YL-2010-004

Inventory Allocation for Online Graphical Display Advertising

Abstract

We discuss a multi-objective/goal programming model for the allocation of inventory of graphical advertisements. The model considers two types of campaigns: guaranteed delivery (GD), which are sold months in advance, and non-guaranteed delivery (NGD), which are sold using real-time auctions. We investigate various advertiser and publisher objectives such as (a) revenue from the sale of impressions, clicks and conversions, (b) future revenue from the sale of NGD inventory, and (c) “fairness” of allocation. While the first two objectives are monetary, the third is not. This combination of demand types and objectives leads to potentially many variations of our model, which we delineate and evaluate. Our experimental results, which are based on optimization runs using real data sets, demonstrate the effectiveness and flexibility of the proposed model.

keywords:

Advertising, Guaranteed Delivery, Linear Programming, Multi-objective, Fairness1 Introduction

Online graphical display advertising is a form of online advertising where advertisers can explicitly or implicitly target users visiting Web pages, and show graphical (e.g., image, video) ads to those users. For instance, a brokerage firm may wish to target Males from California who visit a Finance web site in the month of November 2010, and show an ad promoting its special offers to those users. Similarly, a different advertiser may wish to automatically target users who visit a Finance web site, specifically those who are likely to click on their ad highlighting a lower mortgage rate. Online graphical display advertising is a multi-billion dollar industry that is related to, but distinct from, sponsored search advertising [2], where advertisers bid for keywords entered by users on a search page, and from content match advertising [8], where advertisers bid for clicks and text-matching techniques (as opposed to user targeting) are used to show contextually relevant text advertisements on Web pages.

As with most forms of online advertising [7], one of the central questions that arises in the context of online graphical display advertising is that of inventory allocation, i.e., determining how to allocate supply/inventory (user visits) to demand (advertiser campaigns) so as to optimize for various publisher and advertiser objectives. However, even formulating the inventory allocation problem for online graphical display advertising is quite challenging, for two reasons.

First, the same inventory can be sold in two different forms: guaranteed delivery and non-guaranteed delivery. In guaranteed delivery, an advertiser can purchase a certain number of targeted user visits from a publisher several months in advance, and the publisher guarantees these visits and incurs penalties if the guarantees are not met. For instance, an advertiser may wish to purchase 100 million user visits by Males in California on a Sports web site during Superbowl 2011, and the Sports web site publisher will guarantee these user visits even though the serving date is months away from the booking date. On the other hand, in non-guaranteed delivery, advertisers can bid in real-time in a spot market for user visits, and the highest bidder obtains the right to show an ad to the user. For instance, if a user visits a Finance web page, then there may be multiple advertisers bidding for the ad slot on the page, and the highest bidder can show an ad to the user. An interesting aspect is that the same user visits are eligible for both guaranteed delivery and non-guaranteed delivery. A typical use case is that some inventory not fully allocated to guaranteed campaigns can be sold to non-guaranteed campaigns. However, not all visits from this inventory will fetch the same price in the spot-market. This leads to the first question addressed by this work: How does a publisher allocate inventory to both guaranteed and non-guaranteed advertising campaigns, while still ensuring that the guaranteed advertiser objectives are met, and publisher revenue is maximized?

Second, unlike sponsored search and content match advertising, where the goals of advertisers are to obtain clicks/ conversions on ads, the goals of advertisers in online graphical display can be quite varied. At one end of the spectrum are brand advertisers (e.g., major department stores), whose primary goal is to reach a large and diverse audience and promote their brand, rather than immediate clicks or purchases. At the other end of the spectrum are performance advertisers (e.g., credit card companies), whose primary goal is to obtain immediate online clicks and conversions. In the middle, there are performance-brand advertisers (e.g., car companies), whose goal is both to promote the brand, as well as to obtain immediate leads of users who are in the market to buy a car. The varied goals of advertisers also lead to multiple currencies by which graphical display advertisements are bought: brand advertisers typically buy impressions (expressed in CPM, or Cost Per Mille (1000 impressions)), while performance advertisers typically pay per click (CPC or Cost Per Click) or conversion (CPA, or Cost Per Action), while brand-performance advertisers may use a combination of CPM and CPC/CPA. Thus, the second question we address is: How does a publisher allocate inventory across diverse advertisers and payment types so that advertiser and publisher objectives are met?

1.1 Contributions

Given the aforementioned unique requirements for online graphical display advertising, one of the main technical contributions of this paper is an inventory allocation optimization model that can capture these requirements. At a high-level, the proposed allocation model represents forecasts of future inventory (user visits) and guaranteed advertiser campaigns as nodes in a bipartite graph. Each edge of the bipartite graph connects a user visit to an eligible guaranteed advertiser campaign. In addition, each user visit is annotated with a forecast of the highest bid fetched on the non-guaranteed marketplace and a forecast of the expected pay-out. Similarly, each edge of the graph is annotated with a forecast of the click or conversion probability for the advertiser campaign and the specific user visit.

Given the previous model, the objectives for online graphical display advertising are captured as follows. There are two parts to the objective function: one that captures guaranteed campaigns, and the other that captures non-guaranteed campaigns. The objective for the latter is simply to maximize the revenue for the publisher, since advertisers only bid for what the user visit is worth to them. The objective for the guaranteed campaigns, on the other hand, is more complex because advertisers could be interested in brand awareness, or performance, or both. Furthermore, the publisher faces penalties for under-delivering – that is displaying an advertisement to fewer users than agreed on.

In our model, delivery guarantees are treated as feasibility constraints. (If the instance is infeasible, we trim the demand to find the feasible solution with the minimum under-delivery penalties.) The objective for guaranteed contracts has two parts. The brand awareness objective is captured in terms of “representativeness” (see [15]), which tries to maximize the reach of the guaranteed campaign by uniformly distributing the contracts among the user visits to the extent possible 111Reach can also be specified in terms of users as opposed to user visits (as above) by using user cookie information, but we do not elaborate on this extension here. The performance objectives for guaranteed campaigns are captured as the expected pay-out, i.e., the probability of clicks and conversions, times the value of each click and conversion.

