M-estimators for Isotonic Regression

Abstract

In this paper we propose a family of robust estimates for isotonic regression: isotonic M-estimators. We show that their asymptotic distribution is, up to an scalar factor, the same as that of Brunk ’s classical isotonic estimator. We also derive the influence function and the breakdown point of these estimates. Finally we perform a Monte Carlo study that shows that the proposed family includes estimators that are simultaneously highly efficient under gaussian errors and highly robust when the error distribution has heavy tails.

Keywords: Isotonic Regression, M-estimators, Robust Estimates.

1 Introduction

Let be independent random variables collected along observation points according to the model

| (1) |

where the ’s are i.i.d. symmetric random variables with distribution . In isotonic regression the trend term is monotone non-decreasing, i.e., , but it is otherwise arbitrary. In this set-up, the classical estimator of is the function which minimizes the distance between the vector of observed and fitted responses, i.e, it minimizes,

| (2) |

in the class of non-decreasing piecewise continuous functions. It is trivial but noteworthy that Equation (2) posits a finite dimensional convex constrained optimization problem. Its solution was first proposed by Brunk (1958) and has received extensive attention in the Statistical literature (see e.g., Robertson, Wright and Dyskra (1988) for a comprehensive account). It is also worth noting that any piecewise continuous non-decreasing function which agrees with the optimizer of (2) at the ’s will be a solution. For that reason, in order to achieve uniqueness, it is traditional to restrict further the class to the subset of piecewise constant non-decreasing functions. Another valid choice consists in the interpolation at the knots with non-decreasing cubic splines or any other piecewise continuous monotone function, e.g., Meyer (1996). We will call this estimator the L isotonic estimator.

The sensitivity of this estimator to extreme observations (outliers) was noted by Wang and Huang (2002), who propose minimizing instead using the norm, i.e. , minimizing

This estimator will be call here L1 Isotonic estimator. Wang and Huang (2002) developed the asymptotic distribution of the trend estimator at a given observation point and obtained the asymptotic relative efficiency of this estimator compared with the classical L2estimator. Interestingly, this efficiency turned out to be , the same as in the i.i.d. location problem.

In this paper we will propose instead a robust isotonic M-estimator aimed at balancing robustness with efficiency. Specifically we shall seek the minimizer of

| (3) |

where is a an estimator of the error scale previously obtained and satisfies the following properties

- A1

-

(i) is non-decreasing in , (ii) , (iii) is even, (iv) is strictly increasing for and (v) has two continuous derivatives and is bounded and monotone non-decreasing.

Clearly, the choice corresponds to taking while the option is akin to opting for . These two estimators do no require the scale estimator

Note that the class of M-estimators satisfying A1 does not include estimators with a redescending choice for . We believe that the strict differentiability conditions on required in A1 are not strictly necessary, but they make the proofs for the asymptotic theory simpler. Moreover, some functions which are not twice differentiable everywhere such as or the Hubers’ functions defined below in (7) can be approximated by functions satisfying A1.

The asymptotic distribution of the L2 isotonic estimators at a given point was found by Brunk (1970) and Wright (1981) and the one of the L1 estimator by Wang (2002). They prove that the distribution of these estimators conveniently normalized converge to the distribution of the slope at zero of the greatest convex minorant of the two-sided Brownian Motion with parabolic drift. In this paper, we prove a similar result for isotonic M-estimators. The focus of this paper is on estimation of the trend term at a single observation point . We do not address the issue of distribution of the whole stochastic process . Recent research along those lines are given by Kulikova and Lopuhaä (2006) and a related result with smoothing was also obtained simultaneously in Pal and Woodroofe (2006).

