The Generalized Shiryaev’s Problem

and

Skorohod Embedding111This research was

supported in part by the Natural Sciences and Engineering

Research Council (NSERC) of Canada.

Abstract

In this paper we consider a connection between the famous Skorohod embedding problem and the Shiryaev inverse problem for the first hitting time distribution of a Brownian motion: given a probability distribution, , find a boundary such that the first hitting time distribution is . By randomizing the initial state of the process we show that the inverse problem becomes analytically tractable. The randomization of the initial state allows us to significantly extend the class of target distributions in the case of a linear boundary and moreover allows us to establish connection with the Skorohod embedding problem.

keywords:

First hitting time, Shiryaev’s inverse boundary problem, Skorohod embedding1 Introduction

Let be an arbitrary process with the left-continuous sample paths and let be a continuous absorbing boundary satisfying the condition . The random variable

is called the first hitting time for the process . The problem

| Given a process, , and the boundary, , | (1) | ||

| find the distribution . |

is the starting point of a very rich research area in the theory of stochastic processes. If is a diffusion process, the problem of finding the distribution of is a classical one. The first papers on the problem were published by P. Levy, A. Khintchine and A. Kolmogorov in the 1920s. These results are discussed in the monograph333Khintchine called (1) the second problem of diffusion. Khintchine (1933). Khintchine gave a complete solution of the problem for sufficiently smooth boundaries. This solution was expressed in terms of a boundary value problem for the associated partial differential operator (infinitesimal generator). Since then many books and research papers were published in this area. The monograph Lerche (1986) summarizes known analytical results obtained by the mid-1980s. In Karatzas and Shreve (2005) the link between analytical methods and the martingale approach is considered, the paper Durbin (1971) discusses computational aspects of the problem, while the Taylor expansions of the probability distribution of are considered in Hobson et al. (1999).

The following, inverse to (1), problem was proposed by Albert Shiryaev in the mid-’s in his Banach Center lectures:

| Given a process, , and a distribution, , | (2) | ||

| find a boundary, , such that . |

Problem (2), to the best of our knowledge, was proposed by A. Shiryaev in the case when is a Brownian motion and is an exponential distribution. If is a Brownian motion with a random initial value, i.e., the process is a Brownian motion starting at a random point , we will refer to Problem (2) as a generalized Shiryaev’s problem (GSP).

The third problem considered in this paper is the Skorohod embedding problem:

| Given a probability measure, , with a finite second moment, | (3) | ||

| and a Wiener process, , find an integrable stopping time, , | |||

| such that the distribution of is . |

This problem has a long list of references. Here we mention only the original paper Skorohod (1965) and a survey by Obloj (2004) where many important applications and various solutions of the Skorohod embedding problem can be found.

It is intuitively appealing that there must be a connection between the problems (2) and (3). Indeed if a monotone continuous function solves Problem (2) for a Wiener process , and the distribution function , then the first hitting time, , is a solution of the Skorohod problem with . The only problem with the latter condition is that is usually unknown in analytical form. Moreover, the boundary might not belong to the class of monotone functions.

Models using the first hitting time distribution find extensive application in the areas of portfolio credit risk modeling (see Iscoe and Kreinin (1999), Iscoe et al. (1999), Schmidt and Novikov (2008)) and pricing of credit derivatives (Avellaneda and Zhu (2001), Hull and White (2001)). In these contexts the process represents the so-called distance to default of an obligor (see Avellaneda and Zhu (2001)), while the first hitting time represents a default event. The boundary therefore acts a barrier separating the healthy states of the obligor from the default state. For this reason, the boundary, , is often called the default boundary in the applied literature on credit risk modeling. In particular, an interesting model of default events with a randomized boundary was proposed in Schmidt and Novikov (2008).

The inverse problem (2) was considered in Iscoe et al. (1999) when the process is a Brownian random walk444A Brownian random walk is a discrete time process with Gaussian increments and variance proportional to the time step.. A detailed analysis of the inverse problem in the discrete time setting is given in Iscoe and Kreinin (1999) as well as a Monte Carlo based solution. Their approach is applicable to a much more general class of processes , not just Brownian random walks, and is computationally simple to implement.

