Factor models and variable selection in high-dimensional regression

analysis

Alois Kneiplabel=e1]akneip@uni-bonn.de

[Pascal Sardalabel=e2]Pascal.Sarda@math.ups-tlse.fr

[

Universität Bonn and Université Paul Sabatier

Statistische Abteilung

Department of Economics

and Hausdorff

Center for Mathematics

Universität Bonn

Adenauerallee 24-26

53113 Bonn

Germany

Institut de Mathématiques

Laboratoire de Statistique

et Probabilités

Université Paul Sabatier

UMR 5219

118, Route de Narbonne

31062 Toulouse Cedex

France

(2011; 3 2011)

Abstract

The paper considers linear regression problems where the number of

predictor variables is possibly larger than the sample size. The

basic motivation of the study is to combine the points of view of model

selection and functional regression by using a factor approach: it is

assumed that the predictor vector can be decomposed into a sum of two

uncorrelated random components reflecting common factors and specific

variabilities of the explanatory variables. It is shown that the

traditional assumption of a sparse vector of parameters is restrictive

in this context. Common factors may possess a significant influence on

the response variable which cannot be captured by the specific effects

of a small number of individual variables. We therefore propose to

include principal components as additional explanatory variables in an

augmented regression model. We give finite sample inequalities for

estimates of these components. It is then shown that model selection

procedures can be used to estimate the parameters of the augmented

model, and we derive theoretical properties of the estimators. Finite

sample performance is illustrated by a simulation study.

62J05,

62H25,

62F12,

Linear regression,

model selection,

functional regression,

factor models,

doi:

10.1214/11-AOS905

keywords:

[class=AMS]

.

keywords:

.

††volume: 39††issue: 5

and

1 Introduction

The starting point of our analysis is a high-dimensional linear

regression model

of the form

(1)

where , , are i.i.d. random pairs

with and . We will assume without loss of generality that

for all .

Furthermore, is a vector of parameters in

and are centered i.i.d.

real random variables independent with with

. The dimension of the

vector of parameters is assumed to be typically larger than the sample

size .

Roughly speaking, model (1) comprises two main

situations which have been considered independently in two separate

branches of statistical literature. On one side, there is the situation

where represents a (high-dimensional) vector of

different predictor variables. Another situation arises when the

regressors are discretizations (e.g., at different observations

times) of a same curve. In this case

model (1) represents a discrete version of an

underlying continuous functional linear model. In the two

setups, very different strategies for estimating

have been adopted, and underlying structural

assumptions seem to

be largely incompatible. In this paper we will study similarities and

differences of

these methodologies, and we will show that

a combination of ideas developed in the two settings leads to new

estimation procedures

which may be useful in a number of important applications.

The first situation is studied in a large literature on model selection

in high-dimensional

regression. The basic structural assumptions can be described as follows:

•

There is only a relatively small number of predictor variables

with which have a significant

influence on the outcome . In other words,

the set of nonzero coefficients is sparse, .

•

The correlations between different explanatory variables

and , , are “sufficiently” weak.

The most popular procedures to identify and estimate nonzero

coefficients are Lasso and the Dantzig selector. Some

important references are Tibshirani (1996), Meinshausen and Bühlmann (2006),

Zhao and Yu (2006), van de Geer (2008), Bickel, Ritov and Tsybakov (2009),

Candes and Tao (2007) and Koltchinskii (2009). Much work in this domain is

based on the assumption that the columns ,

, of the design matrix are almost orthogonal. For example,

Candes and Tao (2007) require that “every set of columns with

cardinality less than approximately behaves like an orthonormal

system.” More general conditions have been introduced by

Bickel, Ritov and Tsybakov (2009) or Zhou, van de Geer and

Bülhmann (2009). The theoretical

framework developed in

these papers also allows one to study model selection for regressors

with substantial amount of correlation, and it provides a basis for the

approach presented in our paper.

In sharp contrast, the setup considered in the literature on functional

regression rests upon

a very different type of structural assumptions. We will consider the

simplest case

that for random functions

observed at an equidistant

grid . Structural assumptions on coefficients and

correlations between

variables can then be subsumed as follows:

•

, where

is a continuous slope function,

and as , .

•

There are very high correlations between

explanatory variables and , . As , for any fixed .

Some important applications as well as theoretical results on

functional linear regression are, for example, presented in

Ramsay and Dalzell (1991), Cardot, Ferraty and Sarda (1999), Cuevas, Febrero and Fraiman (2002),

Yao, Müller and Wang (2005), Cai and Hall (2006), Hall and Horowitz (2007),

Cardot, Mas and Sarda (2007) and Crambes, Kneip and Sarda (2009). Obviously, in this

setup no variable

corresponding to a specific observation at grid point

will possess a particulary high influence on , and there will

exist a large number of small, but nonzero coefficients of

size proportional to . One may argue that dimensionality reduction

and therefore some underlying concept of “sparseness” is always

necessary when dealing with high-dimensional problems. However, in

functional regression sparseness is usually not assumed with respect to

the coefficients , but the model is rewritten using a

“sparse” expansion of the predictor functions .

The basic idea relies on the so-called Karhunen–Loève decomposition

which provides a decomposition of

random functions in terms of functional principal components of the

covariance operator of .

In the discretized case analyzed in this paper this amounts to consider

an approximation of by

the principal components

of the covariance matrix . In practice, often a small number of

principal components will suffice

to achieve a small -error. An important points is now that even if

the eigenvectors corresponding to the leading eigenvalues of

can be well estimated by the

eigenvectors (estimated principal

components) of the empirical covariance

matrix .

This is due to the fact that if the predictors

represent discretized values of a continuous functional

variable, then for sufficiently

small the eigenvalues will necessarily be of an

order larger

than and will thus exceed the magnitude of purely

random components.

From a more general point of view the underlying theory will be

explained in detail in Section 4.

Based on this insight, the most frequently used approach in functional

regression is to approximate in

terms of the first estimated principal

components ,

and to rely on the approximate model . Here,

serves as smoothing parameter. The new coefficients

are estimated by least squares, and . Resulting rates of convergence

are given in Hall and Horowitz (2007).

The above arguments show that a suitable regression analysis will

have to take into account the underlying structure of the explanatory

variables .

The basic motivation of this paper now is to combine the points of view of

the above branches of literature

in order to develop a new approach for model

adjustment and variable selection

in the practically

important situation of strongly correlated regressors. More precisely,

we will concentrate

on factor models by assuming

that the can be decomposed in the form

(2)

where and are two uncorrelated random

vectors in . The random vector is intended

to describe high correlations of the while the components

, , of are uncorrelated. This implies

that the covariance matrix of

adopts the decomposition

(3)

where , while

is a diagonal matrix with diagonal entries

, .

Note that factor models can be found in any textbook on multivariate

analysis and must be

seen as one of the major tools

in order to analyze samples of high-dimensional vectors.

Also recall that a standard factor model is additionally based on the

assumption that

a finite

number of factors suffices to approximate precisely. This

means that the matrix only possesses nonzero

eigenvalues.

