Killed Brownian motion with a prescribed lifetime distribution

and models of default

Boris Ettingerlabel=e1]ettinger@princeton.edu

[Steven N. Evanslabel=e2]evans@stat.berkeley.edu

[Alexandru Heninglabel=e3]hening@stats.ox.ac.uk

[

Princeton University, University of California and University of Oxford

B. Ettinger

Department of Mathematics

Princeton University

Fine Hall, Washington Road

Princeton, New Jersey 08544-1000

USA

S. N. Evans

Department of Statistics

University of California

367 Evans Hall #3860

Berkeley, California 94720-3860

USA

A. Hening

Department of Statistics

University of Oxford

1 South Parks Road

Oxford OX1 3TG

United Kingdom

(2014; 12 2011; 9 2012)

Abstract

The inverse first passage time problem asks whether, for a Brownian

motion and a nonnegative random variable , there exists a

time-varying barrier such that . We study a “smoothed” version of

this problem and ask whether there is a “barrier” such that

, where is a killing rate parameter,

and is a nonincreasing function. We

prove that if is suitably smooth, the function is twice continuously differentiable, and the

condition

holds for the hazard rate of , then there exists a unique

continuously differentiable function solving the smoothed problem.

We show how this result leads to flexible models of default for which

it is possible to compute expected values of contingent claims.

60J70,

91G40,

91G80,

Credit risk,

inverse first passage time problem,

killed Brownian motion,

Cox process,

stochastic intensity,

Feynman–Kac formula,

doi:

10.1214/12-AAP902

keywords:

[class=AMS]

keywords:

††volume: 24††issue: 1

,

and

t1Supported in part by NSF grant DMS-09-07630.

\pdfkeywords

60J70, 91G40, 91G80, Credit risk, inverse first passage time problem, killed Brownian motion,

Cox process, stochastic intensity, Feynman–Kac formula

1 Introduction

Investors are exposed to credit risk, or counterparty risk, due to the

possibility that one or more counterparties in a financial agreement

will default, that is, not honor their obligations to make certain

payments. Counterparty risk has to be taken into account when pricing a

transaction or portfolio, and it is necessary to model the occurrence

of default jointly with the behavior of asset values.

The default time is sometimes modeled as the first passage time of a

credit index process below a barrier. Black and Cox BC76 were

among the first to use this approach. They define the time of default

as the first time the ratio of the value of a firm and the value of its

debt falls below a constant level, and they model debt as a zero-coupon

bond and the value of the firm as a geometric Brownian motion. In this

case, the default time has the distribution of the first-passage time

of a Brownian motion (with constant drift) below a certain barrier.

Hull and White HW01 model the default time as the first time a

Brownian motion hits a given time-dependent barrier. They show that

this model gives the correct market credit default swap and bond prices

if the time-dependent barrier is chosen so that the first passage time

of the Brownian motion has a certain distribution derived from those

prices. Given a distribution for the default time, it is usually

impossible to find a closed-form expression for the corresponding

time-dependent barrier, and numerical methods have to be used.

We adopt a perspective similar to that of Hull and White HW01 .

Namely, we model the default time as

(1)

where the diffusion is some credit index process, is an

independent mean one exponentially distributed random variable, is a suitably smooth, nonincreasing function with

and , and is a rate parameter. Then

(2)

The random time is a “smoothed-out” version of the stopping

time of Hull and White; instead of killing as soon at it crosses

some sharp, time-dependent boundary, we kill at rate if it is in state at time . That

is,

When the credit index value is large, corresponding to a time

when the counterparty is in sound financial health, the killing rate

is close to and default in an ensuing

short period of time is unlikely, whereas the killing rate is close to

its maximum possible value, , when is low and default is

more probable. Note that if we consider a family of -valued,

nonincreasing functions that converges to the indicator

function of the set and

tends to , then the corresponding stopping time

converges to the Hull and White stopping time .

The hazard rate of the random time is

(3)

On the other hand, suppose that is a

nonnegative random variable with

survival function .

Writing for the derivative of , the corresponding hazard rate is

As a result, a necessary condition for a function to exist such that

the corresponding random time has the same distribution as

is that

(4)

We show in Theorem 2.1 that if is a Brownian motion

with a given suitable random initial condition, assumption

(4) holds, and the survival function is twice

continuously differentiable, then there is a unique differentiable

function such that the stopping time has the same

distribution as . In particular, we establish that the function

can be determined by solving a system consisting of a parabolic

linear PDE with coefficients depending on and a nonlinear ODE

for with coefficients depending on the solution of the PDE. Note from

(2) that changing the function on a set with Lebesgue

measure zero does not affect the distribution of , and so we have

to be careful when we talk about the uniqueness of . This minor

annoyance does not appear if we restrict to continuous .

