Statistical inference across time scales

Abstract

We investigate statistical inference across time scales. We take as toy model the estimation of the intensity of a discretely observed compound Poisson process with symmetric Bernoulli jumps. We have data at times for over , for different sizes of relative to in the limit . We quantify the smooth statistical transition from a microscopic Poissonian regime ( to a macroscopic Gaussian regime (). The classical quadratic variation estimator is efficient in both microscopic and macroscopic scales but surprisingly shows a substantial loss of information in the intermediate scale that can be explicitly related to . We discuss the implications of these findings beyond this idealised framework.

Keywords: Discretely observed random process, LAN property, Information loss.

Mathematical Subject Classification: 62B15, 62B10, 62M99 .

1 Introduction

1.1 Motivation

We specialise in this paper on the example of a discretely observed compound Poisson process with symmetric Bernoulli jumps. This toy model is central to several application fields, e.g. financial econometrics or traffic networks (see the discussion in Section 3 and the references therein). Moreover, it already contains several interesting properties that enlight a tentative concept of statistical inference across scales. Consider a -dimensional random process defined by

| (1.1) |

where the are independent, identically distributed with

and independent of the standard homogeneous Poisson process with intensity . Suppose we have discrete data over at times . This means that we observe

| (1.2) |

and we obtain a statistical experiment by taking as the law of defined by (1.2) when is governed by (1.1).

On the one hand, if we observe microscopically, that is if as , then asymptotically, we can – essentially – locate the jumps of that convey all the relevant information about the parameter .

In that case, is “close” to the continuous path . On the other hand, if we observe macroscopically, that is if under the constraint333This condition ensures that asymptotically infinitely many observations are recorded in the limit . , we have a completely different picture: the diffusive approximation

| (1.3) |

becomes valid, where is a standard Wiener process. Inference on essentially transfers into a Gaussian variance estimation problem; in that case, the state space rather becomes . Finally if we observe in the intermediate scale , we observe a process presenting too many jumps to be located accurately from the data, and too few to verify the Gaussian approximation (1.3). Therefore, depending on the scale parameter , the state space may vary, and it has an impact on the underlying random scenarios , although the interpretation of the parameter of interest remains the same at all scales. What we have is rather a family of experiments

| (1.4) |

where denotes the law of given by (1.2) and these experiments may exhibit different behaviours at different scales . Heuristically, we would like to state that in the microscopic scale , the measure conveys the same information about as the law of

| (1.5) |

that is if the jump times of were observed. On the other side, in the macroscopic scale with , the measure shall convey the same information about as the law of

| (1.6) |

that is if the data were drawn as a Brownian diffusion with variance . The following questions naturally arise:

-

i)

How does the model formulated in (1.4) interpolate – from a statistical inference perspective – from microscopic (when ) to macroscopic scales (when )? In particular, how do intrinsic statistical information indices (such as the Fisher information) evolve as varies?

-

ii)

Is there any nontrivial phenomenon that occurs in the intermediate regime

-

iii)

Given i) and ii), if a statistical procedure is optimal on a given scale , how does it perform on another scale? Is it possible to construct a single procedure that automatically adapts to each scale , in the sense that it is efficient simultaneously over different time scales?

1.2 Main results

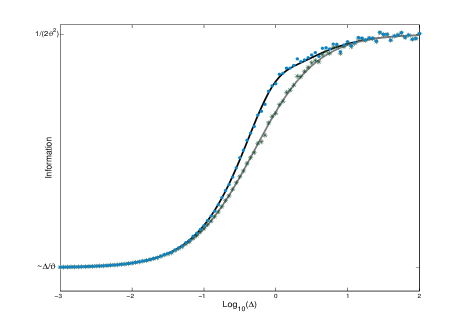

In this paper, we systematically explore questions i), ii) and iii) in the simplified context of the experiments built upon the continuous time random walks model (1.1) for transparency. Some extensions to non-homogeneous compound Poisson processes are given, and the generalisation to a more general compound law is also discussed. As for i), we prove in Theorems 2.2, 2.4 and 2.5 that the LAN condition (Locally Asymptotic Normality444Recommended references are the textbooks [8] and [14], but we recall some definitions in Section 2.2 for sake of completeness.) holds for all scales . This means that can be approximated – in appropriate sense – by the law of a Gaussian shift. We derive in particular the Fisher information of and observe that it smoothly depends on the scale . We shall see that the answer to ii) is positive. More precisely, we first prove in Theorem 2.6 that the normalised quadratic variation estimator