In the following we will more generally assume that a small number of

eigenvectors of

suffices to approximate with high accuracy.

We want to emphasize that the typical structural assumptions to be

found in the literature

on high-dimensional regression are special cases of

(2). If and thus , we are in the

situation of uncorrelated regressors which has been widely studied in

the context of model

selection. On the other hand, and thus

reflect the structural assumption of functional regression.

In this paper we assume that as well as represent

nonnegligible parts of the

variance of . We believe that this approach may well describe

the situation encountered in many relevant applications. Although

standard factor models are usually considered in the case

, (2) for large values of may be of

particular interest in time

series or spatial analysis. Indeed, factor models for large with a

finite number

of nonzero eigenvalues of play an important role

in the

econometric study of multiple time series and panel data. Some

references are Forni and Lippi (1997), Forni et al. (2000), Stock and Watson (2002), Bernanke and Boivin (2003) and

Bai (2003, 2009).

Our objective now is to study linear regression (1)

with respect to

explanatory variables which adopt decomposition (2). Each

single variable ,

, then possesses a specific variability induced by

and may

thus explain some part of the outcome . One will, of course,

assume that only few

variables have a significant influence on which enforces the use

of model selection

procedures.

On the other hand, the term represents a common

variability. Corresponding principal components quantify

a simultaneous variation of many individual regressors. As a

consequence, such principal

components may possess some additional power for predicting

which may

go beyond the effects of individual variables. A rigorous discussion

will be given in Section 3. We want to note that the concept of

“latent variables,” embracing the common influence of a large group

of individual

variables, plays a prominent role in applied, parametric multivariate analysis.

These arguments motivate the main results of this paper. We propose to

use an “augmented”

regression model which includes principal components as additional

explanatory variables.

Established model selection procedures like the Dantzig selector or the

Lasso can then be

applied to estimate the nonzero coefficients of the augmented model. We

then derive theoretical

results providing bounds for the accuracy of the resulting estimators.

The paper is organized as follows: in Section 2 we formalize

our setup.

We show in Section 3 that the traditional sparseness

assumption is restrictive

and that a valid model may have to include principal components. The

augmented model is thus introduced with an estimation procedure.

Section 4 deals with

the problem how accurately true principal components can be estimated

from the sample

. Finite sample inequalities are

given, and we show

that it is possible to obtain sensible estimates of those components

which explain a considerable percentage of the

total variance of all , . Section 5

focuses on

theoretical properties of the augmented model, while in Section 6 we present

simulation results illustrating the

finite sample performance of our estimators.

2 The setup

We study regression of a response

variable on a set of i.i.d. predictors ,

, which adopt

decomposition (2) with , , , for

all , .

Throughout the following sections we additionally assume that there

exist constants

and such that with

the following assumption (A.1) is satisfied

for all :

{longlist}[(A.1)]

for all .

Recall that is the covariance matrix of with , where and is a diagonal matrix with diagonal entries , . We denote as the empirical covariance matrix

based on the sample , .

Eigenvalues and eigenvectors of the standardized matrices and will

play a central

role. We will use and to denote the eigenvalues of

and , respectively, while and denote corresponding

orthonormal eigenvectors.

Note that all eigenvectors of and

(or

and

) are identical, while

eigenvalues differ by the factor . Standardization is important

to establish convergence results

for large , since the largest eigenvalues of tend to

infinity as .

From a conceptional point of view we will concentrate on the case that

is large

compared to . Another crucial, qualitative assumption

characterizing our approach is the dimensionality reduction of using a small number of

eigenvectors (principal components) of

such that (in a good approximation)

.

We also assume that .

Then all leading principal components of

corresponding to the largest eigenvalues explain a considerable percentage

of the total variance of and .

Indeed, if , we

necessarily have

and .

Then , and the first principal component of

explains a considerable proportion

of the total variance of .

We want to emphasize that this situation is very different from the

setup which is usually considered in the literature on the analysis of

high-dimensional covariance matrices; see, for example, Bickel and Levina (2008). It is then assumed that the variables of interest are only

weakly correlated and that the largest eigenvalue

of the corresponding scaled covariance matrix

is of order . This means that

for large the first principal component only explains

a negligible percentage of the total variance of ,

.

It is well known that in this case no consistent estimates of

eigenvalues and principal components can be obtained from an

eigen-decomposition of

.

However, we will show in Section 4

that principal components which are able to explain a considerable

proportion of total variance can be estimated consistently. These

components will be an intrinsic part of the augmented model presented

in Section 3.

We will need a further assumption which ensures that all covariances

between the different variables are well approximated by their

empirical counterparts:

{longlist}[(A.2)]

There exists a such that

(4)

(5)

(6)

(7)

hold simultaneously with probability , where

as , .

The following proposition provides a general sufficient condition on

random vectors for which (A.2) is satisfied provided that the rate of

convergence of to 0 is sufficiently fast.

Proposition 1

Consider independent and identically distributed random vectors , , such that for ,

and

(8)

for positive constants and with moreover . Then, for any positive constant such that

and

(9)

Note that as the right-hand side of (1) converges

to 1 provided that is chosen sufficiently large and that

for some . Therefore, assumption

(A.2) is satisfied if the components of the random variables

possess some exponential moments. For the specific case of

centered normally distributed random variables, a more precise bound in

(1) may be obtained using Lemma 2.5 in Zhou, van de Geer and

Bülhmann (2009)

and large deviations inequalities obtained by Zhou, Lafferty and Wassermn (2008). In

this case it may also be shown

that for sufficiently large events (4)–(7) hold

with probability tending to 1 as without any

restriction on the quotient .

Of course, the rate in (4)–(7) depends on the tails of the distributions: it would be possible

to replace this rate with a slower one in case of heavier tails than in

Proposition 1. Our theoretical results could be modified

accordingly.

3 The augmented model

Let us now consider the structural model (2) more

closely. It implies that

the vector of predictors can be decomposed into

two uncorrelated random vectors and .

Each of these

two components separately may possess a significant influence on the

response variable . Indeed, if and

were known, a possibly substantial improvement of model (1) would consist

in a regression of on the variables and

(10)

with different sets of parameters and , , for each contributor. We here again assume that ,

, are

centered i.i.d. random variables with which

are independent of

and .

By definition, and possess substantially different

interpretations. describes the part of which is

uncorrelated with all other variables. A nonzero coefficient

then means that the variation of has a specific

effect on

. We will of course assume that such nonzero coefficients are

sparse,

for some . The

true variables are unknown, but with

model (10) can obviously be rewritten in the form

(11)

The variables are heavily correlated. It therefore does not

make any sense to assume that for some any

particular variable possesses a specific influence on the

predictor variable. However, the term

may represent an important,

common effect of all predictor variables. The vectors

can obviously

be rewritten in terms of principal components.