In Theorem 4.1 we give an analogue of the existence part

of the above result when is the indicator of the set .

Having proven the existence and uniqueness of a barrier , we

consider the pricing of certain contingent claims in

Section 5. For simplicity, we take the asset price

to be a geometric Brownian motion

where is a standard Brownian motion. We take the

credit index

to be given by

where is another standard Brownian motion, and take the default

time to be given by (1), where the exponential random

variable is independent of the asset price and the credit index

. We assume that the Brownian motions and are correlated;

that is, that their covariation is for some constant

. We consider claims with a payoff of the form

for some fixed maturity . We show how it is

possible to compute conditional expected values such as

In Section 6 we report the results of some experiments

where we solved the PDE/ODE system for the barrier numerically.

Finally, in Section 7, we follow DP11 to

demonstrate how it is possible to use market data on credit default

swap prices to determine the survival function .

1.1 The FPT and IFPT problems

We end the this Introduction with a brief discussion

of the literature dealing with first passage times of diffusions across

time-dependent barriers.

Consider a Brownian motion defined on a filtered

probability space which satisfies the usual conditions. Define the

diffusion via the SDE

where we assume that the coefficients

and

are

such that the SDE has a unique strong solution.

For a Borel function

, the first passage time of the diffusion

process below the barrier is the stopping time

(5)

The following two problems related to this notion have been discussed

in the literature.

The first passage time problem (FPT): For a given barrier

, compute the

survival function of the first time that goes below ; that

is, find

(6)

The inverse first passage time problem (IFPT): For a given

survival function , does there exist a barrier such that

for all ?

A large class of first passage time problems may be

solved within a PDE framework.

Let

be the sub-probability density of the diffusion killed at .

Then, by the Kolmogorov forward equation, satisfies

(7)

where is the probability density of .

For nice enough functions this system has a unique solution, and we

can express the survival probability as

This approach is used in L86 , V09

to get closed form solutions for some classes of boundaries.

An integral equation technique is used in

P2002a , P2002b , PS06 , V09 to find the derivative in

the FPT problem for a Brownian motion. Writing , the

derivative satisfies a Volterra integral equation of the first kind

of the form

This and other such integral equations can be used

to find numerically.

Shiryaev is generally credited with introducing the IFPT problem in

1976 (we have not been able to find an explicit reference).

Most authors have investigated numerical methods for finding the

boundary. Details can be found in HW00 , HW01 , IK02 , ZSP03 .

It is shown in AZ01 that for sufficiently smooth boundaries the

density and the boundary are a solution of the

following free boundary problem:

(8)

where is again the probability density of . The existence and

uniqueness of a viscosity solution of (8) is established

in CCCS11 along with upper and lower bounds on the asymptotic

behavior of . That paper also shows that this does in fact

produce a boundary that gives the survival function . To our

knowledge it has not be proven that a strong solution to the system

(8) exists, nor that there is a smooth solving the

IFPT.

A variation of the IFPT is studied in DP11 , DaPi13 . There the barrier is

fixed at zero (i.e., ), and it is the volatility parameter

, that is, allowed to vary. The authors show that

this problem admits an explicit solution for every differentiable

survival function.

2 Global existence and uniqueness

Suppose for the remainder of this paper that , where

is a standard Brownian motion, and is a random

variable, independent of and with density .

In this case, (2) is

which, by time reversal, becomes

Set

(9)

That is, is the sub-probability density of

killed at the random time .

It is well known that if is smooth enough, then is the unique

solution of the PDE

Any solution to this PDE satisfies

(10)

Our question as to whether we can find a “barrier” giving us the

survival function is now equivalent to whether the system

(11)

has solutions . Differentiating the third equation from

(11) with respect to and then using the first equation

together with an integration by parts, we get that

(12)

where we recall that .

A second differentiation in followed by another integration by

parts yields

Note that (2) may be rearranged to give an ODE for of the

form , where the function is

constructed from the function (which, of course, depends in turn

on ). Re-writing this integral equation in the form leads to the following theorem, our main

result.

