Fractal Dimensions for Continuous Time Random Walk Limits

Abstract.

In a continuous time random walk (CTRW), each random jump follows a random waiting time. CTRW scaling limits are time-changed processes that model anomalous diffusion. The outer process describes particle jumps, and the non-Markovian inner process (or time change) accounts for waiting times between jumps. This paper studies fractal properties of the sample functions of a time-changed process, and establishes some general results on the Hausdorff and packing dimensions of its range and graph. Then those results are applied to CTRW scaling limits.

Key words and phrases:

Fractional Brownian motion, Lévy process, strictly stable process, continuous time random walk, Hausdorff dimension, packing dimension, self-similarity.1. Introduction

Continuous time random walks have attracted a lot of attention in recent years. They provide flexible models for anomalous diffusion phenomena in a wide range of scientific areas including physics, finance and hydrology. Consider a random walk on , where model the particle jumps. The continuous time random walk (CTRW) imposes a random waiting time between jumps. Let , where are nonnegative random variables. The CTRW jumps to location at time . The number of jumps by time is given by the counting process , where . The time-changed process represents the location of a random walker at time . A standard assumption in the literature is that are iid. In recent years CTRW with dependent jumps or/and waiting times have also been considered, see for example [12, 26, 41].

The scaling limit of a CTRW is a time-changed (or iterated) process of the form , where the outer process is the scaling limit of the random walk and the inner process accounts for the random waiting times . This has been proved by Meerschaert and Scheffler [29], and Becker-Kern, Meerschaert and Scheffler [3, 4] under the assumption that are iid, the jumps belong to the domain of attraction of an operator stable law and the waiting times belong to the strict domain of attraction of a positive stable random variable with index . In this case, the outer process is an operator stable Lévy process with values in and the inner process is the inverse of a -stable subordinator with . Namely,

| (1.1) |

The aforementioned authors further proved that the density function of solves fractional partial differential equations; see [1, 2, 25] and the references therein for further information on PDE connections of CTRW limits.

When the independence assumption on the jumps is removed, Meerschaert, Nane and Xiao [26] showed that the outer process can be taken as a fractional Brownian motion, a stable Lévy process or a linear fractional stable motion. More general inner processes may also be possible if the waiting times are dependent.

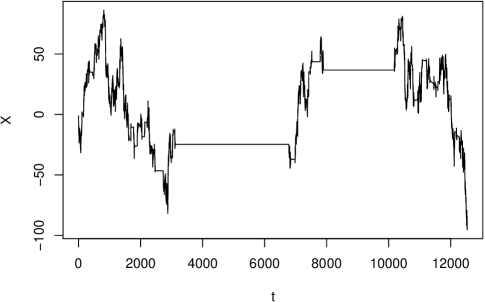

In general, a CTRW limiting process is non-Markovian, non-Gaussian and satisfies a form of self-similarity. Figure 1 illustrates a typical trajectory of the time-changed process , in the case where the outer process is a Brownian motion. The graph resembles that of a Brownian motion, interrupted by long resting periods. This process is the long-time scaling limit of a CTRW with mean zero, finite variance jumps and heavy tailed waiting times in the domain of attraction of a -stable subordinator, see [29].

This paper is concerned with fractal properties of the CTRW limiting process defined by for . In particular we determine the Hausdorff and packing dimensions of the range and the graph . There has been a large literature on sample path and fractal properties of Lévy processes [40, 43], and Gaussian or stable random fields [19, 44]. Several methods have been developed for computing the Hausdorff dimensions of the range and graph of stochastic processes under “minimal” conditions. To give a brief description of the general method, let be a stochastic process with values in (for simplicity we assume that the components of are independent). If there exist positive constants and such that

| (1.2) |

then one can prove

| (1.3) |

and

| (1.4) |

In the above and sequel, denotes Hausdorff dimension. Moreover, if there exist positive constants and such that

| (1.5) |

then equalities hold in both (1.3) and (1.4). The above method can be applied to a wide class of stochastic processes, including self-similar processes with stationary increments such as stable Lévy processes, fractional Brownian motion and the iterated Brownian motion ([9, 10]). See [14, 45, 38] for further information.