is asymptotically efficient – it is asymptotically normal and its asymptotic variance is equivalent to the inverse of the Fisher information – in both microscopic and macroscopic regimes. In the microscopic regime, it stems from the fact that the approximation

becomes valid, as the jumps are , and the efficiency is then a consequence of being the maximum likelihood estimator in the approximation experiment (1.5). In the macroscopic regime, thanks to the diffusive approximation (1.3) we have

which is precisely the maximum likelihood estimator in the macroscopic approximation experiment (1.6). Surprisingly, fails to be efficient when

| (1.7) |

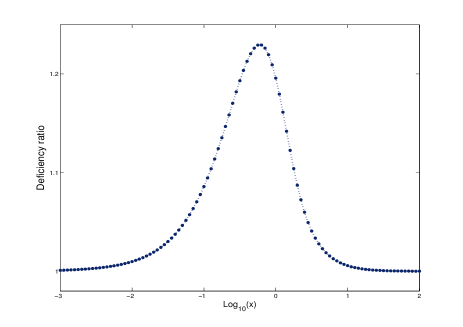

More precisely, we show in Theorem 2.7 that, although rate optimal, misses the optimal variance by a non-negligible factor, depending on , that can reach up to . This phenomenon is due to the fact that in the intermediate regime (1.7), the process is sampled at a rate which has the same order as the intensity of its jumps. On the one hand, gives no accurate information whereas a jump has occured or not during the period , contrary to the case . On the other hand, there are not enough jumps to validate the approximation of by a Gaussian random variable, contrary to the case . Finally, we construct in Theorem 2.9 a one-step correction of that provides an estimator efficient in all scales, giving a positive answer to iii).

The paper is organised as follows. We first propose in Section 2.1 a canonical framework for different time scales by considering the family of experiments . The way the scale parameter depends on defines the terms microscopic, intermediate and macroscopic scales rigorously. Specialising to model (1.1) for transparency, the results about the structure of the corresponding are stated in Section 2.2. We show in Theorems 2.2, 2.4 and 2.5 that the LAN (Local Asymptotic Normality) property holds simultaneously over all scales and provides an explicit expression for the Fisher information. The proof follows the classical route of [8] and boils down to obtaining accurate approximations of the distribution

in the limit or . Note that does not depend on since has stationary increments. However explicit, the intricate form of requires asymptotic expansions of modified Bessel functions of the first kind. In the macroscopic regime however, we were not able to obtain such expansions. We take another route instead, proving directly the asymptotic equivalence in the Le Cam sense, a stronger result at the expense of requiring a rate of convergence of to , presumably superfluous. We show in Theorems 2.6 and 2.7 of Section 2.3 that the quadratic variation estimator is rate optimal and efficient in both microscopic and macroscopic regimes, but not in the intermediate scales (1.7). This negative result is however appended with the construction of an adaptive estimator, constructed by a standard one-step correction of based on the likelihood at intermediate scales, and efficient over all scales (Theorem 2.9). Moreover this estimator has the advantage of being computationally implementable, contrary to the theoretical optimal maximum likelihood estimator. Section 3 gives some extensions in the case of a non-homogeneous compound Poisson process (Theorem 3.2) and addresses the generalisation to more general compound laws. The comparison to related works on estimating Lévy processes from discrete data is also discussed. Section 4 is devoted to the proofs.