Consequently, the final allocation objective has three parts: non-guaranteed revenue, guaranteed representativeness, and guaranteed clicks/conversions. While multi-objective programming has been a standard technique for some time, previous optimization models for online advertising (see e.g. [17, 18]) have used a single objective function. One of our major contributions is to use the multi-objective optimization framework [24] to model the sometimes conflicting objectives in a rigorous way.

While the multi-objective optimization model described above captures the various objectives, it also introduces a new set of challenges both in terms of operability and in terms of computational feasibility. Specifically, with regard to operability, the question that arises is: how do we trade-off between the various objectives (such as representativeness and non-guaranteed revenue), which do not even have the same units? With regard to computational feasibility, the question that arises is: how do we solve a multi-objective formulation efficiently over large volumes of data (tens of billions of user visits per day and hundreds of thousands of advertiser campaigns per year)? Another key technical contribution of this paper is a method that enables operators of the system to trade-off between multiple objectives based on the monetary unit of a single objective. For instance, an operator can trade-off representativeness in terms of the impact it has on non-guaranteed revenue, which is expressed in monetary units. A significant advantage of this method is that it also allows for an efficient solution, which can be solved on a small sample of the original bipartite graph, without significantly compromising accuracy.

We note that there are two other closely related topics that impact inventory allocation: pricing and ad serving. While the details of these methods are beyond the scope of this paper, the proposed allocation method works with quite general pricing and ad serving techniques. Specifically, in terms of pricing, we assume that guaranteed campaigns are priced using some external method (which may itself use forecasts of non-guaranteed bids to ensure appropriate prices), and the inventory allocation model can work with the booked prices without regards to how exactly the prices were computed. Similarly, we assume that we have some forecast of non-guaranteed bids, but do not make any assumptions on how the bids by themselves are generated by individual campaigns. In terms of ad serving, the allocation model produces both a primal and dual solution, the latter of which can be stored compactly and interpreted by the ad server to serve ads to user visits in an online, real-time manner (e.g., see [10, 26]).

We have implemented the proposed inventory allocation model and the solution techniques, motivated by the context of an operational online graphical display advertising system. Our results using real user visits, guaranteed campaigns, non-guaranteed bids, and click/conversion data, indicate that the proposed approach is both versatile in capturing and trading off between various advertiser and publisher objectives, as well as efficient to solve with high accuracy.

In summary, the main contributions of this paper are:

-

•

A formalization of the inventory allocation model and objectives for online graphical display advertising (Section 2).

-

•

A multi-objective optimization formulation and various solution techniques for optimizing the multiple objectives (Section 3).

-

•

An experimental evaluation of the proposed techniques using real data sets (Section 4).

2 Model and Objectives

We begin by first defining some notation, and then motivating and formalizing the various objectives in online graphical display advertising.

2.1 Supply and Demand Model

As mentioned earlier, the main goal of inventory allocation is to match supply (user visits) and demand (advertising campaigns). We thus begin by modeling user visits, advertising campaigns, and their interaction.

User visits can be represented as attributes-value pairs, where the attributes represent the properties of a user, the properties of the page they visit, as well as the time stamp of the visit. An example user visit could be represented as: Gender = Male, AgeGroup = 30-40, Interests = {Sports, Finance}, Location = California, …, PageCategory = {Sports}, …, Day = 15 Jan 2011, Time = 12:35pm GMT.

A display advertising campaign targets a subset of user visits by specifying a targeting predicate. For instance, an advertising campaign that targets Males in California visiting Sports pages in the month of Jan 2011 can be represented as: Gender {Male} Location {California} PageCategory {Sports} Duration [1 Jan 2011 - 31 Jan 2011]. A user visit is said to be eligible for an advertising campaign if the attribute-value pairs of the user visit satisfy the targeting predicate of the advertising campaign. In the rest of this paper, we will focus on just the eligibility relationship between user visits and advertising campaigns, and not on the specific attribute-value pairs or the targeting predicates.

Advertising campaigns can be of two types: guaranteed campaigns, whereby the publisher guarantees a fixed number of user visits to an advertiser in advance, and non-guaranteed campaigns, where advertisers bid in real-time for user visits. Both guaranteed and non-guaranteed campaigns can have one or more advertiser goals: to obtain user visits (this is the only goal that is guaranteed in a guaranteed campaign), to obtain clicks, and/or to obtain conversions. In non-guaranteed campaigns, however, these objectives are converted into a bid by a bidding agent and thus, for the purpose of modeling, they can be represented as a bid for each user visit. Guaranteed campaigns, on the other hand, need to be modeled in more detail. Specifically, a guaranteed campaign has a user visit goal (the guarantee), a penalty function that specifies the penalty to be paid by the publisher if the guarantee is not met, and a value for each click and/or conversion. A key aspect that enables yield optimization for clicks and/or conversions is the probability of a click and/or conversion given a user visit.

Finally, for reasons of scale, it is usually not practical to work with all future user visits for a duration of many months (many large publishers have billions of impressions per day). Consequently, the inventory allocation problem often has to be solved on a sample of user visits, and thus each sampled user visit is annotated with a sample weight.

The following notation summarizes the above discussion:

-

•

: Set of user visits

-

•

: Sample weight of user visit

-

•

: The payout for user visit by non-guaranteed campaigns

-

•

: Set of guaranteed campaigns

-

•

: User visit goal for guaranteed campaign

-

•

: Penalty function for guaranteed campaign , which maps under-delivery (how much a guarantee is missed) to a penalty.