Theorem 2.1

Suppose the following:

•

The survival function is twice continuously

differentiable with first and second derivatives and

and for all for some

constant .

•

The initial density satisfies

, for all

, , and the functions

, , are bounded.

•

The function is nonincreasing and belongs to

, and for some , for

and for .

Then, there exists a unique continuously differentiable function

such that the following three

equations hold:

(14)

and

for all .

{pf}

From now on we assume for ease of notation that . The

modifications necessary for general are straightforward. The

proof will be via a sequence of lemmas, all of them assuming the

hypotheses of Theorem 2.1 (with ). We start

with the following simple observation.

Lemma 2.2

Suppose that

for some continuous function such that for , .

Then, for each there exists a unique

such that

{pf}

Set

Then

and, by assumption,

Furthermore, is continuous and strictly decreasing in . So, by

the intermediate value property, we can find a unique such that .

Lemma 2.3((Global uniqueness))

Suppose there exist continuous functions such that equations

(14), (LABEL:e2) and (2.1) are satisfied for and

. Then for all .

{pf}

Recall that we are assuming to simplify notation.

Suppose that and are two continuous solutions of

(14), (LABEL:e2) and (2.1). It follows from Lemma 2.2

and (LABEL:e2) that . Set , and suppose that .

Define by

where for . Define functions

, , by , . Then ,

and

Fix , and set

By the triangle inequality, for ,

where

and

Consider the integrand in . Note that

Similar arguments for the integrands in and

using the boundedness and global Lipschitz properties of

, and establish that, for a suitable

constant ,

for . It follows from Grönwall’s

inequality that for , and so for , contrary to the definition of and the assumption that

is finite.

Lemma 2.4((Global existence))

Define to be the supremum of the set of such that equations

(14), (LABEL:e2) and (2.1) have a continuous solution on

. Then .

{pf}

Suppose to the contrary that . From Lemma 2.3,

the equations have a unique solution on . By time-reversal,

equation (14) is equivalent to

(17)

Similarly, (LABEL:e2) is equivalent to

For put

(19)

Consider . It follows from the continuity

of the sample paths of that as

We claim that . If this was not the case, then,

by passing to a subsequence we would have converging to

some other extended real and hence, by dominated convergence,

contradicting the definition of [where we used the natural

definitions , ].

Using dominated convergence in (2.1) we get that there exists a

continuous such that all three equations hold on .

All we need to do now is show that we can extend the existence from

to for some . This amounts to

proving existence on starting at a different initial

condition—replacing the

original probability density by the density of the probability measure

This will follow if we can establish the local existence, that is, the

existence for some , of a solution of the following PDE/ODE system:

We note that the expression for is not the analogue of

the one for that arises immediately from differentiating

(2.1), which in turn arose from rearranging (2) and

integrating. However, adding

to the right-hand

side of (2) and then solving for leads to an expression

of this form. Note that

and, by dominated convergence, that

with ,

,

all finite. Therefore, we

can apply Theorem 3.14 below to get that there is a time

and a unique pair satisfying the

PDE/ODE system above with twice continuously differentiable

in on and once continuously differentiable in on

, that is, , and with . Thus, we have proven that we have a unique continuous

satisfying equations (14), (LABEL:e2) and (2.1) on

. This contradicts the maximality of . As a result,

and we are done.

Theorem 3.14 below gives local in time existence and

uniqueness of solutions to the system (11). However, we require

the global uniqueness result Lemma 2.3 because it is not

a priori clear that all the solutions to equations

(14)–(2.1) are solutions to the system (11).

Remark 2.6.

It follows from the (2.1), the smoothness assumptions on , the

smoothness assumptions on , the smoothness assumptions on and

the assumption that is everywhere positive that the function

has a finite right derivative at . In the standard inverse first

passage problem, the analogous property for the boundary often fails

(e.g., when the lifetime distribution is exponential).

As a corollary we get the global existence and uniqueness of the

PDE/ODE system.

Corollary 2.7

Suppose that the conditions of Theorem 2.1 hold. Then

the system

(20)

has a unique solution .

3 Local existence and uniqueness

We now consider the PDE/ODE system (20). We have already

used the standard notation and to denote the first and

second derivatives of a function of one variable or the first and

second partial derivatives with respect to the variable of a

function of several variables. Because we repeatedly deal with the

function , it will be convenient to

recycle notation and define a function by . We will

then set and

. We will continue to use the

notation and with its old meaning, but there

should be no confusion between the different objects and

. Similarly, we set and

put . Finally, for two functions ,

and fixed define ,

.