Let us recall that denote the

eigenvalues of the standardized covariance matrix of ,

and corresponding orthonormal eigenvectors. We have

where . As outlined in

the previous

sections we now

assume that the use of principal components allows for a considerable

reduction of

dimensionality, and that a small number of leading principal components

will suffice

to describe the effects of the variable . This may be

seen as an analogue of the sparseness assumption made for the .

More precisely, subsequent analysis will be based on the assumption

that the

following augmented model holds for some suitable :

(12)

where and

. The use of instead

of is motivated by the fact that

,

. Therefore the are standardized variables

with . Fitting an augmented model requires

us to select an appropriate as well as to determine sensible

estimates of . Furthermore, model selection

procedures like Lasso or Dantzig have to be applied in order to

retrieve the nonzero coefficients , , and , . These issues will be addressed in subsequent

sections.

Obviously, the augmented model may be considered as a synthesis of the

standard type

of models proposed in the literature on functional regression and model

selection. It generalizes the classical multivariate linear

regression model (1). If a -factor model holds

exactly, that is,

, then the only substantial restriction

of (10)–(12) consists in the assumption

that depends linearly on

and .

We want to emphasize, however, that our analysis does not require the

validity of

a -factor model. It is only assumed that there exists “some”

and

satisfying our assumptions which lead

to (12) for a sparse set of coefficients .

3.1 Identifiability

Let and .

Since , , are eigenvectors of

we have for

all , . By assumption the random vectors

and are uncorrelated, and hence

for all

. Furthermore, for all

. If the augmented model (12) holds, some

straightforward computations then show that under (A.1) for any alternative

set of coefficients , ,

(13)

We can conclude that the coefficients , and

, , in (12)

are uniquely determined.

Of course, an inherent difficulty of (12) consists

of the fact that it contains the unobserved, “latent” variables

.

To study this problem,

first recall that our setup imposes the decomposition (3) of the

covariance matrix of . If a factor

model with factors

holds exactly, then the possesses rank . It

then follows from

well-established results in multivariate analysis that if

the matrices and are uniquely

identified.

If , then also are

uniquely determined (up to sign) from the structure of .

However, for large , identification is possible under even more

general conditions.

It is not necessary that a -factor model holds exactly. We only

need an additional assumption on the magnitude

of the eigenvalues of defining the

principal components of to be considered.

{longlist}

[(A.3)]

The eigenvalues of are

such that

for some with .

In the following we will qualitatively assume that as well as

. More specific assumptions will be made in the sequel.

Note that

eigenvectors are only unique up to sign

changes. In the following we will always assume that the right

“versions” are used. This will go without saying.

Theorem 1

Let

and . Under assumptions

(A.1) and (A.2) we have for all

, and all satisfying

(A.3):

(14)

(17)

For small , standard factor analysis uses special algorithms in

order to identify . The theorem tells us that for large

this is unnecessary since then the eigenvectors

of provide a good approximation. The

predictor of possesses an error of order

. The error decreases as increases, and

thus yields a good approximation of if is

large. Indeed, if [for fixed , ,

and ] then by (1) we have

. Furthermore, by

(17) the error in predicting by converges to

zero as .

A crucial prerequisite for a reasonable analysis of the model is

sparseness of

the coefficients . Note that if is large compared to ,

then by

(17)

the error in replacing by is negligible

compared to the estimation error induced by the

existence of the error terms . If and

, then the true coefficients and

provide a sparse solution of the regression problem.

Established

theoretical results [see Bickel, Ritov and Tsybakov (2009)] show that under some

regularity conditions (validity of the “restricted eigenvalue

conditions”) model selection procedures allow to identify such

sparse solutions even if there are multiple vectors of coefficients

satisfying the normal equations. The latter is of course always the

case if . Indeed, we will show in the following sections that

factors can be consistently estimated from the data, and that

a suitable application of Lasso or the Dantzig-selector leads to consistent

estimators , satisfying

, , as .

When replacing by , there are alternative sets

of coefficients leading to the same prediction error as in

(17). This is due to the fact that . However, all

these alternative solutions are nonsparse and cannot be

identified by Lasso or other procedures. In particular, it is easily

seen that

(19)

By (1) all values are of order

. Since

, this implies that many are

nonzero. Therefore, if for some , then

contains a large number of small,

nonzero coefficients

and is not at all sparse. If is large compared to no known

estimation procedure will be able to provide consistent estimates of

these coefficients.

Summarizing the above discussion we can conclude:

{longlist}

[(2)]

If the variables are heavily correlated and follow an

approximate

factor model, then one may reasonably expect substantial effects of the

common, joint variation of all variables and, consequently, nonzero coefficients

and in (10) and (12).

But then a “bet on sparsity” is unjustifiable when dealing with the standard

regression model (1). It follows from

(19) that for large model (1)

holds approximately for a nonsparse set of coefficients , since many

small, nonzero coefficients are necessary in order to capture the

effects of

the common joint variation.

The augmented model offers a remedy to this problem by

pooling possible

effects of the joint variation using a small number of additional variables.

Together with the familiar assumption of a small number of variables possessing

a specific influence, this leads to a sparse model with at most nonzero

coefficients which can be recovered from model selection procedures

like Lasso or

the Dantzig-selector.

In practice, even if

(12) only holds approximately, since a too-small value

of has been selected, it may be able to quantify at least some

important part of the

effects discussed above. Compared to an analysis based on a standard

model (1),

this may lead to a substantial improvement of model fit as well as to more

reliable interpretations of significant variables.

3.2 Estimation

For a pre-specified we now define a procedure for estimating

the components of the corresponding augmented model (12)

from given data.

This obviously specifies suitable procedures

for approximating the unknown values as well as to apply

subsequent model selection procedures in order to retrieve nonzero coefficients

and , , . A discussion

of the

choice of can be found in the next section.

Recall from Theorem 1 that for large the eigenvectors

of

are well approximated by the

eigenvectors of the standardized covariance matrix . This motivates us to use the

empirical principal components of in order

to determine estimates of and .

Theoretical support

will be given in the next section.

Define as the

eigenvalues of the standardized empirical covariance matrix , while are associated orthonormal eigenvectors.

We then estimate by

When replacing by in

(12), a direct application of model selection

procedures does not seem to be adequate, since and

the predictor variables are heavily correlated. We therefore

rely on a projected model. Consider the projection matrix on the

orthogonal space of the space spanned by the eigenvectors

corresponding to the largest eigenvalues of

where ,

and .

It will be shown in the next section that for large and the additional

error term can be assumed to be reasonably small.

In the following we will use to denote the

vectors with entries .

Furthermore, consider the -dimensional vector of

predictors

,

. The Gram matrix in

model (20) is a block matrix defined as

where is the identity matrix of size . Note that the

normalization of the predictors in (20) implies that

the diagonal elements of the Gram matrix above are equal to 1.

Arguing now that the vector of parameters in model (20) is

-sparse, we may use a selection procedure to recover/estimate

the nonnull parameters. In the following we will concentrate on the

Lasso estimator introduced in Tibshirani (1996). For a pre-specified

parameter , an estimator is then obtained as

(21)

being the -dimensional matrix with

rows . We can alternatively use the Dantzig

selector introduced in Candes and Tao (2007).

