An Application of Renewal Theorems to Exponential Moments of Local Times

Abstract.

In this note we explain two transitions known for moment generating functions of local times by means of properties of the renewal measure of a related renewal equation. The arguments simplify and strengthen results on the asymptotic behavior in the literature.

Key words and phrases:

Renewal Theorem, Local Times2000 Mathematics Subject Classification:

Primary 60J27; Secondary 60J551. Introduction and Results

Suppose is a time-homogeneous continuous time Markov process on a countable set with transition probabilities for . We fix some arbitrary and denote by the time spends at until time :

A quantity that has been studied in different contexts is the moment generating function , where and is a positive real number.

To explain our interest in let us have a brief look at the parabolic Anderson model with Brownian potential, i.e.

| (1.1) |

with homogeneous initial conditions . Here, , denotes the discrete Laplacian , and is a family of independent Brownian motions. It is known (see for instance Theorem II.3.2 of [CM94]) that the moments of solve discrete-space heat equations with one-point potentials. In particular, solves

| (1.2) |

with homogeneous initial conditions. The discrete Laplacian acts on both spatial variables and seperately. Applying the Feynman-Kac formula one reveals that

where are independent simple random walks. Hence, for corresponding to the difference walk (or equivalently corresponding to a simple random walk with doubled jump rate)

The notion of weak -intermittency, i.e. exponential growth of the second moment , now explains the interest in the study of the exponential moment of for continuous time Markov processes.

Applying the variation of constant formula to solutions of (1.2) one can guess that the following renewal equation holds for fixed and :

| (1.3) |

Indeed, expanding the exponential one can show directly the validity of Equation (1.3) for general time-homogeneous Markov processes on countable state spaces (see Lemma 3.2 of [AD09]). The same equation holds for with replaced by . As the analysis does not change we restrict ourselves to .

In Section III of [CM94] and as well in Lemma 1.3 and Theorem 1.4 of [GdH06] analytic techniques were applied to understand the longtime behavior of solutions of (1.2) by means of spectral properties of the discrete Laplacian with one-point potential. They showed that the exponential growth rate

exists and obeys the following transition in :

where is the Green function . This first transition in can be proved analytically, as identifying corresponds to identifying the smallest eigenvalue of the perturbed operator . As multiplication with is a one-dimensional perturbation and for the discrete Laplacian explicit formulas for eigenfunctions are available, all necessary quantities can be calculated. In particular the exponential growth rate , in the general case of our Theorem 1 represented by the Laplace transform of the transition probabilities, has been described for the simple random walk as the unique solution of

where denotes the -dimensional torus and . Compared to this expression, our Laplace transform representation is particularly useful (and easy to prove) as it immediately provides the qualitative behavior of as a function of .

Replacing the discrete Laplacian by a generator of a finite range random walk, in [DD06] the second moment of solutions of (1.1) were analyzed via a random walk representation. For more general initial conditions this leads to a renewal equation similar to (1.3). The authors analyzed their equation (3.16) directly without appealing to the renewal theorem. In precisely the same manner as we do in the proof of our Theorem 1 one can proceed in their case and strengthen the asymptotics of their Equation (3.15).

Assuming only that for some (by we denote strong asymptotic equivalence at infinity) a second transition was revealed in Proposition 3.12 of [AD09] by a Laplace transform technique combined with Tauberian theorems: at the critical point the growth is of linear order if and only if . As for the simple random walk on the local central limit theorem implies , linear growth occurs for dimensions at least .

The main goal of the following is to show how the known results easily follow from different renewal theorems utilizing the fact that Equation (1.3) is a renewal equation of the type

| (1.4) |

with , initial condition , and renewal measure . This approach is robust as there is no need to assume any properties of the underlying Markov process (neither symmetry to obtain a self-adjoint operator, nor polynomial decay for Tauberian theorems or finite range transitions kernels for the random walk representation).

The two transitions will now appear in terms of whether or not the renewal measure

-

•

is a probability measure,

-

•

has finite mean.

In the supercritical case without any further consideration we obtain the strong asymptotics of . This of course is stronger than considering the Lyapunov exponent that appears in [CM94], [GdH06], and [AD09] as we exclude the possible existence of a subexponential factor. With further considerations this can be proved analytically but comes here for free from the renewal theorem.

For the statement of the theorem we denote by the expected time of hitting of two independent copies of . In contrast to the Green function here we count the hitting time of the entire paths not only of the paths at same time. The Laplace transform in time of is denoted by , , and weak asymptotic equivalence at infinity by (i.e. there are constants such that ).

Theorem 1.

Suppose is a time-homogeneous Markov process on started in . Then for the following holds:

-

(1)

If , then and

-

(2)

If , then

where the weak asymptotic bounds are and . If moreover

then

-

(3)

If , then

Remark 1.

In the general case, we only obtained weak convergence at criticality in the previous theorem with asymptotic bounds and . Under the stronger assumptions , in Proposition 3.12 of [AD09] strong asymptotics were obtained by Tauberian theorems. The case of is contained in the second part, is contained in the first part of our previous theorem and also strong asymptotics for can be obtained by extended renewal theorems. Here, we can directly use the infinite mean renewal Theorem 1 of [AA87] to obtain precisely the same strong asymptotics as of Proposition 3.12 of [AD09].

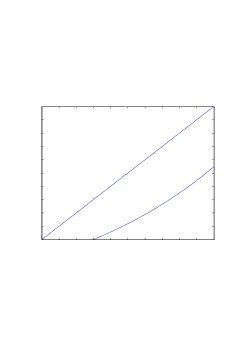

Qualitative properties of the exponential growth rate have been considered for the simple random walk (see Section III of [CM94], Theorem 1.4 of [GdH06]) and in the polynomially case (see Corollary 3.10 of [AD09]). The representation of the growth rate in the previous theorem directly shows that the qualitative behavior (see Figure 1 for the qualitative behavior of plotted against the identity function) is valid for general Markov processes:

Corollary 1.