-

•

: The value of a click for a guaranteed campaign

-

•

: The value of a conversion (action) for a guaranteed campaign

-

•

: The probability that a user corresponding to user visit clicks on an ad corresponding to guaranteed campaign

-

•

: The probability that a user corresponding to user visit converts on an ad corresponding to guaranteed campaign

-

•

: Set of user visits that are eligible for guaranteed campaign .

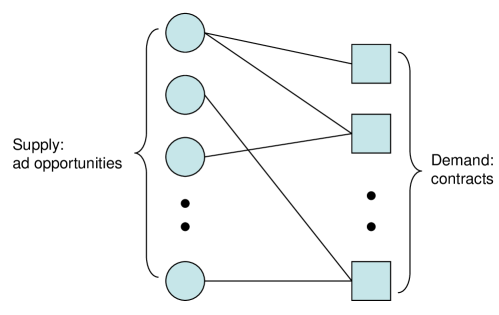

It is often convenient to view the user visits and guaranteed campaigns in a bipartite graph, with user visits on one side, guaranteed campaigns, on the other, and an edge between a user visit and a guaranteed campaign if , that is if satisfies the targeting predicates of . An example of such graph is shown in Figure 1.

It should be noted that the construction of this graph, which may involve tens of thousands of nodes and millions of edges, is in itself a major computational task.

2.2 Objectives

In this section, we motivate and formalize the various objectives that are relevant to the inventory allocation problem. In the next section, we introduce a mathematical model to trade-off and optimize across these different objectives.

An overriding objective of publishers is to minimize the penalties incurred in case guarantees are not met. Minimizing penalties is important because the publisher not only incurs an immediate monetary loss, but also because the publisher could suffer longer-term losses due to advertiser attrition. Define as the weight of user that is allocated to guaranteed campaign . Then the amount of user visits delivered to a guaranteed campaign is , and the objective of minimizing penalties can be formalized as:

| (1) |

However, in this paper we avoid this issue by ensuring feasibility of the constraints (see section 3.1).

At a high-level, there are two parts to the inventory allocation problem, corresponding to non-guaranteed and guaranteed campaigns. The objective for non-guaranteed campaigns is simple: to maximize the revenue for the publisher, since advertisers only bid what each user visit is worth to them. Modeling the objectives for guaranteed campaigns, on the other hand, is more complex because advertisers could be interested in brand awareness/reach or performance (clicks, conversions) or both. We thus have three objectives: non-guaranteed revenue, brand awareness/reach, and performance.

Before formalizing the above objectives, we introduce some notation:

-

•

: The weight of user visit that is allocated to non-guaranteed campaigns

-

•

: The total amount of user visits eligible for guaranteed campaign

-

•

: The ideal fully representative target allocation fraction of user visit to guaranteed campaign (motivated further below)

2.2.1 Non-Guaranteed Revenue

The prices paid by non-guaranteed advertisers depend heavily on the particular user. Therefore, a natural goal of an allocation is to maximize the publisher’s revenue by allocating the highest valued user visits to the non-guaranteed contracts. Since the amount of revenue that a publisher obtains from a user visit is , this objective is written as:

| (2) |

2.2.2 Brand Awareness/Reach

There are two primary reasons why it is important to have a brand awareness/reach objective. The first reason is that brand advertisers typically want to reach a large swath of their target audience. For instance, a brand advertiser who targets user visits from the US will likely be quite unhappy if all of their delivered user visits are from fourteen year old males in Wyoming, and none from the rest of the population (even though all the delivered user visits technically satisfy the targeting predicate of the advertiser). In other words, brand advertisers often want a representative subset of their target audience222Advertisers could potentially control their target allocation (other than uniformly at random) more closely if they desire, at the cost of targeting more defined, and therefore likely more expensive, inventory.

The second reason for having a brand awareness and reach objective is more subtle, and it relates to the interaction with non-guaranteed campaigns. Specifically, if the primary goal of the publisher was to maximize short-term revenue, then he could allocate all of the high-value impressions to the highest bidding non-guaranteed campaigns, and allocate only the remaining impressions to the guaranteed campaigns. However, this is clearly detrimental to the advertiser, and is also a dangerous road to take for the publisher: by selectively allocating the most expensive user visits to the non-guaranteed contracts, the publisher risks alienating in the long term the guaranteed advertisers, many of whom pay a large premium for guarantees. In fact as Ghosh et al. [15] recently argued, in these situations price serves as a signal of value, thus the user visits with the highest may also be the ones most desired by the guaranteed contracts.

Therefore, it is in the long-term interests of publishers to allocate each guaranteed campaign a representative sub-set of targeted user visits. Ideally, every eligible user visit should be equally likely to see an ad from . A similar argument holds on a temporal scale. A week long contract should have the same probability of being displayed on all days of the week. That is, it should be allocated uniformly during the course of the week—after all, if an advertiser wanted the contract to be shown only on Tuesday, she would have added that to the targeting constraints.

To model these representativeness constraints, let be the ideal target allocation. Note that directly encodes the fact that no user visit is preferred by over others. To maximize long term revenue, the publisher should strive to find an allocation close to . In this paper we use the -norm distance to measure closeness to the target allocation. We denote the importance of a representative allocation to advertiser and write the objective as:

| (3) |

For consistency with other objectives, we will use the maximization form:

| (4) |

Note that alternative forms such as an entropy function or K-L divergence can also be used, as they retain the essential features of separability (by advertiser) and convexity. Similarly, other target allocations besides the perfectly uniform target allocation can also be considered but these variants are beyond the scope of this paper.

2.2.3 Clicks/Conversions for Guaranteed Campaigns

An advertiser in a guaranteed campaign may have multiple objectives, such as clicks and conversions, besides obtaining the guaranteed user visits. The publisher’s objective is to maximize the yield from such goals, while also directing such clicks and conversions to the advertisers who value them the most. This can be modeled as trying to maximize the expected value of clicks and conversions across all user visits:

For compactness we define:

| (5) |

Then we can rewrite the performance objective as:

| (6) |

Note that when we refer to “clicks” below, it is to be understood to include the subsequent conversions.

