-Penalization for Mixture Regression Models

Abstract

We consider a finite mixture of regressions (FMR) model for high-dimensional inhomogeneous data where the number of covariates may be much larger than sample size. We propose an -penalized maximum likelihood estimator in an appropriate parameterization. This kind of estimation belongs to a class of problems where optimization and theory for non-convex functions is needed. This distinguishes itself very clearly from high-dimensional estimation with convex loss- or objective functions, as for example with the Lasso in linear or generalized linear models. Mixture models represent a prime and important example where non-convexity arises.

For FMR models, we develop an efficient

EM algorithm for numerical optimization with provable convergence

properties. Our penalized estimator is

numerically better posed (e.g., boundedness of the

criterion function) than unpenalized maximum likelihood estimation, and it

allows for effective statistical regularization including variable

selection. We also present some asymptotic theory and oracle inequalities:

due to non-convexity of the negative log-likelihood function, different

mathematical arguments are needed than for problems with convex

losses. Finally, we apply

the new method to both simulated and real data.

Keywords Adaptive Lasso, Finite mixture models, Generalized EM algorithm, High-dimensional estimation, Lasso, Oracle inequality

This is the author’s version of the work (published as a discussion paper in TEST, 2010, Volume 19, 209-285). The final publication is available at www.springerlink.com.

1 Introduction

In applied statistics, tremendous number of applications deal with relating a random response variable to a set of explanatory variables or covariates through a regression-type model. The homogeneity assumption that the regression coefficients are the same for different observations is often inadequate. Parameters may change for different subgroups of observations. Such heterogeneity can be modeled with a Finite Mixture of Regressions (FMR) model. Especially with high-dimensional data, where the number of covariates is much larger than sample size , the homogeneity assumption seems rather restrictive: at least a fraction of covariates may exhibit a different influence on the response among various observations (i.e., sub-populations). Hence, addressing the issue of heterogeneity in high-dimensional data is important in many practical applications. We will empirically demonstrate with real data in Section 7.2 that substantial prediction improvements are possible by incorporating a heterogeneity structure to the model.

We propose here an -penalized method, i.e., a Lasso-type estimator (Tibshirani, 1996), for estimating a high-dimensional Finite Mixture of Regressions (FMR) model where . Our procedure is related to the proposal in Khalili and Chen (2007). However, we argue that a different parameterization leads to more efficient computation in high-dimensional optimization for which we prove numerical convergence properties. Our algorithm can easily handle problems where is in the thousands. Furthermore, regarding statistical performance, we present an oracle inequality which includes the setting where : this is very different from Khalili and Chen (2007) who use fixed asymptotics in the low-dimensional framework. Our theory for deriving oracle inequalities in the presence of non-convex loss functions, as the negative log-likelihood in a mixture model is non-convex, is rather non-standard but sufficiently general to cover other cases than FMR models.

From a more general point of view, we show in this paper that high-dimensional estimation problems with non-convex loss functions can be addressed with high computational efficiency and good statistical accuracy. Regarding the computation, we develop a rather generic block coordinate descent generalized EM algorithm which is surprisingly fast even for large . Progress in efficient gradient descent methods build on various developments by Tseng (2001) and Tseng and Yun (2008), and their use for solving Lasso-type convex problems has been worked out by, e.g., Fu (1998), Friedman et al. (2007), Meier et al. (2008) and Friedman et al. (2010). We present in Section 7.3 some computation times for the more involved case with non-convex objective function using a block coordinate descent generalized EM algorithm. Regarding statistical theory, almost all results for high-dimensional Lasso-type problems have been developed for convex loss functions, e.g., the squared error in a Gaussian regression (Greenshtein and Ritov, 2004; Meinshausen and Bühlmann, 2006; Zhao and Yu, 2006; Bunea et al., 2007; Zhang and Huang, 2008; Meinshausen and Yu, 2009; Wainwright, 2009; Bickel et al., 2009; Cai et al., 2009b; Candès and Plan, 2009; Zhang, 2009) or the negative log-likelihood in a generalized linear model (van de Geer, 2008). We present a non-trivial modification of the mathematical analysis of -penalized estimation with convex loss to non-convex but smooth likelihood problems.

When estimation is defined via optimization of a non-convex objective function, there is a major gap between the actual computation and the procedure studied in theory. The computation is typically guaranteed to find a local optimum of the objective function only, whereas the theory is usually about the estimator defined by a global optimum. Particularly in high-dimensional problems, it is difficult to compute a global optimum and it would be desirable to have some theoretical properties of estimators arising from local optima. We do not provide an answer to this difficult issue in this thesis. The beauty of, e.g., the Lasso or the Dantzig selector (Candès and Tao, 2007) in high-dimensional problems is the provable correctness or optimality of the estimator which is actually computed. A challenge for future research is to establish such provable correctness of estimators involving non-convex objective functions. A noticeable exception is presented in Zhang (2010) for linear models, where some theory is derived for an estimator based on a local optimum of a non-convex optimization criterion.

The rest of this article is mainly focusing on Finite Mixture of Regressions (FMR) models. Some theory for high-dimensional estimation with non-convex loss functions is presented in Section 5 for more general settings than FMR models. The further organization of the paper is as follows: Section 2 describes the FMR model with an appropriate parameterization, Section 3 introduces -penalized maximum-likelihood estimation, Sections 4 and 5 present mathematical theory for the low- and high-dimensional case, Section 6 develops some efficient generalized EM algorithm and describes its numerical convergence properties, and Section 7 reports on simulations, real data analysis and computational timings.

2 Finite mixture of Gaussian regressions model

Our primary focus is on the following mixture model involving Gaussian components:

| (1) | |||

Thereby, are fixed or random covariates, is a univariate response variable and denotes the free parameters and is given by . The model in (2) is a mixture of Gaussian regressions, where every component has its individual vector of regression coefficients and error variances . We are particularly interested in the case where .

2.1 Reparameterized mixture of regressions model

We prefer to work with a reparameterized version of model (2) whose penalized maximum likelihood estimator is scale-invariant and easier to compute. The computational aspect will be discussed in greater detail in Sections 3.1 and 6. Define new parameters

This yields a one-to-one mapping from in (2) to a new parameter vector

and the model (2) in reparameterized form then equals:

| (2) | |||

with . This is the main model we are analyzing and working with.

The log-likelihood function of this model equals

| (3) |

Since we want to deal with the case, we have to regularize the maximum likelihood estimator (MLE) in order to obtain reasonably accurate estimates. We propose below some -norm penalized MLE which is different from a naive -norm penalty for the MLE in the non-transformed model (2). Furthermore, it is well known that the (log-) likelihood function is generally unbounded. We will see in Section 3.2 that our penalization will mitigate this problem.

3 -norm penalized maximum likelihood estimator

We argue first for the case of a (non-mixture) linear model why the reparameterization above in Section 2.1 is useful and quite natural.

3.1 -norm penalization for reparameterized linear models

Consider a Gaussian linear model

| (4) |

where are either fixed or random covariates. In short, we often write

with vectors and , vector and matrix . In the sequel, denotes the Euclidean norm. The -norm penalized estimator, called the Lasso (Tibshirani (1996)), is defined as

| (5) |

Here is a non-negative regularization parameter. The Gaussian assumption is not crucial in model (3.1) but it is useful to make connections to the likelihood framework. The Lasso estimator in (5) is equivalent to minimizing the penalized negative log-likelihood as a function of the regression coefficients and using the -penalty : equivalence here means that we obtain the same estimator for a potentially different tuning parameter. But the Lasso estimator in (5) does not provide an estimate of the nuisance parameter .