Finally, from , we define corresponding

estimators for , , and ,

,

in the unprojected model (12).

The following theorem shows that principal components which are able

to explain a considerable proportion of total variance can be estimated

consistently.

For simplicity, we will concentrate on the case

that as well as are large enough such that

{longlist}[(A.4)]

and

.

Theorem 2

Under assumptions (A.1)–(A.4) and under events

(4)–(7) we have for all and all

,

(22)

(23)

(24)

Theorem 2 shows that for sufficiently large () the eigenvalues and eigenvectors of

provide reasonable estimates of and

for .

Quite obviously it is not possible to determine sensible estimates of

all

principal components of . Following

the proposition it is required that as well as be

of order at least

. Any smaller component cannot be

distinguished from

pure “noise” components. Up to the -term this corresponds to

the results

of Hall and Hosseini-Nasab (2006) who study the problem of the

number of principal components that can be consistently estimated in a

functional

principal component analysis.

The above insights are helpful for selecting an appropriate in a

real data

application. In tendency, a suitable factor model will incorporate

components which explain a large percentage of the total variance of

, while is very small.

If for a sample of high-dimensional vectors a principal

component analysis leads to the conclusion that the first (or second,

third) principal components explains a large

percentage of

the total (empirical) variance of the observations, then such a

component cannot be generated by “noise” but reflects an underlying

structure. In particular, such a component

may play a crucial role in modeling a response variable according to

an augmented regression model of the form

(12).

Bai and Ng (2002) develop criteria of selecting the dimension in a

high-dimensional factor model. They rely on an adaptation of the well-known

AIC and BIC procedures in model selection. One possible approach is as

follows: Select a maximal possible dimension and estimate

by .

Then determine an estimate by minimizing

(26)

over . Bai and Ng (2002) show that

under some regularity conditions this criterium (as well as a number of

alternative versions) provides asymptotically consistent estimates

of the true factor dimension as . In our

context these

regularity conditions are satisfied if (A.1)–(A.4) hold for all

and ,

and if there exists some

such

that ,

for all .

Now recall the modified version (20) of the

augmented model used

in our estimation procedure. The following theorem establishes bounds for

the projections as well as

for the

additional error terms .

Let denote the

population version of .

Theorem 3

Assume (A.1) and (A.2). There then exist constants

, , , such that for all satisfying

(A.3) and (A.4), all , ,

(27)

(28)

hold with probability , while

holds with probability at least . Here,

.

Note that if satisfies a -dimensional factor model,

that is, if the rank of

is equal to , then . The theorem then states that for large and

the projected variables ,

,

“in average” behave similarly to the specific variables .

Variances will be close

to .

5 Theoretical properties of the augmented model

We come back to model (12). As shown in Section 3.2,

the Lasso or the Dantzig selector may be used to determine estimators

of the parameters of the model. Identification of sparse solutions as

well as

consistency of estimators require structural assumptions on the

explanatory variables. The weakest assumption on the correlations

between different variables seems to be the so-called restricted eigenvalue condition introduced by Bickel, Ritov and Tsybakov (2009);

see also Zhou, van de Geer and

Bülhmann (2009).

We first provide

a theoretical result which shows that for large the design

matrix of the

projected model

(20) satisfies the restricted eigenvalue conditions

given in Bickel, Ritov and Tsybakov (2009) with high probability. We will

additionally assume that are large enough such that

{longlist}[(A.5)]

Let denote an arbitrary subset of indices, with . For a vector , let be the vector in

which has the same coordinates as on and zero

coordinates on the complement of . We define in the same

way . Now for and for an integer

, , denote by the subset of corresponding to largest in absolute value coordinates of outside of , and define . Furthermore,

let .

Proposition 2

Assume (A.1) and (A.2). There then exists

a constant , such that for all

, , satisfying (A.3)–(A.5),

and

(30)

holds with probability .

Asymptotically, if and are large, then , , provided that

, and are sufficiently small compared to . In this

case the proposition implies

that with high probability the restricted eigenvalue condition

of Bickel, Ritov and Tsybakov (2009) [i.e., ] is satisfied. The same holds for the conditions

which

require , where

The following theorem now provides bounds for the estimation

error and the prediction loss for the Lasso estimator of the

coefficients of the augmented model. It generalizes the results of

Theorem 7.2 of Bickel, Ritov and Tsybakov (2009) obtained under the standard

linear regression model. In our analysis merely the values of

for are of interest. However, only slight

adaptations of the proofs are necessary in order to derive

generalizations of the bounds provided by Bickel, Ritov and Tsybakov (2009) for

the Dantzig selector () and for the loss, . In

the latter case, has to be replaced by

. In the following, let and be defined

as in Theorem 3.

Theorem 4

Assume (A.1), (A.2) and

suppose that the error terms

in model (12)

are independent random variables with . Now consider the Lasso estimator

defined by (21) with

where

, is a positive constant and .

If is sufficiently large, then for all

, , satisfying (A.3)–(A.5) as well

as , the following inequalities hold with

probability at least :

(32)

where . Moreover,

(33)

holds with probability at least .

Of course, the main message of the theorem is asymptotic in nature. If

tend to infinity

for fixed values of and , then the estimation error and

the prediction error converge at rates

and , respectively.

For values of and tending to infinity as the sample size tends

to infinity, the rates are more complicated. In particular, they depend

on how fast converges to

zero as .

Similar results hold for the estimators based on the Dantzig selector.

Remark 1.

Note that Proposition 2 as well as the results of

Theorem 4 heavily depend on the validity of assumption (A.1)

and the corresponding value , where

. It is immediately

seen that the smaller the the smaller the value of

in (2). This means that all

variables , have to possess a

sufficiently large specific variation which is not shared by other

variables. For large this may be seen as a restrictive assumption.

In such a situation one may consider a restricted version of model

(12), where variables with extremely small values

of are eliminated. But for large we can infer from

Theorem 3 that a small value of

indicates that also is small. Hence, an extension of our

method consists of introducing some threshold

and discarding all those variables ,

, with . A precise analysis is not

in the scope of the present paper.

Remark 2.

If

the augmented model reduces to the

standard linear regression model (1) with a

sparse set

of coefficients, for some .

An application of our estimation procedure is then unnecessary, and coefficients

may be estimated by traditional model selection procedures. Bounds on

estimation errors can therefore be directly obtained from the results

of Bickel, Ritov and Tsybakov (2009), provided that the restricted eigenvalue

conditions are satisfied.

But

in this situation

a slight adaptation of the proof of Proposition 2

allows us to establish

a result similar to (2) for the standardized variables

.

Define as the -matrix with generic elements

. When assuming (A.1), (A.2) as well as , then for the following inequality holds with

probability :

where . Recall, however, from the discussion in Section 3.1

that is a restrictive condition in the

context of highly correlated regressors.

