnmR. J.\binitsR. J. (\byear2003). \btitleSemiparametric Regression. \bseriesCambridge Series in Statistical and Probabilistic Mathematics \bvolume12. \bpublisherCambridge Univ. Press, \baddressCambridge. \biddoi=10.1017/CBO9780511755453, mr=1998720 \bptokimsref \endbibitem

- Thorburn et al. (2001) {barticle}[pbm] \bauthor\bsnmThorburn, \bfnmD.\binitsD., \bauthor\bsnmDundas, \bfnmD.\binitsD., \bauthor\bsnmMcCruden, \bfnmE.\binitsE., \bauthor\bsnmCameron, \bfnmS.\binitsS., \bauthor\bsnmGoldberg, \bfnmD.\binitsD., \bauthor\bsnmSymington, \bfnmI.\binitsI., \bauthor\bsnmKirk, \bfnmA.\binitsA. and \bauthor\bsnmMills, \bfnmP.\binitsP. (\byear2001). \btitleA study of hepatitis C prevalence in healthcare workers in the west of Scotland. \bjournalGut \bvolume48 \bpages116–120. \bidissn=0017-5749, pmcid=1728181, pmid=11115832 \bptokimsref \endbibitem

- Vansteelandt, Goetghebeur and Verstraeten (2000) {barticle}[mr] \bauthor\bsnmVansteelandt, \bfnmS.\binitsS., \bauthor\bsnmGoetghebeur, \bfnmE.\binitsE. and \bauthor\bsnmVerstraeten, \bfnmT.\binitsT. (\byear2000). \btitleRegression models for disease prevalance with diagnostic tests on pools of serum samples. \bjournalBiometrics \bvolume56 \bpages1126–1133. \biddoi=10.1111/j.0006-341X.2000.01126.x, issn=0006-341X, mr=1806746 \bptokimsref \endbibitem

- Wahed et al. (2006) {barticle}[auto:STB—2012/01/18—07:48:53] \bauthor\bsnmWahed, \bfnmM. A.\binitsM. A., \bauthor\bsnmChowdhury, \bfnmD.\binitsD., \bauthor\bsnmNermell, \bfnmB.\binitsB., \bauthor\bsnmKhan, \bfnmS. I.\binitsS. I., \bauthor\bsnmIlias, \bfnmM.\binitsM., \bauthor\bsnmRahman, \bfnmM.\binitsM., \bauthor\bsnmPersson, \bfnmL. A.\binitsL. A. and \bauthor\bsnmVahter, \bfnmM.\binitsM. (\byear2006). \btitleA modified routine analysis of arsenic content in drinking-water in Bangladesh by hydride generation-atomic absorption spectrophotometry. \bjournalJ. Health, Population and Nutrition \bvolume24 \bpages36–41. \bptokimsref \endbibitem

- Xie (2001) {barticle}[auto:STB—2012/01/18—07:48:53] \bauthor\bsnmXie, \bfnmM.\binitsM. (\byear2001). \btitleRegression analysis of group testing samples. \bjournalStat. Med. \bvolume20 \bpages1957–1969. \bptokimsref \endbibitem