In mixture models, it will be crucial to have a good estimator of and the role of the scaling of the variance parameter is much more important than in homogeneous regression models. Hence, it is important to take into the definition and optimization of the penalized maximum likelihood estimator: we could proceed with the following estimator,

| (6) |

Note that we are penalizing only the -parameter. However, the scale parameter estimate is influenced indirectly by the amount of shrinkage .

There are two main drawbacks of the estimator in (3.1). First, it is not equivariant (Lehmann, 1983) under scaling of the response. More precisely, consider the transformation

| (7) |

which leaves model (3.1) invariant. A reasonable estimator based on transformed data should lead to estimators which are related to through and . This is not the case for the estimator in (3.1). Secondly, and as important as the first issue, the optimization in (3.1) is non-convex and hence, some of the major computational advantages of Lasso for high-dimensional problems is lost. We address these drawbacks by using the penalty term leading to the following estimator:

This estimator is equivariant under the scaling transformation (7), i.e., the estimators based on transform as and . Furthermore, it penalizes the -norm of the coefficients and small variances simultaneously which has some close relations to the Bayesian Lasso (Park and Casella, 2008). For the latter, a Bayesian approach is used with a conditional Laplace prior specification of the form

and a noninformative scale-invariant marginal prior for . Park and Casella (2008) argue that conditioning on is important because it guarantees a unimodal full posterior.

Most importantly, we can re-parameterize to achieve convexity of the optimization problem

This then yields the following estimator which is equivariant under scaling and whose computation involves convex optimization:

| (8) |

From an algorithmic point of view, fast algorithms are available to solve

the optimization in (8). Shooting algorithms (Fu, 1998)

with coordinate-wise descent

are especially suitable, as demonstrated by, e.g., Friedman et al. (2007), Meier et al. (2008) or

Friedman et al. (2010). We describe in Section 6.1 an

algorithm for estimation in a mixture of regressions model, a more complex

task than

the optimization for (8). As we will see in Section

6.1, we

will make use of the Karush-Kuhn-Tucker (KKT) conditions in the M-Step of a

generalized EM algorithm. For the simpler criterion in

(8) for a non-mixture model, the KKT conditions imply the

following which we state without a proof. Denote by the inner product in -dimensional Euclidean space and by

the th column vector of .

Proposition 1.

3.2 -norm penalized MLE for mixture of Gaussian regressions

Consider the mixture of Gaussian regressions model in (2.1). Assuming that is large, we want to regularize the MLE. In the spirit of the approach in (8), we propose for the unknown parameter the estimator:

| (10) | ||||

| (11) | ||||

| (12) |

where with . The value of parameterizes three different penalties.

The first penalty function with is independent of the component probabilities . As we will see in Sections 6.1 and 6.4, the optimization for computing is easiest, and we establish a rigorous result about numerical convergence of a generalized EM algorithm. The penalty with works fine if the components are not very unbalanced, i.e., the true ’s aren’t too different. In case of strongly unbalanced components, the penalties with values are to be preferred, at the price of having to pursue a more difficult optimization problem. The value of has been proposed by Khalili and Chen (2007) for the naively parameterized likelihood from model (2). We will report in Section 7.1 about empirical comparisons with the three different penalties involving .

All three penalty functions involve the -norm of the component

specific

ratios and hence small variances are

penalized. The penalized criteria therefore stay finite whenever

: this is in sharp contrast to the unpenalized MLE

where the likelihood is unbounded if ; see, for example,

McLachlan and Peel (2000).

Proposition 2.

Assume that for all . Then the penalized negative log-likelihood is bounded from below for all values from (12).

A proof is given in Appendix C. Even though Proposition 2 is only stated and proved for the penalized negative log-likelihood with , we expect that the statement is also true for or .

Due to the -norm penalty, the estimator is shrinking some of the components of exactly to zero, depending on the magnitude of the regularization parameter . Thus, we can do variable selection as follows. Denote by

| (13) |

Here, is the th coefficient of the estimated regression parameter belonging to mixture component . The set denotes the collection of non-zero estimated, i.e., selected, regression coefficients in the mixture components. Note that no significance testing is involved, but, of course, depends on the specification of the regularization parameter and the type of penalty described by .

3.3 Adaptive -norm penalization

A two-stage adaptive -norm penalization for linear models has been proposed by Zou (2006), called the adaptive Lasso. It is an effective way to address some bias problems of the (one-stage) Lasso which may employ strong shrinkage of coefficients corresponding to important variables.

The two-stage adaptive -norm penalized estimator for a mixture of Gaussian regressions is defined as follows. Consider an initial estimate , for example, from the estimator in (10). The adaptive criterion to be minimized involves a re-weighted -norm penalty term:

| (14) | ||||

where . The estimator is then defined as

| (15) |

where is as in (12).

The adaptive Lasso in linear models has better variable selection properties than the Lasso, see Zou (2006), Huang et al. (2008), van de Geer et al. (2010). We present some theory for the adaptive estimator in FMR models in Section 4. Furthermore, we report some empirical results in Section 7.1 indicating that the two-stage adaptive method often outperforms the one-stage -penalized estimator.

3.4 Selection of the tuning parameters

The regularization parameters to be selected are the number of components , the penalty parameter and we may also want to select the type of the penalty function, i.e., selection of .

One possibility is to use a modified BIC criterion which minimizes

| (16) |

over a grid of candidate values for , and maybe also . Here, denotes the estimator in (10) using the parameters in (11), and is the negative log-likelihood. Furthermore, is the effective number of parameters (Pan and Shen, 2007).

Alternatively, we may use a cross-validation scheme for tuning parameter selection minimizing some cross-validated negative log-likelihood.

Regarding the grid of candidate values for , we consider , where is given by

| (17) |

At , all coefficients of the one-component model are exactly zero. Equation (17) easily follows from Proposition 1.

For the adaptive -norm penalized estimator minimizing the criterion in (3.3), we proceed analogously but replacing in (16) by in (15). As initial estimator in the adaptive criterion, we propose to use the estimate in (10) which is optimally tuned using the modified BIC or some cross-validation scheme.

4 Asymptotics for fixed and

Following the penalized likelihood theory of Fan and Li (2001), we establish first some asymptotic properties of the estimator in (11). As in Fan and Li (2001), we assume in this section that the design is random and that the number of covariates and the number of mixture components are fixed as sample size . Of course, this does not reflect a truly high-dimensional scenario, but the theory and methodology is much easier for this case. An extended theory for potentially very large in relation to is presented in Section 5.

Denote by the true parameter.

Theorem 1.

A proof is given in Appendix A. Theorem 1 can be easily misunderstood. It does not guarantee the existence of an asymptotically consistent sequence of estimates. The only claim is that a clairvoyant statistician (with pre-knowledge of ) can choose a consistent sequence of roots in the neighborhood of (van der Vaart, 2007). In the case where has a unique minimizer, which is the case for a FMR model with one component, the resulting estimator would be root- consistent. But for a general FMR model with more than one component and typically several local minimizers, this does not hold anymore. In this sense, the preceding theorem might look better than it is.

Next, we present an asymptotic oracle result in the spirit of Fan and Li (2001)

for the two-stage adaptive procedure described in

Section 3.3.

Denote by the population analogue of (13),

i.e., the set of non-zero regression coefficients. Furthermore, let

be the sub-vector of parameters corresponding to the true non-zero regression

coefficients (denoted by ) and analogously for .

Theorem 2.