However, the time-changed process considered in this paper does not satisfy (1.5). In fact, if we consider the process in Figure 1, where is a Brownian motion in and is the inverse of a -stable subordinator defined by (1.1), then the inner process remains constant over infinitely many intervals, corresponding to the jumps of the stable subordinator . Hence the graph of the process remains flat over these resting intervals, as evidenced by Figure 1. More precisely, it can be proved by using Proposition 2 in Chapter III of Bertoin [5] that, for any , . This implies that . Hence does not satisfy (1.5). As we will see from Propositions 3.1 and 3.6, the actual value of may be strictly smaller than what is suggested by (1.4).

Packing dimension was introduced in 1980’s by Tricot [42] as a dual concept to Hausdorff dimension, and has become a useful tool for analyzing fractal sets and sample paths of stochastic processes. It is known that Hausdorff and packing dimensions of a set characterize different geometric aspects of and many random fractals arising in studies of stochastic processes have different Hausdorff and packing dimensions. See [40, 43] and the references therein for more information and [22, 20, 38] for recent development. A fractal set with the property is usually called a regular fractal. We will see that the range and graph of CTRW limits considered in Section 3 are often regular fractals.

The rest of this paper is organized as follows. In Section 2 we prove under quite general conditions that

| (1.6) |

| (1.7) |

and

| (1.8) |

where is the -valued process defined by (see (2.12) and (2.13) below). These results are applied in Section 3 to the scaling limits of continuous time random walks. First we consider the uncoupled case, in which the iid waiting times are independent of the iid particle jumps . Then we treat certain coupled examples, where the jump depends on the previous waiting time. We also consider triangular array CTRW limits, which lead to general inverse subordinators. Finally we examine the case of correlated jumps. In all these cases, the outer process is either a Lévy process or a fractional Brownian motion.

2. General Results

In this section we prove some general results on the Hausdorff and packing dimensions of the range and graph of the time-changed process defined by for . We assume that is a stochastic process with values in and is a process with and nondecreasing continuous sample functions. Both processes and are defined on a probability space , and they are not necessarily independent. In the following section, the results in this section will be applied to CTRW scaling limits. There, will be taken as the inverse of a strictly increasing subordinator , defined by (1.1). For a coupled CTRW, where the jump variable depends on the waiting time, the inner process and the outer process in the scaling limit are dependent.

First we recall briefly the definitions of Hausdorff and packing dimension. More detailed information together with their applications to stochastic processes and other areas can be found in Falconer [13], Kahane [19], Taylor [40] and Xiao [43]. For any , the -dimensional Hausdorff measure of is defined by

| (2.1) |

where denotes the open ball of radius centered at The sequence of balls satisfying the two conditions on the right-hand side of (2.1) is called an -covering of . It is well-known that - is a metric outer measure and every Borel set in is - measurable. The Hausdorff dimension of is defined by

It is easily verified that satisfies the -stability property: For any , one has

| (2.2) |

Similarly to (2.1), the -dimensional packing measure of is defined as

where - is the set function on subsets of defined by

The packing dimension of is defined by It can be verified that also satisfies the -stability property analogous to (2.2).

The packing dimension can also be defined through the upper box-counting dimension. For any and any bounded set let be the smallest number of balls of radius needed to cover . The upper box-counting dimension of is defined as

| (2.3) |

Tricot [42] proved that the packing dimension of can be obtained from by

| (2.4) |

see also Falconer [13, p.45]. It is well known that for every (bounded) set ,

| (2.5) |

The following theorem determines the Hausdorff and packing dimension of the range in terms of the range of .

Theorem 2.1.