6 Simulation study

In this section we study the finite sample performance of the

estimators discussed in the proceeding sections. We consider a factor

model with factors. The first

factor is

, , while the second factor is

given by

, , and ,

. For different values of and

observations with

, ,

are generated according to the

model

(35)

(36)

where , , , and

are independent variables. Our study

is based

on nonzero -coefficients whose values

are , , and , while

the error variance is set to .

The parameters of the augmented model with are estimated by

using the Lasso-based estimation procedure described in Section 3.2.

The behavior of the estimates is compared to the Lasso estimates of the

coefficients of a standard regression model (1).

All results reported in this section are obtained by applying the

LARS-package by Hastie and Efron implemented in R. All tables

are based on 1,000 repetitions of the simulation experiments.

The corresponding R-code can be obtained from the authors upon request.

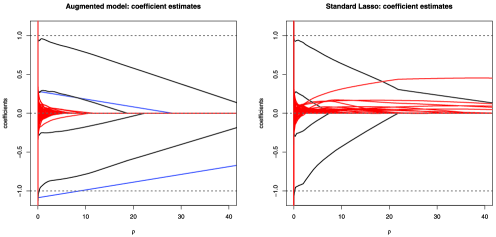

Figure 1 and Table 1 refer to the situation with ,

, and . We then

have , , while the first and second factor

explain 40% and 20% of

the total variance of , respectively.

Figure 1: Paths of Lasso estimates for the augmented model (left panel) and

the standard linear model (right panel) in dependence of ;

black—estimates

of nonzero ; red—estimates of coefficients with ;

blue—.

Table 1: Estimation errors for different sample sizes ()

Sample sizes

Parameter

estimates

Prediction

Opt.

Sample

Exact

Opt.

Lasso applied to augmented model:

00,50

00,50

0.3334

0.8389

0.0498

0.1004

100

0,100

0.2500

0.5774

0.0328

0.0480

250

0,250

0.1602

0.3752

0.0167

0.0199

500

0,500

0.1150

0.2752

0.0096

0.0106

5,000

0,100

0.0378

0.0733

0.0152

0.0154

100

2,000

0.2741

0.8664

0.0420

0.0651

Sample

Exact

Opt.

Lasso applied to standard linear regression

model:

00,50

00,50

2.2597

1.8403

0.0521

0.1370

100

0,100

2.2898

1.9090

0.0415

0.0725

250

0,250

2.3653

1.7661

0.0257

0.0345

500

0,500

2.4716

1.7104

0.0174

0.0207

5,000

0,100

0.5376

1.5492

0.0161

0.0168

100

2,000

3.7571

2.2954

0.0523

0.1038

Figure 1 shows estimation results of one typical simulation with

.

The left panel contains the parameter estimates for the augmented

model. The paths

of estimated

coefficients for the 4 significant variables (black

lines), the 96 variables with (red lines), as well as of

the untransformed estimates

(blue lines) of , ,

are plotted as a function of . The four significant coefficients

as well as

and can immediately been identified in the

figure. The

right panel shows a corresponding plot of estimated coefficients when

Lasso is directly applied to the standard regression model (1). As has to be

expected by (19) the necessity of compensating the

effects of

by a large number of small, nonzero coefficients

generates a

general “noise level” which makes it difficult to identify the four

significant

variables in (36). The penalties in the figure as

well as

in subsequent tables have to be interpreted in terms of the scaling used

by the LARS-algorithm and have to be multiplied with in order to

correspond to the standardization used in the proceeding sections.

The upper part of Table 1 provides simulation results with

respect to the augmented model for different sample sizes and .

In order to access the quality of parameter estimates we evaluate

as well as at the optimal value of , where the

minimum of is obtained. Moreover, we record the value

of where the minimal sample prediction error

(37)

ia attained. For the same value we also determine the exact

prediction error

(38)

for a new observation independent of . The columns

of Table 1 report the average values of the corresponding quantities

over the 1,000

replications. To get some insight into a practical choice of the

penalty, the last

column additionally yields the average value of the parameters minimizing

the -statistics. is computed by using the R-routine

“summary.lars” and plugging in the true error variance . We see that in all situations

the average value of minimizing is very close to the

average

providing the smallest prediction error. The penalties for optimal

parameter estimation are, of course, larger.

It is immediately seen that the quality of estimates considerably

increases when going from to . An interesting result

consists of the fact that the prediction error is smaller for

than for , . This may be interpreted as a consequence of

(17).

The lower part of Table 1 provides corresponding simulation results

with respect to Lasso estimates

based on the standard regression model. In addition to the minimal

error in estimating the parameters of

(36)

we present the minimal -distance , where

is the (nonsparse) set

of parameters minimizing the population prediction error. Sample and

exact prediction errors are obtained by straightforward modifications

of (37) and (38). Quite obviously, no reasonable

parameter estimates are obtained in the cases with . Only for

, , the table indicates a comparably small error

. The prediction error shows a somewhat

better behavior. It is, however, always larger than the prediction

error of the augmented model. The relative difference increases with .

It was mentioned in Section 4 that a suitable criterion to estimate

the dimension of an approximate factor model consists in minimizing

(26). This criterion proved to work well in our simulation

study. Recall that the true factor dimension is . For the

average value of the estimate determined

by (26) is 2.64. In all other situations reported in Table

1 an estimate

is obtained in each of the 1,000 replications.

Table 2: Estimation errors under

different setups ()

Parameter estimates

Prediction

Opt.

Sample

Exact

Opt.

Lasso applied to augmented model:

0.06

1

0.3191

0.6104

0.0670

0.2259

2.46

0.2

1

0.2529

0.5335

0.0414

0.0727

3.92

0.4

1

0.2500

0.6498

0.0319

0.0454

4.35

0.6

1

0.2866

1.1683

0.0273

0.0350

4.56

0.06

0

0.0908

0.4238

0.0257

0.0311

4.62

0.2

0

0.1044

0.4788

0.0257

0.0316

4.69

0.4

0

0.1192

0.6400

0.0250

0.0314

4.74

0.6

0

0.1825

1.1745

0.0221

0.0276

5.13

Sample

Exact

Opt.

Lasso applied to standard linear regression

model:

0.06

1

5.0599

1.9673

0.0777

0.3758

1.95

0.2

1

3.4465

2.3662

0.0583

0.1403

2.63

0.4

1

2.9215

2.0191

0.0425

0.0721

2.45

0.6

1

3.2014

2.2246

0.0277

0.0387

1.47

0.06

0

0.4259

0.4259

0.0216

0.0285

4.80

0.2

0

0.4955

0.4955

0.0222

0.0295

4.24

0.4

0

0.6580

0.6580

0.0228

0.0303

3.17

0.6

0

1.1990

1.1990

0.0215

0.0283

1.66

Finally, Table 2 contains simulations results for , , and

different values of

. All columns have to be

interpreted similar to those of Table 1. For

suitable parameter estimates can obviously only been determined by

applying the augmented model. For

model (36) reduces to a sparse,

standard linear

regression model. It is then clearly unnecessary to apply the

augmented model.