2 Statement of the results

2.1 Building up statistical experiments across time scales

Let and be such that . On a rich enough probability space , we observe the process defined in (1.1) at frequency over the period . Thus we observe defined in (1.2), and with no loss of generality555By assuming , the first data point does not give information about the parameter . If only asymptotic properties of the statistical model are studied, which is always the case here, it has no effect., we take . We obtain a family of statistical experiments

where denotes the law of when has the form (1.1), and is a parameter set with non empty interior. The experiment is dominated by the counting measure on . Abusing notation slightly, we may666By taking for instance . (and will) identify with the canonical observation in . Since has stationary and independent increments under , we obtain the following expression for the likelihood

where we have set, for ,

| (2.1) |

We shall repeatedly use the terms microscopic, intermediate and macroscopic scale (or regime). In order to define these terms precisely, we let depend on with , and we adopt the following terminology.

Definition 2.1.

The sub-family of experiments is said to be

-

1.

On a microscopic scale (or regime) if as .

-

2.

On an intermediate scale (or regime) if as , for some .

-

3.

On a macroscopic scale (or regime) if and as .

2.2 The regularity of across time scales

Let us recall777See for instance the textbooks [8] or [14]. that the family of experiments satisfies the Local Asymptotic Normality (LAN) property at point with normalisation if, for every such that , the following decomposition holds

| (2.2) |

where

| (2.3) |

and

| (2.4) |

If (2.2), (2.3) and (2.4) hold, we informally say that is regular with information . This means that locally around , the law of can be approximated by the law of a Gaussian shift experiment, where one observes a single random variable

with being approximately distributed as a standard Gaussian random variable under as . In particular, the optimal rate of convergence for recovering from is the same as the one obtained from . It is given by provided as . Note also that if the convergence of the remainder term in (2.4) holds locally uniformly in , then can be replaced by any function such that

without affecting the LAN property. Hereafter, the symbol means asymptotic equivalence up to constants. Our first result states the LAN property for the experiment on every scale .

Theorem 2.2 (The intermediate regime).

Assume as . Then the family is regular and we have

with

where, for and ,

denotes the modified Bessel function of the first kind.

Remark 2.3.

By taking constant, we include the case of a fixed , therefore the same regularity result holds for . An inspection of the proof of Theorem 2.2 reveals that the mapping is continuous over .

Our next result shows that formally we can let in the expression of given by Theorem 2.2 in the microscopic case. Moreover we obtain a simplified expression for the information rate.

Theorem 2.4 (The microscopic case).

Assume as Then the family is regular and we have

The macroscopic case is a bit more involved. In that case, we cannot formally let in the expression of given by Theorem 2.2. However we have the following simplification.

Theorem 2.5 (The macroscopic case).

Assume , as and . Then the family is regular and we have

The condition is technical but quite stringent; it stems from our method of proof, see Section 4.3. It is presumably superfluous, but we do not know how to relax it.

2.3 The distortion of information across time scales

On each scale , let us introduce the empirical quadratic variation estimator

that mimics the behaviour of the maximum likelihood estimator in both macroscopic and microscopic regimes (see Section 1). More precisely, we have the following asymptotic normality result.

Theorem 2.6.

On a microscopic scale , we have

On a macroscopic scale with , we have on the contrary

As a consequence, we readily see that is asymptotically normal and that its asymptotic variance is equivalent to on a microscopic scale and to on a macroscopic scale. At a heuristical level, this phenomenon can be explained directly by the form of the empirical quadratic variation estimator, as we already did in Section 1. At intermediate scales however, this is no longer true.

Theorem 2.7 (Loss of efficiency in the intermediate regime).

Remark 2.8.

Let us denote by

the squared error loss of the quadratic variation estimator. By Theorems 2.2, 2.4 and 2.5, the family is regular in all regimes and we may apply the classical minimax lower bound of Hajek, see for instance Theorem 12.1 in [8]: we have, for any and such that

| (2.6) |

On the one hand, Theorem 2.6 suggests888This is actually true as the uniform integrability of under , locally uniformly in , can easily be obtained. We leave the details to the reader. that the lower bound (2.6) can be achieved in microscopic and macroscopic regimes. On the other hand, Theorem 2.7 shows that inequality (2.6) is strict in the intermediate case, whenever the restriction (2.5) is satisfied, thus revealing a loss of efficiency in this sense. Define

where is defined in Theorem 2.2. An inspection of the proof of Theorem 2.7 shows that , for some univariate function , and that

The maximal loss of information is obtained for

as . Numerical simulations show that the maximum loss of efficiency is close to .