Let be the iterated process with values in defined by , where the processes and satisfy the aforementioned conditions. If a.s. and there exist constants and such that for all constants

| (2.6) |

then almost surely

| (2.7) |

Proof.

Since the process is non-decreasing and continuous, the range is the random interval . Hence .

It follows from the -stability of and (2.6) that a.s. Hence almost surely. On the other hand, (2.6) implies

| (2.8) |

where denotes the set of positive rational numbers. Since almost surely, we see that there is an event with such that for every we have and for all . Since for every there is a such that , we derive that

Combining the upper and lower bounds for yields the first equation in (2.7). The proof of the second equation in (2.7) is very similar and is omitted. ∎

Applying Theorem 2.1 to the space-time process with values in , one obtains immediately the following corollary.

Corollary 2.2.

Let be the iterated process with values in as in Theorem 2.1. If a.s. and there exist constants and such that for all constants

| (2.9) |

then

| (2.10) |

and

| (2.11) |

The random set in the left hand side of (2.10) may be interesting, but it is quite different than the graph of . In order to determine the Hausdorff and packing dimension of the graph set of , we will make use of the -valued process defined on the probability space by

| (2.12) |

where is defined by

| (2.13) |

Since is nondecreasing and continuous, it can be verified that the function is strictly increasing and right continuous, thus can have at most countably many jumps. Moreover, one can verify that for all and for all .

Theorem 2.3.

Proof.

We only prove (2.15), and the proof of (2.16) is similar. The sample function is a.s. strictly increasing and we can write the unit interval [0, 1] in the state space of as

| (2.17) |

where for each , is a subintervals on which is a constant. Using we can express , which is the gap corresponding to the jumping site of , except in the case when . In the latter case, .

Notice that () are disjoint intervals and

Thus, over each interval , the graph of is a horizontal line segment. More precisely, we can decompose the graph set of as

| (2.18) |

Hence, by the -stability of , we have

| (2.19) |

On the other hand, every can be written as for some and , we see that

| (2.20) |

It follows from (2.14) that

| (2.21) |

Combining this with the assumption that almost surely, we can find an event such that and for every we derive from (2.21) that

| (2.22) |

since for some , and implies . Combining (2.20) and (2.22) yields

| (2.23) |

Many self-similar processes with stationary increments satisfy (2.6) and (2.14), hence Theorems 2.1 and 2.3 have wide applicability. To apply the above theorems to CTRW scaling limits, we now take to be the inverse of a subordinator . We assume that has no drift, and its Laplace transform is given by

where the Laplace exponent

| (2.24) |

We also assume that the Lévy measure of satisfies , so that the sample function is a.s. strictly increasing.

Let denote the inverse of defined by (1.1). Since the sample function of is strictly increasing, we see that the function is almost surely continuous and nondecreasing. Moreover, .

3. Continuous Time Random Walk Limits

In the following, we compute the Hausdorff and packing dimensions of the range and graph of the sample path of scaling limits of continuous time random walks.

3.1. CTRW with iid jumps: The uncoupled case

Consider a CTRW whose iid waiting times belong to the domain of attraction of the positive -stable random variable , and whose iid jumps belong to the strict domain of attraction of the -dimensional stable random vector . We assume that and are independent; that is, the CTRW is uncoupled.

It follows from Theorem 4.2 in Meerschaert and Scheffler [29] that the scaling limit of this CTRW is a time-changed process , where is the inverse (1.1) of a -stable subordinator . Since is self-similar with index , its inverse is self-similar with index . Since is independent of , the CTRW scaling limit is self-similar with index .

Proposition 3.1.

Let , where is a stable Lévy motion of index with values in and is the inverse of a stable subordinator of index , independent of . Then

| (3.1) |

and

| (3.2) |

Proof.

The result (3.1) follows from Theorem 2.1 (or Corollary 2.4) and the known results on the Hausdorff and packing dimension of the range of the stable Lévy process . The former is due to Blumenthal and Getoor [6, 7], and the latter is due to Pruitt and Taylor [36].