In the notation we have introduced, we wish to consider the system

(21)

for some . [In the proof of

Theorem 2.1 we choose to satisfy , but we may take an arbitrary

value for and still obtain a local existence and uniqueness

result.]

We have assumed in the statement of Theorem 2.1 that

and with , , , and for finite constants ,

, . Furthermore, we have assumed for some that

for , that for and that and

for all . Set

, and note that . It

is immediate that and . Moreover, the functions and

are supported on and

.

Definition 3.1.

For , let

be the Banach space consisting of pairs of functions

such that , and

Definition 3.2.

Given constants , , , , , and , define the closed subset by

The following is the main result of this section.

Theorem 3.3

Suppose that the assumptions of Theorem 2.1 hold.

Suppose also that the constants , , , , and are such that:

•

,

•

for ,

•

,

•

,

•

.

Then for sufficiently small, there is a contractive map

defined by

,

where

(24)

We will prove Theorem 3.3 in a series of lemmas. Each

lemma will assume the hypotheses of Theorem 3.3 and the

bounds established in the previous lemmas.

Remark 3.4.

Since is continuous and positive, for any there exists

such that for . Therefore, we are not

restricting the possible values of by the above assumptions. We

will also assume without loss of generality that .

Lemma 3.5((Boundedness of ))

Suppose that

, with .

Then, there exists a time such that

Therefore, there exists a time such that whenever

and ,

\upqed

Lemma 3.9

For a sufficiently small time , the set is

mapped into itself by .

{pf}

The above lemmas provided the necessary bounds. Now, note that if we

start with , then we first get the

function from the last two equations in (24) by simply

integrating. The integration is well defined because the denominator is

bounded in absolute value below by and the numerator is bounded

above. Thus . Next, having in hand we get the

function from the first two equations of (24). We note

that, by Duhamel’s formula, the function has actually more than the

desired smoothness, namely, .

Lemma 3.10

Suppose that . Set

and . For any

there exists such that

(28)

{pf}

Note that the functions , satisfy

(29)

Subtracting the two equations gives

Using the fact that the functions , and are

Lipschitz, that and are bounded, and that their first

derivatives are bounded,

we find that

Integrating and recalling that leads to

Hence,

and by the above bound on for any

we can choose small enough that

\upqed

Lemma 3.11

Suppose that . Set

and . For any

there exists such that

(30)

{pf}

The following equations hold:

(31)

By Duhamel’s formula we have

(32)

and

(33)

where we recall that denotes convolution on . Subtracting the two equations gives

Bounding in terms of the norm and using the fact that

Suppose that the conditions of

Theorem 2.1 hold. Then, there exists a time such

that the system

has a unique solution .

{pf}

Note there exist strictly positive constants and such

that , , when

, ,, and

. Putting all the estimates

from the above lemmas together we have that, if is

fixed, then for small enough,

Thus there exists a such that the map is a contraction. Since

is a closed subset of the Banach space

, the contraction mapping theorem gives that there

exists a unique fixed point, that is, a pair with such that

(40)

We can now argue that our fixed point has more smoothness than

it seems a priori. The third equation in (40) implies that

must be continuously differentiable with a bounded derivative. This,

together with the first equation from (40) then tells us that

has a continuous derivative in time. Therefore, we must have

.

Corollary 3.15

Assume the hypotheses of

Theorem 3.14 and the extra conditions

(41)

Then, there exists a time such that the system

has a unique solution .

Furthermore, and .

{pf}

First note that by Lemma 2.2 we have that is uniquely

determined. From Theorem 3.14 we have that there exist

unique , with and satisfying the PDE and having everywhere in

Set and note that the first

two conditions from (41) yield, together with the

PDE, . The function belongs to , and

belongs to . The above equation for is equivalent,

after using the PDE, to

Integrating and using the fundamental theorem of calculus, we get

The unique solution to this differential equation is for

some constant . This together with yields

for . Thus

Then, taking a derivative and using the PDE,

Because for , for and , we see that

\upqed

4 Discontinuous killing

Next, we consider

the existence of a barrier when killing is done nonsmoothly.

That is, we ask whether there exists a function such that, for a

given ,

(42)

Note that is

the time during the interval spent by a Brownian motion started

at below the barrier .