Since is regular for every , an asymptotically normal estimator with asymptotic variance equivalent to is given by the maximum likelihood estimator. However due to the absence of a closed-form for the likelihood ratio that involves the intricate function defined in (2.1) (see also Section 4.1.1), it seems easier to start from which is already rate-optimal by Theorem 2.6 and correct it by a classical one-step iteration based on the Newton-Rhapson method, see for instance the textbook [14] pp. 71–75. To that end, define

| (2.7) |

Theorem 2.9.

In all three regimes (microscopic, intermediate and macroscopic), we have

Proof.

In essence the regularity of enables to apply Theorem 5.45 of Van der Vaart [14]. ∎

Theorem 2.9 expresses the fact that automatically adapts to and is therefore optimal across scales.

3 Discussion

The compound Poisson process with Bernoulli symmetric jumps defined in (1.1) is the simplest model of a continuous time symmetric random walk on a lattice that diffuses to a Brownian motion on a macroscopic scale. The intensity of the Poisson arrivals on a microscopic scale is transferred into the variance of the Brownian motion on a macroscopic scale:

| (3.1) |

in distribution as , where is a standard Brownian motion. The statistical inference program we have developed across time scales on the toy model given by can be useful in several applied fields. For instance, in financial econometrics, may be viewed as a toy model for a price process (last traded price, mid-price or bets bid/ask price) observed at the level of the order book, see e.g. [2] or [9]. The parameter can be interpreted as a trading intensity on microscopic scales that transfers into a macroscopic volatility in the diffusion regimes. Our results convey the message that if a practitioner samples at high frequency at the same rate as price changes, which is customary in practice, then the realised volatility estimator is not efficient, and a modified estimator like should be used instead. However, this framework is a bit too simple and needs to be generalised in order to be more realistic in practice. Two directions can be explored in a relatively straightforward manner:

-

i)

The extension to a non-homogeneous intensity Poisson process.

-

ii)

The extension to an arbitrary compound law on a discrete lattice.

Extension to the non-homogeneous case

Theorems 2.2, 2.4 and 2.5 extend to the non-homogeneous case, when one allows the intensity of the jumps to depend on time. In this setting, the counting process defined in (1.1) is defined on and has intensity

where

is the nonvanishing (integrable) intensity function, so that the process

is a martingale. The homogenous case is recovered by setting for every . In this context, the macroscopic approximation (3.1) becomes

in distribution as . We state – without proof – an extension of Theorems 2.2, 2.4 and 2.5 for the associated family of experiments across scales.

Assumption 3.1.

We have that is continuously differentiable for almost all and moreover .

Theorem 3.2.

The proof of Theorem 3.2 relies on the approximation

for , where as in all three regimes. Assumption 3.1 ensures that the convergence of the remainder is uniform in and . This reduction enables us to transfer the problem of proving Theorems 2.2, 2.4 and 2.5 when substituting independent identically distributed random variables by independent non-equally distributed ones. This is not essentially more difficult, and the regularity of enables us to piece together the local information given by each increment in order to obtain the formulae of Theorem 3.2.

An analogous program as in Section 2.3 for the distortion of information could presumably be carried over, with appropriate modifications. For instance, one can show that

in -probability, in all three regimes. Then, in order to estimate efficiently, one should rather consider a contrast estimator that maximises

for a suitable function , and make further assumptions on existence of a unique maximum for the limit – whenever it exists – of under as . We do not pursue this here.