In order to prove (3.2), we first recall from Pruitt and Taylor [35] their result on the Hausdorff dimension of the range of the Lévy process with independent stable components: for any constant ,

| (3.3) |

Theorem 3.2 in Meerschaert and Xiao [32] (see also Khoshnevisan and Xiao [22] for more general results) shows that also equals the right hand side of (3.3). Therefore, (3.2) follows from the above and Theorem 2.3. ∎

If the CTRW jumps have finite second moments, then the limiting process is , where is a Brownian motion, and Proposition 3.1 with gives

| (3.4) |

The Hausdorff dimension of the graph of a stable Lévy process in was determined by Blumenthal and Getoor [8] when and is symmetric, by Jain and Pruitt [17] when is transient (i.e. ) and by Pruitt and Taylor [35] in general. The packing dimension of the graph of was determined by Rezakhanlou and Taylor [37]. Combining their results with Corollary 2.2, we obtain

| (3.5) |

Clearly, this is different from (3.2). Moreover, we notice that the results (3.1) and (3.5) do not depend on , because the set is a.s. a closed interval, so the range dimension is the same after the time change.

3.2. CTRW with iid jumps: The coupled case

In some applications, it is natural to consider a coupled CTRW where are iid, but the jump depends on the preceding waiting time . We can also extend the results of the last section to certain coupled CTRW limits. In the coupled case, the CTRW has scaling limit and the so-called oracle CTRW has scaling limit , see [16, 18]. If are independent, they have a.s. no simultaneous jumps, and the two limit processes are the same. The proof of Theorem 2.3 extends immediately to the process in this case, with the same dimension results. This is because the graphs of and have the same Hausdorff and packing dimension, as they differ by at most a countable number of discrete points. In the following, we discuss examples for , with the understanding that the same dimension results hold for .

The simplest case is , in which case . This process is self-similar with index , see for example Becker-Kern et al. [3]. It follows from Theorems 2.1, 2.3 and the fact that for any constant ,

that

| (3.6) |

and

| (3.7) |

We should also mention that by applying the “uniform” Hausdorff and packing dimension results for the -stable subordinator (see Perkins and Taylor [33]), which states that almost surely

we obtain (3.6) directly by choosing .

Shlesinger et al. [39] consider a CTRW where the waiting times are iid with the -stable random variable and and, conditional on , the jump is normal with mean zero and variance . Then is symmetric stable with index . This model was applied to stock market prices by Meerschaert and Scalas [27]. Becker-Kern et al. [3] show that the CTRW limit is (), where is a real-valued stable Lévy process with index and is the inverse of a -stable subordinator. Then is self-similar with index , the same as Brownian motion. However, the Hausdorff dimensions of the range and graph of are completely different than those for Brownian motion.

3.3. CTRW with iid jumps: Triangular array limits

Proposition 3.1 and (3.10) rely on the Hausdorff and packing dimension results for sample functions of stable or, more generally, operator stable Lévy processes. The Hausdorff dimensions and potential theoretic properties of general Lévy processes have been studied by several authors ([34, 21, 23]) and the packing dimension results have been proved by Khoshnevisan and Xiao [22] and Khoshnevisan, Schilling and Xiao [20]. These results are useful for studying fractal properties of the CTRW limits under more general settings such as triangular array schemes.

In particular, for any Lévy process with values in and characteristic exponent (i.e., ), Corollary 1.8 in [23] shows that for any ,

| (3.11) |

where is the Euclidean norm on . On the other hand, Theorem 1.1 in Khoshnevisan and Xiao [22] shows that for any ,

| (3.12) |

where, for all , is defined by

(More precisely, Theorem 1.1 in [22] is proved for , but its proof works for arbitrary . Another way to get (3.12) from Thorem 1.1 in [22] is to use the stationarity of increments of .)

By combining (3.11) and (3.12) with Theorems 2.1 and 2.3 we extend the results in the previous sections to more general time-changed processes.