Both methods then lead to roughly equivalent parameter estimates.

We want to emphasize that ,

constitutes a particularly

difficult situation. Then the first and second factor only explain

6% and 3% of the variance of . Consequently, is very

small and one will expect a fairly large error in estimating . Somewhat surprisingly the augmented

model still provides reasonable parameter estimates,

the only problem in this case seems to be a fairly large prediction error.

Another difficult situation in an opposite direction is , . Then both factors together explain 90%

of the variability of , while only explains the remaining

10%. Consequently, is very small and one may expect problems in

the context of the restricted eigenvalue condition. The

table shows that this case yields the smallest

prediction error, but the quality of parameter estimates deteriorates.

Appendix

{pf*}

Proof of Proposition 1

Define , ,

. For any and , noting that

, we have

where is the indicator function. We have

and

Applying the Bernstein inequality for bounded centered random variables

[see Hoeffding (1963)] we get

The result (1) is now a consequence of (Appendix) since

\upqed{pf*}

Proof of Theorem 1

For any symmetric matrix , we denote by

its eigenvalues. Weyl’s

perturbation theorem [see, e.g., Bhatia (1997), page 63] implies that

for any symmetric matrices and

and all

(5)

where is the usual matrix norm defined as

Since ,

(5) leads to .

By assumption, is a diagonal matrix

with diagonal entries , . Therefore and (14)

is an immediate consequence.

In order to verify (1) first note that Lemma A.1 of

Kneip and Utikal (2001) implies that for symmetric matrices and

where , are the eigenvectors corresponding

to the eigenvalues By assumption (A.3)

this implies

for all .

Since ,

the second part of (1) follows from

, .

By (A.3) we necessarily have for all

.

Consequently, .

Furthermore,

note that . Since and are uncorrelated, (14) and (1)

lead to

Since the second part of (1) follows from similar

arguments.

Finally, using the Cauchy–Schwarz inequality (17) is a

straightforward

consequence of (1).

{pf*}Proof of Theorem 2

With and , inequality (5)

implies that for all

But by assumptions (A.3) and (A.4), relation (22) leads to

. Equations (24) and (2)

then are immediate consequences of (9) and (10)

{pf*}Proof of Theorem 3

Choose an arbitrary . Note that

.

Since

we obtain the decomposition

Under

events (4)–(7), we have as well as

.

Furthermore,

and

for . Therefore,

Obviously, . It

now follows from Theorem 2

that there exists a constant , which can be chosen

independently of

all values

satisfying assumptions (A.3) and (A.4), such that

Since events (4)–(7) have probability ,

assertion (27) is an immediate consequence.

In order to show (28) first recall that the eigenvectors of

possess the well-known

“best basis” property, that is,

For and

define by

and

, . The

above property then implies

that for any

Since the vectors and

only

differ in the th element, one can conclude that for any

We obtain as

well as for .

At the same time under

events (4)–(7),

Note that for all .

By the Cauchy–Schwarz inequality, Theorem 2 and

Assumption (A.4), we have

as well as

.

The bounds for and derived in

Theorem 2 then imply that under

events (4)–(7) there exists a constant , which can be chosen independently of

all values

satisfying assumptions (A.3) and (A.4),

such that

(15)

At the same time,

by Theorem 2 it follows that there exist constants

such that

and ,

Note that

. Under

events (4)–(7), we can now conclude from

(Appendix)–(Appendix) that there exists a constant , which can be chosen independently of all

values satisfying Assumptions (A.3) and (A.4), such that

holds with . Since events (4)–(7) have probability ,

assertion (28) of Theorem 3 now is an immediate

consequence of (Appendix), (Appendix)

and (Appendix).

and Theorem 2 and assumptions (A.1)–(A.4) imply that under

events (4)–(7) there exist some constants

, which can be chosen independently of

all values

satisfying assumptions (A.3) and (A.4), such that

(21)

and

(22)

hold for all .

Now note that our setup implies that and

hold

for all

.

The Chebyshev inequality thus implies

that the event

(23)

holds with probability at least . We can thus infer from

(26)–(22)

that there exists some positive constant , which can be

chosen independently of the values satisfying (A.3)–(A.5),

such that under events (4)–(7) and (23)

Recall that events (4)–(7) and (24)

simultaneously hold with probability at least ,

while (23) is satisfied with

probability at least . This proves

assertion (3) with .

{pf*}Proof of Proposition 2

Let denote the diagonal matrix

with diagonal entries and split the -dimensional vector in two vectors and

, where is the

-dimensional vector with the upper components of

, and is the

-dimensional vector with the lower components of

. Then

The matrix is a diagonal matrix with entries , and for all . Together with the bounds for derived in Theorem 2 we can conclude that under

(4)–(7) there exists a constant

, which can be chosen independently of

all values

satisfying assumptions (A.3) and (A.4), such that

where , respectively, , is the -dimensional vector with the last

coordinates of , respectively, . The Cauchy–Schwarz inequality leads to . Since

we have

and the same upper bound holds for the terms and so that

Obviously, for all .

Using Theorem 2, one can infer that under

(4)–(7),

where the constant can be chosen independently of

all values

satisfying assumptions (A.3) and (A.4). When combining the above inequalities,

the desired result follows from (A.5) and the bound on to be obtained

from (27)

{pf*}Proof of Theorem 4

The first step of the proof consists of showing that under events

(4)–(7) the following inequality holds with probability

at least

(24)

where , and

is a sufficiently large positive constant.

Since and, hence, and are

independent of the i.i.d. error terms

, it follows from standard

arguments that

(25)

holds with probability at least . Therefore, in order

to prove

(24) it only remains to show that under events (4)–(7)

there exists a positive constant , which can be chosen

independently of the values satisfying (A.3)–(A.5), such that

Using the Cauchy–Schwarz inequality and the fact that , inequalities

(21) and (22) imply that under events

(4)–(7),

one obtains

Since also , similar

arguments show that under (4)–(7)

for

all .

The Cauchy–Schwarz inequality yields , , as well as

Necessarily, and hence .

It therefore follows from (24), (2),

(27) and (A.5) that under events (4)–(7)

there are

some constants , such that for all

and

,

and

Result (26) is now a direct consequence of (Appendix)–(Appendix). Note that all constants in

(Appendix)–(Appendix) and thus also the constant

can be chosen independently of the values

satisfying (A.3)–(A.5).

Under event (24) as well as , inequalities (B.1), (4.1), (B.27) and (B.30) of

Bickel, Ritov and Tsybakov (2009) may be transferred in our context which yields

(31)

where is the set of nonnull coefficients of . This implies that

(32)

Events (4)–(7) hold with probability , and

therefore the probability of event (24) is at least

. When combining

(2), (27) and (32), inequalities

(4) and (32) follow from

the definitions of and ,

since under

(4)–(7)

and

It remains to prove assertion (4) on the prediction

error. We have

Under event (24) as well as , the first part of inequalities (B.31) in the proof of

Theorem 7.2 of Bickel, Ritov and Tsybakov (2009) leads to

(34)

Under events (4)–(7), (24) as well as

(23), inequality (4) now follows from (Appendix), (34) and (3). The assertion

then is a consequence

of the fact that (4)–(7) are satisfied with

probability , while (24) and

(23) hold with probabilities at least and

, respectively.