3 The mathematical models

In the previous section we described the competing objectives faced by a publisher in allocating user visits to guaranteed contracts. In this section we formally state the mathematical problem that incorporates these objectives subject to the feasibility constraints.

There are three types of constraints that the allocation must satisfy to be feasible. First, the desired number of user visits must be allocated for each guaranteed contract:

| (Demand Constraints) |

Next, each user visit can be allocated to exactly one guaranteed or non-guaranteed contract.

| (Supply Constraints) |

Finally, we must ensure that the allocation is always non-negative.

| (Non-Negativity Constraints) | ||||

Putting together the objectives from the previous section with the set of constraints, we may state our generic multi-objective optimization:

| (7) |

| (8) | |||||

| (9) | |||||

| (10) | |||||

| (11) |

Note that the non-negative variables transform what would be inequality supply constraints into equalities. Since is actually the leftover supply inventory that will be sold to the non-guaranteed delivery spot market, the term can be viewed as the total non-guaranteed revenue that can be obtained for an allocation , with remnant inventory . The second objective is the revenue obtained from clicks on the displayed advertisements.

3.1 Ensuring feasibility

In this model formulation, guarantees are treated as constraints (Demand Constraints). Consequently, before we optimize for the other objectives, we need to ensure that the model is feasible, i.e., there is sufficient supply for guaranteed campaigns. Note that even if a publisher is careful to accept only guaranteed campaigns that are feasible at the time of booking, the model could become infeasible at a later point because forecasts of user visits could change due to unforeseen events.

In order to make the model feasible, we add dummy user visits that have unlimited supply but a very high cost of being used, and connect them to all the guaranteed campaigns. The cost associated with using each dummy user visit for a guaranteed campaign corresponds to the penalty incurred by that guaranteed campaign in case of under-delivery (note that if has multiple penalty values for under-delivery, then these can be represented as multiple dummy user visits, each with a different cost of being used). The cost associated with using real user visits is 0.

Given the above set up, the goal is to find the minimum cost allocation to guaranteed campaigns. Since this problem is a pure network with a linear objective function, it can be solved very efficiently [4]. If the cost of the optimal allocation is 0, then it implies that all the guaranteed campaigns can be satisfied, and hence that the original model is feasible. If the cost of the optimal allocation is greater than 0, then it implies that some guaranteed campaigns will under-deliver. Furthermore, the optimal allocation to the dummy user visits will indicate how much each guaranteed campaign needs to under-deliver so that overall penalty cost is minimized. In this case, the user visit goal for each guaranteed campaign is reduced by the amount of allocation to the dummy user visits in order to make the model feasible. We then follow one of the procedures described in the remainder of this section.

3.2 Multi-objective programming

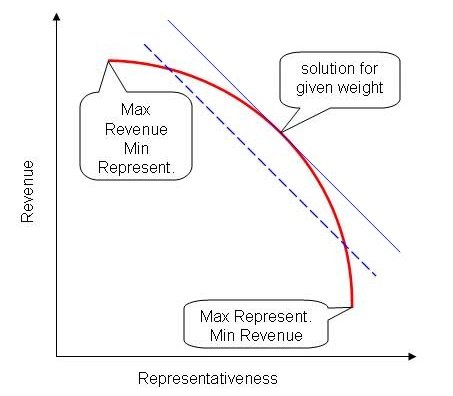

We may approach a multi-objective function model in a number of ways (see [24]). One general approach is to obtain an “efficient frontier” of solutions where at each point on the curve the value of one objective can only be improved at the expense of degrading another (see the generic example in Figure 2, where we notionally trade off total revenue and “representativeness”). The user may then choose any point on this curve as the “solution”.

More algebraic approaches include using a weighted sum of the multiple objectives and/or using “goal programming”, whereby the objectives are handled sequentially, with the additional constraint(s) that previous objectives retain a certain fraction of their optimal value. Since we have three objectives here there are clearly several variations, which we explore below.

In what follows, it will be convenient to define the 3 objective components as follows:

| (12) | |||||

| (13) | |||||

| (14) |

Depending on the data available, we may formulate solution strategies which employ:

-

1.

A single parametrized objective function.

-

2.

A two-objective function model in various flavors

-

3.

A three-objective function model, also in several flavors.

3.3 Single objective

The parameter is the weight for the “representativeness” component. The parameter , in conjunction with the reflects the means by which we attribute value to clicks. We observe that a feature of this model is that the shadow value of the supply constraint is always no less than the reserve price, i.e. .

Here, we assume that a value of is available, from either historical data or business considerations. We consider explicitly two cases for the value of :

-

•

The values of the are computed via (5) with . Then is the value of a click relative to a unit of revenue from the objective .

-

•

The are actual expected monetary value of allocating an impression of type to contract , in which case .

In both cases, the model involves the addition of a linear term in to the strictly convex distance function . The objective thus remains strictly convex quadratic in and linear in . Optimization of this model is straightforward in principle, using a commercial solver such as XpressMP [27]. If a sufficiently powerful large-scale nonlinear network code were available, this could also be used since our constraints are of the pure network type.

3.4 Two objectives

If all of the above data are not available to us, we must resort to multi-objective or goal programming. Let us first assume that is not known, but the click-related data ( are available. In this case, we may initially solve:

| (16) |

subject to (8)-(11). Note that this is a linear pure network minimum cost flow problem which can be solved very rapidly by special purpose software (e.g., see Bertsekas [4]). Let the optimal value of this linear program (LP) be .