Extension to more general compound laws

The situation is a bit more delicate when one tries to generalise Theorems 2.2, 2.4 and 2.5 to an arbitrary compound law , for every , with

(and for obvious identifiability conditions). We then observe a process of the form (1.1), except that the jumps are now distributed according to

In order to keep up with the preceding case, we normalise the compound law, imposing

| (3.2) |

First, in the microscopic case, we approximately observe over the period a random number of jumps, namely which is of order . Second, conditionally on , the size of the jumps form a sequence of independent and identically distributed random variables with law . On the other side, in the macroscopic limit, the effect of the size of the jumps is only tracked through their second moment, which is normalised to by (3.2). Therefore it gives no additional information about . The situation is rather different from the case of symmetric Bernoulli jumps: here, the extraneous information about lies in the effect of the jumps, which are recovered in the microscopic regime and lost in the macroscopic one. There is however one way to reconcile with our initial setting, assuming that the compound law does not depend on and is known for simplicity. Then, for , we have

where is the probability that a random walk with law started at reaches in steps exactly. Therefore

| (3.3) |

In the symmetric Bernoulli case, we have , where is the modified Bessel function of the first kind. Anticipating the proof of Theorems 2.2, 2.4 and 2.5, analogous results could presumably be obtained for an arbitrary compound law satisfying (3.2), provided accurate asymptotic expansions of are available in the viscinity of and . The same subsequent results about the distortion of information that are developed in Section 2.3 would presumably follow, with the same estimators and , and the appropriate changes for in (2.7).

Relation to other works

Concerning the estimation of the law of the jumps, say , we have an inverse problem. One tries to recover from the observations of a compound Poisson process, the link between and the law of the process being given by (3.3). In the setting of positive compound laws, Buchmann and Grübel [4, 5] succeed to invert that relation and give an estimator of in the discrete and continuous case. That method which consists in inverting (3.3) is called decompounding. It was generalised by Bogsted and Pitts [3] to renewal reward processes when the law of the holding times is known, inrestriction to the case of having positive jumps only.

The compound Poisson process is a pure jump Lévy process that can be studied accordingly. Using the Lévy-Khintchine formula, it is possible to estimate nonparametrically its Lévy measure which is given by the product in that case. This strategy is exploited by van Es et al. [15] for a known intensity. This estimation procedure does not restrict to compound Poisson processes and it includes the case of pure jump Lévy processes in general. Nonparametric estimation of the Lévy measure from high frequency data (that corresponds to our microscopic case is thoroughly studied in Comte and Genon-Catalot [6] as well as in the intermediate regime (with fixed) in [7]. In that latter case, we also have the results of Neumann and Reiß [12].

4 Proofs

4.1 Preparation

4.1.1 Some estimates for

We have, for :

where is the probability that a symmetric random walk in started from has value after steps exactly:

Let us introduce the modified Bessel function of the first kind999The function can also be defined as the solution to the differential equation

for every , and where

denotes the Gamma function. Straightforward computations show that

| (4.1) |

See for instance [13], p. 21 Example 4.7. We gather some technically useful properties of the function that we will repeatedly use in the sequel.

Lemma 4.1.

-

1.

For every and , we have

(4.2) -

2.

For every and , we have

(4.3)

4.1.2 The Fisher information of

For , let denote the experiment generated by the observation of the incerement . Since has independent stationary increments, we have, for

Using that , it follows that

| (4.4) |

as a product of independent observations given by the increments , each experiment being dominated by the counting measure on with density given by (4.1) that does not depend on . Moreover, has (possibly infinite) Fisher information given by

which does not depend on . We study the regularity of in the classical sense of Ibragimov and Hasminskii (see [8] p. 65).

Definition 4.2.

The experiment is regular (in the sense of Ibragimov and Hasminskii) if

-

The mapping is continuous on for every .

-

The Fisher information is finite: for every .

-

The mapping is continuous in .

Lemma 4.3.

The experiments are regular.

Proof.

For every , , therefore i) is readily satisfied since and . We also have for every , then is well defined, but possibly infinite. In order to prove ii), we write

| (4.5) |

where we have set, for every ,

and used Property (4.2). It follows that

| (4.6) |

Moreover the function is decreasing (see (4.3)), thus

| (4.7) |

and since has all moments under , we obtain ii). We proceed similarly for iii). First, for any and such that , we have

for some . Second, we write

and, differentiating a second time, we obtain that equals

Therefore, taking square and summing in , we derive

| (4.8) |

From ii), we have

| (4.9) |

and this last quantity has moments of all orders under , locally uniformly in . Likewise, using (4.9) and (4.2), it is easily seen that

Thus has moments of all orders under locally uniformly in , thanks to (4.3) and (4.7). The same property carries over to the term within the expectation in (4.8) and we thus obtain iii) by letting . ∎

By the factorisation (4.4), we infer that has Fisher information

which is finite thanks to ii) of Lemma 4.3.