This article is structured as follows. In Section 2 we propose the robust isotonic M-estimator. In Section 3 we obtain the limiting distribution of the isotonic M-estimator when the error scale is known. In Section 4 we prove that under general conditions the M-estimators with estimated scale have the same asymptotic distribution than when the scale is known. In Section 5 we define an influence function which measures the sensitivity of the isotonic M-estimator to an infinitesimal amount of pointwise contamination. In Section 6 we calculate the breakdown point of the isotonic M-estimators. In Section 8 we compare by Monte Carlo simulations the finite sample variances of the estimators for two error distributions: normal and Student with three degrees of freedom. In Section 7 we analyze two real dataset using The L2 and the isotonic M-estimators. Section 9 is an Appendix containing the proofs.

2 Isotonic M-Estimators

In similarity with the classical setup, we consider isotonic M-estimators that minimize the objective function (3) within the class of piecewise constant non-decreasing functions. As in the L2 and L1 cases, the isotonic M-estimator is a step function with knots at (some of) the ’s. In Robertson and Waltman (1968) it is shown that maximum-likelihood-type estimation under isotonic restrictions can be calculated via min-max formulae. Assume first that we know that the scale parameter (e.g. , the MAD, of the s) is . Since we are considering M-estimators with non-decreasing (see A1), they can be view as the maximum likelihood estimators corresponding to errors with density

Then we can compute the isotonic M-estimator at a point using the min-max calculation formulae

| (4) |

where is the unrestricted M-estimator which minimizes

| (5) |

where . Alternatively, if is convex and differentiable, as we are assuming, the terms in (4) can be represented uniquely as a zero of

| (6) |

In particular, when where is a probability density, the isotonic M-estimator coincides with the maximum likelihood estimator when is is assumed to have density . In particular if is the N density, the MLE is the M-estimator which defined by and therefore it coincides with the classical estimator. When is the density of a double exponential distribution, the MLE is the M-estimator defined by and therefore it coincides with the L1 isotonic estimator. In these two cases the estimators are independent of the value of One popular family of functions to define M-estimators is the Huber family

| (7) |

Clearly, when is replaced by equations (4)-(6) still holds with replaced by Since is non-decreasing, the function defined in equation (6) is non-increasing as a function of . This entails the fundamental identities given below

| (8) | ||||

| (9) |

These identities will be very useful in the development of the asymptotic distribution.

3 Asymptotic Distribution

In this section we derive the asymptotic distribution of the isotonic M-estimator of We first make the sample size explicit in the formulation of the model by postulating

| (10) |

where the errors form a triangular array of i.i.d. random variables with distribution and is a triangular array of observation points. Their exact location is described by the function . The values may be fixed or random but we will assume that there exists a continuous distribution function which has as support a finite closed interval such that

| (11) |

Without loss of generality we shall assume in the sequel it is the interval .

We will study the asymptotic distribution of where is an interior point of The classical L2 isotonic estimator with at the boundary of the support of is known to suffer from the so-called spiking problem (e.g., Sun and Woodroofe, 1999), i.e., is not even consistent. We further make the following assumptions.

- A2

-

The function is continuously differentiable in a neighborhood of with .

- A3

-

For a fixed , we assume the function has two continuous derivatives in a neighborhood of , and .

- A4

-

The error distribution has a density symmetric and continuous with .

We consider first the case where is known. Our first aim is to show that isotonic M-estimation is asymptotically a local problem. Specifically, we will see in Lemma 1 that depends only on those corresponding to observation points lying in a neighborhood of order about . This result is similar to Prakasa Rao (1969), Lemma 4.1, who stated it in the context of density estimation. Our treatment here will parallel that of Wright (1981), who worked on the asymptotics of the isotonic regression estimator when the smoothness of the underlying trend function is specified via the number of its continuous derivatives.

Specifically, since we may choose for an arbitrary and sufficiently large, positive numbers and for which

With this, define the localized version of the isotonic M-estimator as

| (12) |

Then we have the following Lemma

Is is also noteworthy that the estimator in Equation (12) is not computable, for and depend on the distribution which is generally unknown. For computational purposes this implies that the calculation of these estimators will indeed be global for fixed sample sized. Lemma 1 is, however, crucial to study the asymptotic properties of .