Existence of the solution to the continuous-time inverse problem (2) is analyzed in Chadam et al. (2006). In Peskir (2002), an integral equation for the boundary is derived when is a Brownian motion. A general analysis of the integral equations for the boundary and existence and uniqueness theorems are considered in Jaimungal et al. (2009a). The randomized inverse problem is considered in Jaimungal et al. (2009b) and in the preliminary publication Jackson et al. (2009).

The Shiryaev problem is notoriously difficult and analytical solutions are known only in a few cases only (see Shepp (1967), Salminen (1988), Lerche (1986), Peskir and Shiryaev (2006), Breiman (1967), Alili and Patie (2005), Novikov (1981), Peskir (2002)). However, existence of the solution to the problem has been proven for an arbitrary target distribution, , by Dudley and Gutmann (1977) and by Anulova (1980). Unfortunately, an analog of this existence theorem in its most general form cannot be proven for the the Generalized Shiryaev’s problem and in fact counter-examples do exist (see Jaimungal et al. (2009b) and Proposition 2 below). Nonetheless, the randomized version does admit closed form solutions for a large class of distributions of the first hitting time, , including the gamma distribution (see Jackson et al. (2009) and more generally Jaimungal et al. (2009b)) as well as a subset of one-sided stable distributions (see Corollary 1 below).

One of our main goals is to establish a connection between the Generalized Shiryaev’s problem and the Skorohod embedding problem. The remainder of this paper is organized as follows. In Section 2 we proved a new short derivation for the Laplace transform of the distribution of the first hitting time and the distribution of the initial random position of the process . When the boundary is linear, we find solutions for a class of mixtures of gamma distributions of the first hitting time and for a class of stable distributions. In Section 3 we analyze the structure of the solutions to the Shiryaev’s problem and introduce the minimal solution which possess a very elegant structure. The randomization of the initial state of the process allows us to stretch the boundary and transform it into a straight line. In this case we have a simple relation between the distributions of and . This observation allows us to connect the Skorohod embedding problem to the Generalized Shiryaev problem as shown in Section 4.

This paper is self-contained; it represents an extended version of the talk given at the Bachellier colloquium, January 2011, Metabief.

Acknowledgement. We are very grateful to Yuri Kabanov and Tom Sailsbury for pointing out the appealing similarity of the Problems under consideration and asking about the connection between the inverse Problem (2) and the Skorohod embedding problem. We would also like to thank Lane Hughston and Mark Davis for the interesting comments on earlier stages of this work. The authors are indebted to Albert Shiryaev, Alexander Novikov, Raphael Douady, Isaac Sonin and Nizar Touzi for the interesting discussions during the Bachellier colloquium.

2 Randomization of the initial state

2.1 General equation

Let be a filtered probability space and let be the Cartesian product of the space of continuous functions on the positive semi-axis and . Consider a random variable on this probability space. We assume that is an augmented filtration where is the natural filtration, generated by the standard Wiener process and assume that . We also assume that the random variable is independent of the process .

Let and let . Consider now the linear boundary, , . Denote the first hitting time of the process to by , i.e.,

The Generalized Shiryaev’s Problem (GSP) for the process is formulated as follows:

| (4) |

The triplet is called a solution of the Generalized Shiryaev’s Problem.

We are interested in the solutions to the GSP and their properties. In particular, we are interested in the solution of Problem (4) when belongs to the class of Gamma distributions, , with the probability density function

Remark 1.

The case corresponds to the original formulation of Shiryaev’s problem with a randomized initial point. In this case the distribution .

To solve the problem, we will derive a connection between the Laplace transforms of the target distribution and the initial starting point . To this end, denote

| (5) |

where, as usual, , is the set of non-negative real numbers, and let . The function on , is completely monotone (see Feller (1971)), , where

The class of completely monotone functions form an algebra: the sum and the product of completely monotone functions belong to . According to the classical Bernstein’s Theorem (see Feller (1971)), if and , then there exists a cumulative distribution function, , satisfying (5).

The following statement for completely monotone functions is very well known (see Feller (1971), Criterion ):

Proposition 1.

If is a completely monotone function, and the first derivative then .

Let us now derive the main equation for the Laplace transforms of the distributions of and .

Theorem 1.