Theorem 4.1

There exists a function such that, for a

given, twice continuously differentiable satisfying

, , equation (42) holds for

all .

{pf}

Let be a smooth decreasing function supported on with

. Put

and

so that

(43)

Note also that

(44)

and

(45)

Let and be the

two barriers corresponding to and

. The existence and uniqueness of these

two barriers follows by Theorem 2.1. From (43) we

have that

and both of these functions give a stopping time with the correct

distribution for the case where is the indicator of

. Because of (46), it must be the case that

for Lebesgue almost all .

5 Pricing claims

Suppose that the asset price is a geometric Brownian

motion given by

(47)

where

is a standard Brownian motion. We model default

using a diffusion , where

(48)

with another standard Brownian motion. We assume

that the Brownian motions and are correlated with correlation

; that is, the cross-variation of the two processes

satisfies

We can assume without loss of generality that for two independent

Brownian motions we have

In the following we will look at pricing contingent claims with a fixed

maturity and payoff of the form

for the random time

where is an independent exponentially distributed random variable

with mean one.

Note that

More generally, we will be interested in expressions of the form

which we interpret as the price of the payoff at time

given that default has not yet occurred.

Consider the Markov process , where , are as above,

and is a process that, when started at is at after

units of time, that is, . The generator of is

We want to compute

The Feynman–Kac formula says that the solution to the PDE

(49)

satisfies

Thus, if we assume the Brownian motion has a random starting point

with density , that is, independent of , then

Using this and the Markov property, one can find the function

satisfying

The price at time , given that we know the history of the price

process and that default has not happened up to time , is

It follows from the SDE for that

so if we observe the asset price , then we can reconstruct the

standard Brownian motion . On the other hand,

Now,

We therefore want to be able to compute for a function the conditional expected value

with a standard Brownian motion independent of

. We can do this using Feynman–Kac.

The denominator in the formula for the price at time is a special case

of the numerator we have just calculated

with , and it can be dealt with in the same way.

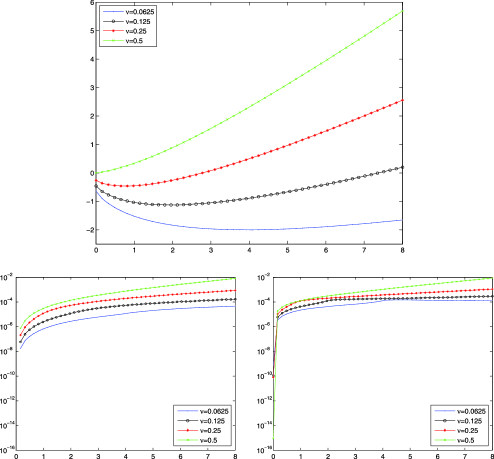

Figure 1: This figure displays the results of the numerical experiments

described in Section 6. We fix the standard

deviation for the initial distribution of the credit index process

to be and the killing parameter to be .

The first row gives the barriers for the rate parameters

of the exponential default time distribution.

The first (resp., second) panels in the second row give the relative

errors between

the actual survival function values [resp., the actual hazard

function values ] and the numerically

computed ones; see the text for details.

We have thus observed that computing the price of a contingent claim

reduces to solving certain PDEs with coefficients depending on the path

of the asset price.

6 Numerical results

In this section we present the results of somenumerical experiments.

We solved the PDE/ODE system (20) usingthe pseudo-spectral

implicit-explicit fourth order Runge–Kutta schemeARK4(3)6L[2]SA-ERK,

taking 8192 nodes and period 16, developed in MR03 . For the

function we used the Fejér kernel of order 512 applied to

the indicator of the set ; in other

words is the Cesàro sum of the truncated Fourier series of

order 512 of the indicator of the set . The time horizon was taken to be , the initial distribution

of the credit index process was taken to be normal [ with standard deviation ], and the time to

default was taken to have an exponential distribution [ with rates ].

For the first experiment, we fix the killing parameter to .

We show the resulting barriers in Figure 1. We also show

the relative error between the survival function and the

numerically computed value of [recall

(11)], and the relative error between the hazard rate

and the numerically computed value of

[recall (12)].