Given an stochastic process , we denote by “” the random variable that corresponds to the slope at zero of the greatest convex minorant of The following theorem gives the asymptotic distribution of .

Theorem 1

Remark 1

Notice that in the case of the L2 isotonic estimator the function , so and so that EG( and . Then the standardizing constant is given by

as it is known for the L2 isotonic estimator.

Remark 2

In the case of L1 isotonic regression notice that in the function , so sign for or else is left undefined. Our method is thus not applicable as the assumptions on do not hold. However, consider a sequence of functions for which

| (15) |

and so that there is continuity of the first 3 derivatives everywhere; for a construction of such type of functions it is enough to consider quartic splines (e.g., De Boor, 2001). In this setup we get

Letting and so that , we obtain

as it is known in the case of L1 isotonic regression (see Wang and Huang, 2002).

Remark 3

A similar construction to Equation (15) may be applied to the functions in the Huber’s family.

4 Robust Isotonic M-Estimators with a Previous Scale Estimator

We will consider now the more realistic case where is not known and it is replaced by an estimator previously calculated. Then, in order to obtain an scale equivariant estimator we should replace in (5) and (6) by a robust scale equivariant estimator In Remarks 4 and 5 below we give some possible choices for

In the next Theorem it is shown that under suitable regularity conditions, it can be proved that if converges to fast enough, both isotonic M-estimators, the one using the fixed scale and the one using the scale , have the same asymptotic distribution. Making explicit the scale in the notation, denote the isotonic M-estimator of based on a fixed scale by Then

where solves

| (16) |

over .

We need the following Additional Assumptions:

- A5

-

There exists such that for and if

- A6

-

The estimator satisfies

Then we have the following Theorem:

Theorem 2

Assume A1-A6 Then

Assume also that (11) holds, then both estimators have the same asymptotic distribution.

Remark 4

In the context of nonparametric regression Ghement, Ruiz and Zamar (2008) propose to use as scale estimator given by

where is an M-estimator of scale, i.e., is defined as the value satisfying

| (17) |

where is a function which is even, non-decreasing for bounded and continuous. The right hand side is generally taken so that if is N(0,1), This condition makes the estimator converging to the standard deviation when applied to a random sample of the N(0,1) distribution. A popular family of functions to compute scale M-estimators is the bisquare family given by

| (18) |

Ghement et al. (2008) prove that if is continuous under general conditions on Condition A6 is satisfied with defined by

| (19) |

Remark 5

An alternative scale estimator, which does not require the continuity of is provided by

where are the residuals corresponding to the L1isotonic estimator. We conjecture but we do not have a proof that this estimator converges also with rate to median

5 Influence Function

In order to obtain the influence function of the isotonic M-estimator at a given point we need to assume that the pair is random. In this case the isotonic regression model assumes that where is independent of and is non-decreasing. We assume that the error term has a symmetric density , and that the observation point has a distribution with density .

We start assuming that is known and suppose that we want to estimate Given an arbitrary distribution of , the isotonic M-estimating functional of which we henceforth denote by is defined in three steps as follows. First for let be defined as the value satisfying

Let

and then is defined by

Let be the empirical distribution of , then if is the estimator defined in (4), we have

It is immediate that if is the joint distribution corresponding to model (1) we have so that the isotonic M-estimator is Fisher-consistent. Consider now the contaminated distribution

where represents a point mass at . In this case we define the influence function of by

| (20) |

Then, we have the following Theorem:

Theorem 3

Consider the isotonic regression model given in (1) and let be an isotonic M-estimating functional, where is an interior observation point. Then, under assumptions A1-A4 we have

| (21) |

Notice that in the numerator of (20) appears the square of the bias instead of the plain bias as in the classical definition of Hampel (1974). Therefore for the isotonic M-estimator the bias caused by a point mass contamination is of order instead of the usual order of .