Proposition 3.2.

Let , where is a Lévy process with values in and characteristic exponent and let be the inverse of a subordinator with characteristic exponent . If is a Lévy process in and its characteristic exponent satisfies

| (3.13) |

for all with large, where is a constant. Then almost surely,

and almost surely, where

The packing dimensions of and are given as follows, which may be different from the Hausdorff dimensions given in Proposition 3.2.

Proposition 3.3.

Next we consider a generalized CTRW limit, as in [31], obtained by using a triangular array scheme. This limit can be applied as a stochastic model for ultraslow diffusion (cf. [30, 11]).

At each scale we are given iid waiting times and iid jumps . Assume the waiting times and jumps form triangular arrays whose row sums converge in distribution. More specifically, let and , we require that and as , where the limits and are independent Lévy processes. Letting , the CTRW scaling limit [31, Theorem 2.1].

A power law mixture model for waiting times was proposed in [30]: Take an iid sequence of random variables with and assume for , so that the waiting times are power laws conditional on the mixing variables. The waiting time process , which is a subordinator with Laplace transform , where (2.24) holds. The Lévy measure of is given by

| (3.14) |

where is the distribution of the mixing variable [30, Theorem 3.4 and Remark 5.1]. A computation [30, Eq. (3.18)] using shows that

| (3.15) |

Then the inverse subordinator [30, Theorem 3.10].

Now we take , where are constants and is the unit mass at . In this case, the subordinator is , which is a mixture of independent -stable subordinators (). See Chechkin et al. [11] for some applications of such CTRW and its scaling limit .

In order to apply Propositions 3.2 and 3.3 to establish Hausdorff and packing dimension results for the above time-changed process , we will make use of the following technical result.

Lemma 3.4.

Let , where are constants and are independent stable subordinators of index and . Let be a strictly stable Lévy motion of index with values in . We assume and are independent and let be the characteristic exponent of the Lévy process . Then for all that satisfies

| (3.16) |

where is a constant which may depend on , for .

Proof.

For simplicity, we assume that the characteristic exponent of is . Then the Lévy process has characteristic exponent

| (3.17) |

Since , we have for all . Moreover, for some constant . Hence

From here it is elementary to verify (3.16). ∎

By using Lemma 3.4, Propositions 3.2 and 3.3 we derive the following proposition. Since the proof is similar to that of Proposition 4.1 in [32] (see also Proposition 7.7 in [21]), we omit the details.

Proposition 3.5.

Let , where is a strictly stable Lévy motion of index with values in and is the inverse of a subordinator , where and are independent stable subordinators of index and . Suppose also that is independent of . Then

| (3.18) |

and

| (3.19) |

3.4. CTRW with correlated jumps

Now consider an uncoupled CTRW whose jumps form a correlated sequence of random variables, and whose waiting times are iid and belong to the domain of attraction of a positive -stable random variable .

We further assume that and are independent. In this case, Meerschaert, et al. [26] show that, under certain conditions on the correlation structure of , the CTRW scaling limit is the -self-similar process , where is a fractional Brownian motion with index , and is the inverse of a -stable subordinator which is independent of .

The following proposition determines the Hausdorff and packing dimension of the sample path of .

Proposition 3.6.

Let , where is a fractional Brownian motion with values in of index and is the the inverse of a -stable subordinator which is independent of . Then

| (3.20) |

and

| (3.21) |

Proof.

Eq. (3.20) follows from Theorem 2.1 and the well known result on Hausdorff and packing dimension of the range of fractional Brownian motion (see, e.g., Chapter 18 of [19]). In order to prove (3.21), by Theorem 2.3 it is sufficient to prove that for the -valued process defined by and for any constant , we have

| (3.22) |

Thanks to (2.5), we can divide the proof of (3.22) into proving the upper bound for and the lower bound for separately. These are given as Lemmas 3.7 and 3.9 below. ∎

Lemma 3.7.

