Phasetype distributions, autoregressive processes and overshoot

Sören Christensen

Christian-Albrechts-Universität, Mathematisches Seminar, Kiel, Germany

Abstract: Autoregressive processes are intensively studied in statistics and other fields of applied stochastics. For many applications the overshoot and the threshold-time are of special interest. When the upward innovations are in the class of phasetype distributions we determine the joint distribution of this two quantities and apply this result to problems of optimal stopping. Using a principle of continuous fit this leads to explicit solutions.

Keywords: Autoregressive; Threshold times; Phasetype innovations; Optimal stopping

Subject Classifications: 60G40; 62L15; 60G99

1 Introduction

Autoregressive processes play an important role in many areas of applied probability and statistics. They can be seen as one of the building blocks for many models in time-series analysis and estimation and testing techniques are well developed. In this article we study the following setting:

Let , be a sequence of independent and identically distributed random variables on a probability space and let be the filtration generated by . Define the autoregressive process of order 1 (AR(1)-process) by

i.e.

The random variables are called the innovations of . Using the difference notation the identity can be written as

where , and .

This shows that AR(1)-processes are the discrete-time analogon to (L vy-driven) Ornstein-Uhlenbeck processes. We just want to mention that many arguments in the following can be carried over to Ornstein-Uhlenbeck processes as well.

Autoregressive processes were studied in detail in the last decades. The joint distribution of the threshold-time

and the overshoot

was of special interest. If the process is a random walk and many results about this distributions are well known. Most of them are based on techniques using the Wiener Hopf-factorization – see [4, Chapter VII] for an overview. Unfortunately no analogon to the Wiener-Hopf factorization is known for AR(1)-processes, so that other ideas are necessary. To get rid of well-studied cases we assume that in the following.

This first passage problem for AR(1)-processes was considered in different applications, such as signal detection and surveillance analysis, cf. [6]. In applications the distribution of this quantities are approximated using Monte-Carlo simulations or Markov chain approximations, cf. e.g. [16]. But e.g. for questions of optimization analytic solutions are necessary.

Using martingale techniques exponential bounds for the expectation of can be found. Most of these results are based on martingales defined by using integrals of the form

| (1) |

where is the logarithm of the Laplace transform of the stationary distribution discussed in Section 3. For the integral to be well defined it is necessary that for all – cf. [11] and the references therein.

On the other hand if one wants to obtain explicit results about the joint distribution of and the overshoot it is useful to assume to be exponentially distributed. In this case explicit results are given in [3, Section 3] by setting up and solving differential equations. Unfortunately in this case not all exponential moments of exist and the integral described above cannot be used.

The contribution of this article is twofold:

-

1.

We find the joint distribution of and the overshoot for a wide class of innovations: We assume that , where and are independent, has a phasetype distribution and is arbitrary. This generalizes the assumption of exponentially distributed innovations to a much wider class. In Section 2 we establish that and the overshoot are – conditioned on certain events – independent and we find the distribution of the overshoot. In Section 3 we use a series inspired by the integral (1) to construct martingales with the objective of finding the distribution of .

This leads to explicit expressions for expectations of the form for general functions and . -

2.

As an application we consider the (Markovian) problem of optimal stopping for with discounted non-negative continuous gain function , i.e. we study the optimization problem

where denotes the set of stopping times with respect to ; to simplify notation here and in the following we set the payoff equal to on . Just very few results are known for this problem. In [10] and [3] the innovations are assumed to be exponentially distributed and in [5] asymptotic results were given for .

Following the approach described in [3] the problem can be reduced to determining an optimal threshold. This is summarized in Section 4. In a second step we use the joint distribution of and the overshoot to find the optimal threshold. To this end we use the principle of continuous fit, that is established in Section 6. An example is given in Section 7.

2 Innovations of phasetype

In this section we recall some basic properties of phasetype distributions and identify the connection to AR(1)-processes. In the first subsection we establish the terminology and state some well-known results, that are of interest for our purpose. All results can be found in [1] discussed from the perspective of queueing theory.

In the second subsection we concentrate on the threshold-time distribution for autoregressive processes when the positive part of the innovations is of phasetype. The key result for the next sections is that – conditioned to certain events – the threshold-time is independent of the overshoot and the overshoot is phasetype distributed as well.

2.1 Definition and some properties

Let , , and .