(Asymptotic oracle result for

adaptive procedure)

Consider model (2.1) with random design, fixed and .

If , and if

satisfies , then, under the regularity

conditions (A)-(C) from Fan and Li (2001) on the joint density function of , there exists a

local minimizer of

in (3.3) () which satisfies:

-

1.

Consistency in variable selection: .

-

2.

Oracle Property: , where is the Fisher information knowing that (i.e., the submatrix of the Fisher information at corresponding to the variables in ).

A proof is given in Appendix A. As in Theorem 1, the assertion of the theorem is only making a statement about some local optimum. Furthermore, this result only holds for the adaptive criterion with weights coming from a root- consistent initial estimator : this is a rather strong assumption given the fact that Theorem 1 only ensures existence of such an estimator. The non-adaptive estimator with the -norm penalty as in (11) cannot achieve sparsity and maintain root- consistency due to the bias problem mentioned in Section 3.3 (see also Khalili and Chen (2007)).

5 General theory for high-dimensional setting with non-convex smooth loss

We present here some theory, entirely different from Theorems 1 and 2, which reflects some consistency and optimality behavior of the -norm penalized maximum likelihood estimator for the potentially high-dimensional framework with . In particular, we derive some oracle inequality which is non-asymptotic. We intentionally present this theory for -penalized smooth likelihood problems which are generally non-convex; -penalized likelihood estimation in FMR models is then a special case discussed in Section 5.3. The following Sections 5.1 - 5.2 introduce some mathematical conditions and derive auxiliary results and a general oracle inequality (Theorem 3); the interpretation of these conditions and of the oracle result is discussed for the case of FMR models at the end of Section 5.3.1.

5.1 The setting and notation

Let be a collection of densities with respect to the Lebesgue measure on (i.e., the range for the response variable). The parameter space is assumed to be a bounded subset of some finite-dimensional space, say

where we have equipped (quite arbitrarily) the space with the sup-norm . In our setup, the dimension will be regarded as a fixed constant (which still covers high-dimensionality of the covariates, as we will see). Then, equivalent metrics are, e.g., the ones induced by the -norm ().

We observe a covariate in some space and a response variable . The true conditional density of given is assumed to be equal to

where

That is, we assume that the true conditional density of given is depending on only through some parameter function . Of course, the introduced notation also applies to fixed instead of random covariates.

The parameter is assumed to have a nonparametric part of interest and a low-dimensional nuisance part , i.e.,

with

In case of FMR models, and involves the parameters . More details are given in Section 5.3.

With minus the log-likelihood as loss function, the so-called excess risk

is the Kullback-Leibler information. For fixed covariates , we define the average excess risk

and for random design, we take the expectation .

5.1.1 The margin

Following Tsybakov (2004) and van de Geer (2008) we call the behavior of the excess risk near the margin. We will show in Lemma 1 that the margin is quadratic.

Denote by

the log-density. Assuming the derivatives exist, we define the score function

and the Fisher information

Of course, we can then also look at using the parameter function .

In the sequel, we introduce some conditions (Conditions 1 - 5). Their

interpretation for the case of FMR models is given at the end of Section

5.3.1. First, we will assume boundedness of third

derivatives.

Condition 1 It holds that

where

For a symmetric, positive semi-definite matrix , we let

be its smallest eigenvalue.

Condition 2 For all ,

the Fisher information matrix is positive definite and, in fact,

Further we will need the following identifiability condition.

Condition 3 For all , there exists an

, such that

Based on these three conditions, we have the following result:

Lemma 1.

Assume Conditions 1, 2, and 3. Then

where

A proof is given in Appendix B.

5.1.2 The empirical process

We now specialize to the case where

where (with some abuse of notation)

We also write

to make the dependence of the parameter function on more explicit.

We will assume that

This can be viewed as a combined condition on and . For example, if is bounded by a fixed constant this supremum (for fixed ) is finite.

Our parameter space is now

| (18) |

Note that is, in principle, -dimensional. The true parameter is assumed to be an element of .

Let us define

and the empirical process for fixed covariates

We now fix some and and define the event

| (19) |

5.2 Oracle inequality for the Lasso for non-convex loss functions

For an optimality result, we need some condition on the design. Denote the active set, i.e., the set of non-zero coefficients, by

and let

Further, let

Condition 4 (Restricted eigenvalue condition). There exists a constant such that, for all satisfying

it holds that

For , we use the notation

We also write for ,

Thus

and the bound in the restricted eigenvalue condition then reads

Bounding in terms of can be done directly using, e.g., the Cauchy-Schwarz inequality. The restricted eigenvalue condition ensures a bound in the other direction which itself is needed for an oracle inequality. Some references about the restricted eigenvalue condition are provided at the end of Section 5.3.1.

We employ the Lasso-type estimator

| (20) |

We omit in the sequel the dependence of on . Note that we consider here a global minimizer which may be difficult to compute if the empirical risk is non-convex in . We then write . We let

which depends only on the estimate , and we denote by

Theorem 3.

A proof is given in Appendix B. We will give an interpretation of this result in Section 5.3.1, where we specialize to FMR models. In the case of FMR models, the probability of the set is large as shown in detail by Lemma 3 below.

Before specializing to FMR models, we present more general results for

lower bounding the probability of the set . We make the following

assumption.

Condition 5 For the score function , we have

for some function .

Condition 5 primarily has notational character. Later, in Lemma 2 and particularly in Lemma 3, the function needs to be sufficiently regular to ensure small corresponding probabilities.

Define

| (21) |

As we will see, we usually choose .

Let denote the conditional probability given

, and with the

expression we denote the indicator function.

Lemma 2.

A proof is given in Appendix B.

5.3 FMR models

In the finite mixture of regressions model from (2.1) with components, the parameter is , where the are the inverse standard deviations in mixture component and the are the mixture coefficients. For mathematical convenience and simpler notation, we consider here the -transformed and parameters in order to have lower and upper bounds for and . Obviously, there is a one-to-one correspondence between and from Section 2.1.

Let the parameter space be

| (22) |

and .

We consider the estimator

| (23) |

This is the estimator from Section 3.2 with . We emphasize the boundedness of the parameter space by using the notation . In contrast to Section 4, we focus here on any global minimizer of the penalized negative log-likelihood which is arguably difficult to compute.

In the following, we transform the estimator to in the parameterization from Section 2.1. Using some abuse of notation we denote the average excess risk by .

5.3.1 Oracle result for FMR models

We specialize now our results from Section 5.2 to FMR

models.

Proposition 3.

Proof.

This follows from straightforward calculations. ∎

In order to show that the probability for the set is large, we

invoke Lemma 2 and the following result.

Lemma 3.

A proof is given in Appendix B.

Hence, the oracle result in Theorem 3 for our -norm

penalized estimator in the FMR model holds on a set , summarized in Theorem 4, and this

set has large probability due to Lemma 2 and

Lemma 3 as described in the following corollary.

Corollary 1.

Theorem 4.

(Oracle result for FMR models). Consider a fixed design FMR model as in (2.1) with in (5.3). Assume Condition 4 (restricted eigenvalue condition) and that for the estimator in (23). Then on , which has large probability as stated in Corollary 1, for the average excess risk (average Kullback-Leibler loss),

where and are defined in Lemma 1 and Condition 4, respectively.

The oracle inequality of Theorem 4 has the following well-known interpretation. First, we obtain

That is, the average Kullback-Leibler risk is of the order (take , use definition (21) and the assumption on in Lemma 3 above) which is up to the factor the optimal convergence rate if one would know the non-zero coefficients. As a second implication we obtain

saying that the noise components in have small estimated values (e.g., its -norm converges to zero at rate ).