Alternatively, it is also of interest to know what happens when we are estimating and contamination takes place at a point According to (21), the influence function in this case is zero. This occurs because in this case for sufficiently small .

It is easy to show that when we use a scale defined by a continuous functional, the influence function of the isotonic M-estimator is still given by (21).

6 Breakdown Point

Roughly speaking the breakdown point of an estimating functional of is the smallest fraction of outliers which suffices to drive to infinity. More precisely, consider the contamination neighborhood of the distribution of size defined as

where is an arbitrary distribution of such that takes values in and in . The asymptotic breakdown point of at is defined by

We start considering the case that is known. Then we have the following theorem.

Theorem 4

Consider the isotonic regression model given in (1) and let be an isotonic M-estimating functional where is an interior observation point. Then under assumptions A1-A4 we have

In the special case when is uniform, this becomes

| (22) |

which takes a maximum value of at

In the case that is replaced by an estimator derived from a continuous functional it can be proved that the breakdown point of satisfies

7 Examples

Example 1

In this section we consider data on Infant Mortality across Countries. The dependent variable, the number of infant deaths per each thousand births is assumed decreasing in the country’s per capita income. These data are part of the R package “faraway” and was used in Faraway (2004). The manual of this package only mentions that the data are not recent but it does not give information on the year and source. In Figure 1 we compare the L2 isotonic regression estimator with the isotonic M-estimator computed with the Huber’s function with and as in Remark 2, where is defined by (17)-(19) with and There are four countries with mortality above 250: Saudi Arabia (650), Afghanistan (400), Libya (300) and Zambia (259). These countries, specially Saudi Arabia and Libya due to their higher relative income per capita, exert a large impact on the L2 estimator. The robust choice, on the other hand, appears to resistant to these outliers and provides a good fit.

Example 2

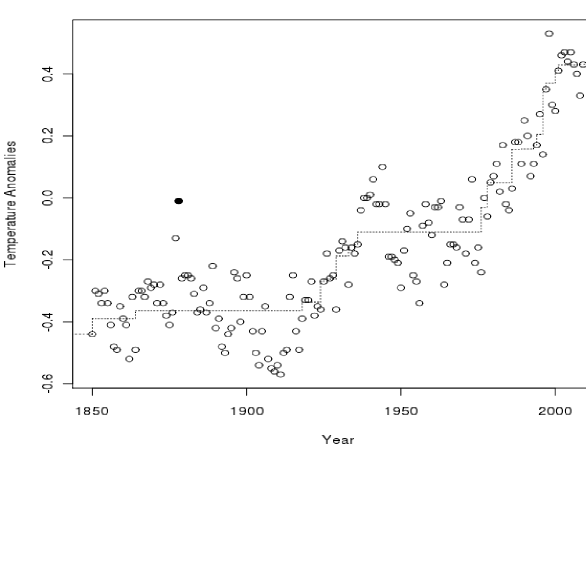

We reconsider the Global Warming dataset first analyzed in the context of isotonic regression by Wu, Woodroofe and Mentz (2001) from a classical perspective and subsequently analyzed from a Bayesian perspective in Alvarez and Dey (2009). The original data is provided by Jones et al. (see http//cdiac.esd.ornl.gov/trends/temp/jonescru/jones.html) containing annual temperature anomalies from 1858 to 2009, expressed in degrees Celsius and are relative to the 1961-1990 mean. Even though the global warming data, being a time series, might be affected by serial correlation, e.g. Fomby and Vogelsang (2002), we opted for simplicity as an illustration to ignore that aspect of the data and model it as a sequence of i.i.d. observations.