We may now append a constraint specifying that at least a certain fraction of this monetary value be preserved and solve the model:

| (17) |

| (18) |

It may be shown (see Appendix) that the unknown parameter is equal to the inverse of the dual value for the constraint (18).

Suppose now that a value for is available but is not. We may initially solve

| (19) |

subject to (8)-(11). Let the optimal value of this linear program (LP) be . We may now append a constraint specifying that at least a certain fraction of this “click value” (however it is quantified) be preserved, and solve the model:

| (20) |

| (21) |

The third variant combines the two objectives and in the second stage model, after solving a first stage model:

| (22) |

subject to (8)-(11). Since this is also a linear pure network minimum cost flow problem is can be solved very rapidly by special purpose software. Let the optimal value of this linear program be

In this approach, the second model is of the form:

| (23) |

where is the fraction of NGD revenue we wish to preserve.

3.5 Three objectives

From an operability point of view, it is unlikely that both the parameters and would be known, or even understood very well. In that case, we cannot avoid turning to goal programming and the use of more intuitive “knobs” for the business to use in the decision making process. Our goal program reduces to a sequence of three models. In principle, these models could be solved in any order, but we take the point of view that the nonlinear objective should be optimized last, in order to avoid imposing a nonlinear constraint. Such a non-linear constraint would be computationally crippling at the scale we are contemplating. The last model therefore must optimize representativeness subject to constraints on non-guaranteed revenue and click value.

We again emphasize that, given appropriate , these last two quantities can reasonably be thought of in monetary terms, whereas may not.

Since non-guaranteed revenue is undeniably monetary, the most intuitive procedure might be to first solve for , i.e. solve the problem (22) and then solve for maximum click value:

| (24) |

| (25) |

where are as defined in constraint (23). Let the optimum objective function value be .

Clearly we could reverse the first two steps. This would likely produce different results, but both would be feasible.

There is however a severe computational disadvantage to this 3 step process. While step 1 is a pure network optimization model, the second step involves a side constraint (23) or (21) which destroys the orders of magnitude speed advantage of pure network optimizers over general LP solvers. In an effort to avoid this, we might omit the side constraint from the second model, leaving it a pure network model. However there is now no guarantee that the third model, incorporating (26), will be feasible. We might then relax the side constraints until feasibility is obtained, but rigor is lost.

4 Experiments

We now present some experimental results using a snapshot of real online graphical display advertising data sets. The main goal is to quantify the benefits of the multi-objective optimization approach proposed in this paper as compared to the more traditional single-objective optimization approaches. We note that our specific focus is on quantifying the relative benefits of the various optimization approaches for a given data/forecast snapshot, and not on online ad serving mechanisms (e.g., [10, 26]) that account for forecast errors, and could use periodic re-optimization.

4.1 Experimental setup

The data snapshot consists of guaranteed campaigns, forecasts of user visits, non-guaranteed bids and clicks, all based on a subset of historical data from an operational display advertising system. The generated optimizer graph has 32,390 supply nodes, 2,696 demand nodes and 1,407,753 edges. The supply weight () ranges from to . The user visit goal () ranges from to . The non-guaranteed price () ranges from 0.046 to 4.350. The click probability () ranges from to 0.947 (the experiments only evaluate clicks, not conversions).

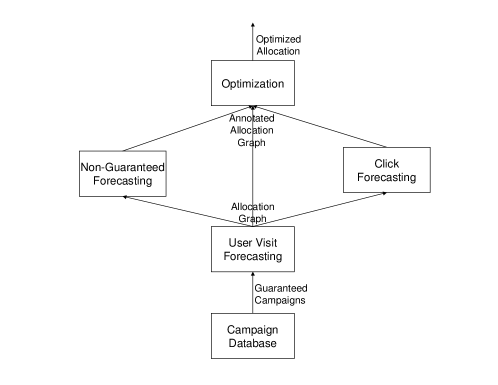

Figure 3 shows the experimental flow based on the data snapshot. The first step is to invoke the User Visit Forecasting module to generate a forecast of user visits that correspond to the guaranteed campaigns, and construct the allocation graph. The next two (parallel) steps are to invoke the Non-Guaranteed Forecasting and Click Forecasting modules to annotate the allocation graph with the non-guaranteed revenue information () and the click probabilities (, respectively. The final step is to run the Optimizer to solve the various optimization methods proposed in the paper.

The metrics that we measure for the various optimization runs are the non-guaranteed revenue, the total value of clicks, and the representativeness of guaranteed campaigns. The experiments are run for various values of the model parameter settings. For the experiments, all the allocation priorities are set to 1 and all the click values are set to 10.

The experiments were run on a 64bit/64GB/2GHz Linux box using the optimization package Xpressmp333Recently acquired by Fair Isaac (FICO) [27].

4.2 Forecast models

Although the forecast models used here are not the focus of this paper, we include a brief description of each for completeness.

4.2.1 Supply Forecasting

User visit forecasting uses time-series trend predictions to predict the trend/growth in user visits for various pockets of supply such as Sports or Finance. Our specific implementation uses SARIMA [23] for time-series predictions.

In addition, to generate the allocation graph, we need to produce a sample of user visits. For this, we follow the sampling procedure outlined in Vee et al [26], which produces a unbiased sample for the class of optimization models that we consider in this paper. Specifically, for each guaranteed campaign, the supply forecast selects eligible user visits uniformly at random. Once all of the user visits for all campaigns are chosen, the weights given to each user visit is normalized so that the total weight of any subset of user visits is — in expectation — equal to the predicted available supply. The allocation graph is then created by adding edges from the campaigns to their eligible user visits.