Note that the Conditions 1, 2, 3 and 5 hold automatically for FMR models, as described in Proposition 3. We do require a restricted eigenvalue condition on the design, here Condition 4. In fact, for the Lasso or Dantzig selector in linear models, restricted eigenvalue conditions (Koltchinskii, 2009; Bickel et al., 2009) are considerably weaker than coherence conditions (Bunea et al., 2007; Cai et al., 2009a) or assuming the restricted isometry property (Candès and Tao, 2005; Cai et al., 2009b); for an overview among the relations, see van de Geer and Bühlmann (2009).

5.3.2 High-dimensional consistency of FMR models

We finally give a consistency result for FMR models under weaker

conditions than the oracle result from Section 5.3.1. Denote by the true parameter

vector in a FMR model. In contrast to Section 4, the number

of covariates can grow with the

number of observations . Therefore, also the true parameter

depends on . To guarantee consistency we have to assume some sparsity

condition, i.e., the -norm of the true parameter can only grow

with .

Theorem 5.

6 Numerical optimization

We present a generalized EM (GEM) algorithm for optimizing the criterion in (11) in Section 6.1. In Section 6.2 and 6.3, we give further details on speeding-up and on initializing the algorithm. Finally, we discuss numerical convergence properties in Section 6.4. For the convex penalty () function, we prove convergence to a stationary point.

6.1 GEM algorithm for optimization

Maximization of the log-likelihood of a mixture density is often done using the traditional EM algorithm of Dempster et al. (1977). Consider the complete log-likelihood

Here , , are i.i.d. unobserved multinomial variables showing the component-membership of the th observation in the FMR model: if observation belongs to component , and otherwise. The expected complete (scaled) negative log-likelihood is then

and the expected complete (scaled) penalized negative log-likelihood is

The EM algorithm works by alternating between the E- and M-Step. Denote the

parameter value at EM-iteration by (), where is a vector of starting

values.

E-Step: Compute ,

or equivalently for and

Generalized M-Step: Improve w.r.t .

-

a)

Improvement with respect to :

fix at the present value and improve

(24) with respect to the probability simplex

Denote by which is a feasible point of the simplex. We propose to update as

where . In practice, is chosen to be the largest value in the grid () such that (24) is not increased. In our examples, worked well.

-

b)

Coordinate descent improvement with respect to and :

A simple calculation shows that the M-Step decouples for each component into distinct optimization problems of the form

(25) with

Problem (25) has the same form as (8); in particular, it is convex in . Instead of fully optimizing (25), we only minimize with respect to each of the coordinates, holding the other coordinates at their current value. Closed-form coordinate updates can easily be computed for each component () using Proposition 1:

where is defined as

and .

Because we only improve instead of a full minimization, see M-Step a) and b), this is a generalized EM (GEM) algorithm. We call it the block coordinate descent generalized EM algorithm (BCD-GEM); the word block refers to the fact that we are updating all components of at once. Its numerical properties are discussed in Section 6.4.

Remark 1.

For the convex penalty function with , a minimization with respect to in M-Step a) is achieved with , i.e., using . Then, our M-Step corresponds to exact coordinate-wise minimization of .

6.2 Active set algorithm

There is a simple way to speed-up the algorithm described above. When updating the coordinates in the M-Step b), we restrict ourselves during every 10 EM-iterations to the current active set (the non-zero coordinates) and visit the remaining coordinates every 11th EM-iteration to update the active set. In very high-dimensional and sparse settings, this leads to a remarkable decrease in computational times. A similar active set strategy is also used in Friedman et al. (2007) and Meier et al. (2008). We illustrate in Section 7.3 the gain of speed when staying during every 10 EM-iterations within the active set.

6.3 Initialization

The algorithm of Section 6.1 requires the specification of starting values . We found empirically that the following initialization works well. For each observation , , draw randomly a class . Assign for observation and the corresponding component the weight and weights for all other components. Finally, normalize , , to achieve that summing over the indices yields the value one, to get the normalized values . Note that this can be viewed as an initialization of the E-Step. In the M-Step which follows afterwards, we update all coordinates from the initial values , , , , .

6.4 Numerical convergence of the BCD-GEM algorithm

We address here the convergence properties of the BCD-GEM algorithm described in Section 6.1. A detailed account of the convergence properties of the EM algorithm in a general setting has been given by Wu (1983). Under regularity conditions including differentiability and continuity, convergence to stationary points is proved for the EM algorithm. For the GEM algorithm, similar statements are true under conditions which are often hard to verify.

As a GEM algorithm, our BCD-GEM algorithm has the descent property which means that the criterion function is reduced in each iteration:

| (27) |

Since is bounded from below

(Proposition 2), the following result holds.

Proposition 4.

For the BCD-GEM algorithm, decreases monotonically to some value .

In Remark 1, we noted that, for the convex penalty function with , the M-Step of the

algorithm corresponds to exact coordinate-wise minimization of

. In this case, convergence

to a stationary point can be shown.

Theorem 6.

A precise definition of a stationary point in a non-differentiable setup and a proof of the Theorem are given in Appendix C. The proof uses the crucial facts that is a convex function in and that it is strictly convex in each coordinate of .

7 Simulations, real data example and computational timings

7.1 Simulations

We consider four different simulation setups. Simulation scenario 1 compares the performance of the unpenalized MLE with our estimators from Section 3.2 (FMRLasso) and Section 3.3 (FMRAdapt) in a situation where the total number of noise covariates grows successively. For computing the unpenalized MLE, we used the R-package FlexMix (Leisch, 2004; Grün and Leisch, 2007, 2008); Simulation 2 explores sparsity; Simulation 3 compares cross-validation and BIC; and Simulation 4 compares the different penalty functions with the parameters . For every setting, the results are based on 100 independent simulation runs.

All simulations are based on Gaussian FMR models as in (2); the coefficients and the sample size are specified below. The covariate is generated from a multivariate normal distribution with mean 0 and covariance structure as specified below.

Unless otherwise specified, the penalty with is used in all simulations. As explored empirically in Simulation 4, in case of balanced problems (approximately equal ), the FMRLasso performs similarly for all three penalties. In unbalanced situations, the best results are typically achieved with . In addition, unless otherwise specified, the true number of components is assumed to be known.

For all models, training-, validation- and test data are generated of equal size . The estimators are computed on the training data, with the tuning parameter (e.g., ) selected by minimizing twice the negative log-likelihood (log-likelihood loss) on the validation data. As performance measure, the predictive log-likelihood loss (twice the negative log-likelihood) of the selected model is computed on the test data.

Regarding variable selection, we count a covariable as selected if for at least one . To assess the performance of FMRLasso on recovering the sparsity structure, we report the number of truly selected covariates (True Positives) and falsely selected covariates (False Positives).

Obviously, the performances depend on the signal-to-noise ratio (SNR) which we define for an FMR model as

where the last equality follows since .