In this subsection we consider a Markov chain in continuous time with state space . The states are assumed to be transient and is absorbing. Denote the generator of by , i.e.

If we write for all , then is a semigroup and the general theory yields that

Since is assumed to be absorbing has the form

for an -matrix , where denotes the column-vector with entries 1.

We consider the survival time of , i.e. the random variable

Let be an initial distribution of . Here and in the following is assumed to be a row-vector.

Definition 2.1.

is called a distribution of phasetype with parameters and we write for short.

Let and for a parameter . In this case it is well-known that is exponentially distributed with parameter . This special case will be the key example we often think of. Furthermore let us mention that the class of phasetype distributions is stable under convolutions and mixtures. This shows that the important classes of Erlang- and hyperexponential distributions are of phasetype.

Exponential distributions have a very special structure, but phasetype distributions are flexible:

Proposition 2.1.

The distributions of phasetype are dense in the space of all probability measures on with respect to convergence in distribution.

Proof.

See [1, III, Theorem 4.2]. ∎

The definition of phasetype distributions does not give rise to an obvious calculus with these distributions, but the theory of semigroups leads to simple formulas for the density and the Laplace-transform as the next lemma shows. All the formulas contain matrix exponentials. The explicit calculation of such exponentials can be complex in higher dimensions, but many algorithms are available for a numerical approximation.

Proposition 2.2.

-

(a)

The eigenvalues of have negative real part.

-

(b)

The distribution function of is given by

-

(c)

The density is given by

where .

-

(d)

For all with it holds that

where is the -identity matrix.

In particular is a rational function.

Proof.

See [1, II, Corollary 4.9 and III, Theorem 4.1]. ∎

An essential property for the applicability of the exponential distribution in modeling and examples is the memoryless property, which even characterizes the exponential distribution. The next lemma can be seen as a generalization of this property to distributions of phasetype.

Lemma 2.3.

Let and write

Then is a distribution function of a phasetype distribution with parameters , where for all .

Proof.

By Proposition 2.2 the random variable has a continuous distribution. Therefore using the Markov-property of we obtain

where is the -th unit vector. ∎

For the application to autoregressive processes we need the generalization of the previous lemma to the case that the random variable is not necessarily positive.

Lemma 2.4.

Let be stochastically independent random variables, where is -distributed. Furthermore let and . Then

where .

Proof.

2.2 Phasetype distributions and overshoot of AR(1)-processes

We again consider the situation of Section 1. In addition we assume the innovations to have the following structure:

where and are non-negative and independent and is -distributed. In this context we remark that each probability measure on with can be written as where and are probability measures with and denotes convolution (cf. [4, p.383]).

As a motivation we consider the case of exponentially distributed innovations. If is exponentially distributed then it holds that for all and measurable

| (2) |

where is a threshold-time, and is exponentially distributed with the same parameter as the innovations (cf. [3, Theorem 3.1]). This fact is well known for random walks, cf. [4, Chapter XII.]. The representation of the joint distribution of overshoot and reduces to finding a explicit expression of the Laplace-transform of . In this subsection we prove that a generalization of this phenomenon holds in our more general situation.

To this end we use an embedding of into a stochastic process in continuous time as follows:

For all denote the Markov chain which generates the phasetype-distribution of by and write

Hence the process is constructed by compounding the processes restricted to their lifetime. Obviously is a continuous time Markov chain with state space , as one immediately checks, cf. [1, III, Proposition 5.1]. Furthermore we define a process by

See Figure 1 for an illustration. It holds that

so that we can find in . Now let be the threshold-time of the process over the threshold , i.e.

By definition of it holds that

| (3) |

For the following result we need the event that the associated Markov chain is in state when crosses , i.e. the event

For the following considerations we fix the threshold .

In generalization of the result for exponential distributed innovations the following theorem states that – conditioned on – the threshold-time and the overshoot are independent and the overshoot is phasetype distributed as well.

Theorem 2.5.

Let , , and write

Then

This immediately implies a generalization of (2) to the case of general phasetype distributions:

Corollary 2.6.

It holds that

where is a -distributed random variable (under ).

3 Explicit representations of the joint distribution of threshold time and overshoot

Corollary 2.6 reduces the problem of finding expectations of the form to finding for and . The aim of this section is to construct martingales of the form as a tool for the explicit representation of . To this end some definitions are necessary:

We assume the setting of the previous section, i.e. we assume that the innovations can be written in the form

where and are non-negative and independent and is -distributed.