4.2.2 Non-Guaranteed Forecasting

The goal of the Non-Guaranteed Forecasting module is to predict the expected revenue obtained by selling a particular user visit in the non-guaranteed marketplace. We observed that the prices paid for ad opportunities by the non-guaranteed contracts followed a log normal distribution, with prices ranging from under $0.10 CPM to above $10 CPM. To predict the price of an individual user visit, we trained a generalized least squares regression model on the logarithm of the prices. Each user visit was annotated with a set of user features, for example, age, gender, etc, and a set of page features, for example Sports, Finance, etc. We used the value predicted by the model as the non-guaranteed price .

4.2.3 Click forecasting

Click forecasting estimates the probability that a displayed ad will be clicked in a particular user visit context. Estimation of click-through rates (CTR) is extensively applied in pay-for-performance systems that attempt to maximize expected revenue [20, 22]. The estimates can be based on historical click-through performance statistics of features that are selected as significant predictors of CTR. In this work, we use a logistic regression model with the following functional form:

| (28) |

where are predicates of features of the user visit and the ad such as user age and gender, page content category, ad position in page, etc. Using historical data from web traffic that consist of page visits with corresponding user visit and click statistics, we learned the logistic regression parameters.

Finally, each edge in the allocation graph, which represents a contract and a corresponding eligible ad opportunity, is annotated with features . The click model is used to produce an estimate of the probability of click for each graph edge.

4.3 Experimental results

We now present our experimental results for various models and parameter settings. Each optimization for a particular parameter combination takes about 5 to 10 minutes, which is quite acceptable as an offline optimization step that can inform online serving algorithms (e.g., [10, 26]).

4.3.1 Baseline and Single-Objective Solutions

As a baseline, we compute the optimization solution that only ensures feasibility by minimizing the total under-delivery penalty, but does not explicitly optimize for the other objectives. The result for this baseline solution is shown in the first row of Table 1) and is used as the basis for normalization. We then optimize for each single objective separately and report the normalized solutions in the same table — here NGD refers to non-guaranteed revenue, and GD refers to guaranteed representativeness. It can be seen that while optimizing a single objective may significantly improve that objective, it has a potentially significant impact on the other objectives.

| Objective | NGD | Click | NGD+Click | GD |

|---|---|---|---|---|

| Baseline | 1 | 1 | 1 | -1 |

| NGD | 1.0165 | 1.0905 | 1.0229 | -0.9836 |

| Click | 1.0062 | 2.9136 | 1.1722 | -2.2214 |

| NGD+Click | 1.0131 | 2.9013 | 1.1774 | -1.7440 |

| GD | 0.9968 | 0.9226 | 0.9903 | -0.0027 |

4.3.2 Two-Objective Formulation

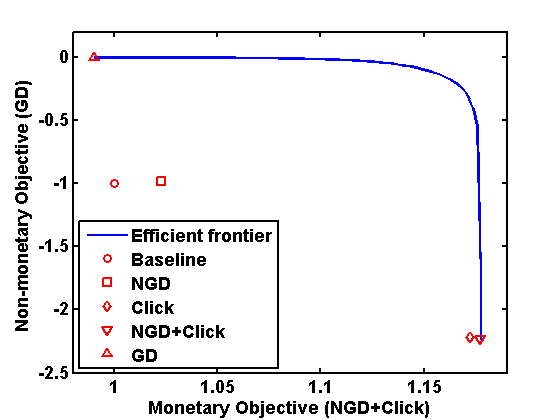

We run the 2-step programming algorithm (Section 3.4) with 100 different values of the parameter. Table 2 shows the objectives in normalized scale for a subset of the generated efficient solutions. The whole efficient frontier by using all the 100 points is depicted in Figure 4, which shows the trade-off between the monetary objective (non-guaranteed revenue plus click value) and the non-monetary objective (representativeness).

| NGD | Click | NGD+Click | GD | |

|---|---|---|---|---|

| 0.8411 | 0.9968 | 0.9226 | 0.9903 | -0.0027 |

| 0.8570 | 0.9978 | 1.1269 | 1.0090 | -0.0028 |

| 0.8729 | 0.9993 | 1.3260 | 1.0277 | -0.0034 |

| 0.8888 | 1.0016 | 1.5171 | 1.0464 | -0.0046 |

| 0.9047 | 1.0047 | 1.6990 | 1.0651 | -0.0069 |

| 0.9205 | 1.0079 | 1.8810 | 1.0838 | -0.0109 |

| 0.9364 | 1.0094 | 2.0801 | 1.1026 | -0.0181 |

| 0.9523 | 1.0110 | 2.2782 | 1.1213 | -0.0328 |

| 0.9682 | 1.0127 | 2.4763 | 1.1340 | -0.0660 |

| 0.9841 | 1.0131 | 2.6861 | 1.1587 | -0.1474 |

| 0.9999 | 1.0131 | 2.9013 | 1.1774 | -1.7440 |

Figure 4 also shows the baseline and single-objective solutions as different symbols. The baseline solution and most of the single-objective solutions are located in the interior of the feasible solution region and dominated by efficient solutions on the frontier. Further, the efficient frontier shows that a very small loss in one objective can lead to a significant gain in the other objective, thereby enabling a better combined trade-off as compared to single-objective solutions.

The above results clearly demonstrate that explicitly capturing and solving for multiple objectives dominates ignoring the objectives, or just optimizing for a single objective.