If a random variable is a solution to the Problem (4) then the function satisfies the equation

| (6) |

Proof.

The process is a martingale with respect to the filtration . Consider the exponential martingale , . It is not difficult to show that if is finite almost surely then the exponential martingale is bounded for all . Therefore, by the optional stopping theorem,

Moreover, the expected value

Furthermore, he have and

Therefore . Finally, we obtain Equation (6).

2.2 Gamma-distributed first hitting time

In the case , the random variable solving Problem (4) admits the following simple probabilistic interpretation.

Theorem 2.

Let , for some . Suppose that . Then satisfies

| (7) |

and the random variable

| (8) |

where and are independent gamma-distributed random variables with a common shape parameter : and , with

| (9) |

Proof.

We have

From (6) we obtain

If the quadratic equation

has real roots and . Then, taking into account that , we find

The additive representation (8) for follows immediately from the latter equation.

Remark 2.

It follows from Theorem 2 that if the GSP has a solution for , given , then it also has a solution for any . We will generalize this property for a larger class of distributions in the next section.

Theorem 2 can also be generalized in the following direction. Consider a class of random variables which are mixtures of gamma-distributed random variables with respect to shape and scale parameters. Write,

where is a mixing measure having a support, , , and . Then

In this case

| (10) |

where and satisfy (9). Therefore, we see that the random variable which leads to the hitting time distribution is in fact a mixture of the sums of independent gamma-distributed random variables.

This generalization is interesting because it is known that the class of finite mixtures of gamma-distributed random variables form a dense set in the space of random variables. Moreover, an arbitrary random variable can be obtained as a weak limit as the number of gamma distributions ,

Unfortunately, this sequence of approximations can not be used to extend the solution (10) through weak convergence because the parameter has a bounded support. In particular, we cannot approximate constant almost surely random variables using the random variables, .

2.3 Stable distribution of the first hitting time

So far, we have considered the case when has finite mean, . However, it is also interesting to analyze the case of one-sided stable distributions with infinite expected value. For this case, we take the slope coefficient . Then, if one takes the random variable such that

then it follows from (6) that

where and . Thus, we obtain

Corollary 1.

If has a stable distribution with the parameter , , then has a stable distribution with the parameter .

3 Structure of the solutions to Shiryaev’s problem

3.1 General results

Theorem 2 describes the solutions to the Shiryaev’s problem when the first hitting time is gamma-distributed. In this case, it can be shown that the condition is necessary and sufficient for existence of the random variable (see Jackson et al. (2009) and Jaimungal et al. (2009b)). Thus if the problem has a solution for the slope then it has a solution for any . The following statement generalizes this result.

Theorem 3.

Given , suppose there exist and such that Equation (6) is satisfied:

Then for any there exists a random variable such that

| (11) |

Proof.

The function satisfies the relation . Therefore, it is enough to prove that . Let . Consider the function

Obviously, , and

The first derivative of is

Let us prove that the function . We have

| (12) |

Then if , we derive from (12) the inequality

| (13) |

Denote derivative of the function by . . Differentiating Equation (12) we find

| (14) |

The latter Equation and (13) imply the inequality

Denote . From Equation (14) we derive

| (15) |

The coefficients satisfy the relations

Taking into account that , we find

| (16) |

The coefficient satisfies the relation

| (17) |

Thus, in Equation (15). Then from (15) we prove by induction that

Therefore . Then we have

Since and we derive from Proposition 1 that , as was to be proved.

The next proposition demonstrates that there exist parameters of the GSP such that the problem does not have a solution.

Proposition 2.

Suppose . Then the Problem (4) does not have a solution if .

Proof.

Indeed, from Equation (6) we find

and

Substituting into these equations, we find

The equations for the first two moments of imply

Finally, we obtain

Proposition 2 is thus proved.

Remark 3.

Remark 4.

If is a constant with probability , Equation (6) does not have a solution. The GSP can not be solved using our randomization approach in this case.

Theorem 3 and Proposition 2 imply that the admissible set for the coefficient is either the semi-infinite interval or an empty set. If has finite first two moments and the random variable exists for some then for each there exists a random variable solving Problem (4). In this manner, we can obtain a family of solutions parameterized by the slope coefficient . Furthermore, the variance of the random variable is a monotone function of and the one with minimal variance is what we call the minimal solution to Problem (4). In particular, if has an exponential distribution with parameter , then the random variable corresponds to the minimal solution has slope . In this case the random variable is Erlang distributed with order two.