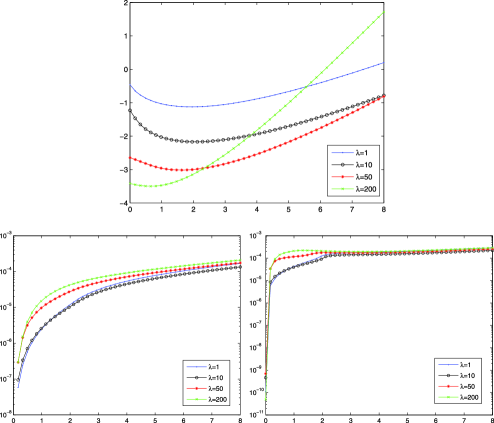

For the second experiment, we take the exponential rate to be

and the standard deviation to be . We look at

the graphs for when the killing parameter is .

The barriers, together with the relative errors in the survival

functions and hazard rates are given in Figure 2.

Figure 2: In this figure we fixed the standard deviation to

and the rate parameter to . The first row gives the barriers

for the killing parameters . The first and second

panels in the second row give the relative errors for the survival function

(resp., the hazard function).

7 Calibrating the default distribution using CDS rates

For the sake of completeness, we review briefly the scheme proposed in

DP11 for determining the distribution of the time to default.

A credit default swap (CDS) is a contract between two parties.

The buyer of the swap makes a number of predetermined

payments until the moment of default.

The seller is liable to pay the unrecovered value of the underlying

bond in the event of a default before maturity.

Normalizing the notional value of the bond to ,

the seller’s contingent payment is ,

where is the recovery rate,

which we take to be constant.

The premium payments are made at a set of times .

The maturities are a subset of the premium payment times;

that is, they are of the form , , .

For there is

an upfront premium and a running premium rate

(having accrual factors ). Denote the

price at time zero of a zero coupon risk-free bond with maturity

by .

It follows from standard nonarbitrage arguments that

where is the tail of the distribution of the

time to default.

Suppose now that the

default distribution has piecewise constant hazard rate; that is, that

where for . Given the market data

we can find, using

equation (7), the constants

We use the following procedure to find the barrier . Set

and . Given the initial density , which we can

choose to be any strictly positive function , that is, twice

continuously differentiable with bounded , and , we want

to find a barrier such that for we have

This can be achieved by solving the ODE/PDE system (20).

Next, set , , , and find a barrier

with such that on we have

This procedure can be repeated until we find a function on

, that is, continuously differentiable everywhere, except

perhaps the finite number of points .

8 Duhamel’s formula

For the sake of reference, we provide a statement of Duhamel’s formula.

Given functions and

, the solution of

(51)

is given by

where

(53)

Acknowledgments

We are grateful to Professor Jon Wilkening

for helpful comments regarding Section 6 and to an

anonymous referee for suggestions which improved this paper.

References

(1){barticle}[auto:STB—2013/09/05—09:00:14]

\bauthor\bsnmAvellaneda, \bfnmM.\binitsM. and \bauthor\bsnmZhu, \bfnmJ.\binitsJ.

(\byear2001).

\btitleModelling the distance-to-default process of a firm.

\bjournalRisk

\bvolume14

\bpages125–129.

\bptokimsref

\endbibitem

(2){barticle}[auto:STB—2013/09/05—09:00:14]

\bauthor\bsnmBlack, \bfnmF.\binitsF. and \bauthor\bsnmCox, \bfnmJ. C.\binitsJ. C.

(\byear1976).

\btitleValuing corporate securities: Some effects of bond indenture

provisions.

\bjournalJ. Finance

\bvolume31

\bpages351–367.

\bptokimsref

\endbibitem

(3){barticle}[mr]

\bauthor\bsnmChen, \bfnmXinfu\binitsX.,

\bauthor\bsnmCheng, \bfnmLan\binitsL.,

\bauthor\bsnmChadam, \bfnmJohn\binitsJ. and \bauthor\bsnmSaunders, \bfnmDavid\binitsD.

(\byear2011).

\btitleExistence and uniqueness of solutions to the inverse boundary crossing

problem for diffusions.

\bjournalAnn. Appl. Probab.

\bvolume21

\bpages1663–1693.

\biddoi=10.1214/10-AAP714, issn=1050-5164, mr=2884048

\bptokimsref

\endbibitem

(4){bmisc}[auto:STB—2013/09/05—09:00:14]

\bauthor\bsnmDavis, \bfnmM. H. A.\binitsM. H. A. and \bauthor\bsnmPistorius, \bfnmM. R.\binitsM. R.

(\byear2011).