4.3.3 Three-Objective Formulation

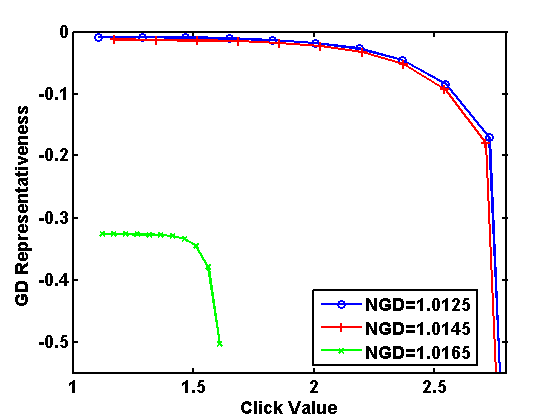

We run the 3-step programming algorithm (Section 3.5) with 100 different combinations of the and parameters. Table 3 shows the objectives in normalized scale for a subset of the generated efficient solutions. Note that the efficient frontier for the tri-objective optimization problem is a surface in a 3D space. One way to visualize the efficient frontier is to project it to a 2D space by fixing the level in the third dimension. Figure 5 shows three such contours in the space of click value and GD representativeness for evenly-spaced NGD revenues. The trade-off among the three objectives can be observed by comparing points on the same contour and between different contours.

| NGD | Click | NGD+Click | GD | ||

|---|---|---|---|---|---|

| 0.9961 | 0.3812 | 1.0125 | 1.1075 | 1.0208 | -0.0084 |

| 0.9961 | 0.6906 | 1.0125 | 2.0067 | 1.0990 | -0.0180 |

| 0.9961 | 1.0000 | 1.0125 | 2.9058 | 1.1772 | -1.7272 |

| 0.9981 | 0.4073 | 1.0145 | 1.1740 | 1.0284 | -0.0129 |

| 0.9981 | 0.7037 | 1.0145 | 2.0281 | 1.1027 | -0.0232 |

| 0.9981 | 1.0000 | 1.0145 | 2.8823 | 1.1770 | -1.7225 |

| 0.9999 | 0.6967 | 1.0165 | 1.1209 | 1.0255 | -0.3264 |

| 0.9999 | 0.8483 | 1.0165 | 1.3649 | 1.0468 | -0.3280 |

| 0.9999 | 0.9999 | 1.0165 | 1.6090 | 1.0680 | -0.5039 |

4.4 Discussion

The results above and especially the efficient frontier give us a global picture of the trade-off among different objectives. It reveals what percentage of one objective can be gained at the cost of one percent of another objective and how the trade-off rate changes with the location of the solution, thereby providing valuable insight in setting the right parameters in a real production system to truly reflect the business priority. Perhaps more importantly, it demonstrates the significant benefit of a combined optimization model for multiple objectives, as opposed to optimizing for just a single objective.

5 Further extensions

We have referred throughout to revenue gained through clicks. We might also include other non-monetary terms, using or some other parameter as a conversion factor. One candidate for this treatment is relevance, when would encode the probability of relevance of ad to user and the payoff to advertiser for such relevance.

Another candidate for future work is the exploration of ways to to incorporte uncertainty into the strictly deterministic model we have described here. Preliminary stochastic programming experiments [5] indicate that uncertainty in the inventory supply can have a significant impact. Other sources of uncertainty arise in sampling error and click and conversion rate estimation.

6 Related work

Operations Research techniques, and optimization in particular, have been used for decades in planning advertising campaigns in other media, such as print, radio and television (see [6] for example). The potential of the WWW for more targeted advertising was realized in the 1990’s and became a subject of research. Langheinrich et al [17] reported on a study where they attempted to target display ads to users in order to optimize expected revenue, without using intrusive data gathering techniques. While “unintrusiveness” seems to have become less of a concern to advertisers and publishers, their optimization approach was influential. Tomlin [25], noting a similarity between this problem and the traffic distribution model (see [28]), suggested adding an entropy term to the linear cost function proposed in [17] to essentially smooth the allocations and prevent “bang-bang” solutions; characteristic of LP models. Chickering and Heckerman [9] employed an alternate smoothing technnique, involving binning, and gave computational experience. A good survey of these and later developments is given in [18].

Since that time, the development of Computational Advertising as a discipline has led to the consideration of many variants of the graphical advertising allocation problem. A crucial development in this process was the promulgation of the concept of “fairness” in allocation to offset extreme LP solutions. While we have used the approach of [15], an alternate approach is taken by [13]. Some of our early work was presented in [1] and [29]. Feldman et al [14] have considered the online ad allocation problem in the more general setting of the matching problem, while Roels and Fridgeirsdottir [21] have considered a dynamic version assuming the inventory follows a Markov process. Easterly [11] and Han [16] discuss online advertising from a Revenue Management point of view.

Two other modules in the online advertising supply chain make use of the results of an allocation model such as we have described. These are Ad Serving and Admission Control. The Ad Server interprets the output of the allocation model as a set of frequencies with which specific ads should be shown to users in the supply pools when they visit a web page. Considerable practical advantages ensue when the solution can be stored in compact form and rapidly reconstructed on the fly by the ad server when a page requests ads. This process has been studied by Devanur and Hayes [10] and Vee et al [26], using the dual values associated with the demand constraints and, implicitly, the graph structure to determine the contracts for which a new arriving impression is eligible. The optimization models we have studied provide the necessary dual values, but online ad serving is not considered in this paper.

Admission Control is the process of determining whether a proposed new guaranteed campaign should be accepted, that is whether the existing obligations can still be satisfied in a modified solution if the new contract is accepted. Versions of this problem have been studied by Feige et al [12] and Aleai et al [3] and considered as an (NP-hard) combinatorial optimization problem. Radovanovic and Zeevi [19] have proposed a relaxed, more tractable, variant of the Admission Control process.

7 Conclusion

In this paper we have shown that multi-objective optimization provides an efficient and flexible framework for the allocation of user visits to guaranteed and non-guaranteed campaigns. The proposed models also incorporate a very flexible means of taking into account revenue derived from clicks, as well as non-monetary objectives — in particular “representativeness” or “fairness” — in the allocation of eligible user visits to campaigns. We are able to do this using off-the-shelf software, such as a commercial scale optimization system (we used XpressMP) for large scale quadratic programming, or specialized network optimization codes for some steps.

We believe that the proposed models can be extended to other objectives of interest such as ad relevance. As part of future research, we are exploring extensions to the model to include stochastic elements, such as uncertainty in supply and demand, and nonlinear pricing.