3.2 Esscher families

Consider a non-negative random variable and denote its Laplace transform. It is convenient to introduce a family of random variables,

which we call the Esscher family generated by the random variable . As before, let be the first hitting time and be its Laplace transform. Suppose the generalized Shiryaev’s Problem (4) has a solution for some fixed slope . Consider now two Esscher families and generated by and , respectively.

Proposition 3.

For each there exist and such that and and is a solution to the Generalized Shiryaev’s problem.

Proof.

Denote , , and take , . Consider the random variable . Then after simple transformations we find

Thus, the triplet form a solution of the problem.

4 Connection to Skorohod problem.

We are now in a position to construct a solution to the Skorohod problem through the solution to the Generalized Shiryaev’s problem. Suppose that the distribution of the stopped process has a non-negative support, , and the continuous distribution, , can be matched by a corresponding distribution of the random variable for some . Taking into account that for the linear boundary , , we immediately obtain that and the Laplace transform of the density of satisfies

In this case

Similarly, the Skorohod problem can be solved for the distributions with . In this case, the first hitting time is understood as

i.e., the first time the process touches the boundary from below. Clearly, the initial point must then have support on the negative real axis.

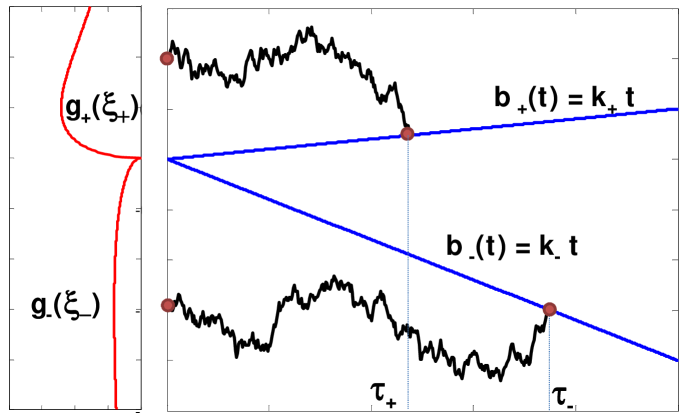

The solution to the general Skorohod problem – without restrictions on the support of the distribution of – can then be obtained as follows: Let us represent the random variable as a mixture of the random variables and :

Suppose that the Skorohod problem for the random variables and can be solved by the boundaries and and the random variables and , respectively (see Figure 1). Then we have the following

Proposition 4.

The random variable

and the boundary solve the Skorohod problem for the random variable .

Remark 5.

In this manner, the Skorohod problem is solved by randomizing the starting point of the Brownian motion over the entire real line, and searching for the first hitting time when the process enters the wedge region described by the lines and .

5 Conclusion

We have demonstrated that randomization of the initial state of the process is a very powerful tool for solving and tying together the Generalized Shiryaev’s Problem and the Skorohod Embedding Problem. The randomization of the initial state of the process allows us to reduce the problem to the linear boundary case and obtain closed-form solutions for several important classes of the distribution of the first hitting time.

This linearization of the boundary makes the relation between the Shiryaev’s and Skorohod problems transparent. Furthermore, it allows us to develop a new solution to the Skorohod problem.

We close this paper with a brief discussion of the directions for future research. In the present paper we discussed the case of a scalar process whose distribution of the first hitting time must be matched. One interesting open question is to prove existence of the solution to the Generalized Shirayaev’s problem when has a continuous infinitely divisible distribution. Another interesting generalization that requires much attention is the Generalized Shirayaev’s problem for a vector-valued process . Such generalization will prove extremely useful in application settings as well as providing an interesting mathematical playground.

References

- Alili and Patie (2005) Alili, L., Patie, P., 2005. On the first crossing times of a Brownian motion and a family of continuous curves. C.R. Acad. Sci. Paris Ser.I340, 225–228.

- Anulova (1980) Anulova, S., 1980. On markov stopping times with a given distribution for a Wiener process. Theory Probab. Applications 5, 362–366.