Let the assumptions of Proposition 3.6 hold and let be a constant. Then

| (3.23) |

In order to prove Lemma 3.7, we will make use of the fact that for every the function () satisfies the uniform Hölder condition of order and the following Lemma 3.8, which is an immediate consequence of Lemma 3.2 in Liu and Xiao [24]. It can also be derived from Lemma 6.1 in Pruitt and Taylor [35].

Let be a fixed constant. A collection of intervals of length in is called -nested if no interval of length in can intersect more than intervals of . Note that for each integer , the collection of dyadic intervals is -nested with .

Lemma 3.8.

Let be a -stable subordinator and let be a -nested family. Denote by the number of intervals in which intersect . Then there exists a positive constant such that for all and all ,

| (3.24) |

If one takes , then we have

| (3.25) |

Now we are ready to prove Lemma 3.7.

Proof of Lemma 3.7. The proof is based on a moment argument. We divide the interval into dyadic intervals of length .

First we construct a covering of the range by using balls in of radius as follows. Define so that for each , the image is contained in a ball in of radius and can be covered by at most

| (3.26) |

balls of radius . By the self-similarity and stationarity of increments of , we have

| (3.27) |

where the last inequality follows from the well known tail probability for the supremum of Gaussian processes (e.g., Fernique’s inequality).

In order to get a covering for , let be the collection of dyadic intervals of order in . Let be the number of dyadic intervals in which intersect . Applying (3.25) in Lemma 3.8 with , we obtain that

| (3.28) |

Since , we see that can be covered by at most balls in of radius . Denote by the smallest number of balls in of radius that cover , then

It follows from (3.27), (3.28) and the independence of and that

Hence, for any ,

It follows from the Borel-Cantelli lemma that almost surely

for all large enough. This and (2.3) imply that a.s. Since is arbitrary, we obtain from the above and (2.5) that almost surely.

Next we construct a covering for the range by using balls in of radius . Let be the collection of intervals in of the form , where is an integer. Then the class is -nested. Let be the number of intervals in that intersect . By Lemma 3.8 with and , we derive . Thus can almost surely be covered by intervals of length from .

On the other hand, the image can be covered by at most

balls of radius , where , and then similar to (3.27) we derive

| (3.29) |

Denote by the smallest number of balls in of radius that cover , then

By (3.29) and the independence of and we have

Hence, for any , the Borel-Cantelli Lemma implies that a.s.

for all large enough. This and (2.3) imply that almost surely which, in turn, implies a.s.

Lemma 3.9.

Under the assumptions of Proposition 3.6, we have

| (3.30) |

Proof.

Since the projection of into is and a.s. when . This implies the first inequality in (3.30).

To prove the inequality in (3.30) for the case , by Frostman’s theorem (cf. [19, p.133]) along with the inequality

it is sufficient to prove that for every constant , we have

| (3.31) |

Since , we have . We only need to verify (3.31) for every .

For this purpose, we will make use of the following easily verifiable fact (see, e.g., Kahane [19, p.279]): If is a standard normal vector in , then there is a finite constant such at for any constants and ,

Fix such that . We use to denote the conditional expectation given the subordinator , apply the above fact with and use the self-similarity of to derive

| (3.32) |

where the last equality follows from the -self-similarity of and the constant . Recall from Hawkes [15, Lemma 1] that, as ,

where . We verify easily

Remark 3.10.

Other iterated processes can arise as scaling limits of CTRW with dependent and/or heavy-tailed jumps or waiting times. For example, the process can be taken as a linear fractional stable motion, see [26]. Our main theorems in Section 2 are applicable to these self-similar processes too. However, the problems for determining the Hausdorff dimensions of the range and graph sets of the processes and have not been satisfactorily solved, see [38, 45] for partial solutions.

References

- [1] B. Baeumer and M. M. Meerschaert, Stochastic solutions for fractional Cauchy problems. Fractional Calculus Appl. Anal. 4 (2001), 481–500.