Lemma 4.4.

For every , we have

| (4.10) |

Moreover in the microscopic and intermediate regimes, we have

| (4.11) |

of Lemma 4.11.

In the course of the proof of Lemma 4.3, we have seen by (4.6) that

It follows that

Since is regular by Lemma 4.3, we have . Combining this with the equality

that we obtained in (4.5), we derive

and (4.10) follows. Expanding (4.10) further, we obtain the useful representation

| (4.12) |

Let us now assume that . We will need the following asymptotic expansion of the function near .

Lemma 4.5.

We have, for ,

| (4.13) |

where is continuous and satisfies when .

Proof of Lemma 4.5.

We have an expression of as a power series, thus its Taylor expansion in a neighborhood of is given by

where

Then is continuous and satisfies when . ∎

By Lemma 4.5, a simple Taylor expansion shows that

where , for some deterministic locally bounded . Plugging this last expression in (4.12), we obtain

with having the same property as , whence (4.11) in the microscopic case. In the intermediate case, since is continuous on , we readily obtain the result using that is equivalent to as . The proof of Lemma 4.4 is complete. ∎

4.2 Proof of Theorems 2.2 and 2.4

A technically convenient consequence of Lemma 4.4 in the microscopic and macroscopic cases is that it suffices to prove Theorems 2.2 and 2.4 with instead of , provided the convergence (2.4) is valid locally uniformly. As is the product of generated by the that form independent and identically distributed random variables under with distribution depending on , we are in the framework of Theorem 3.1’ p. 128 in Ibragimov and Hasminskii [8] and the LAN property is a consequence of the following two conditions:

-

For every and such that , we have

as .

-

For every and , we have

as .

In the same way as for the proof of ii) in Lemma 4.3, we have

Therefore, taking squares and summing in , i) is proved if we show that

| (4.14) |

as . Using (4.3), we have

hence is less than

for a locally bounded , which in turn is less than

| (4.15) |

for some locally bounded on . Since is a compound Poisson process under with intensity and jumps in with equal probability, the characteristic function of is explicitly given by

from which we obtain

| (4.16) |

Integrating (4.15), we derive

where has the same property as . Since is of order as in both microscopic and intermediate scales, we obtain (4.14) and i) follows.

4.3 Proof of Theorem 2.5

The strategy of the proof is quite different from that of Theorems 2.2 and 2.4, for we were not able to obtain asymptotic expansions for in a viscinity of with appropriate bounds on the stochastic remainders.

Consider instead the experiment generated by the observation of independent centred Gaussian random variables with variance , for satisfying the rate restriction

| (4.18) |

We plan to prove that under the restriction (4.18), the experiments and are asymptotically equivalent as . Theorem 2.5 then follows from the Le Cam theory, see for instance [10]. To that end, we map each increment in with

where the are independent random variables uniformly distributed on . Let us denote by the experiment generated by the . Since the increments take values in , we have a one-to-one correspondence between and the increment and therefore the experiments and are equivalent. Moreover, and live on the same state space and have smooth densities with respect to the Lebesgue measure. The proof of Theorem 2.5 is therefore implied by the following bound

locally uniformly in and where denotes the variational norm. This bound is implied in turn by the bound

| (4.19) |

locally uniformly in , since each experiment is the -fold product independent and identically distributed random variables101010For instance, by using the bound . Let us further denote by and the densities of and the Gaussian law respectively. We have

where, applying sucessively the triangle inequality and Cauchy-Schwarz, for any ,