In Figure 2 we plot the L2 isotonic estimator, which for these data is identical to the isotonic M-estimate with k=0.98. Visual inspection of the plot shows a moderate outlier corresponding to the year 1878 (shown as a solid circle). That apparent outlier, however, has no effect on the estimator due to the isotonic character of the regression.The fact that the L2 and the isotonic M-estimates coincide for these data seems to indicate that the phenomenon of Global Warming is not due to isolated outlying anomalies, but it is due instead to a steady increasing trend phenomenon. In our view, that validates from the point of view of robustness, the conclusions of other authors on the same data (e.g. Wu, Woodroofe and Mentz (2001), and Álvarez and Dey (2009)) who have rejected the hypothesis of constancy in series of the worlds annual temperatures in favor of an increasing trend.

8 Monte Carlo results

Interestingly the limiting distribution of the Isotonic M-estimator is based on the ratio

as in the the i.i.d. location problem (e.g. Maronna, Martin and Yohai, 2006). The slower convergence rate, however, entails that the respective asymptotic relative efficiencies are those of the location situation taken to the power . Specifically, note that from Theorem 1 for any isotonic M-estimator

| (23) | |||

| (24) |

where avar stands for asymptotic variance and var for variance.

In order to determine the finite sample behavior of the isotonic M-estimators we have performed a Monte Carlo study. We took i.i.d. samples from the model (1) with trend term and where the distribution is N(0,1) and Student with three degrees of freedom. The values corresponds to a uniform limiting distribution for .

We estimated at , the true value of which is using three isotonic estimators: the L2 isotonic estimator, the L1 isotonic estimator and the same isotonic M-estimator that was used in the examples. We performed replicates at two sample sizes, and . Dykstra and Carolan (1998) have established that the variance of the random variable “” is approximately 1.04. Using this value, we present in Table 1 sample mean square errors (MSE) times as well as the corresponding asymptotic variances.

|

|||||||||||||||||||||||||||||||||||||

Table 1. Sample MSE and avar for Isotonic Regression Estimators.

We note that for both distributions, the empirical MSEs for are close to the avar values. We also see that under both distributions the M-estimator is more efficient that the L1 one, that the M- estimator is more efficient than the L1 one for both distributions and that the L1 estimator is slightly less efficient than the L2 estimator for the normal case but much more efficient for the Student distribution. In summary, the isotonic M-estimate seems to have a good behavior under both distributions.

9 Appendix

9.1 Proof of Lemma 1

Without loss of generality we can assume that Given , for sufficiently large there exist positive numbers and for which

As in Wright (1981), we first argue that

where

| (25) | ||||

| (26) |

To see this, note that the complement of is the set in which, for all and all we have that . Since is non-decreasing we can write

This in turn entails that in

Using the fact that the maximum and the minimum may be reversed in computing these estimators (e.g. Robertson and Waltman, 1968) and a similar argument for in equation (25) one can show that

So we need to prove that

We will prove The result for can be obtained in a similar manner.

Let

| (27) | ||||

| (28) |

Since

it will be enough to prove that

| (29) |

Since the proofs of (29) for and are similar, (29) will be only proved for By the fundamental identity (9) we have

| (30) |

In the sequel in order to simplify notation we will omit the subindex writing , and making it explicit only when there is a risk of confusion. We can write

and by a Taylor expansion we get

where . Put , then

Thus, since is increasing we get

| (31) |

Put . As , we obtain

| (32) | |||

| (33) |

Therefore the event defined in (30) is included in the event defined by

The equation above can be rewritten in terms of integrals with respect to the empirical distribution of the ’s as

| (34) |

Since are i.i.d., relabelling the ’s on the left hand side we get that

| (35) |

where

| (36) |

Adding and subtracting we can write

| (37) |

Using (11), for large enough, the second term in the above equation is bounded by

and since by the inverse function theorem , we obtain that for some constant which does not depend on we can write

| (38) |

Consider now the first term in the right hand side of Equation (37). Using (11) we have

Therefore

with . Then, for some constant which does not depend on we can write

| (39) |

From (30), (34), (35), (36), (37), (38) and (39) we derive that there exists a constant independent of such that for large enough and

| (40) |

At this point, we use the Hàjek-Renyi Maximal Inequality (e.g., Shorack, 2000) which asserts that for a sequence of independent random variables with mean and finite variances and for a positive non-decreasing real sequence ,

| (41) |

Using this inequality from (40) we get that

| (42) |

Approximating the Riemann sum we obtain

| (43) |

and since by (11) , for large enough we have

| (44) |

From (42), (43) and (44) we derive that for large enough

Then the Lemma follows immediately.