References

Bai (2003){barticle}[mr]

\bauthor\bsnmBai, \bfnmJushan\binitsJ.

(\byear2003).

\btitleInferential theory for factor models of large dimensions.

\bjournalEconometrica

\bvolume71

\bpages135–171.

\biddoi=10.1111/1468-0262.00392, issn=0012-9682, mr=1956857

\bptokimsref

\endbibitem

Bai (2009){barticle}[mr]

\bauthor\bsnmBai, \bfnmJushan\binitsJ.

(\byear2009).

\btitlePanel data models with interactive fixed effects.

\bjournalEconometrica

\bvolume77

\bpages1229–1279.

\biddoi=10.3982/ECTA6135, issn=0012-9682, mr=2547073

\bptokimsref

\endbibitem

Bai and Ng (2002){barticle}[mr]

\bauthor\bsnmBai, \bfnmJushan\binitsJ. and \bauthor\bsnmNg, \bfnmSerena\binitsS.

(\byear2002).

\btitleDetermining the number of factors in approximate factor models.

\bjournalEconometrica

\bvolume70

\bpages191–221.

\biddoi=10.1111/1468-0262.00273, issn=0012-9682, mr=1926259

\bptokimsref

\endbibitem

Bernanke and Boivin (2003){barticle}[auto:STB—2011/09/12—07:03:23]

\bauthor\bsnmBernanke, \bfnmB. S.\binitsB. S. and \bauthor\bsnmBoivin, \bfnmJ.\binitsJ.

(\byear2003).

\btitleMonetary policy in a data-rich environment.

\bjournalJournal of Monetary Economics

\bvolume50

\bpages525–546.

\bptokimsref

\endbibitem

Bickel and Levina (2008){barticle}[mr]

\bauthor\bsnmBickel, \bfnmPeter J.\binitsP. J. and \bauthor\bsnmLevina, \bfnmElizaveta\binitsE.

(\byear2008).

\btitleRegularized estimation of large covariance matrices.

\bjournalAnn. Statist.

\bvolume36

\bpages199–227.

\biddoi=10.1214/009053607000000758, issn=0090-5364, mr=2387969

\bptokimsref

\endbibitem

Bickel, Ritov and Tsybakov (2009){barticle}[mr]

\bauthor\bsnmBickel, \bfnmPeter J.\binitsP. J.,

\bauthor\bsnmRitov, \bfnmYa’acov\binitsY. and \bauthor\bsnmTsybakov, \bfnmAlexandre B.\binitsA. B.

(\byear2009).

\btitleSimultaneous analysis of lasso and Dantzig selector.

\bjournalAnn. Statist.

\bvolume37

\bpages1705–1732.

\biddoi=10.1214/08-AOS620, issn=0090-5364, mr=2533469

\bptokimsref

\endbibitem

Cai and Hall (2006){barticle}[mr]

\bauthor\bsnmCai, \bfnmT. Tony\binitsT. T. and \bauthor\bsnmHall, \bfnmPeter\binitsP.

(\byear2006).

\btitlePrediction in functional linear regression.

\bjournalAnn. Statist.

\bvolume34

\bpages2159–2179.

\biddoi=10.1214/009053606000000830, issn=0090-5364, mr=2291496

\bptnotecheck year\bptokimsref

\endbibitem

Candes and Tao (2007){barticle}[mr]

\bauthor\bsnmCandes, \bfnmEmmanuel\binitsE. and \bauthor\bsnmTao, \bfnmTerence\binitsT.

(\byear2007).

\btitleThe Dantzig selector: Statistical estimation when is much

larger than .

\bjournalAnn. Statist.

\bvolume35

\bpages2313–2351.

\biddoi=10.1214/009053606000001523, issn=0090-5364, mr=2382644

\bptokimsref

\endbibitem

Cardot, Ferraty and Sarda (1999){barticle}[mr]

\bauthor\bsnmCardot, \bfnmHervé\binitsH.,

\bauthor\bsnmFerraty, \bfnmFrédéric\binitsF. and \bauthor\bsnmSarda, \bfnmPascal\binitsP.

(\byear1999).

\btitleFunctional linear model.

\bjournalStatist. Probab. Lett.

\bvolume45

\bpages11–22.

\biddoi=10.1016/S0167-7152(99)00036-X, issn=0167-7152, mr=1718346

\bptokimsref

\endbibitem

Cardot, Mas and Sarda (2007){barticle}[mr]

\bauthor\bsnmCardot, \bfnmHervé\binitsH.,

\bauthor\bsnmMas, \bfnmAndré\binitsA. and \bauthor\bsnmSarda, \bfnmPascal\binitsP.

(\byear2007).

\btitleCLT in functional linear regression models.

\bjournalProbab. Theory Related Fields

\bvolume138

\bpages325–361.

\biddoi=10.1007/s00440-006-0025-2, issn=0178-8051, mr=2299711

\bptokimsref

\endbibitem

Crambes, Kneip and Sarda (2009){barticle}[mr]

\bauthor\bsnmCrambes, \bfnmChristophe\binitsC.,

\bauthor\bsnmKneip, \bfnmAlois\binitsA. and \bauthor\bsnmSarda, \bfnmPascal\binitsP.

(\byear2009).

\btitleSmoothing splines estimators for functional linear regression.

\bjournalAnn. Statist.

\bvolume37

\bpages35–72.

\biddoi=10.1214/07-AOS563, issn=0090-5364, mr=2488344

\bptokimsref

\endbibitem

Cuevas, Febrero and Fraiman (2002){barticle}[mr]

\bauthor\bsnmCuevas, \bfnmAntonio\binitsA.,

\bauthor\bsnmFebrero, \bfnmManuel\binitsM. and \bauthor\bsnmFraiman, \bfnmRicardo\binitsR.

(\byear2002).

\btitleLinear functional regression: The case of fixed design and functional

response.

\bjournalCanad. J. Statist.

\bvolume30

\bpages285–300.

\biddoi=10.2307/3315952, issn=0319-5724, mr=1926066

\bptokimsref

\endbibitem

Forni and Lippi (1997){bbook}[auto:STB—2011/09/12—07:03:23]

\bauthor\bsnmForni, \bfnmM.\binitsM. and \bauthor\bsnmLippi, \bfnmM.\binitsM.

(\byear1997).

\btitleAggregation and the Microfoundations of Dynamic Macroeconomics.

\bpublisherOxford Univ. Press, \baddressOxford.