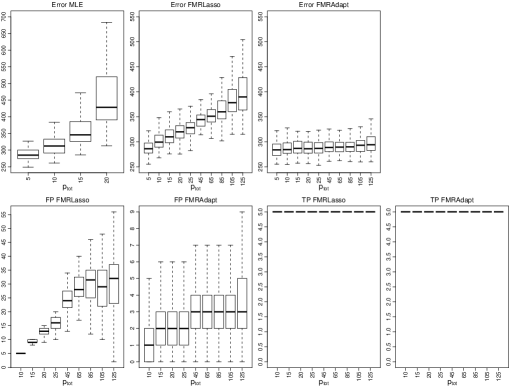

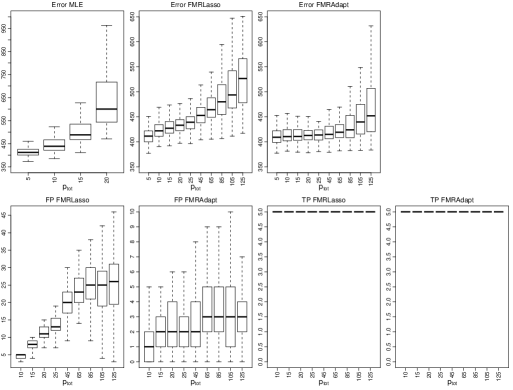

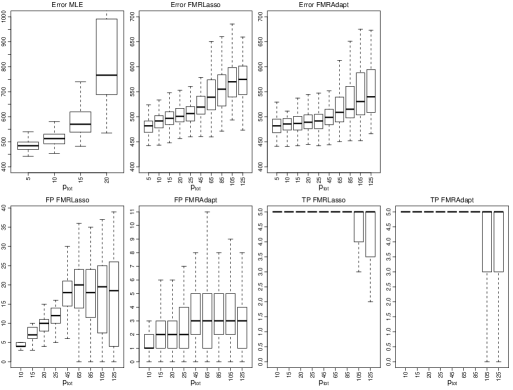

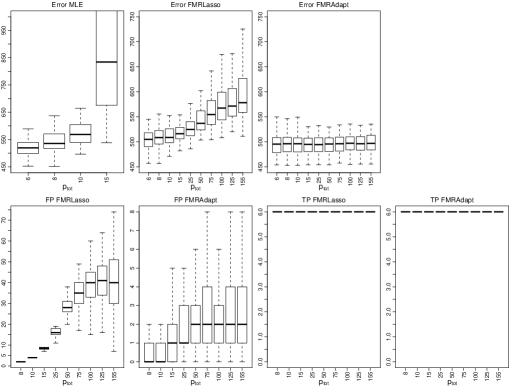

7.1.1 Simulation 1

We consider five different FMR models: M1, M2, M3, M4 and M5. The parameters , the sample size of the training-, validation- and test-data, the correlation structure of covariates and the signal-to-noise ratio (SNR) are specified in Table 1. Models M1, M2, M3 and M5 have two components and five active covariates, whereas model M4 has three components and six active covariates. M1, M2 and M3 differ only in their variances , and hence have different signal-to-noise ratios. Model M5 has a non-diagonal covariance structure. Furthermore, in model M5, the variances , are tuned to achieve the same signal-to-noise ratio as in model M1.

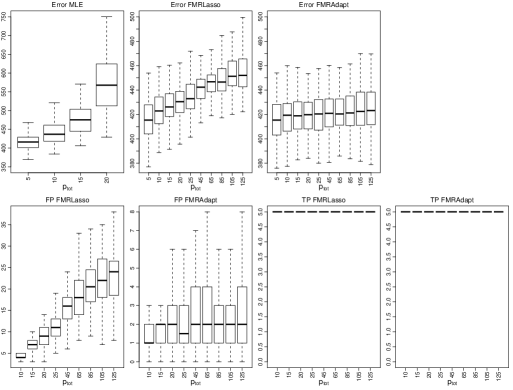

We compare the performances of the maximum likelihood estimator (MLE), the FMRLasso and the FMRAdapt in a situation where the number of noise covariates grows successively. For the models M1, M2, M3, M5 with two components, we start with (no noise covariates) and go up to (120 noise covariates). For the three component model M4, we start with (no noise covariates) and go up to (149 noise covariates).

The boxplots in Figures 1 - 5 of the predictive log-likelihood loss, denoted by Error, the True Positives (TP) and the False Positives (FP) over 100 simulation runs summarize the results for the different models. We read off from these boxplots that the MLE performs very badly when we add noise covariates. On the other hand, our penalized estimators remain stable. For example, for M1 the MLE with performs worse than the FMRLasso with , or for M4 the MLE with performs worse than the FMRLasso with . Impressive is also the huge gain of the FMRAdapt method over FMRLasso in terms of log-likelihood loss and false positives.

| M1 | M2 | M3 | M4 | M5 | |

| n | 100 | 100 | 100 | 150 | 100 |

| (3,3,3,3,3) | (3,3,3,3,3) | (3,3,3,3,3) | (3,3,0,0,0,0) | (3,3,3,3,3) | |

| (-1,-1,-1,-1,-1) | (-1,-1,-1,-1,-1) | (-1,-1,-1,-1,-1) | (0,0,-2,-2,0,0) | (-1,-1,-1,-1,-1) | |

| - | - | - | (0,0,0,0,-3,2) | - | |

| 0.5, 0.5 | 1, 1 | 1.5, 1.5 | 0.5, 0.5, 0.5 | 0.95, 0.95 | |

| 0.5, 0.5 | 0.5, 0.5 | 0.5, 0.5 | 1/3, 1/3, 1/3 | 0.5, 0.5 | |

| SNR | 101 | 26 | 12.1 | 53 | 101 |

7.1.2 Simulation 2

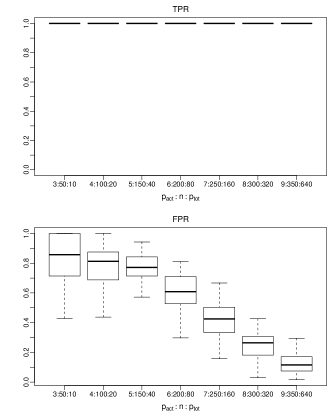

In this section, we explore the sparsity properties of the FMRLasso. The model specifications are given in Table 2. Consider the ratios . The total number of covariates grows faster than the number of observations and the number of active covariates : when is doubled, is raised by one and is raised by from model to model. In particular, we obtain a series of models which gets “sparser” as grows (larger ratio ). In order to compare the performance of the FMRLasso, we report the True Positive Rate (TPR) and the False Positive Rate (FPR) defined as:

These numbers are reported in Figure 6. We see that the False Positive Rate approaches zero for sparser models, indicating that the FMRLasso recovers the true model better in sparser settings regardless of the large number of noise covariates.

| 3 | 4 | 5 | 6 | 7 | 8 | 9 | |

|---|---|---|---|---|---|---|---|

| n | 50 | 100 | 150 | 200 | 250 | 300 | 350 |

| 10 | 20 | 40 | 80 | 160 | 320 | 640 | |

| (3, 3, 3, 0, 0, …) | |||||||

| (-1, -1, -1, 0, 0, …) | |||||||

| 0.5, 0.5 | |||||||

| 0.5, 0.5 |

7.1.3 Simulation 3

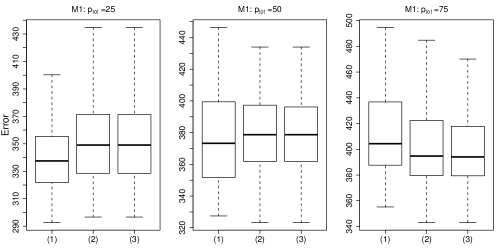

So far, we regarded the number of components as given, while we have chosen an optimal by minimizing the negative log-likelihood loss on validation data. In this section, we compare the performance of 10-fold cross-validation and the BIC criterion presented in Section 3.4 for selecting the tuning parameters and . We use model M1 of Section 7.1.1 with . For each of these models, we tune the FMRLasso estimator according to the following strategies:

-

(1)

Assume the number of components is given (). Choose the optimal tuning parameter using 10-fold cross-validation.