- Avellaneda and Zhu (2001) Avellaneda, M., Zhu, J., 2001. Distance to default. Risk 14(12), 125–129.

- Breiman (1967) Breiman, L., 1967. First exit times from a square root boundary. In Fifth Berkeley Symposium 2(2), 9–16.

- Chadam et al. (2006) Chadam, J., Cheng, L., Chen, X., Saunders, D., 2006. Analysis of an inverse first passage problem from risk management. SIAM Journal on Mathematical Analysis 38(3), 845–873.

- Dudley and Gutmann (1977) Dudley, R., Gutmann, S., 1977. Stopping times with given laws. Sem. de Probab.XI, Lecture Notes in Math. 11, 51–58.

- Durbin (1971) Durbin, J., 1971. Boundary-crossing probabilities for the brownian motion and Poisson processes and techniques for computing the power of the Kolmogorov-Smirnov test. Journal of Applied Probability 8(3), 431–453.

- Feller (1971) Feller, W., 1971. An introduction to probability theory and its applications, vol.II. John Wiley & Sons New York.

- Hobson et al. (1999) Hobson, D. G., Williams, D., Wood, A., 1999. Taylor expansions of curve-crossing probabilities. Bernoulli 5(5), 779–795.

- Hull and White (2001) Hull, J., White, A., 2001. Valuing credit default swaps II: modeling default correlations. Journal of Derivatives 8(3), 29–40.

- Iscoe and Kreinin (1999) Iscoe, I., Kreinin, A., 1999. Default boundary problem. Technical report Algorithmics Inc.

- Iscoe et al. (1999) Iscoe, I., Kreinin, A., Rosen, D., 1999. Integrated market and credit risk portfolio model. Algorithmics Research Quarterly 2(3), 21–38.

- Jackson et al. (2009) Jackson, K., Kreinin, A., Zhang, W., 2009. Randomization in the first hitting time problem. Statistics and Probability Letters.

- Jaimungal et al. (2009a) Jaimungal, S., Kreinin, A., Valov, A., 2009a. Integral equations and the first passage time of Brownian motions. arXiv:0902.2569.

- Jaimungal et al. (2009b) Jaimungal, S., Kreinin, A., Valov, A., 2009b. Randomized first passage times. arXiv:0911.4165v1.

- Karatzas and Shreve (2005) Karatzas, I., Shreve, S. E., 2005. Brownian motion and stochastic calculus. Springer-Verlag New York.

- Khintchine (1933) Khintchine, A. Y., 1933. Asymptotische gesetze der wahrscheinlichkeits rechnuung. Springer Berlin.

- Lerche (1986) Lerche, H., 1986. Boundary crossing of Brownian motion. Lecture Notes in Stat. 40, Springer–Berlin.

- Novikov (1981) Novikov, A., 1981. Martingale approach to first passage problems for nonlinear boundaries. Proceedings of the Steklov Inst. of Math. 158, –.

- Obloj (2004) Obloj, J., 2004. The Skorokhod problem and its offspring. Preprint 886, Laboratoire de Probabilites et Modeles Aleatoires Univer. Paris VI & VII.

- Peskir (2002) Peskir, G., 2002. On integral equations arising in the first-passage problem for Brownian motion. Journal Integral Equations. Appl. 14(4), 397–423.

- Peskir and Shiryaev (2006) Peskir, G., Shiryaev, A., 2006. Optimal stopping and free-boundary problems. Lectures in Mathematics. Birkhauser, –.

- Salminen (1988) Salminen, P., 1988. On the first hitting time and the last exit time for a Brownian motion to/from a moving boundary. Adv. Appl. Probab. 20(2), 411–426.

- Schmidt and Novikov (2008) Schmidt, T., Novikov, A., 2008. A structural model with unobserved boundary. Applied Mathematical Finance 15(2), 183–203.

- Shepp (1967) Shepp, L., 1967. A first passage problem for the Wiener process. Ann. Math. Stat. 38(6), 1912–1914.

- Skorohod (1965) Skorohod, A., 1965. Studies in the theory of random processes. Translated from the Russian by Scripta Technica, Inc. Addison-Wesley Publishing Co., Inc., Reading, Mass.