Set . We claim that for , the terms , and are hence (4.19) and the result, for an appropriate choice of so that the convergence can hold locally uniformly in . Since is the density of the Gaussian law , we readily obtain

using . For the term , we observe that since , we have

where the are independent and symmetric. By Hoeffding inequality, this term is further bounded by

for every . If , one readily checks that

Moreover, if , we have, by Chernov inequality,

and this term is also . Thus and have the right order and it remains to bound the main term . By Plancherel equality we obtain the following explicit expression:

with

for any . By a first order expansion, we have that is less than

for some bounded function . Set . We thus obtain that is less than a constant times

If we pick such that , the term is of order . For the term

noting that , we bound the -periodic, even and continuous function by its supremum . The integrability of away from 0 enables to conclude that is of order . Finally, by Gaussian approximation, we readily obtain that is of order

In conclusion, we have that is dominated by the term and is thus of order . It follows that is of order and the choice implies thanks to the restriction condition . The proof of Theorem 2.5 is complete.

4.4 Proof of Theorem 2.6

Set

Under , the variables are independent, identically distributed, and we have

by (4.16). Moreover, for every ,

therefore, by the central limit theorem in distribution under as in all three regimes (microscopic, intermediate and macroscopic). We thus obtain the following representation

and the result follows from and

as in all three regimes.

4.5 Proof of Theorem 2.7

By (4.11) of Lemma 4.4, it suffices to prove

| (4.20) |

Up to taking a subsequence, we may assume that as . Using (4.12) and Theorem 2.6, for every , we have

where is a univariate function since has density with respect to the counting measure on . Therefore, Theorem 2.7 is equivalent to proving that

| (4.21) |

Using (4.2) of Lemma 4.1 we have

where

is positive (see Theorem 1 of Baricz [1]) and is in according to (4.3) of Lemma 4.1. We derive

hence (4.21). Since as , the conclusion follows.

References

- [1] Baricz, Á. (2008). Functional inequalities involving Bessel and modified Bessel functions of the first kind. Expositiones Mathematicae 26, 279–293.

- [2] Bauwens, L. and Hautsch, N (2006). Modelling high frequency financial data using point processes. Discussion paper.

- [3] Bogsted, M. and Pitts, S. (2010). Decompounding random sums: a nonparametric approach. Ann Inst Stat Math 62, 855–872.

- [4] Buchmann, B. and Grübel, R. (2003). Decompounding: an estimation problem for Poisson random sums. Ann. Statist 31, 1054–1074.

- [5] Buchmann, B. and Grübel, R. (2004). Decompounding Poisson random sums: recursively truncated estimates in the discrete case. Ann. Inst. Math 56, 743–756.

- [6] Comte, F. and Genon-Catalot, V. (2009). Nonparametric estimation for pure jump Lévy processes based on high frequency data. Stochastic Processes and their Applications 119, 4088 -4123.

- [7] Comte, F. and Genon-Catalot, V. (2010). Nonparametric adaptive estimation for pure jump Lévy processes. Annales de l’I.H.P., Probability and Statistics 46, 595–617.

- [8] Ibragimov, I.A. and Hasminskii, R.Z (1981). Statistical Estimation. Asymptotic Theory. Springer-Verlag.

- [9] Masoliver, J., Montero, M., Perelló, J. and Weiss, G.H. (2008). Direct and inverse problems with some generalizations and extensions. Arxiv preprint 0308017v2.

- [10] Le Cam, L. and Yang, L.G. (2000) Asymptotics in Statistics: Some Basic Concepts. 2nd edition. New York: Springer-Verlag.

- [11] Nasell, I. (1974). Inequalities for Modified Bessel Functions. Math. Comp. 28, 253 – 256.

- [12] Neumann, M. and Reiß, M. (2009). Nonparametric estimation for Lévy processes from low-frequency observations. Bernoulli 15, 223–248.

- [13] Sato, K-I. (1999). Lévy Processes and Infinitely Divisible Distributions. Cambridge University Press.

- [14] van der Vaart, A.W. (1998). Asymptotic Statistics. Cambridge University Press.

- [15] van Es, B., Gugushvili, S. and Spreij, P. (2007). A kernel type nonparametric density estimator for decompounding. Bernoulli 13, 672–694.

- [16] Watson, G.N (1922). A Treatise on the Theory of Bessel Functions. Cambridge University Press.