-

(2)

Assume the number of components is given (). Choose by minimizing the BIC criterion (16).

-

(3)

Choose the number of components and by minimizing the BIC criterion (16).

The results of this simulation are presented in Figure 7, where boxplots of the log-likelihood loss (Error) are shown. All three strategies perform equally well. With the BIC criterion in strategy (3) always chooses . For the model with , strategy (3) chooses in simulation runs and in two runs. Finally, with , the third strategy chooses in runs and eight times.

7.1.4 Simulation 4

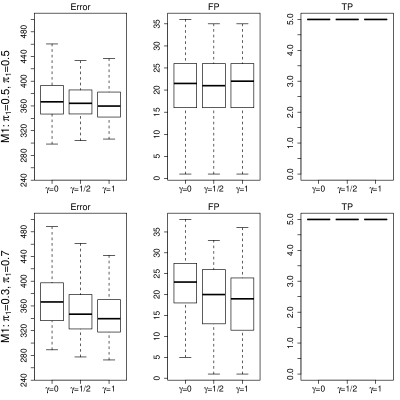

In the preceding simulations, we always used the value in the penalty term of the FMRLasso estimator (11). In this section, we compare the FMRLasso for different values . First, we compute the FMRLasso for on model M1 of Section 7.1.1 with . Then we do the same calculations for an “unbalanced” version of this model with and .

In Figure 8, the boxplots of the log-likelihood loss (Error), the False Positives (FP) and the True Positives (TP) over 100 simulation runs are shown. We see that the FMRLasso performs similarly for . Nevertheless, the value is slightly preferable in the “unbalanced” setup.

7.2 Real data example

We now apply the FMRLasso to a dataset of riboflavin (vitamin ) production by Bacillus Subtilis. The real-valued response variable is the logarithm of the riboflavin production rate. The data has been kindly provided by DSM (Switzerland). There are covariates (genes) measuring the logarithm of the expression level of 4088 genes and measurements of genetically engineered mutants of Bacillus Subtilis. The population seems to be rather heterogeneous as there are different strains of Bacillus Subtilis which are cultured under different fermentation conditions. We do not know the different homogeneity subgroups. For this reason, a FMR model with more than one component might be more appropriate than a simple linear regression model.

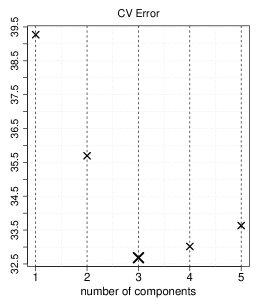

We compute the FMRLasso estimator for components. To keep the computational effort reasonable, we use only the 100 covariates (genes) exhibiting the highest empirical variances. We choose the optimal tuning parameter by 10-fold cross-validation (using the log-likelihood loss). As a result, we get five different estimators which we compare according to their cross-validated log-likelihood loss (CV Error). These numbers are plotted in Figure 9. The estimator with three components performs clearly best, resulting in a 17% improvement in prediction over a (non-mixture) linear model, and it selects 51 genes. In Figure 10, the coefficients of the most important genes, ordered according to , are shown. From the important variables, only gene 83 shows the opposite sign of the estimated regression coefficients among the three different mixture components. However, it happens that some covariates (genes) exhibit a strong effect in one or two mixture components but none in the remaining other components. Finally, for comparison, the one-component (non-mixture) model selects 26 genes, of which 24 are also selected in the three-component model.

7.3 Computational timings

In this section, we report on the run times of the BCD-GEM algorithm on two high-dimensional examples. In particular, we focus on the substantial gain of speed achieved by using the active set version of the algorithm described in Section 6.2. All computations were carried out with the statistical computing language and environment R. Timings depend on the stopping criterion used in the algorithm. We stop the algorithm if the relative function improvement and the relative change of the parameter vector are small enough, i.e.,

with

We consider a high-dimensional version of the two component model M1 from Section 7.1.1 with , and the riboflavin dataset from Section 7.2 with three components, and . We use the BCD-GEM algorithm with and without active set strategy to fit the FMRLasso on a small grid of eight values for . The corresponding BIC, CPU times (in seconds) and number of EM-iterations are reported in Tables 4 and 4. The values for the BCD-GEM without active set strategy are written in brackets. For model M1 and an appropriate with minimal BIC score, the active set algorithm converges in 5.96 seconds whereas the standard BCD-GEM needs 53.15 seconds. There is also a considerable gain of speed for the real data: 0.89 seconds versus 3.57 seconds for with optimal BIC. Note that in Table 4, the BIC scores sometimes differ substantially for inappropriate values of . For such regularization parameters, the solutions are unstable and different local optima are attained depending on the algorithm used. However, if the regularization parameter is in a reasonable range with low BIC score, the results stabilize.

| 10.0 | 15.6 | 21.1 | 26.7 | 32.2 | 37.8 | 43.3 | 48.9 | |

|---|---|---|---|---|---|---|---|---|

| BIC | 2033 (2022) | 1606 (1748) | 951 (959) | 941 (940) | 989 (983) | 1236 (1073) | 1214 (1216) | 1206 (1203) |

| CPU [s] | 26.78 (269.91) | 17.05 (165.78) | 8.63 (82.78) | 5.96 (53.15) | 5.08 (44.23) | 4.23 (37.27) | 3.35 (18.99) | 3.30 (15.62) |

| EM-iter. | 277.0 (341.5) | 196.0 (205.0) | 96.0 (100.5) | 63.5 (64.5) | 56.0 (53.5) | 41.5 (46.0) | 31.5 (23.0) | 25.0 (19.0) |

| 3.0 | 13.8 | 24.6 | 35.4 | 46.2 | 57.0 | 67.8 | 78.6 | |

|---|---|---|---|---|---|---|---|---|

| BIC | 560 (628) | 536 (530) | 516 (522) | 532 (525) | 541 (540) | 561 (580) | 592 (591) | 611 (613) |

| CPU [s] | 22.40 (29.98) | 1.35 (3.28) | 0.89 (3.57) | 0.86 (3.34) | 0.78 (3.87) | 0.69 (2.42) | 0.37 (2.56) | 0.85 (4.05) |

| EM-iter. | 3389 (2078) | 345 (239) | 287 (266) | 298 (247) | 296 (290) | 248 (184) | 129 (192) | 313 (302) |

8 Discussion

We have presented an -penalized estimator for a finite mixture of high-dimensional Gaussian regressions where the number of covariates may greatly exceed sample size. Such a model and the corresponding Lasso-type estimator are useful to blindly account for often encountered inhomogeneity of high-dimensional data. On a high-dimensional real data example, we demonstrate a 17% gain in prediction accuracy over a (non-mixture) linear model.

The computation and mathematical analysis in such a high-dimensional mixture model is challenging due to the non-convex behavior of the negative log-likelihood. Moreover, with high-dimensional estimation defined via optimization of a non-convex objective function, there is a major gap between the actual computation and the procedure analyzed in theory. We do not provide an answer to this issue in this thesis. Regarding the computation in FMR models, a simple reparameterization is very beneficial and the -penalty term makes the optimization problem numerically much better behaved. We develop an efficient generalized EM algorithm and we prove its numerical convergence to a stationary point. Regarding the statistical properties, besides standard low-dimensional asymptotics, we present a non-asymptotic oracle inequality for the Lasso-type estimator in a high-dimensional setting with general, non-convex but smooth loss functions. The mathematical arguments are different than what is typically used for convex losses.