Let be the Laplace-transform of , i.e. for all with real part so small that the expectation exists. Since and Proposition 2.2 yields the existence of for all with smaller then the smallest eigenvalue of . is analytic on this stripe and – because of independence – it holds that

where denotes the Laplace-transform of and is the Laplace-transform of . is analytic on and can be analytically extended to by Proposition 2.2. Here denotes the spectrum, i.e. the set of all eigenvalues. Hence can be extended to as well and this extension is again denoted by . Note that this extension can not be interpreted from a probabilistic point of view because does not exist for with too large real part.

To guarantee the convergence of we assume a weak integrability condition – the well known Vervaat condition

| (4) |

see [8, Theorem 2.1] for a characterization of such conditions in the theory of perpetuities. We do not go into details here, but just want to use the fact that converges to a (finite) random variable in distribution, that fulfills the stochastic fixed point equation

where denotes convolution. Since the AR(1)-process has the representation

and convergence in distribution is equivalent to the pointwise convergence of the Laplace-transforms the Laplace-transform of fulfills

| (5) |

for all such that the Laplace-transform of exists.

The right hand side defines a holomorphic function on that is also denoted by , where we write . For the convergence of the series note that – as described above – it converges for all such that . For all other the series also converges since there exists such that for all .

Furthermore the identity

| (6) |

holds, whenever are in the domain of . To avoid problems concerning the applicability of (6) we assume that

| (7) |

We would like to mention, that the function was used and studied in [11] as well.

The next two lemmas are helpful in the construction of the martingales.

Lemma 3.1.

Let such that exists. Then for all it holds that

where .

Proof.

In the following calculation we use the fact that all matrices commutate and that all eigenvalues of have negative real part. It holds

We obtain

∎

We write for short. For all fulfilling

| (8) |

we define the function

This series converges because is bounded in . Note that the summand of this series is similar to the integrand in (1).

Lemma 3.2.

There exists such that for all and with it holds that

Proof.

For all with sufficiently small the expected value exists for all since has (finitely many) negative eigenvalues. This leads to

∎

The next step is to find a family of equations characterizing

using martingale techniques where , . To this end we consider

for all and fulfilling (8) where . For the special value we write and this function is well-defined by (7).

Putting together the results of Lemma 3.1 and Lemma 3.2 we obtain the equation

| (9) |

for all with sufficiently small modulus.

Before stating the equations we need one more technical result.

Lemma 3.3.

Let be a -distributed random variable and denote by the holomorphic extension of the logarithmized Laplace-transform of . Here denotes the -th unit vector. Let be so small that exists. Then it holds that

where

Proof.

Simple calculus similar to the previous ones yields the result. ∎

Theorem 3.4.

For all and it holds that

where is given in the previous Lemma.

Proof.

Write for with so small that .

The discrete version of It ’s formula yields

and is a martingale. The optional sampling theorem applied to yields

using equality (9). The dominated convergence theorem shows that

note that the dominated convergence theorem is applicable to both summands since has negative eigenvalues and so is bounded in for with being bounded above. Corollary 2.6 leads to

where is distributed and the previous Lemma implies

Since is bounded both sides of the equation

are holomorphic in and the identity theorem for holomorphic functions yields that these extensions agree on their domains. Keeping (7) in mind we especially obtain for

Furthermore both sides of the equations are again holomorphic functions in on. Another application of the identity theorem proves the assertion. ∎

The equation in the theorem above appears useful and flexible enough for the explicit solution as shown in the next subsections.

3.1 The case of exponential positive innovations

As described above the case of -distributed positive innovations is of special interest. In this case we obtain the solution directly from the results above. Hence let , , and . It is not relevant which we take; because the expressions simplify a bit we choose . Then we obtain

and

for . Theorem 3.4 yields

Theorem 3.5.

In [3] the special case of positive exponential distributed innovations was treated by finding and solving ordinary differential equations for . For this case – i.e. – we obtain

To get more explicit results we need a simple expression for . Using identity (5) we find such an expression as

where denotes the -Pochhammer-symbol and denotes the Euler function. This leads to

and the numerator is given by

Note that we used the -binomial-theorem in the third step (see [7, (1.3.15)] for a proof). An analogous calculation for the denominator yields

and we obtain

Theorem 3.6.