\bptokimsref

\endbibitem

Forni et al. (2000){barticle}[auto:STB—2011/09/12—07:03:23]

\bauthor\bsnmForni, \bfnmM.\binitsM.,

\bauthor\bsnmHallin, \bfnmM.\binitsM.,

\bauthor\bsnmLippi, \bfnmM.\binitsM. and \bauthor\bsnmReichlin, \bfnmL.\binitsL.

(\byear2000).

\btitleThe generalized dynamic factor model: Identification and estimation.

\bjournalReview of Economics and Statistics

\bvolume82

\bpages540–554.

\bptokimsref

\endbibitem

Hall and Horowitz (2007){barticle}[mr]

\bauthor\bsnmHall, \bfnmPeter\binitsP. and \bauthor\bsnmHorowitz, \bfnmJoel L.\binitsJ. L.

(\byear2007).

\btitleMethodology and convergence rates for functional linear regression.

\bjournalAnn. Statist.

\bvolume35

\bpages70–91.

\biddoi=10.1214/009053606000000957, issn=0090-5364, mr=2332269

\bptokimsref

\endbibitem

Hall and Hosseini-Nasab (2006){barticle}[mr]

\bauthor\bsnmHall, \bfnmPeter\binitsP. and \bauthor\bsnmHosseini-Nasab, \bfnmMohammad\binitsM.

(\byear2006).

\btitleOn properties of functional principal components analysis.

\bjournalJ. R. Stat. Soc. Ser. B Stat. Methodol.

\bvolume68

\bpages109–126.

\biddoi=10.1111/j.1467-9868.2005.00535.x, issn=1369-7412, mr=2212577

\bptokimsref

\endbibitem

Hoeffding (1963){barticle}[mr]

\bauthor\bsnmHoeffding, \bfnmWassily\binitsW.

(\byear1963).

\btitleProbability inequalities for sums of bounded random variables.

\bjournalJ. Amer. Statist. Assoc.

\bvolume58

\bpages13–30.

\bidissn=0162-1459, mr=0144363

\bptokimsref

\endbibitem

Kneip and Utikal (2001){barticle}[mr]

\bauthor\bsnmKneip, \bfnmAlois\binitsA. and \bauthor\bsnmUtikal, \bfnmKlaus J.\binitsK. J.

(\byear2001).

\btitleInference for density families using functional principal component

analysis.

\bjournalJ. Amer. Statist. Assoc.

\bvolume96

\bpages519–542.

\bnoteWith comments and a rejoinder by the authors.

\biddoi=10.1198/016214501753168235, issn=0162-1459, mr=1946423

\bptokimsref

\endbibitem

Meinshausen and Bühlmann (2006){barticle}[mr]

\bauthor\bsnmMeinshausen, \bfnmNicolai\binitsN. and \bauthor\bsnmBühlmann, \bfnmPeter\binitsP.

(\byear2006).

\btitleHigh-dimensional graphs and variable selection with the lasso.

\bjournalAnn. Statist.

\bvolume34

\bpages1436–1462.

\biddoi=10.1214/009053606000000281, issn=0090-5364, mr=2278363

\bptokimsref

\endbibitem

Ramsay and Dalzell (1991){barticle}[mr]

\bauthor\bsnmRamsay, \bfnmJ. O.\binitsJ. O. and \bauthor\bsnmDalzell, \bfnmC. J.\binitsC. J.

(\byear1991).

\btitleSome tools for functional data analysis (with discussion).

\bjournalJ. Roy. Statist. Soc. Ser. B

\bvolume53

\bpages539–572.

\bidissn=0035-9246, mr=1125714

\bptnotecheck related\bptokimsref

\endbibitem

Stock and Watson (2002){barticle}[mr]

\bauthor\bsnmStock, \bfnmJames H.\binitsJ. H. and \bauthor\bsnmWatson, \bfnmMark W.\binitsM. W.

(\byear2002).

\btitleForecasting using principal components from a large number of

predictors.

\bjournalJ. Amer. Statist. Assoc.

\bvolume97

\bpages1167–1179.

\biddoi=10.1198/016214502388618960, issn=0162-1459, mr=1951271

\bptokimsref

\endbibitem

Tibshirani (1996){barticle}[mr]

\bauthor\bsnmTibshirani, \bfnmRobert\binitsR.

(\byear1996).

\btitleRegression shrinkage and selection via the lasso.

\bjournalJ. Roy. Statist. Soc. Ser. B

\bvolume58

\bpages267–288.

\bidissn=0035-9246, mr=1379242

\bptokimsref

\endbibitem

van de Geer (2008){barticle}[mr]

\bauthor\bparticlevan de \bsnmGeer, \bfnmSara A.\binitsS. A.

(\byear2008).

\btitleHigh-dimensional generalized linear models and the lasso.

\bjournalAnn. Statist.

\bvolume36

\bpages614–645.

\biddoi=10.1214/009053607000000929, issn=0090-5364, mr=2396809

\bptokimsref

\endbibitem

Yao, Müller and Wang (2005){barticle}[mr]

\bauthor\bsnmYao, \bfnmFang\binitsF.,

\bauthor\bsnmMüller, \bfnmHans-Georg\binitsH.-G. and \bauthor\bsnmWang, \bfnmJane-Ling\binitsJ.-L.

(\byear2005).

\btitleFunctional linear regression analysis for longitudinal data.

\bjournalAnn. Statist.

\bvolume33

\bpages2873–2903.

\biddoi=10.1214/009053605000000660, issn=0090-5364, mr=2253106

\bptokimsref

\endbibitem

Zhao and Yu (2006){barticle}[mr]

\bauthor\bsnmZhao, \bfnmPeng\binitsP. and \bauthor\bsnmYu, \bfnmBin\binitsB.

(\byear2006).

\btitleOn model selection consistency of Lasso.

\bjournalJ. Mach. Learn. Res.

\bvolume7

\bpages2541–2563.

\bidissn=1532-4435, mr=2274449

\bptokimsref

\endbibitem

Zhou, Lafferty and Wassermn (2008){bmisc}[auto:STB—2011/09/12—07:03:23]

\bauthor\bsnmZhou, \bfnmS.\binitsS.,

\bauthor\bsnmLafferty, \bfnmJ.\binitsJ. and \bauthor\bsnmWassermn, \bfnmL.\binitsL.

(\byear2008).

\bhowpublishedTime varying undirected graphs.

In Proceedings of the 21st Annual Conference on Computational

Learning Theory (COLT’08).

Available at arXiv:0903.2515.

\bptokimsref

\endbibitem

Zhou, van de Geer and

Bülhmann (2009){bmisc}[auto:STB—2011/09/12—07:03:23]

\bauthor\bsnmZhou, \bfnmS.\binitsS., \bauthor\bparticlevan de

\bsnmGeer, \bfnmS.\binitsS. and \bauthor\bsnmBülhmann, \bfnmP.\binitsP.

(\byear2009).

\bhowpublishedAdaptive Lasso for high dimensional regression and

Gaussian graphical modeling. Preprint.

\bptokimsref

\endbibitem