Appendix A Proofs for Section 4

A.1 Proof of Theorem 1

A.2 Proof of Theorem 2

In order to keep the notation simple, we give the proof for a two class mixture with . All arguments in the proof can also be used for a general mixture with more than two components. Remember that is given by

where

is the log-likelihood function. The weights

are given by , , and

.

Assertion 1.

Let be a root- consistent local minimizer of

(construction as in Fan and Li (2001)).

For all , we easily see from consistency of that It then remains to show that for all , Assume the contrary, i.e., w.l.o.g there is an with such that with non-vanishing probability.

By Taylor’s theorem, applied to the function , there exists a (random) vector on the line segment between and such that

Now, using the regularity assumptions and the central limit theorem, term (1) is of order . Similarly, term (2) is of order by the law of large numbers. Term (3) is of order by the law of large numbers and the regularity condition on the third derivatives (condition (C) of Fan and Li (2001)). Therefore, we have

As is root- consistent we get

| (28) | |||||

From the assumption on the initial estimator, we have

Therefore, the second term in the brackets of (28) dominates the first and the probability of the event

tends to 1. But this contradicts the assumption that is a

local minimizer

(i.e., ).

Assertion 2.

Write

. From part 1), it

follows that with probability tending to one is a root- local minimizer of .

By using a Taylor expansion we find,

Now term (1) is of order (law of large numbers); term (2) is of order (consistency); and term (3), with some abuse of notation an -vector of matrices, is of order (law of large numbers and regularity condition on the third derivatives). Therefore, we have

or

| (29) |

Notice that by the central limit theorem. Furthermore, as . Therefore,

follows from Equation (29).

Appendix B Proofs for Section 5

B.1 Proof of Lemma 1

Using a Taylor expansion,

where

Hence

Now, apply the auxiliary lemma below, with ,

, and

.

Auxiliary Lemma. Let have the following properties:

(i) such that ,

(ii) , , such that , .

Then ,

where

Proof (Auxiliary Lemma)

If , we have for all .

If and , we also have .

If and , we have .

B.2 Proof of Lemma 2

In order to prove Lemma 2, we first state and proof a suitable entropy bound:

We introduce the norm

For a collection of functions on , we let be the entropy of equipped with the metric induced by the norm (for a definition of the entropy of a metric space see van de Geer (2000)).

Define for ,

Entropy Lemma For a constant depending on and , we have for all and ,

Proof (Entropy Lemma) We have

It follows that

Let denote the covering number of a metric space with metric (induced by the norm) , and be its entropy (for a definition of the covering number of a metric space see van de Geer (2000)). If is a ball with radius in Euclidean space , one easily verifies that

Thus Moreover, applying a bound as in Lemma 2.6.11 of van der Vaart and Wellner (1996) gives

We can therefore conclude that

Let’s now turn to the main proof of Lemma 2.

In what follows, are constants depending on , , and . The truncated version of the empirical process is

Let be arbitrary. We invoke Lemma 3.2 in van de Geer (2000), combined with a symmetrization lemma (e.g., a conditional version of Lemma 3.3 in van de Geer (2000)). We apply these lemmas to the class

In the notation used in Lemma 3.2 of van de Geer (2000), we take , and . This then gives

Here, we use the bound (for ),

We then invoke the peeling device: split the set into sets

where , and . There are no more than indices with . Hence, we get

with probability at least

Finally, to remove the truncation, we use

Hence

B.3 Proof of Theorem 3

Case 1 Suppose that

Then we find

Case 2 Suppose that

and that

Then we get

So then

Case 3 Suppose that

and that

Then we have

So then

We can then apply the restricted eigenvalue condition to . This gives

So we arrive at

B.4 Proof of Lemma 3

Let be a standard normal random variable. Then by straightforward computations, for all ,

and

Thus, for independent copies of , and ,

The result follows from this, as

and has a normal mixture distribution.

B.5 Proof of Theorem 5

On , defined in (19) with ( as in Lemma 3; i.e., in (21)), we have the basic inequality

Note that and . Hence, for sufficiently large,

and therefore also

It holds that (since for some sufficiently large), and , and due to the assumption about we obtain on the set that . Finally, the set has large probability, as shown by Lemma 2 and using Proposition 3 and Lemma 3 for FMR models.

Appendix C Proofs for Sections 3 and 6

C.1 Proof of Proposition 2

We restrict ourselves to a two class mixture with k = 2. Consider the function defined as

| (30) | ||||

We will show that is bounded from above for . Then, clearly, is bounded from below for .

The critical point for unboundedness is if we choose for an arbitrary sample point a such that and let . Without the penalty term in (C.1) the function would tend to infinity as . But as for all , cannot be zero, and therefore forces to tend to 0 as .

Let us give a more formal proof for the boundedness of . Choose a small and . As , , there exists a small constant such that

| (31) |

holds for all as long as , and

| (32) |

holds for all as long as .

Furthermore, there exists a small constant such that

| (33) |

hold for all , and

| (34) |

hold for all .

C.2 Proof of Theorem 6

The density of the complete data is given by

whereas the density of the observed data is given by

with

Furthermore, the conditional density of the complete data given the observed data is given by . Then, the penalized negative log-likelihood fulfills the equation

where (compare Section 6.1) and .

By Jensen’s inequality, we get the following important relationship

| (36) |

see also Wu (1983). and are continuous functions in and . If we think of them as functions of with fixed , we write also and . Furthermore, is a convex function of and strictly convex in each coordinate of . As a last preparation, we give a definition of a stationary point for non-differentiable functions (see also Tseng (2001)):

Definition 1.

Let be a function defined on an open set . A point is called stationary if

We are now ready to start with the proof which is inspired by Bertsekas (1995). We write

where denotes the number of coordinates. Remark that the first coordinates are univariate, whereas is a “block coordinate” of dimension .

Proof.

Let be the sequence generated by the BCD-GEM algorithm. We need to prove that for a converging subsequence , is a stationary point of . Taking directional derivatives of Equation (C.2) yields

Note that as is minimized for (Equation (36)). Therefore, it remains to show that for all directions . Let

Using the definition of the algorithm, we have

| (37) |

Additionally, from the properties of GEM (Equation (C.2) and (36)), we have

| (38) |

Equation (38) and the converging subsequence imply that the sequence converges to . Further, we have

| (39) | |||||

We conclude that the sequence converges to zero.

We now show that converges to zero (). Assume the contrary, in particular that does not converge to 0. Let . Without loss of generality (by restricting to a subsequence), we may assume that there exists some such that for all . Let . This differs from zero only along the first component. As belongs to a compact set () we may assume that converges to . Let us fix some . Notice that . Therefore, lies on the segment joining and , and belongs to because is convex. As is convex and minimizes this function over all values that differ from along the first coordinate, we obtain

From Equation (37) and (C.2), we conclude

Using (39) and continuity of in both arguments and , we conclude by taking the limit :

Since this contradicts the strict convexity of as a function of the first block-coordinate. This contradiction establishes that converges to .

From the definition of the algorithm, we have

By continuity and taking the limit , we obtain

Repeating the argument we conclude that is a coordinate-wise minimum. Therefore, following Tseng (2001), is easily seen to be a stationary point of , in particular for all directions . ∎

Acknowledgements N.S. acknowledges financial support from Novartis International AG, Basel, Switzerland.

References

- Bertsekas (1995) Bertsekas, D. (1995) Nonlinear programming. Belmont, MA: Athena Scientific.