If is -distributed and it holds that

For the special case this formula was obtained by an approach via differential equations based on the generator in [10, Theorem 3].

Noting that

by direct calculation we find

This reproduces Theorem 3.3 in [3]. Note that in that article the stopping time was considered. But this leads to analogous results since

and

3.2 The general case

Theorem 3.4 gives a powerful tool for the explicit calculation of in many cases of interest as follows:

By Lemma 3.3 we see that is a rational function of with poles in for all . We assume for simplicity that all eigenvalues are pairwise different (for the general case see the remark at the end of the section). Then partial fraction decomposition yields the representation

and since is rational in with the same poles we may write

Theorem 3.4 reads

and the uniqueness of the partial fraction decomposition yields

i.e.

where , . This leads to

Theorem 3.7.

If is invertible, then is given by

Remark 3.8.

Note that the assumption of distinct eigenvalues was made for simplicity only. When it is not fulfilled we can use the general partial fraction decomposition formula and obtain the analogous result.

4 Applications to optimal stopping

To tackle the optimal stopping problem

it is useful to reduce the (infinite dimensional) set of stopping times to a finite dimensional subclass. A often used class for this kind of problems is the class of threshold-times. This reduction can be carried out in two different ways:

-

(a)

We use elementary arguments to reduce the set of potential optimal stopping times to the subclass of threshold-times, i.e. to stopping times of the form

for some . Then we find the optimal threshold. A summary of examples where is approach can be applied is given below.

-

(b)

We make the ansatz that the optimal stopping time is of threshold type, identify the optimal threshold and use a verification theorem to prove that this stopping time is indeed optimal.

On (a): In [3, Section 2] the idea of an elementary reduction of optimal stopping problems to threshold-problems was studied in detail. For arbitrary innovations this approach can be applied to power gain function, i.e. . This problem that is known as the Novikov-Shiryaev problem and was completely solved for random walks in [12] and [13]. Furthermore the approach applies to gain functions of call-type .

For the special case of nonnegative innovations a much wider class of gain functions can be handled such as exponential functions.

On (b): To use the second approach described above the following easy verification theorem is useful.

Lemma 4.1.

Let , write and assume that

-

(a)

for all .

-

(b)

for all .

Then and is optimal.

Proof.

By the independence of property implies that is a supermartingale under each measure . Since it is positive the optional sampling theorem leads to

where the second inequality holds by since for all . On the other hand , i.e. and is optimal. ∎

5 On the explicit solution of the optimal stopping problem

Now we are prepared to solve the optimal optimal stopping problem

Section 4 gives conditions for the optimality of threshold-times. In this cases we can simplify the problem to

Now take an arbitrary starting point . Then we have to maximize the real function

where is -distributed, . The results of the previous section give rise to an explicit calculation of and of .

Hence we are faced with the well-studied maximization problem for real functions, that can – e.g. – be solved using the standard tools from differential calculus.

If we have found a maximum point of and , then

is an optimal stopping time when is started in .

A more elegant approach for finding the optimal threshold is the principle of continuous fit:

6 The principle of continuous fit

The principles of smooth and continuous fit play an important role in the study of many optimal stopping problems. The principle of smooth fit was already introduced in [9] and has been applied in a variety of problems, ranging from sequential analysis to mathematical finance. The principle of continuous pasting is more recent and was introduced in [14] as a variational principle to solve sequential testing and disorder problems for the Poisson process. For a discussion in the case of L vy processes and further references we refer to [2]. Another overview is given in [15, Chapter IV.9] and one may summarize, see the above reference, p. 49:

“If enters the interior of the stopping region immediately after starting on , then the optimal stopping point is selected so that the value function is smooth in . If does not enter the interior of the stopping region immediately, then is selected so that is continuous in .”

Most applications of this principle involve processes in continuous time. In discrete time an immediate entrance is of course not possible, so that one can not expect the smooth-fit principle to hold. In this section we prove that the continuous-fit principle holds in our setting and illustrate how it can be used for an easy determination of the optimal threshold.

We keep the notations and assumptions of the previous sections and – as before – we assume that the optimal stopping set is an interval of the form and consider the optimal stopping time .

Furthermore we assume that

| (10) |

Note that this condition is obviously fulfilled in the cases discussed above. If is continuous under an appropriate integrability condition it furthermore holds that

| (11) |

Proof.