- [2] B. Baeumer, M. M. Meerschaert and E. Nane, Brownian subordinators and fractional Cauchy problems. Trans. Amer. Math. Soc. 361 no. 7, (2009), 3915–3930.

- [3] P. Becker-Kern, M. M. Meerschaert and H. P. Scheffler, Limit theorems for coupled continuous time random walks. Ann. Probab. 32 (2004), 730–756.

- [4] P. Becker-Kern, M. M. Meerschaert and H. P. Scheffler, Limit theorems for continuous-time random walks with two scales. J. Appl. Probab. 41 (2004), 455–466.

- [5] J. Bertoin, Lévy Processes. Cambridge University Press, 1996.

- [6] R. M. Blumenthal and R. Getoor, Some theorems on stable processes. Trans. Amer. Math. Soc. 95 (1960), 263–273.

- [7] R. M. Blumenthal and R. Getoor, A dimension theorem for sample functions of stable processes. Illinois J. Math. 4 (1960), 370–375.

- [8] R. M. Blumenthal and R. Getoor, The dimension of the set of zeros and the graph of a symmetric stable process. Illinois J. Math. 6 (1962), 308–316.

- [9] K. Burdzy, Some path properties of iterated Brownian motion. In: Seminar on Stochastic Processes (E. Çinlar, K.L. Chung and M.J. Sharpe, eds.), pp. 67–87, Birkhäuser, Boston, 1993.

- [10] K. Burdzy, Variation of iterated Brownian motion. In: Workshops and Conference on Measure-valued Processes, Stochastic Partial Differential Equations and Interacting Particle Systems (D.A. Dawson, ed.), pp. 35–53, Amer. Math. Soc. Providence, RI, 1994.

- [11] A. V. Chechkin, R. Gorenflo and I. M. Sokolov, Retarding subdiffusion and accelerating superdiffusion governed by distributed-order fractional diffusion equations. Physical Review E 66 (2002), 6129–6136.

- [12] A. V. Chechkin, M. Hofmann and I. M. Sokolov, Continuous-time random walks with correlated waiting times. Phys. Rev. E 80 (2009), 031112.

- [13] K. J. Falconer, Fractal Geometry – Mathematical Foundations and Applications. New York: Wiley, 1990.

- [14] K. J. Falconer, The horizon problem for random surfaces. Math. Proc. Cambridge Philos. Soc. 109 (1991), 211–219.

- [15] J. Hawkes, A lower Lipschitz condition for stable subordinator. Z. Wahrsch. Verw. Gebiete 17 (1971), 23–32.

- [16] B.I. Henry and P. Straka (2011) Lagging and leading coupled continuous time random walks, renewal times and their joint limits. Stochastic Processes and their Applications 121(2), 324–336.

- [17] N. C. Jain and W. E. Pruitt, The correct measure function for the graph of a transient stable process. Z. Wahrsch. Verw. Gebiete 9 (1968), 131–138.

- [18] A. Jurlewicz, P. Kern, M. M. Meerschaert, and H.-P. Scheffler, Oracle continuous time random walks, preprint available at www.stt.msu.edu/users/mcubed/OCTRW.pdf

- [19] J.-P. Kahane, Some Random Series of Functions. 2nd edition, Cambridge University Press, Cambridge, 1985.

- [20] D. Khoshnevisan, R. Schilling and Y. Xiao, Packing dimension profiles and Lévy processes, (2010), Sumbitted.

- [21] D. Khoshnevisan and Y. Xiao, Lévy processes: Capacity and Hausdorff dimension. Ann. Probab. 33 (2005), 841–878.

- [22] D. Khoshnevisan and Y. Xiao, Packing dimension of the range of a Lévy process. Proc. Amer. Math. Soc. 136 (2008), 2597–2607.

- [23] D. Khoshnevisan, Y. Xiao and Y. Zhong, Measuring the range of an additive Lévy processes. Ann. Probab. 31 (2003), 1097–1141.