- Bickel et al. (2009) Bickel, P., Ritov, Y. and Tsybakov, A. (2009) Simultaneous analysis of Lasso and Dantzig selector. Annals of Statistics, 37, 1705–1732.

- Bunea et al. (2007) Bunea, F., Tsybakov, A. and Wegkamp, M. (2007) Sparsity oracle inequalities for the Lasso. Electronic Journal of Statistics, 1, 169–194.

- Cai et al. (2009a) Cai, T., Wang, L. and Xu, G. (2009a) Stable recovery of sparse signals and an oracle inequality. IEEE Transactions on Information Theory, to appear.

- Cai et al. (2009b) Cai, T., Xu, G. and Zhang, J. (2009b) On recovery of sparse signals via minimization. IEEE Transactions on Information Theory, 55, 3388–3397.

- Candès and Plan (2009) Candès, E. and Plan, Y. (2009) Near-ideal model selection by minimization. Annals of Statistics, 37, 2145–2177.

- Candès and Tao (2005) Candès, E. and Tao, T. (2005) Decoding by linear programming. IEEE Transactions on Information Theory, 51, 4203–4215.

- Candès and Tao (2007) Candès, E. and Tao, T. (2007) The Dantzig selector: statistical estimation when p is much larger than n (with discussion). Annals of Statistics, 35, 2313–2404.

- Dempster et al. (1977) Dempster, A., Laird, N. and Rubin, D. (1977) Maximum likelihood from incomplete data via the EM algorithm. Journal of the Royal Statistical Society, Series B, 39, 1–38.

- Fan and Li (2001) Fan, J. and Li, R. (2001) Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of the American Statistical Association, 96, 1348–1360.

- Friedman et al. (2007) Friedman, J., Hastie, T., Hoefling, H. and Tibshirani, R. (2007) Pathwise coordinate optimization. Annals of Applied Statistics, 1, 302–332.

- Friedman et al. (2010) Friedman, J., Hastie, T. and Tibshirani, R. (2010) Regularized paths for generalized linear models via coordinate descent. Journal of Statistical Software, 33, 1–22.

- Fu (1998) Fu, W. J. (1998) Penalized regression: the Bridge versus the Lasso. Journal of Computational and Graphical Statistics, 7, 397–416.

- Greenshtein and Ritov (2004) Greenshtein, E. and Ritov, Y. (2004) Persistence in high-dimensional predictor selection and the virtue of over-parametrization. Bernoulli, 10, 971–988.

- Grün and Leisch (2007) Grün, B. and Leisch, F. (2007) Fitting finite mixtures of generalized linear regressions in R. Computational Statistics & Data Analysis, 51, 5247–5252.

- Grün and Leisch (2008) Grün, B. and Leisch, F. (2008) FlexMix version 2: Finite mixtures with concomitant variables and varying and constant parameters. Journal of Statistical Software, 28, 1–35.

- Huang et al. (2008) Huang, J., Ma, S. and Zhang, C.-H. (2008) Adaptive Lasso for sparse high-dimensional regression models. Statista Sinica, 18, 1603–1618.

- Khalili and Chen (2007) Khalili, A. and Chen, J. (2007) Variable selection in finite mixture of regression models. Journal of the American Statistical Association, 102, 1025–1038.

- Koltchinskii (2009) Koltchinskii, V. (2009) The Dantzig selector and sparsity oracle inequalities. Bernoulli, 15, 799–828.

- Lehmann (1983) Lehmann, E. (1983) Theory of Point Estimation. Pacific Grove, CA: Wadsworth and Brooks/Cole.

- Leisch (2004) Leisch, F. (2004) FlexMix: A general framework for finite mixture models and latent class regression in R. Journal of Statistical Software, 11, 1–18.

- McLachlan and Peel (2000) McLachlan, G. J. and Peel, D. (2000) Finite mixture models. Wiley, New York.

- Meier et al. (2008) Meier, L., van de Geer, S. and Bühlmann, P. (2008) The group Lasso for logistic regression. Journal of the Royal Statistical Society, Series B, 70, 53–71.

- Meinshausen and Bühlmann (2006) Meinshausen, N. and Bühlmann, P. (2006) High dimensional graphs and variable selection with the Lasso. Annals of Statistics, 34, 1436–1462.

- Meinshausen and Yu (2009) Meinshausen, N. and Yu, B. (2009) Lasso-type recovery of sparse representations for high-dimensional data. Annals of Statistics, 37, 246–270.

- Pan and Shen (2007) Pan, W. and Shen, X. (2007) Penalized model-based clustering with application to variable selection. Journal of Machine Learning Research, 8, 1145–1164.

- Park and Casella (2008) Park, T. and Casella, G. (2008) The Bayesian Lasso. Journal of the American Statistical Association, 103, 681–686.

- Tibshirani (1996) Tibshirani, R. (1996) Regression shrinkage and selection via the Lasso. Journal of the Royal Statistical Society, Series B, 58, 267–288.

- Tseng (2001) Tseng, P. (2001) Convergence of a block coordinate descent method for nondifferentiable minimization. Journal of Optimization Theory and Applications, 109, 475–494.

- Tseng and Yun (2008) Tseng, P. and Yun, S. (2008) A coordinate gradient descent method for nonsmooth separable minimization. Mathematical Programming, Series B, 117, 387–423.

- Tsybakov (2004) Tsybakov, A. (2004) Optimal aggregation of classifiers in statistical learning. Annals of Statistics, 32, 135–166.

- van de Geer (2000) van de Geer, S. (2000) Empirical Processes in M-Estimation. Cambridge University Press.

- van de Geer (2008) van de Geer, S. (2008) High-dimensional generalized linear models and the Lasso. Annals of Statistics, 36, 614–645.

- van de Geer and Bühlmann (2009) van de Geer, S. and Bühlmann, P. (2009) On the conditions used to prove oracle results for the Lasso. Electronic Journal of Statistics, 3, 1360–1392.

- van de Geer et al. (2010) van de Geer, S., Zhou, S. and Bühlmann, P. (2010) Prediction and variable selection with the Adaptive Lasso. arXiv:1001.5176v2.

- van der Vaart (2007) van der Vaart, A. (2007) Asymptotic Statistics. Cambridge University Press.

- van der Vaart and Wellner (1996) van der Vaart, A. and Wellner, J. (1996) Weak Convergence and Empirical Processes. Springer-Verlag.

- Wainwright (2009) Wainwright, M. (2009) Sharp thresholds for high-dimensional and noisy sparsity recovery using -constrained quadratic programming (Lasso). IEEE Transactions on Information Theory, 55, 2183–2202.

- Wu (1983) Wu, C. (1983) On the convergence properties of the EM algorithm. Annals of Statistics, 11, 95–103.

- Zhang (2010) Zhang, C.-H. (2010) Nearly unbiased variable selection under minimax concave penalty. Annals of Statistics, 38, 894–942.

- Zhang and Huang (2008) Zhang, C.-H. and Huang, J. (2008) The sparsity and bias of the Lasso selection in high-dimensional linear regression. Annals of Statistics, 36, 1567–1594.

- Zhang (2009) Zhang, T. (2009) Some sharp performance bounds for least squares regression with L1 regularization. Annals of Statistics, 37, 2109–2144.

- Zhao and Yu (2006) Zhao, P. and Yu, B. (2006) On model selection consistency of Lasso. Journal of Machine Learning Research, 7, 2541–2563.

- Zou (2006) Zou, H. (2006) The adaptive Lasso and its oracle properties. Journal of the American Statistical Association, 101, 1418–1429.