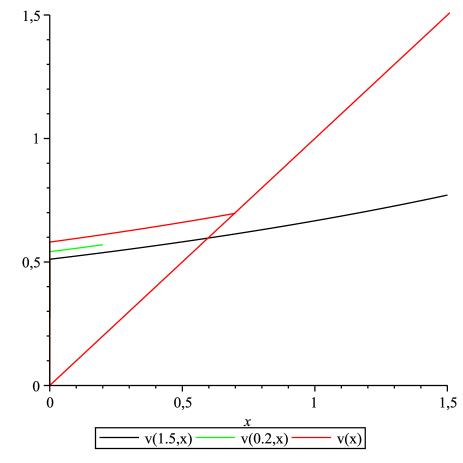

Figure 2 illustrates how the continuous fit principle can be used: We consider the candidate solutions

and solve the equation , where is defined as in the previous section. If the equation has a unique solution we can conclude that this solution must be the optimal threshold as illustrated in the following Section.

7 Example

We consider the gain function and -distributed innovations; in this setting we always assume to have values in . The discussion in Section 4 guarantees that the optimal stopping time is of threshold-type. The optimal threshold can be found by the continuous fit principle described in the previous section:

The problem is solved if we find a unique that solves the equation

where we used Theorem 3.6 in the last step. This equation is equivalent to

| i.e. | |||

| i.e. |

where

Note that and

Since we furthermore obtain for . Hence there exists a unique solution of the transcendental equation .

The optimal stopping time is

and the value function is given by

In Figure 2 is plotted for the parameters , .

References

- [1] Søren Asmussen. Applied probability and queues, volume 51 of Applications of Mathematics (New York). Springer-Verlag, New York, second edition, 2003. Stochastic Modelling and Applied Probability.

- [2] Sören Christensen and Albrecht Irle. A note on pasting conditions for the American perpetual optimal stopping problem. Statist. Probab. Lett., 79(3):349–353, 2009.

- [3] Sören Christensen, Albrecht Irle, and Alexander A. Novikov. An Elementary Approach to Optimal Stopping Problems for AR(1) Sequences. Submitted to Sequential analysis, 2010.

- [4] William Feller. An introduction to probability theory and its applications. Vol. II. John Wiley & Sons Inc., New York, 1966.

- [5] Mark Finster. Optimal stopping on autoregressive schemes. Ann. Probab., 10(3):745–753, 1982.

- [6] Marianne Fris n and Christian Sonesson. Optimal surveillance based on exponentially weighted moving averages. Sequential Analysis, 25(10):379–403, 2006.

- [7] George Gasper and Mizan Rahman. Basic hypergeometric series, volume 96 of Encyclopedia of Mathematics and its Applications. Cambridge University Press, Cambridge, second edition, 2004. With a foreword by Richard Askey.

- [8] Charles M. Goldie and Ross A. Maller. Stability of perpetuities. Ann. Probab., 28(3):1195–1218, 2000.

- [9] Valeria I. Mikhalevich. Bayesian choice between two hypotheses for the mean value of a normal process. Visnik Kiiv. Univ., 1:101–104, 1956.

- [10] Alexander A. Novikov. On Distributions of First Passage Times and Optimal Stopping of AR(1) Sequences. Theory of Probability and its Applications, 53(3):419–429, 2009.

- [11] Alexander A. Novikov and Nino Kordzakhia. Martingales and first passage times of sequences. Stochastics, 80(2-3):197–210, 2008.

- [12] Alexander A. Novikov and Albert N. Shiryaev. On an effective case of the solution of the optimal stopping problem for random walks. Teor. Veroyatn. Primen., 49(2):373–382, 2004.

- [13] Alexander A. Novikov and Albert N. Shiryaev. On solution of the optimal stopping problem for processes with independent increments. Stochastics, 79(3-4):393–406, 2007.

- [14] Goran Peškir and Albert N. Shiryaev. Sequential testing problems for Poisson processes. Ann. Statist., 28(3):837–859, 2000.

- [15] Goran Peškir and Albert N. Shiryaev. Optimal stopping and free-boundary problems. Lectures in Mathematics ETH Zürich. Birkhäuser Verlag, Basel, 2006.

- [16] George C. Runger and Sharad S. Prabhu. A Markov chain model for the multivariate exponentially weighted moving averages control chart. J. Amer. Statist. Assoc., 91(436):1701–1706, 1996.