8 acknowledgments

We gratefully acknowledge the assistance of Sumanth Jagannath and Wenjing Ma in processing the data for our experiments, and Jianchang Mao for managing much of the click model development.

References

- [1] D. Agarwal, J. Tomlin, and J. Yang. A log-linear model for allocating overlapping inventory to on-line advertisers. Presented at INFORMS, October 2008.

- [2] G. Aggarwal, A. Goel, and R. Motwani. Truthful auctions for pricing search keywords. In Proc. of the 7th ACM Conf. on Electronic Commerce, pages 1–7, 2006.

- [3] S. Aleai, E. Arcaute, S. Khuller, W. Ma, A. Malekian, and J. Tomlin. Online allocation of display advertisements subject to advanced sales contracts. In Proc. of the 3rd Int. Workshop on Data Mining and Audience Intelligence for Advertising (ADKDD), pages 69–77, 2009.

- [4] D. Bertsekas. Network Optimization: Continuous and Discrete Models. Athena Scientific Press, 1998.

- [5] V. Bharadwaj, M. Saunders, and J. Tomlin. Sensitivity of an inventory allocation model for online advertising with stochastic supply. Presented at EURO XXIV, July 2010.

- [6] S. Bollapragada, H. Chen, M. Phillips, M. Garbiras, M. Scholes, T. Gibbs, and M. Humphreville. NBC’s optimization systems increase revenues and productivity. Interfaces, 32(1):47 – 60, 2002.

- [7] A. Z. Broder. Computational advertising and recommender systems. In RecSys ’08, pages 1–2, Lausanne, Switzerland, 2008.

- [8] A. Z. Broder, M. Fontoura, V. Josifovski, and L. Riedel. A semantic approach to contextual advertising. In Proc. ACM SIGIR, 2007.

- [9] D. M. Chickering and D. Heckerman. Targeted advertising with inventory management. In EC ’00: Proceedings of the 2nd ACM conference on Electronic commerce, pages 145–149, New York, NY, USA, 2000. ACM.

- [10] N. Devanur and T. Hayes. The adwords problem: Online keyword matching with budgeted bidders under random permutations. Presented at EC, 2009.

- [11] A. Easterly. Revenue management in online advertising: Challenges and opportunities. Presented at INFORMS, October 2009.

- [12] U. Feige, N. Immorlica, V. Mirrokni, and H. Nazerzadeh. A combinatorial allocation mechanism with penalties for banner advertising. Presented at INFORMS, October 2008.

- [13] J. Feldman, M. Henzinger, N. Korula, V. S. Mirrokni, and C. Stein. Online stochastic packing applied to display ad allocation. CoRR, abs/1001.5076, 2010.

- [14] J. Feldman, A. Mehta, V. Mirrokni, and S. Muthukrishnan. Online stochastic matching: Beating 1-1/e. Presented at FOCS, October 2009.

- [15] A. Ghosh, R. McAfee, K. Papineni, and S. Vassilvitskii. Randomized bidding for maximally representative allocation. In Proc. WINE, December 2009.

- [16] P. Han. Yield optimization in display ad networks. Presented at INFORMS, October 2009.

- [17] M. Langheinrich, A. Nakamura, N. Abe, T. Kamba, and Y. Koseki. Unintrusive optimization techniques for web advertising. In Proc. of World Wide Web Conf. (WWW1999), 1999.

- [18] A. Nakamura and N. Abe. Improvements to the linear programming based scheduling of web advertisements. J. Electronic Commerce Research, 5:75–98, 2005.

- [19] A. Radovanovic and A. Zeevi. Revenue maximization in reservation-based online advertising. Presented at INFORMS, October 2009.

- [20] M. Richardson, E. Dominowska, and R. Ragno. Predicting clicks: Estimating the click-through rate for new ads. In Proc. of World Wide Web Conf. (WWW2007), 2007.

- [21] G. Roels and K. Fridgeirsdottir. Dynamic revenue mangement for online display advertising. http://escholarship.org/uc/item/7kq702dz, 2008.

- [22] B. Shaparenko, O. Çetin, and R. Iyer. Data-driven text features for sponsored search click prediction. In Proc. of the 3rd Int. Workshop on Data Mining and Audience Intelligence for Advertising (ADKDD), pages 46–54, 2009.

- [23] R. Shumway and D. Stoffer. Time Series Analysis and Its Applications. Springer, 2007.

- [24] R. Steuer. Multiple criteria optimization: theory, computation, and application. Wiley, New York, 1986.

- [25] J. Tomlin. An entropy approach to unintrusive targeted advertising on the web. In Proc. of World Wide Web Conf. (WWW2000), 2000.

- [26] E. Vee, S. Vassilvitskii, and J. Shanmugasundarum. Optimal online assignment with forecasts. Proc. of the ACM Conf. on Electronic Commerce, 2010.

-

[27]

Dash Optimization. XpressMP—Optimizer Reference Manual, 2008. - [28] A. Wilson. Entropy in Urban and Regional Modelling. Pion Press, London, 1970.

- [29] J. Yang and J. Tomlin. Advertising inventory allocation based on multi-objective optimization. Presented at INFORMS, 2008.

Appendix

The goal programming model (17), (8)-(11), (18) in section 3.4 is equivalent to finding a value of which preserves a specified fraction of revenue, given a value of . To see this, let us write the Lagrangian of the problem (15), (8)-(11) as:

where the and are the appropriate Lagrange multipliers on the equality and inequality constraints.

The KKT optimality conditions for this problem are:

Now consider the Lagrangian of the problem (17), (8)-(11), (18), introducing Lagrange multiplier :

The KKT optimality conditions are:

Comparing terms in the Lagrangians and the two sets of KKT conditions we see that . In particular, we see that . Thus we may obtain the parameter as from the solution to the goal programming problem.