9.2 Proof of Theorem 1

Without loss of generality we can assume that Since , and is arbitrary, we will consider the localized estimator

| (45) |

where is defined as the root of

| (46) |

over . Note that the localized estimator depends on the ’s that lie on a neighborhood about which shrinks at a rate . To proceed with the development of the asymptotic distribution let now , and . With this notation, is a root of the partial sums in the parametrization

| (47) |

where . So that the relabelling implies . Consequently,

Now a Taylor expansion of around for any gives

which entails that

Using the equivariance of M-estimators, the monotonicity of and the fact that is bounded, it can be proved that

where solves

| (48) |

and

Thus, using that the are bounded over we have

This entails that

where

Then, we only need to obtain the asymptotic distribution of

Let be the solution of

Since we have that

| (49) |

where

| (50) |

We will approximate now as follows

| (51) |

and therefore

| (52) |

| (53) |

and

| (54) |

Then, taking and applying the law of large numbers is easy to show that a.s. and therefore by (49) and (50) too. Since satisfies (48), by a Taylor expansion of we get

From here we obtain

and then

| (55) |

By (48), the Law of the Large Numbers, and bounded we have

and

Then, (55) entails

| (56) |

Let

| (57) |

By (53) and the Central Limit Theorem we have that for any set of finite numbers , the random vector converges in distribution to N(0, where with

Moreover, using standard arguments, it can be proved that is tight. Then, we have

| (58) |

where is a two sided Brownian motion

As for the second term in the right hand side of (56) define

| (59) |

For we can write

| (60) |

and then

| (61) |

Integrating by parts we get

| (62) |

and by (11) we have

| (63) |

We can write

and by(11) we get

| (64) |

Therefore by (62), (63) and (64) we get

and for (61) we get that for

| (65) |

Now we compute the variance of From (60) we have

9.3 Proof of Theorem 2

We require the following Lemma

Lemma 2

Assume A1-A5 Then,

| (68) |

Proof

Taking the first derivative of Equation (16) with respect to yields

and then

Let Then by A5 we obtain

Therefore

Proof of Theorem 2

By the mean value theorem

where is some intermediate point between and . Hence, by Lemma 2 we have

and A6 implies

9.4 Proof of Theorem 3

Without loss of generality we can assume that We consider first the case Assume that . Then represents a contamination model where an outlier is placed at the observation point with value which is below the trend at the point. Let be the value such that

It is immediate that

| (69) |

Then should be the value of satisfying

| (70) |

and, since by (69) we have

| (71) |

Applying the Mean Value Theorem to the first term of (71) we can find such that

| (72) |

As for the second term in (71) we also have that

where . Since is odd and even, , so that the first term above vanishes. As for the second term, notice that

| (73) |

The first integral factor in the right hand side of the above display can be further approximated. By the Mean Value Theorem, there exists such that and

| (74) |

From expressions (72)-(74) we obtain that Equation (71), can be written as

Dividing both sides of this equation by and using that and when we obtain

| (75) |

Finally, according to (69) and using the Mean Value Theorem, we can write

where . Then using equation (75) we obtain that

The proof in the case the that is similar

We consider now the case To prove this part of the theorem is enough to show that there exists , so that implies

and to prove this is enough to show that

| (76) |

When this is immediate. Consider the case that

Clearly for

| (77) | ||||

It is also easy to show that implies

| (78) |

and for and for all

| (79) |

Then, using (77)-(79) and the fact that in order to prove (76), it is enough to show that

| (80) |

Recall that is the solution of

where

Clearly and since and are both increasing in we get Then, since is bounded, we can find so that for we have

and therefore Then (80) holds and this proves the Theorem for the case The proof for the case is similar.