- [24] L. Liu and Y. Xiao, Hausdorff dimension theorems for self-similar Markov processes. Probab. Math. Statist. 18 (1998), 369–383.

- [25] M. M. Meerschaert, D. A. Benson, H. P. Scheffler and B. Baeumer, Stochastic solution of space-time fractional diffusion equations. Phys. Rev. E 65 (2002), 1103–1106.

- [26] M. M. Meerschaert, E. Nane and Y. Xiao, Correlated continuous time random walks. Statist. Probab. Lett. 79 (2009), 1194–1202.

- [27] M. M. Meerschaert and E. Scalas, Coupled continuous time random walks in finance. Physica A 370 (2006), 114–118.

- [28] M. M. Meerschaert and H. P. Scheffler, Limit Distributions for Sums of Independent Random Vectors: Heavy Tails in Theory and Practice. Wiley Interscience, New York, 2001.

- [29] M. M. Meerschaert and H. P. Scheffler, Limit theorems for continuous time random walks with infinite mean waiting times. J. Appl. Probab. 41 (2004), 623–638.

- [30] M. M. Meerschaert and H. P. Scheffler, Stochastic model for ultraslow diffusion. Stoch. Process. Appl. 116 (2006), 1215–1235.

- [31] M. M. Meerschaert and H. P. Scheffler, Triangular array limits for continuous time random walks. Stochastic Processes Appl. 118 (2008), 1606–1633.

- [32] M. M. Meerschaert and Y. Xiao, Dimension results for the sample paths of operator stable processes. Stoch. Process. Appl. 115 (2005), 55–75.

- [33] E. A. Perkins and S. J. Taylor, Uniform measure results for the image of subsets under Brownian motion. Probab. Th. Rel. Fields 76 (1987), 257–289.

- [34] W. E. Pruitt, The Hausdorff dimension of the range of a process with stationary independent increments. J. Math. Mech. 19 (1969/1970), 371–378.

- [35] W. E. Pruitt and S. J. Taylor, Sample path properties of processes with stable components. Z. Wahrsch. Verw. Gebiete 12 (1969), 267–289.

- [36] W. E. Pruitt and S. J. Taylor, Packing and covering indices for a general Lévy process. Ann. Probab. 24 (1996), 971–986.

- [37] F. Rezakhanlou and S. J. Taylor, The packing measure of the graph of a stable process. Astérisque No. 157–158 (1988), 341–362.

- [38] N.-R. Shieh and Y. Xiao, Hausdorff and packing dimensions of the images of random fields. Bernoulli 16 (2010), 926–952.

- [39] M. Shlesinger, J. Klafter and Y.M. Wong, Random walks with infinite spatial and temporal moments. J. Statist. Phys. 27 (1982), 499–512.

- [40] S. J. Taylor, The measure theory of random fractals. Math. Proc. Cambridge Philos. Soc. 100 (1986), 383–406.

- [41] V. Tejedor and R. Metzler, Anomalous diffusion in correlated continuous time random walks. J. Phys. A: Math. Theor. 43 (2010), 082002.

- [42] C. Tricot, Two definitions of fractional dimension. Math. Proc. Cambridge Philo. Soc. 91 (1982), 57–74.

- [43] Y. Xiao, Random fractals and Markov processes. In: Fractal Geometry and Applications: A Jubilee of Benoit Mandelbrot, (Michel L. Lapidus and Machiel van Frankenhuijsen, editors), pp. 261–338, American Mathematical Society, 2004.

- [44] Y. Xiao, Sample path properties of anisotropic Gaussian random fields. In: A Minicourse on Stochastic Partial Differential Equations, (D. Khoshnevisan and F. Rassoul-Agha, editors), Lecture Notes in Math. 1962, pp. 145–212. Springer, New York, 2009.

- [45] Y. Xiao and H. Lin, Dimension properties of the sample paths of self-similar processes. Acta Math. Sinica N. S. 10 (1994), 289–300.