\bhowpublishedOn an explicit solution to an inverse-first passage problem and

quantification of counterparty risk via Bessel bridges. Preprint.

\bptokimsref

\endbibitem

(5){bmisc}[auto:STB—2013/09/05—09:00:14]

\bauthor\bsnmDavis, \bfnmM. H. A.\binitsM. H. A. and \bauthor\bsnmPistorius, \bfnmM. R.\binitsM. R.

(\byear2013).

\bhowpublishedExplicit solution to an inverse

first-passage time problem for Lévy processes.

Application to counterparty credit risk.

Available at \arxivurlarXiv:1306.2719v1.

\bptokimsref

\endbibitem

(7){barticle}[auto:STB—2013/09/05—09:00:14]

\bauthor\bsnmHull, \bfnmJ. C.\binitsJ. C. and \bauthor\bsnmWhite, \bfnmA.\binitsA.

(\byear2000).

\btitleValuing credit default swaps I: No counterparty default risk.

\bjournalJournal of Derivatives

\bvolume8

\bpages29–40.

\bptokimsref

\endbibitem

(8){bmisc}[auto:STB—2013/09/05—09:00:14]

\bauthor\bsnmIscoe, \bfnmI.\binitsI. and \bauthor\bsnmKreinin, \bfnmA.\binitsA.

(\byear2002).

\bhowpublishedDefault boundary problem. Working paper, Algorithmics Inc. Research Paper Series.

\bptokimsref

\endbibitem

(9){barticle}[mr]

\bauthor\bsnmKennedy, \bfnmChristopher A.\binitsC. A. and \bauthor\bsnmCarpenter, \bfnmMark H.\binitsM. H.

(\byear2003).

\btitleAdditive Runge–Kutta schemes for convection–diffusion–reaction equations.

\bjournalAppl. Numer. Math.

\bvolume44

\bpages139–181.

\biddoi=10.1016/S0168-9274(02)00138-1, issn=0168-9274, mr=1951292

\bptokimsref

\endbibitem

(10){bbook}[mr]

\bauthor\bsnmLerche, \bfnmHans Rudolf\binitsH. R.

(\byear1986).

\btitleBoundary Crossing of Brownian Motion. Its Relation to the Law of the Iterated Logarithm and to Sequential

Analysis.

\bseriesLecture Notes in Statistics

\bvolume40.

\bpublisherSpringer, \blocationBerlin.

\bidmr=0861122

\bptokimsref

\endbibitem

(11){barticle}[mr]

\bauthor\bsnmPeskir, \bfnmGoran\binitsG.

(\byear2002).

\btitleLimit at zero of the Brownian first-passage density.

\bjournalProbab. Theory Related Fields

\bvolume124

\bpages100–111.

\biddoi=10.1007/s004400200208, issn=0178-8051, mr=1929813

\bptokimsref

\endbibitem

(12){barticle}[mr]

\bauthor\bsnmPeskir, \bfnmGoran\binitsG.

(\byear2002).

\btitleOn integral equations arising in the first-passage problem for

Brownian motion.

\bjournalJ. Integral Equations Appl.

\bvolume14

\bpages397–423.

\biddoi=10.1216/jiea/1181074930, issn=0897-3962, mr=1984752

\bptokimsref

\endbibitem

(13){bbook}[mr]

\bauthor\bsnmPeskir, \bfnmGoran\binitsG. and \bauthor\bsnmShiryaev, \bfnmAlbert\binitsA.

(\byear2006).

\btitleOptimal Stopping and Free-Boundary Problems.

\bpublisherBirkhäuser, \blocationBasel.

\bidmr=2256030

\bptokimsref

\endbibitem

(14){bmisc}[mr]

\bauthor\bsnmValov, \bfnmAngel Veskov\binitsA. V.

(\byear2009).

\bhowpublishedFirst passage times: Integral equations, randomization and analytical approximations.

Ph.D. thesis, Univ. Toronto.

\bidmr=2753142

\bptokimsref

\endbibitem

(15){barticle}[mr]

\bauthor\bsnmZucca, \bfnmCristina\binitsC. and \bauthor\bsnmSacerdote, \bfnmLaura\binitsL.

(\byear2009).

\btitleOn the inverse first-passage-time problem for a Wiener process.

\bjournalAnn. Appl. Probab.

\bvolume19

\bpages1319–1346.

\biddoi=10.1214/08-AAP571, issn=1050-5164, mr=2538072

\bptokimsref

\endbibitem