10 Proof of Theorem 4.

Without loss of generality we can assume that It is easy to see that the least favorable contaminating distribution is concentrated at where tends to or to

A necessary and sufficient condition for is that the equation

| (81) |

have a bounded solution solution for all and that the equation

| (82) |

have a solution for all .

Taking we find that a sufficient condition for the existence of a bounded solution of (81) for all is that

and this is equivalent to

| (83) |

Taking we obtain that a sufficient condition for the existence of solution of (82) for all is that

and this equivalent to

| (84) |

References

Alvarez, E.E. y Dey, D.K. (2009), Bayesian Isotonic Changepoint Analysis. Annals of the Institute of Statistical Mathematics, 61, 355–370.

Brunk, H.D. (1958). On Estimation of Parameters Restricted by Inequalities, Ann. Math. Statist., 29, 437–454.

*Brunk, H.D. (1970) Estimation of Isotonic Regression, Nonparametric Techniques in Statistical Inference, 177–195, Cambridge Univ. Press.

De Boor, C. (2001) A Practical Guide to Splines, Springer, New York.

Dykstra, R. and Carolan, C. (1998) The Distribution of the of two-sided Brownian Motion with Quadratic Drift. J. Statist. Computat. Simulation, 63, 47–58.

Faraway, J.J. (2004). Linear Models with R, Chapman & Hall/CRC, Boca Raton, FL.

Fomby, T.B. and Vogelsang, T.J. (2002) The application of size-robust trend statistics to global-warming temperature series, Journal of Climate, 15, 117–123.

Hampel, F. R. (1974). The influence curve and its role in robust estimation. J. Amer. Statist. Assoc.,69, 383-393.

Ghement, I.R., Ruiz, M. and Zamar, R.H. (2008). Robust Estimation of Error Scale in Nonparametric Regression Models. Journal of Statistical Planning and Inference, 138, 3200-3216.

Kulikova,V.N., and Lopuhaä, H.P. (2006) The limit process of the difference between the empirical distribution function and its concave majorant, Statistics & Probability Letters, 76, 1781–1786.

Maronna, R.A., Martin, R.D., and Yohai, V.J. (2006). Robust Statistics Theory and Methods, John Wiley, New York.

Meyer, M. (1996) Shape Restricted Inference with Applications to Nonparametric Regression, Smooth Nonparametric Regression, and Density Estimation, Ph.D. Thesis, Statistics, University of Michigan.

Pal, J.K. and Woodroofe, M. (2006) On the Distance Between Cumulative Sum Diagram and Its Greatest Convex Minorant for Unequally Spaced Design Points, Scand. J. Statist. 33, 279–291.

Prakasa Rao, B.L.S. (1969) Estimation of a Unimodal Density. Sankhyã A, 31, 23–36.

Robertson, T., Waltman, P., (1968). On Estimating Monotone Parameters. Ann. Math. Statist., 39, 1030–1039.

Robertson, T., Wright, F.T. and Dyskra, R. L. (1988) Order Restricted Statistical Inference. New York John Wiley.

Shorack, G. R. (2000) Probability for Statisticians. Springer, New York.

Sun, J. and Woodroofe, M. (1999) Testing uniformity versus a monotone density. Ann. Statist. 27, 1, 338-360.

Wang, Y., and Huang, J., (2002) Limiting Distribution for Monotone Median Regression. J. Statist. Plann. Inference, 108, 281–287.

Wright, F.T. (1981) The Asymptotic Behavior of Monotone Regression Estimates. Ann. Statist. 9, 443–448.

Wu, W.B.; Woodroofe, M. and Mentz, G.B. (2001) Isotonic regression: another look at the change-point problem. Biometrika 88, 793-804.