Suppose is a time-homogeneous Markov process on started in . Then for the following holds for :

-

(1)

and if and only if ,

-

(2)

the function is strictly convex for ,

-

(3)

for all , and , as .

2. Proofs

Proof of Theorem 1.

The proof of Theorem 1 is based on the renewal equation (1.4) setting , , and .

1. The assumptions of the theorem directly imply that in this case is not a probability measure. Either the measure is infinite (with density bounded by ) or it is finite with total mass strictly larger than .

From the definition of the Laplace transform we obtain for that

is a probability measure. As by assumption , we obtain that is directly Riemann integrable and has finite mean . Hence,

is a proper renewal equation. The classical renewal theorem (see for instance page 363 of [F71]) implies that

proving the claim.

2. In the critical case , the measure as defined above indeed is a probability measure which does not necessarily has finite mean. Furthermore, the situation is different from the first case as now the initial condition is not directly Riemann integrable. Iterating Equation (1.3) we obtain the representation

where denotes -fold convolutions. Note that convergence of the series is justified by boundedness of . In the case of finite mean, Equation (1.2) of page 358 of [F71] and the renewal theorem on page 360 now directly imply

For renewal measure with infinite mean we again use the convolution representation of to apply Lemma 1 of [E73] showing that the denominator needs to be replaced by the truncated mean .

3. For we may directly use the proof of Proposition 3.11 of [AD09] as there no additional structure was assumed. We repeat the simple argument for completeness. Taking Laplace transform of Equation (1.3) and solving the multiplication equation in Laplace domain (note that under Laplace transform the convolution turns into multiplication) we obtain with

for . As by assumption the second factor converges to the constant as tends to zero, Karamata’s Tauberian theorem (see Theorem 1.7.6 of [BGT89]) implies the result. Note that as is increasing, the Tauberian condition for that theorem is fulfilled. ∎

Proof of Corollary 1.

Part 1. of Theorem 1 shows that understanding suffices to understand . This is not difficult due to the following observation: as is bounded by , is finite for all , strictly decreasing and convex with . Hence, if and only if . This implies that precisely for . Hence, parts 1. and 2. are proved as .

First note that the first part of 3. is immediate as . Continuity of and imply that for there is such that for . Hence,

Since for we obtain

This combined with the first part of 3. proves the second part. ∎

3. Related Work

After submission of this paper the authors learned about an unpublished manuscript of Philippe Carmona. In this note a large deviation principle for was established taking into account the renewal theorem.

There are two more papers which we would like to mention for continuous space analogue questions. In their analysis of laws of the iterated logarithms for local times of symmetric Lévy processes, moment generating functions of local times were considered in [MR96]. They exploited the renewal equation (1.3) where now the transition probabilities need to be replaced by transition kernels. Solving in Laplace domain as we did in part 3. of the proof of Theorem 1 they transformed back via inverse Laplace transformation to estimate rather delicately the difference

Their estimate is uniform in and but does not establish convergence as tends to infinity. Applying our proofs to the renewal equation representation (see the proof of their Lemma 2.6), one obtains the same results for local times of Lévy processes as we obtained in discrete space.

Recently, a parabolic Anderson model in with Lévy driver was consider in [FK1] and [FK2]. As their results are based on the same renewal equation (see for instance Equation (2.2) of [FK2] or (4.15) of [FK1]) that we used, one can strengthen their bounds away from the notion of Lyapunov exponents to strong asymptotics with the same expressions for constants and exponential rates as in our discrete setting. This is not surprising as also for their Lévy process driven version of the parabolic Anderson model the afore mentioned correspondence of second moments and exponential moments of local times of the corresponding Lévy process holds true.

References

- [AA87] K.K. Anderson, K.B. Athreya. A Renewal Theorem in the Infinite Mean Case Annals of Probability 15 (1987), 388-393

- [BGT89] N.H. Bingham, C.M. Goldie, J.L. Teugels. Regular variation Encyclopedia of Mathematics and its Applications 27 (1989), xx+494

- [AD09] F. Aurzada, L. Döring. Intermittency and Aging for the Symbiotic Branching Model to appear in Ann. Inst. H. Poincaré Probab. Statist. (2010)

- [CM94] R. Carmona, S. Molchanov. Parabolic Anderson problem and intermittency Mem. Amer. Math. Soc. 108 (1994), viii+125

- [DD06] A. Dembo, J.D. Deuschel. Aging for Interacting Diffusion Processes Ann. Inst. H. Poincaré Probab. Statist. 43(4) (2007), 461-480

- [E73] B. Erickson. The strong law of large numbers when the mean is undefined Trans. Amer. Math. Soc. 54 (1973), 371-381

- [F71] W. Feller. An introduction to probability theory and its applications. Vol. II. John Wiley & Sons, Inc., New York-London-Sydney (1971), xxiv+669 pp.

- [FK1] M. Foondun, D. Khoshnevisan. Intermittency for nonlinear parabolic stochastic partial differential equations Electr. Journal of Prob. 14 (2009), 548-568

- [FK2] M. Foondun, D. Khoshnevisan. On the global maximum of the solution to a stochastic heat equation with compact-support initial data, Preprint

- [GdH06] J. Gärtner, F. den Hollander. Intermittency in a catalytic random medium Annals of Probability 34(6) (2006), 2219-2287.

- [MR96] M. Marcus, J. Rosen. Laws of the iterated logarithm for the local times of symmetric Lévy processes and recurrent random walks Annals of Probability 22 (1994), 620-659